It’s all eyes on federal banking regulators as investors sift through the aftermath of last week’s market-rattling collapse of Silicon Valley Bank.

The name of the game — and the key to a near-term market bounce — could be a deal that makes depositors at Silicon Valley Bank, or SVB, whole, analysts said. And efforts by regulators appeared to be focused on soothing worries over the ability of companies to access uninsured deposits — most such deposits exceed the FDIC’s $250,000 cap — in order to prevent runs similar to the event that capsized SVB from occurring elsewhere.

“If a deal gets struck tonight that doesn’t haircut depositors, the market is going to rally strongly,” said Barry Knapp, managing partner and director of research at Ironsides Macroeconomics, in a phone interview Sunday afternoon.

Investors will also be assessing the fallout to see if it complicates the Federal Reserve’s plans to hike interest rates further and potentially faster than previously expected in its bid to tamp down inflation.

SVB was closed by California regulators on Friday and taken over by the Federal Deposit Insurance Corp., which was conducting an auction of the bank Sunday afternoon, according to news reports.

See: U.S. and U.K. regulators consider ways to help SVB depositors, FDIC auctioning assets – reports

“We want to make sure that the troubles that exist at one bank don’t create contagion to others that are sound,” Treasury Secretary Janet Yellen said in a Sunday morning interview on “Face the Nation” on CBS, while ruling out a bailout that would rescue bondholders and shareholders of SVB parent SVB Financial Group SIVB.

“We are concerned about depositors and are focused on trying to meet their needs,” she said.

Continued uncertainty could leave a “sell first, ask questions later” dynamic in effect Monday.

“In what is an already jittery market, the emotional response to a failed bank reawakens our collective muscle memory of the GFC,” Art Hogan, chief market strategist at B. Riley Financial Wealth, told MarketWatch in an email, referring to the 2007-2009 financial crisis. “When the dust settles, we will likely find that SVB is not a ‘systematic’ issue.”

Weekend Snapshot: What’s next for stocks after Silicon Valley Bank collapse as investors await crucial inflation reading

Knapp warned that market turmoil with significant potential downside for stocks could ensue if depositors are forced to take a haircut, likely sparking runs at other institutions. A deal that leaves depositors whole would lift the overall market and allow bank stocks, which got hammered last week, to “rip” higher “because they are cheap” and the banking system “as a whole…is in really good shape.”

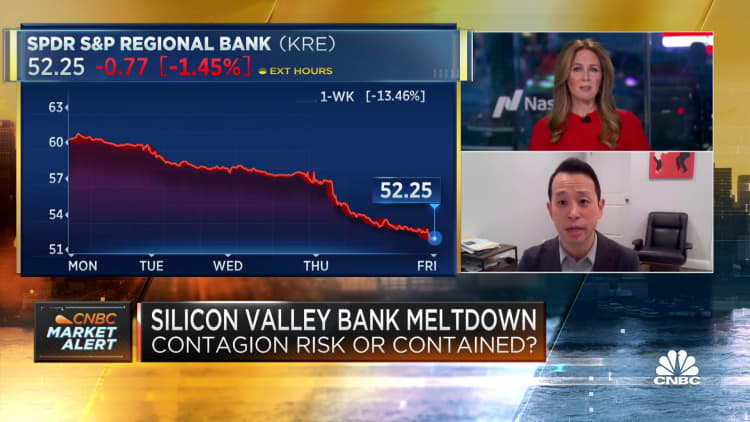

Muscle memory, meanwhile, was in effect at the end of last week. Banking stocks dropped sharply Thursday, led by shares of regional institutions, and extended their losses Friday. The selloff in bank stocks pulled down the broader market, leaving the S&P 500

SPX,

-1.45%

down 4.6%, nearly wiping out the large-cap benchmark’s early 2023 gains.

The Dow Jones Industrial Average

DJIA,

-1.07%

saw a 4.6% weekly fall, while the Nasdaq Composite

COMP,

-1.76%

declined 4.7%. Investors sold stocks but piled into safe-haven U.S. Treasurys, prompting a sharp retreat in yields, which move opposite to prices.

SVB’s failure is being blamed on a mismatch between assets and liabilities. The bank catered to tech startups and venture-capital firms. Deposits grew rapidly and were placed in long-dated bonds, particularly government-backed mortgage securities. As the Federal Reserve began aggressively raising interest rates roughly a year ago, funding sources for tech startups dried up, putting pressure on deposits. At the same time, Fed rate hikes triggered a historic bond-market selloff, putting a big dent in the value of SVB’s securities holdings.

See: Silicon Valley Bank is a reminder that ‘things tend to break’ when Fed hikes rates

SVB was forced to sell a large chunk of those holdings at a loss to meet withdrawals, leading it to plan a dilutive share offering that stoked a further run on deposits and ultimately led to its collapse.

Analysts and economists largely dismissed the notion that SVB’s woes marked a systemic problem in the banking system.

Also see: 20 banks that are sitting on huge potential securities losses—as was SVB

Instead, SVB appears to be a “a rather special case of poor balance-sheet management, holding massive amounts of long-duration bonds funded by short-term liabilities,” said Erik F. Nielsen, group chief economics adviser at UniCredit Bank, in a Sunday note.

“I’ll stick my neck out and suggest that markets are vastly overreacting,” he said.

Implications for the Fed’s monetary policy path also loom large. Fed-funds futures traders last week moved to price in a more-than-70% chance of an outsize 50-basis-point, or half a percentage point, rise in the benchmark interest rate at the Fed’s March meeting after Chair Jerome Powell told lawmakers that rates would need to move higher than previously anticipated.

Expectations swung back to a 25-basis-point, or quarter-point move, as the SVB collapse unfolded, with traders also scaling back expectations for when rates will likely peak.

Meanwhile, a flight to safety saw the yield on the 2-year Treasury note, which had earlier in the week topped 5% for the first time since 2007, end the week down 27.3 basis points at 4.586%.

The market reaction wasn’t unusual, said Michael Kramer of Mott Capital Management, in a Sunday note, and should reverse once the situation around SVB calms down.

Powell said incoming economic data would determine the size of the Fed’s next rate move. The market reaction to a stronger-than-expected rise in February nonfarm payrolls, which was tempered by a slowdown in wage growth and a rise in the unemployment rate, was clouded by the tumult around SVB.

“I think they will raise rates by at least 25 basis points and signal that more rate hikes are coming,” Kramer said. “If they were to pause rate hikes unexpectedly, it would send a warning message that they are seeing something of grave concern, causing a significant change in their policy path, and that would not be bullish for stocks.”