(Bloomberg) — Super Micro Computer Inc.’s 20% rout Friday was a much-needed win for short sellers facing billions of dollars in losses amid its blistering rally.

Most Read from Bloomberg

Traders who bet against the semiconductor company netted paper profits of $1.2 billion on the one-day dip, its biggest drop since August. Even with the gains, the contrarian group is still down roughly $4.8 billion in paper losses over the last year as the stock has surged more than 760%, according to data from S3 Partners LLC.

“If you’ve been short on the way up, you probably are feeling a lot of pain,” said Michael Sansoterra, chief investment officer at Silvant Capital Management.

Shares fell as much as 9.5% Tuesday morning, even after Rosenblatt Securities boosted its price target on the company to a Wall Street high of $1,300 from $700, citing continued momentum in artificial intelligence computing.

“We expect Supermicro to achieve significant market share gains, potentially reaching double digits in the next few years from its current mid-single digits, with a special emphasis on enterprise solutions,” analyst Hans Mosesmann wrote in a note. “A pivotal factor in Supermicro’s growth trajectory is the adoption of liquid cooling technology, a critical development for overcoming challenges in cloud computing at scale in AI.”

Still, short sellers are sticking to their bets that Super Micro’s climb will eventually end. In the last 30 days, the group has increased shares shorted by 12%, piling an additional $623 million into bets against the artificial intelligence darling, per S3.

On Friday, the cost of puts — which serve as downside protection — sank less than equivalent calls, which give exposure to added gains. That dynamic reversed trading patterns earlier in the week, when seemingly boundless euphoria for AI pumped interest in call options and propelled the one-month call skew to its highest level in more than a year.

Short sellers may be emboldened by the San Jose, California-based company’s sharp moves higher. The stock rallied 246% in 2023 and is up about 160% so far this year, a jump that has some resemblance to the social media-fueled gains of AMC Entertainment Holdings Inc. and GameStop Corp.

Read more: Super Micro CEO Eyes $25 Billion in Sales — But Needs More Chips

“All of a sudden it kind of got a meme stock kind of feel,” said Brian Mulberry, client portfolio manager at Zacks Investment Management, adding that Super Micro does have good things going for it like underlying growth.

Still, its run has been helped by the “AI wave,” Mulberry added. “It got pumped up to a point and then you start to see the shorts build in and it’s like, all right, I’ve seen this movie before.”

Read more: Super Micro’s Vertical Stock Move Suggests a ‘Casino Mentality’

–With assistance from Carly Wanna.

(Adds stock move at market open, comments from Rosenblatt Securities.)

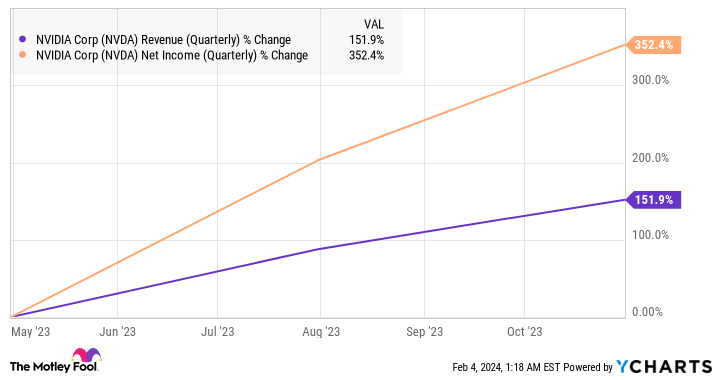

The artificial intelligence (AI) gravy train has given several stocks a big boost over the past year, notably Nvidia, which has capitalized on the booming demand for AI chips and enjoyed an eye-popping jump in its revenue and earnings. Shares of Nvidia have shot up a terrific 215% in the past year.

As the chart shows, the stock’s surge is justified, considering how rapidly its revenue and earnings have increased in recent quarters.

NVDA Revenue (Quarterly) Chart

However, the big jump in price means that shares of Nvidia are not in value territory anymore. Nvidia sports a stunning price-to-sales ratio of 37. It also trades at a lofty 90 times trailing earnings, which is higher than its five-year average of 79.

Of course, Nvidia can justify these expensive multiples by sustaining its solid growth in the future, but there are cheaper options to capitalize on the AI wave as well. Super Micro Computer(NASDAQ: SMCI) and Qualcomm(NASDAQ: QCOM) are two attractively valued stocks that you may consider buying right now.

1. Super Micro Computer

Super Micro Computer is already in red-hot form on the stock market, surging a whopping 587% in the past year and crushing Nvidia’s returns by a huge margin. However, shares of the company that’s known for making AI server and storage solutions continue to trade at very attractive levels despite this huge jump.

You can buy Super Micro stock for just 3.3 times sales right now. Buying the stock at this valuation looks like a no-brainer, not only because it is way cheaper than Nvidia, but also because it is growing at a tremendous pace.

Super Micro released its fiscal 2024 second-quarter results (for the three months ended Dec. 31) on Jan. 29. The company’s revenue more than doubled from the year-ago period to $3.66 billion last quarter. Its non-GAAP (generally accepted accounting principles) net income shot up from $3.26 per share in the year-ago period to $5.59 per share.

The company’s impressive revenue and earnings growth was driven by the rapid deployment of AI servers. Super Micro has optimized its server solutions according to the requirements of AI servers, helping data center operators reduce electricity and cooling costs. Its server rack solutions are used for deploying AI chips from multiple vendors such as Nvidia, Intel, and Advanced Micro Devices.

The good part is that the company is witnessing terrific demand for its offerings, which is why it has been focused on enhancing its production capacity. Charles Liang, CEO of Super Micro, pointed out on the company’s latest earnings conference call:

Today, our production utilization rate is about 65% across our USA, Netherlands, and Taiwan facilities, and they are quickly filling. To address this immediate capacity challenge, we are adding two new production facilities and warehouses near our Silicon Valley HQ, which will be operating in a few months. The new Malaysia facility will focus on expanding our building blocks with lower costs and increased volume, while other new sites will support our annual revenue capacity above $25 billion.

It won’t be surprising to see Super Micro eventually hitting $25 billion in annual revenue thanks to its capacity expansion moves, as demand for AI servers is expected to grow fivefold between 2023 and 2027, generating an annual revenue of $150 billion at the end of the forecast period.

More importantly, Super Micro is already benefiting from this solid growth in AI server demand, as its latest guidance update tells us. The company now expects to end fiscal 2024 with revenue of $14.5 billion at the midpoint of its guidance range, which would be a 106% jump over the prior year. Super Micro was earlier expecting fiscal 2024 revenue to land at $10.5 billion.

Assuming Super Micro does hit its annual revenue guidance and maintains its sales multiple, its market capitalization could increase to $48 billion. That would be a 50% jump from current levels, which is why investors looking to add an AI stock to their portfolios should consider acting quickly before Super Micro heads higher.

2. Qualcomm

Share of Qualcomm have underperformed the broader market over the past year with gains of just 5%, which is not surprising, considering the mobile chipmaker’s tepid financial performance.

QCOM Revenue (TTM) Chart

Qualcomm has been weighed down by poor smartphone sales in the past year. According to market research firm IDC, smartphone shipments were down 3.2% in 2023 to 1.17 billion units. Qualcomm gets more than two-thirds of its total revenue from selling chipsets used in smartphones, so the weakness in this segment was bound to have a negative impact on the company’s performance.

The good news for Qualcomm is that the smartphone market is set for a solid turnaround from 2024. The turnaround is already underway, with smartphone shipments rising 8.5% in the fourth quarter of 2023, outpacing the 7.3% growth that analysts were looking for.

Morgan Stanley is anticipating the global smartphone market to grow by 4% in 2024 and 4.4% next year. However, the pace of growth in Q4 2023 points toward better smartphone sales growth this year, with AI expected to play a central role in driving a stronger performance.

Counterpoint Research estimates that shipments of generative AI-powered smartphones could hit 100 million units in 2024. Annual shipments of AI-enabled smartphones are expected to hit 522 million units in 2027, clocking an annual growth rate of 83%.

In all, a total of 1 billion AI-powered smartphones are expected to be shipped over the next four years. Qualcomm is already on its way to capitalizing on this opportunity, with its Snapdragon 8 Gen 3 chip powering AI features on Samsung‘s latest Galaxy S24 Ultra smartphone. Qualcomm’s management pointed out on the latest earnings conference call that Samsung’s S24 family of devices includes “on-device AI features such as live translate interpreter, chat assist, nightography, and more.”

Additionally, Qualcomm has “extended a multi-year agreement with Samsung relating to Snapdragon platforms for flagship Galaxy smartphone launches starting in 2024.” This should pave the way for Qualcomm to take advantage of the nascent AI-enabled smartphone market in the long run, considering that Samsung is the world’s second-largest smartphone manufacturer.

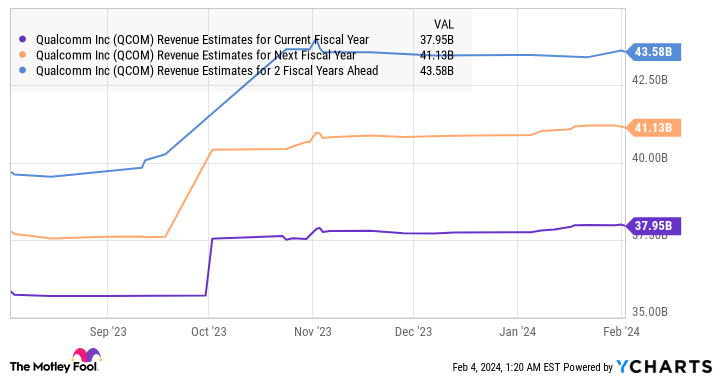

It is worth noting that analysts have already been raising Qualcomm’s revenue growth estimates of late.

QCOM Revenue Estimates for Current Fiscal Year Chart

AI could give the company an additional lift and help Qualcomm outpace analysts’ expectations in the future. But even if the company hits $44 billion in annual revenue over the next couple of years and maintains its current sales multiple of 5, its market capitalization could jump to $220 billion. That would be a 39% increase over current levels.

However, don’t be surprised to see Qualcomm stock delivering stronger gains on the back of a faster jump in its revenue. Moreover, the market may reward it with a higher sales multiple based on its AI prospects, which is why savvy investors would do well to buy the stock now.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Nvidia, and Qualcomm. The Motley Fool recommends Intel and Super Micro Computer and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $45 calls on Intel, and short February 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.

Shares of Super Micro Computer(NASDAQ: SMCI) were rallying big for the second day in a row on Tuesday, up 5.3% as of 12:46 p.m. ET.

The company didn’t disclose any new company-specific news today, but will appear at an industry analyst conference tomorrow. In addition, today’s rally was likely further fueled by a similar two-day rally for Nvidia, Super Micro’s close partner in artificial intelligence (AI) servers, which did have some positive news.

Following yesterday’s new product announcements at CES around AI PCs and autonomous driving, the AI chip giant received a buy rating and target price upgrade from Wall Street amid increasing AI-related optimism. Nvidia’s good day carried Super Micro along with it.

Nvidia is upgraded as a “best idea” in 2024

Today, Nvidia received a reaffirmation of a buy rating from Oppenheimer analyst Rick Schafer. In a note to investor clients, Schafer boosted price targets for four artificial intelligence “top picks” for 2024. These included Nvidia, with a $650 price target, along with positive notes on three other AI-related chip stocks, Marvell Technology, Broadcom, and Monolithic Power Systems.

In general, positive AI and Nvidia-related notes also filter down to Super Micro Computer, which has become a preferred server provider for AI-related applications. Last quarter, SMCI management noted that more than 50% of its revenue came from AI-related servers. That’s a higher percentage than rivals such as Hewlett-Packard Enterprise, which only got about 16% of its revenue from AI-related servers last quarter.

On a related note, it appears HP Enterprise is reportedly in talks to purchase router company Juniper Networks for about $13 billion, according to The Wall Street Journal. The deal seems a bit odd, as adding Juniper would add routing capabilities in between data centers, but doesn’t seem particularly relevant for AI servers themselves. So, to have a potential Super Micro competitor seemingly take its eye off the ball with a large acquisition and a reach for growth could also be seen as a positive for Super Micro.

Finally, Super Micro management will attend the CJS Securities 24th annual “New Ideas for the New Year” conference tomorrow. Investors may be anticipating good news or perhaps an earnings pre-announcement, which Super Micro has done in the past. However, Super Micro did not pre-announce its results last quarter.

A reasonably priced play on AI

Super Micro rallied over 246% in 2023, and is already up nearly 20% for 2024. That being said, the stock is still slightly below the all-time highs reached last August.

The stock certainly isn’t as cheap as it once was at 31 times trailing earnings. However, that’s actually cheaper than several other AI plays on a relative basis, and Super Micro management has already forecast 40%-plus growth this fiscal year.

Investors will get more color on the company’s trajectory tomorrow, with earnings coming up in a few weeks.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

Billy Duberstein has positions in Broadcom and Super Micro Computer and has the following options: short January 2025 $110 puts on Super Micro Computer, short January 2025 $125 puts on Super Micro Computer, short January 2025 $130 puts on Super Micro Computer, short January 2025 $280 calls on Super Micro Computer, short January 2025 $380 calls on Super Micro Computer, and short January 2025 $85 puts on Super Micro Computer. His clients may own shares of the companies mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool recommends Broadcom, Marvell Technology, and Super Micro Computer. The Motley Fool has a disclosure policy.

Investors have a lot to celebrate. The stock market will end 2023 near all-time highs after a fierce rebound that saw the Nasdaq Composite surge more than 40% this year, one of its best performances in decades.

It sets a high bar for 2024 as investors seek ways to continue the momentum. Three Fool.com contributors sifted through their top ideas to identify Amazon(NASDAQ: AMZN), Super Micro Computer(NASDAQ: SMCI), and SentinelOne(NYSE: S) as AI stocks with the right stuff to outperform a hot market in 2024.

Here is the investment pitch for each.

Amazon’s AI could be looking at a breakout year

Jake Lerch (Amazon): As of this writing, Amazon is up 83% year to date. It’s been an incredible year for the company, but I believe 2024 could be even better.

That’s because Amazon has only scratched the surface of its artificial intelligence (AI) potential. Indeed, in a recent interview with CNBC, CEO Andy Jassy said that “generative AI is going to change every customer experience.”

AI could prove to be an enormous competitive advantage for Amazon, which prides itself on anticipating customers’ wants and needs.

Take Alexa, Amazon’s signature virtual assistant. Jassy noted in the interview that, “if you’ve studied generative AI and you’re still scoffing, you’re really not paying attention. … We think we have a real opportunity to be the leader there, and we’re in the process of building a much more expansive large language model underneath Alexa that will make her both much more knowledgeable and much more conversational.”

In other words, get ready for a ChatGPT-like experience coming to an Alexa-enabled device near you soon. Need a new pair of shoes? Amazon wants you to talk with Alexa about the style you’re looking for, compare prices, and then buy — through an Amazon e-commerce partner, of course.

What’s more, Amazon already has a massive treasure trove for training large language models — its own data. With every search, review, or purchase, Amazon collects data that could be used to help it train and tailor its AI.

Amazon is something of a sleeping giant when it comes to AI. And 2024 could be the year that this goliath really springs to life.

The emergence of generative AI plays into the hands of this company

Will Healy(Super Micro): Super Micro Computer is not a household name for AI or tech investors. But it existed for more than 30 years and it began by selling motherboards.

Today, it’s best known for selling switches, servers, and solutions for storage and networking. However, it also offers combined hardware and software solutions that have become important amid the rise of generative AI.

Additionally, its rack-scale solutions support the cloud, metaverse, 5G, and edge infrastructure. Users may also like that Super Micro designs its products to save energy and minimize the impact on the environment. That growth helped it secure over 6 million square feet of manufacturing space and establish operations in more than 100 countries.

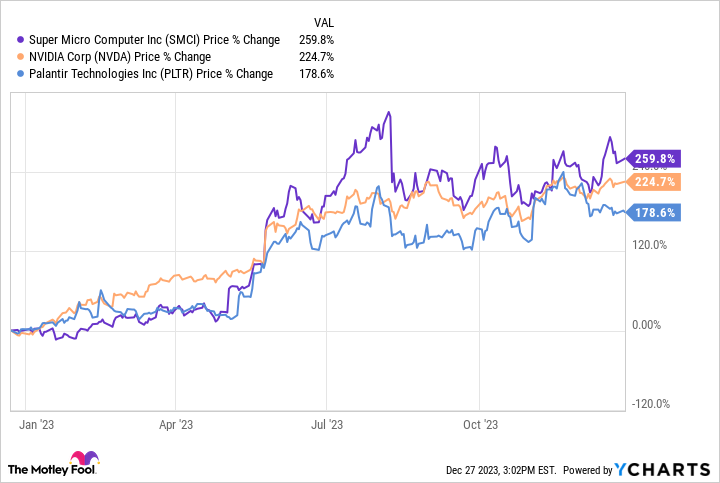

Thanks primarily to AI-driven interest, the AI stock is up more than 250% over the last year — outperforming powerhouse AI stocks such as Nvidia and Palantir.

SMCI Chart

There’s no guarantee Super Micro will repeat those results in 2024, and supply constraints and higher capital expenditures spending weighed on the financials. Its $2.1 billion in net sales for the first quarter of fiscal 2024 (ended Sept. 30) grew 14% yearly after revenue had surged 37% higher in fiscal 2023. Also, fiscal Q1 net income of $157 million fell short of the $184 million earned in the same year-ago quarter.

Still, with the AI-driven growth in the pipeline, that decline will probably amount to a temporary setback. The company forecasts net sales of $10 billion to $11 billion, which would mean 47% growth at the midpoint.

Moreover, Super Micro’s valuation significantly lags other AI giants despite the massive stock price gains. Its forward P/E ratio of 17 trails Nvidia’s forward earnings multiple of 40 and Palantir’s forward valuation of almost 71. That implied potential for multiple expansion and Super Micro’s positioning in the AI industry will likely mean the stock continues to march higher in 2024.

Wall Street hasn’t yet caught up to SentinelOne’s progress

Justin Pope (SentinelOne): Cybersecurity company SentinelOne went public at the height of the last bull market. The stock initially soared, then crashed as investors fled growth stocks due to rising interest rates. SentinelOne remains over 60% off its former high despite shares surging roughly 90% in 2023. But Wall Street could still be missing just how much SentinelOne progressed over these past 24 months.

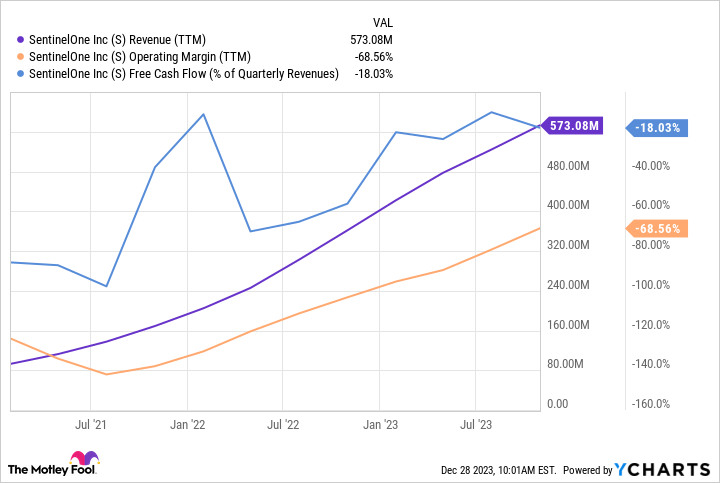

The stock’s valuation peaked at a price-to-sales (P/S) ratio of over 106 but sits at just 14 today. Not only has the share price come down, but SentinelOne has been rapidly growing its business. Revenue has multiplied, and profit margins are racing higher:

S Revenue (TTM) Chart

Notably, there are plenty of opportunities for SentinelOne to keep growing and become profitable over the long term. Artificial intelligence is the foundation of its core endpoint security product and is showing up in product expansions. Its Singularity Data Lake and Cloud Security products more than doubled sales year over year in Q3, and it’s begun rolling out Purple AI, a generative AI that can assist customers in using SentinelOne’s security products.

Analysts see SentinelOne’s revenue surpassing $1 billion over the next few years. Assuming profitability continues improving as revenue grows, the stock is a prime candidate to outgrow and outrun the broader market in 2024.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for two decades, Motley Fool Stock Advisor, has more than tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now… and Amazon made the list — but there are 9 other stocks you may be overlooking.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Jake Lerch has positions in Amazon and Nvidia. Justin Pope has positions in SentinelOne. Will Healy has positions in Palantir Technologies. The Motley Fool has positions in and recommends Amazon, Nvidia, and Palantir Technologies. The Motley Fool recommends Super Micro Computer. The Motley Fool has a disclosure policy.