Today, as the MarketBeat Podcast celebrates the milestone of Episode 50, Kate welcomes back a popular guest, Jason Brown of the Brown Report. Today, he discusses three widely held large caps. If you don’t own these as individual stocks, you may own them inside index funds. Their sheer size means they have influence over index direction. Jason presents a strong bull case for the future of each stock, regardless of the current market downturn. And he shares why he believes they are likely to hold near recent support levels, rather than continue falling. In today’s episode, Kate and Jason discuss: Why Amazon could be considered a “good company” because it has carved out a secure role as a company consumers trust to buy the goods they need and want. It’s hard for other companies to compete with that. Jason believes the downside potential for Amazon is limited, but based on the chart, he sees more room to grow to the upside. He walks listeners through some of the price points he’s seeing. What is the significance of the “unknown” business (at least to consumers) Amazon Web Servers, which has huge corporations as customers? Jason’s next stock is Google/Alphabet, which he believes is one of the best positioned to emerge from the post-pandemic, interest-rate driven selloff Why Google’s ad-based business model is likely to hold up even in a recession, or gas price increases or interest-rate hikes, even if some advertisers slash spending Jason’s third stock is Tesla, where he sees ongoing potential due to the business itself, and the stock’s chart Why Jason says it’s more important to look at Tesla’s future, not the news today, such as disappointing Q3 deliveries Is there upside in not-yet-available products such as electric boats and motorcycles? Why Tesla’s focus on EVs means it can continue growing without distractions, as the legacy automakers have How to find Jason, and download the Stock Market Starter Pack and Stock Options Starter Pack: https://thebrownreport.com/ Let’s all become smarter investors together. Subscribe to the MarketBeat Podcast today.

After slipping to its lowest level since 2013, Biogen Inc. (NASDAQ:BIIB) was all but forgotten by growth investors. That changed in dramatic fashion late last month when the biotech’s pipeline got a major boost.

MarketBeat.com – MarketBeat

Why Did Biogen’s Stock Jump Higher?

On September 27th, Biogen along with co-development partner and Japanese pharmaceutical leader Eisai announced positive top-line data from their Phase 3 trial of lecanemab. The investigational treatment for early-stage Alzheimer’s disease met its primary endpoint in reducing cognitive and functional decline by 27%. It also met the secondary endpoint of changing amyloid levels in the brain in a statistically significant manner.

The news was greeted with intense buying activity for a stock that had plunged 58% from its summer 2021 peak. Biogen shares gapped up 40% on the day of the announcement in 15-times the 90-day average volume. The stunning gapper erased 10 months of losses in a single day, bringing newfound hope to biotech investors.

The FDA has agreed to use the Biogen/Eisai trial as a confirmatory study. This means that it will be used to confirm the clinical benefit of the Alzheimer’s candidate as it reviews the pair’s Biologic License Application (BLA). The regulatory body granted priority review for the BLA and set an action date target of January 6th.

As the market awaits the pivotal FDA decision, additional data from the lecanemab study is expected to be released at the Clinical Trials on Alzheimer’s Congress (CTAC) conference held in San Francisco from November 29th through December 2nd.

Is it a Good Time to Invest in Biogen Stock?

Unfortunately for Biogen shareholders, the big rally was short-lived but not by any fault of the company. Selling pressure set in because of the broader market downturn causing the stock to slide back to the mid-$200’s.

A second burst came on Thursday, however, when Biogen benefitted from a strong day in the market and surged back to the $270 level. Yet it is still trading below where it soared on the Phase 3 lecanemab update, giving investors an opportunity to pounce on a name that has momentum on its side and a potential catalyst to come in January’s anticipated FDA decision.

While some sell-side research firms have taken a cautious stance after the big move (and due to FDA uncertainty), others see more gains ahead. More than a dozen analysts have called Biogen stock a buy since the big news, expecting the positive trial outcome to pave the way for FDA approval. Several of the revised price targets run well into the $300’s.

However, there’s reason to be cautious here because Biogen is no stranger to extreme volatility. Less than two years ago, the stock went on a wild up and down ride related to another Alzheimer’s drug (aducanumab). The FDA initially offered a positive review of the drug only to decline endorsement days later. Marketed under the Aduhelm name, the drug was ultimately not covered by Medicare, dealing a devastating blow to the company and its investors.

Many are expecting this time to be different. The data around lecanemab has been particularly strong which, combined with the limited options for Alzheimer’s patients, makes it hard to deny. According to the Alzheimer’s Association, more than 6 million Americans are living with Alzheimer’s disease. Within the next 30 years, the costs associated with Alzhiemer’s and other forms of dementia are expected to approach $1 trillion.

What are Biogen’s Growth Prospects?

The developments around lecanemab will dictate where Biogen’s stock goes in the near-term. Even if it clears regulatory hurdles, securing approval from the Centers for Medicare and Medicaid Services is another hurdle. Getting FDA approval without the backing of Medicare would be a major setback.

While Biogen has become synonymous with Alzheimer’s treatment over the last few years, the company has a larger growth driver at hand. Led by its flagship Tecfidera product, multiple sclerosis (MS) drugs account for approximately two-thirds of Biogen’s revenue. And with generic competition on the rise in the MS market, the need for a non-MS blockbuster such as lecanemab can’t come soon enough.

Outside of its MS and Alzheimer’s programs, Biogen owns the first approved treatment for spinal muscular atrophy. It has also achieved milestones on new treatments for depression and various neuromuscular disorders. It is ramping up its own biosimilar product launches to combat the growing threat of generics. Looking into the back half of the decade, new programs in neuropsychiatry, Parkinson’s disease, lupus and stroke are expected to progress.

In the meantime, Biogen’s five different MS products will be leaned on to build off last year’s $7.1 billion revenue total. Whether its latest Alzheimer’s drug turns into a blockbuster or not, the company is positioned to become more diversified over time. This translates to a diminishing risk profile which, combined with the emerging growth prospects, makes the stock attractive here.

September inflation report came in hotter than expected, increasing the chances of aggressive interest rate hikes later this year. Since analysts expect the economy to tip into a recession next year, dividend-paying stocks Walmart (WMT), Coca-Cola (KO), and Greif (GEF), which are backed by solid fundamentals, could help you plan your retirement even in a bear market. Read more….

shutterstock.com – StockNews

The Federal Reserve has undertaken a series of interest rate hikes in an effort to control the surging inflation. Despite rate hikes, inflation came in hotter than expected in September, rising 0.4% sequentially and 8.2% from a year ago. The report initially rattled financial markets,with stock market futures plunging and Treasury yields increasing.

The latest GDP estimate showed that theU.S. economy contracted in the first half of this year. JPMorgan Chase & Co. (JPM) Chief Executive Officer Jamie Dimon cautioned about thepossibility of a recession, as persistent and elevated inflation could cause interest rates to rise higher than 4.5%.

The S&P 500 has slid more than 20% this year, signaling a bear market. However, theremight still be opportunities left for long-term investors, as bear markets usually don’t continue for long.

Given this backdrop, fundamentally strong dividend stocks Walmart Inc. (WMT), The Coca-Cola Company (KO), and Greif, Inc. (GEF) could be solid investments to ensure a stable income stream.

WMT engages in the operation of retail, wholesale, and other units worldwide. The company operates through three segments: Walmart U.S.; Walmart International; and Sam’s Club.

On October 3, WMT’s division Sam’s Club launched its expanded Photo and Customization Services, where its members are granted access to professional photographers, enhanced photo printing services, as well as made-to-order apparel and home goods, making Sam’s Club the first to do so in the warehouse space.

On September 28, WMT celebrated the grand opening of Walmart’s first of four Next Generation Fulfillment Centers in Joliet, Illinois. The new FC should improve the company’s operative capacity and might drive up its revenues.

In February, WMT declared an annual dividend of $2.24 per share to be paid in four quarterly installments of $0.56 per share. Its annual dividend yields 1.69% on prevailing prices. The company’s dividend payouts have increased at a 1.9% CAGR over the past three and five years. The company has a record of 48 years of consecutive dividend growth.

WMT’s total revenues came in at $152.86 billion for the second quarter that ended July 31, 2022, up 8.4% year-over-year. Its consolidated net income came in at $5.15 billion, up 17.9% year-over-year, while its EPS stood at $1.88, up 23.7% year-over-year.

The consensus EPS estimate of $1.48 for the fiscal fourth quarter ending April 2023 represents a 14.1% improvement year-over-year. The consensus revenue estimate of $144.64 billion for the same quarter indicates a 3.1% increase from the prior-year period. The company has an impressive earnings surprise history, surpassing the consensus EPS estimates in three of the trailing four quarters.

Over the past three months, the stock has gained 5.5% to close the last trading session at $132.28.

WMT’s POWR Ratings reflect this promising outlook. The company’s overall A rating translates to Strong Buy in our proprietary rating system. The POWR Ratings assess stocks by 118 different factors, each with its own weighting.

It has an A grade for Sentiment and a B for Growth, Stability, and Quality. It is ranked #6 out of 38 stocks in the A-rated Grocery/Big Box Retailers industry.

To see the additional POWR Ratings for WMT for Value and Momentum, click here.

Beverage company KO manufactures, markets, and sells various non-alcoholic beverages worldwide. The company provides sparkling soft drinks, flavored and enhanced water, sports drinks, juice, dairy and plant-based beverages, tea and coffee, and energy drinks.

On September 29, KO and Molson Coors Beverage Company (TAP) announced that they had entered into an exclusive agreement to develop and commercialize Topo Chico Spirited, a line of spirit-based, ready-to-drink cocktails. The new product launch might bolster the company’s revenue stream.

On July 21, KO declared a quarterly dividend of 44 cents per common share, which was payable to shareholders on October 3. Its annual dividend of $1.76 yields 3.15% on prevailing prices. The company’s dividend payouts have increased at a 3.1% CAGR over the past three years and a 3.6% CAGR over the past five years. The company has a record of 59 years of consecutive dividend growth.

KO’s net operating revenue increased 11.8% year-over-year to $11.33 billion in the second quarter that ended July 1. Its non-GAAP gross profit grew 7.2% from the year-ago value to $6.67 billion, while its non-GAAP net income improved 4.4% year-over-year to $3.06 billion. The company’s non-GAAP net earnings per common share increased 2.9% from its year-ago value to $0.70.

Street expects KO’s revenue to increase 8.9% year-over-year to $42.09 billion in the fiscal year 2022. Its EPS is estimated to grow 5.9% year-over-year to $2.46 in the same year. It has surpassed EPS estimates in all four trailing quarters, which is impressive.

KO’s shares have gained 2.5% over the past five days to close the last trading session at $55.87.

KO’s overall B rating equates to a Buy in our proprietary rating system. The stock has a B grade for Stability, Sentiment, and Quality. It’s ranked #17 out of 35 stocks in the A-rated Beverages industry.

Click here to get the KO ratings for Growth, Value, and Momentum.

GEF is a global producer of industrial packaging products and services. The company operates through three segments: Global Industrial Packaging; Paper Packaging & Services; and Land Management.

On August 30, GEF declared quarterly cash dividends of $0.50 per share on its Class A common stock and $0.75 per share on its Class B common stock, which was payable on October 1, 2022. Its annual dividend of $2.00 yields 3.37% on prevailing prices. The company’s dividend payouts have increased at a 2.2% CAGR over the past three years and a 2.3% CAGR over the past five years.

For the fiscal third quarter that ended July 31, 2022, GEF’s net sales increased 8.8% year-over-year to $1.62 billion. The company’s operating profit increased 18.8% year-over-year to $205.70 million. Also, its net income rose 23.4% year-over-year to $146.10 million, while its class A common stock EPS grew 24.9% from its prior-year quarter to $2.36.

For the fiscal year ending October 2022, GEF’s EPS and revenue are expected to increase 43.2% and 16% year-over-year to $8.02 and $6.45 billion, respectively. It has surpassed the consensus EPS estimates in each of the trailing four quarters.

The stock has declined 1.4% over the past five days to close the last trading session at $59.34.

GEF’s POWR Ratings reflect this promising outlook. The stock has an overall rating of A, translating to a Strong Buy in our proprietary rating system. It also has a B grade for Value and Quality. Within the A-rated Industrial – Packaging industry, it is ranked #3 out of 22 stocks.

Beyond what we’ve stated above, we have also given GEF grades for Growth, Momentum, Stability, and Sentiment. Get all GEF ratings here.

WMT shares were trading at $130.77 per share on Friday afternoon, down $1.51 (-1.14%). Year-to-date, WMT has declined -8.54%, versus a -23.65% rise in the benchmark S&P 500 index during the same period.

About the Author: Kritika Sarmah

Her interest in risky instruments and passion for writing made Kritika an analyst and financial journalist. She earned her bachelor’s degree in commerce and is currently pursuing the CFA program. With her fundamental approach, she aims to help investors identify untapped investment opportunities.

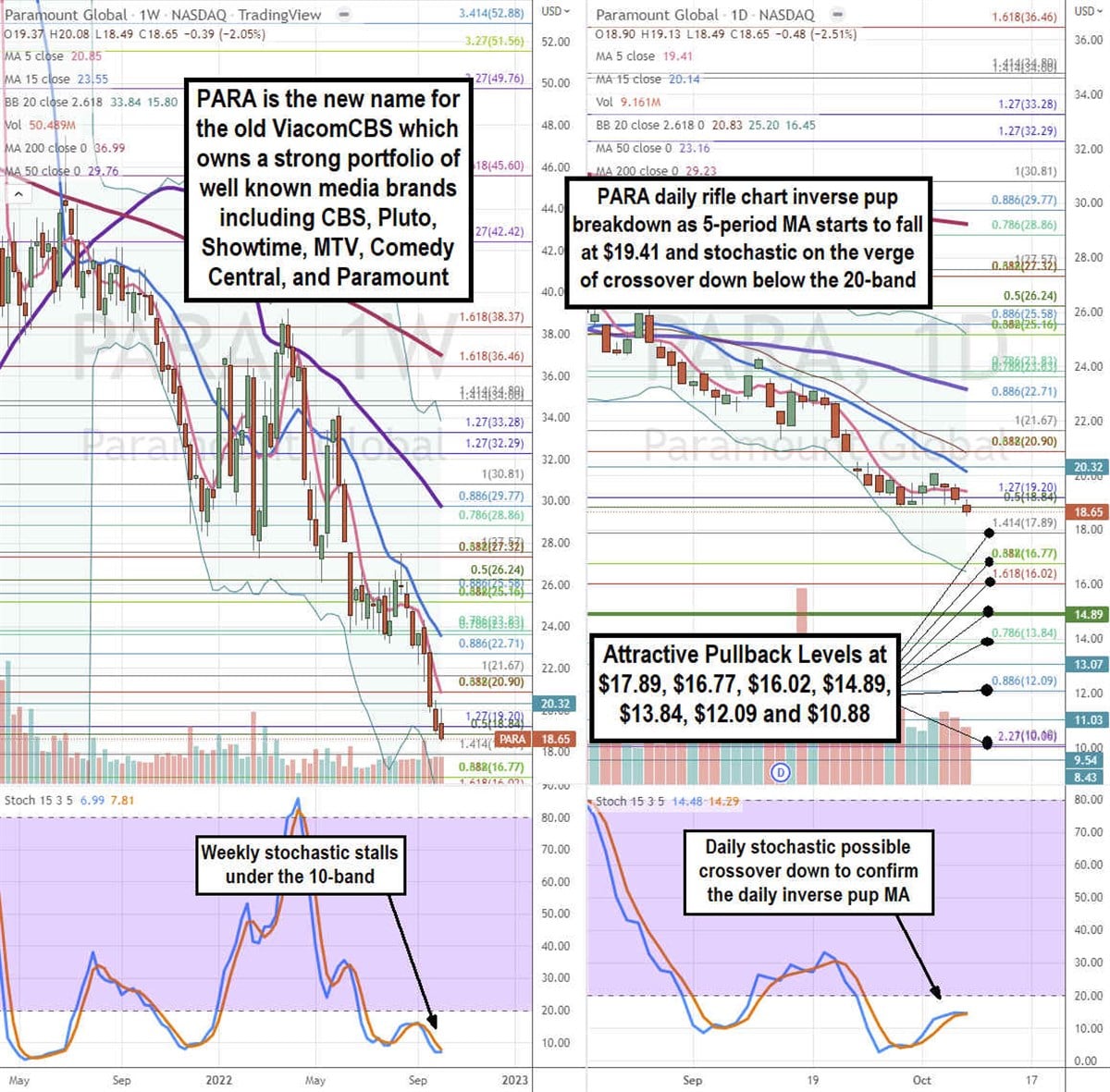

Global media entertainment giant Paramount Global(NASDAQ: PARA) has undergone an image makeover and rebranding after its stock collapsed as ViacomCBS. Hoping to shed its controversial past with the Redstone family drama and the Archegos Capital Management $20 billion blowup, the company has emerged as a still profitable sum-of-all parts media empire which may be vastly overlooked by the market. Its shares trade at less than a fifth of its value just over a year ago. Paramount Global is an entertainment powerhouse with brands that include Paramount, Pluto, Showtime, CBS, CBS Sports, Nickelodeon, MTV, Comedy Central, BET and the Smithsonian Channel. CBS is the No. 1 broadcast network in the country and it grew its market share by 20% from last year. Warren Buffett increased his shares from 68.95 million to 78.42 million through the Berkshire Hathaway Inc. (NYSE: BRK.A) 13F filing for Q2 2022 on August 15. Shares have since fallen as they now sell for 8x forward earnings with a 5.15% annual dividend yield.

MarketBeat.com – MarketBeat

Top Gun 2 Kills It

Paramount Studios released five No. 1 box office films in a row. It had the strongest movie of the year, “Top Gun 2,” which raked in $1.45 billion worldwide on a $170 million budget. The movie has surpassed the $714 million box office mark in the U.S., making it the 22nd largest grossing movie of all time in unadjusted global earnings. Management showed impeccable timing for the release of the surprise blockbuster.

Using the rifle charts on the weekly and daily time frames provides a precision view of the landscape for PARA stock. The weekly rifle chart has been collapsing on the inverse pup breakdown through the $23.83 Fibonacci (fib) level. The weekly 5-period moving average (MA) resistance continues to fall at $20.85 followed by the weekly 15-period MA resistance at $23.55. The weekly lower Bollinger Bands (BBs) sit at $15.80 still above its weekly market structure low (MSL) buy trigger at $14.89. The weekly stochastic rejected the 20-band bounce attempt and crossed back down through the 10-band to stall again for a possible bounce or mini inverse pup. The daily rifle chart is forming an inverse pup breakdown as shares fall under the daily five-period MA at $19.41, followed by a falling daily 15-period MA at $20.14. The daily lower BBs sit at $16.45 as the stochastic stalls below the 20-band for a possible crossover back down to confirm the daily MA inverse pup breakdown. Attractive pullback levels sit at the $17.89 fib, $16.77 fib, $16.02 fib, $14.89 weekly MSL trigger, $13.84 fib, $12.09 fib and the $10.88 fib level.

Digital Driving Growth

On August 4, Paramount released its fiscal Q2 results for the quarter ending June 2022. The company reported earnings per share (EPS) of $0.64, beating $0.62 consensus analyst estimates by $0.02. Revenues climbed 18% year-over-year (YoY) to $7.78 billion, beating consensus analyst estimates for $7.55 billion. Paramount+ added 4.9 million new subscribers and removed 1.2 million Russia subscribers to grow to over 43 million subscribers. Advertising revenues rose 25% in the DTC segment, driven by increases impressions on both Paramount+ and Pluto TV. Advertising revenues fell (-6%) to $2.17 billion due to lower linear impressions and FX.

Semiconductor companies, such as NVIDIA Corporation (NVDA), are struggling amid the market downturn, export restrictions, and slowing demand. However, the broader technology market is expected to endure short-term uncertainties and keep growing due to continued digitization. Hence, we think quality technology stocks Cisco (CSCO) and Hackett Group (HCKT) are better investments than NVDA. Keep reading….

shutterstock.com – StockNews

NVIDIA Corporation (NVDA) provides graphics, computation, and networking solutions globally. On October 7, new restrictions were imposed on chipmakers, including NVDA, to prevent technology from advancing China’s military power. The companies must now obtain a license from the Commerce Department to export advanced chips and chip-making equipment.

The above restrictions have closely followed last month’s announcement in which the White House blocked NVDA from exporting high-end graphics chips to China due to similar concerns. The company said the ban impacted $400 million in potential sales to China.

For the fiscal 2022 second quarter, NVDA’s non-GAAP net income and EPS declined 50.7% and 51% year-over-year to $1.29 billion and $0.51, respectively. Also, analysts expect its EPS and revenue for the fiscal 2023 third quarter (ending October 2022) to come in at $0.71 and $5.85 billion, indicating a 39.3% and 17.6% year-over-year decline, respectively. The stock has plummeted 59.9% year-to-date.

The recently released jobs data for September seems to have paved the way for another significant interest rate increase by the Federal Reserve during its meeting next month. This indicates another headwind for tech companies.

Despite the current headwinds, demand for ubiquitous tech goods and services is expected to keep growing amid the increasing adoption of cloud computing, artificial intelligence (AI), virtual reality (VR), the internet of things (IoT), and increasing automation of business processes.

The global technology market is expected to grow at a CAGR of 25.7% over the next five years to reach $3.17 billion by 2027, with the United States expected to strengthen its leadership in this space.

Hence, we suggest investing in fundamentally strong technology stocks Cisco Systems, Inc. (CSCO) and Hackett Group Inc. (HCKT) instead of NVDA for better risk-adjusted returns.

CSCO designs, manufactures, and sells internet protocol-based networking and other products across networking, security, collaboration, applications, and the cloud. The company operates through three geographic segments: the Americas; Europe, the Middle East, and Africa (EMEA); and Asia Pacific, Japan, and China (APJC).

On October 5, CSCO announced an expansion of its existing SD-WAN partnership with Microsoft (MSFT) to allow customers to sidestep the public internet and MPLS to send their Cisco SD-WAN traffic over the latter’s Azure cloud backbone. This is expected to add value by providing speed and cost benefits.

For the fiscal year 2022 ended July 31, CSCO’s revenue increased 3.6% year-over-year to $51.6 billion, while its operating income increased 8.9% year-over-year to $13.97 billion. The company’s non-GAAP net income increased 3.7% year-over-year to $14.10 billion, which translates to an EPS of $3.36, up 4.3% year-over-year.

Analysts expect CSCO’s revenue and EPS for the fiscal year 2023 to increase 5% and 5.1% year-over-year to $54.11 billion and $3.53, respectively. The company has an impressive earnings surprise history, surpassing the consensus EPS estimates in each of the trailing four quarters.

Over the past month, CSCO’s stock slumped 9.6% to close the last trading session at $40.27.

CSCO’s overall B rating equates to a Buy in our POWR Ratings system. The POWR Ratings assess stocks by 118 different factors, each with its own weighting.

HCKT operates as a business and technology consulting firm. The company offers benchmarking, executive advisory, business transformation, and cloud enterprise application implementation.

On September 22, HCKT announced the launch of a new Market Intelligence Service for software and service providers and users. The service will measure software and service providers’ ability to deliver business value and their unique capabilities to help companies achieve Digital World Class performance.

HCKT believes the new service will be a powerful and attractive value proposition for all C-level executives and their respective teams.

HCKT’s total revenue increased 3.7% year-over-year to $75.93 million for the second quarter of 2022. The company’s total assets stood at $217.89 million as of July 1, 2022, compared to $207.54 million as of December 31, 2021.

Analysts expect HCKT’s revenue and EPS for the fiscal year 2022 to increase 6.6% and 10.4% year-over-year to $297.20 million and $1.45, respectively. Also, the company has surpassed the consensus EPS estimates in each of the trailing four quarters.

HCKT’s stock has slumped 2.4% over the past month to close the last trading session at $19.05.

HCKT’s promising outlook is reflected in its overall POWR Rating of A, which translates to a Strong Buy in our proprietary rating system. It also has a grade of A for Sentiment and Quality and a B for Value and Stability.

Click here for an additional rating of HCKT (Growth and Momentum).

NVDA shares were trading at $116.70 per share on Monday afternoon, down $4.06 (-3.36%). Year-to-date, NVDA has declined -60.29%, versus a -23.32% rise in the benchmark S&P 500 index during the same period.

About the Author: Santanu Roy

Having been fascinated by the traditional and evolving factors that affect investment decisions, Santanu decided to pursue a career as an investment analyst. Prior to his switch to investment research, he was a process associate at Cognizant.

With a master’s degree in business administration and a fundamental approach to analyzing businesses, he aims to help retail investors identify the best long-term investment opportunities.

On September 27, 2022, the British pound sterling fell (-3.5%) to $1.084 hitting 37-year lows against the U.S. dollar. The pound tumbled further to a low of $1.0350 after U.K. Chancellor of Exchequer commented two days later there would be “more to come” in regard to the misguided economic stimulus plan of the new U.K. government led by Prime Minister Liz Truss. Three weeks into her term, Truss made a misstep of massive proportions by arguing that the stimulus plan would kickstart the U.K. economy after a decade-long slump.

MarketBeat.com – MarketBeat

Egg in the Face

The stimulus plan includes a multitude of tax cuts for higher income earnings and business incentives that spooked investors to dump the pound and buy the U.S. dollar. The proposed tax cuts would be the highest in nearly 50-years trimming the the top income tax and corporate tax rate. The U.K. government is expected to turn on the printing presses to finance the deficit causing the yield for the 10-year U.K. bonds to spike towards 12-year highs at 3.759%. This comes just days after the Bank of England raised interest rates by 50 basis points stating that the U.K. economy is very likely in a recession. Inflation rose to a near 40-year high in August hitting 9.9%. A series of expenses ranging from Brexit, the pandemic, rising energy costs have thinned out the nation’s finances.

Walking Back Tax Cuts

The public backlash, crash of the British pound, FTSE index sell-off to March lows, rebuke from the IMF, and a sell-off in U.K. bonds forcing the Bank of England (BoE) to ‘blink’ and launch a temporary quantitative easing (QE) program prompted the new U.K. government to drop its previously announced income tax cuts on high earners. The finance minister Kwasi Kwarteng announced, “It is clear that the abolition of the 45p tax rate has become a distraction from our overriding mission to tackle the challenges facing our economy. As a result, I’m announcing we are not proceeding with the abolition of the 45p tax rate. We get it, and we have listened.” This caused the pound sterling to rebound and bond yields to fall and stabilize.

Why Did the BoE Blink?

The Bank of England was the first central bank to ‘blink’ and intervene in its bond market to combat spiking yields. However, the reasons for the intervention are not what most people think. British government bonds also known as gilts saw yields spiking as investors dumped the bonds. British pension funds hold nearly $1.7 trillion in assets. These funds often utilize derivatives to both hedge interest rate risk and optimize gains on certain trading strategies. Derivatives utilize massive leverage. The spike in gilt yields caused some massive derivative trades to collapse sparking margin calls on U.K. pension funds which could have triggered a U.K. version of a Lehman Brothers meltdown moment. The BoE intervened by buying up bonds to push down long-term yields by over 100 basis points and took down U.S. 10-year treasury yields as well.

Not Likely in the U.S.

The Fed has taken a very hawkish stance implying they would not stop rate hikes until inflation fell under its stated target of 2% regardless of a U.S. recession. While it’s not clear if that means maintaining an aggressive rate cut strategy or pulling back the magnitude of the rate hikes back under 75-basis points. The latter would like to put in a floor for the equity markets. Many are speculating that the intervention by the BoE could set a precedent for the world’s central banks including the U.S. Federal Reserve to blink amid spiking bond yields. The BoE intervention temporarily stabilized the equity markets as the odds of a 50-basis point rate hike in the November FOMC meeting improved to 43.5%. This sparked debate whether our own Fed would blink if a similar scenario occurred. However, the 75-basis point rate hike odds rebound back to 81% by the end of the week as equity markets sold off towards yearly lows on the Oct. 7 jobs report came in stronger than expected at 288,000 versus 275,000 expectations. This still indicates a hot labor market as the unemployment rate stands at 3.5% down from 3.7%. This means the Fed will have to stay aggressive on inflation as the economy is still not slowing down fast enough.

Interest rates are nearing new highs which has pushed stocks to new lows. Now oil is looking higher as well. Time to take a technical take on the markets.

shutterstock.com – StockNews

So many markets are at critical areas on the charts. A quick walk through of each of these should help shed some insight into what price points to watch for bearish break-downs or bullish break-outs over the coming weeks. Interest rates will likely hold the key until after the next Fed meeting in early November.

The 10-year Treasury yield is fast approaching recent highs once again near the 4% level. An upside break-out would likely send stocks to new lows while a re-test of the 3.5% area would be bullish for equities.

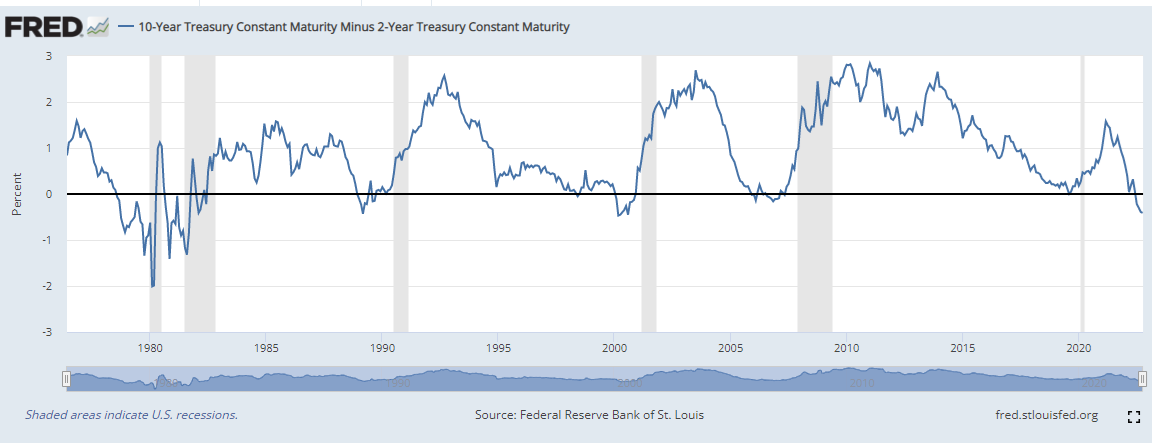

The 2-year Treasury yield is at a similar inflection point, albeit with a higher yield. A move past 4.5% would not be a welcome sight for stock traders. Note that the 2-10 is still deeply inverted, which is normally a recessionary sign.

The NASDAQ 100 (QQQ) is hovering right at major support near $270. Not yet oversold yet but definitely getting closer.

S&P 500 and Russell 2000 displaying identical patterns. Whether stocks hang on and bounce or breakdown and fall further remains to be seen.

Gold and oil are also at major inflection points on the charts, although oil getting a little overbought short-term.

Implied volatility in stocks (VXN and VIX) is nearing the recent highs once again, although not quite there yet. Nervousness abounds as stocks fall towards recent lows.

How this ultimately plays out is anyone’s guess. I prefer to stay hedged and nimble, which is the approach that has been working well recently in the POWR Options portfolio. The recent semiconductor pairs trade -bearish lower rated WOLF and bullish higher rated AVGO- was closed in one day for a 19% profit.

POWR Options

What To Do Next?

If you’re looking for the best options trades for today’s market, you should check out our latest presentation How to Trade Options with the POWR Ratings. Here we show you how to consistently find the top options trades, while minimizing risk.

If that appeals to you, and you want to learn more about this powerful new options strategy, then click below to get access to this timely investment presentation now:

SPY shares closed at $362.79 on Friday, down $-10.41 (-2.79%). Year-to-date, SPY has declined -22.73%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Tim Biggam

Tim spent 13 years as Chief Options Strategist at Man Securities in Chicago, 4 years as Lead Options Strategist at ThinkorSwim and 3 years as a Market Maker for First Options in Chicago. He makes regular appearances on Bloomberg TV and is a weekly contributor to the TD Ameritrade Network “Morning Trade Live”. His overriding passion is to make the complex world of options more understandable and therefore more useful to the everyday trader.

Tim is the editor of the POWR Options newsletter. Learn more about Tim’s background, along with links to his most recent articles.

In last week’s commentary, we discussed the importance of the mid-June lows for the S&P 500 (SPY) and the possibility of an undercut and then a rebound. In many ways, this is exactly what markets do -> frustrate the maximum amount of bulls and bears. Certainly, the bears were ebullient about this breakdown with many adding to shorts and puts, while many bulls probably capitulated. Now, we are more than 5% above these lows. Next on the docket is the September jobs report tomorrow and a CPI report next week. These will play a large role in determining the path and nature of this bear market rally. In today’s commentary, I want to discuss some lessons from the past 2 bear market rallies and how we are going to apply them to our portfolio. Read on below to find out more….

shutterstock.com – StockNews

(Please enjoy this updated version of my weekly commentary originally published October 6th, 2022 in the POWR Stocks Under $10 newsletter).

Over the last week, the S&P 500 (SPY) is up by 4.4%, although it was up more than 6% at some point, before some profit-taking into the September jobs report.

It’s been a broad-based rally with strength across the board. Not surprisingly, we are seeing the biggest moves in the most oversold sectors like metals, energy, and tech.

Why is the Market Rallying?

From a technical perspective, we have a double bottom, especially with the drop below support and quick recovery. As long as this double bottom is intact, we have to respect the bull case.

To be clear, this is a bounce. But given the strong technical setup and bearish sentiment, my gut tells me this is likely to turn into a bear market rally that lasts for weeks and tests important resistance levels on the upside.

And if the fundamentals evolve in a supportive manner, then the bear market rally can even turn into something more meaningful. Every bull market started as a bear market rally, but not every (or most) bear market rally turn into bull markets.

Again, I think we are at the same precipice. If this is a normal, cyclical recession, then buying at these levels is likely to be rewarded in six to twelve months’ time.

If this is more in the vein of 2002 or 2008, then stocks are probably in the middle innings of their descent. In that case, the S&P 500 is likely to break 3,000 and we could see the retracement of the entire rally that began in March 2020.

Earnings and Rates

So far, all of the market weakness can be attributed to inflation and higher rates pushing down multiples for the S&P 500 (SPY).That’s because earnings growth has managed to remain positive despite the numerous headwinds faced by the economy and increasing concerns of an imminent recession.

So, the Q3 earnings season is just beginning and will play a major role in determining whether the bounce can turn into a rally, or whether it will quickly roll over. Just to set the stage, analysts are forecasting 2.9% earnings growth for Q3.

This is a drastic cut from expectations of nearly 10% earnings growth in Q3 a couple of months ago. It’s largely a result of companies’ warnings and guidance lower given the numerous headwinds.

Objectively, it’s not bad. But, it’s an indication that markets are expecting some pain which creates the potential for an upside surprise. And, this is exactly what happened in Q2 and was one of the factors behind the 18% rally for the S&P 500 between mid-June and early August.

On the rate front, there are some subtle developments that are conflicting with the last CPI report which sent short-term and long-term rates, shooting up to new highs.

In essence, we are seeing real estate prices decline, used car prices decline, and freight prices drop, in addition to the relief from lower energy prices.

Just like the cyclical vs secular recession debate has major implications, the inflation debate is equally compelling and interesting. There is one camp that sees inflation as an onion.

Just because the outside is fine, doesn’t mean that the core isn’t rotten. Essentially that core inflation is its own beast with only a mild connection to more volatile, cyclical factors.

The other camp sees core inflation as simply lagging behind more real-time indicators like those mentioned above. This camp believes that inflation has already peaked and that core CPI is simply a lagging indicator.

Last 2 Bear Market Rallies

Going back and studying the last 2 bear market rallies in 2022 is quite instructive.

Both saw double-digit gains in a short period of time and massive gains in the most oversold stocks and sectors. Certain sectors and stocks even were able to make new highs.

Basically, we have to take advantage of these rallies while being mindful of the endgame, especially if the fundamentals are deteriorating.

These bear market rallies can help us identify which stocks and sectors are benefitting from secular trends vs cyclical trends. And that can really help fuel outperformance during the next bull market.

For instance, I’m noticing incredible strength and accumulation in energy, lithium, and alternative energy stocks. On the other hand, oversold stocks can be bought for trade and just trade as these are liable to roll over and make new lows.

What To Do Next?

If you’d like to see more top stocks under $10, then you should check out our free special report:

What gives these stocks the right stuff to become big winners, even in the brutal 2022 stock market?

First, because they are all low priced companies with the most upside potential in today’s volatile markets.

But even more important, is that they are all top Buy rated stocks according to our coveted POWR Ratings system and they excel in key areas of growth, sentiment and momentum.

Click below now to see these 3 exciting stocks which could double or more in the year ahead.

SPY shares closed at $362.79 on Friday, down $-10.41 (-2.79%). Year-to-date, SPY has declined -22.73%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Jaimini Desai

Jaimini Desai has been a financial writer and reporter for nearly a decade. His goal is to help readers identify risks and opportunities in the markets. He is the Chief Growth Strategist for StockNews.com and the editor of the POWR Growth and POWR Stocks Under $10 newsletters. Learn more about Jaimini’s background, along with links to his most recent articles.

Lets talk about the #1 mistake made by investors during a bear market. Better yet, let’s solve this problem by explaining how easy it is to actually make trading profits during a bear market. Remember the definition of insanity is doing the same thing expecting a different result. So lets try something new to get you on the right side of the stock market (SPY) action. Read on below for more.

shutterstock.com – StockNews

I just read another email from a StockNews customer who says this bearish market has pushed them to the sidelines. And they will “Wait and See” to determine what to do next.

Sorry friends…this is just investing suicide.

There is no other way to say it. And yet, this is the most common response by investors when times get tough like it has in 2022.

I want to point out the insanity of this approach in the hopes to get people on a more successful investing path.

The Danger of “Wait and See”

On the surface, this seems so logical. To appreciate that the current market conditions are rough. And thus you will wait and see what happens next to then plot your course forward.

Now the reality check…

“There is ALWAYS a bull market somewhere”

This not just an amusing expression…but a statement of fact.

There is always something going up even in the darkest of times. And thus there is NEVER a good reason to be out of the market.

The key is aligning your portfolio with the prevailing trends. And since we are in the midst of a long term bear market, then what is going up are investments that profit as the market goes down like inverse ETFs and put options.

Inverse ETFs are just one of the tools I have used in my Reitmeister Total Return service to produce a +4.65% gain as the S&P 500 (SPY) dove over 15% to new lows (8/15/22 to 9/30/22).

Then you have Tim Biggam taking advantage of a string of winning put trades in his POWR Options service. Customers of this service have enjoyed a stunning +65.44% gain since the service opened in November 2021.

By the way you can start a 30 day trial to the above services to enjoy these winning trades. We will discuss that in a minute, but first I need to share one more key point which is…

Inflation is Destroying Your Cash Accounts

Right now cash is trash.

The math is abundantly clear. Inflation is raging at 8% and yet your bank is paying you a small fraction of that which means that every minute your money is in cash…you are losing out to inflation.

So the “Wait and See” approach to move to cash is insuring you a hefty loss as inflation is such a silent killer of wealth. Thus, cash it is not as safe as you imagined.

This alone should have you curious to see if there is a better way in which to invest. Like the approaches discussed in the previous section in the Reitmeister Total Return and POWR Options service.

What to Do Next?

Start your 30 day trial to POWR Platinum…this is the bundle of all of our active trading services.

Not only does it include access to the winning trades in my Reitmeister Total Return service, or Tim Biggam’s POWR Options…but also these additional popular services:

POWR Growth– Jaimini Desai harnesses the Top 10 Growth Stocks strategy and its +49.10% average annual return.

POWR Trends– In depth commentaries and top picks from the most exciting growth trends from EVs to Space Exploration to Internet of Things to Genomics and more.

POWR Value– Steve Reitmeister hand picks the best value stocks by utilizing the Top 10 Value Stocks strategy with +37.67% average annual returns.

POWR Ratings Premium – Giving full access to our coveted POWR Ratings for over 5,300 stocks and 2,000 ETFs.

POWR Stocks Under $10 – Based on our most powerful stock picking strategy, with market shattering +59.43% average annual returns. And shockingly good results during bear markets too!

AND coming soon….

In just 2 weeks we’re adding a brand new service called POWR Breakouts, that utilizes chart patterns in combination with the fundamental strength of our POWR Ratings to find the stocks most likely to breakout in any market. Truly a best of both worlds approach to find the most timely stocks.

There really is something here for every investor and EVERY market condition. Without doubt, this is the best way to discover which of our services is right for you, so after your trial you can just keep what suits you most.

And the cost?

Just $1 for the next 30 days.

During your all access trial you’ll get all the current picks, every new trade—including 2 exciting picks coming Monday morning—plus in-depth analysis & market commentary from our experts to put you on the right side of the market action.

I’m supremely confident that with all these market beating services at your disposal you’ll achieve significant outperformance in 2022 and want to remain a member for a long long time.

But if I’m wrong you can cancel at any time and be fully protected by our industry-leading performance guarantee. That means we’ll gladly refund every penny you paid for your subscription if we fail to help you beat the market.

So don’t delay, click the link below to get started now:

SPY shares fell $0.18 (-0.05%) in after-hours trading Friday. Year-to-date, SPY has declined -22.73%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

Bounces will pop up here and there as they did this past week…but don’t think for a second that this bear market is over because the Fed is not yet done with their mission to tamp down the flames of recession. When all is said and done we will have a recession and the S&P 500 (SPY) will be much lower. This leads to the key question: Where is bottom? Investing veteran Steve Reitmeister shares his views in his updated market outlook below.

shutterstock.com – StockNews

September was downright brutal ending with a crescendo of selling that sent stocks to the lowest levels of this bear market. Not surprisingly this created ripe conditions for a 6% relief rally for the S&P 500 (SPY) to kick off October…how quickly that party ended.

Thursday investors took a modest step back. But then after hours we received word of a terrible earnings report from Advanced Micro Devices (AMD).

These are not just AMD problems. Unfortunately it speaks to a wide spread slow down in computer products along with supply chain issues that will no doubt harm many in the sector.

Couple the above with a Friday jobs report that was just a tad too good which investors know will embolden the Fed to keep raising rates aggressively. This increases the odds of a hard landing for the economy down the road pushing more investors to hit the sell button.

Long story short…welcome back to the bear market. Get the rest of the investment story and trading plan in the fresh commentary below…

Market Commentary

Right now investors are in a can’t win situation as good news sparks stock sell off as readily as bad news. Yes, that is quite odd but it aligns with the general premise of…

Don’t Fight the Fed!

When the Fed was lowering rates, as they did for nearly 12 years straight, we all used this saying as a battle cry to stay bullish. That is because lower rates are a catalyst for economic growth, which is great fuel for stock prices.

Now we have the opposite.

A Fed that is dead set on extinguishing the flames of inflation with the most aggressive rate hiking policy in history. Meaning the pace at which they are raising rates is unprecedented.

The reason for this fast pace is not just the high rate of inflation. Sadly, the Fed was asleep at the wheel calling early inflation “transitory” and thus not something to be burdened with.

When the Fed finally woke up to the stickiness of this inflation, then their only recourse was to aggressively raise rates. The goal is to slow down the economy, which by extension will tame inflation.

Or let me put it another way. Recession by its very nature leads to less demand. Everyone who ever took Econ 101 knows this will lower prices thus reigning in inflation.

Putting these pieces together means the Fed is actively trying to create a recession. And yes, recessions and bear markets go together like peanut butter and jelly.

This explains why “Don’t Fight the Fed!” now translates as “watch out below!” for stock prices.

And this also explains why even good news on the economic front is greeted with selling. The most recent instance of that was the October Employment Report on Friday showing robust job gains that only gives the Fed a green light to continue to aggressively raise rates.

The only real questions are how deep of a recession will we have and thus how far down stock prices should go?

Those betting on a soft landing would be right to think the recent lows at 3,585 for the S&P 500 (SPY) would seem like a fair bottom for stocks as it represents a nearly 26% decline from the all time highs.

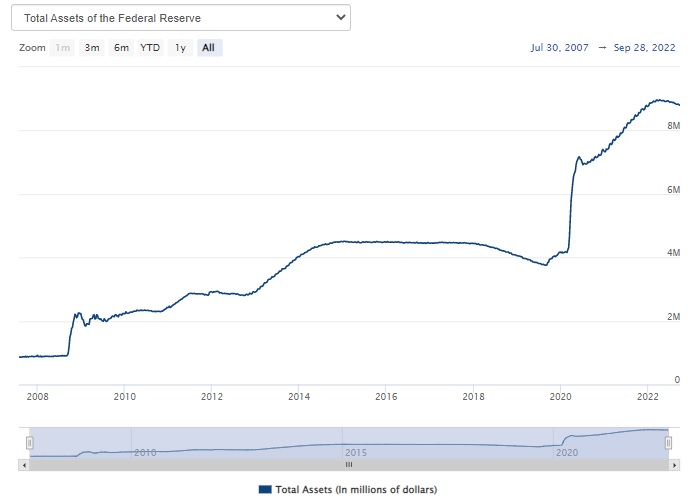

Unfortunately I have yet to talk to anyone calling for a soft bottom. That’s because with the Fed slow to react to inflation, that they have to be more aggressive in the steps taken. Not just the pace they are raising rates, but also the unwinding of Quantitative Easing. (aka Quantitative Tightening).

Most investors forgot about this one.

Now they are unwinding that massive balance sheet $90 billion dollars a month. Here again, lets go back to our Econ 101.

If the Fed sells these bonds, then it increases the supply of bonds. If demand is the same as the past, then it will naturally lead to higher rates to attractive investors to buy the bonds. This is yet another form of putting the brakes on the economy.

Back to the point…where is all of this heading?

Unfortunately the smart money is on much higher rates and a much weaker economy and thus much lower stock prices.

Let’s not forget that the average bear market endures a 34% decline in stock prices. That would equate to 3,180 this time around.

But also the average bear market comes hand in hand with a Fed that was LOWERING rates to help the economy recover. Now you have the exact opposite. So it likely points to a weaker economy and lower lows.

Second, when you have low rates on bonds, it makes the stock market look like a more attractive investment by comparison. That is NOT true when rates are going higher.

Imagine Treasury yields of 5-7%. That will be the safe money investment choice. Likely corporate bonds paying 2-3% above that.

It will be very tempting to take that safer route to investment returns. Especially if you believe that rates will come down in the future only padding the return on these bond investments.

This is another way of saying that demand for stocks will not be as strong at the bottom of this cycle as the typical recession and bear market. And thus it is not crazy to contemplate that stocks will need to fall further to get more investors off the sidelines.

That is why you need to contemplate that 40% drop is not out of the question. That translates to 2,891 for the S&P 500 (SPY).

No one rings a bell at the top or the bottom. So timing this perfectly is not in the cards.

However, it does say that right now the wise choice is to bet on stocks going lower…much lower.

What To Do Next?

Discover my special portfolio with 9 simple trades to help you generate gains as the market descends further into bear market territory.

This plan has been working wonders since it went into place mid August generating a +4.65% gain as the S&P 500 (SPY) tanked over 15%.

If you have been successfully navigating the investment waters in 2022, then please feel free to ignore.

However, if the bearish argument shared above does make you curious as to what happens next…then do consider getting my updated “Bear Market Game Plan” that includes specifics on the 9 unique positions in my timely and profitable portfolio.

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”) CEO, Stock News Network and Editor, Reitmeister Total Return

SPY shares fell $0.17 (-0.05%) in after-hours trading Friday. Year-to-date, SPY has declined -22.73%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

First Citizens, like its entire industry, has seen net interest income and margins expand as interest rates increase. That typically occurs in an environment of rising rates.

Regional banks can fly beneath the radar as investment opportunities. Unless you live in an area where one of these banks operates, they aren’t obvious candidates that fall under the famous Peter Lynch “buy what you know” category of investment ideas. But a screener, such as the one you’ll find on MarketBeat.com, can help you identify some not immediately obvious names.

First Citizens is a North Carolina-based regional bank that operates 529 branches and offices in 19 states and Washington, DC. It has a market capitalization of $13.48 billion, making it the largest company within the southeast/regional bank sub-industry.

The stock has been outperforming not only the financial sector as a whole, but also its regional banking peers. Shares are up 5.78% in the past month and 25.47% in the past three months.

The stock staged a cup-with-handle breakout on September 12, but chopped along with the broader market volatility. It’s been unable to sustain the breakout, and closed below its 50-day moving average the week ended September 30, but regained that price line. It’s currently trading above its 10- and 21-day moving averages.

The company reports third-quarter earnings on October 27, with Wall Street eyeing net income of $19.77 per share on revenue of $1.02 billion. Those would be increases of 62% and 110%, respectively.

For the full year, analysts expect the company to earn $69.33 per share, up 29% over 2021. Next year, that’s seen rising an additional 31% to $91.05 per share.

Other banks, of course, will benefit from a rising-rate environment, and some are already showing share-price appreciation reflecting strong fundamentals.

Currently, Pennsylvania-based Fulton Financial (NASDAQ: FULT) is also outperforming financials as a whole. The stock is up 5.94% in the past month and 15.43% in the past three months.

Fulton has a market capitalization of $2.635 billion, putting it either the higher end of the small-cap categorization or lower end of mid-cap.

It’s currently forming a cup-with-handle pattern, with a potential buy point above $17.67. It’s been languishing below that point since mid-August.

Fulton is due to report its third quarter on October 18, after the closing bell. Analysts expect the company to earn $0.44 per share on revenue of $198.64 million. Both would be lower than the year-earlier results, but often, positive guidance can offset declines in revenue or earnings, and send the stock higher.

Fulton is categorized as a super-regional bank, meaning it has significant operations in several states.

Larger, more familiar super-regional banks include PNC (NYSE: PNC). This Pittsburgh-based bank has a large presence in the northeast, with more than 2,600 branches. The stock has been in a correction since January, but so far, has been finding a floor between $146 and $147.

Another large-cap super-retional is U.S. Bancorp (NYSE: USB), which is down 24.37% year-to-date. It’s also been correcting since January. Unlike PNC, it’s not clear that it’s found its price floor yet.

It’s not always the largest, most familiar names that offer the best opportunity at any given time. While it’s true that the traditional advice to “buy low, sell high” is correct in any market cycle, it’s not necessarily best to identify the most beaten-down stocks, when a stock that’s holding up better than the broader market may present more opportunity.

Mid-caps typically are those with a market capitalization between $2 and $10 billion. They often have fewer shares in float than you’ll find with larger stocks. These characteristics make mid-caps somewhat more volatile and riskier than large caps, at least in terms of broad asset classes.

Digi International advanced 2.34% in nearly triple average turnover Wednesday, tacking on gains to its recent outperformance, which includes gains of:

1 month: +16.19%

3 months: +58.88

Year-to-date: +53.32

The Minnesota-based company specializes in the Internet of Things, which involves connecting products, apps, and services through various wireless devices. Those devices can include factory and industrial settings; household applications, such as appliances and security systems; and automotive gear, among many other examples.

Digi International gapped up 15.66% on August 4 following the company’s fiscal third-quarter report, in which it topped earnings and revenue views, as you can see using MarketBeat data on the stock.

Earnings growth accelerated in the past two quarters, from 13% to 80%, while revenue growth accelerated from 8% to 31% in the past three quarters. Its three-year annual earnings growth rate is 34%, while revenue grew 12%.

That level of fundamental strength is driving the stock price increases. An increase in fourth-quarter guidance also helps.

On a technical basis, the stock is in a buy range, but continue to be cognizant of broad-market volatility that could pull it, and any stock, sharply lower.

Lamb Weston is in the decidedly unglamorous business of producing, packaging, and distributing frozen potato products to restaurants, as well as via private-label brands for consumers. But potatoes are apparently in high demand: The stock advanced 4.19% Monday following a better-than-expected fiscal first quarter.

Earnings of $0.75 per share marked a 317% increase over the year-ago quarter. MarketBeat earnings data for Lamb Weston show the company trounced views by $0.26 per share. Revenue was slightly disappointing, coming in at $1.13 billion, versus analyst expectations of $1.14 billion. Still, that was a year-over-year increase of 14%.

Lamb Weston shares built upon Wednesday’s gains, rallying in Thursday morning trading. Analysts see the company growing earnings by 36% for the full year, which is fiscal 2023. Next year, that’s expected to rise another 32%, to $3.72. That kind of potential is attracting institutional buyers, MarketBeat data show.

Another food-related mid-cap flashing gains for the week is restaurant franchisor Wingstop.

There was no specific company news, but the stock has been the subject of recent positive attention from Wall Street, according to MarketBeat analyst data for the stock. In the past month, Stephens initiated coverage with an overweight rating and Wedbush boosted its price target with a rating of outperform

As noted previously by MarketBeat, Wingstop is among food-related stocks that have been capitalizing on consumers’ willingness to continue purchasing food, including dining out, even as they cut back on other discretionary items.

The consensus rating is “moderate buy,” with a price target of $138.65, a potential upside of 4.21%.

The company is slated to report its fiscal third quarter on October 26, before the opening bell. Analysts expect earnings of $0.35 per share on revenue of $89.30 million. Those would be increases on both the top- and bottom lines.

Earnings data compiled by MarketBeat show that Wingstop beat earnings views in the most recent quarter, although revenue lagged. That didn’t stop investors from piling in, as margins came in well above views.

For the past two years, since the covid pandemic hit in late-February 2020, the cruise industry has taken one punch after another. And, while the situation has improved from the extended period when cruises were not allowed to sail from United States ports, that does not mean that it’s back to 2019 for Royal Caribbean International (RCL) , Carnival Cruise Line (CCL) , and Norwegian Cruise Line (NCLH) .

The industry has done a remarkable job bringing operations back to near-normal. All three cruise lines not only have put all their ships back in service, they’re also still moving forward with plans for new ships and other investments including improvements to private islands, and developing new ports.

That being said, Carnival just reported its second-quarter earnings and the market did not like the numbers at all. Shares of all three cruise lines were down double digits on Sept. 30, but traders clearly missed that aside from rising costs and a loss (both of which were expected) the cruise line largely delivered good news.

Image source: Shutterstock

Carnival Did Well in Areas it Controls

Carnival reported a GAAP net loss of $770 million for the quarter. That was driven by higher costs with the company specifically citing advertising expenses and having some of its fleet unavailable to produce revenue.

While the company’s year-to-date adjusted cruise costs excluding fuel per ALBD during 2022 has benefited from the sale of smaller-less efficient ships and the delivery of larger-more efficient ships, this benefit is offset by a portion of its fleet being in pause status for part of the year, restart related expenses, an increase in the number of dry dock days, the cost of maintaining enhanced health and safety protocols, inflation and supply chain disruptions. The company anticipates that many of these costs and expenses will end in 2022.

If you’re investing in any cruise line you have to do so on a very long-term basis. That makes profitability less of a concern than the company building back its business and Carnival showed some very positive signs in that direction.

Revenue increased by nearly 80% in the third quarter of 2022 compared to second quarter 2022, reflecting continued sequential improvement.

Onboard and other revenue per PCD for the third quarter of 2022 increased significantly compared to a strong 2019

Total customer deposits were $4.8 billion as of August 31, 2022, approaching the $4.9 billion as of August 31, 2019, which was a record third quarter.

New bookings during the third quarter of 2022 primarily offset the historical third quarter seasonal decline in customer deposits ($0.3 billion decline in the third quarter of 2022 compared to $1.1 billion decline for the same period in 2019).

Carnival (and likely all the cruise lines) is being hurt by prices generally being depressed and some passengers paying for their trips using future cruise credits from cruises canceled during the pandemic. That’s not really what matters though. Carnival has been increasing passenger loads and getting people back on its ships.

“Since announcing the relaxation of our protocols last month, we have seen a meaningful improvement in booking volumes and are now running considerably ahead of strong 2019 levels,” Carnival CEO Josh Weinstein said. “We expect to further capitalize on this momentum with renewed efforts to generate demand. We are focused on delivering significant revenue growth over the long-term while taking advantage of near-term tactics to quickly capture price and bookings in the interim.”

Basically, cruise prices are cheap right now because it’s more important to get customers back on board than it is to maintain pricing integrity. That’s a tactic that could hurt long-term pricing, but the cruise industry is less vulnerable than other vacation options because there have always been large pricing variations based on the calendar and the age of the ship being booked.

It’s a Long Voyage for Cruise Lines

Carnival was trading at its 52-week low after it reported. That’s a pretty major overreaction given that the cruise industry was barely operating in the fall of 2021.

Yes, the industry has a long way to go. All three major cruise lines took on billions of dollars of debt during the pandemic. Refinancing that debt in an environment with higher interest rates is a challenge, but it’s one Carnival (and its rivals) have been meeting.

That has come with some shareholder dilution. Carnival sold $1.15 billion in new stock during the quarter, but the company has over $7.4 billion in liquidity. Weinstein is optimistic (he has to be, that’s part of his job) about the future.

“During our third quarter, our business continued its positive trajectory, achieving over $300 million of adjusted EBITDA and reaching nearly 90% occupancy on our August sailings. We are continuing to close the gap to 2019 as we progress through the year, building occupancy on higher capacity and lower unit costs,” he said.

Usually it’s easy to dismiss a CEO making upbeat comments after posting a loss, but in this case, Carnival has basically followed the recovery path it laid out once it returned to sailing. Both Royal Caribbean and Norwegian have followed similar paths and while meaningful shareholder returns may take time, these are strong companies built for the long-term that made a lot of money before the pandemic and should do so again.