CenturyLink merged with Qwest to become the third-largest telecommunications company in the U.S. in 2010. The Company continued to gobble up technology companies like Savvis, a cloud infrastructure company in 2012 and broadband provider Level 3 Communications in 2017. The Company changed its name from CenturyLink to Lumen Technologies (NYSE: LUMN) on Sept. 18, 2020. Legacy copper-based services would continue under CenturyLink and fiber-based products and services would service under the Quantum Fiber brand. The Company provides cloud, IT, voice, TV, infrastructure, internet, and broadband services to enterprise, small business, and residential customers. It’s Quantum Fiber is the growth engine as it expands in over 30 U.S. cities and metro areas expanding access to millions of new consumers. Value investors may be interested in its assets which include over 400,000 route fiber miles serving customers in over 60 countries. Google Fiber (NASDAQ: GOOG) has deployed 50,000 miles of fiber in 60 markets at a cost of over $14 billion, twice the market cap of Lumen stock. The cheap price-to-book ratio of 0.5 makes it an asset play if it continues to sell off more pieces of the whole, gets acquired, or goes private. Can the new CEO effectively change its downward trajectory?

MarketBeat.com – MarketBeat

Raising Cash and Fending Off Competition

The Company has been shedding some of its businesses to pay down debt which will be reduced to $20.4 billion after paying it tax bill between $900 million to $1 billion for its 20-state ILEC sales of its LATAM business to Apollo for $7.5 billion. The Board of Directors made the decision to eliminate the $1.00 annual dividend and implement a stock buyback program up to $1.5 billion with a two-year time. The Company expects an inflation impact for the full-year next year. Further focus on the digitization of front and back office functions is a top priority. Lumen faces competition from the big broadband providers like AT&T (NYSE: T), Verizon (NYSE: VZ), and Comcast (NASDAQ: CMCSA) as well as cloud service and applications providers including Amazon Web Services (NASDAQ: AMZN), Microsoft Azure (NASDAQ: MSFT), and Google Cloud (NASDAQ: GOOG).

Top and Bottom Line Downward Trajectories

Lumen reported its Q3 2022 earnings on Nov. 2, 2022. The Company reported earnings-per-share (EPS) of $0.14 missing consensus analyst estimates for $0.35 by (-$0.21). Net income was $578 million versus $544 million in the year-ago period. Special items of (-$527 million) and (-$31 million) dropped EPS from $0.57 to $0.14. Revenues continued to drop (-10.2%) year-over-year (YoY) to $4.39 billion missing analyst estimates of $4.41 billion. Adjusted EBITDA fell to $1.688 billion compared to $2.078 billion in the year ago period. The Company completed the $2.7 billion divestiture of its Latin American business Stonepeak. The Company generated $620 million in free cash flow. Lumen completed its $7.5 billion divestiture of its 20-state ILEC business to Apollo on Oct. 3, 2022. The Company eliminated its stock dividend and authorized a two-year and up to $1.5 billion share buyback program. Entered into an exclusive arrangement to sell its EMEA business to Colt Technology for $1.8 billion. Incoming Lumen President and CEO Kate Johnson who commented, “The opportunity for Lumen is significant, and I am eager to leverage today’s announcements and the adjusted capital allocation priorities to drive profitable growth and shareholder value. Jeff, the Lumen Board, and I are fully aligned on these decisions. I look forward to hitting the ground running on November 7.” The Company expects adjusted EBITDA in the range of $6.9 billion to $7.1 billion for fiscal full-year 2022.

Department of Defense Contract

On Nov. 1, 2022, Lumen announced it won a $1.5 billion cap 10-year defense contract from the Defense Information Systems Agency. Lumen will provide essential network transport and communications services to enable the U.S. Department of Defense (DOD) to recognizes its national security objectives in the Asia Pacific region and Alaska. The contract services range from internet, ethernet, and wavelength to protect America’s interests. Lumen’s dark fiber has been used exclusively for government contract services and is posted under the CenturyLink segment.

Breakdown After a Breakdown

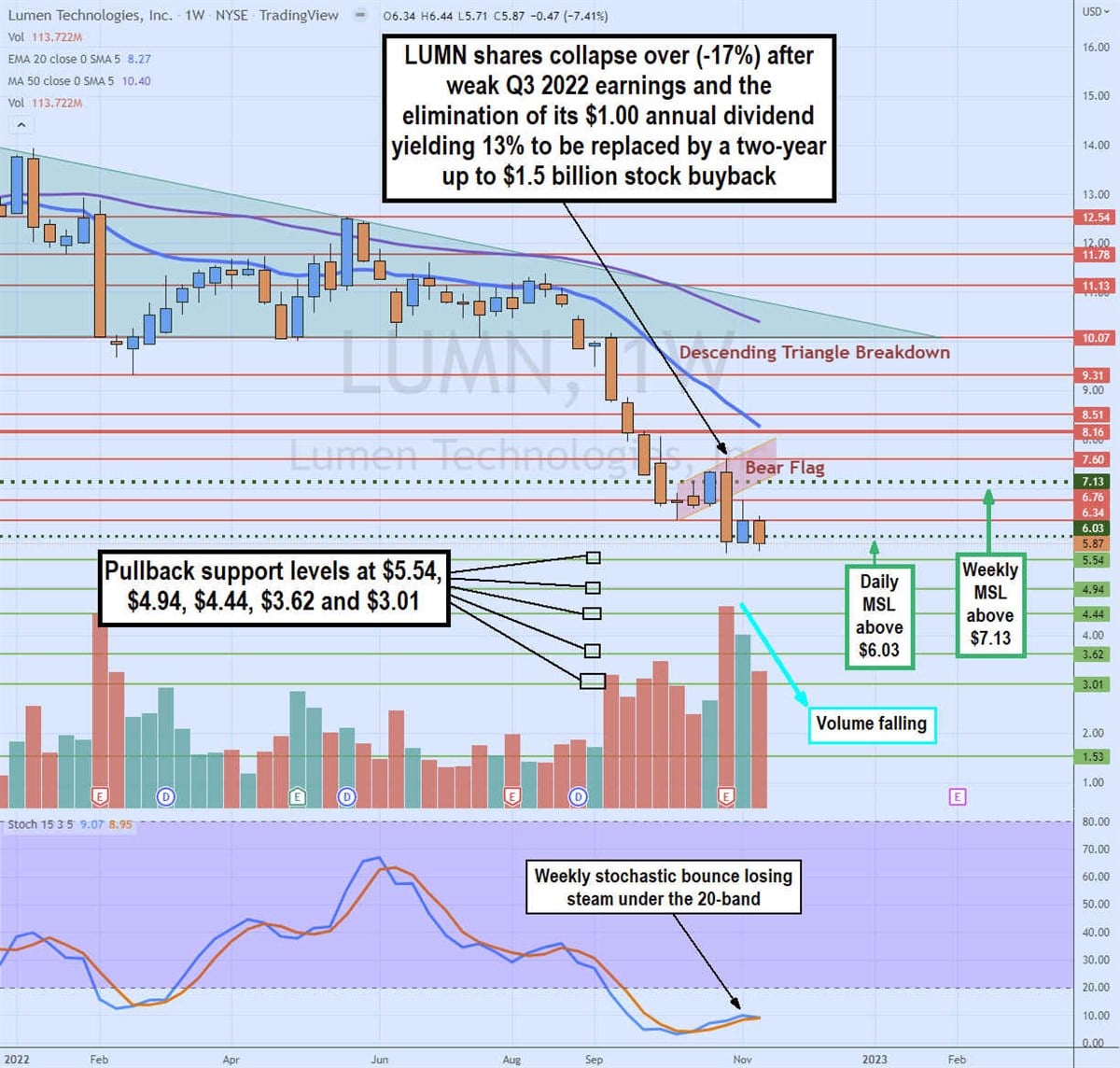

The LUMN weekly candlestick chart illustrates the descending triangle breakdown occurring in August 2022 as each preceding bounce was lower until the $10.07 support finally gave in. Shares managed to fall to a swing low of $6.34 before triggering the weekly market structure low (MSL) for a rally back up to $7.60 in October to Nov. 1, 2022. On Nov. 2, 2022, LUMN shares collapsed over (-17%) on in reaction to its Q3 2022 earnings report and dividend elimination triggering the weekly bear flag breakdown. The weekly 20-period exponential moving average (EMA) resistance hasn’t tested yet as it continues to fall to $8.27 followed by the 50-period MA at $10.40. The daily MSL trigger sets at $6.03 after making a new swing low of $5.68. Pullback support levels sit at the $5.68 swing low to $5.54, $4.94, $4.44, $3.62, and $3.01.

Alphabet is a part of the Entrepreneur Index, which tracks some of the largest publicly traded companies founded and run by entrepreneurs.

We are approaching that time of year when the stock market gets into a holiday mood triggering a Santa Claus rally into the new year. With the S&P 500 index (NYSEARCA: SPY) trading down (-17%) and Nasdaq (NASDAQ: QQQ) down a naughty (-29%) for the year, investors are left to ponder if markets have the wherewithal to stage a Santy Claus Rally. The biggest concern for the markets is rising interest rates. The U.S. Federal Reserve will have its final meeting for the year concluding on Dec. 14, 2022. They will determine the final interest rate hike and provide commentary and a question-and-answering session detailing their thoughts heading into next year. Leading up to the rate decision, there are two crucial economic reports and a slew of other factors to be aware of. Here’s what needs to happen for the Santa Claus rally to occur.

MarketBeat.com – MarketBeat

The Fed: Grinch or Santa?

Will the U.S. Federal Reserve (Fed) be a hero or villain in its final Federal Open Market Committee (FOMC) meeting of the year on Dec. 14, 2022? The October CPI report indicated that inflation was falling as headline CPI came in at 7.7% versus the 7.9% expectations. This sent markets skyrocketing higher as Wall Street figured that would be enough for the Fed to ease up on the gas pedal and slow down its rate hikes. The Fed confirmed that it is possible to slow down the rate hikes but they could go on for longer than expected. They would rather overshoot on the rate hikes and then implement rate cuts than undershoot and have inflation rise later. Markets are already expecting a slowdown to 0.25 to 0.50 rate hikes, not 0.75, to end the year at a target rate of 4% to 4.5% by year’s end. The language of the decision is also important as the market expects the Fed to even go so far as to pause interest rate hikes in early 2023. This has caused the SPY and QQQs to rally ahead of time into December. The next two key economic reports are scheduled ahead of the final FOMC meeting.

Jobs Report

The first of the two critical economic reports remaining is the U.S. Bureau of Labor Statistics (BLS) are the Employment Situation Report (aka Jobs Report) on Dec. 2, 2022. Incidentally, the October jobs report actually came in stronger at 263,000 than the 205,000 expect which indicates a still strong labor market, but unemployment ticked higher to 3.7%. The rate of job growth actually slowed down to the lowest in two years. This still should have sent markets lower, but they actually moved up on the report. The November jobs report could actually come in below expectations with the high profile lay-offs from Twitter of over 3,500 jobs, Meta Platforms (NASDAQ: META) of over 11,000 workers, and nearly 10,000 workers at Amazon (NASDAQ: AMZN), Cisco Systems (NASDAQ: CSCO) of 4,000 workers, Lyft (NASDAQ: LYFT) of 700 workers, and a hiring freeze from Disney (NYSE: DIS).

CPI Report

The most important economic report ahead of the FOMC is the Consumer Price Index (CPI) report on Dec. 13, 2022, at 8:30 am EST, the day before the FOMC rate decision. This is the inflation gauge. The last report for October 2022 surprised the markets by coming in at 7.7% versus 7.9% expectations indicating the lowest inflation since January 2022. This was the report that prompted the rally heading into December. The next CPI report which will be a reading for the prior month November is expected to come in at 7.6%. That’s the line in the sand. If the CPI comes in under 7.6% then markets should rally higher. The magnitude of the rally depends on how far below 7.6% the number actually comes in at. On the flipside, if the CPI comes in higher than 7.6%, then markets may likely sell-off unless there is dovish language in the report.

Sell the News?

There is one more caveat to be aware of. Since the markets are forward-thinking, it often likes to anticipate an event ahead of time resulting in the opposite effect afterward. This is often coined as “Buy the Rumor, Sell the News”. If the markets expect the Fed to slow down its rate hikes due to falling inflation, as it does now, then markets may actually rally ahead of time into the FOMC meeting. If the market rallies too hard ahead of the rate decision, then it may actually sell off on the rate decision regardless. It’s prudent to give it until the next day’s reaction to gauge if the market will follow through higher. Since the Fed decision is in the middle of the month, it still leaves enough time for a Santa Claus rally to occur since it usually takes place near the end of the month and year. It’s prudent to have a shopping list of stocks ready in the event it takes place this year.

There are preps all around for the holiday season. Consumers eye discounts, and retail stores increase their in-store workforce. With inflation finally showing signs of slowing down and consumer demand remaining robust, it could be wise to pick up fundamentally strong retail stocks Walmart (WMT), Dollar General (DG), Dillard’s (DDS), Torrid Holdings (CURV), and J.Jill (JILL) to capitalize on the holiday retail sales boom. Continue reading….

shutterstock.com – StockNews

The Fed has aggressively increased interest rates this year to tame the multi-decade-high inflation. After six consecutive interest rate hikes, inflation seems to have started cooling off, as evidenced by October’s lower-than-expected Consumer Price Index (CPI).

Moreover, Federal Reserve Vice Chair Lael Brainard indicated that the central bank could soon slow down the pace of its interest rate increases. According to the National Retail Federation (NRF), holiday retail sales are expected to grow by 6% to 8% this year.

According to the U.S. Bureau of Economic Analysis, the personal consumption expenditure index shows an average increase of 6.2% year-over-year. NRF Chief Economist Jack Kleinhenz said, “Consumer demand really remains intact even though we are seeing rising interest rates, persistent inflation, (and) certainly political uncertainty.”

According to NRF and Prosper Insights & Analytics, holiday shoppers will spend an average of $832.84 on gifts and holiday items this year, in line with the 10-year average. Senior Director of Industry and Consumer Insights Katherine Cullen said, “Almost regardless of what’s going on in the economy, consumers want to celebrate holidays. They want to give gifts to their loved ones, and they want to make this time of year feel special.”

Several major retailers are directing the majority of their holiday hires to work on store floors this year as Americans shift from mainly shopping online to shopping in physical stores. According to the annual holiday purchase intentions survey from The NPD Group, the number of consumers planning to shop online for the holidays fell from 85% last year to 80% this year.

Amid this backdrop, investors could look to capitalize on the holiday retail sales boom by investing in the fundamentally strong retail stocks Walmart Inc. (WMT), Dollar General Corporation (DG), Dillard’s, Inc. (DDS), Torrid Holdings Inc. (CURV), and J.Jill, Inc. (JILL).

WMT engages in the operation of retail, wholesale, and other units worldwide. The company operates through three segments: Walmart U.S, Walmart International, and Sam’s Club.

Over the last three years, WMT’s dividend payouts have grown at a 1.9% CAGR. Its four-year average dividend yield is 1.72%, and its forward annual dividend of $2.24 per share translates to a 1.49% yield. It is expected to pay a quarterly dividend of $0.56 per share on January 3, 2023.

On October 31, 2022, Popable, a pop-up shop marketplace platform, and WMT announced a strategic partnership that allows small businesses to rent retail space in WMT stores across the country for short-term leasing.

The partnership is believed to help small business owners thrive, keeping excess inventory moving and creating greater built-in foot traffic. WMT will benefit from the utilization of its store space.

For the fiscal third quarter ended October 31, 2022, WMT’s total revenues increased 8.7% year-over-year to $152.81 billion. Its adjusted operating income increased 3.9% year-over-year to $6.02 billion. In addition, its adjusted EPS came in at $1.50, representing a 3.4% increase from the year-ago quarter.

WMT’s revenue for the quarter ending January 31, 2023, is expected to increase 4.2% year-over-year to $157.91 billion. Its EPS for the quarter ending April 30, 2023, is expected to grow 10.1% year-over-year to $1.43. The company has an impressive earnings surprise history, surpassing the consensus EPS estimates in three of the trailing four quarters. The stock has gained 3.8% year-to-date to close the last trading session at $150.23.

WMT’s POWR Ratings reflect solid prospects. The stock has an overall rating of A, equating to a Strong Buy in our proprietary rating system. The POWR Ratings assess stocks by 118 different factors, each with its own weighting.

Within the A-rated Grocery/Big Box Retailers industry, it is ranked #12 out of 39 stocks. The company has an A grade for Sentiment and a B for Stability and Quality.

Click here to see the additional POWR Ratings of WMT for Growth, Value, and Momentum.

DG is a discount retailer providing various merchandise products in the southern, southwestern, Midwestern, and eastern United States. It offers consumable products, packaged food, perishables, health and beauty products, pet supplies, pet food, and tobacco products. It also provides apparel and accessories.

Over the last three years, DG’s dividend payouts have grown at an 18.3% CAGR. Its four-year average dividend yield is 0.79%, and its forward annual dividend of $2.20 per share translates to a 0.85% yield. It paid a quarterly dividend of $0.55 per share on October 18, 2022.

On August 17, 2022, DG donated an additional $1 million to Feeding America to commemorate its one-year partnership anniversary. The donation intends to support community food banks and help provide increased access to nutritious food resources through Feeding America.

DG’s CEO, Todd Vasos, said, “We are proud to leverage our unique store footprint to help increase access to a variety of nutritious foods that help provide meals to individuals facing hunger.”

For the fiscal second quarter ended July 29, 2022, DG’s net sales increased 9% year-over-year to $9.43 billion. The company’s gross profit increased 11.3% from the year-ago period to $3.04 billion. Its net income increased 6.4% year-over-year to $678.03 million. Additionally, its EPS came in at $2.98, representing a 10.8% increase from the prior-year quarter.

Analysts expect DG’s EPS and revenue for the quarter ended October 31, 2022, to increase 21.9% and 10.7% year-over-year to $2.53 and $9.43 billion, respectively. The company has a commendable earnings surprise history, surpassing the consensus EPS estimates in three of the trailing four quarters. The stock has gained 9.3% year-to-date to close the last trading session at $257.70.

DG’s strong fundamentals are reflected in its POWR Ratings. The stock has an overall rating of B, which translates to a Buy in our proprietary rating system. In addition, it has a B grade for Stability. It is ranked #26 in the same industry.

We have also given DG grades for Growth, Value, Momentum, Sentiment, and Quality. Get all DG ratings here.

DDS operates retail department stores in the southeastern, southwestern, and midwestern areas of the United States. Its stores offer merchandise, fashion apparel, accessories, cosmetics, home furnishings, and other consumer goods.

Over the last three years, DDS’ dividend payouts have grown at a 21.1% CAGR. Its four-year average dividend yield is 2.14%, and its forward annual dividend of $0.80 per share translates to a 0.22% yield. It is expected to pay a quarterly dividend of $0.20 per share on January 30, 2023.

For the fiscal third quarter ended October 29, 2022, DDS’ net sales increased 4% year-over-year to $1.57 billion. The company’s total assets increased 1.4% year-over-year to $3.79 billion. Its EPS came in at $10.96, representing an 11.7% increase from the prior-year period.

DDS’ EPS and revenue for fiscal 2023 are expected to increase 6.5% and 5% year-over-year to $42.64 and $6.96 billion, respectively. It has an impressive earnings surprise history, surpassing the consensus EPS estimates in each of the trailing four quarters. The stock has gained 46.6% year-to-date to close the last trading session at $359.20.

DDS’ POWR Ratings reflect solid prospects. The company has an overall rating of B, which equates to a Buy. It is ranked #9 out of 66 stocks in the Fashion & Luxury industry. In addition, it has an A grade for Quality and a B for Value.

Click here to see the other ratings of DDS for Growth, Momentum, Stability, and Sentiment.

CURV is a company providing women’s plus-size apparel and intimates. The company designs, develops, and merchandises its products under the Torrid and Torrid Curve brand names. It is involved in selling apparel products, including tops, bottoms, dresses, sleepwear, swimwear, and non-apparel products comprising accessories, footwear, and beauty products.

CURV’s net sales for the second quarter ended July 30, 2022, increased 2.4% year-over-year to $340.87 million. The company’s income from operations increased 198.4% year-over-year to $39.42 million. Moreover, its total liabilities declined 5% to $795.21 million compared to $836.82 million for the fiscal year ended January 29, 2022.

Analysts expect CURV’s EPS for the quarter ending April 30, 2023, to increase 7.8% year-over-year to $0.25. The company has a commendable earnings surprise history, surpassing the consensus EPS estimates in three of the trailing four quarters. Over the past month, the stock has fallen 12.6% to close the last trading session at $4.16.

CURV’s positive outlook is reflected in its POWR Ratings. The stock has an overall rating of B, which translates to a Buy in our proprietary rating system. It is ranked #4 out of 46 stocks in theSpecialty Retailers industry. It has an A grade for Growth and a B for Quality.

In total, we rate CURV on eight different levels. Beyond what we stated above, we have also given CURV grades for Value, Momentum, Stability, and Sentiment. Get all CURV ratingshere.

JILL operates as an omnichannel retailer of women’s apparel under the J.Jill brand. The company offers knit and woven tops, bottoms, dresses, sweaters, outerwear, footwear, and accessories, including scarves, jewelry, and hosiery.

On August 4, 2022, JILL launched Welcome Everybody, a new online shopping experience in stores celebrating all women’s totality and marking a transformative moment in the brand’s evolution.

Claire Spofford, CEO and President of JILL, believes that this venture could modernize the company’s value proposition, introduce new customers to relevant and compelling products, and clearly communicate what it offers.

JILL’s net sales for the second quarter ended July 30, 2022, increased marginally from the year-ago period to $160.34 million. The company’s gross profit rose 2.8% year-over-year to $112.47 million. Also, its adjusted EBITDA gained 8.8% year-over-year to $35.57 million.

Its adjusted net income increased 34.6% year-over-year to $17.69 million. Its adjusted EPS came in at $1.24, representing a 33.3% increase from the prior-year quarter. In addition, its adjusted income from operations increased 16.8% year-over-year to $28.19 million.

Analysts expect JILL’s EPS and revenue for fiscal 2023 to increase 26.8% and 4% year-over-year to $2.70 and $608.80 million, respectively. JILL has an impressive earnings surprise history, surpassing the consensus EPS estimates in each of the trailing four quarters. The stock has gained 31.5% year-to-date to close the last trading session at $25.23.

It is no surprise that JILL has an overall rating of A, which equates to a Strong Buy. It is ranked first in the Fashion & Luxury industry. In addition, it has an A grade for Sentiment and Quality and a B for Value.

To see the other ratings of JILL for Growth, Momentum, and Stability,click here.

WMT shares were trading at $152.06 per share on Monday afternoon, up $1.83 (+1.22%). Year-to-date, WMT has gained 6.34%, versus a -15.93% rise in the benchmark S&P 500 index during the same period.

About the Author: Malaika Alphonsus

Malaika’s passion for writing and interest in financial markets led her to pursue a career in investment research.

With a degree in Economics and Psychology, she intends to assist investors in making informed investment decisions.

The Dow Jones Industrial stocks (DIA) have barely budged this year even with so many stocks cratering in the stock carnage of 2022. Look for the mighty Dow to eventually fall fast as 2023 begins.

shutterstock.com – StockNews

Stocks have certainly bounced strongly off their recent lows. NASDAQ 100 (QQQ) is now up just over 12% from the October lows. S&P 500 (SPY) added on almost 15% in the same time frame. The Dow Jones Industrials (DIA) has been the star performer, gaining nearly 18% in the past two months.

Lower interest rates and not so terrible earnings have certainly provided some fuel for the recent red-hot rally. Now that earnings season is winding down and rates are finding a floor, look for stocks to have trouble gaining ground from here. This is especially true for the Dow 30 stocks which have gotten too far ahead of themselves on a comparative and actual basis. Plus, the Dow is about to enter a seasonally bearish period as 2023 starts. Traders and investors looking to short stocks may be wise to consider doing it with DIA for these three reasons just mentioned.

Comparatives

The Dow Jones Industrials (DIA) have undoubtedly been the best performing of the three major indices so far in 2022. DIA is down just under 4% year-to-date while the S&P 500 (SPY) has lost over 14% and the NASDAQ 100 (QQQ) dropped nearly 29% this year. Factor in the higher dividend yield of the DIA versus SPY or QQQ and that overall performance gap widens a little more.

Normally these three indices tend to move in unison – or be much more highly correlated to use a fancier term. Look for both the SPY and QQQ to be relative out-performers, and the DIA the weakest of the three, in ‘23 to close this performance gap back to a more traditional relationship.

The Dow Jones has gotten somewhat cheaper from a P/E valuation perspective. The current P/E stands at just under 21 today versus just over 22 a year ago, or a drop of roughly 5%.

Compare that relative drop to similar metrics on both the S&P 500 and NASDAQ 100. Both indices have seen their current valuations fall by well over 30% on a P/E basis. In fact, SPY is now trading at a significantly lower P/E multiple than DIA. 12 months ago SPY was trading at almost a 7 point premium to DIA.

Technicals

DIA is once again hit overbought readings on the chart that have corresponded with tops in the past. Shares are hovering around 70 on a 9-day RSI basis. Bollinger Percent B breached 100 but has since softened. MACD got to an extreme but is poised to go negative and generate a sell signal. DIA is trading at a big premium to the 20-day moving average and has stalled out at $340 overhead resistance once again. A pullback towards the $328 area to test the 20-day moving average seems the most likely course.

Seasonality

The calendar suggests the Dow will start to slowdown as the New Year approaches. January has been the worst performing month over the past 20 years with gains less than half of the time and an average loss of -0.70%. November, conversely, has been one of the best months while December checks in at just above average.

Stock traders looking to position for a weak start to 2023 may want to consider shorting DIA near the end of 2022.

Option traders could elect to put on a bearish calendar spread trade by buying January puts and hedging by selling December puts to position for an eventual pullback in January but perhaps further consolidation in December. This is especially true given that implied volatility (IV) has fallen to comparatively cheap levels at just 31%, especially versus historic volatility of twice that at 62%.

POWR Options

What To Do Next?

If you’re looking for the best options trades for today’s market, you should check out our latest presentation How to Trade Options with the POWR Ratings. Here we show you how to consistently find the top options trades, while minimizing risk.

If that appeals to you, and you want to learn more about this powerful new options strategy, then click below to get access to this timely investment presentation now:

shares closed at $396.03 on Friday, up $1.79 (+0.45%). Year-to-date, has declined -15.65%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Tim Biggam

Tim spent 13 years as Chief Options Strategist at Man Securities in Chicago, 4 years as Lead Options Strategist at ThinkorSwim and 3 years as a Market Maker for First Options in Chicago. He makes regular appearances on Bloomberg TV and is a weekly contributor to the TD Ameritrade Network “Morning Trade Live”. His overriding passion is to make the complex world of options more understandable and therefore more useful to the everyday trader.

Tim is the editor of the POWR Options newsletter. Learn more about Tim’s background, along with links to his most recent articles.

More economists are pointing out the recessionary storm clouds that do not portend well for stock prices. Gladly the stock market (SPY) offers the opportunity to make profits no matter of direction…if you apply the right strategies. This article will give more details on the market outlook along with a trading strategy with 9 picks to come out on the right side of the action. Read on below for more….

shutterstock.com – StockNews

Let me jump to the vital conclusion of this week’s commentary.

Not only do I believe we have a much steeper bear market in front of us, but I have hand selected 9 trades to set you up for gains as the market tumbles to new lows.

More on that a little later. First, it’s important that you appreciate the gathering storm clouds for recession in the next 12 months and why stocks will soon tumble much lower…

Earlier this week I put forward my most consequential commentary to help explain why a recession and steeper bear market are on the way. In fact, I shed light on why the Fed very much wants, and even needs, this to happen.

Yes, that sounds pretty conspiratorial on the surface. However, I think as you read through it the verity of the case will emerge quite easily.

I will share the link below in case you have not read it yet as it forms a good back drop for what we discuss next:

One of the key points in there is about the Feds array of tools to help reign in demand to bring down inflation. The least talked about, and yet still powerful tool, is the idea of “talking down the market”.

Here is the key section from the article on that topic:

“So “talking down the market” is about creating a pessimistic atmosphere that leads to lower demand. That can best be understood by appreciating that the people who own the most stocks are also the wealthiest people in the country who spend the most as consumers. Those very same people are also the captains of industry who control corporate purse strings.

With that in mind now consider this chain reaction:

More Bearish on Stock Market > More Pessimistic Economic Outlook > Less Spending (consumer and business) > Lower Demand > Lower Inflation

Once again it seems that I am going the conspiratorial route with this conversation. But do consider the STERN comments made by Fed officials every time we have had a spike in stock prices over the last few months. This is the very essence of talking down the markets.”

With that backdrop in place consider the speech made by Fed Governor Bullard Thursday morning that got stocks heading lower in a hurry. Here is a link to a more complete article on what he discussed. And here is what I believe to be the key eye-opening comment:

“However, Bullard’s presentation argued that 5% could serve as the low range for the where the funds rate needs to be, and that upper bound could be closer to 7%. That is well out of sync with current market pricing, which also sees the fed funds rate topping out around 5% by mid-2023.”

Let me reframe this vital conversation.

Many traders thought that the potential signs of peaking inflation found in the CPI report this month was good cause to start the next bull market. This had them believing that the previously understood 5% level for Fed Funds rate was never going to be achieved because not necessary.

Not only is Bullard saying that 5% is still in play. Rather, it is at the low end of the range of what is needed to corral inflation with 7% a real possibility. That level of hawkishness is comes hand in hand with a recession.

Let me assure you that the leaders of the early November rally up to 4,000 did not appreciate this vital fact. Heck, even the bears pushing stocks down to 3,491 in early October did not appreciate this possibility which now doubt will have detrimental effects on the economy and stock market by extension.

Once again, the recession and bear market thesis is still in full swing with lower lows on the way this year. That is why a recent Wall Street Journal survey showed that market experts now have a 65% expectation of a recession coming within the next 12 months.

Note that the average recession and bear market came with only a 40% expectation of that negative outcome. So, this shows you a very marked increase in negativity of what the future holds for investors.

For these reasons, and many more, I still believe that the 2,800 to 3,200 is the basic range of this bear market’s bottom for the S&P 500 (SPY). And if you stuck a gun to my head to pick the precise level I would say a little under 3,000 would probably be the proper cause for panic and capitulation that should mark the true and lasting bottom.

However, we are getting way ahead of ourselves as that is like happening 3-6 months from now.

Simply stated, you should expect more stock market downside in the weeks and months ahead. Thus, best to prepare your portfolio accordingly to not just survive…but thrive in that market environment.

What To Do Next?

Discover my special portfolio with 9 simple trades to help you generate gains as the market descends further into bear market territory.

This plan has been working wonders since it went into place mid August generating a robust gain for investors as the market tanked.

And now is great time to load back as we deal with yet another bear market rally before stocks hit even lower lows in the weeks and months ahead.

If you have been successful navigating the investment waters in 2022, then please feel free to ignore.

However, if the bearish argument shared above does make you curious as to what happens next…then do consider getting my updated “Bear Market Game Plan” that includes specifics on the 9 unique positions in my timely and profitable portfolio.

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”) CEO, Stock News Network and Editor, Reitmeister Total Return

SPY shares were unchanged in after-hours trading Friday. Year-to-date, SPY has declined -15.65%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

Share buybacks, capacity expansion, acquisition plans, and semiconductor trade skirmishes all factor into the recent uptrend in Netherlands-based chip gear maker ASML (NASDAQ: ASML).

MarketBeat.com – MarketBeat

Shares soared 17.82% in the past week and 52.41% in the past month, and are currently trading 24% above their 50-day moving average.

The uptrend began in October, on the heels of ASML’s better-than-expected third-quarter results. After that report, several analysts upgraded the stock or boosted their price targets, as you can see using MarketBeat analyst data.

The consensus price target is now $797.29, a potential upside of 38.25%. Positive news was cited as a catalyst for the price target increase. Analysts’ consensus rating on the stock is “buy,” but that should not be taken as a recommendation. It’s always important to evaluate any stock within the parameters of your risk tolerance, existing holdings, and financial goals.

That said, ASML is showing unusual strength. Other large chip gear makers, such as Applied Materials (NASDAQ: AMAT) and Lam Research (NASDAQ: LRCX)also rallied recently, but have trended lower in the past week, while ASML has maintained its gains.

Rally’s Pace Picked Up

ASML’s rally gathered steam on November 10, when the stock gapped up 14.57% in more than double the average turnover. The company held an investors’ day, at which it announced several initiatives and updates, including:

Despite an uncertain macro environment, the company expects longer-term demand and capacity to show healthy growth.

It expects industry developments and innovation to drive growth across semiconductor markets.

The company plans to boost its capacity to meet future demand.

CEO Peter Wennink said that even if China sales were excluded, that would not affect the company’s growth forecasts. His comments addressed concerns about U.S. restrictions on chip manufacturing gear to China.

ASML also instituted a new share buyback program valued at around $12.2 billion, set to run through December 2025.

ASML is part of the chip-equipment-gear industry. It manufactures extreme ultraviolet lithography systems, which it sells to semiconductor makers. It has carved out a niche in that category, giving it a dominant place in the wider semiconductor business.

The company’s sales and earnings dipped in 2022, as chipmakers cut plans for capital spending. For the full year, Wall Street is eying net income of $14.14 per share, a decrease of 13%. However, that’s seen rising by 34% next year, to $18.92 per share.

Recent price action has been encouraging, although the stock has been underperforming the broad market in the past 12 months. A weekly chart gives the clearest indication of the company’s long downtrend, and where it’s currently trading, relative to its late 2021 highs.

Shares retreated to a two-and-a-half-year low in October, shortly before the earnings release set the tone for a fresh rally. The stock has ticked higher, and is now back at its May 2022 level.

ASML has characteristics of a growth stock, even in the current market downturn. For example, its price-to-earnings ratio is 39, which could be considered high.

It’s true that it has a lot of ground to make up before regaining its September 2021 high of $895.93, but with this month’s price action, shares cleared a shorter-term consolidation that began in August. ASML is now trading above several key moving averages. In a potentially encouraging sign, the shorter-term averages are turning higher as the longer-term 200 day line turns lower.

That’s a positive trend, and the stock may be headed for a bullish crossover in the next several session, as the 50-day line rises above the 200-day. That could be an indication that the current uptrend has enough momentum to lift the stock even higher, as analysts expect.

You want to know more about the SLB dividend. Well, this is the right place because by the end of this article you will understand what SLB dividend is, why the distribution was cut and why it is a good choice for income investors who can sustain a little risk.

MarketBeat.com – MarketBeat

The key takeaway for potential SLB investors is that SLB, formerly Schlumberger, is a multinational organization and the world’s largest oilfield services operator, period. This is key to know because the oilfield services industry is in the midst of a generational-quality super-cycle that began during the COVID-19 pandemic. This supercycle is expected to last for up to a decade or longer and will drive revenue, profits and capital gains for investors.

The real opportunity at this time is dividend increases. The oilfield services stocks are well-known, or were before the pandemic, as dividend growers. Because SLB cut its distribution to preserve capital and cash during the crisis it is in a position to not only increase its payment but to make a series of large annual increases that will help to drive share prices back to their all-time highs or higher.

Schlumberger Ltd. Overview

Schlumberger Ltd., doing business as SLB, is a global oilfield services company and the world’s largest offshore driller. The company operates out of 4 primary offices that are located in Paris, Houston, London and The Hague. The stock trades on the NYSE, Euronext, LSE and Swiss SIX exchanges and is a very wide and tightly held company.

SLB was founded in 1926 by two French brothers as the Electrical Prospecting Company. The two had experience conducting geophysical surveys throughout Europe and North America and went into business providing services and equipment. Among the company’s many feats is the 1st ever-recorded electrical resistivity test of a well, a test that is used today in the oil and gas industry to assess the structure of geological formations.

The company expanded its operations into the US and logged its 1st well there in 1929. By 1934 the brothers were opening the Schlumberger Well Survey Company in Houston, Texas. In 1948 the company opened its research division, the Schlumberger-Doll Research Center, and then in 1956 Schlumberger Ltd. was formed as the holding company for all Schlumberger business.

The company continued to grow via expansions and acquisitions until the COVID-19 pandemic hit. While the acquisitions did not end the company was forced to lay off about 25% of its workforce. Since then, it has been slowly rebuilding the workforce to meet the increasing demand from the industry.

The company’s latest innovations center around GHG and sustainability. It has made advances in carbon capture, methane control, and flare control that are driving a reduction in emissions globally. While the company is not shifting away from carbon-based energy, it is committed to advancing the industry in a sustainable manner.

SLB Dividend History

SLB is a regular dividend payer is not a consistent dividend grower. The company, aside from a distribution cut in 2020 related to the COVID-19 pandemic, has only ever increased its payment but not at a sustained, annual pace. For the first 25 years or so there were regular increases but that stopped in 2018 and carried through until 2021. Between those two times, the company’s payout fell from $0.50 per quarter or $2.00 annually to only $0.13 per quarter or $0.54 annually. This is a decline of 73% and the payout was not recovered by 2022 when others in the oil & gas industry were already reinstating theirs. Why buy dividend stocks? Because they pay you to own them and provide leverage for a portfolio.

Ratings: SLB

Schlumberger Dividend Statistics

Schlumberger’s dividend was yielding about 1.35% in late 2022 and is expected to rise in the coming years. The payout ratio was also low at 32% which helped to drive the expectation for future increases. The only bad news at the time was the -20% CAGR which was due to the COVID-19-related distribution cut in 2020. Before that, Schlumberger had only ever increased its payment since the dividend’s first distribution in 1989.

Schlumberger Inside And Institutional Ownership

The insiders don’t hold a large amount of SLB stock but they do own some and they don’t sell it very often. The institutions, on the other hand, hold a great deal of the stock, more than 79% of it, and they have been buying it since 2021 and at an aggressive pace.

Schlumberger Analysts Activity

The analysts’ sentiment in SLB stock warmed in 2021 and has the consensus rating up to a Moderate Buy from a firm Hold in the previous years. The warming sentiment was compounded by a rising price target that is leading the stock higher. The high price target has the stock at a new multi-year high and completing reversal in price action that should get the stock back up to all-time highs or higher by the time the super-cycle is over.

Schlumberger Debt Ratings

Schlumberger uses debt to finance growth, capex, and other corporate uses and is rated investment grade by all three major rating agencies.

SLB Dividend Growth CAGR

The SLB dividend history CAGR is the compound annual growth rate or the average growth rate of the dividend payment over a set number of years. It is an important metric for those who want to learn how dividend stocks work. This is usually expressed as a 3, 5, or 10-year CAGR and is used to gauge the rate of increase an investor can expect. Because dividend increases can offset the impact of inflation on investment dollars, the higher the better. SLB dividend history shows a mixed CAGR because of the pandemic-driven distribution cut but that is expected to improve significantly over the next decade.

Dividend Capture Strategy for SLB

Step #1 – Target The Dividend

The first step is to target the dividend you want to capture. Stocks like SLB are a good choice because they make regular payments that are well-telegraphed to the market. Once done, it’s time to go to the next step.

Step #2 – Buy The Stock

Once the dividend is targeted it’s time to wait for the next declaration. Once declared, watch the stock price for an opportune entry point ahead of the Date of Record. The stock has to be owned at the close of business on the Date of Record for the investor to receive the recently declared distribution amount.

Step #3 – Hold The Stock

This step is simple, all you have to do is hold the stock past the Date of Record until the ex-Dividend Date which is the next day.

Step #4 Sell The stock

This step is harder because the price of a stock typically falls by the dividend amount on the ex-dividend day. If, however, a good entry was made there should be ample margin to produce a profit from the now “captured” dividend payment. When should you sell a dividend stock? The best time is when you can make a profit.

Schlumberger Dividend Is Growing

Schlumberger cut its distribution during the pandemic and that was smart. The move didn’t hurt the share prices and has helped to ensure the balance sheet is still healthy. Now, the payment is as safe as ever and there is a robust outlook for dividend increases in the coming years. Not only is the company in good shape, but a supercycle in oil-field services is underway. That’s a good reason to buy a dividend stock. How to invest in dividend stocks. Very carefully.

FAQs

Does SLB pay a dividend?

Does SLB pay dividends? Yes, it does. The company has a healthy cash flow and returns cash to its shareholders on a regular basis.

Does SLB pay monthly dividends?

SLB stock dividend is an annualized payment that is distributed in 4 quarterly payments. The payments are declared each quarter following board approval and the stock goes ex-dividend about 6 weeks later.

What is Schlumberger yield?

Schlumberger dividend yield has varied over time as the stock price changes and the distribution amount too. The yield in late 2022 was about 1.35% but that was after a COVID-19-related distribution cut that did little to hurt share prices.

is a smart mobility technology solutions company that operates three segments: Government Solutions, Commercial & Fleet Services, and Parking Solutions. Government Solutions services the dreaded photo enforcement cameras for running red lights, speeding, and school bus safety. Verra detects and processes traffic violations through its road safety camera programs with municipalities and school districts. This segment continues to prosper as more municipalities consider adding these photo enforcement cameras for public safety and revenues. Commercial & Fleet Services offer automated toll and violations management and title and registration solutions to rental car companies and fleet owners. It owns nearly a 90% market share of this segment. The Company renewed its tolls and violations contract with Avis Budget Group (NASDAQ: CAR) competitor Hertz Global (NYSE: HTZ) for five-years. Parking Solutions provide parking software and hardware solutions to parking operations and facilities including universities, municipalities, healthcare facilities and transportation hubs in the U.S. and Canada. The Company has bounced back since the pandemic lockdowns which shut down traffic as commuters stayed home. The start of the school season also helped jump revenues as school bus camera violations commence again. Upon initial reading of its Q3 earnings release, it appears to have been a large beat, but upon closer examination, there was some financial engineering involved to make a weaker quarter appear stronger than the year-ago period.

MarketBeat.com – MarketBeat

Financial Engineering

Service revenues climbed to $180.6 million, up from $141.8 million in Q3 of 2021. However, products revenues fell to $17.04 million in Q3 2022 from $20.28 million in the prior year. The cost of service revenue, product sales, operating expenses, and general and administrative expenses all rose higher in the quarter for a total of $152.16 million versus $120.2 million a year ago. Interest expense nearly doubled to $20.26 million from $11.64 million in Q3 2021. This led to the net income of $24.58 million which was lower than the $27.3 million a year ago. However, EPS was $0.15 versus $0.14 due to the reduction in shares from 165.4 million to 158.2 million diluted weighted average shares outstanding. The Company authorized a $125 million stock buyback program over the next 12 months in May 2022. On May 12, 2022, Verra paid $50 million to a third-party financial institution for the initial delivery of 2,739,726 shares. The final settlement occurred on Aug. 3, 2022, with the delivery of 445,086 shares. The Company paid an additional $6.9 million to buy back 445,791 shares. On Aug. 19, 2022, Verra paid $68.1 million to receive and initial delivery of 3.3 million shares and the final settlement is expected to occur in Q4 2022. The Company paid $125 million for stock buybacks and $0.1 million for transaction costs up to Sept. 30, 2022.

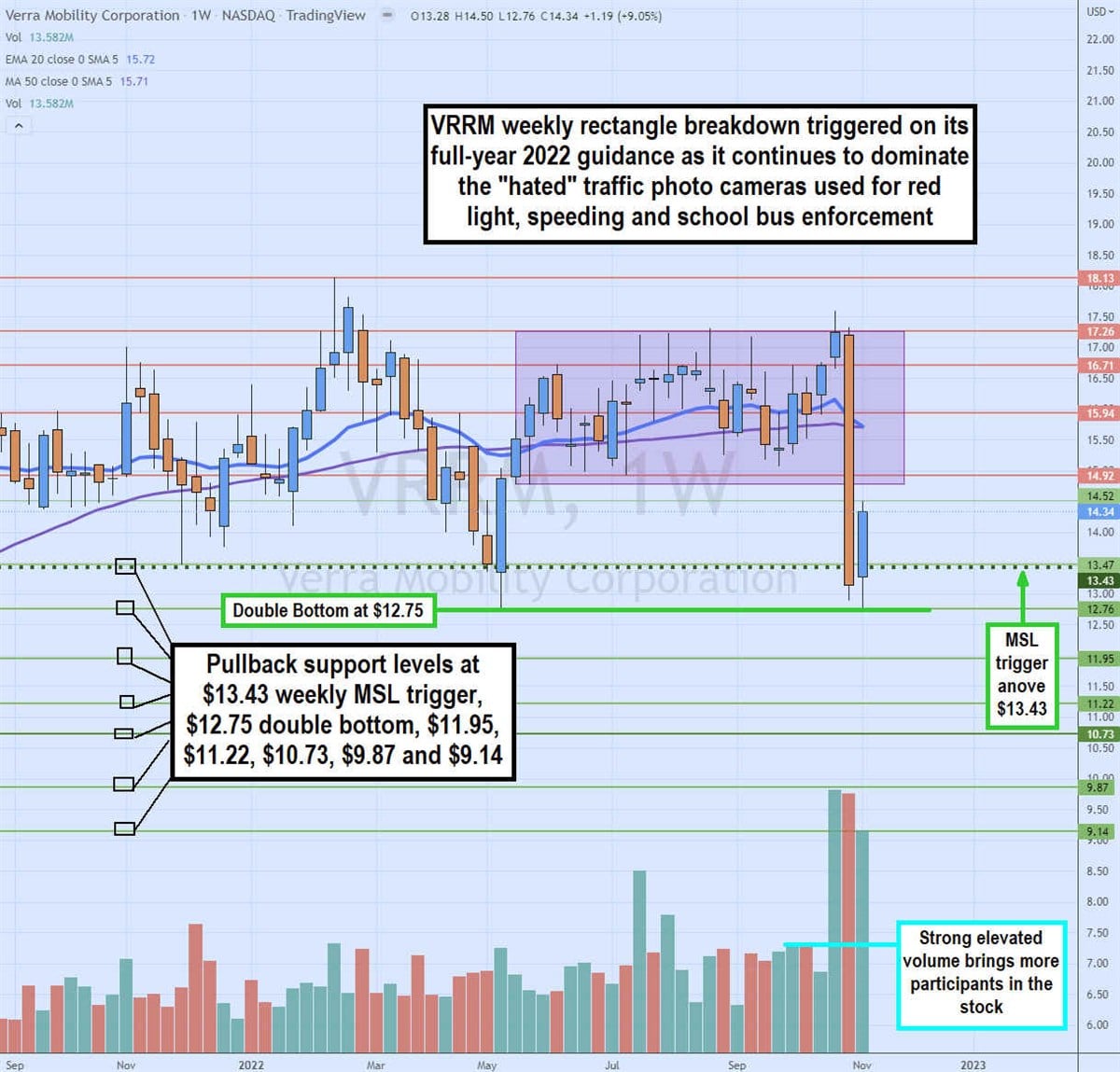

Rectangle Breakdown and Double Bottom in the Weekly Charts

The VRRM chart is about as simple as it gets due to the relatively small range indicating a lack of volatility. The weekly candlestick chart for VRRM illustrates the rectangle price range between $14.75 to the $17.60 for the past 10 months. Shares finally broke the range to the downside in reaction to its recent Q3 2022 earnings report falling to a low of $12.76 before bouncing to form a double bottom. The weekly 20-period exponential moving average (EMA) overlaps the weekly 50-period MA at $15.71 with no channel between them. Shares managed to rally off the double bottom on the breakout through the $13.43 weekly market structure low (MSL) trigger. It’s worth noting that daily trading volume has steadily been climbing from the beginning of 2022. VRRM averaged a few hundred thousand shares per day in early 2022 to a range of 1.5 million to 4 million shares a day by November 2022. The additional volume is a good indicator of growing liquidity and a potential indication of a capitulation on the double bottom formation after earnings. Pullback support areas sit at the $13.43 weekly MSL trigger, $12.75 double bottom, $11.95, $11.22, $10.74, $9.87, and $9.14.

Growth is Still There

Verra released its Q3 2022 earnings report on Nov. 2, 2022, for the quarter ending September 2022. The Company reported earnings-per-share (EPS) profit of $0.27 beating consensus analyst estimates for a profit of $0.14 by $0.13. Net income was $24.6 million versus $27.3 million in the year-ago period. Adjusted EBITDA was $90.9 million versus $82.1 million in the year ago period with EBITDA margin at 46% versus 51%, respectively. Revenues grew 21.9% YoY to $197.66 million versus $197.34 million consensus analyst estimates.

Macro Trends

Verra Mobility CEO David Roberts said, “We delivered an outstanding third quarter, highlighted by strong revenue and adjusted EBITDA growth and solid free cash flow generation. We are benefitting from several macro trends, including continued robust travel demand by consumers and businesses as well as strong and growing interest in automated enforcement for road safety and increased traffic flow. We are poised to close out 2022 on a high note and are excited to start 2023 with strong operating momentum across our three business units.” The Company still plans to expand into Europe and expects to gain from the $2.7 billion Federal Infrastructure Investment and Jobs Act which directly allocates funds for school bus and traffic safety programs.

By the time you get through this article, you’ll know what you need to know about the stock, the Jack in the Box share price and its dividend.

The key takeaway: Jack in the Box can offer a turnaround story and a growth story as well as a Jack in the Box stock price that comes with an established dividend. The company is not yet well known as a dividend grower but that may change down the road. Until then, as an investor, you can look forward to growth and an attractive payout.

Jack in the Box Inc. Overview

Jack in the Box was founded in 1951 when its owner Robert Oscar Peterson rebranded an existing fast food concept as Jack in the Box. The new chain was to be drive-thru oriented and featured the first two-way intercom for drive-thru service. The concept proved popular and led to the design of the iconic Jack in the Box drive-thru locations featuring a smiling clown across California and the west.

The original chain was company owned and private and eventually sold to Ralston Purina, which operated it for many years. During this time, the company grew and expanded until hitting a slow patch in the early 1980s. It was about this time that Ralston Purina decided to sell the company to management. Management reinvigorated the brand and by 1987, it went public.

Longtime CEO Larry Comma altered the business during the early 2000s which led to brand stagnation and reduced sales and profits. In 2018, the franchisees held a “no confidence” vote, which led to his resignation. The current CEO, Darin Harris, came on board in June 2020 after serving as a franchise operator for Qdoba and Papa John’s and as a senior executive for Captain D’s, Arby’s and Cici’s Pizza.

Today, the company has accelerated the switch from company-owned to franchised, leaning hard on digital, expanding into new territories, and unifying system-wide menu choices. These efforts helped reestablish Jack in the Box as a player during the COVID-19 pandemic and set it up for long-term sustained growth as well. The company sells a diverse range of chicken finger meals, hamburgers, chicken sandwiches and international-themed items like tacos and egg rolls.

Jack in the Box Dividend and Dividend History

Jack in the Box first paid its dividend in 2014 so it has a recent dividend history. The company has increased its payout over the years if not at a consecutive annual pace. The average rate of increase is running well over 10% and company metrics suggest it could sustain a few more like it if it chose to do so. The dividend yield is attractive as well, about 2%, above the broad market average. The company pays its dividend on a quarterly basis and buys back shares as well. The board of directors approved a fresh buyback allotment late in 2022 that is worth $200 million to investors over the course of several years.

Dividend stocks are the foundation of many investment strategies. How many dividend stocks you purchase is up to you, but Jack in the Box could be one of them. Read on for more information and to learn how dividend stocks work.

Ratings: JACK

Let’s take a look at dividend safety and attractiveness, its positive balance sheet and analyst ratings to help you determine whether JACK fits into your investment goals.

Dividend Safety and Attractiveness

By Wall Street standards, you can consider Jack in the Box dividends relatively safe, with a low 28% payout ratio. This means the company only pays 28% of its earnings as dividends, a very reasonable amount that leaves ample cash flow to service debt and fund expansion plans. The yield near 2% is less attractive than competitors but the payout is cheap compared to competitors as well. Jack in the Box was trading near 15x its current-year earnings outlook in 2022 while competitors traded 19x to 25x earnings.

Positive Balance Sheet

Jack in the Box carries debt and net debt as well but the balance sheet is well managed. The long-term debt-to-asset ratio is very low at just over 1x assets, a strong position for a growth company.

Analyst Consensus

The analysts’ consensus in Jack in the Box slipped to a firm “hold” following the Del Taco acquisition because it was a little confusing. Why did Jack buy a taco store after it had already sold a taco store, Qdoba? Regardless of the reason, it was accretive to the top and bottom lines so sentiment should improve as results roll in and the expansion plans gain traction.

JACK Dividend Growth CAGR

The compound annual growth rate (CAGR) for Jack in the Box is the mean annual growth rate of an investment over a specified period of time longer than one year. The higher the CAGR, the better and a reason to buy dividend stocks. Jack’s CAGR in 2022 was only 2%. That said, the company had not increased its dividend for several years before and the last two increases were 10% and 33%, which are substantial increases and attractive to dividend growth investors. Note that a high CAGR could decline in the following years and create a headwind for share prices.

Dividend Capture Strategy for JACK

Let’s walk through the dividend capture strategies for Jack in the Box.

Step 1: Buy Jack in the Box stock.

Buy the stock for the first step in the dividend capture strategy. You must do this before the day of record or the day of official ownership of the stock. You can hold the stock for the least amount of time by buying on the day of record or just before — only shareholders of record on the day of record can receive an upcoming payment.

Step 2: Hold Jack in the Box stock.

Next, hold Jack in the Box stock until after the day of record. Doing this entitles you to receive the upcoming dividend. It doesn’t matter whether or not the investor owns the stock on the day the payment is distributed — any owner of record will receive the payment.

Step 3: Sell Jack in the Box stock.

The third and most difficult step involves selling the stock. Owners of record can sell the stock as soon as the ex-dividend day, which is the day after the date of record. The tricky part is selling the stock at break even or higher because any losses will cut into the profits earned by “capturing” the dividend. Jack stock price tends to rise as the date of record approaches, then falls the day after and often by the dividend amount, which often happens among known dividend payers.

Additional Strategy: Invest in Jack in the Box.

How to invest in dividend stocks like Jack in the Box? Follow steps one and two but hold off on step three from above. Dividend stocks and income investing involve buying and holding so you can earn dividends over time. When you should sell dividend stocks depends on the portfolio strategy, share price and market action.

Jack in the Box Winds Up for Growth

Jack in the Box offers an interesting play on fast food and hamburgers for three reasons:

The first is CEO Darin Harris, who seems clued into what the modern fast-food consumer wants.

The opportunity for growth, which is phenomenal. The company would have to triple in size to outcompete the No. 3 player, Wendy’s, and then triple again to match the No. 2 player, Burger King.

The dividend, which has not grown now but will once the growth story has matured.

FAQs

Let’s take a look at some questions about Jack in the Box stock.

Is Jack in the Box’s dividend growing?

The Jack stock dividend continues to grow but is not yet a well-known dividend grower. The company has only made dividend increases but far fewer have been consecutive. The payout ratio is low so increases could be substantial at some point in the future.

What is Jack in the Box’s dividend yield?

The Jack in the Box dividend yield varies with the share price but tends to run in the range of 2% or so. The yield is lower than competitors in the burger/fast food arena but there are mitigating factors that include the company’s growth opportunity and the outlook for future dividend increases.

When does Jack in the Box pay dividends?

Jack in the Box dividend is an annualized payout that comes in four installments. Distributions are made once per quarter following the board’s approval. Jack in the Box has never paid a special dividend or irregular or extra dividend but it could happen in the future.

As many Americans fire up their furnaces for the winter months, they’ll also be eyeing their home heating bills. They’re going to be paying more, and several companies will be the beneficiary of those higher prices. Among them will be several midstream oil and gas companies that are responsible for keeping natural gas flowing across the country.

MarketBeat.com – MarketBeat

Midstream companies are among the most stable investments in the oil and gas industry. Many operate as master limited partnerships (MLPs). These companies aren’t known for generating significant capital growth. In fact, they’re known as the “utilities” of the natural gas sector.

Investing in MLPs isn’t for every investor as they do present some tax implications. But for investors who have wealth preservation and income as their most important goals, these stocks make up for that with generous dividends.

This article will look at three of the top companies that investors should be looking at right now. Each offers a healthy dividend, but also may be ready to deliver some share price appreciation. But first, let’s answer this question.

Is It Too Late to Invest in Natural Gas Stocks?

It wouldn’t seem to be the case. A poll conducted by Pew Research Center in March 2022 found that over two-thirds of Americans support the use of a diverse energy mix that includes natural gas.

Many of these respondents still want the United States to be carbon neutral by 2050. But most of the respondents were concerned about “unexpected problems” that could result from reducing fossil fuel production.

One of those unexpected problems is on full display since the Russian invasion of Ukraine. Europe relies on Russia for much of its natural gas needs. To meet that need this winter, many European Union nations are looking for natural gas from elsewhere. And the United States is a prime candidate.

Enterprise Products Partners

With a $54 billion market cap, Enterprise Products Partners (NYSE: EPD) is one of the largest midstream companies. In its most recent quarter, the company’s natural gas pipelines transported a record $17.5 trillion BTUs per day which speaks to the ongoing demand for natural gas.

Many analysts note that over 30% of the company’s shares (or “units” since it’s an MLP) are owned by company insiders. The thesis is that this level of ownership means that management has a personal stake in making sure the business is run in a prudent manner. And that is reflected in the company’s balance sheet which keeps a significant amount of cash on hand.

Some of that cash is used to support the dividend which currently has a yield of over 7.6%. Plus, the company just increased its dividend for its 25th consecutive year making it part of the dividend aristocrat club.

As of this writing, EPD stock has just crossed above both its 50- and 200-day simple moving averages after a period of consolidation. This may create an opportunity for investors to capture a little share price growth to end the year.

Enbridge

Enbridge (NYSE: ENB) has a market cap of over $81 billion. I could list many of the same positives for Enbridge as I did for Enterprise Products Partners. This is a very fundamentally sound company with a secure dividend that currently yields over 6%.

One differentiating factor for Enbridge is its ability to capitalize on the growing liquefied natural gas (LNG) market. As mentioned above, Europe is looking to the West for natural gas which will have to be transported as LNG. Enbridge has several projects that are near liquefication terminals. The company expects this will allow it to garner a fair share of this business, which adds growth potential to the solid dividend offered by Enbridge.

Magellan Midstream Partners

The third midstream company to watch is Magellan Midstream Partners (NYSE: MMP). It checks in with the smallest market cap of the three companies. At just over $10 billion, it could be considered a mid-cap company.

MMP stock is up over 10% for the year and is trading above its 50- and 200-day moving averages at the time of this writing. But investors are really buying a stock like this for secure income. The company does have a dividend yield of just over 8%. And the company has increased that dividend for 19 consecutive years.

If International Game Technology PLC (NYSE: IGT) were a slot machine, it would be showing three diamonds. The stock is up more than 60% from its September 2022 low and on the move following a sparkling third-quarter performance.

MarketBeat.com – MarketBeat

As far as reopening plays go, the electronic gaming equipment maker is proving to be a diamond in the rough. While most airlines and restaurants experience bumpy recoveries, casinos are booming.

According to the American Gaming Association, the U.S. casino industry had its best quarter ever in Q3. Commercial casino operators hauled in more than $15 billion as consumers continued to spend on experiences in the face of elevated gas and grocery prices. And since this excludes revenue at tribal casinos, the overall figure is likely much higher.

Americans’ willingness to visit casinos during economic weakness is welcomed news for IGT. Casinos are more likely to spend on new slot machines and table games when business is good. This along with the emergence of online gaming was evident in the company’s latest report.

How Were IGT’s Third Quarter Financial Results?

IGT reported an 8% year-over increase in third-quarter revenue. Leading the way was the Global Gaming division, which recorded a 31% jump in revenue as casinos reopened and reactivated installed equipment. IGT generates revenue not only from new equipment sales, but also from various maintenance and service streams. Revenue was down 4% in the Global Lottery business.

Third quarter earnings per share (EPS) came in at $0.43, which marked a 13% improvement from the prior year period. Both revenue and EPS topped Wall Street expectations.

As the income statement strengthened, so too did the balance sheet. IGT ended the period with $5.1 billion in net debt, a 16% year-over-year decline. Lower debt is a positive not only because it reduces interest expense, but also improves the company’s chances of securing additional funding to pursue organic growth or M&A opportunities. At 3.1x, IGT’s net debt leverage ratio is the lowest it has ever been. This is nothing short of remarkable considering what it endured during the early pandemic.

IGT wasn’t the only one that had a good third quarter. In September 2022, one lucky player at Foxwoods Resort Casino in Connecticut won over $1.2 million playing IGT’s Wheel of Fortune Pink Diamond slot machine. Given the Wheel of Fortune franchise has awarded more than 1,100 millionaires since its 1996 inception, it’s easy to see why casino operators (and their visitors) consider these must-have machines.

What is the Outlook for IGT?

Management maintained its 2022 revenue forecast of $4.1 billion to $4.2 billion, with $1 billion expected in the current quarter. At the midpoint, the full-year outlook represents minimal growth beyond 2021 levels. But some growth off a strong base beats a reversion to 2020 levels as has been commonplace in other reopening industries. In 2021, IGT’s revenue surged 31% and it swung from a deep loss to a big profit.

Longer-term, the mid-cap company has a pair of aces in the hole that are expected to complement the traditional gaming equipment business. Online gaming is becoming a bigger part of the mix as states legalize Internet-based casinos. IGT’s suite of online gaming products gives casinos a cost-friendly alternative to developing an online gaming platform in-house.

Sports betting is the real kicker in the IGT growth story. The company’s sports betting solutions similarly represent a quick way to enter the market — and avoid being late to the game.

Will IGT Stock Keep Trending Higher?

IGT is a three-headed growth monster with promising opportunities in land-based casinos, online gambling and sports betting. Having a trio of diversified growth drivers in hand should keep investors coming to the tables.

Another aspect of the investment that could keep buyers interested is the dividend which was reinstated late last year. IGT presently has a 3.3% forward yield that is among the best in the consumer discretionary sector. This gives the stock a rare combination of growth and income that has been hard to come by in the market.

Of course, a major economic recession could dent people’s enthusiasm for in-person or online gaming. Thus far, Americans’ appetite for a night out at the casino has been resilient, though, and the stickiness of this trend will be a key theme to watch. If it recedes, expect IGT’s ascent to do the same. A setback in regulatory approvals could also slow the stock’s roll.

Since the Q3 report, a few sell-side analysts have weighed in on where IGT goes from here. The price target range of $25 to $29 implies limited upside after last week’s high volume gapper, a reflection of the uncertain economic outlook and tough market for growth names.

Yet with long-term secular headwinds in its favor tied to the legalization of online gaming and sports betting, over time IGT could easily push past Wall Street’s latest targets. Any macro-related weakness would make the stock worth a roll of the dice.

Usio, Inc. (NASDAQ:USIO – Get Rating) major shareholder Topline Capital Partners, Lp sold 357,529 shares of the business’s stock in a transaction dated Friday, November 11th. The shares were sold at an average price of $2.06, for a total transaction of $736,509.74. Following the completion of the sale, the insider now directly owns 2,427,912 shares of the company’s stock, valued at approximately $5,001,498.72. The sale was disclosed in a legal filing with the Securities & Exchange Commission, which is accessible through the SEC website. Large shareholders that own more than 10% of a company’s stock are required to disclose their sales and purchases with the SEC.

Topline Capital Partners, Lp also recently made the following trade(s):

On Wednesday, November 9th, Topline Capital Partners, Lp sold 112,508 shares of Usio stock. The shares were sold at an average price of $2.11, for a total transaction of $237,391.88.

On Thursday, October 6th, Topline Capital Partners, Lp sold 11,771 shares of Usio stock. The stock was sold at an average price of $1.68, for a total transaction of $19,775.28.

On Tuesday, August 16th, Topline Capital Partners, Lp sold 44,950 shares of Usio stock. The stock was sold at an average price of $1.60, for a total transaction of $71,920.00.

Usio Trading Up 1.3 %

Shares of NASDAQ USIO opened at $2.27 on Wednesday. The company has a market cap of $57.49 million, a price-to-earnings ratio of -8.41 and a beta of 1.83. Usio, Inc. has a 12 month low of $1.22 and a 12 month high of $8.62. The stock has a 50-day moving average price of $1.75 and a two-hundred day moving average price of $2.04.

Institutional Inflows and Outflows

Institutional investors have recently bought and sold shares of the business. Essex Investment Management Co. LLC raised its stake in Usio by 2.5% during the first quarter. Essex Investment Management Co. LLC now owns 218,111 shares of the company’s stock worth $781,000 after acquiring an additional 5,293 shares in the last quarter. Accurate Wealth Management LLC acquired a new position in Usio during the first quarter worth about $42,000. Vanguard Group Inc. raised its stake in Usio by 13.7% during the first quarter. Vanguard Group Inc. now owns 1,000,801 shares of the company’s stock worth $3,583,000 after acquiring an additional 120,821 shares in the last quarter. Renaissance Technologies LLC increased its stake in shares of Usio by 4.8% in the first quarter. Renaissance Technologies LLC now owns 525,591 shares of the company’s stock valued at $1,882,000 after buying an additional 24,250 shares during the period. Finally, Cruiser Capital Advisors LLC increased its stake in shares of Usio by 64.8% in the first quarter. Cruiser Capital Advisors LLC now owns 126,401 shares of the company’s stock valued at $453,000 after buying an additional 49,701 shares during the period. Institutional investors and hedge funds own 16.94% of the company’s stock.

Analyst Ratings Changes

Several equities research analysts recently weighed in on USIO shares. Barrington Research cut their price objective on shares of Usio from $7.00 to $4.00 and set a “market perform” rating for the company in a research report on Friday, August 12th. Maxim Group cut their price objective on shares of Usio from $8.00 to $5.00 and set a “buy” rating for the company in a research report on Monday, August 15th.

Usio, Inc, together with its subsidiaries, provides integrated electronic payment processing services to merchants and businesses in the United States. The company offers various types of automated clearing house (ACH) processing; and credit, prepaid card, and debit card-based processing services. Its ACH transaction processing services include Represented Check, a consumer non-sufficient funds check that is presented for payment electronically rather than through the paper check collection system; and Accounts Receivable Check Conversion, a consumer paper check payment that is converted into an e-check.

See Also

Receive News & Ratings for Usio Daily – Enter your email address below to receive a concise daily summary of the latest news and analysts’ ratings for Usio and related companies with MarketBeat.com’s FREE daily email newsletter.

is a supplier of analog and mixed-signal integrated circuits (IC) and high-performance electronic components for the power supply market. It allows for efficient and compact AC-DC power conversion products for power supply ranging from under one watt up to 500 watts of output. Its ICs enable for the conversion of high-voltage alternate power (AC) from a wall outlet to low-voltage direct current (DC) used for electronic devices ranging from battery chargers, LED lights, and smartphones to appliances. Its SCALE gate drivers are critical components in high-power systems in electric vehicles (EVs), motors, solar and wind turbines, and DC transmission lines. Its products are key components in the clean energy ecosystem movement as it enables the generation and transmission of green and renewable energy in applications measured in milliwatts to megawatts. It’s EcoSmart energy efficiency technology saves billions of kilowatt hours from being wasted and its ICs eliminate billions of electronic components in AC-DC power supply, gate drivers, and LEDs.

Power Integrations reported their Q3 2022 earnings on Nov. 2, 2022. The Company reported earnings-per-share (EPS) of $0.84 to beat consensus analyst estimates for $0.85 by $0.01. Revenues continued to drop (-9.4%) year-over-year (YoY) to $160.23 million, falling short of analyst expectations for $164.29 million. The Board of Directors have authorized a $100 share buyback subject to pre-determined price/volume thresholds with no expiration.

More Weakness Expected Ahead

Unfortunately, the Company lowered its guidance for Q4 2022 with revenues coming in between $120 to $130 versus $159.89 consensus analyst estimates. GAAP gross margins are expected between 55.5$ to 56% and GAAP operating expenses are expected between $42 to $42.5 million. Power Integrations CEO Balu Balakrishnan commented, “Demand has continued to weaken, particularly in appliances and other consumer applications, and inventories have accumulated in the supply chain. While our near-term revenue outlook is therefore muted, we continue to gain market share across a broad set of end markets while making excellent progress on growth initiatives like automotive, motor drive, and our proprietary GaN technology. Our board of directors has committed $100 million to share repurchases, reflecting our strong balance sheet and our high level of confidence in our long-term growth prospects.”

Cowen Cuts Rating to Market Perform

On Nov. 3, 2022, Cowen lowered POWI shares to a Market Perform with a $65 price target. It’s analyst Matthew Ramsay commented, “POWI has a strong portfolio with GaN quickly gaining traction, but limited visibility into a recovery in consumer-related markets likely caps upside to shares. With our estimates moving down sharply, we believe current valuation appropriately balances the budding growth opportunities with consumer weakness.”

Weekly ABCD Reversal Harmonic Pattern in Effect

The weekly candlestick chart on POWI indicates an ABCD harmonic bullish reversal pattern. This pattern is comprised of three price swings as indicated on the chart with an initial price fall from point A to point B $106 to $72.50, then a price rise from point B up to point C from $72.50 to $98.92, then a price fall from point C through point D from $98.92 through $65.45 to form a swing low bottom at $59.16 in the last week of October 2022. The ABCD pattern has specific rules when trading. The buy territory is when shares rise through point D which is $65.45. There is also a weekly market structure low (MSL) that triggered the breakout through $67.14. This caused shares to spike up through the weekly 20-period exponential moving average (EMA) resistance around $72.50 towards is falling weekly 50-period MA resistance at $80.10. There are two upside targets measured by the Fibonacci retracements from point A ($106) to point D (65.45) level. The first target sits at the 32.8% retracement level at $80.94 and the second target sits at the 61.8% retracement level at $90.51. Stop-loss levels remain under point D at the $63.70 level and the $60.01 level. Pullback support levels below that sit at $55.78 and $50.34.

Long-Term Secular Growth Drivers

While the near-term headwinds continue to erode Power Integrations performance, long-term secular growth drivers still exist. It’s gallium-nitride (GaN) technology increases efficiency by expanding dollar content. The transition to clean and renewable energy generation is a direct growth driver. The global movement to reduce carbon emissions is a boon to its business. Power Integration has a strong presence in renewable energy, electric transportation, and efficient high-voltage DC transmission. It’s Eco-Smart technology saves nearly 1.6 million homes’ worth of electricity usage by reducing standby consumption for appliances and electronics. The transition to highly integrated power supplies is ongoing as it saves on labor and materials costs while increases efficiency. The high-voltage, which has grown 3X since 2010, continues to expand with advanced chargers, smart home products and appliances, LED lighting, electrification, and electric vehicles.