[ad_1]

Analyst Report: Intuit Inc

[ad_2]

[ad_1]

Crypto equities, which had strongly outperformed Bitcoin over the past 18 months, are now showing signs of fatigue.

Amidst a broader market pullback, investors appear to be fleeing riskier corners of the market.

After a stellar 18-month run, crypto equities are beginning to lose momentum relative to Bitcoin, according to the latest report shared by Matrixport. The 10x Research Crypto Stocks Index surged as much as 500% during the period, far outpacing Bitcoin’s 117% gain.

However, recent corrections in key names like Strategy, Coinbase, and Metaplanet have pushed the index lower, which is now resting at 427%. Adding to the slowdown, Circle’s IPO, which was initially well-received, failed to sustain investor demand, which evidenced fading enthusiasm for new listings.

Institutional activity also appears subdued. This could be in part due to the seasonally weaker summer months, which have left the sector without strong catalysts. With no significant crypto IPOs on the immediate horizon, Matrixport believes that equities may enter a consolidation phase, even as Bitcoin maintains steadier performance.

Crypto equities faced another difficult session on August 20. In fact, today’s trading saw Strategy and Coinbase both retreat further in line with a broader risk-off mood. Coinbase (COIN) fell around 2% in early trading to $296 Strategy (MSTR) slipped even further, declining 2% to $330. USDC issuer, Circle (CRCL), also slid 3.62% to $130.34, and lost nearly $5 during the same period.

Over the last 24 hours, the price of Bitcoin has decreased by 2% to a level slightly above $112,500, while Ethereum managed to recover from its nosedive and now sits at $4,300.

QCP Capital observed that all eyes are on Fed Chair Jerome Powell’s upcoming remarks scheduled during this week’s Jackson Hole symposium, as his guidance will shape the direction of monetary policy amid the delicate balance between easing inflation and rising labor risks.

Despite positive developments in the crypto industry, such as the passage of the GENIUS Act and institutional adoption exceeding $100 billion, the recent sell-off indicates that short-term positioning remains fragile.

According to the firm, risk assets could experience further volatility if Powell delivers a hawkish message or if labor and inflation data come in stronger than expected.

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

[ad_2]

Chayanika Deka

Source link

[ad_1]

Investors for Paris Compliance, which seeks to hold publicly traded companies accountable for their climate commitments, argues the companies have breached the Alberta Securities Act “with long-standing and widespread inaccurate and incomplete disclosure” related to net-zero commitments.

“By extensively using net-zero terminology in their communications, Cenovus and Enbridge have led reasonable investors and the public to believe that their business models are aligned with the net-zero energy transition, which in fact threatens both their existing business and fossil fuel expansion plans,” the group said in its submissions to the Alberta Securities Commission.

It said it opted to take its complaint to the ASC instead of the federal Competition Tribunal under new anti-greenwashing rules because “investors have a strong interest in the credible and timely enforcement of securities law.”

It adds that nothing in the amendments to the Competition Act, which became law last year, supersedes the obligations of securities regulators to also crack down on greenwashing. It cites guidance from Canadian Securities Administrators, a national umbrella group, that says environmental disclosures should be subject to the same standards as financial reporting.

Under the Competition Act changes, private parties, including environmental groups, can now launch a complaint directly.

But Michael Sambasivam, senior analyst with Investors for Paris Compliance, said that shouldn’t be necessary. “We don’t believe the burden for enforcement for these kinds of complaints should be on private citizens and private groups.”

He said his group zeroed in on the two companies to capture two separate segments of the energy business—Cenovus produces the raw product, while Enbridge transports it. Sambasivam said they also both “offered some of most consistently flagrant violations of Canadian security principles” of the company disclosures it looked at.

After the Competition Bureau’s anti-greenwashing provisions took effect, Cenovus was among the oilsands companies to pull its net-zero statements from its website. Uncertainty over whether the company has abandoned those commitments is a “form of incomplete disclosure disallowed by the Alberta Securities Act,” the complaint said.

The complaint also makes note of public lobbying that it says contradicts climate commitments. Top executives of both companies were among the signatories to an open letter from oil and gas industry leaders to newly elected Prime Minister Mark Carney this spring that, among other things, urged Ottawa to scrap its cap on greenhouse gas emissions and industrial carbon levy.

Enbridge remains committed to achieving net zero emissions from its operations by 2050 while at the same time delivering energy people rely on, spokesman Jesse Semko said in an emailed statement. The company has reduced emissions from its operations by 22% compared to its 2018 baseline through improved efficiency, purchasing less carbon-intensive electricity and investing in renewables, he added. “We also remain committed to accuracy and transparency—and we stand behind the information we share in our reports and communications.”

Investors for Paris Compliance argues emissions from the end use of the fossil fuels produced and shipped should be taken into account in net zero reporting, not just emissions from operations.

Cenovus did not respond to a request for comment.

The group is asking the ASC to investigate existing and past climate disclosures from Cenovus and Enbridge to assess their accuracy and adequacy. The investigation should consider evidence from peers and competitors, it said. It also wants the ASC to work with other provincial securities regulators on guidance for net zero claims for Canadian publicly listed companies.

A spokeswoman for the commission says it and its counterparts have given companies guidance and resources to help them prepare disclosures of material climate-related risks, as well as avoiding language that could be considered greenwashing. She said it does not comment on reviews it does of complaints.

[ad_2]

The Canadian Press

Source link

[ad_1]

The financial services industry is deploying generative AI throughout operations and investment banking is realizing high returns.

Agentic AI can enhance operations across all financial institutions including:

Chip giant Nvidia, for one, has seen a sharp rise in the use of its agentic AI model application among financial services firms and is working to provide more computing power to drive adoption across the industry, Kevin Levitt, who leads global business development for financial services at the company, told Bank Automation News.

Financial services is a leading vertical at Nvidia, Levitt said.

“FIs have a long track record of adopting and integrating new technology. … They know how to integrate these new technologies into their functions and to find returns on them.”

One of the most successful gen AI use cases within financial services has been assisting analysts at investment houses generate equities reports, Levitt said.

“They’re using these [AI] agents to cover specific equities and update research reports on those stocks,” Levitt said. “The agents can handle 10 times the previous volume of documents than a human could, and they’re actually extracting information with greater accuracy.”

One investment house that Levitt did not identify reported that it has “reduced the report generation time from 40 hours down to 15 minutes,” he said. “That’s a 160X improvement.”

Chris Ackerson, senior vice president of product at AI-driven tech provider AlphaSense, agrees. He also told BAN that many financial institutions are using gen AI-driven assistants to help junior bankers write PowerPoint decks and reports.

AlphaSense’s gen AI tool scans the internet, including for specific information such as SEC filings, to find pertinent information for the analyst’s report, he said.

“Traditionally it would have taken many hours or maybe even days to find the right information and synthesize it,” Ackerson said. But with gen AI “that [process] can be automated and analysts can focus on higher order tasks.”

The tool is multidimensional, allowing it to be used to conduct due diligence for M&A activities, another time-consuming activity for FIs, he said.

Nearly 80% of the world’s top asset management firms use AlphaSense’s AI-driven solution, including Goldman Sachs, J.P. Morgan and Morgan Stanley, Ackerson said.

Check out our exclusive new bank industry data here.

[ad_2]

Vaidik Trivedi

Source link

[ad_1]

“Depending what sector, what area you’re in, you’re going to have a favourite.”

While Trump may be pro-business and focused on cutting red tape and taxes — and markets had a good run during his last presidency — Harris presents less of a concern when it comes to geopolitical risks, said Mona Heidari, senior financial advisor at BlueShore Financial.

This “contributes to stronger investor sentiments and stronger investor confidence to invest in the stock market,” Heidari said.

On conference call to discuss Gildan Activewear Inc.’s latest results, chief executive Glenn Chamandy said Thursday that tariffs factor into costs and can create inflation, but it’s still unclear what their overall effect would be. He expressed optimism that Gildan won’t be disadvantaged.

“If tariffs come in, they come in for everybody, so we’ll be in the same position that we’re in today,” he told investors on the call.

Higher spending from the government—which both candidates are likely to do—can be inflationary, making price growth stickier, said Kevin Headland, chief investment strategist at Manulife Investment Management. So can tariffs and tax cuts, he added.

A TD Economics report from mid-October said the Democrats “have a historical edge when it comes to stock market performance,” but that this is likely a reflection of the state of the economy when they take office.

Currie noted that the health-care sector usually does worse in U.S. election years, and that’s no exception this time around. Both parties like to say leading up to an election that they will fight big drug companies and insurance companies, but their promises are usually overhyped, he said.

[ad_2]

The Canadian Press

Source link

[ad_1]

Share prices were up 5% in after-hours trading on Thursday after the strong earnings beat.

Amazon Web Services (AWS) remains the golden goose, even though very few of Amazon’s retail customers know it exists. Revenues climbed 19% during the quarter, and totalled $27.4 billion. Amazon’s advertising revenues were another highlighted area of the report, as they were up 19%. Overall operating profits grew 56% year over year to $17.4 billion, mostly credited to the 27,000 jobs cut by the company since 2022.

Founder, executive chairman and former president and CEO of Amazon, Jeff Bezos was in the headlines this week in his role as owner of the Washington Post. He refused to allow the Post’s editorial team to print their endorsement of Kamala Harris for president, and it was met with widespread outrage from Post readers. As of Tuesday, more than 250,000 subscriptions were cancelled as a result.

Fortunately for Bezos, he purchased the Washington Post (one of the world’s premier news brands) for “chump change”—$250 million (roughly a mere 1.2% of his net worth). So, if he drives it into the ground, I don’t think he’ll shed tears.

No doubt co-founder and CEO of Tesla, Elon Musk, is making similar calculations with his luxury purchase two years ago of Twitter (which he rebranded as X). Critics say he has turned the social platform into an echo chamber for Republican presidential candidate Donald Trump. What are the billions for, if a person can’t even enjoy themselves by buying a little media, am I right? (That’s sarcasm.)

So far we’ve yet to see analysis to show Bezos’ editorial decision affecting Amazon’s share price or revenue numbers. Apparently Republicans buy Amazon Prime, too.

While not having quite as large a market cap as Nvidia and Apple, other mega tech stocks in the U.S. are no slouches. For example, Microsoft is also as valuable as the entirety of Canada’s stock exchanges at $3.2 trillion. Alphabet and Meta clock in at $2.1 trillion and $1.5 trillion respectively. (All figures in this section are in U.S. dollars.)

Here’s what these companies announced this week.

All three companies crushed earning estimates across the board. However, shareholders’ reactions to these earnings beats were still muted. Meta shares were down 2.5% in after-hours trading on Wednesday, and it was a similar situation for Microsoft. Alphabet fared better as its shares were up 3%.

It’s hard to put these numbers into the massive context into which they belong, because the world has never seen anything like these companies before. Here are highlights from the earnings calls. (Scroll the chart left to right with your fingers or press shift, as you use scroll wheel on your mouse to read.)

[ad_2]

Kyle Prevost

Source link

[ad_1]

While some financial advisors recommend the 50-30-20 rule, where 50% of your pay goes to fixed expenses, 30% to discretionary and 20% to savings, putting aside just 10% of your take-home pay for savings is OK, too. “We can be as efficient with that 10% as we can possibly be… meaning we could put your savings in a diversified portfolio where the expected returns are going to be higher and over a longer period of time.”

Ayana Forward, a financial advisor and founder of Retirement in View in Ottawa, acknowledges how hard it can be for single women—and all women—to create a plan to invest, particularly early in their careers. “You have all kinds of competing priorities,” she says, including possible childcare expenses, a mortgage, car payments and school debts. However, Forward encourages women to begin saving anything they can as soon as possible to build habits and benefit from compound interest, which is when your money’s interest starts earning interest of its own.

Here’s how that can look: Let’s say you take $100 a week from your miscellaneous allotment and invest it at an interest rate of 5% and watch it grow. After 30 years, if you had put that $100 in a savings account with no or a low interest rate, you’d only have $156,100—but because you invested it, you’d have $345,914. (Calculate your savings with our compound interest calculator.)

What are your absolute must-haves in life? Your non-negotiables? You don’t have to give those up—you may just have to find an alternative way to make them work while meeting your savings goals. “My client, who is a college instructor, loves to travel, and her trips are usually tax deductible,” says Hughes. But to be able to afford her trips while continuing to save, she picked up a part-time job. “It gave her some extra income since she was determined to meet her goal, which was to own a place of her own,” says Hughes.

Whether you pick up a side hustle or not, chances are there will still be a few sacrifices you’ll need to make. It comes down to looking at your budget and deciding what you want to prioritize in the immediate time period, says Cornelissen, and deciding what you can let go of for a while.

Or it can relieve you from doing the opposite, over-saving for fear of not having enough money. Knowing how much money is going in and going out of your account is key to making a plan for your money.

If you’re employed full-time, find out if your company offers a pension or an employer-sponsored plan, such as RRSP matching (where an employer contributes the same amount as an employee to a registered retirement savings plan). This will help you determine how much you need to save for retirement. “If you don’t have a pension, you’ll need to save more than someone who has a pension,” says Forward.

Also, when planning for your retirement explore government income sources that may be available, like the Canada Pension Plan (CPP) and Old Age Security (OAS). “You can go into your My Service Canada account to get those benefit statements so you know what you’ll be receiving from those programs,” says Forward. (You can log into your My Service Canada account using a unique password or use your bank account log in.)

[ad_2]

Renée Reardin

Source link

[ad_1]

Despite these setbacks, CPKC posted an income gain of 7% year over year. The four categories that made the most impact were grain, energy, plastics and chemicals, and they grew revenues by 11%. CPKC says the shipment of wheat to Mexico from the Canadian and American Prairies over the past 12 months was exactly the type of “synergy win” that it was hoping for when the former Canadian Pacific acquired Kansas City Southern back in 2021. This railway remains the only one to span Canada, the United States and Mexico.

CNR CEO Tracy Robinson commented on the railway’s operational challenges. “Our scheduled operating plan demonstrated its resilience in the third quarter, allowing us to adapt our operations to challenges posed by wildfires and prolonged labor issues,” she said. “Our operations recovered quickly and the railroad is running well. As we close 2024, we will continue to focus on recovering volumes, growth, and ensuring our resources are aligned to demand.”

CNR’s revenues were up 3% year over year; however, increased expenses meant the company’s operating ratio rose 1.1% to 63.1% (indicating that expenses are growing as a share of revenue). The railway announced it was raising its quarterly dividend from $0.79 to $0.845. This raise of nearly 7% is right in line with CNR’s mission to conservatively raise its dividend payouts each year.

For more information on these railroads, check out my article on Canadian railway stocks at MillionDollarJourney.ca.

Thursday’s revenue miss left some Rogers shareholders shaking their heads.

Here’s what the large mobile company reported this week:

While solid earnings numbers did take away some of the sting, Rogers’ share price was down 3% on Thursday. Lower-than-expected numbers for new wireless customers were at the root of low revenue growth. The oligopolistic Canadian wireless market remains uncharacteristically competitive as Rogers, Telus and Bell all continue to fight for market share. That competition is hurting profit margins for all three telecommunications giants at the moment. (Unlike in past years, when the three telcos all enjoyed charging some of the highest wireless plan fees in the world.)

One highlight for Rogers was its sports revenue vertical, which was up 11% from last quarter. Rogers has really doubled down on its sports media strategy over the last few years and now owns a controlling share of the:

Despite owning all those household-name sports assets, it’s worth noting that Rogers’ wireless and cable divisions were responsible for close to 90% of revenues, with sports and media making up the rest.

[ad_2]

Kyle Prevost

Source link

[ad_1]

Changes to the BoC rate impacts the prime rate set by Canadian lenders, which in turn affects the pricing of variable-based borrowing products, which are based on the prime rate plus or minus a percentage. Following this most recent cut, the prime rate at most Canadian lenders will drop to 5.95% from 6.45%. What does that mean to your money and your debt? Keep reading.

When the central bank lowers its benchmark rate, it typically does so in quarter-point increments —unless there’s an economic reason for a heftier cut. Half-percentage point decreases like today’s are rare, but they do have a precedent; the last time the BoC doled out cuts of this size was back in March 2020, when it implemented three in rapid succession to support the economy amid the onset of the COVID-19 pandemic. Outside of the COVID era, today’s rate cut is the largest since March 2009.

That the BoC is once again supersizing its cuts points to concerns that the economy is slowing at a faster pace than expected. The most recent inflation report for September from Statistics Canada revealed the year-over-year inflation as measured by the Consumer Price Index (CPI) fell to 1.6%, which is below the BoC’s 2% target. That’s considered sustainable for the Canadian economy. The BoC tweaks its benchmark rate to keep it as close as possible to target. When inflation is running hot, it hikes rates to cool consumer spending and access to credit. The opposite occurs when inflation gets too soft; the BoC must ease borrowing conditions to encourage consumption, and bolster economic growth, otherwise it risks an impending recession. We’re in the latter situation right now.

Should economic data, such as inflation, GDP, and job market numbers, continue to trend as it has, additional rate cuts are a certainty, including more supersized cuts. Much will hinge on the next CPI report, due out on November 19. Should inflation remain sluggish, that increases the chances of another half-point cut in the BoC’s next rate announcement, on December 11.

The BoC is also keen to lower its rate down to “neutral” state, which is a range between 2.25% to 3.25%. This again is a rate that neither inflames or stunts economic growth, and remaining above it too long poses economic risk.

Following this rate cut today, the overnight lending rate remains 0.50% above the higher end of the neutral range. Overall, analysts think the BoC will lower its rate by another 1.75% by the end of 2025.

What does it mean for you, your home, your finances and more? Read on.

Whether you’re shopping for a brand new mortgage rate or renewing your existing term, today’s rate cut will make it slightly more affordable to do so.

Variable mortgage rate holders are the most heavily impacted by the October rate cut, as their mortgage payments—or the portion of their payment that services interest—will immediately decrease along with their lenders’ prime rate. These borrowers in Canada also have much to look forward to, with anticipated rate cuts on the horizon.

[ad_2]

Penelope Graham

Source link

[ad_1]

Seagate Technology Holdings plc (NASDAQ:STX – Get Free Report) SVP John Christopher Morris sold 1,131 shares of the company’s stock in a transaction that occurred on Tuesday, October 22nd. The stock was sold at an average price of $111.90, for a total value of $126,558.90. Following the transaction, the senior vice president now owns 7,191 shares in the company, valued at $804,672.90. This trade represents a 0.00 % decrease in their position. The transaction was disclosed in a document filed with the SEC, which is accessible through the SEC website.

STX opened at $112.64 on Wednesday. The company’s 50-day simple moving average is $104.92 and its two-hundred day simple moving average is $99.52. The stock has a market capitalization of $23.71 billion, a P/E ratio of 73.14 and a beta of 1.04. Seagate Technology Holdings plc has a 52-week low of $64.12 and a 52-week high of $115.32.

Seagate Technology (NASDAQ:STX – Get Free Report) last issued its quarterly earnings data on Tuesday, October 22nd. The data storage provider reported $1.58 earnings per share for the quarter, beating analysts’ consensus estimates of $1.26 by $0.32. Seagate Technology had a net margin of 5.11% and a negative return on equity of 8.41%. The company had revenue of $2.17 billion for the quarter, compared to the consensus estimate of $2.13 billion. During the same quarter in the prior year, the firm earned ($0.34) earnings per share. The firm’s revenue for the quarter was up 49.1% compared to the same quarter last year. Research analysts forecast that Seagate Technology Holdings plc will post 7.09 EPS for the current fiscal year.

The company also recently disclosed a quarterly dividend, which will be paid on Monday, January 6th. Investors of record on Sunday, December 15th will be issued a $0.72 dividend. This represents a $2.88 annualized dividend and a dividend yield of 2.56%. This is a positive change from Seagate Technology’s previous quarterly dividend of $0.70. Seagate Technology’s payout ratio is presently 181.82%.

A number of institutional investors have recently bought and sold shares of STX. Quarry LP purchased a new position in shares of Seagate Technology during the 2nd quarter worth $27,000. Kayne Anderson Rudnick Investment Management LLC raised its holdings in Seagate Technology by 2,407.1% in the 2nd quarter. Kayne Anderson Rudnick Investment Management LLC now owns 351 shares of the data storage provider’s stock worth $36,000 after purchasing an additional 337 shares during the period. Family Firm Inc. purchased a new position in Seagate Technology during the second quarter valued at $41,000. Larson Financial Group LLC grew its holdings in Seagate Technology by 15,766.7% during the second quarter. Larson Financial Group LLC now owns 476 shares of the data storage provider’s stock valued at $49,000 after purchasing an additional 473 shares during the period. Finally, Gilliland Jeter Wealth Management LLC purchased a new stake in Seagate Technology in the third quarter worth about $55,000. Institutional investors own 92.87% of the company’s stock.

Several equities research analysts recently weighed in on the company. Robert W. Baird lifted their price target on Seagate Technology from $100.00 to $120.00 and gave the company an “outperform” rating in a research report on Wednesday, July 24th. TD Cowen boosted their target price on shares of Seagate Technology from $110.00 to $135.00 and gave the company a “buy” rating in a report on Wednesday, July 24th. Wedbush increased their price target on shares of Seagate Technology from $100.00 to $130.00 and gave the stock an “outperform” rating in a research note on Monday, July 22nd. Wells Fargo & Company boosted their price objective on shares of Seagate Technology from $90.00 to $120.00 and gave the stock an “equal weight” rating in a research note on Wednesday, July 24th. Finally, Morgan Stanley lifted their target price on shares of Seagate Technology from $115.00 to $133.00 and gave the company an “overweight” rating in a report on Wednesday, July 24th. Two equities research analysts have rated the stock with a sell rating, seven have given a hold rating and twelve have issued a buy rating to the company. Based on data from MarketBeat.com, the stock currently has an average rating of “Hold” and a consensus price target of $115.94.

Check Out Our Latest Research Report on Seagate Technology

Seagate Technology Holdings plc provides data storage technology and solutions in Singapore, the United States, the Netherlands, and internationally. It provides mass capacity storage products, including enterprise nearline hard disk drives (HDDs), enterprise nearline solid state drives (SSDs), enterprise nearline systems, video and image HDDs, and network-attached storage drives.

Receive News & Ratings for Seagate Technology Daily – Enter your email address below to receive a concise daily summary of the latest news and analysts’ ratings for Seagate Technology and related companies with MarketBeat.com’s FREE daily email newsletter.

[ad_2]

ABMN Staff

Source link

[ad_1]

That, together with the fear of a stock-market correction, has prompted a lot of Canadians who never considered owning the precious metal before to wonder whether this age-old asset should be part of their portfolios. After all, Canada’s largest robo-advisor, Wealthsimple, allocates 2.5% of its clients’ accounts to gold—and 10% in its halal portfolios.

Should it be part of yours? Or would you just be buying in at the peak? There’s no way to know, except in hindsight. There will always be “gold bugs” out there urging you to sell everything and buy gold before the world goes to pot. Their advice is best avoided.

Here instead are some important facts around investing in gold that will help you make a better-informed decision.

Gold is used for a wide range of products—such as jewellery, dental fillings and electronics—but most of it is simply stored in vaults, in the form of gold bars. Like money itself or cryptocurrency, gold is valuable because people have decided it is. But unlike the other two, it’s immune to manipulation.

As of mid-October, all the refined gold in the world, an estimated 212,582 tonnes, was worth a staggering USD$18.3 trillion. Mines around the world poured another 1,788 tonnes in the first half of 2024. So, the supply of gold is increasing, but slowly. And there’s little anyone can do to change that.

As an investment, gold is classified as a commodity. That is, it’s a standardized and graded substance that trades globally. But unlike, say, soybeans or Brent crude oil, you can store a meaningful amount of gold in your jewellery drawer or safe deposit box. It’s also uniquely non-perishable; part of its appeal in ancient times was the fact it didn’t corrode like other metals. So, you can hold it indefinitely.

If you own gold as an investment, it won’t generate any income; it’ll just go up and down in value according to supply and demand. Over the very long term, its price tends to track the rate of inflation.

Most importantly, gold has a history as a store of value and unit of exchange. Many central banks still hold it to help stabilize their currencies. In developing countries like India and China, many people consider it more trustworthy than paper or electronic money. This is why it continues to hold a privileged place in investment portfolios.

[ad_2]

Michael McCullough

Source link

[ad_1]

Netflix (NFLX/NASDAQ) shareholders were happy on Thursday, as they saw share prices rise 5% in after-hours trading on the back of another excellent earnings announcement. (All figures in U.S. dollars.) Earnings per share came in at $5.40 (versus $5.12 predicted) and revenues were $9.83 billion (versus $9.77 billion predicted).

Paid memberships also topped expectations, at 282.7 million, compared to the 282.15 million predicted by analysts. Netflix chalked up the increase in viewers to new hit shows such as The Perfect Couple, Nobody Wants This and Tokyo Swindlers, as well as new seasons of favourites Emily in Paris and Cobra Kai. Looking ahead to the next quarter, Netflix is banking on the new season of Squid Game and its foray into the world of live sports. Two National Football League (NFL) games and a massively anticipated boxing bout between Jake Paul and Mike Tyson represent new attractions for the streaming giant.

Tuesday was a massive earnings day for United Airlines (UAL/NASDAQ) as earnings per share came in at $3.33, well outpacing the $3.17 that analysts were predicting. (All figures in U.S. dollars.) Revenues were $14.84 billion (versus $14.78 billion predicted). Shares were up more than 13% on the outperformance and the news that the airline was starting a $1.5-billion share buyback program.

Corporate revenue was up more than 13% year over year, while basic economy seat sales clocked an even more impressive 20% increase. Last week, the company announced new international routes headed to Mongolia, Senegal, Spain, Greenland and more.

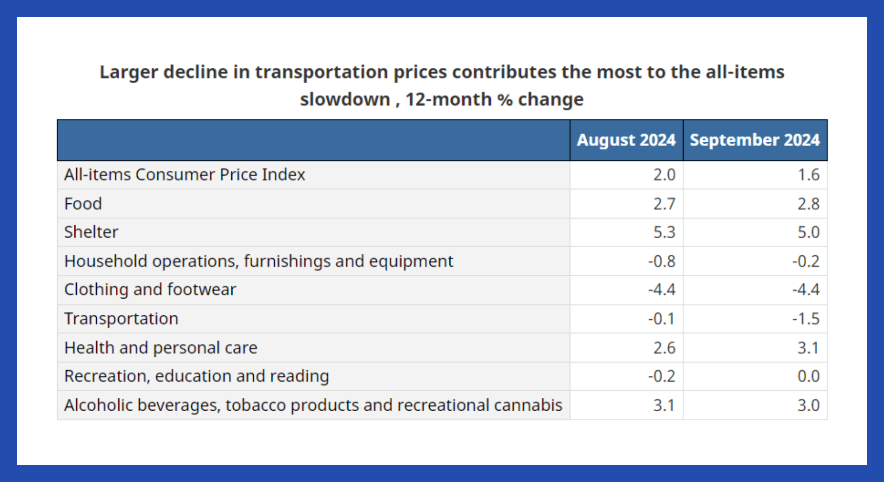

It doesn’t seem that long ago that annualized inflation rates were topping 8%, and there appeared to be no end in sight. Well, the end has arrived. Statistics Canada announced this week that the Consumer Price Index (CPI) annualized inflation rate for September had dropped all the way down to 1.6%. That’s substantially lower than the Bank of Canada’s 2% target.

Led by deflation in clothing and footwear, as well as transportation, the downward trend appears to be widespread. Gasoline was also down 10.7% from this time last year.

Source: Statistics Canada

Of course, increased shelter costs remain the major concern for many Canadians. Rent increases were up 8.2% year-over-year; while that’s down from August’s figure of 8.9%, it’s still a bitter pill to swallow for many.

[ad_2]

Kyle Prevost

Source link

[ad_1]

For a decade now, big acquisitions by Canadian oil-and-gas producers have mostly been met with distaste by investors. So we’ll take it as a heartening sign how well the markets received Canadian Natural Resources’ (CNQ/TSX) decision to buy the Alberta upstream assets of Chevron Corp. (CVX/NYSE) for USD$6.5 billion in cash. CNQ stock rose 3.7% Monday in the wake of the announcement. Chevron was up 0.7% on a day when oil prices increased.

The assets in question comprise a 20% stake in the Athabasca Oil Sands Project, along with 70% of the Kaybob Duvernay shale play. That should add 122,500 barrels of oil equivalent per day to Canadian Natural Resource’s 2025 output, the company said. It also announced a 7% bump to its quarterly dividend, to 56.25 Canadian cents a share, beginning in January.

Chevron explained the asset sale in terms of freeing up cash for U.S. shale acquisitions as well as targeted positions abroad, such as in Kazakhstan, which it considers to hold better long-term profit potential.

Reports of the death of the Magnificent 7 tech stocks’ decade-long run are greatly exaggerated, Nvidia (NVDA/Nasdaq) seemed to say this week as its shares rose past $130. (All figures in U.S. dollars.) That pushed its market capitalization ahead of Microsoft Corp. to $3.19 trillion. That leaves only Apple, with a market cap of $3.4 trillion, worth more than the AI-focused chip-maker.

Nvidia’s stock is up 26% in the past month, compared to a 6% advance for the S&P 500. Nvidia has grown tenfold in just two years. The price movement this week appeared to come from a positive report from Super Micro Computer, a provider of advanced server products and services. It found that sales of its liquid cooling products, deployed alongside Nvidia’s graphics processing units (GPUs), would be even stronger than expected this quarter. Analyst estimates of Nvidia’s adjusted EBITDA (earnings before interest, taxes, depreciation and amortization) for the three-month period ended this month is $21.9 billion.

Posting its second straight disappointing set of quarterly results on Tuesday, beverage-and-snack maker PepsiCo lowered its full-year guidance for organic revenue unrelated to acquisitions.

Results were hampered by recalls of the company’s Quaker Foods products, related to potential salmonella contamination. PepsiCo also experienced weak demand in the U.S. and business disruptions in some overseas markets, such as the Middle East. Pepsi’s North American beverage volumes fell 3% year-over-year, mostly due to declines in energy drink sales. Meanwhile, its Frito-Lay division suffered a 1.5% decline.

“After outperforming packaged food categories in previous years, salty and savory snacks have underperformed year-to-date,” executives said in a prepared statement. Overall, PepsiCo revised its 2024 sales growth outlook from the previous 4% to low single digits.

[ad_2]

Michael McCullough

Source link

[ad_1]

At a time when Canada, just like every other country, is looking for highly skilled workers, our tax rates make it more difficult for them to choose to work here. This is equally true for Canadian citizens and potential new immigrants. Anecdotally, I’m hearing more and more from clients and people in my network that their children who have chosen to study abroad aren’t coming back home because they can earn and keep more of their income elsewhere. I’m not surprised.

Our high tax rates also make it hard to attract investment into our country and for existing businesses to expand. That is essential to improve productivity, innovate, create jobs and compete against peers in lower-tax jurisdictions.

The Allan Small Financial Show, featuring three tax experts—Fred O’Riordan of Ernst & Young, Jake Fuss of The Fraser Institute and Tim Cestnick, a Globe and Mail tax columnist and CEO of Our Family Office—originally aired on September 18, 2024.

We need a better, more thoughtful tax strategy as a country—one that is fair for everyone. Canada has not taken a hard, comprehensive look at our tax system since 1962, when Prime Minister John Diefenbaker appointed the Royal Commission on Taxation.

At the very least, it would be an opportunity to streamline what is a very complicated system, as I see it. At best, it may point to a better way forward. One potential way to streamline our tax system, and make it more efficient and fair, is to implement a flat tax rate across the board. This is not a new concept for taxation.

For the past decade, Estonia has reaped the rewards of having the most competitive, simple and transparent tax system in the OECD. Its personal and corporate tax rates are 20%. It’s set to increase to 22% in 2025 to match its consumption tax, which increased from 20% to 22% in 2024. In the case of individuals, the tax rate does not apply to dividend income; and businesses only pay tax on distributed profits.

The result: the country has been very successful attracting startups and investment.

And we don’t have to leave Canada for an example of a flat tax. From 2001 to 2014, Alberta had a single 10% personal and business income tax rate, dubbed the Alberta Tax Advantage. The Fraser Institute is now calling for Alberta to implement an even lower flat tax of 8% on personal and business income to attract people, businesses and investment in the province and to encourage spending. When Canadians pay less tax, they have more to spend and put back into the Canadian economy.

Another potential way to ensure tax fairness and generate revenue to meet government responsibilities is to foster more opportunities for the public, business and government to collaborate. For example, why not give individuals and businesses the ability to invest in infrastructure projects, such as new roads and highways, and get a rate of return over time.

[ad_2]

Allan Small, FMA, FCSI

Source link

[ad_1]

Some experts speculate the real sticking point in negotiations isn’t about wages but protection from automation. The ILA refused to allow its members to work on automated vessels docking at U.S. ports. As a result, American ports are getting more and more inefficient, ranking not only behind ports in China, but also Colombo, Sri Lanka. (The Container Port Performance Index is put together annually by The World Bank and S&P Global Market Intelligence.)

For reference, the highest-rated port in Canada is Halifax, listed at 108th in the world. Halifax’s port efficiency was well behind not only Sri Lanka, but also economic powerhouses like Tripoli, Lebanon. To give further Canadian context, Montreal is 348th, and Vancouver is 356th, which is just ahead of Benghazi, Libya.

Something tells me that negotiating for USD$300,000-per-year dockworkers is not going to help these North American efficiency numbers. The higher salaries get, the more attractive automation strategies will quickly become. Clearly there will be an eventual reckoning. In the meantime, for at least one more important presidential news cycle, dockworkers will be able to extract large wage gains as they hold the broader economy hostage.

As income-oriented Canadian investors start to grow less enamoured of high-interest savings accounts and guaranteed investment certificates (GICs), the dividend yields of dependable North American utility stocks should begin to look more attractive. Given how quickly interest rates are likely to fall, it’s clear that there is a stampede of investors heading for the stocks of utility companies.

The iShares U.S. Utilities ETF (IDU/NYSE) is up more than 30% year to date, and the iShares S&P/TSX Capped Utilities Index ETF (XUT/TSX) is up about 15% year to date. (Check out MoneySense’s ETF screener for Canadian investors.)

Most of the time utilities (especially those in sectors regulated by federal and local governments) are perceived as “boring.” Sure, the profits are dependable, but if the government is going to determine how much is paid for electricity or natural gas, then a company’s profit margins are tough to change. The dividend income is dependable. But that’s really the whole sales job in a nutshell.

Lately, however, due to AI’s electricity needs and possible AI-fuelled efficiency increases, utilities have been getting some glowing press. Falling interest rates mean that annual interest costs will drop (utilities often have to borrow a lot of money to complete big projects). Meanwhile, Canadian investors looking for safe cash flow are pouring in. Utility stocks make up about 4% of the S&P/TSX Composite Index. The largest utility companies—such as Fortis, Emera, Hydro-One and Brookfield Infrastructure—are some of Canada’s largest companies.

Some of the same income-oriented investors who like utility stocks may also be interested in two new exchange-traded funds (ETFs) that J.P. Morgan Asset Management Canada just launched. The JPMorgan US Equity Premium Income Active ETF (JEPI/TSX) and the JPMorgan Nasdaq Equity Premium Income Active ETF (JEPQ) use options strategies to “juice” the income already provided by higher-dividend-yielding stocks.

[ad_2]

Kyle Prevost

Source link

[ad_1]

The CAPE Ratio assesses a stock’s price compared to its average earnings over the past 10 years, adjusted for inflation. A high CAPE Ratio suggests that stocks might be overvalued relative to historical earnings, indicating potential downside risks.

The picture isn’t as clear-cut as it seems, however. One of the primary drawbacks of equal weighting, as critics point out, is the additional drag on performance from its methodology.

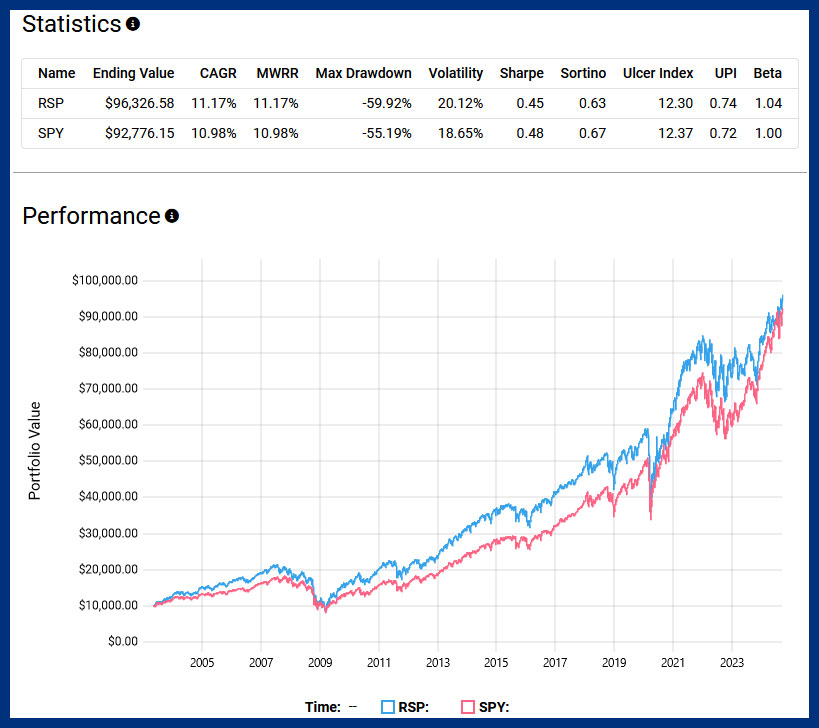

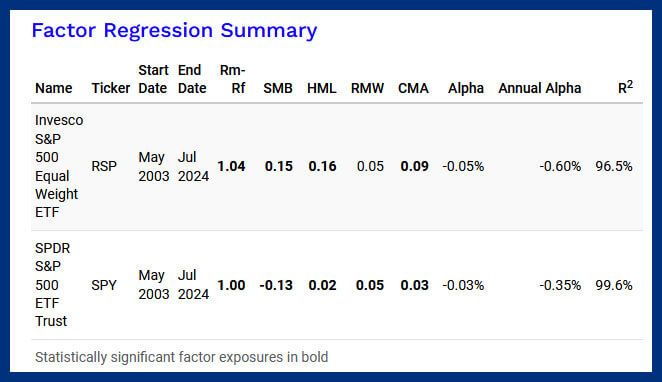

Take the Invesco S&P 500 Equal Weight ETF (RSP) as an example. It has a 21% turnover and a 0.20% expense ratio. The Canadian-listed version is the Invesco S&P 500 Equal Weight Index ETF (EQL, EQL.F). In contrast, SPY maintains a mere 2% turnover and a lower expense ratio of 0.0945%.

While it’s true that RSP outperformed SPY in total returns since its inception in April 2003, the victory isn’t as clear-cut as it might seem. The risk-adjusted return of RSP, indicated by a Sharpe ratio of 0.45, is slightly lower than SPY’s 0.48. What does that mean? It could suggest that RSP took on higher volatility for only marginally better returns. Moreover, RSP experienced a deeper maximum drawdown than SPY. A maximum drawdown measures the largest single drop from peak to trough during a specified period, indicating a higher historical risk of losses for investors.

Further analysis via factor regression reveals that most of RSP’s outperformance can be attributed to the size. Essentially, RSP’s equal-weighted methodology has inadvertently skewed its exposure towards smaller and more undervalued companies, which historically have contributed to outperformance.

This raises a critical point: If the goal is to invest in these kinds of companies, wouldn’t it be more straightforward and efficient to target them directly based on fundamental metrics rather than adopting a blanket equal-weighting approach to the entire S&P 500?

I find myself siding with cap weighting now. The primary appeal is simplicity. Market-cap strategies require fewer decisions regarding rebalancing or reconstitution, which in turn keeps sources of friction like turnover and fees considerably lower—resulting in fewer headwinds to performance.

In an ideal frictionless world, the appeal of equal weighting is clear. However, the reality of quarterly rebalancing and higher fees associated with equal-weight ETFs has not historically yielded better risk-adjusted returns over the last two decades.

[ad_2]

Tony Dong

Source link