Investors who didn’t panic sell through President Trump’s tariff-related comments this month have almost recouped all their losses, with the S&P 500 within half a percent of its all-time close from earlier this month.

There are a few reasons why the minor sell-off that began with trade war threats on China has been erased:

Promising developments for U.S.-China relations

A wave of stronger-than-expected corporate earnings

Investors’ realization that short-term noise won’t derail the structural bull market

As Opening Bell Daily readers know, a similar pattern unfolded during April’s Liberation Day sell-off.

Remember, the S&P 500 has endured two bear markets and two corrections since 2020.

And only one of those can be tied to an actual recession, which occurred at the start of a once-in-a-generation pandemic.

The economy has otherwise grown consistently over the last five years, and equities and earnings have strengthened in kind.

Here’s how veteran strategist Ed Yardeni, founder of Yardeni Research, explains it:

“Corrections tend to occur when investors fear a recession that doesn’t happen. Bear markets tend to be caused by recessions. Currently, the economy remains resilient, and a recession is unlikely, in our opinion.”

In effect, social media posts coming out of the White House — market-moving as they may be — do not exactly impact the structural tailwinds driving financial markets:

Meanwhile, the government shutdown has delayed recent labor market data, leaving investors with one less potentially negative catalyst to trade off.

Indeed, recent headwinds in mind, the team at UBS Global Wealth Management maintains that the bull market is still intact.

“Investors should ensure they have adequate allocation to equities,” said UBS’ Ulrike Hoffmann-Burchardi, chief investment officer for the Americas and global head of equities.

Volatility has returned to markets but it’s going to take a lot more jitters to derail this bull run.

Over the last two trading sessions, regional bank fears tied to Zions Bancorp and Western Alliance pushed the VIX — Wall Street’s fear gauge — as high as 28.99 for the first time since April’s Liberation Day sell-off.

That jump provided just the fodder bearish forecasters have been looking for to bolster their theories of bubbles and crashes.

An Inc.com Featured Presentation

Yet the index closed Friday at 20.78, within range of its long-run average. That only feels high because the VIX has hovered at a tepid 17 through most of the summer.

As it turns out, history suggests the momentary surge in volatility offers a point for the optimists.

Since the start of 2024, the S&P 500 has averaged a 2.2 percent gain the next month whenever the VIX rose above its long-term average of 19.5, according to DataTrek Research.

Stocks have climbed at an 82 percent win rate with this indicator

It was triggered each of the last two weeks

“The VIX is widely cited and closely watched because most traders know it has a good track record of signaling near term lows,” wrote DataTrek co-founders Nicholas Colas and Jessica Rabe in a recent note to clients, adding that they do not believe the recent move warrants concern about a weakening bull market.

CBOE launched the VIX index in 1990, and it’s closed at 19.5 on average over the last three decades.

In bull markets, volatility is usually below 19.5

In bear markets, it’s usually above 19.5

As the DataTrek team and other market veterans have pointed out, heightened volatility indeed often presents a buy-the-dip opportunity.

Here’s the VIX chart again, highlighting a range of closing levels from the last 12 months.

When you compare that to the S&P 500 over the last year, the spikes in volatility indeed have marked local bottoms for stocks.

The above and below charts are nearly inverted mirror images.

None of the above is likely to placate the bears, who will point to heightened volatility as reason to brace for armageddon.

Earnings reports next week, including from Tesla and Netflix, will provide a deeper look at U.S. corporate profits while delayed U.S. inflation data will mark another test of the stock market, which has become shakier even as it remains around record highs.

The fourth year of the S&P 500’s bull run kicked off this week with some significant gyrations after a long period of market calm.

Revived U.S.-China trade tensions and credit concerns at regional U.S. banks drove the anxiety. The CBOE market volatility index, known as Wall Street’s “fear gauge”, has surged in recent days and hit its highest level in nearly six months on Friday.

“The market is becoming more volatile, but it’s also coming off of a very non-volatile period where we didn’t have a lot of risk catalysts bubbling to the top,” said Michael Reynolds, vice president of investment strategy at Glenmede.

An Inc.com Featured Presentation

“Once you have valuations hit sort of full levels, as we’re seeing now almost across the board, you have to be on the lookout for incremental risk catalysts.”

The spark for the latest volatility was a surprise resurgence in U.S.-China trade tensions. Stocks slumped late last week after the U.S. threatened to significantly hike tariffs by November 1 over China’s rare-earth export controls.

The U.S.-China trade issue will be key for markets in the coming week, said Doug Beath, global equity strategist at Wells Fargo Investment Institute. U.S. President Donald Trump confirmed on Friday that he would meet with Chinese President Xi Jinping in two weeks in South Korea.

Sharp swings in global financial shares to end the week also kept investors on edge as they weighed the extent of credit concerns emerging from regional U.S. banks.

Major stock indexes posted weekly gains and are on pace for strong years. The benchmark S&P 500 is up 13.3 percent year-to-date and 1.3 percent below its record high. But there are signs the market is weakening under the surface.

The percentage of S&P 500 stocks in some form of an uptrend declined from 77 percent in early July to 57 percent as of Tuesday while the number of stocks in a downtrend increased from 23 percent to 44 percent over that time, according to Adam Turnquist, chief technical strategist for LPL Financial.

That “narrowing gap highlights emerging cracks in the market’s foundation,” Turnquist said in written commentary. Similarly, Kevin Gordon, senior investment strategist at Charles Schwab, said he will be watching how broadly based the market’s gains are going forward.

“If you have a fewer number of companies that are actually moving higher, but the indexes do move higher because of the megacaps, that’s a really important divergence,” Gordon said.

Attention will be on third-quarter earnings after major banks started the reporting season on a strong note. Aside from streaming giant Netflix and electric vehicle maker Tesla, other companies due to report in the coming week include consumer companies Procter & Gamble and Coca-Cola, aerospace and defense giant RTX and tech stalwart IBM.

The corporate results and executive comments will offer insight into the economy as the U.S. government shutdown has stopped economic data releases since October 1, including monthly employment data.

Corporate “reports and what companies say is really our best chance at assessing what the broader economic health is,” Gordon said.

The government has said it will release the U.S. consumer price index for September on Friday, nine days late, saying the CPI data allows the Social Security Administration to meet deadlines for timely payment of benefits.

The CPI report, which is a closely watched inflation gauge, will be released days before the Federal Reserve’s next monetary policy meeting on October 28-29. The U.S. central bank is widely expected to cut interest rates by a quarter percentage point again, after weakening jobs data prompted the Fed to lower rates last month for the first time this year.

“We’d really have to see something out of left field in terms of notable inflation pressures to knock the Fed off of a rate cut path at the October meeting,” Glenmede’s Reynolds said.

Reporting by Lewis Krauskopf; Editing by David Gregorio and Cynthia Osterman

The economy’s biggest risk may not be tariffs or private credit but the stock market itself, where roughly $9 trillion in equity gains over the past year have powered high-income spending that could quickly reverse if portfolios start flashing red instead of green.

“The surge in stock prices is so key to the well-to-do who are driving consumer spending,” Mark Zandi, Moody’s Analytics chief economist, told Yahoo Finance on Friday. “If that gets turned into reverse and we see stock prices decline, then that’s the real threat to the economy in my mind.”

Moody’s estimates the top 10% of earners account for about half of all consumer spending, a dynamic that’s kept growth steady even as inflation and tariffs bite lower-income households. That link between spending power and market performance has become increasingly evident amid fresh market swings.

US stocks rose on Friday as President Trump eased fears of a further trade escalation with China, rebounding from Thursday’s steep losses sparked by renewed worries over private credit. Regional banks, including Zions (ZION) and Western Alliance (WAL), also recovered after reports of fraudulent loans and mounting credit stress added to investor jitters against the backdrop of a prolonged government shutdown.

Still, Zandi said those risks pale next to what’s building in financial markets, where a sharp reversal could quickly shake the confidence of the wealthy households powering US growth.

“Of all the risks out there, from what’s going on in the banking system to the government shutdown and everything else, that’s the one that’s at the top of my list of worries,” he said.

“I’m more sanguine about the banking system,” he added. “I’m less sanguine about financial markets. Valuations are high. …Everything feels a bit juiced, overvalued, bordering on frothy.”

Zandi warned that froth is directly tied to the same high-income households driving US consumption. That means if market gains unwind, the very group propping up spending could quickly pull back.

Deborah Weinswig, founder and CEO of Coresight Research, which tracks global retail and consumer trends, said the split between high- and low-income households is at its highest level since January 2020.

“The high-end consumer right now is still very strong and stronger than we would have even expected,” Weinswig said, noting spending among wealthier shoppers has continued to rise through the fall.

At the same time, lower-income households are stretching their budgets by visiting more stores per trip, about five or six now versus three before the pandemic, as they hunt for bargains and stack promotions.

America’s economy is increasingly driven by wealthy consumers — a risky dependence if the market turns. (Courtesy: Getty Images) ·RUNSTUDIO via Getty Images

“We continue to see this middle [consumer] being really squeezed,” she said, pointing to discount and luxury retailers as the clear winners. “Those value-oriented retailers on the bottom and those true luxury brands on the top — that’s where we continue to see a lot of strength.”

Weinswig said the retailers that stand to gain the most in this environment include Walmart (WMT), which continues to attract higher-income shoppers, along with the warehouse clubs like Costco (COST), BJ’s (BJ), and Sam’s Club, which she said have the strongest community ties and most sophisticated consumer data.

TJX Companies (TJX), Ross Stores (ROST), and Burlington (BURL) also stand out as shoppers trade down and hunt for bargains.

“We’re going to start to see not only bifurcation of the consumer, but also in some of these stocks,” she added, predicting sharper performance gaps ahead between retailers that can adapt and those that can’t.

But even as some retailers benefit from that bifurcation, there are signs the broader spending picture is starting to soften. According to Deloitte’s 2025 holiday retail survey, overall spending is expected to drop 10% from last year with consumers across all income levels projected to cut back.

“Consumers are feeling an affordability pinch at the moment,” Mike Daher, Deloitte vice chair, told Yahoo Finance. “They’re going that extra mile to make sure they get a higher ROI on their personal spending.”

That value-seeking mindset even extends to higher earners.

Among households earning at least $200,000 a year, about one in four are now exhibiting value-seeking behavior, Deloitte’s data showed.

“They’re either holding back from buying altogether, looking for cheaper alternatives, or waiting for more promotions to happen,” Daher said.

It’s a signal that even the top of the consumer pyramid, the same cohort keeping the US economy afloat, could be nearing a breaking point.

“Those on the lower end of the economy are suffering,” he said, noting recent bankruptcies in the auto sector, including collapses at First Brands and Tricolor, underscore how overextended borrowers and weaker consumers are feeling the squeeze.

“If there’s weakness in consumer capability and wealth and health in there,” he continued. “We’re going to have more of a problem.”

Allie Canal is a Senior Reporter at Yahoo Finance. Follow her on X @allie_canal, LinkedIn, and email her at alexandra.canal@yahoofinance.com.

Best-selling author Andrew Ross Sorkin examines the lessons from the Stock Market crash of 1929 in his new book, “1929: Inside the Greatest Crash in Wall Street History – and How It Shattered a Nation.”

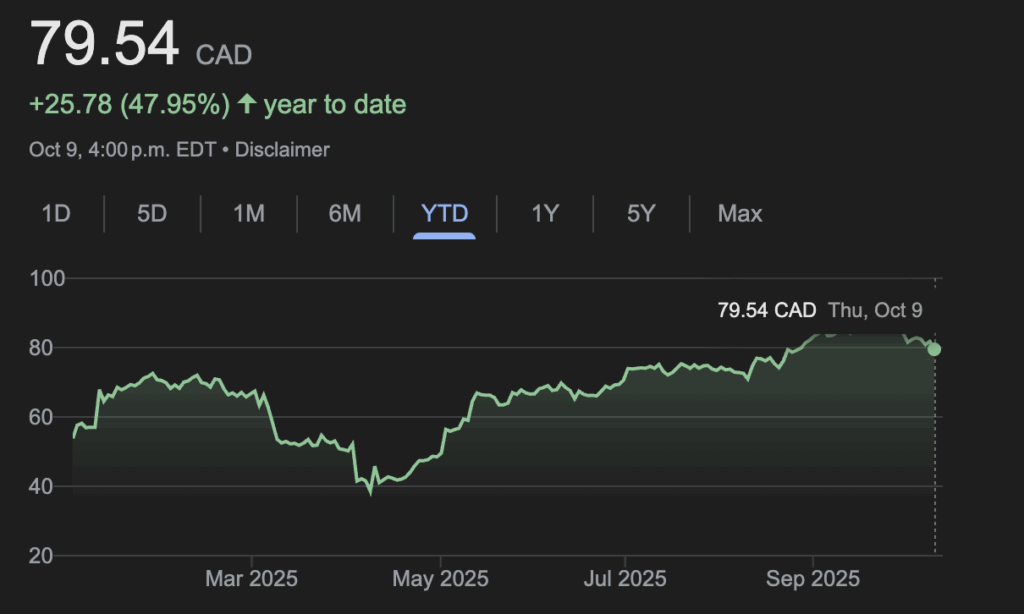

The Cenovus offer values MEG at $8.6 billion, including assumed debt, and is made up of half cash and half stock. MEG shareholders are set to vote on the proposal on Oct. 22.

Cenovus and MEG have neighbouring oilsands properties at Christina Lake, south of Fort McMurray, Alta.

U.S. fuel distributor Sunoco LP’s proposed takeover of Calgary-based fuel retailer and refiner Parkland Corp. (TSX:PKI) has cleared a key regulatory milestone with Ottawa’s approval under the Investment Canada Act. The transaction is expected to close in the fourth quarter of this year, subject to remaining regulatory approvals and the satisfaction or waiver of customary closing conditions, Parkland said in a release Tuesday. A review under the Investment Canada Act considers whether foreign investments would be a net benefit to the country or cause potential harm to national security.

The Parkland-Sunoco deal was announced at a time of fraught Canada-U.S. relations and amped-up resource nationalism amid the onslaught of U.S. President Donald Trump’s tariffs. Earlier this year, Ottawa recently updated national security guidelines under the act to account for potential harms to Canada’s economic security. The government said it will consider the size of the Canadian business, its place in the innovation ecosystem and the impact on Canadian supply chains.

Parkland and Sunoco announced the friendly cash-and-stock deal valued at US$9.1 billion including assumed debt in May following a bitter proxy battle with investors in the Canadian company unhappy with its performance and strategy.

Parkland owns the Ultramar, Chevron and Pioneer gas station chains as well as several other brands in 26 countries. Sunoco outlets that had long operated in Canada were rebranded in 2009 under the Petro-Canada banner. Parkland also runs a refinery in Burnaby, B.C., which supplies nearly one-third of the region’s domestically supplied gasoline and jet fuel.

The deal cleared a key U.S. antitrust hurdle last month when the waiting period under the Hart-Scott-Rodino Act expired. Shareholders approved the takeover in June.

Cineplex selling Cineplex Digital Media to U.S. company Creative Realities for $70M

Cineplex Inc. (TSX:CGX) has signed a deal to sell its Cineplex Digital Media subsidiary to Creative Realities Inc., a U.S.-based digital signage company, for $70 million. CDM offers digital signage for a wide range businesses including retailers and banks as well as digital menu boards for restaurants.

Article Continues Below Advertisement

As part of the deal, Cineplex has signed a long-term agreement to continue as CDM’s exclusive advertising sales agent for CDM operated digital-out-of-home networks across Canada.

Cineplex chief executive Ellis Jacob says the sale will provide the company with meaningful capital to continue to deliver value for shareholders. Cineplex says proceeds of the sale will be used to strengthen its balance sheet and provide cash for share buybacks, debt reduction, and general corporate purposes.

The deal is expected to close in the coming weeks, subject to regulatory approvals and other customary closing conditions.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

By now, investors have no excuse for missing how quickly markets can turn on President Trump’s word.

On account of his posts on Truth Social, stocks turned positive once again Tuesday after Friday’s sharp sell-off.

The pattern has become familiar this year:

An Inc.com Featured Presentation

Tariffs threats drag stocks lower

Reassurance or a pivot pushes stocks back up

U.S. stocks have now recovered more than two-thirds of their losses from Friday’s decline, which marked the largest erasure of market value in six months.

Naturally, the latest dip and bounce can be traced back to President Trump in a near carbon copy of April’s “Liberation Day” episode.

Each major statement from the White House this year has coincided with a near-term bottom, and the investors who have caught on to that rhythm have made money either holding through the volatility or buying the dip.

Even novice traders have learned to monitor the president’s social media feed as a new macro indicator.

While his individual posts vary in tone and content, they continue to dictate short-term direction for asset prices as well as volatility.

Consider how the VIX — Wall Street’s fear gauge — spiked 35 percent on Friday and remained elevated before falling Tuesday, once traders gained more clarity on tariffs.

Just as he has “called” the local bottoms for asset prices, he has “called” the local tops for volatility all year.

The above and below charts are effectively inverses of one another, with swings in each index tied to Trump’s tweets.

These charts suggest that the “buy the dip” reflex should no longer be considered a contrarian move so long as it’s tied to tariff news.

Rather than reacting to policy decisions, it’s now possible in theory to front-run swings in asset prices so long as you can correctly predict how global capital pools will interpret the tone of a tweet.

Markets rebound after Trump appears to soften tone on China tariffs – CBS News

Watch CBS News

The U.S. stock market rebounded on Monday after President Trump appeared to walk back imposing new tariffs on Chinese goods. CBS News senior business and technology correspondent Jo Ling Kent has more.

No two speculative booms are exactly alike, of course, but they share some common elements. Typically, there is great excitement among investors about new technology—in today’s case, A.I.—and its potential to boost profits for companies positioned to take advantage of it. In the twenties, commercial radio was a novel and revolutionary medium: tens of millions of Americans tuned in. Sorkin points out that, between 1921 and 1928, stock in Radio Corporation of America, the Nvidia of its day, went from $1 ½ to $85 ½.

Another hallmark of a stock bubble is that, at some point, its participants largely give up on conventional valuation measures and buy in simply because prices are rising and everybody else is doing it: FOMO rules the day. By some metrics, valuations were even higher during the late-nineteen-nineties internet stock bubble than they were in the late twenties. And according to the latest report from the Bank of England’s Financial Policy Committee, which was released last week, valuations in the U.S. market are, by one measure, “comparable to the peak of the dot-com bubble.” That’s true according to the cyclically-adjusted price-to-earnings (CAPE) ratio, which tracks stock prices relative to corporate earnings averaged over the previous ten years. If, instead of looking back, you focus on predictions of future earnings, valuations are less stretched: the Bank of England report noted that they remain “below the levels reached during the dot-com bubble.” But that’s just another way of saying that investors are betting on earnings growing rapidly in the coming years. And this is a moment when many companies have so far seen precious little return for their A.I. investments.

To be sure, not everyone agrees that stock prices have departed from reality. In a note to clients last week, analysts at Goldman Sachs said the market’s rise, which is heavily concentrated in Big Tech stocks, “has, so far, been driven by fundamental growth rather than irrational speculation.” Jensen Huang, the chief executive of Nvidia, whose chips power A.I. systems at companies such as OpenAI, Google, and Meta, said that he believed the world was at “the beginning of a new industrial revolution.” However, even the authors of the Goldman report acknowledged that there are elements of the current situation “that rhyme with previous bubbles,” including the big gains in stock prices and the emergence of questionable financing schemes. Last month, Nvidia announced it would invest up to one hundred billion dollars over the next decade in OpenAI, the parent company of ChatGPT, which is already a big purchaser of Nvidia’s chips and will likely need more to power its expansion. Nvidia has said OpenAI isn’t obligated to spend the money it invests on Nvidia chips, but the deal, and others like it, have sparked comparisons to the dot-com bubble, when some big tech companies engaged in so-called “circular” transactions that ultimately didn’t work out.

Another recurring feature of the biggest asset booms is outright chicanery, such as fraudulent accounting, the marketing of worthless securities, and plain old stealing. Galbraith referred to this phenomenon as “the bezzle.” In hard times, he noted, creditors are tight-fisted and audits are scrupulous: as a result, “commercial morality is enormously improved.” In boom times, creditors are more trusting, lending standards get debased, and borrowed money is plentiful. But there “are always many people who need more,” Galbraith explained, and “the bezzle increases rapidly,” as it did in the late twenties. “Just as the boom accelerated the rate of growth,” he went on, “so the crash enormously advanced the rate of discovery.”

Sorkin traces the fates of Albert Wiggin and Richard Whitney, who, at the time of the crash were, respectively, the C.E.O. of Chase National Bank and the vice-president of the New York Stock Exchange. Both men were involved in the failed effort, orchestrated by Lamont, to stabilize the market. In 1932, Wiggin went on to become a director of the Federal Reserve Bank of New York. But, during the Pecora investigation, which began that same year, it emerged that, beginning in September of 1929, Wiggin had secretly shorted the stock of his own bank, using a pair of companies he owned to make the trades. He was forced to resign from the Fed. In 1930, Whitney, the scion of a prominent New England family, became the president of the stock exchange, but he was ultimately exposed as an embezzler and served more than three years in Sing Sing.

On being reminded of stories like these, it’s tempting to cast the leaders of nineteen-twenties Wall Street as a bunch of crooks. Sorkin resists the impulse. In an afterword, he writes, “The difficulty is that, other than the disgraced Richard Whitney and Albert Wiggin, it is hard to make the case that any of the era’s other major financial figures did anything appreciably worse than most individuals would have done in their positions and circumstances.” Given the role that Wall Street’s élite played in inflating and promoting the bubble, this is either a generous view or a jaded commentary on the fallen nature of mankind. In any case, though, it’s true that speculative booms tend to take on a life of their own, creating incentives and opportunities that warp people’s judgment at all levels of the economy, from small investors and professional intermediaries to major corporate and financial institutions.

One aspect of the current boom that hasn’t received sufficient attention is how it has extended from the stock market to the credit markets, where there has been enormous growth in so-called “private lending” by non-bank institutions, including private-equity companies, hedge funds, and specialized credit firms. Last week, news organizations reported that the Department of Justice had opened an investigation into the collapse of First Brands, an acquisitive Cleveland-based auto-parts firm that, with Wall Street’s help, had apparently raised billions of dollars in opaque transactions. One creditor told a bankruptcy court that up to $2.3 billion in collateral had “simply vanished,” and called for the appointment of an independent examiner. A lawyer for First Brands said the company denied any wrongdoing and attributed the collapse to “macroeconomic factors” beyond its control.

The sudden demise of a single highly leveraged company that operated in a sector far from the A.I. frontier may be a one-off event, with no broader implications. Or it could conceivably be a harbinger of what lies ahead. We won’t know for a while—perhaps a good while. But in the words of the nineteenth-century English journalist Walter Bagehot, whom Galbraith quoted, “every great crisis reveals the excessive speculations of many houses which no one before suspected.” This time is unlikely to be different. ♦

Stocks are rebounding after President Trump softened his tone on China, easing concerns that trade tensions between the two nations could escalate after he late Friday announced an additional 100% tariff on Chinese imports.

The S&P 500 jumped 96 points, or 1.5%, to 6,637 in morning trade, while the Dow Jones Industrial Average rose 561 points, or 1.2%. The tech-heavy Nasdaq composite gained 1.9%.

Monday’s gains erased some of Friday’s losses, when the S&P 500 shed 2.7%, marking the index’s worst day since April.

On Friday, investors were spooked by Mr. Trump’s announcement of a fresh round of tariffs on imports from China, pointing to new Chinese rules that require companies to get special approval to export products containing rare-earth materials from China.

But on Sunday, Mr. Trump struck a more conciliatory note, writing on social media that “all will be fine” with China and saying that Chinese President Xi Jinping “doesn’t want Depression for his country, and neither do I.”

“Markets woke up Monday to the smell of détente — that familiar scent of risk-on optimism that only comes after a weekend of mutual saber-rattling followed by a wink and a handshake from Washington,” Stephen Innes of SPI Asset Management said in a report.

Yet Friday’s market rout underscores that global trade conflict can still rattle investors, noted Chris Larkin, managing director of trading and investing at E*TRADE from Morgan Stanley, in an email.

“Although the White House appeared to moderate its stance over the weekend, additional flareups still have the potential to trigger sharp responses from the markets,” Larkin said. “Barring additional surprises, though, this week should be about the new earnings season, especially with key inflation data delayed until next week.”

Barring a breakthrough in the U.S. government shutdown, the biggest news of the week will come Tuesday, when U.S. banks kick off earnings season by releasing their most recent quarterly financial results. United Airlines and Johnson & Johnson also report this week.

Chipmakers were some of the biggest gainers in early Monday trading, with Advanced Micro Devices gaining 3.4% and Micron jumping 4.9%. Broadcom and Nvidia each gained closed to 3%.

History suggests three years is still “young” compared to the other bull runs.

There have been 11 other bull markets since World War II, and only once did a bull make it this far without reaching its fourth anniversary.

“Just remember, prior bulls that made it this far had many years left,” Detrick said.

While some Wall Street strategists point to elevated valuations and dot-com comparisons as reason to believe the rally will soon end, the AI trade continues to accelerate and recession fears have dwindled all year.

Unprecedented Big Tech strength, however, has created a narrow and top-heavy market.

The equal-weight S&P 500, for instance, has underperformed the traditional market-cap weighted benchmark over the last three years.

A few details on the performance gap:

A handful of mega-cap drive the market

Index-fund investors are increasingly concentrated

Breadth remains weak even as the index hits records

The average S&P 500 stock has seen modest returns

Depending how optimistically you view the data, you could see all of the above as a signal of resilience or fragility — resilience because the top is so strong, fragility because leadership is so narrow.

Broader economic factors like the Federal Reserve, disruptions in Washington, and geopolitical uncertainty have done little to discourage investors so far.

As far as the central bank, markets see multiple rate cuts heading into 2026.

The outlook remains paradoxical. Good news for the economy isn’t necessarily good news for stocks.

If the economy does get stronger, it could mean fewer rate cuts are needed and so dampen investor enthusiasm.

If growth slows, it could push policymakers to cut rates more than expected — which could push stocks higher.

“Something has to give,” said Seth Carpenter, chief global economist for Morgan Stanley. “If the economy is strong, the market is expecting too many cuts, and if the economy is weak, earnings are likely not as good as hoped.”

After nearly a decade spent studying the most famous stock market crash in history, financial journalist Andrew Ross Sorkin warns that the Wall Street of today echoes the market of 1929, when highs preceded a massive slump, leading to the Great Depression.

Artificial intelligence and technology have contributed to a remarkable boom in recent years. But, Sorkin said, today’s economy is being propped up by the AI boom, and it’s too soon to tell if this is a sugar rush, a short-term and unsustainable boost to the markets. But, Sorkin is positive there’s a crash coming.

“I just can’t tell you when, and I can’t tell you how deep,” he said. “But I can assure you, unfortunately, I wish I wasn’t saying this, we will have a crash.”

The Roaring ’20s

Despite a tumble this Friday, stocks on Wall Street have shot up in recent months. Still, some investors are getting weak in the knees, fearing stocks are overheated. Sorkin, author of “1929: Inside the Greatest Crash in Wall Street History – and How It Shattered a Nation,” out Oct. 14, says the U.S. is in a new roaring 20s, the 2020s, with stocks pushing to record highs, just as they were in the 1920s.

Market highs today have him feeling anxious.

“I’m anxious that we are at prices that may not feel sustainable. And what I don’t know is we are either living through some kind of remarkable boom and part of that’s artificial intelligence and technology, and all of that, or everything’s overpriced,” he said.

Andrew Ross Sorkin and Lesley Stahl at the NYSE

60 Minutes

The market of 1929 was fueled by rampant speculation, including by ordinary investors unaware of the mounting risks, and of heavy borrowing. People of modest means were lured by Wall Street bankers and other stock market touts to invest using what was then a newfangled concept: credit. It was called buying on a margin. You only had to put down 10% of the stock price, borrowing the rest from your banker.

Before 1919, most people did not take on credit or debt, influenced by religious views and moral norms against borrowing money, Sorkin said. That changed when General Motors, in 1919, started lending people money so they could afford to buy the company’s cars. It changed out Americans shopped.

“And then the bankers realize what’s happening, and they realize that they can lend out money so that more folks can buy stocks. It was all sort of wrapped in the flag of democratizing access,” Sorkin said. “And in good times, when the stock is going up, it’s like free money. In bad times, you’re on the hook, and you’re on the hook in a very bad way.”

Today, it’s hundreds of billions being invested in AI, with some investment pros warning of a possible bubble as stocks soar to stratospheric heights even amid significant economic uncertainty, such as Friday’s slide after President Trump threatened more China tariffs.

“I think it’s hard to say we’re not in a bubble of some sort,” Sorkin said. “The question is always when is the bubble going to pop?”

Protecting consumers in the market

When things got out of control in 1929, frightened traders dumped stocks as investors lost their businesses and homes. In the years since, laws, regulations and agencies have been put in place to protect investors.

Some of those barriers to prevent exploitation are now coming down, Sorkin said. U.S. Securities and Exchange Commission rules have become less stringent and “the Consumer Protection Bureau practically doesn’t exist anymore.”

“That’s what concerns me,” Sorkin said. “It’s not that we’re going off a cliff tomorrow. It’s that there’s speculation in the market today, there’s an increasing amount of debt in the market today, and all of that’s happening against the backdrop of the guardrails coming off.”

Those guardrails include ones that allow only the wealthy to invest directly in private companies that have fewer regulations, like AI startups before they go public.

In recent decades, people who could invest in private equity and venture capital outperformed investors who did not. Those kinds of assets, generally restricted to wealthy investors, are potentially more rewarding, but also riskier.

“Public companies, after the SEC was created, were required to have all sorts of disclosure rules so that the public could understand what’s going on inside them. Private companies don’t have that,” Sorkin said. “But historically, the average ordinary American wasn’t really allowed to invest in the private companies. But in this flag of democratizing finance, there’s a lot of people who want access to that.”

Some people feel elite investors have better access, while others are unable to get in early on opportunities, Sorkin said. There’s been a push by both the Trump administration and the financial sector to open up the market to more people.

But that would also require moving the guardrails designed to protect people.

“They have protected a lot of people, but some people would say they protected people from getting rich,” Sorkin said.

Push today for democratizing investing

In his latest annual letter to investors, BlackRock CEO Larry Fink suggested opening retirement 401(k)s to riskier private investments in the name of democratizing investing. He said there were opportunities for investing in AI or data centers.

Right now money managers are precluded from investing in those types of assets in many retirement products, but the Trump administration is in the process of changing that, Fink explained.

The new investment opportunity comes with risk.

“But everything is risky other than keeping your money in a bank account overnight,” Fink said.

Larry Fink, CEO of Blackrock

60 Minutes

Fink, who once called bitcoin the domain of money launderers and thieves, also wants to add crypto to investment portfolios.

“The markets teach you, you have to always relook at your assumptions,” he said. “There is a role for crypto in the same way there is a role for gold — that is, it’s an alternative.”

He sees it, as he does AI, as an opportunity to add diversity to a portfolio.

But Sorkin says some crypto products, like meme coins, can be abused in ways similar to 1929, with speculators sending the value of cryptocurrencies soaring before they come crashing down. Sorkin has his own personal example involving a television appearance with Fink.

“He makes a joke, I think, about how there should be a Sorkin coin. Well, two hours later, somebody makes a Sorkin coin. And all of a sudden, this Sorkin coin is now worth millions of dollars. And I’m watching it,” Sorkin said.

The Sorkin coin peaked at $170 million worth of trading in a day.

“And I think today it does something like $20 or $21 a day,” Sorkin said.

Stocks took a nosedive on Friday after President Trump threatened a big tariff hike on China. Until then, Wall Street had been at record highs for months, which is why we decided to check in with Andrew Ross Sorkin, one of the country’s most influential financial reporters.

He’s just written a book called “1929” about the market crash a century ago. We wondered if he’d run out of news to cover, oris he alerting us that what’s been happening in the markets lately – is a replay of what led to the most devastating financial collapse in our history?

Imagine the New York Stock Exchange back then: the crush of frightened traders dumping stocks, investors losing their shirts, businesses, their homes, sweeping away the Roaring ’20s, walking that same but transformed floor today.

Andrew Ross Sorkin: Everything’s digital.

Lesley Stahl: Well, yeah, OK.

Andrew Ross Sorkin says we’re in our own roaring ’20s: the 2020s. with stocks climbing for months, just like then.

Andrew Ross Sorkin: The crazy part about this is, from 1928 to September of 1929, the stock market was up 90%!

Lesley Stahl: When you say the stock market was way up, immediately I think of now. Are you scared?

Andrew Ross Sorkin: I’m anxious. I’m anxious that we are at prices that may not feel sustainable. And what I don’t know is we are either living through some kind of remarkable boom and part of that’s artificial intelligence and technology and all of that, or everything’s overpriced.

Lesley Stahl: Or we’re reliving–

Andrew Ross Sorkin: 1929.

Andrew Ross Sorkin: There was so much anxiety.

Andrew Ross Sorkin and Lesley Stahl at the NYSE

60 Minutes

Sorkin has covered the markets for two decades. He joined the New York Times after college, soon founding the DealBook newsletter covering finance. He also co-hosts “Squawk Box” on CNBC, runs the DealBook Summit, where he interviews the high and mighty, he co-created “Billions” the TV show, wrote a bestseller about the 2008 crash, and now, a book about 1929.

Lesley Stahl: We’re always being undone by bubbles. There was the internet bubble in 2000, the housing in 2008. Are we in another bubble? An AI bubble or something like that?

Andrew Ross Sorkin: I think it’s hard to say we’re not in a bubble of some sort. The question is always when is the bubble going to pop?

Lesley Stahl: One symptom of a bubble is when the market goes up and up, but the underlying economy – the real economy – goes soft. And that appears to be happening right now.

Andrew Ross Sorkin: I would argue to you that the economy is being propped up, almost artificially, by the artificial intelligence boom. There are hundreds of billions of dollars that are being invested today in artificial intelligence. This is either a gold rush or a sugar rush and we probably won’t know for a couple of years which one it is.

1929 was a sugar rush caused by speculation and debt. People who didn’t really have much money were lured by Wall Street bankers to invest using a newfangled concept to take on debt, called credit. You only had to put down 10% of the stock price, borrowing the rest from your broker.

Andrew Ross Sorkin: Prior to 1919, most people did not take on credit or debt at all. It was a sin. It was a moral sin to use credit–

Lesley Stahl: Oh, really?

Andrew Ross Sorkin: –to buy anything. And it was really General Motors that basically came up with the idea that we’re gonna lend you money so you can afford to buy our cars.

Lesley Stahl: Brilliant.

Andrew Ross Sorkin: And then the bankers realize what’s happening, and they realize that they can lend out money so that more folks can buy stocks. It was all sort of wrapped in the flag of democratizing access. And in good times, when the stock is going up, it’s like free money. In bad times, you’re on the hook, and you’re on the hook in a very bad way.

Since then, laws, regulations, and agencies have been put in place to protect investors – especially the less affluent – from being exploited.

Lesley Stahl: We put up barriers after 1929.

Andrew Ross Sorkin: Yes.

Lesley Stahl: Protections.

Andrew Ross Sorkin: Yes.

Andrew Ross Sorkin

60 Minutes

Lesley Stahl: So those are coming down. They’re tumbling down one — the SEC rules aren’t as stringent anymore.

Andrew Ross Sorkin: Yes. The Consumer Protection Bureau practically doesn’t exist anymore.

Lesley Stahl: Correct.

Andrew Ross Sorkin: That’s what concerns me. It’s not that we’re going off a cliff tomorrow. It’s that there’s speculation in the market today, there’s an increasing amount of debt in the market today, and all of that’s happening against the backdrop of the guardrails coming off.

Including guardrails that allow only the wealthy to invest directly in private companies that have fewer regulations, like AI startups before they go public.

Andrew Ross Sorkin: So over the last 20 or 30 years, folks who had access to, who could invest in private equity, in venture capital, clearly outperformed folks who didn’t. And so–

Lesley Stahl: That’s how you really made money. But you have to remember that these kind of assets are gambles.

Andrew Ross Sorkin: Public companies, after the SEC was created, were required to have all sorts of disclosure rules so that the public could understand what’s going on inside them. Private companies don’t have that. But historically, the average ordinary American wasn’t really allowed to invest in the private companies. But in this flag of democratizing finance, there’s a lot of people who want access to that.

Lesley Stahl: Wow.

Andrew Ross Sorkin: Isn’t this something?

Lesley Stahl: This is spectacular.

Sorkin took us to the Fifth Avenue mansion of one of the big bankers back then, who pushed democratization.

Andrew Ross Sorkin took 60 Minutes to the Fifth Avenue mansion of one of the big bankers back then, who pushed democratization.

60 Minutes

Lesley Stahl: If this idea of bringing a regular guy into buying stock, if that was a big problem back in 1929 why are we going there again? Doesn’t it defy some kind of logic?

Andrew Ross Sorkin: There is a view that it’s been only the elites that have had access to these investments, Facebook before it ever went public, Uber before it went public. So there is this idea that it’s unfair, actually, to the ordinary investor because we haven’t allowed them to get access to some of these investment opportunities early. And there is a real push, partially by the Trump administration, partially by the industry itself, which wants to–

Lesley Stahl: Get more money.

Andrew Ross Sorkin: Get more money in– to open up the market to more and more people.

Lesley Stahl: So we have these guardrails for a reason. I mean, they’re there to protect, and they have protected.

Andrew Ross Sorkin: They have protected a lot of people, but some people would say they protected people from getting rich.

Larry Fink: Many people don’t believe in capitalism anymore. And I think a lot of it is because they were not a part of the growth of the economy.

We went to Larry Fink, CEO of Blackrock, the world’s biggest money manager, handling $12.5trillion in assets, like pension funds. His annual letter to investors is a kind of industry roadmap. This latest one he suggested opening our retirement 401(k)s – bastions of caution – to riskier private investments in the name of, wait for it: democratizing investing.

Larry Fink: As I wrote, there are many great opportunities to be investing in the s- in startup companies, to invest in AI or data centers. Right now, we’re precluded to put those type of assets in many retirement products. And the Trump administration has now said we’re going to allow in our 401(k) products the opportunity to invest in these private markets.

Lesley Stahl: But, they are risky. Aren’t they?

Larry Fink: Yes. But everything is risky other than keeping your money in a bank account overnight.

Lesley Stahl: But we’re talking about 401(k)s.

Larry Fink: Yes.

Lesley Stahl: Investing out of retirement accounts.

Larry Fink: Yes.

Lesley Stahl: You’re risking the nest egg or part of the– a little part of the nest egg.

Larry Fink: But what the markets will teach you over the last 100 years, even at the worst moments, if you have the ability to persevere and you have a long-term horizon, you’re going to do fine. And a diversified portfolio is essential. We’re not suggesting, you know, one shoe fits all. We are suggesting the opportunity to have that ability to invest in these private market investments.

Larry Fink, CEO of Blackrock

60 Minutes

He also believes we should be investing in crypto.

Lesley Stahl: It wasn’t that long ago that the big bankers, Jamie Dimon and Larry Fink, were saying that crypto was stupid and a fraud.

Larry Fink: I did say Bitcoin, because we were talking about Bitcoin then, was the domain of money launderers and thieves. But you know, the markets teach you, you have to always relook at your assumptions. There is a role for crypto in the same way there is a role for gold, that is it’s an alternative. For those looking to diversify this is not a bad asset, but I don’t believe that it should be a large component of your portfolio.

But Sorkin says some crypto can be abused in ways similar to 1929. Take meme coins: cryptocurrencies that can be manipulated by speculators who pumped them up, then let them crash.

Andrew Ross Sorkin: There are a number of examples where it felt like there was an inside group of people who were colluding to pump up some of these cryptocurrencies, and other things. I’ll give you a bizarre story of my own. I was on television with Larry Fink, and he makes a joke, I think, about how there should be a Sorkin coin. Well, two hours later, somebody makes a Sorkin coin. And all of a sudden, this Sorkin coin is now worth millions of dollars. And I’m watching it.

Lesley Stahl: Are you serious?

Andrew Ross Sorkin: Go up, and up, and up, and up, and up.

The sorkin coin peaked at $170 million worth of trading in a day.

Andrew Ross Sorkin: And I think today it does something like $20 or $21 a day, so…

Lesley Stahl: [makes spiral noise]

Sorkin is trusted by the world’s top business leaders, who talk to him often exclusively.

Lesley Stahl: What role do you think these business leaders should be playing now?

Andrew Ross Sorkin: My own view is that most CEOs in America today are very scared to speak out publicly about anything. They are so worried that they are going to be potentially attacked by the administration, or regulated. They’re gonna have a merger in front of some agency that’s not gonna be allowed to go through. They are so nervous about criticizing anything that’s going on with this administration.

Lesley Stahl: There are some economists who suggest that because Mr. Trump ties his success to the success of the market, that he’s not gonna let anything like what happened in 1929 happen. And that we should feel secure because of that.

Andrew Ross Sorkin: I think it’s hard to know how things get out of control. When confidence disappears, it happens like this. [SNAP]

Lesley Stahl: So, you spent nearly 10 years on this book. The inevitable question is: do you think that we will have a crash or not?

Andrew Ross Sorkin: The answer is we will have a crash; I just can’t tell you when, and I can’t tell you how deep. But I can assure you, unfortunately, I wish I wasn’t saying this, we will have a crash.

Produced by Shachar Bar-On. Associate producer, Jinsol Jung. Broadcast associate, Aria Een. Edited by Sean Kelly.

Trump announces additional 100% tariff on China starting next month – CBS News

Watch CBS News

President Trump says the U.S. is imposing an additional 100% tariff on imports from China starting Nov. 1. Today’s announcement follows heavy losses on the stock market. CBS News MoneyWatch correspondent Kelly O’Grady reports.

Cineplex says box office revenue for the third quarter totalled $159.5 million, down from $174.9 million a year earlier.

Cineplex chief executive Ellis Jacob says outside a tough comparative last August, with the release of Deadpool & Wolverine, the third-quarter box office performed well compared with a year ago. He added that the success of Taylor Swift, The Official Release Party of A Showgirl last weekend marked a dynamic start to the fourth quarter.

Cineplex has 171 movie theatres and entertainment venues across Canada.

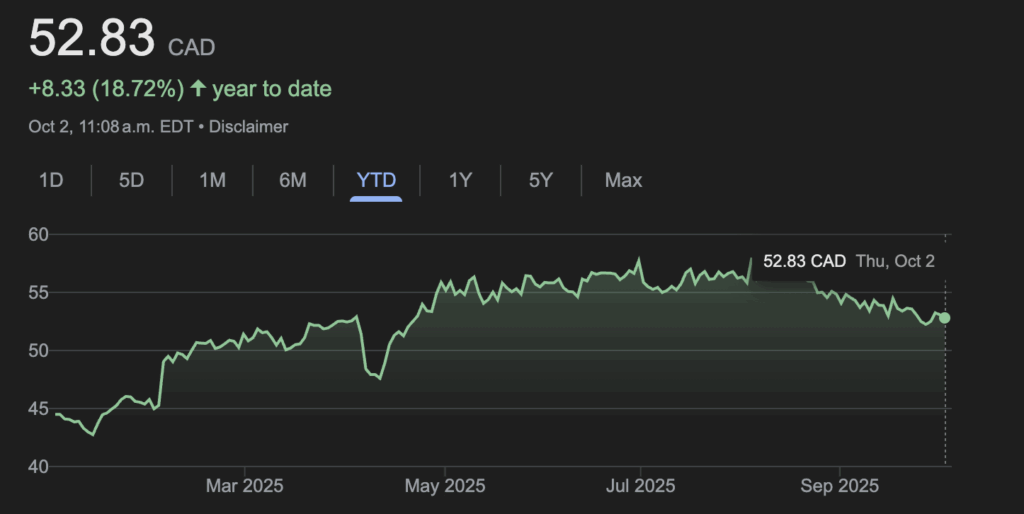

Aritzia’s Q2 profit surge driven by U.S. customer growth, operational changes: CEO

Artizia Inc. (TSX:ATZ)

Numbers for its second quarter of 2025:

Profit: $66.3 million (up from $18.2 million a year ago)

Sales: $812.1 million (up from $615.7 million)

Aritzia Inc. said strength in its U.S. business and moves to avoid higher shipping fees boosted its latest quarterly results. “We’ve seen outstanding new customer growth in the United States, where our base of loyal clients expands quarter after quarter. We’re also super pleased with our second-quarter results in Canada,” Aritzia CEO Jennifer Wong told analysts on a call Thursday.

The Vancouver-based clothing retailer reported $66.3 million in net income during its second quarter, up from $18.2 million during the same period last year. Its net revenue rose by almost a third to $812.1 million, from $615.7 million during the same period a year earlier.

The company said its U.S. net revenue rose more than 40 per cent to $486.1 million, accounting for just under 60 per cent of its total revenue. Wong also noted the company launched a new international e-commerce platform in August, which she said was fuelling higher revenue growth. “Its performance in the first six weeks has meaningfully exceeded our expectations, and we’re confident we’ll hit our target to triple sales within two years or less,” she said.

In August, the U.S. ended what’s known as the de minimis exemption, which had allowed packages worth $800 or less to ship south of the border without duties. “Previously, under the de minimis exemption, we utilized our existing supply chain network in Canada to fulfil a portion of U.S. e-commerce orders. However, the removal of the de-minimis exemption in August required an operational pivot,” Wong said.

She said the company relocated all U.S. order fulfilment to its Ohio distribution centre, which was expanded last year to more than double its previous size. Wong said the company hired additional staff at the facility.

Article Continues Below Advertisement

“Despite headwinds from the elimination of the de minimis and higher reciprocal tariff rates on Vietnam and Cambodia, our proactive mitigation strategies and strong revenue growth have positioned us very well,” she said. “As a result, our margin outlook for fiscal 2026 is unchanged at 15.5 to 16.5 per cent. We’re leveraging our agile global supply chain to minimize tariff exposure where possible.”

Todd Ingledew, Aritzia’s chief financial officer, said that due to the retailer’s year-to-date performance and improved expectations for the second half of the year, it is raising its net revenue forecast for the full fiscal year to between $3.3 billion and $3.5 billion. In its first-quarter report in January, Aritizia had predicted net revenue of $3.1 billion to $3.25 billion.

For the second quarter, Aritzia’s net income per diluted share came in at 56 cents compared to 16 cents per diluted share a year earlier. On an adjusted basis, Aritzia’s net income amounted to $69.8 million, rising from $24.5 million during the second quarter of last year.

U.S. government to take 10-per-cent stake in Canadian mining company Trilogy Metals

Vancouver-based Trilogy Metals Inc. (TSX:TMQ) says the U.S. government will take a 10% stake in the mineral exploration company, which has mining interests in Alaska that Washington wants to see developed. The U.S. government is spending US$35.6 million on the stake, and has options to increase it further in the future. The transaction remains subject to regulatory and other approvals.

The announcement comes as U.S. President Donald Trump signed an executive order that directs a road to be built in Alaska allowing access to the Ambler mining district, an area rich in copper where Trilogy Metals has an interest through a joint venture. The long-debated Ambler Road project was approved in the first Trump administration, but was later blocked by the Biden administration after an analysis determined the project would threaten caribou and other wildlife and harm Indigenous peoples that rely on hunting and fishing.

“This proposed partnership with the U.S. Government represents a significant milestone for Trilogy Metals and for the development of a secure, domestic supply of critical minerals for America in Alaska,” Trilogy Metals CEO Tony Giardini said in a news release. The partnership interest underscores the strategic importance of Trilogy’s Upper Kobuk Mineral Projects in supporting U.S. energy, technology, and national security priorities, he said.

U.S. Secretary of the Interior Doug Burgum said the investment will help secure critical mineral supplies.

“They’re (Trilogy Metals) one of the companies that has mining claims in this area that is a remote wilderness right now, and again making that investment so we can make sure that we’re securing these critical mineral supplies and that ownership in that company will benefit the American people,” he said.

President Trump is steering the White House into the unusual territory of an investment firm.

The administration revealed a 10 percent stake in Trilogy Metals that sent the stock price for the tiny Canadian mining company up nearly 300 percent over the last 48 hours. It’s the latest in a string of bets that underscore America’s shift away from regulation and toward ownership.

Over the last few months, the U.S. government has also taken positions in Intel, MP Materials, and Lithium Americas.

An Inc.com Featured Presentation

Alongside Trilogy Metals, each of those companies operate at the heart of the semiconductor and critical minerals supply chains that are powering the artificial intelligence boom.

The approach marks a departure from the previous administration’s inkling for tax incentives, subsidies and regulations and instead mirrors something like a venture-capital strategy.

The share prices for these four companies have skyrocketed in kind.

To be clear, the White House isn’t necessarily picking industry-leading companies. But because the White House picks them, investors are repositioning as if these names will emerge as winning bets.

The four picks so far reflect the administration’s focus on the energy and materials needed to compete in the AI race, though some commentators have compared the entire strategy to that of China’s state-backed markets model.

As part of the Trilogy Metals deal, President Trump also approved a permit for a mining road in northwest Alaska, which the administration believes will unlock “the minerals we need to win the AI arms race against China,” according to Interior Secretary Doug Burgum.

In any case, the consequences aren’t yet clear as to the long-term effects of the government participating in the market it’s supposed to oversee.

Yet while the line between national security and financial interests have blurred, that hasn’t discouraged investors.

Now, is it really so surprising that a White House endorsement would move stocks this much? The returns have become impossible to ignore.

If you bought shares of Intel the day before the government announced its stake in August, for example, you would have doubled your money by now.

It’s possible the administration will still expand its portfolio across the energy and defense sectors, which opens up more lanes to speculate which company could see the next triple-digit surge.

For some opportunistic investors, the easiest new strategy this year may just be “buy what the White House buys.”

The S&P 500 and home prices are at record highs, but when you price them in hard assets instead of dollars the “everything rally” disappears.

If you measure prices in dollars, this looks like the golden age for wealth. Nearly every asset class hovers at record highs. Yet that illusion fades once you look past nominal dollars to real purchasing power.

Since 2020, the US dollar’s purchasing power has fallen more than 20 percent while cumulative inflation has increased 25 percent. Meanwhile, the S&P 500 is up 106 percent, and home prices, as measured by the S&P Case-Shiller Home Price Index, have appreciated 52 percent.

An Inc.com Featured Presentation

That conundrum also explains why everyday Americans continue to feel downbeat about the economic outlook.

The record highs investors celebrate are as much a byproduct of a shrinking yardstick as genuine value creation.

Despite the S&P 500 doubling in nominal terms over the last five years, it’s collapsed in bitcoin terms, and remains down 13 percent when priced in gold.

The same pattern holds for home prices denominated in bitcoin and gold.

As the charts illustrate, this dynamic is not new, though the majority of global investors still haven’t caught on.

It was only last week JPMorgan strategists led by Nikolaos Panigirtzoglou published a note citing the “debasement trade” — the rise of gold and bitcoin in the face of persistent government deficits, inflation, and waning faith in fiat currencies.

Indeed, retail inflows into hard-asset ETFs have steadily increased while institutional positioning has lagged, suggesting the shift is being driven from the ground up, rather than top down.

Equity and property investors have been able to outpace currency debasement over the last five years, and that appears unlikely to change anytime soon.

Markets will continue to secure new all-time highs, though only in nominal terms. The debasement trade, now that it’s been formalized by JPMorgan, simply gives a name to what’s already been unfolding for years.

As long as the U.S. dollar remains in a structural bear market, the bull market in asset prices will keep feeling stronger than it actually is.

Maple Leaf Foods is keeping a 16 per cent stake in Canada Packers and the two companies have entered into an evergreen supply agreement. It will also be an anchor customer for Canada Packers which will supply pork for its prepared meats business.

Michael McCain, executive chair at both companies, says Maple Leaf Foods and Canada Packers are moving forward as independent entities, each with a clear investment profile and experienced teams. He says the McCain family and McCain Capital Inc. are fully committed to the future of both companies.

TMX Group acquires U.S.-based data and analytics provider Verity

TMX Group (TSX:X) says it has acquired Verity, an investment research management system, data, and analytics provider. Financial terms of the agreement were not immediately available.

Verity has two core products. VerityRMS is a research management system, while VerityData offers enhanced data sets and insights primarily focused on public equity filings.

TMX Datalinx president Michelle Tran says the addition of Verity strengthens the company’s ability to serve a growing global client base.

TMX Group is the operator of the Toronto Stock Exchange and other markets.

MEG Energy says Glass Lewis recommends shareholders back Cenovus offer

MEG Energy Corp. (TSX:MEG) says a second major independent proxy advisory firm has recommended its shareholders back a takeover offer for the company by Cenovus Energy Inc. (TSX:CVE). The company says Glass, Lewis & Co. has issued a report recommending shareholders vote for the cash-and-stock offer by Cenovus over a rival all-stock offer by Strathcona Resources Ltd.

The report comes after proxy advisory firm Institutional Shareholder Services Inc. said last week that MEG shareholders should support the Cenovus bid.

Article Continues Below Advertisement

The Cenovus offer must be approved by a two-thirds majority vote by MEG shareholders, expected to be held on Oct. 9. Strathcona (TSX:SCR) has said it intends to vote its 14.2 per cent interest in MEG against the deal.

Cenovus and MEG have side-by-side oilsands properties at Christina Lake, south of Fort McMurray, Alta., while Strathcona also has operations in the region.

Stella-Jones signs deal to buy Brooks Manufacturing for US$140 million

Utility pole company Stella-Jones Inc. (TSX:SJ) has signed a deal to buy U.S.-based Brooks Manufacturing Co. for US$140 million.

Brooks is a maker of treated wood distribution crossarms and transmission framing components. It was founded in 1915 and operates a facility in Bellingham, Wash.

Stella-Jones chief executive Eric Vachon called the acquisition a natural fit. “The addition of Brooks bolsters Stella-Jones’ suite of solutions, enhancing its ability to meet the growing demand of utilities and unlock new growth opportunities,” Vachon said in a statement Tuesday. “The acquisition reflects our strategic focus and aligns with our vision to make Stella-Jones a partner of choice to our infrastructure customers.”

Brooks’ sales for 2024 totalled about US$84 million.

RBC Capital Markets analyst James McGarragle called the deal a “strategically positive move.” “It creates a valuable growth platform for Stella-Jones by diversifying its product offering and leveraging Brooks’ established brand and customer relationships,” McGarragle wrote in a note to clients. “Furthermore, the acquisition aligns with Stella-Jones’ long-term strategic objectives to expand beyond traditional product categories and accelerate growth in the infrastructure segment, positioning the company to capitalize on ongoing investments in utility modernization.”

The deal is subject to closing conditions, including U.S. regulatory approval, and is expected to occur by the end of the year. The deal for Brooks follows the acquisition by Stella-Jones of Locweld Inc., a designer and manufacturer of lattice transmission towers and steel poles, earlier this year.

Investors bought the dip on the government shutdown.

On Wednesday, the S&P 500 closed above 6,700 for the first time ever, securing its 29th record-high of the year after US lawmakers failed to avert the closure of the federal government.

Stocks traded lower to start the trading session but reversed course to close the day in the green.

An Inc.com Featured Presentation

But that resilience matches history. Equities have finished higher across the five government shutdowns seen since 1995. In January 2019, the longest funding gap on record at 22 trading days, the S&P 500 advanced more than 10 percent.

Wednesday’s record high signals that either investors are betting on a brief and so inconsequential shutdown, or they simply can’t be bothered to care.

After all, earnings remain robust, the AI trade is only accelerating and recession odds continue to dwindle.

Still, the shutdown does prevent key data releases, including the September jobs report due Friday. But given the collapse in response rates to government surveys and diminishing credibility of official data, this is a less consequential detail than years past.

As much as the Federal Reserve, politicians and media pay attention to Labor Department reports, investors increasingly rely on private-sector gauges like ADP’s payroll report or more modern measures from firms like Indeed and LinkedIn.

To be clear, alternative indicators point to a slowing labor market with minimal hiring. ADP just reported a decline of 32,000 jobs in September, marking the weakest print since March 2023 and well below expectations for an increase of 45,000.

The irony, though, is that the shutdown seems to be juicing the market’s bullish impulse, regardless of a potential blackout on economic data.

Without the establishment jobs report, there are fewer catalysts available to challenge the prevailing narrative of strong earnings and imminent rate cuts.

CME data shows 99 percent and 87 percent odds for a quarter-point cut in October and December, respectively.

The market’s reaction to the shutdown reflects the opportunism of Wall Street. With Washington in gridlock, investors actually face even less friction to push against the bullish story that’s been driving asset prices higher.

It seems that in the potential absence of government data, traders are choosing to default to the trend that’s playing out right in front of them — more record highs, AI-fueled earnings, and a growth story that’s put bears on the wrong side of the tape all year.

Stocks closed at record highs Wednesday despite a U.S. government shutdown expected to idle hundreds of thousands of workers and hobble federal agencies charged with dispensing a range of critical services. So why do investors seem unfazed?

Although shutdowns have serious, real-world consequences for millions of Americans, data shows they tend to have a modest impact on financial markets and the broader economy, especially if the closure is brief.

“Most of the economic activity is delayed and usually gets made up shortly after a shutdown ends,” Sameer Samana, senior global market strategist at Wells Fargo Investment Institute, told CBS News. “So I can’t imagine this will be anything terribly disruptive for the equity markets.”

Over the previous 22 shutdowns the U.S. has seen since 1976, the S&P 500 rose during some of the closures while rising at other times. Overall, the stock index gained an average of 0.3% during the episodes, according to an analysis from Carson Group (see following chart).

What’s more, the stock index jumped 13% on average in the 12 months following the shutdowns, the asset management firm found.

“Government shutdowns are inconvenient and messy, but there is little evidence that they have a significant impact on the economy,” said Scott Helfstein, head of investment strategy at investment firm Global X, in a report.

During the longest shutdown in U.S. history, which started in December of 2018 and extended into January of the following year, some 800,000 federal workers were furloughed or worked without pay. That put many employees under severe financial pressure, driving some to food banks and others to launch online fundraising campaigns.

Yet for the $30 trillion U.S. economy as a whole, that lost income amounted to a drop in the bucket, noted Thomas Ryan, North America economist at investment advisory firm Capital Economics. Consumption across the U.S. dipped for the two months the government remained shuttered, but quickly recovered.

With Wall Street shrugging off the headlines, the S&P 500 closed up 0.3% on Wednesday, topping the all-time high it set last week. The blue-chip Dow Jones Industrial Average also finished in record territory.

Why this time could be different

The caveat? History is a guide — not a guarantee that events will follow the same script. The political dynamics shaping the latest meltdown in Congress obviously differ from previous eras, making it hard to predict how long the latest shutdown will last. An impasse lasting a month or more would fuel market uncertainty and could shake investor confidence, according to Wall Street analysts.

“Right now uncertainty is picking up again with new tariffs announced last week, and this just adds to it, which can paralyze growth for the foreseeable future,” economist Daniel Altman and author of newsletter High Yield Economics, told CBS News. “It makes it harder for stocks to continue rising if nobody knows what the fiscal picture is going to be like for the next year.”

If the shutdown drags on, companies could also press pause on making investment and hiring decisions, which would weigh on stock prices, Altman said.

The latest closure will have another immediate impact that could fray investor nerves — halting the flow of economic reports that economists use to assess everything from the rate of inflation to the pace of job growth.

Without critical economic data, investors could start to feel like they are “flying blind,” Vital Knowledge market analyst Adam Crisafulli said in a report.

Megan Cerullo is a New York-based reporter for CBS MoneyWatch covering small business, workplace, health care, consumer spending and personal finance topics. She regularly appears on CBS News 24/7 to discuss her reporting.