[ad_1]

The results announced late Wednesday provided a pulse check on the frenzied spending on AI technology that has been fueling both the stock market and much of the overall economy since OpenAI released its ChatGPT three years ago.

Nvidia has been by far the biggest beneficiary of the run-up because its processors have become indispensable for building the AI factories that are needed to enable what’s supposed to be the most dramatic shift in technology since Apple released the iPhone in 2007. But in the past few weeks, there has been a rising tide of sentiment that the high expectations for AI may have become far too frothy, setting the stage for a jarring comedown that could be just as dramatic as the ascent that transformed Nvidia from a company worth less than $400 billion three years ago to one worth $4.5 trillion at the end of Wednesday’s trading.

Nvidia’s report for its fiscal third quarter covering the August-October period elicited a sigh of relief among those fretting about a worst-case scenario and could help reverse the recent downturn in the stock market.

“The market should belt out a heavy sigh, given the skittishness we have been experiencing,” said Sean O’Hara, president of the investment firm Pacer ETFs.

The company’s stock price gained more than 5% in Wednesday’s extended trading after the numbers came out. If the shares trade similarly Thursday, it could result in a one-day gain of about $230 billion in stockholder wealth.

Nvidia earned $31.9 billion, or $1.30 per share, a 65% increase from the same time last year, while revenue climbed 62% to $57 billion. Analysts polled by FactSet Research had forecast earnings of $1.26 per share on revenue of $54.9 billion. What’s more, the Santa Clara, California, company predicted its revenue for the current quarter covering November-January will come in at about $65 billion, nearly $3 billion above analysts’ projections, in an indication that demand for its AI chips remains feverish.

The incoming orders for Nvidia’s top-of-the-line Blackwell chip are “off the charts,” Nvidia CEO Jensen Huang said in a prepared statement that described the current market conditions as “a virtuous cycle.” In a conference call, Nvidia Chief Financial Officer Collette Kress said that by the end of next year the company will have sold about $500 billion in chips designed for AI factories within a 24-month span Kress also predicts trillions of dollars more will be spent by the end of the 2020s.

In a conference call preamble that has become like a State of the AI Market address, Huang seized the moment to push back against the skeptics who doubt his thesis that technology is at tipping point that will transform the world. “There’s been a lot of talk about an AI bubble. From our vantage point, we see something very different,” Huang insisted while celebrating “depth and breadth” of Nvidia’s growth.

The upbeat results, optimistic commentary and ensuring reaction reflects the pivotal role that Nvidia is playing in the future direction of the economy — a position that Huang has leveraged to forge close ties with President Donald Trump, even as the White House wages a trade war that has inhibited the company’s ability to sell its chips in China’s fertile market.

Trump is increasingly counting on the tech sector and the development of artificial intelligence to deliver on his economic agenda. For all of Trump’s claims that his tariffs are generating new investments, much of that foreign capital is going to data centers for AI’s computing demands or the power facilities needed to run those data centers.

“Saying this is the most important stock in the world is an understatement,” Jay Woods, chief market strategist of investment bank Freedom Capital Markets, said of Nvidia.

The boom has been a boon for more than just Nvidia, which became the first company to eclipse a market value of $5 trillion a few weeks ago, before the recent bubble worries resulted in a more than 10% decline. As OpenAI and other Big Tech powerhouses snap up Nvidia’s chips to build their AI factories and invest in other services connected to the technology, their fortunes have also been soaring. Apple, Microsoft, Google parent Alphabet Inc. and Amazon all boast market values in the $2 trillion to $4 trillion range.

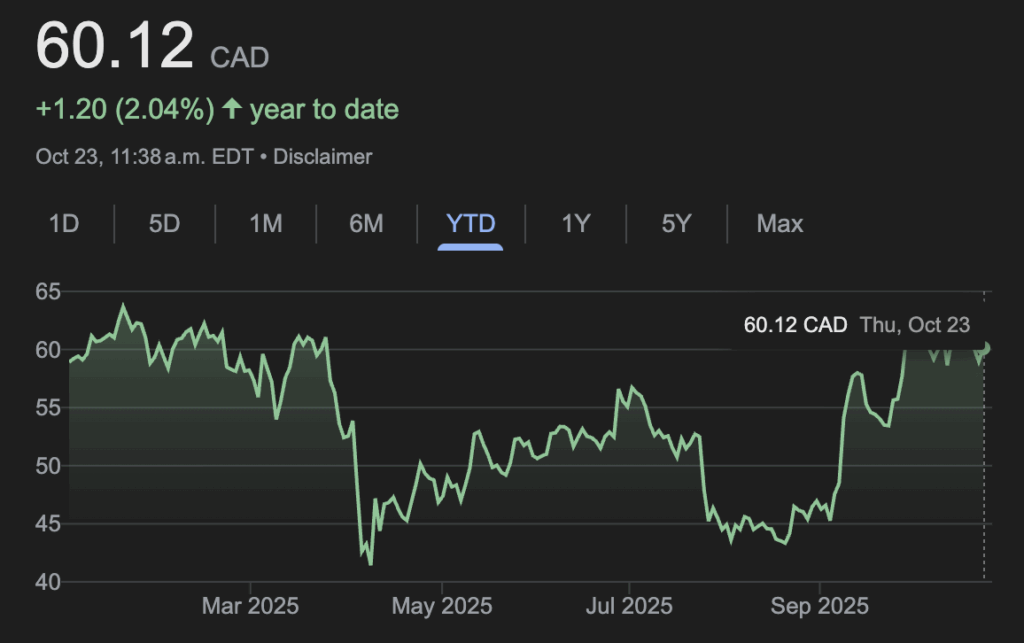

Freezer issue dents Metro’s bottom line in Q4, says costs to continue into Q1

Metro Inc. (TSX:MRU)

Numbers for its fourth quarter of 2025:

- Profit: $217 million (down from $219.9 million a year ago)

- Revenue: $5.11 billion (up from $4.94 billion)

Grocery and drugstore retailer Metro Inc. was hit by costs related to problems at its frozen food distribution centre in Toronto in the fourth quarter, with financial impacts expected to continue into the first quarter. The company said operations at the facility resumed last week after it was shut down for almost two months, but the temporary closure cost it $22.5 million in Q4 as it reported slightly lower annual profits.

Metro chief executive Eric La Flèche said the company expects the distribution centre to be essentially back to normal by the end of December. “I want to thank all our teams who continue to execute our contingency plan to supply our stores, thereby minimizing the impact on our customers,” he said in a statement on Wednesday.

Metro was forced to stop work at the Toronto frozen food distribution centre on Sept. 12 due to an issue with its refrigeration system. It resumed operations on Nov. 10. La Flèche said on the call that a mechanical issue, not one related to automation, was responsible for the problems with the refrigeration system. He added that the company is currently working with insurers to confirm the amount it will be able to recover.

“Looking forward to Q1 of 2026, we estimate that the direct costs associated with the rental of temporary chilling equipment and with the execution of our contingency plan will impact our net earnings by approximately $15 million to $20 million,” chief financial officer Nicolas Amyot said on the company’s conference call Wednesday.

[ad_2]

The Canadian Press

Source link