U.S. stocks finished lower on Thursday for the second day in a row as Minneapolis Federal Reserve Bank President Neel Kashkari played down the odds of the Fed pausing its interest-rate hikes, while investors awaited an update on the state of the U.S. labor market due out Friday. The S&P 500 SPX, -1.02%

finished down 38.76 points, or 1%, at 3,744.52. The Dow Jones Industrial Average DJIA, -1.15%

retreated 346.93 points, or 1.2%, to 29,926.94, while the Nasdaq Composite COMP, -0.68%

fell 75.33 points, or 0.7%, to 11,073.31.

U.S. stocks opened lower Wednesday, giving back some of this week’s sharp gains as Treasury yields rise and investors assess data showing job growth in September. The Dow Jones Industrial Average DJIA, -0.14%

fell 1% soon after the bell, while the S&P 500 SPX, -0.20%

dropped 1.1% and the Nasdaq Composite COMP, -0.25%

slid 1.4%, according to FactSet data, at last check. U.S. private sector employers added 208,000 jobs last month, up from a revised 185,000 in August, according to ADP’s employment report Wednesday. September’s employment growth was slightly stronger than the 200,000 of job gains expected by economists polled by the Wall Street Journal. Meanwhile, the yield on the 10-year Treasury note jumped about 10 basis points Wednesday to around 3.72%.

Elon Musk would lose about 13.5 million Twitter followers, if he pushes through his plan to get rid of most spam accounts, according to data crunched by CodeClan, a Scottish digital skills academy.

The Tesla Inc. TSLA, -3.84%

CEO on Tuesday gave up a legal battle and agreed to pay $44 billion to take over the social-media company. Musk has said he wants less than 5% of Twitter TWTR, -2.35%

accounts to be spam.

But Musk’s losses pale in comparison with singer Justin Bieber, who would lose 27.6 million of his 114.2 million followers, according to the data.

Britney Spears would lose the highest percentage of fake followers out of the top 20 with some 48% of her 55.8 million followers being classified as fakes.

Former President Barack Obama would lose 19.3 million of his 131.9 million followers, the data shows.

Among other high profile names; Katy Perry has about 23.3 million fakes among her 108.9 million followers, or 21.4% of the total; Rihanna has about 26.5 million fakes, or 24.9% of her 106.5 million followers; Lady Gaga has 10.9 million fakes in her roster of 84.7 million followers, for 12.9% of the total; Kim Kardashian has about 14 million fakes, or 19.4% of her 72.4 million followers, and Ellen DeGeneres has about 24.4 million fakes, equal to 31.5% of her 77.5 million followers.

In the world of politics, Indian Prime Minister Narendra Modi has about 17.5 million fakes in his 78.8 million followers, equal to 22.2% of the total.

CNN Breaking News has about 7.7 million fakes, or 12.2% of its 63.1 million followers. Bill Gates has about 14.3 million fakes, or 24.2% of his 58.9 million followers. And NASA has some 14.7 million fakes, or 26.8% of its 57.1 million followers.

Twitter shares were slightly lower premarket, while Tesla was down 1.1%.

Shares of Digital World Acquisition Corp. DWAC, +0.03%,

the special-purpose acquisition company, or SPAC, buying the company behind former President Donald Trump’s Truth Social social-media company, was slightly higher premarket after falling more than 5% Tuesday in the wake of the Musk/Twitter news.

The SPAC has fallen 67% in the year to date, while the S&P 500 SPX, -1.28%

has fallen 20%.

U.S. stock indexes ended modestly lower on Wednesday, despite briefly turning positive in the final hour of trading, while data showed steady growth in private-sector jobs and in the service sector, indicating more scope for the Federal Reserve to continue to raise interest rates.

How stocks traded?

The Dow Jones Industrial Average DJIA, +0.03%

lost 42.45 points, or 0.1%, to finish at 30,273.87

The S&P 500 SPX, +0.21%

was off 7.65 points, or 0.2%, ending at 3,783.28

The Nasdaq Composite COMP, +18.82%

shed 27.77 points, or 0.2%, to end at 11,148.64

On Tuesday, the Dow jumped 825 points, or 2.8%, while the S&P 500 increased 3.1% and the Nasdaq Composite rallied 3.3%.

What drove markets?

Wall Street stocks finished in the red after three main indexes bounced back from earlier losses in the final hour of trade, following a strong September private employment report in the morning.

Data released Wednesday showed that private-sector payrolls rose by 208,000 in September, indicating steady growth and supporting the view that the Fed has enough scope to keep raising interest rates. Economists surveyed by The Wall Street Journal had expected a rise of 200,000.

The report came two days before the closely watched nonfarm payrolls data issued by the Bureau of Labor Statistics. Investors are eying on it for important guidance on the Fed’s policy stance in the November meeting.

Friday’s employment report is expected to show the economy added 275,000 jobs in September, compared with 315,000 new positions added in August, according to a survey polled by Dow Jones.

“That certainly could move the needle,” said Kristina Hooper, chief global market strategist at Invesco. “Again, it doesn’t mean that it actually is going to change the market, but it could be the catalyst for short term rally if we get a disappointing jobs report.”

“But keep in mind, that’s just the anticipation of a Fed pivot based on data. But that does not ensure a Fed pivot. And so it could be one of those short-term rallies like the one we saw earlier this week,” Hooper said.

In other data Wednesday, an ISM barometer of U.S. business conditions in the service sector dipped to 56.7% in September but still showed steady growth and rising employment in a sign the economy is still expanding.

The U.S. trade deficit in August fell to $67.4 billion, the lowest level since mid 2021, paving the way for a resumption of growth in gross domestic product in the third quarter.

The S&P 500 had just enjoyed its largest two day percentage gain since April 2020 on Monday and Tuesday, and the best start to a quarter since 1938, according to Dow Jones Market data.

The bounce followed three quarters of declines, the worst such run since 2008, during which time the S&P 500 fell 24.8% to a near two-year trough as investors worried that the Federal Reserve’s interest rate hikes to crush inflation would harm the economy.

Brian Mulberry, client portfolio manager at Zacks Investment Management, believes the volatility in the stocks will continue because markets are getting a very “consistent message” from the Fed.

“Given what has happened over the last five trading sessions alone, we would be basically telling our clients to tighten your seatbelt a little bit because it’s definitely going to continue to be a bumpy ride,” Mulberry told MarketWatch in a phone interview on Wednesday. “If we get a ‘Goldilocks’ (jobs) report, that would mean decent economic activity is going on. That’s good for earnings overall in the market, but it’s not growing to a point where interest rates would have to be ratcheted up another 125 basis points by the end of the year.”

One major reason behind the rise early this week was the view that the Fed would pivot away from its aggressive monetary tightening.

Johanna Chua, chief Asia economist at Citi, said that though U.S economic growth remained in better shape than other countries and Fed officials continued to sound hawkish, the market risked being wrongfooted by any signs that interest rates could soon peak.

“Even as the overall fundamental setup has not changed… trimming of bearish risk/bearish rates/bullish USD positions has driven a sharp reversal,” Chua said.

Mary Daly, president of the Federal Reserve Bank of San Francisco said Wednesday that the Federal Reserve needs to keep raising its benchmark interest rate in order to cool inflation that hit a 40-year high earlier this year and has shown little signs of cooling. Atlanta Fed President Raphael Bostic will speak at 4 p.m. Eastern.

CLX22,

rose $1.24, or 1.4%, to settle at $87.76 a barrel on the New York Mercantile Exchange.

The S&P 500’s energy sector SP500.10, -0.07%

rose 2.1% following the news, up 12.6% over the last three trading days. According to Dow Jones Market Data, it was the best three-day percentage gain since November 2020 when it gained 16.1%. Shares of Schlumberger SLB, +0.77%

gained 6.3% at the close, while Exxon Mobil XOM, +1.32%

shares advanced 4%.

Companies in focus

Shares of Helen of Troy Ltd. HELE, -2.75%

finished 3.4% higher Wednesday, after the consumer products company, with brands including OXO, Hydro Flask and Braun, reported fiscal second-quarter earnings that beat expectations but cut its full-year outlook, as rising inflation has prompted consumers to change their spending patterns.

Shares of Monopar Therapeutics Inc. MNPR, +6.36%

gained 1.8% after the company said it completed enrollment in a Phase 2b clinical trial evaluating its experimental therapy aimed at preventing severe oral mucositis in patients undergoing chemoradiotherapy for oropharyngeal cancer.

Shares of Eiger BioPharmaceuticals Inc. EIGR, +0.85%

tumbled 5% after the company said it will not pursue emergency authorization of its experimental treatment for mild and moderate COVID-19 infections.

Shares of Lamb Weston Holdings Inc. LW, +2.45%

ended 4.2% higher Wednesday, after the potato supplier reported fiscal first-quarter profit that beat expectations, higher prices helped offset a volume decline.

Vice Chairman Greg Abel, the likely successor to CEO Warren Buffett, bought about $68 million of the company’s shares last Thursday in what appears to be his first purchases of Berkshire stock since he assumed the position in 2018.

In several Form 4 filings Monday with the Securities and Exchange Commission, Abel disclosed that he purchased 168 Berkshire Hathaway (ticker: BRK/A, BRK/B) Class A shares through the Gregory Abel Revocable Trust on behalf of his wife, children, and other family members.

The Dow booked its best day since February on Monday, after stocks booked a brutal month of September, as expectations for a potential pause in rate hikes from the Federal Reserve after December gathered steam. The Dow Jones Industrial Average DJIA, +2.66%

rose about 765 points, or 2.7%, ending near 29,490, which was its best daily percentage gain since February 25, according to Dow Jones Market Data. The S&P 500 index SPX, +2.59%

gained 2.6%. The Nasdaq Composite Index COMP, +2.27%

advanced 2.3%. Stocks kicked off October on a high note, after booking their worse first 9 months of a year in two years. The rally came as the surging dollar DXY, -0.49%

against a basket of rival currencies took a breather and the benchmark 10-year Treasury rate retreated from its recent high of 4%, near 3.7% on Monday. Fed-funds futures traders on Monday also were pricing in a less dramatic rise in the central bank’s policy rate in early 2023, according to the CME FedWatch Tool.

While September lived up to its reputation as a brutal month for stocks, October tends to be a “bear-market killer,” associated with historically strong returns, especially in midterm election years.

Skeptics, however, are warning investors that negative economic fundamentals could overwhelm seasonal trends as what’s traditionally the roughest period for equities comes to an end.

Rough stretch

U.S. stocks ended sharply lower on Friday, posting their worst skid in the first nine months of any year in two decades. The S&P 500 SPX, -1.51%

recorded a monthly loss of 9.3%, its worst September performance since 2002. The Dow Jones Industrial Average DJIA, -1.71%

fell 8.8%, while the Nasdaq Composite COMP, -1.51%

on Friday pushed its total monthly loss to 10.5%, according to Dow Jones Market Data.

October’s track record may offer some comfort as it has been a turnaround month, or a “bear killer,” according to the data from Stock Trader’s Almanac.

“Twelve post-WWII bear markets have ended in October: 1946, 1957, 1960, 1962, 1966, 1974, 1987, 1990, 1998, 2001, 2002 and 2011 (S&P 500 declined 19.4%),” wrote Jeff Hirsch, editor of the Stock Trader’s Almanac, in a note on Thursday. “Seven of these years were midterm bottoms.”

According to Hirsch, Octobers in the midterm election years are “downright stellar” and usually where the “sweet spot” of the four-year presidential election cycle begins (see chart below).

“The fourth quarter of the midterm years combines with the first and second quarters of the pre-election years for the best three consecutive quarter span for the market, averaging 19.3% for the DJIA and 20.0% for the S&P 500 (since 1949), and an amazing 29.3% for NASDAQ (since 1971),” wrote Hirsch.

SOURCE: STOCKTRADERSALMANAC

‘Atypical period’

Skeptics aren’t convinced the pattern will hold true this October. Ralph Bassett, head of investments at Abrdn, an asset-management firm based in Scotland, said these dynamics could only play out in “more normalized years.”

“This is just such an atypical period for so many reasons,” Bassett told MarketWatch in a phone interview on Thursday. “A lot of mutual funds have their fiscal year-end in October, so there tends to be a lot of buying and selling to manage tax losses. That’s kind of something that we’re going through and you have to be very sensitive to how you manage all of that.”

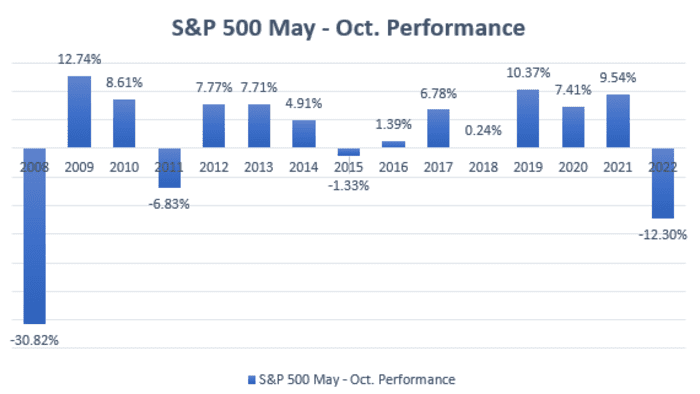

An old Wall Street adage, “Sell in May and go away,” refers to the market’s historical underperformance during the six-month period from May to October. Stock Trader’s Almanac, which is credited with coining the saying, found investing in stocks from November to April and switching into fixed income the other six months would have “produced reliable returns with reduced risk since 1950.”

Strategists at Stifel, a wealth-management firm, contend the S&P 500, which has fallen more than 23% from its Jan. 3 record finish, is in a bottoming process. They see positive catalysts between the fourth quarter of 2022 and the start of 2023 as Fed policy plus S&P 500 negative seasonality are headwinds that should subside by then.

“Monetary policy works with a six-month lag, and between the [Nov. 2] and [Dec. 14] final two Fed meetings of 2022, we do see subtle movement toward a data-dependent Fed pause which would bullishly allow investors to focus on (improving) inflation data rather than policy,” wrote strategists led by Barry Bannister, chief equity strategist, in a recent note. “This could reinforce positive market seasonality, which is historically strong for the S&P 500 from November to April.”

October crashes

Seasonal trends, however, aren’t written in stone. Dow Jones Market Data found the S&P 500 recorded positive returns between May and October in the past six years (see chart below).

SOURCE: FACTSET, DOW JONES MARKET DATA

Anthony Saglimbene, chief markets strategist at Ameriprise Financial, said there are periods in history where October could evoke fear on Wall Street as some large historical market crashes, including those in 1987 and 1929, occurred during the month.

“I think that any years where you’ve had a very difficult year for stocks, seasonality should discount it, because there are some other macro forces [that are] pushing on stocks, and you need to see more clarity on those macro forces that are pushing stocks down,” Saglimbene told MarketWatch on Friday. “Frankly, I don’t think we’re going to see a lot of visibility at least over the next few months.”

It was a September investors will remember — and not in a good way.

A Friday drop left the S&P 500 and Dow Jones Industrial Average with their biggest monthly losses since March 2020. And it was the worst September performance for both indexes since 2002. Seasonally inclined investors may wonder what that means for October.

Dow Jones Market Data took a look at how equities have done in the wake of particularly brutal Septembers.

But first, how does the month just ended stack up? The S&P 500 SPX, -1.51%

fell 9.34%, while the Dow DJIA, -1.71%

dropped 8.84% and the Nasdaq Composite COMP, -0.43%

declined 10.5%. The Nasdaq’s drop marked its worst September performance since 2008.

Sample size is limited. Not counting the current month, the S&P 500 has seen a September decline of 7% or more 11 times, according to data going back to 1928. The Dow has dropped 7% or more in September 13 times based on data back to 1928. The Nasdaq Composite has suffered a fall of 9% or more in September six times going back to 1986.

Dow Jones Market Data found that in Octobers that follow a 7% or larger fall in September, the S&P 500 rises 0.53% on average in October and sees a median gain of 1.81%. That’s better than the average for all Octobers at 0.47% and the median at 1.03%. October is positive in years following an outsize September loss 54.55% of the time, versus 57.45% for all Octobers (see table below).

S&P 500

Category

7% or worse

All

Average

0.53%

0.47%

Median

1.81%

1.03%

Worst Performance

-16.94%

-21.76%

Best Performance

16.30%

16.30%

% of October’s higher

54.55%

57.45%

Seasonal patterns, however, are only a guide. As MarketWatch’s Isabel Wang noted in a Friday report, many strategists are skeptical of October’s reputation as “bear killer.” They argued that a macroeconomic environment dominated by central banks aggressively tightening monetary policy in a bid to wring out inflation is likely to overshadow favorable seasonal factors.

October is also associated with historical market crashes, including those in 1987 and 1929. The S&P 500 plunged nearly 17% in October 2008 following a 9.1% fall in September in the wake of the collapse of Lehman Brothers.

Dow Jones Market Data, meanwhile, found that in Octobers following a September drop of 7% or more, the Dow has seen an average fall of 1.51% and a median drop of 1.46%. That compares with an average rise of 0.37% for all Octobers and a median gain of 0.79%. The S&P 500 has risen 46.15% of the time in Octobers that follow a 7% or more September decline, versus a rise 57.6% of the time for all Octobers (see table below).

DJIA

Category

7% or worse

All

Average

-1.51%

0.37%

Median

-1.46%

0.79%

Worst Performance

-20.36%

-23.22%

Best Performance

10.60%

10.65%

% of October’s higher

46.15%

57.60%

And here are the numbers for the Nasdaq in October following a September drop of 9% or more:

Category

9% or worse

All

Average

2.19%

0.73%

Median

4.26%

2.16%

Worst Performance

-17.73%

-27.23%

Best Performance

17.17%

17.17%

% of October’s higher

50.00%

54.90%

Since 1950, September has been the worst performing month of the year for the Dow Jones Industrial Average, S&P 500 and Russell 1000 and the worst for the Nasdaq Composite since 1971 and the small-cap Russell 2000 since 1979, according to the Stock Trader’s Almanac.

U.S. stocks end sharply lower Friday, closing out a brutal month of September and posting their worst skid in the first 9-months of a year in two decades as higher rates and recession fears grip investors. The Dow Jones Industrial Average DJIA, -1.71%

tumbled about 495 points Friday, or 1.7%, ending near 28,730 as heavy selling intensified into the closing bell. The S&P 500 index [s:spx] shed 1.5%, while the Nasdaq Composite Index COMP, -1.51%

finished down 1.5%. Losses for the week and month were far worse. The Dow led the major stock indexes lower with a 2.9% weekly skid, to end September down 8.8%. But the S&P 500 and Nasdaq recorded bigger monthly losses of 9.3% and 10.5%, respectively, according to FactSet data. The Federal Reserve’s unwavering stance in September on raising rates until inflation finds a path down to its 2% target has been blamed for the sharp selloff. The task has been complicated by a roaring labor market and soaring home prices, which keep pressure on shelter costs. Home prices have only begun to show signs of a retreat after gaining 45% nationally during the pandemic, which will keep focus on next week’s jobs update for August. For the year so far, the Dow fell 21%, the S&P 500 skid 24.8% and the Nasdaq shed 32.4%, which marked their worst first 9-month fall in a year since 2002, according to Dow Jones Market Data.

U.S. stocks opened lower Friday, feeling pressure after the Federal Reserve’s preferred inflation measure showed prices increased more than expected in August. The core personal-consumption price index, which strips out food and energy costs, rose 0.6% in August, compared with a forecast for a 0.5% increase. Investors were also monitoring a speech by Russian President Vladimir Putin, who announced plans to annex large swaths of Ukrainian territory. The Dow Jones Industrial Average DJIA, +0.01%

fell 84 points, or 0.3%, while the S&P 500 SPX, +0.33%

was down 0.1%. The Nasdaq Composite attempted to stabilize after a Thursday plunge, trading near unchanged.

This week Freddie Mac said the average interest rate on a 30-year mortgage loan in the U.S. had climbed to 6.70% from 6.29% the week before and 6.02% two weeks ago. The average rate a year ago was 3.01%.

Would-be sellers who have low-rate mortgage loans are reluctant if it means they need to take out a new loan to fund their next home. Would-be buyers are forced out of the market, as the monthly principal and interest payment for a new 30-year loan, based on Freddie Mac’s figures, has increased 53% from a year ago.

Home-sale contracts are being canceled at a record pace in some areas.

The dollar has strengthened as the Federal Reserve has taken the lead among central banks in raising interest rates. This is reverberating across the world, making it more costly for countries to make interest payments on dollar-denominated debt and increasing the cost of any commodity traded in dollars.

The rising dollar lowers prices on imported goods for Americans and can also lower their international travel costs. But Michael Wilson, Morgan Stanley’s chief equity strategist, warns that earnings for the S&P 500 SPX, -1.51%

would decline as a direct result of the strong dollar and called the current foreign-exchange backdrop an “untenable situation” for the stock market.

This is what happens when bearish sentiment runs high

Michael Brush interviews David Baron, co-manager of the Baron Focused Growth Fund BFGFX, -0.76%,

who describes opportunities cropping up as institutional investors dump stocks. He also explains his winning long-term strategy, which has included a very long-term investment in Tesla Inc. TSLA, -1.10%.

When interest rates rise, bond prices fall. But it also means that if you have money to put to work, bond yields have become much more attractive.

Khuram Chaudhry, a European equity quantitative strategist at JPMorgan in London, makes the case for buying bonds now.

What about preferred stocks?

Getty Images/iStockphoto

Preferred stocks feature stated dividend yields and prices that move the same way bond prices do. That means prices for many issues are now heavily discounted to face value and that current yields are much higher than they were at the end of 2021. Here’s an in-depth guide on how to research preferred stocks and make your own selections.

Stanley Druckenmiller predicted a “hard landing” in 2023 for the U.S. economy while speaking at CNBC’s Delivering Alpha Investor Summit on Sept. 28.

Bloomberg

Stanley Druckenmiller predicted a U.S. recession in 2023 as a result of monetary policy tightening by the Federal Reserve. That may not be much of a stretch, considering that the U.S. economy contracted during the first half of 2022, according to revised GDP figures from the Bureau of Economic Analysis.

After the new U.K. government of Prime Minister Liz Truss announced a massive tax cut along with a new spending program to help counter rising fuel costs and new borrowing, the pound hit a new low against the dollar on Sept. 26 as investors and money managers panicked and sold-off U.K. government bonds. Steve Goldstein explains how and why the Bank of England came tot the rescue.

After Tesla CEO Elon Musk said the upcoming Cybertruck would be sufficiently waterproof to “serve briefly as a boat,” the San Francisco Bay Ferry offered this advice to patrons.

Want more from MarketWatch? Sign up for this and other newsletters, and get the latest news, personal finance and investing advice.

U.S. stocks dropped sharply Friday, with major indexes posting their lowest finishes since 2020 and logging a third straight quarterly decline as investors grew more fearful that aggressive interest rate hikes by the Federal Reserve will drive the economy into a downturn in an attempt to quell inflation.

What’s happening

The Dow Jones Industrial Average DJIA, -1.71%

dropped 500.10 points, or 1.7%, to close at 28,725.51.

The S&P 500 SPX, -1.51%

dropped 54.85 points, or 1.5%, to end at 3,585.61.

The Nasdaq Composite COMP, -0.43%

shed 161.88 points, of 1.5%, finishing at 10,575.61.

The drop left the Dow and S&P 500 at their lowest since November 2020, while the Nasdaq posted its lowest close since July 29, 2020. The Dow dropped 8.8% in September, while the S&P 500 tumbled 9.3% and the Nasdaq lost 10.5%.

For the quarter, the Dow dropped 6.7%, the S&P 500 declined 5.3% and the Nasdaq gave up 4.1%.

What’s driving the market

In keeping with the historical pattern, U.S. stocks suffered during the month of September as an assertive Federal Reserve helped push Treasury yields and the dollar higher, which in turn undermined equity valuations.

Investors on Friday digested a reading from the personal consumption expenditure inflation index for August, which showed that core consumer prices climbed by 0.6% last month, more than Wall Street’s forecast of 0.5%. The core inflation measure excludes volatile food and energy prices.

“That means the Fed will remain hell-bent on killing inflation. And the best way to do that is to increase rates, kill the housing market, and get rental costs down. The PCE doesn’t have housing and rents as a big component as the CPI does, so the fact that it is rising is a warning sign,” said Louis Navellier, founder of Navellier & Associates, in emailed comments.

The reading largely confirmed similar data from the consumer-price index, another closely watched inflation barometer, which sent stocks lower earlier this month. Since that report was released just over two weeks ago, the S&P 500 has fallen more than 10%.

Helping to underscore this point, data out of the eurozone showed inflation accelerated at a record pace last month.

In other news, investors also heard from Fed Vice Chair Lael Brainard, who reiterated that the central bank would keep interest rates elevated to combat inflation, even if it harms the economy.

Since it will take time for high interest rates to bring inflation down, Brainard said the Fed is “committed to avoiding pulling back prematurely.”

Investors were also keeping an eye on megacap tech stocks. Apple Inc. AAPL fell 3% on Friday after leading markets lower a day earlier following a downgrade by Bank of America.

A final reading on the University of Michigan consumer-sentiment index for September showed consumers’ view of the economy improved somewhat during the month due to falling gas prices, even as their outlook remained broadly pessimistic.

Investors are now facing “what may be one of the most important earning seasons in a very long time, with a major rally in the cards if earnings don’t disappoint, and if the bears are right, lead to a further leg down if earnings disappoint and 4th quarter estimates are cut,” Navellier said.

Micron Technology MU, +0.18%

stock rose 0.2% after a report that Japan will grant it a $320 million subsidy to make advanced memory chips at its Hiroshima plant. That came a day after Micron posted quarterly earnings that included a forecast for a loss in the coming quarter and plans to scale back a build out of capacity.

— Steve Goldstein and Barbara Kollmeyer contributed to this article

U.S. stocks tumbled on Thursday to end sharply lower, with the S&P 500 posting its worst daily decline since mid-September. The Dow Jones Industrial Average DJIA, -1.54%

shed about 1.5%, or roughly 457 points, ending near 29,226, after falling more than 600 points at the session’s low. The S&P 500 index SPX, -2.11%

closed down 2.1%, marking its worst daily percentage decline since Sept. 13 when it tumbled 4.3%, according to FactSet data. The tech-heavy Nasdaq Composite Index COMP, -2.84%

bore the brunt of the day’s selling among the three major equity benchmarks, declining 2.8%. Investors were reacting Thursday to a flurry of economic data that suggested no letup in the Federal Reserve’s plans to keep increasing rates to fight inflation. That included a weekly report on U.S. jobless benefit claims showed the number of Americans initially applying for unemployment benefits fell to 193,000 in the week ended September 24, the lowest level since April. Apple Inc AAPL, -4.91%

shares also were in focus for a second trading day, booking a 4.9% decline and pulling down the Dow.

This is a Real-time headline. These are breaking news, delivered the minute it happens, delivered ticker-tape style. Visit www.marketwatch.com or the quote page for more information about this breaking news.

Stocks were trading near session lows heading into the final hour of trading Thursday, after economic data reinforced expectations the Federal Reserve will continue aggressively tightening monetary policy. The Dow Jones Industrial Average DJIA, -1.54%

was down 647 points or 2.2%, while the S&P 500 SPX, -2.11%

dropped 2.8% to 3,616. The Nasdaq Composite COMP, -2.84%

tumbled 3.6% to 10,653.

Rite Aid Corp. stock RAD, +7.16%

slid 11% in premarket trade Thursday, after the pharmacy retail chain posted a wider-than-expected loss for its fiscal second quarter as it booked goodwill impairment charges on its pharmacy services segment as well as charges for higher facility exit and store closures. The company had a net loss of $331.3 million, or $6.07 a share. for the quarter to Aug. 27, wider than the loss of $100.3 million, or $1.86 a share, posted in the year-earlier period. Adjusted per-share loss came to 63 cents, ahead of the loss of 50 cents forecast by FactSet analysts. Revenue fell to $5.901 billion from $6.113 billion a year ago, but was ahead of the $5.773 billion FactSet consensus. “As we look to the second half of the year, we expect continued pressure on consumer spending and supply chain challenges,” CEO Heyward Donigan said in a statement. “At the same time, we are ready to meet a high demand for immunizations, while driving continued strong performance at Elixir and further SG&A expense reductions.” The company is sticking with revenue guidance for fiscal 2023 of $23.6 billion to $24.0 billion, but is expecting a bigger loss — of $520.3 million to $477.3 million. Shares have fallen 52% in the year to date, while the S&P 500 SPX, +1.97%

has fallen 22%.

Stocks booked back-to-back losses on Monday, with the Dow adding to its 1,000-point skid Friday after Federal Reserve Chairman Jerome Powell vowed not to back down on fighting inflation until U.S. costs of living fall back to its 2% target range. The Dow Jones Industrial Average DJIA, +1.92%

shed about 183 points, or 0.6%, to end near 32,099. The S&P 500 index SPX, +1.99%

shed about 0.7%, while the Nasdaq Composite Index COMP, +2.02%

saw the brunt of the day’s losses, ending down 1%, according to FactSet. The S&P 500 and Dow both briefly flipped positive earlier in Monday’s session, but failed to hold those gains as losses mounted heading into the closing bell. Investors still were digesting Powell’s short, but blunt speech at the annual Jackson Hole economic symposium, which was viewed as trigger of Friday’s sharp selloff in equities. The Fed’s more hawkish tone also sent the 10-year Treasury yield up by 7.5 basis points to 3.109% on Monday, the highest level since June 28, according to Dow Jones Market Data based on 3 p.m. Eastern yields.

The stock-market selloff was intensifying Friday afternoon following Federal Reserve Chairman Jerome Powell’s terse speech at Jackson Hole vowing to fight inflation until the battle has been won by bringing the annual cost of living back down to the central banks’s 2% target. The Dow Jones Industrial Average DJIA, +1.88%

was down 740 points, or 2.2%, near 32,549, at last check. That would mark its worst daily percentage decline since June 16, when it tumbled 2.4%, according to Dow Jones Market Data. The S&P 500 SPX, +1.97%

was off 2.6% and the Nasdaq Composite Index was bearing the brunt of the selloff, down 3.2%, according to FactSet. Fed Chair Powell said the Fed will keep working to bring inflation down, even if it means hurting jobs and economic growth and that the process “will also bring some pain to households and businesses.”

U.S. stocks finished modestly higher Wednesday, with all three major stock benchmarks ending a 3-session skid, as investors picked up shares after a sharp market selloff earlier this week. The Dow Jones Industrial Average DJIA, -2.01%

rose about 61 points, or 0.2%, ending near 32,970, while the S&P 500 index SPX, -2.51%

closed up 0.3% and the Nasdaq Composite Index COMP, -3.21%

advanced 0.4%. Stocks booked modest gains as investors remained focused on the Federal Reserve’s inflation fight and Fed Chairman Jerome Powell’s speech at the Jackson Hole, Wyo. symposium on Friday. Recession worries also were in focus, with pending homes sales falling in July, a sign that rate hikes have been helping cool demand, even through shelter costs, specifically rents, have contributed to high U.S. inflation. Benchmark lending climbed Wednesday, with the 10-year Treasury rate TMUBMUSD10Y, 3.802%

climbing to 3.105% Wednesday, the highest since June 28, according to Dow Jones Market Data based on 3 p.m. Eastern levels. The S&P 500’s energy sector helped lead the way higher, up 1.2%, while financial rose 0.5%, according to FactSet

Shares of real estate services companies were knocked lower Wednesday after surprisingly strong inflation data sent Treasury yields climbing. A big jump in longer-term Treasury yields this year has weighed heavily on the housing market, as they reduce affordability by boosting mortgage lending rates. Shares of Redfin Corp. RDFN, -5.86%

slumped 4.6%, Zillow Group Inc. Z, -1.85% ZG, -1.91%

dropped 4.0%, Anywhere Real Estate Inc. HOUS, -6.29%

shed 2.9% and RE/MAX Holdings Inc. RMAX, -1.92%

lost 2.3%. Meanwhile, the yield on the 10-year Treasury note TMUBMUSD10Y, 3.787%

rose 7.6 basis points (0.076 percentage points) to 3.034%. Meanwhile, the S&P 500 SPX, -2.11%

fell 1.0%.