[ad_1]

U.S. Steel Stock Soars on $14.9 Billion Acquisition by Nippon Steel

[ad_2]

[ad_1]

Yields on 3-month

BX:TMUBMUSD03M

and 6-month

BX:TMUBMUSD06M

Treasury bills have been seeing yields north of 5% since March when Silicon Valley Bank’s collapse ignited fears of a broader instability in the U.S. banking sector from rapid-fire Fed rate hikes.

Six months later, the Fed, in its final meeting of the year, opted to keep its policy rate unchanged at 5.25% to 5.5%, a 22-year high, but Powell also finally signaled that enough was likely enough, and that a policy pivot to interest rate cuts was likely next year.

Importantly, the central bank chair also said he doesn’t want to make the mistake of keeping borrowing costs too high for too long. Powell’s comments helped lift the Dow Jones Industrial Average

DJIA

above 37,000 for the first time ever on Wednesday, while the blue-chip index on Friday scored a third record close in a row.

“People were really shocked by Powell’s comments,” said Robert Tipp, chief investment strategist, at PGIM Fixed Income. Rather than dampen rate-cut exuberance building in markets, Powell instead opened the door to rate cuts by midyear, he said.

New York Fed President John Williams on Friday tried to temper speculation about rate cuts, but as Tipp argued, Williams also affirmed the central bank’s new “dot plot” reflecting a path to lower rates.

“Eventually, you end up with a lower fed-funds rate,” Tipp said in an interview. The risk is that cuts come suddenly, and can erase 5% yields on T-bills, money-market funds and other “cash-like” investments in the blink of an eye.

When the Fed cut rates in the past 30 years it has been swift about it, often bringing them down quickly.

Fed rate-cutting cycles since the ’90s trace the sharp pullback also seen in 3-month T-bill rates, as shown below. They fell to about 1% from 6.5% after the early 2000 dot-com stock bust. They also dropped to almost zero from 5% in the teeth of the global financial crisis in 2008, and raced back down to a bottom during the COVID crisis in 2020.

FRED data

“I don’t think we are moving, in any way, back to a zero interest-rate world,” said Tim Horan, chief investment officer fixed income at Chilton Trust. “We are going to still be in a world where real interest rates matter.”

Burt Horan also said the market has reacted to Powell’s pivot signal by “partying on,” pointing to stocks that were back to record territory and benchmark 10-year Treasury yield’s

BX:TMUBMUSD10Y

that has dropped from a 5% peak in October to 3.927% Friday, the lowest yield in about five months.

“The question now, in my mind,” Horan said, is how does the Fed orchestrate a pivot to rate cuts if financial conditions continue to loosen meanwhile.

“When they begin, the are going to continue with rate cuts,” said Horan, a former Fed staffer. With that, he expects the Fed to remain very cautious before pulling the trigger on the first cut of the cycle.

“What we are witnessing,” he said, “is a repositioning for that.”

The most recent data for money-market funds shows a shift, even if temporary, out of “cash-like” assets.

The rush into money-market funds, which continued to attract record levels of assets this year after the failure of Silicon Valley Bank, fell in the past week by about $11.6 billion to roughly $5.9 trillion through Dec. 13, according to the Investment Company Institute.

Investors also pulled about $2.6 billion out of short and intermediate government and Treasury fixed income exchange-traded funds in the past week, according to the latest LSEG Lipper data.

Tipp at PGIM Fixed Income said he expects to see another “ping pong” year in long-term yields, akin to the volatility of 2023, with the 10-year yield likely to hinge on economic data, and what it means for the Fed as it works on the last leg of getting inflation down to its 2% annual target.

“The big driver in bonds is going to be the yield,” Tipp said. “If you are extending duration in bonds, you have a lot more assurance of earning an income stream over people who stay in cash.”

Molly McGown, U.S. rates strategist at TD Securities, said that economic data will continue to be a driving force in signaling if the Fed’s first rate cut of this cycle happens sooner or later.

With that backdrop, she expects next Friday’s reading of the personal-consumption expenditures price index, or PCE, for November to be a focus for markets, especially with Wall Street likely to be more sparsely staffed in the final week before the Christmas holiday.

The PCE is the Fed’s preferred inflation gauge, and it eased to a 3% annual rate in October from 3.4% a month before, but still sits above the Fed’s 2% annual target.

“Our view is that the Fed will hold rates at these levels in first half of 2024, before starting cutting rates in second half and 2025,” said Sid Vaidya, U.S. Wealth Chief Investment Strategist at TD Wealth.

U.S. housing data due on Monday, Tuesday and Wednesday of next week also will be a focus for investors, particularly with 30-year fixed mortgage rate falling below 7% for the first time since August.

The major U.S. stock indexes logged a seventh straight week of gains. The Dow advanced 2.9% for the week, while the S&P 500

SPX

gained 2.5%, ending 1.6% away from its Jan. 3, 2022 record close, according to Dow Jones Market Data.

The Nasdaq Composite Index

COMP

advanced 2.9% for the week and the small-cap Russell 2000 index

RUT

outperformed, gaining 5.6% for the week.

Read: Russell 2000 on pace for best month versus S&P 500 in nearly 3 years

Year Ahead: The VIX says stocks are ‘reliably in a bull market’ heading into 2024. Here’s how to read it.

[ad_2]

[ad_1]

It may be a couple of years since the meme-stock feeding frenzy hit its heights, but we’re still seeing occasional bursts of meme-like activity in number of stocks.

No discussion of meme stocks would be complete without OG AMC Entertainment Holdings Inc.

AMC,

But while the movie theater chain and original meme stock darling still grabs plenty of attention, it no longer fits the bill of a meme stock, according to Alicia Reese, VP of equity research at Wedbush. “AMC has seemingly lost its meme status, its share price having come crashing back down to earth over the past several months, particularly since its APE fold-in and reverse stock split,” she said. “AMC is now trading at a more normalized valuation, even if still at the high-end of its pre-meme historic range.”

AMC’s shares ended Friday’s session at $6.65, a far cry from their high of $393.63 on June 2, 2021, during the meme-stock frenzy.

Related: AMC’s stock falls more than 5% after company completes $350 million equity offering

“AMC’s premium valuation here is driven in part by a sub-section of the shareholders it gained during its meme stage, who have remained loyal to the company and have long claimed to be AMC shareholders for life,” Reese added. “AMC shed all the rest of its meme-era shareholders and are now left with the lifers, along with some institutional shareholders now that valuation has come back to a more normalized range.”

The analyst thinks that in 2024, AMC will continue to issue pre-authorized shares to pay down its high-debt balance, as evidenced by the $350 million equity offering completed this week. “The company is focused on right-sizing the balance sheet, while attempting to maintain strong relations with the AMC lifers still propping up the stock,” said Reese.

Fellow original meme stock GameStop has also been in the news recently, with the company’s board of directors approving a new investment policy, which lets the company invest in equity securities, among other investments. The board also gave Chairman and Chief Executive Ryan Cohen the authority to manage the investment portfolio. The new policy was dubbed “alarming” and “inane” by Wedbush Managing Director Michael Pachter.

“If he can invest in anything – farmland, chicken feed, cryptocurrency – that’s not in the best interests of the shareholders,” he told MarketWatch. “Heaven knows what he will do.”

Related: GameStop’s plan to buy stocks with company cash ‘alarming’ and ‘inane,’ analyst says

As for GameStop, the analyst describes the videogame retailer as a declining business, pointing to the company’s third-quarter revenue of $1.078 billion, which was down from $1.186 billion in the prior year’s quarter. “They are shrinking, period, and they can’t save their way to prosperity,” he added.

The company’s new investment policy could also fuel more meme-style activity, according to Pachter, who says that Cohen’s moves will be closely watched. “He will invest in something and it will possibly become the next meme stock,” the analyst told MarketWatch.

Pachter pointed to Cohen’s decision in 2022 to unload his huge stake in beleaguered home goods retailer and sometime meme stock Bed Bath & Beyond Inc. just months after buying it. In August of that year Cohen sold his entire stake in Bed Bath & Beyond five months after accruing the stake in an activist campaign, amassing a profit of more than $58 million.

Stocktwits, a social platform for investors and traders, told MarketWatch that it has seen a dedicated core audience of retail investors stick with the likes of AMC and GameStop. “Message volume and sentiment have remained elevated on the platform throughout the year, with their audiences growing temporarily around earnings or other events that create volatility,” Tom Bruni, senior writer at Stocktwits, told MarketWatch.

Related: Small-cap Chinese stocks spark meme-like buzz

Retail traders are still on the lookout for high-volatility situations, according to Bruni, who cited the example of Vietnamese electric vehicle stock VinFast Auto Ltd.

VFS,

which had a “crazy month” in August before crashing back down. “However, we would note that there have been fewer instances of these types of meme stocks occurring this year, and their lifespan tended to be pretty short,” he added.

“For stocks with the ‘meme’ potential in 2024, look to beaten-down areas of the market that already have strong retail investor communities around them,” Bruni told MarketWatch. “Several that stick out are electric vehicle stocks (specifically startups), solar stocks, or anything China-related. Traders will likely be looking for stocks at the intersection of these themes, like Lucid Group ($LCID), as potential ‘powder kegs’ for volatility in 2024.”

Shares of Lucid Group Inc.

LCID,

are down 30.2% in 2023, compared with the S&P 500 index’s

SPX

gain of 22.9%.

One thing is for sure – the social media dynamics that created the meme stock phenomenon are not going away. “Internet culture will continue to be more prevalent in markets as the world becomes more digitized and young people age into participation,” Tommy Tranfo, head of community at Stocktwits, told MarketWatch. “Crypto markets are an area where we expect to see a large concentration of this activity, particularly within the context of a crypto bull market, which will likely bring in a new wave of market participants who will skew toward the internet culture demo.”

Related: This EV company has a bigger market cap than Ford or GM. But you may not have heard of it.

“New crypto meme communities such as the $BONK (a dog-themed coin on the Solana blockchain) are already clear examples of this craze taking place,” he added.

[ad_2]

[ad_1]

Options contracts tied to more than $5 trillion worth of stocks, exchange-traded funds and indexes are set to expire on Friday as the latest “triple witching” expiration event collides with the rebalancing of the S&P 500 and Nasdaq-100.

The result could be a high-octane, and potentially extremely volatile, session where tens of billions of contracts and shares could change hands, market strategists said.

According to figures from Rocky Fishman, founder of Asym500, options with a notional value of $5.3 trillion are set to expire, with the biggest slug expiring ahead of the open.

On one side, many traders will be cashing in bullish bets that are deep in the money, while some roll their positions, forcing market-makers to continue to hedge their exposure.

At the same time, managers of index-tracking funds will need to finish adjusting their holdings before the announced index changes take effect.

Already, trading volume has been trending higher all week. In the U.S. market, 17 billion shares changed hands on Thursday, according to Steve Sosnick, chief market strategist at Interactive Brokers, during a phone interview with MarketWatch. That is up from 10.6 billion on Tuesday.

“I expect to see enormous volumes tomorrow in a lot of popular names,” Sosnick said.

“Not only will this one be the largest option expiration of the year (as is typical for December), but it is currently set up to become the largest SPX option expiration in more than a decade,” Fishman said in a report shared with MarketWatch.

Brent Kochuba, founder of Spotgamma, an options-market analytics provider, went even further during a phone interview with MarketWatch: “This might be the biggest options expiration ever.”

As markets have rallied, traders have been scooping up bullish options contracts at a record pace, according to data from Cboe Global Markets, the biggest operator of options exchanges in the U.S.

For S&P 500-linked options, typically the most popular product, 4.8 million contracts changed hands on Thursday, according to Cboe, a new record, surpassing the previous record from Nov. 14.

Also, total call-trading volume for all U.S. equity options exceeded 30 million contracts on Wednesday, according to Goldman Sachs Group, making it one of the busiest days for trading in bullish contracts this year.

Aggressive call-buying over the past month has helped push the S&P 500 to just shy of its record closing high, options-market experts said. The S&P 500

SPX

gained 8.9% in November, its best month of 2023, and the 18th best-performing month of the past 73 years. And it has continued to climb in December, having risen 3.3% through Thursday’s close, according to FactSet data.

Earlier this week, options strategists warned that markets might run into trouble at 4,600 on the S&P 500. They warned that a “call wall” of open-interest in bullish contracts around that level could force market makers to put the breaks on the rally.

Instead, bullish traders blew through the call wall, pushing it higher to 4,700, said Kochuba.

The S&P 500 closed at 4,719.55 on Thursday, its highest close since Jan. 12, 2022, according to FactSet data. The index is now sitting within 1.75 percentage points of its record closing high of 4,796.56 on Jan. 3, 2022.

Traders’ bullishness recently helped push the Cboe Volatility Index

VIX,

otherwise known as Wall Street’s “fear gauge,” to multiyear lows, according to FactSet data.

To be sure, it isn’t just S&P 500 options and contracts tied to popular stocks like Tesla Inc.

TSLA,

seeing explosive volume: Calls tied to the iShares Russell 2000 ETF

IWM,

which tracks the small-cap Russell 2000, hit 1.35 million contracts, the third-highest ever, according to Goldman. Activity in options contracts linked to small-cap stock indexes has surged since late October.

Heavy call buying has pushed the put-call skew for S&P 500 options to its lowest level in a year, according to data from Goldman Sachs Group.

This shows that investors have been scrambling to buy bullish contracts, while largely shunning bearish ones, as stocks marched higher. Goldman analysts described Friday as “the last major liquidity event of the year” in a note to clients obtained by MarketWatch.

“Triple Witching” days happen once a quarter. They are thusly named because options tied to single stocks, ETFs and indexes will expire, alongside index-tracking futures contracts. Options-market experts say they are typically associated with more intraday swings and higher trading volume.

Making things even more interesting is the fact that the quarterly rebalancing of the S&P 500 and Nasdaq-100 is due to take effect after markets close on Friday.

Normally routine, this quarter’s rebalancing is drawing outsize attention following an extremely rare ad hoc rebalancing over the summer to rein in the influence of megacap stocks in the Nasdaq-100.

Earlier this month, Standard & Poor’s announced its rebalancing plans, which included reducing the weighting of two Magnificent Seven stocks, Apple Inc.

AAPL,

and Alphabet Inc.

GOOG,

GOOGL,

At the same time, Amazon.com Inc.

AMZN,

which is also part of the Mag 7, will see its weighting increased. Meanwhile, three companies will join the index, including Uber Inc.

UBER,

while shares of three other companies depart.

Kochuba believes Friday’s expiration could remove the last barrier holding stocks back from rocketing to record highs before the end of the year.

“After OpEx, markets will be able to move more freely,” Kochuba said.

Garrett DeSimone of OptionMetrics cautioned that investors shouldn’t place too much weight on options-market activity and other technical factors.

“At the end of the day, macro trumps everything,” he said during an interview with MarketWatch.

[ad_2]

[ad_1]

The New Year is almost here, and that means it’s time for four of the last dividend cutters of 2020— Boeing, American Airlines Group, Royal Caribbean Group, and Carnival—to bring back their payouts to shareholders.

Continue reading this article with a Barron’s subscription.

View Options

[ad_1]

It has been a record day for 10% of the S&P 500.

A group of 51 stocks in the benchmark equity index swept to record finishes on Tuesday, the most since April 20, 2022, according to a tally from Dow Jones Market Data.

Dow Jones Market Data

Stocks that logged a record close on Tuesday included Allstate Corp

ALL,

Costco Wholesale

COST,

D.R. Horton, Inc.

DHI,

Mastercard

MA,

T-Mobile US Inc.,

TMUS,

Visa Inc.

V,

and Waste Management Inc.,

WM,

among others.

Equities have been in a year-end rally mode, driven higher by tumbling benchmark yields that finance much of the U.S. economy and expectations of coming interest-rate cuts.

The 10-year Treasury rate

BX:TMUBMUSD10Y

fell to 4.2% on Tuesday from a high of about 5% in October.

The Dow Jones Industrial Average

DJIA

on Tuesday ended at its third-highest level on record, while the S&P 500 index

SPX

and Nasdaq Composite Index

COMP

added to a string of new closing highs for 2023. The Dow finished 0.6% away from its record close logged almost two years ago, while the S&P 500 was only 3.2% below its close from the same period, according to Dow Jones Market Data.

The push higher for stocks followed inflation data for November that showed price pressures continued to ease from peak levels, but still were above the Fed’s 2% annual target.

The consumer-price index pegged the annual rate of inflation at 3.1%, down from 3.2% in October, with the “last mile” of inflation expected to be the hardest part to tame.

Investors now will be focused on Wednesday’s Federal Reserve decision. Short-term interest rates are expected to remain unchanged at a 22-year high, but the central bank is expected to update its “dot plot” forecast of rates over a longer time horizon.

“Although the market will focus on the timing of rate cuts, we suspect Chair Powell will be keen to strike notes of caution to avoid financial conditions easing too much further to ensure the Fed continues to see encouraging progress on inflation,” said Emin Hajiyev, senior economist at Insight Investment, in emailed comments.

[ad_2]

[ad_1]

U.S. stocks opened mixed on Tuesday as investors weighed a reading on inflation that was largely in line with economists’ forecasts. The Dow Jones Industrial Average

DJIA,

was up less than 0.1% soon after the opening bell, while the S&P 500

SPX,

slipped 0.2% and the Nasdaq Composite

COMP,

fell 0.1%, according to FactSet data, at last check. The Bureau of Labor Statistics said Tuesday that inflation, as measured by the consumer-price index, rose 0.1% in November for a year-over-year rate of 3.1%. Economists polled by the Wall Street Journal had forecast that inflation would be unchanged in November while rising at an annual pace of 3.1%. So-called core inflation, which excludes energy and food prices, climbed 0.3% last month to increase 4% in the 12 months through November. That was in line with economists’ expectations. In the bond market, the yield on the 10-year Treasury note

TMUBMUSD10Y,

was up one basis point at around 4.24%, according to FactSet data, at last check.

[ad_2]

[ad_1]

U.S. stocks opened mostly lower on Monday, after six straight weeks of gains, as investors look ahead to inflation data and the Federal Reserve’s policy meeting this week. The Dow Jones Industrial Average

DJIA,

was up 0.2% soon after the opening bell, while the S&P 500

SPX,

shed 0.1% and the Nasdaq Composite

COMP,

fell 0.4%, according to FactSet data, at last check. A reading on November inflation, as measured by the consumer-price index, will be released on Tuesday. The following day, the Fed will release a statement on its monetary policy, after concluding its two-day meeting. Last week, all three major U.S. stock benchmarks closed at their highest levels of the year, with the S&P 500 finishing Friday at its highest value since March 29, 2022.

[ad_2]

[ad_1]

The rally lifting U.S. stocks to fresh 2023 highs in the year’s home stretch could be at risk if the Federal Reserve on Wednesday crushes expectations for interest-rate cuts in 2024.

U.S. central bankers and investors haven’t exactly been seeing eye-to-eye about when the Fed will start easing its monetary policy, according to Melissa Brown, senior principal of applied research at Axioma.

Traders also have been flip-flopping on their forecasts for rate cuts over the past few months, based on fed-funds futures data.

Given the whipsaw of recent volatility, it isn’t hard to imagine a jittery market backdrop as investors wait to hear from Fed Chairman Jerome Powell on Wednesday, even though the central bank isn’t expected to change its range for short-term interest rates. Since July, the Fed funds rate rate has been at a 22-year high in a 5.25% to 5.5% range.

U.S. stocks advanced this year after a bruising 2022, adding big gains in November, as benchmark 10-year Treasury yields

BX:TMUBMUSD10Y

tumbled from a 16-year high of 5%. The Dow Jones Industrial Average

DJIA

closed on Friday only 1.5% away from its record close nearly two years ago. The S&P 500 index

SPX

booked its highest finish since March 2022, according to Dow Jones Market Data.

Year Ahead: The VIX says stocks are ‘reliably in a bull market’ heading into 2024. Here’s how to read it.

“I don’t see any report on the horizon that would really make them [the Fed] change their stance on where we are on monetary policy,” said Alex McGrath, chief investment officer at NorthEnd Private Wealth. It is mostly the expectation of Fed rate cuts next year that have supported stock and bond markets rallies recently, he said.

The Dow Jones closed 9.4% higher on the year through Friday, the S&P 500 was up 19.9% and the Nasdaq Composite advanced 37.6% for the same period, according to FactSet data.

“We have been a little skeptical of the market’s excitement over rate cuts early next year,” said Ed Clissold, chief U.S. strategist at Ned Davis Research.

It takes a gradual process for the Fed to move away from its monetary policy tightening, Clissold told MarketWatch. The Fed is likely to pivot its tone from being very hawkish to neutral, remove the tightening bias, and then talk about rate cuts, noted Clissold.

The bond market on Friday already was again flashing signs of a potential rethink by investors about the path of interest rates in 2024.

Junk bonds

JNK

HYG,

often a canary in the coal mine for markets, hit pause on a rally that started in late October as benchmark borrowing costs fell, even though the sector has benefited from big inflows of funds in recent weeks.

Treasury yields for 10-year and 30-year

BX:TMUBMUSD30Y

bonds also shot higher Friday, echoing volatility that took hold in mid-October.

Read: Investors have fought a 2-year battle with the bond market. Here’s what’s next.

Mike Sanders, head of fixed income at Madison Investments, has been similarly cautious. “I think the market is a little too aggressive in terms of thinking that cuts are going to occur in March,” Sanders said. It is more likely that the Fed will start cutting rates in the second half of next year, he said.

“I think the biggest thing is that the continued strength in the labor market continues to make the services inflation stickier,” Sanders said. “Right now we just don’t see the weakness that we need to get that down.”

Friday’s U.S. employment report adds to his concerns. About 199,000 new jobs were created in November, the government said Friday. Economists polled by the Wall Street Journal had forecast 190,000 jobs. The report also showed rising wages and a retreating unemployment rate to a four-month low of 3.7% from 3.9%.

The U.S. central bank will likely “try their best to push back on the narrative of cuts coming very soon,” Sanders said. That could be accomplished in its updated “dot plot” interest rate forecast, also due Wednesday, which will provide the Fed’s latest thinking on the likely path of monetary policy. The Fed’s update in September surprised some in the market as it bolstered the central bank’s stance of higher rates for longer.

There’s still a chance that inflation will reaccelerate, Sanders said. “The Fed is worried about the inflation side more than anything else. For them to take the foot off the brake sooner, it just doesn’t do them any good.”

Ahead of the Fed decision, an inflation update is due Tuesday in the November consumer-price index, while the producer-price index is due Wednesday.

Still, seasonality factors could aid the stock market in December. The Dow Jones Industrial Average in December rises about 70% of the time, regardless of whether it is in a bull or bear market, according to historical data.

See: Stock market barrels into year-end with momentum. What that means for December and beyond.

“The overall market outlook remains constructive,” said Ned Davis’s Clissold. “A soft landing scenario could support the bull market continuing.”

Last week the Dow eked out a gain of less than 0.1%, the S&P 500 edged up 0.2% and the Nasdaq rose 0.7%. All three major indexes went up for a sixth straight week, with the Dow logging its longest weekly winning streak since February 2019, according to Dow Jones Market Data.

[ad_2]

[ad_1]

U.S. stocks closed higher on Friday, shaking off earlier weakness after a strong monthly jobs report, to clinch a sixth straight week in a row of gains. The Dow Jones Industrial Average

DJIA,

advanced about 130 points, or 0.4%, to end near 36,247, according to preliminary FactSet data. The S&P 500 index gained 0.4% Friday and the Nasdaq Composite finished 0.5% higher. A string of weekly gains propelled the S&P 500 index

SPX,

to a fresh 2023 closing high and left the Dow about 1.4% away from its record close set nearly two years ago, according to Dow Jones Market Data. Equities have benefitted from a risk-on tone going into year end, which has been driven by falling 10-year Treasury yields

TMUBMUSD10Y,

and optimism around the Federal Reserve potentially cutting interest rates in the year ahead. That hinges on if inflation continues to ease. November’s robust jobs report served as a reminder Friday of the tough path of the “last mile” in getting inflation down to the Fed’s 2% annual target. As part of this, the 10-year Treasury yield jumped about 11.5 basis points Friday to 4.244%, but still was about 74 basis points lower than its October high. For the week, the Dow was only fractionally higher, the S&P 500 gained 0.2% and the Nasdaq climbed 0.7%.

[ad_2]

[ad_1]

S&P 500 sees highest close since March 2022 as U.S. stocks extend winning streak

[ad_2]

[ad_1]

November’s sharp pullback in 30-year fixed mortgage rates may not last if the labor market remains strong, said Mark Palim, deputy chief economist at Fannie Mae.

Palim was speaking to the robust jobs report released on Friday, showing the U.S. added 199,000 jobs in November and that wages rose, albeit with the figures somewhat inflated by the return of striking workers from the auto industry and from Hollywood.

Homebuyers can benefit from a robust labor market and the near 80 basis point decline in mortgage rates since the end of October, Palim said. But if the “labor markets remain this strong, we believe the pace of mortgage rate declines will likely not continue in the near term or may partially reverse,” he said in a statement.

The benchmark 30-year fixed mortgage rate was edging down to 7.05% on Friday, after surging to nearly 8% in October, according to Mortgage Daily News.

Optimism around the potential for falling mortgage costs to thaw home sales helped lift shares of Toll Brothers Inc.,

TOL,

and a slew of other homebuilders tracked by the SPDR S&P Homebuilders ETF,

XH,

to record highs earlier this week, even while investors in some homebuilder bonds have been sellers in recent weeks.

Yields on 10-year

BX:TMUBMUSD10Y

and 30-year Treasury notes

BX:TMUBMUSD30Y

were up sharply Friday, to about 4.23% and 4.32%, respectively, but still below the highs of about 5% in October. The surge in long-term borrowing costs was stoked by tough talk by Federal Reserve officials about the need to keep rates higher for longer to bring inflation down to a 2% annual target.

Read: Solid job growth, sharp wage gains sends Treasury yields up by the most in months

U.S. stocks were up Friday afternoon, shaking off earlier weakness following the jobs report. The Dow Jones Industrial Average

DJIA

was 0.2% higher, further narrowing the gap between its last record close set two years ago, the S&P 500 index

SPX

and the Nasdaq Composite Index

COMP

also were up 0.2%, according to FactSet data.

[ad_2]

[ad_1]

Advanced Micro Devices is on a roll this week, with its shares marching higher since the chip maker revealed ambitious plans to push into artificial intelligence. Investors looking to dive in best be warned: the stock now looks more expensive than Nvidia.

Continue reading this article with a Barron’s subscription.

View Options

[ad_1]

U.S. stocks closed higher Friday, with the Dow Jones Industrial Average scoring its longest weekly winning streak since February 2019, as investors digested the latest job report.

For the week, the Dow eked out a gain of less than 0.1%, the S&P 500 edged up 0.2% and the Nasdaq advanced 0.7%. All three major indexes rose for a sixth straight week, according to Dow Jones Market Data.

U.S. stocks ended higher Friday as investors parsed a stronger-than-expected job report.

The U.S. Bureau of Labor Statistics said Friday that the economy added 199,000 jobs in November, while the unemployment rate fell to 3.7% from 3.9%. Economists polled by the Wall Street Journal had forecast that 190,000 jobs would be added in the month.

“It’s nice to see that a soft landing still can take place,” Yung-Yu Ma, chief investment officer at BMO Wealth Management, said by phone Friday. But the market had been getting “too optimistic” about potential interest-rate cuts by the Federal Reserve in the early part of next year, he added.

The job report is “perhaps a wash” for markets as “average hourly earnings growth came in a little on the high side,” Ma said. That could contribute to inflationary pressures and push a Fed pivot on rate cuts further out in 2024 than markets were expecting.

“The Fed can probably be patient for a while,” he said. Fed Chair Jerome Powell may “strike a bit more of a hawkish tone” after the central bank’s monetary-policy meeting next week, potentially pushing back against some of the enthusiasm for earlier rate cuts, Ma said.

Average hourly earnings rose 0.4% in November, up 4% year over year, the job report shows.

“Even though the headline 199,000 new jobs created is just slightly above consensus estimates for 190,000 new positions, the lower unemployment rate of 3.7%, coupled with higher-than-expected average hourly earnings, caused a jump higher in Treasury yields,” Quincy Krosby, chief global strategist at LPL Financial, said in emailed comments.

The yield on the 10-year Treasury note

BX:TMUBMUSD10Y

climbed 11.5 basis points Friday to 4.244%, according to Dow Jones Market Data. That’s below its high this year of about 5% in October.

Meanwhile, the stock market’s so-called fear gauge remained low, with the CBOE Volatility Index

VIX

declining to 12.35 on Friday, FactSet data show.

See: The VIX says stocks are ‘reliably in a bull market’ heading into 2024. Here’s how to read it.

In other economic data released Friday, the University of Michigan’s gauge of consumer sentiment rose to a preliminary reading of 69.4 in December, its first increase in five months. Inflation expectations also moderated, the university’s survey of consumer sentiment showed.

Such a big swing for a single reading of the survey is unusual, said Claudia Sahm, a former Federal Reserve economist who now runs a consulting business. “These data usually don’t move like that,” she said during a phone interview with MarketWatch.

Next week’s economic calendar will include a reading on U. S. inflation from the consumer-price index as well as the outcome of the Fed’s two-day policy meeting, scheduled to conclude Dec. 13.

Meanwhile, the S&P 500 notched a sixth straight week of gains, its longest such winning streak since the stretch ending Nov. 15, 2019, according to Dow Jones Market Data. The Dow Jones Industrial Average logged its longest stretch of weekly gains since February 2019.

Steve Goldstein contributed.

[ad_2]

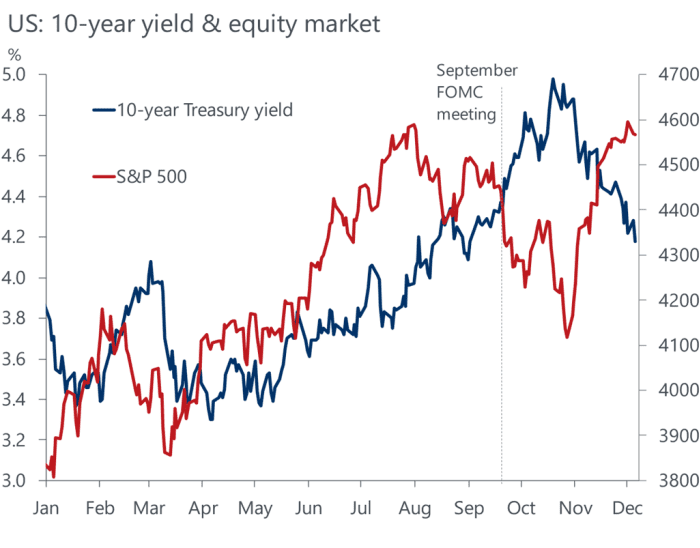

[ad_1]

Financial conditions are now looser than in September, says economist

Getty Images

The feel-good tone gripping markets in the home stretch of 2023 may not be what the Federal Reserve had penciled in for the holidays.

The stock market in December, once again, has been knocking on the door of record levels, driven by optimism about easing inflation and potential Fed rate cuts next year.

But while the prospect of double-digit equity gains this year would be a reprieve for investors after a brutal 2022, the latest rally also points to looser financial conditions.

Ultimately, the risk of looser financial conditions is that they could backfire, particularly if they rub against the Fed’s own goal of keeping credit restrictive until inflation has been decisively tamed.

Read: Inflation is falling but interest rates will be higher for longer. Way longer.

Specifically, the November rally for the S&P 500 index

SPX

can be traced to the 10-year Treasury yield

BX:TMUBMUSD10Y

dropping to 4.1% on Thursday from a 16-year peak of 5% in October.

Oxford Economics

The Fed only exerts direct control over short-term rates, but 10-year and 30-year Treasury yields

BX:TMUBMUSD30Y

are important because they are a peg for pricing auto loans, corporate debt and mortgages.

That makes long-term rates matter a lot to investors in stocks, bonds and other assets, since higher rates can lead to rising defaults, but also can crimp corporate earnings, growth and the U.S. economy.

Michael Pearce, lead U.S. economist at Oxford Economics, thinks the November rally may put Fed officials in a difficult spot ahead of next week’s Dec. 12 to 13 Federal Open Market Committee meeting — the eighth and final policy gathering of 2023.

“The decline in yields and surge in equity prices more than fully unwinds the tightening in conditions seen since the September FOMC meeting,” Pearce said in a Thursday client note.

The Fed next week isn’t expected to raise rates, but instead opt to keep its benchmark rate steady at a 22-year high in a 5.25% to 5.5% range, which was set in July. The hope is that higher rates will keep bringing inflation down to the central bank’s 2% annual target.

Ahead of the Fed’s July meeting, stocks were extending a spring rally into summer, largely driven by shares of six meg-cap technology companies and AI optimism.

Rates in September were kept unchanged, but central bankers also drove home a “higher for longer” message at that meeting, by penciling in only two rate cuts in 2024, instead of four earlier. That spooked markets and triggered a string of monthly losses in stocks.

Pearce said he expects the Fed next week to “push back against the idea that rate cuts could come onto the agenda anytime soon,” but also to “err on the side of leaving rates high for too long.”

That might mean the first rate cut comes in September, he said, later than market odds of a 52.8% chance of the first cut in March, as reflected by Thursday by the CME FedWatch Tool.

Stocks were higher Thursday, poised to snap a three-session drop. A day earlier, the S&P 500 closed 5.2% off its record high set nearly two years ago, the Dow Jones Industrial Average

DJIA

was 2% away from its record close and the Nasdaq Composite Index

COMP

was almost 12% below its November 2021 record, according to Dow Jones Market Data.

Related: What investors can expect in 2024 after a 2-year battle with the bond market

[ad_2]

[ad_1]

Dollar General Corp.’s stock

DG,

rose 1.9% early Thursday, after the discount retailer beat third-quarter earnings estimates and backed its guidance, even as its CEO said it was not happy with its performance. The company posted net income of $276.2 million, or $1.26 a share, for the third quarter, down from $526.2 million, or $2.33 a share, in the year-earlier period. Sales rose 2.4% to $9.694 billion from $9.465 billion a year ago. The FactSet consensus was for EPS of $1.20 and sales of $9.644 billion. Same-store sales fell 1.3%, while FactSet was expecting a 2.1% decline. “While we are not satisfied with our financial results for the third quarter, including a significant headwind from inventory shrink, we are pleased with the momentum in some of the underlying sales trends, including positive customer traffic, as well as market share gains in both dollars and units,” CEO Todd Vasos said in a statement. Vasos returned to the role of CEO in October, after serving in the position from June 2015 to November 2022. Vasos said the company has completed a review of all aspects of the business and identified key areas for improvement both in the near and longer term. For fiscal 2024, it is planning about 2,385 real estate projects, including 800 new stores, 1,500 remodels, and 85 relocations. “This is a modest slow down compared to the number of projects in recent years, which we believe is prudent in this environment,” he said. Dollar General backed its full-year guidance, for a sales increase of 1.5% to 2.5%, and for EPS of $7.10 to $7.60. The company expects same-store sales to be down 1% to flat. The stock is down 45.6% in the year to date, while the S&P 500

SPX,

has gained 19%.

[ad_2]

[ad_1]

U.S. stock indexes ended lower on Wednesday, with the S&P 500

SPX,

and the Dow Jones Industrial Average

DJIA,

booking a third straight session of losses as investors awaited more labor-market data for clarity about the state of the economy. The Dow industrials fell 70 points, or 0.2%, to end at 36,054, while the S&P 500 finished 0.4% lower and the Nasdaq Composite

COMP,

retreated 0.6%. U.S. businesses added 103,000 new jobs in November, paycheck company ADP said on Wednesday, in another sign of slower hiring and a softer labor market. Investors will monitor jobless claims numbers on Thursday morning before contemplating the widely followed official data on nonfarm payrolls, wages and the unemployment rate, due out Friday 8:30 a.m. Eastern time.

[ad_2]

[ad_1]

GitLab Inc.’s stock

GTLB,

surged 15% in extended trading Monday after the software company reported quarterly results that surpassed analyst revenue and earnings estimates. GitLab reported a fiscal third-quarter net loss of $285.2 million, or $1.84 a share, compared with a net loss of $48.5 million, or 33 cents a share, in the same quarter a year ago. Adjusted earnings were 9 cents a share. Revenue catapulted 32% to $149.7 million from $113 million in the same quarter a year earlier. Analysts surveyed by FactSet had expected on average a net loss of a penny a share on revenue of $141.5 million. Shares of GitLab have advanced 16.5% this year. The S&P 500 index

SPX,

is up 19%.

[ad_2]

[ad_1]

A rally in the U.S. stock and bond markets in the past week defied the bears and fueled hopes for more gains to come by year-end and in 2024 as Wall Street bought into the idea that the economy will pull off a “soft landing” after a run of interest-rate hikes by the Federal Reserve.

But market skeptics are putting investors on alert that the “soft-landing” scenario is still at risk with consumer spending and job growth slowing, along with corporate earnings.

“The equity market is misguided,” said Josh Schachter, senior portfolio manager at Easterly Investment Partners, in a phone interview with MarketWatch. “The markets are behaving in almost a bipolar fashion — some asset classes such as bonds

BX:TMUBMUSD10Y,

oil

BRN00,

and dollar

DXY,

are being priced for a recession, while other assets such as equities and bitcoin

BTCUSD,

are priced risk-on.”

U.S. stocks built on their November gains in the past week, with the S&P 500 index

SPX

ending at new 2023 high on Friday and the Dow Jones Industrial Average

DJIA

logging its fifth week in the green. The rebound in stocks was due in part to bond investors starting to believe the Fed is done raising interest rates and is likely to begin cutting them by the first quarter of 2024.

Meanwhile, the narrative that a resilient labor market and steadier-than-expected economic growth should keep a recession at bay has gained traction, bolstering the “goldilocks” scenario for the financial markets.

However, signs are emerging that consumer spending, which accounts for about 70% of the U.S. economic output and has boosted the economy this year, has likely run its course following the post-pandemic recovery. Credit card and car loan delinquency rates are rising, student loan payments have resumed, consumer spending is cooling, and there are warnings from top retailers.

Joseph Quinlan, head of CIO market strategy for Merrill and Bank of America Private Bank, said the “softness” in the U.S. consumer sector is visible but not huge, referring to that as “a canary in a coal mine,” he told MarketWatch via phone on Thursday.

The pullback in consumer spending is welcome news for Fed officials, who have increased interest rates 11 times since March 2022 to get inflation back to its preferred target of 2%. However, some analysts are worried that high interest rates and a decline in pandemic savings could eventually translate to weaker consumers in 2024, potentially another sign of a long-predicted slowdown in the U.S. economy.

“One of the things I’m most concerned about is consumers’ ability to continue to pace the economy — you’ve got several headwinds that haven’t really borne completely out yet,” said Jason Heller, senior executive vice president at Coastal Wealth. “Does the consumer continue to behave the way they behaved the last 36 months? I think you will eventually see a slowdown in consumer spending which is going to mandate a slowdown in the labor market.”

Lauren Goodwin, economist and portfolio strategist at New York Life Investments, acknowledged that a modest slowdown in inflation and employment growth means that a “Fed relief rally” in stocks can be sustained, but her concern is this late-cycle limbo is no different than those of the past, which is a moment of “goldilocks” before the very reason that inflation is moderating — slowing economic growth and employment — becomes clear in the data.

See: ‘We Are Still Headed for a Pretty Hard Landing,’ Ex-Treasury Secretary Larry Summers Says

That’s why the November employment report, which will be released by the Bureau of Labor Statistics next Friday at 8:30 a.m. Eastern, will be key for investors to watch. The U.S is expected to add 172,500 jobs in November after a 150,000 increase in the prior month, according to economists polled by Dow Jones. The percentage of jobless Americans seeking work is forecast to stay the same at 3.9%, leaving it at the highest level since the beginning of 2022.

See: U.S. job growth pick up on the radar this coming week

In fact, nonfarm payroll report publication days have been among the most volatile for stocks in 2023, compared with the release of monthly consumer-price index readings, which sparked some of the biggest daily up and down moves for the S&P 500 and other major indexes in 2022.

See also: Do CPI days still rock the stock market? How 2023 stacks up to 2022

This year, the S&P 500 saw an absolute average percentage change of 1.12% on employment situation release dates, compared with an average percentage move of 0.64% on CPI days, according to figures compiled by Dow Jones Market Data.

That said, analysts are skeptical if the employment data is able to tell “a radically different story” but suggest the labor market will remain relatively tight into 2024, said Quinlan and Lauren Sanfilippo at Merrill and Bank of America Private Bank, in a phone interview.

See: What 2024 S&P 500 forecasts really say about the stock market

Corporate America and their shares are telling investors a different story about next year.

With an estimated average S&P 500 earnings growth of 11.7% next year, the U.S. stock market is nowhere near recessionary concerns, said Heller. “We’ve [the stocks] priced in pretty significant growth in 2024.”

Strategists at Merrill and Bank of America Private Bank are in the camp of expecting a “mid-single digit” earnings growth for the S&P 500 in 2024, as earnings have troughed and the economy will fall back to the 2%-level of real growth after high rates confine consumer spending and corporate profits, cooling a red-hot economy.

To be sure, Wall Street analysts tend to overestimate the earnings-per-share (EPS) for the S&P 500, said John Butters, senior earnings analyst at FactSet.

The current bottom-up EPS estimate for the S&P 500 in 2024 is $246.30. If that holds true, that would be the highest EPS number reported by the large-cap index since FactSet began tracking this metric in 1996.

However, over the past 25 years, the average difference between the EPS estimate at the beginning of the year and the actual EPS number has been 6.9%, meaning analysts on average have overestimated the earnings one year in advance, said Butters in a Friday note (see chart below).

[ad_2]

[ad_1]

U.S. stocks powered higher on Friday, shrugging off tough talk from Federal Reserve Chairman Jerome Powell about it being too early to talk about rate cuts. The Dow Jones Industrial Average

DJIA,

gained about 294 points, or 0.8%, ending near 36,245, according to preliminary FactSet data. The S&P 500 index

SPX,

rose 0.6%, while the Nasdaq Composite Index

COMP,

gained 0.6%. All three indexes also ended the week higher for five straight weeks. The gains allowed the Dow to clinch its highest close since since January 2022, while the S&P 500 finished at its highest level since March 2022, according to Dow Jones Market Data. The powerful rally in equities since early November has been attributed to easing inflation, falling long-term Treasury yields and expectations for rate cuts next year The 10-year Treasury yield

TMUBMUSD10Y,

fell to 4.225% on Friday, after hitting 5% in October, ending the week at its lowest yield since early September, according to DJMD.

[ad_2]