NEW YORK (AP) — U.S. stocks opened with modest gains Monday, as earnings season kicks into a higher gear and investors eye the next policy meeting of the Federal Reserve.

The S&P 500 rose 0.4%. The index is coming off its second weekly loss in a row. The Dow Jones Industrial Average gained 184 points, or 0.4%, as of 9:45 a.m. ET. The Nasdaq added 0.3%.

The major airlines were slightly lower in early trading after thousands of flights were canceled due to a massive winter storm that affected travel from the Rockies all the way to the East Coast. Delta and United each fell 1.2%.

USA Rare Earth, an Oklahoma-based miner of critical minerals, became the latest company to get a boost from an investment by the U.S. government. Shares rose 25%.

Gold gained another 2%, and topped $5,000 an ounce for the first time, while silver jumped 8.6% to around $110 per ounce. The value of precious metals has surged in recent months as investors sought relatively safe places to invest amid rising geopolitical uncertainty.

Natural gas futures climbed another 2.2% as cold weather set in across the country following the winter storm that dumped more than a foot of snow in places and left many without power.

Investors will also be paying close attention to the latest developments at the U.S. Federal Reserve, where officials meet this week to decide where to take interest rates. Most expect central bank officials to stand pat after they cut rates at the final three meetings of 2025.

Markets this week will be focused on corporate earnings, some of which might show the negative effects from recent U.S. tariff policies.

This week will feature the latest financial results from United Airlines, Boeing, General Motors, Meta, Microsoft and Apple.

Markets in Europe showed small gains. In Asia, Japan’s benchmark took a tumble after the yen rebounded against the U.S. dollar on rumors of possible government intervention. The Nikkei 225 index dropped 1.8%.

The Japanese yen has been weakening against the U.S. dollar, and many other major currencies, since 2021. So Japanese consumers and companies pay more now for imported food, fuel and other items needed to keep the world’s fourth largest economy running.

The dollar slipped to 153.83 Japanese yen from 155.01 yen. It had been trading around 158 yen last week.

Peter Schiff claimed Bitcoin is now one of Wall Street’s worst-performing assets, renewing his long-running criticism.

Nate Geraci has responded to Peter Schiff’s latest criticism of Bitcoin (BTC), challenging his claim that the cryptocurrency is lagging behind.

This comes as data reveals that investors have shifted toward precious metals over the past year.

Schiff Calls Out Bitcoin’s Poor Performance

Schiff, a long-time Bitcoin skeptic, recently took to social media to say that the flagship cryptocurrency is now one of the “worst performing assets” on Wall Street.

“Bitcoin was the best performing asset during a time period when hardly anyone owned it. But ever since Wall Street embraced it and most people bought it, it’s been one of the worst performing assets,” he wrote.

However, Geraci, president of NovaDius Wealth Management, has disagreed with this view. The analyst responded to him on X, pointing out that Bitcoin has been outperforming the S&P 500, stating:

“Spot BTC ETFs shattered every ETF launch record (i.e., ‘Wall St embraced it & most people bought it’).”

He further explained that the cryptocurrency has risen roughly 90% since the ETFs debuted, compared with gains of less than 50% in the broader stock market, expressing frustration with the economist’s constant bearish outlook of the digital asset.

Schiff has repeatedly criticized Bitcoin on social media in recent months, arguing that it has failed to live up to its reputation as “digital gold,” while also praising the performance of its traditional precious metals counterparts. Last December, he celebrated gold’s surge past $4,400 by challenging his followers with a poll asking whether the metal would hit $5,000 first or the leading cryptocurrency would plunge to $50,000.

The financial commentator has also previously suggested that Bitcoin’s collapse will occur before any crisis involving the U.S. dollar unfolds.

You may also like:

Shifting Market Dynamics

A new report from Santiment shows that market dynamics are changing, with rising uncertainty about the world’s future outlook pushing investors toward precious metals.

Data indicates that over the past year, silver has surged by 214%, gold has climbed 77%, and Bitcoin has dropped 16%. This divergence could be interpreted as a bullish sign for the lagging crypto market, as the performance of “digital gold” and metals has frequently alternated over the past decade, with Bitcoin often leading during specific cycles.

However, some analysts argue that this preference for physical assets could represent a new long-term trend in the market. Overall, institutional investors have been steadily accumulating crypto, a pattern that has been consistent since late November last year.

SPECIAL OFFER (Exclusive)

SECRET PARTNERSHIP BONUS for CryptoPotato readers: Use this link to register and unlock $1,500 in exclusive BingX Exchange rewards (limited time offer).

NEW YORK (AP) — Stocks rose on Wall Street Tuesday morning and approached more all-time highs.

The S&P 500 added 0.4% and is sitting just below the record it set in late December. The Dow Jones Industrial Average rose 158 points, or 0.3%, after setting a record on Monday. The Nasdaq composite rose 0.4% as of 10:10 a.m. Eastern.

Big technology companies were behind much of the market’s gains. Nvidia jumped 1.5% and was the biggest single force behind the market’s gains. It is among the most valuable companies in the world and its outsized valuation gives it more influence in the market.

Nvidia’s gain, along with a 7.4% gain for Micron, helped counter Apple’s 0.8% loss.

Technology companies, especially those focused on artificial intelligence, are being closely watched this week during the industry’s annual CES trade show in Las Vegas.

AI advances helped propel the broader market to a series of records in 2025. Investors will be watching companies for any updates that could shed more light on the big corporate investments in AI technology.

The price of benchmark U.S. crude oil fell 0.3%, pulling back from sharp gains a day prior when the market reacted to U.S. forces capturing Venezuelan President Nicolás Maduro in a weekend raid.

Treasury yields rose in the bond market. The yield on the 10-year Treasury climbed to 4.18% from 4.15% late Monday. The yield on the two-year Treasury, which moves more closely with expectations for what the Federal Reserve will do, rose to 3.47% from 3.45% late Monday.

Gold prices rose 1% and silver prices rose 4.6%. Such assets are often considered safe havens in times of geopolitical turmoil. The metals have notched record prices over the last year amid lingering economic concerns brought on by conflicts and trade wars.

Outside of company announcements, Wall Street is preparing for several updates on the U.S. labor market this week.

AP business writers Elaine Kurtenbach and Matt Ott contributed to this report.

With U.S. stocks in the midst of a grim month, investors will look in the coming week for signs of strength in the U.S. consumer with Black Friday putting the spotlight on the holiday shopping season.

The rally in stocks has stalled in November, with the benchmark S&P 500 declining more than 4 percent so far during the month. Strong quarterly results from semiconductor giant Nvidia Corp failed on Thursday to calm markets, which have been rattled by concerns about elevated valuations and questions about returns on massive corporate investments in artificial intelligence infrastructure.

Consumer spending, which accounts for more than two-thirds of U.S. economic activity, will now come under Wall Street’s microscope.

The trading week will be interrupted by the Thanksgiving holiday on Thursday, followed by Black Friday, known for ushering in discounts, then Cyber Monday and holiday shopping promotions heading into year end.

An Inc.com Featured Presentation

Recent readings have shown a slump in consumer sentiment, while other data has been missing due to the government shutdown. This could make any signals about holiday spending more significant than usual.

“From a sentiment standpoint, the early reads we get on Black Friday and Cyber Monday, due to the lack of data we have, will be important,” said Chris Fasciano, chief market strategist at Commonwealth Financial Network.

“The entirety of the holiday shopping period will be an important read for where we are with the consumer and what that means for the economy.”

While the S&P 500 remains up 11 percent year-to-date, it has declined just over 5 percent from its late October all-time high. The Cboe Volatility index on Thursday posted its highest closing level since April.

Stock market performance could factor into how consumers spend over the holidays, particularly those with higher incomes who are more invested in equities. Despite the recent wobble, the S&P 500 has soared over 80 percent since its latest bull market began just over three years ago.

“If you get a pullback there, a lot of the wealth in the upper income is in the stock market … so it will be interesting to see if they spend like they have in the past,” said Doug Beath, global equity strategist at the Wells Fargo Investment Institute.

This month, the National Retail Federation said it expected U.S. holiday sales to surpass $1 trillion for the first time. Still, that November-December forecast equated to growth of between 3.7 percent and 4.2 percent from the year-earlier period, slower than the 4.3 percent growth in 2024.

Household balance sheets are “in a very strong place,” yet slowing employment growth could pressure holiday spending, said Michael Pearce, deputy chief U.S. economist at Oxford Economics.

“The most important factor for consumer spending is the health of the labor market,” Pearce said.

Data from the delayed monthly employment report released on Thursday showed U.S. job growth accelerated in September. But the unemployment rate increased to a four-year high of 4.4 percent.

Persistently firm inflation, with import tariffs contributing to higher prices, also could weigh on spending, Pearce said.

Holiday shopping is critical for retailers. Walmart on Thursday raised its annual forecasts in a signal of confidence heading into year end. Reports from other retailers during the week were mixed.

Another read on the consumer will come with Tuesday’s release of U.S. retail sales for September. That report has been delayed along with other government releases because of the 43-day federal shutdown that ended earlier this month.

The influx of pent-up data in the coming weeks could further ramp up volatility for investors as they assess the economy’s health and prospects that the Federal Reserve will cut interest rates at its December 9-10 meeting.

Following the September jobs report, which will be the last monthly employment release before the next Fed meeting, Fed funds futures late on Thursday reflected a 67 percent chance the central bank would hold rates steady in December after quarter-point cuts in each of the prior two meetings.

Morgan Stanley economists said on Thursday they no longer expected the Fed to ease in December but they project three cuts in 2026.

“The policy rate path remains highly data-dependent,” the Morgan Stanley economists said in a note. “In our view, a mixed report means the committee will want to see more data before taking another step.”

Reporting by Lewis Krauskopf; Editing by Alden Bentley and David Gregorio

Analyst compares BTC’s “flat correction” and deep drawdown to the S&P’s 61% crash before its explosive bull run.

A crypto analyst has suggested that Bitcoin (BTC) is tracing a historic pattern last seen in the S&P 500 before a massive 200% jump.

This comparison points to a potential, though not yet certain, launch into a period of exponential growth for the world’s leading cryptocurrency.

A Historical Blueprint for a Bull Run

In a detailed analysis, CrediBULL Crypto drew parallels between Bitcoin’s current price action and the S&P 500’s behavior between 2000 and 2008. The expert noted that both markets experienced mid-cycle tops characterized by extended periods of consolidation without a dramatic peak, called “flat corrections,” before starting the next major upward move.

Following these phases, the S&P 500 suffered a 61% drop, while Bitcoin saw a 76% decline, before each started its final, explosive rally. CrediBULL now says that BTC is at a stage similar to where the S&P 500 was just before it went parabolic, which was followed by a 200% price increase.

“On the SPX, just before we went parabolic, we saw a 37% correction to the downside. Which was immediately followed by new ATH and a 200+% rally off the lows to where we are today,” wrote the technician.

This optimistic outlook is coming at a time when the OG crypto is trying to find stability, currently trading around $92,000 after a difficult month that saw it fall over 14%. The comparison offers a counter-narrative to the bearish sentiment prevailing in the market, suggesting the recent downturn may be a typical, though sharp, correction within a larger bull cycle rather than its end.

CrediBULL insisted that a break of a short-term ascending trend line does not signify a breakdown in overall market structure, cautioning that traders who exited the S&P 500 on a similar technical break missed the huge rally that followed.

For Bitcoin, the trader highlighted $74,000 as the line that truly matters, telling one follower that the “trend line isn’t relevant – 74k is.” Until then, they see BTC “hugging” its main trendline rather than starting the vertical part of the move.

You may also like:

Market Sentiment and Diverging Views

The analyst community is divided on BTC’s immediate future. While the historical pattern offers a hopeful framework, other experts have pointed to lingering headwinds. One of them, Axel Bitblaze, observed that Bitcoin’s recent decline is quite similar to a pattern from early 2025, which ended in a final sharp shakeout. According to him, rising Japanese bond yields and liquidity issues at smaller U.S. banks could serve as potential catalysts for another downturn.

The market is also witnessing a flight of retail investors, with data from November 19 showing that small Bitcoin, Ethereum, and XRP wallets have been reducing their holdings, a behavior that, ironically, has often happened just before market recoveries.

Ultimately, the debate centers on whether Bitcoin is completing a final bearish shakeout or is on the cusp of a historic breakout. CrediBULL argues that the cryptocurrency, being a younger and faster-moving asset, could replicate the S&P’s parabolic move in a much shorter timeframe.

SPECIAL OFFER (Exclusive)

SECRET PARTNERSHIP BONUS for CryptoPotato readers: Use this link to register and unlock $1,500 in exclusive BingX Exchange rewards (limited time offer).

The Bitcoin price is positioning for a potentially explosive move that could take it well beyond its previous all-time highs. Analysts are closely watching a critical resistance level near $116,000, which may serve as the final hurdle before BTC catapults into uncharted territory above $126,000.

Analyst Predicts New Bitcoin Price All-Time High

Crypto analyst Donny Dicey revealed in an X social media post this week that the $116,000 price level is the decisive zone Bitcoin must breach to confirm a breakout toward a new all-time high. His technical analysis suggests that once BTC achieves a clean break above this resistance area, momentum could swiftly carry it above $126,000.

Related Reading

Notably, Bitcoin set a new ATH on October 6, 2025, after breaking through its previous record above $124,000 and climbing past $126,000. Since achieving this level, the price of BTC has fallen dramatically to $115,000. Dicey’s accompanying chart shows the market steadily recovering after testing support near $108,000, marked as a “market structure break” region, with bullish price action consolidating above $109,000.

The analyst has emphasized that each day Bitcoin maintains a close above $109,000 strengthens the probability of a strong upward swing as the market heads into November. This period coincides with the Federal Open Market Committee’s (FOMC) next meeting, where investors are anticipating dovish signals such as rate cuts or the formal end of Quantitative Tightening (QT).

Dicey also notes that bullish S&P 500 earnings, easing global trade tensions from a potential agreement between US President Donald Trump and China’s President Xi Jinping, and improving ISM manufacturing data point to a macro environment supportive of risk assets. A community member commented that whales may have underestimated how much BTC’s demand tends to persist during these conditions. Dicey responded that the same whales might become “exit liquidity” as Bitcoin accelerates higher, possibly missing out on the strongest phase of this cycle.

Consolidation Above January Highs Signal Unbreakable Strength

In a follow-up analysis, Dicey highlighted Bitcoin’s remarkable stability above its January highs, describing its price structure as “unbreakable” amid global macroeconomic uncertainty. He pointed to several converging factors that reinforce BTC’s resilience, including ongoing fiscal and monetary expansion, a weakening US dollar, and renewed confidence in the global business cycle.

Related Reading

The analyst also emphasized that geopolitical tensions tied to US-China relations appear to be subsiding. At the same time, ETF inflows and exponential growth in the Artificial Intelligence (AI) sector contribute to acting as tailwinds for digital assets. He disclosed that despite strong underlying fundamentals, skepticism remains widespread in the market.

According to him, many still believe in the traditional four-year cycle narrative, while retail enthusiasm has not fully returned. Furthermore, the Russell 2000 index has yet to breakout, and rotation from traditional assets, such as the S&P 500 and gold, into Bitcoin remains limited. With these developments subduing broader market participation, Dicey suggests it creates the perfect setup for a powerful rally in BTC once sentiment shifts decisively.

BTC trading at $115,411 on the 1D chart | Source: BTCUSDT on Tradingview.com

Featured image from Pixabay, chart from Tradingview.com

Earnings reports next week, including from Tesla and Netflix, will provide a deeper look at U.S. corporate profits while delayed U.S. inflation data will mark another test of the stock market, which has become shakier even as it remains around record highs.

The fourth year of the S&P 500’s bull run kicked off this week with some significant gyrations after a long period of market calm.

Revived U.S.-China trade tensions and credit concerns at regional U.S. banks drove the anxiety. The CBOE market volatility index, known as Wall Street’s “fear gauge”, has surged in recent days and hit its highest level in nearly six months on Friday.

“The market is becoming more volatile, but it’s also coming off of a very non-volatile period where we didn’t have a lot of risk catalysts bubbling to the top,” said Michael Reynolds, vice president of investment strategy at Glenmede.

An Inc.com Featured Presentation

“Once you have valuations hit sort of full levels, as we’re seeing now almost across the board, you have to be on the lookout for incremental risk catalysts.”

The spark for the latest volatility was a surprise resurgence in U.S.-China trade tensions. Stocks slumped late last week after the U.S. threatened to significantly hike tariffs by November 1 over China’s rare-earth export controls.

The U.S.-China trade issue will be key for markets in the coming week, said Doug Beath, global equity strategist at Wells Fargo Investment Institute. U.S. President Donald Trump confirmed on Friday that he would meet with Chinese President Xi Jinping in two weeks in South Korea.

Sharp swings in global financial shares to end the week also kept investors on edge as they weighed the extent of credit concerns emerging from regional U.S. banks.

Major stock indexes posted weekly gains and are on pace for strong years. The benchmark S&P 500 is up 13.3 percent year-to-date and 1.3 percent below its record high. But there are signs the market is weakening under the surface.

The percentage of S&P 500 stocks in some form of an uptrend declined from 77 percent in early July to 57 percent as of Tuesday while the number of stocks in a downtrend increased from 23 percent to 44 percent over that time, according to Adam Turnquist, chief technical strategist for LPL Financial.

That “narrowing gap highlights emerging cracks in the market’s foundation,” Turnquist said in written commentary. Similarly, Kevin Gordon, senior investment strategist at Charles Schwab, said he will be watching how broadly based the market’s gains are going forward.

“If you have a fewer number of companies that are actually moving higher, but the indexes do move higher because of the megacaps, that’s a really important divergence,” Gordon said.

Attention will be on third-quarter earnings after major banks started the reporting season on a strong note. Aside from streaming giant Netflix and electric vehicle maker Tesla, other companies due to report in the coming week include consumer companies Procter & Gamble and Coca-Cola, aerospace and defense giant RTX and tech stalwart IBM.

The corporate results and executive comments will offer insight into the economy as the U.S. government shutdown has stopped economic data releases since October 1, including monthly employment data.

Corporate “reports and what companies say is really our best chance at assessing what the broader economic health is,” Gordon said.

The government has said it will release the U.S. consumer price index for September on Friday, nine days late, saying the CPI data allows the Social Security Administration to meet deadlines for timely payment of benefits.

The CPI report, which is a closely watched inflation gauge, will be released days before the Federal Reserve’s next monetary policy meeting on October 28-29. The U.S. central bank is widely expected to cut interest rates by a quarter percentage point again, after weakening jobs data prompted the Fed to lower rates last month for the first time this year.

“We’d really have to see something out of left field in terms of notable inflation pressures to knock the Fed off of a rate cut path at the October meeting,” Glenmede’s Reynolds said.

Reporting by Lewis Krauskopf; Editing by David Gregorio and Cynthia Osterman

“Don’t worry about China, it will all be fine!” he wrote. “Highly respected President Xi just had a bad moment. He doesn’t want Depression for his country, and neither do I. The U.S.A. wants to help China, not hurt it!!!”

Meanwhile, Vice President JD Vance told Fox News’s Sunday Morning Futures that the U.S. is willing to be reasonable if China is too, though he insisted Trump has the upper hand with “far more cards” than Beijing holds.

The shift in tone contrasts with Trump’s fiery rhetoric on Friday as he lashed out at China for its new export controls on rare earths, which are critical inputs across a range of industries.

“Market participants appear to be leaning into the TACO trade once more, fueled not only by what we’ve seen in the recent past, but also by conciliatory remarks over the weekend from both President Trump and Vice President Vance, suggesting that Friday’s announcement of additional 100% tariffs on Chinese imports are likely to be little more than a negotiating tactic,” Michael Brown, senior research strategist at Pepperstone, said in a note on Sunday.

Futures tied to the Dow Jones Industrial Average surged 382 points, or 0.84%. S&P 500 futures were up 1.27%, and Nasdaq futures jumped 1.79%.

The yield on the 10-year Treasury tumbled 8.9 basis points to 4.059%. The U.S. dollar was up 0.04% against the euro and up 0.48% against the yen. Gold climbed 1.43% to a new high of $4,057.50 per ounce. U.S. oil futures rose 1.29% to $59.66 a barrel, and Brent crude gained 1.32% to $63.56.

Trump had previously imposed 145% tariffs on China, then put them on hold to allow negotiations to play out. A similar pattern played out with other trade partners like the European Union, causing Wall Street to dismiss maximalist threats with the TACO (Trump always chickens out) trade.

Brown said Trump’s new China tariff, which would go into effect Nov. 1 and bring the overall level to 130%, appears to be another example of his “escalate to de-escalate” strategy.

“Assuming that this is another ‘TACO’ situation, and some clarity on that front is obtained before too long, then this is likely to prove another dip in equities that should be viewed as a buying opportunity, with the path of least resistance continuing to lead higher, if in somewhat choppy fashion,” he added.

At the same time, the Federal Reserve’s shift back to rate cuts amid still-solid economic growth should continue to boost to the dollar, which will likely shrug off tariff threats, Brown predicted.

Similarly, market veteran Ed Yardeni, president of Yardeni Research, also sees the U.S. and China pulling back from the precipice.

“If neither side were to blink, the US and Chinese economies would lead the global economy into a deep recession, if not a depression,” he wrote in a note on Sunday. “But we expect that both sides will blink very soon given the extremely adverse consequences of a trade war between the world’s two biggest economies.”

For its part, Beijing remained defiant, with the commerce ministry saying Sunday that China doesn’t want a tariff war but is also not afraid of one. It also said the export controls are not a ban on rare earth shipments but are a sovereign right.

But China’s new rare earth export policy ups the ante well beyond another tit-for-tat exchange in the trade war against the U.S.

Dean Ball, who served as a senior advisor in the White House Office of Science and Technology Policy earlier this year, wrote on X on Saturday that the policy gives Beijing the power to “forbid any country on Earth from participating in the modern economy.”

Dali Yang, a political science professor at the University of Chicago, sounded a similar alarm in a post on Sunday, saying the move marks a decisive moment that reveals what a China-led order might look like.

Looking beyond rare earths, it’s one that leverages control over strategic materials and technologies to prop up global influence.

“China is effectively saying: ‘We control the arteries of high-tech civilization.’ The rest of the world now sees that message clearly—and is scrambling to build new circulatory systems,” Yang wrote.

Fortune Global Forum returns Oct. 26–27, 2025 in Riyadh. CEOs and global leaders will gather for a dynamic, invitation-only event shaping the future of business. Apply for an invitation.

us dollar, bitcoin all time high, gold rally, silver, inflation, fed rate cut,. Photo by BeInCrypto

Markets are witnessing extraordinary rallies across both risk and safe-haven assets. The S&P 500, gold, silver, and Bitcoin (BTC) are all trending higher.

Experts argue that the economy appears to be doing well, but this prosperity is deceptive. It’s not driven by productivity or innovation but by a loss of confidence in fiat currencies, especially the US dollar.

In a detailed thread on X (formerly Twitter), The Kobeissi Letter, highlighted a notable financial moment — where everything is going up at once, from risky assets like stocks to traditional safe havens like gold and Bitcoin.

BeInCrypto reported yesterday that Bitcoin broke $125,000 amid its Uptober rally. The coin has appreciated 10.6% over the past week, marking a strong start to Q4. At the same time, silver and gold have also gained strongly. The former’s value has increased by more than 60% in 2025.

“Gold has hit 40 record highs in 2025 and is now worth a whopping $26.3 trillion. That’s more than 10 times the value of Bitcoin. Gold, Silver, and Bitcoin are now all in the top 10 largest assets in the world,” the post read.

Historically, safe-haven assets tend to perform best when investors are seeking protection from falling stock markets or economic instability. However, this cycle is defying that pattern. Risk assets and safe havens are now rising together, suggesting a deeper shift in global investor behavior.

The S&P 500 has jumped over 39% in six months, adding trillions in market value. Meanwhile, the Nasdaq 100 has gained for six consecutive months — a rare streak seen only six times since 1986.

“And, the Magnificent 7 companies are investing a record $100B+ per quarter in CapEx to fuel the AI Revolution,” The Kobeissi Letter mentioned.

The post pointed out that the correlation between gold and the S&P 500 reached a record 0.91 in 2024.

“This means that Gold and the S&P 500 were moving in TANDEM 91% of the time,” the analysis revealed.

This raises a critical question: Are markets genuinely strong, or is something else behind the broader rally?

Market analysts argue this does not reflect real economic expansion but rather a weakening trust in the US dollar. Notably, this year has been quite harsh for the greenback. According to The Kobeissi Letter, the US dollar is heading toward its worst annual performance since 1973.

For historical context, in 1973, the dollar experienced a sharp decline, one of the most dramatic in modern history, due to the collapse of the Bretton Woods system and the end of the gold standard.

So far, this year, the dollar has dipped 10%. Moreover, since 2020, the dollar has also lost roughly 40% of its purchasing power.

Furthermore, things could turn for the worse for the currency. According to the CME FedWatch Tool, markets are pricing in a 95.7% probability that the Fed will cut rates again at its October meeting, following a recent reduction in September. Such easing could accelerate the dollar’s downtrend.

“The Fed is cutting rates into 4.0% annualized inflation since 2020. And, the Fed is cutting rates into 2.9%+ Core PCE inflation for the first time since the 1990s. What’s really happening here is assets are pricing in a new era of monetary policy. When safe haven assets, risky assets, real estate, and inflation are all rising together, it’s a macro-based shift. The Fed has zero control of long-term yields,” The Kobeissi Letter noted.

Market commentator Shanaka Anslem Perera described the phenomenon as an ‘illusion of prosperity,’ with rising asset prices driven by investors moving away from fiat currencies.

“The Fed is cutting rates into inflation, printing credibility while calling it policy. When gold, Bitcoin, equities, and real estate all rise together, it’s not a bull market … it’s monetary panic in slow motion,” Perera explained.

He stressed that the simultaneous surge across asset classes suggests that wealth is not being created, but the dollar’s purchasing power is collapsing. In this view, the denominator — the currency itself — is dying.

“This is not a boom. It’s the endgame of a system priced in paper and powered by illusion,” Perera remarked.

Thus, as markets surge and the dollar weakens, the rally reflects more than optimism. Rather than signaling economic strength, it underlines a shift in what investors trust. Markets aren’t celebrating growth — they’re bracing for change.

The government shutdown that began Wednesday will deprive policymakers and investors of economic data vital to their decision-making at a time of unusual uncertainty about the direction of the U.S. economy.The absence will be felt almost immediately, as the government’s monthly jobs report scheduled for release Friday will likely be delayed. A weekly report on the number of Americans seeking unemployment benefits — a proxy for layoffs that is typically published on Thursdays — will also be postponed.If the shutdown is short-lived, it won’t be very disruptive. But if the release of economic data is delayed for several weeks or longer, it could pose challenges, particularly for the Federal Reserve. The Fed is grappling with where to set a key interest rate at a time of conflicting signals, with inflation running above its 2% target and hiring nearly ground to a halt, driving the unemployment rate higher in August.The Fed typically cuts this rate when unemployment rises, but raises it — or at least leaves it unchanged — when inflation is rising too quickly. It’s possible the Fed will have little new federal economic data to analyze by its next meeting on Oct. 28-29, when it is widely expected to reduce its rate again.“The job market had been a source of real strength in the economy but has been slowing down considerably the past few months,” said Michael Linden, senior policy fellow at the left-leaning Washington Center for Equitable Growth. “It would be very good to know if that slowdown was continuing, accelerating, or reversing.”The Fed cut its rate by a quarter-point earlier this month and signaled it was likely to do so twice more this year. Fed officials said they would keep a close eye on how inflation and unemployment evolve, but that depends on the data being available.A key inflation report is scheduled for Oct. 15 and the government’s monthly retail sales report is slated for release the next day.“We’re in a meeting-by-meeting situation, and we’re going to be looking at the data,” Fed Chair Jerome Powell said during a news conference earlier this month.The economic picture has recently gotten cloudier. Despite slower hiring, there are signs that overall economic growth may be picking up. Consumers have stepped up their shopping and the Federal Reserve Bank of Atlanta estimates the economy likely expanded at a healthy clip in the July-September quarter, after a large gain in the April-June period.A key question for the Fed is whether that growth can revive the job market, which this Friday’s report might have helped illustrate. Economists had forecast another month of weak hiring, with just 50,000 new positions added, according to a survey by FactSet. The unemployment rate was projected to stay at a still-low 4.3%.On Wall Street, investors obsess over the monthly jobs reports, typically issued the first Friday of every month. It’s a crucial indicator of the economy’s health and provides insights into how the Fed might adjust interest rates, which affects the cost of borrowing and influences how investors allocate their money.So far, investors don’t seem fazed by the shutdown. The broad S&P 500 stock index rose slightly Wednesday to an all-time high.Many businesses also rely on government data to gauge how the economy is faring. The Commerce Department’s monthly report on retail sales, for example, is a comprehensive look at the health of U.S. consumers and can influence whether companies make plans to expand or shrink their operations and workforces.For the time being, the Fed, economists, and investors will likely focus more on private data.On Wednesday, the payroll provider ADP issued its monthly employment data, which showed that businesses cut 32,000 jobs in September — a signal the economy is slowing. Still, ADP chief economist Nela Richardson said her firm’s report “was not intended to be a replacement” for government statistics.The ADP data does not capture what’s happening at government agencies, for example — an area of the economy that could be significantly affected by a lengthy shutdown.“Using a portfolio of private sector and government data gives you a better chance of capturing a very complicated economy in a complex world,” she said.The Fed will remain open no matter how long the shutdown lasts, because it funds itself from earnings on the government bonds and other securities it owns. It will continue to provide its monthly snapshots of industrial production, which includes mining, manufacturing, and utility output. The next industrial production report will be released Oct. 17.

NEW YORK —

The government shutdown that began Wednesday will deprive policymakers and investors of economic data vital to their decision-making at a time of unusual uncertainty about the direction of the U.S. economy.

The absence will be felt almost immediately, as the government’s monthly jobs report scheduled for release Friday will likely be delayed. A weekly report on the number of Americans seeking unemployment benefits — a proxy for layoffs that is typically published on Thursdays — will also be postponed.

If the shutdown is short-lived, it won’t be very disruptive. But if the release of economic data is delayed for several weeks or longer, it could pose challenges, particularly for the Federal Reserve. The Fed is grappling with where to set a key interest rate at a time of conflicting signals, with inflation running above its 2% target and hiring nearly ground to a halt, driving the unemployment rate higher in August.

The Fed typically cuts this rate when unemployment rises, but raises it — or at least leaves it unchanged — when inflation is rising too quickly. It’s possible the Fed will have little new federal economic data to analyze by its next meeting on Oct. 28-29, when it is widely expected to reduce its rate again.

“The job market had been a source of real strength in the economy but has been slowing down considerably the past few months,” said Michael Linden, senior policy fellow at the left-leaning Washington Center for Equitable Growth. “It would be very good to know if that slowdown was continuing, accelerating, or reversing.”

The Fed cut its rate by a quarter-point earlier this month and signaled it was likely to do so twice more this year. Fed officials said they would keep a close eye on how inflation and unemployment evolve, but that depends on the data being available.

A key inflation report is scheduled for Oct. 15 and the government’s monthly retail sales report is slated for release the next day.

“We’re in a meeting-by-meeting situation, and we’re going to be looking at the data,” Fed Chair Jerome Powell said during a news conference earlier this month.

The economic picture has recently gotten cloudier. Despite slower hiring, there are signs that overall economic growth may be picking up. Consumers have stepped up their shopping and the Federal Reserve Bank of Atlanta estimates the economy likely expanded at a healthy clip in the July-September quarter, after a large gain in the April-June period.

A key question for the Fed is whether that growth can revive the job market, which this Friday’s report might have helped illustrate. Economists had forecast another month of weak hiring, with just 50,000 new positions added, according to a survey by FactSet. The unemployment rate was projected to stay at a still-low 4.3%.

On Wall Street, investors obsess over the monthly jobs reports, typically issued the first Friday of every month. It’s a crucial indicator of the economy’s health and provides insights into how the Fed might adjust interest rates, which affects the cost of borrowing and influences how investors allocate their money.

So far, investors don’t seem fazed by the shutdown. The broad S&P 500 stock index rose slightly Wednesday to an all-time high.

Many businesses also rely on government data to gauge how the economy is faring. The Commerce Department’s monthly report on retail sales, for example, is a comprehensive look at the health of U.S. consumers and can influence whether companies make plans to expand or shrink their operations and workforces.

For the time being, the Fed, economists, and investors will likely focus more on private data.

On Wednesday, the payroll provider ADP issued its monthly employment data, which showed that businesses cut 32,000 jobs in September — a signal the economy is slowing. Still, ADP chief economist Nela Richardson said her firm’s report “was not intended to be a replacement” for government statistics.

The ADP data does not capture what’s happening at government agencies, for example — an area of the economy that could be significantly affected by a lengthy shutdown.

“Using a portfolio of private sector and government data gives you a better chance of capturing a very complicated economy in a complex world,” she said.

The Fed will remain open no matter how long the shutdown lasts, because it funds itself from earnings on the government bonds and other securities it owns. It will continue to provide its monthly snapshots of industrial production, which includes mining, manufacturing, and utility output. The next industrial production report will be released Oct. 17.

Shares of Robinhood jumped 7% in after-hours trading Friday after the retail brokerage was named to the S&P 500.

Key Takeaways:

Robinhood shares jumped 7% after being added to the S&P 500, joining the index on September 22.

Strategy, despite a $95B valuation and $70B in Bitcoin holdings, was left out of the reshuffle.

Robinhood posted strong Q2 earnings, with $989M in revenue and $386M in profit.

Robinhood (HOOD) closed just above $101 and soared past $108 in extended trading following the announcement.

The company’s share price has climbed over 150% year-to-date, driven by strong earnings and growing retail interest in stocks and crypto.

Robinhood will officially join the index on September 22, alongside ad-tech firm AppLovin, according to S&P Dow Jones Indices.

While Robinhood celebrates its inclusion, Strategy, the Bitcoin treasury firm formerly known as MicroStrategy, was left off the list, despite meeting S&P’s $20 billion market cap requirement.

Strategy, which now holds more than $70 billion in Bitcoin, saw its shares fall 3% in after-hours trading following the announcement.

The omission surprised some observers, given Strategy’s $95 billion valuation and its pioneering role in bringing Bitcoin to public balance sheets.

Based in Tysons Corner, Virginia, the company has become synonymous with corporate crypto adoption.

The S&P reshuffle comes amid rising institutional interest in digital assets and a more favorable political environment.

Earlier this year, Coinbase was added to the S&P index, signaling growing recognition of crypto-native companies in traditional financial markets.

Robinhood’s strong fundamentals further fueled its rally. In Q2, the company posted $989 million in revenue, up 45% year-over-year, beating Wall Street estimates.

Net income hit $386 million, with earnings per share of $0.42, well above analyst forecasts.

Crypto trading revenue came in at $160 million, nearly doubling year-over-year but down from the previous quarter’s $252 million.

Meanwhile, income from options trading and equities reached $265 million and $66 million, respectively, making options Robinhood’s top revenue stream once again.

Last month, Robinhood Derivatives took legal action against regulators in Nevada and New Jersey, accusing the states of unfairly blocking its entry into the sports event contracts market, despite recent federal court rulings in favor of rival platform Kalshi.

The firm said it began offering event contracts in both states after federal judges ruled earlier this year that Nevada and New Jersey gaming regulators could not enforce their bans against Kalshi, which offers contracts regulated by the U.S. Commodity Futures Trading Commission (CFTC).

Robinhood argued that regulators have ignored those rulings and continued to threaten enforcement action, creating an uneven playing field.

“If state regulators are permitted to act against Robinhood but not Kalshi, then Robinhood will lose out in the sports event contracts space,” the company said in its filings.

Meanwhile, Robinhood has come under regulatory fire in the EU after launching tokenized stock products linked to private companies like OpenAI and SpaceX.

The Bank of Lithuania confirmed it is investigating the legality and investor disclosures related to these blockchain-based “Stock Tokens,” which launched on June 30.

OpenAI publicly disavowed any connection, stating it never approved the tokens and warning investors to be cautious.

On-chain analytics platform Santiment has weighed in on whether the Bitcoin price has reached its bottom, following its drop to the $108,000 range. The platform alluded to the current social sentiment, suggesting that a further drawdown may be looming.

Bitcoin Price Bottom Not Yet In Amid Spike In Social Dominance

In a research report, Santiment indicated that the Bitcoin price bottom may not yet be in, considering the surge in the social dominance of ‘buy the dip’ mentions. The platform explained that a true bottom is often marked not by price but by a shift in social narrative from ‘buy the dip’ optimism to widespread fear. This creates a strong bearish case that discourages buying.

Related Reading

Santiment suggested that the Bitcoin price typically rebounds when the sentiment is bearish and when investors least expect an uptrend. However, for now, market participants are still getting “antsy and trying to find some entry spots now that prices have cooled down a bit, Santiment analyst Brian Quinlivan explained.

The analyst opined that the cooldown in the Bitcoin price so far is not a huge one, while noting that BTC has detached from the S&P 500. Quinlivan predicted that BTC and other crypto assets could play catch-up to the stock market when the crowd stops getting too optimistic about buying the dip. He added that the true ‘buy the dip’ opportunities happen when the crowd stops believing there is an opportunity.

In the research report, Santiment noted that the current ‘buy the dip’ chatter needs to be suddenly replaced by discussion of the narrative that supports the bearish case. In line with this, the platform advised market participants to pay close attention to the dominant social narrative. According to the report, when the conversation shifts from hopeful buying to widespread fear, it can be a stronger bottom signal than the Bitcoin price alone.

Another Metric To Keep An Eye On

The Santiment report indicated that BTC whale transfers are another key metric to watch for, as they can help determine if the Bitcoin price has reached its bottom. These whales, wallets holding 10 to 10,000 BTC, have not been selling off in any significant way despite the market dip.

Related Reading

According to Maksim, who joined Santiment analyst Brian on the podcast, whenever these wallets do decrease their holdings, it can lead to “postponed price suppression weeks thereafter.” Therefore, Santiment advised market participants to monitor the holdings of large Bitcoin wallets. A lack of selling from whales could indicate underlying strength, while a significant drop can be a warning of future price weakness.

At the time of writing, the Bitcoin price is trading at around $107,800, down in the last 24 hours, according to data from CoinMarketCap.

BTC trading at $109,600 on the 1D chart | Source: BTCUSDT on Tradingview.com

Featured image from Pixabay, chart from Tradingview.com

(Bloomberg) — Stocks struggled for direction as traders weighed prospects of a slower pace of Federal Reserve rate cuts. Treasury 10-year yields hovered near 4.2%.

Most Read from Bloomberg

Wall Street are paring back bets on aggressive policy easing as the US economy remains robust and Fed officials have sounded a cautious tone over the pace of future rate decreases. Rising oil prices and the prospect of bigger fiscal deficits after the upcoming presidential election are only compounding the market’s concerns. Since the end of last week, traders have trimmed the extent of expected Fed cuts through September 2025 by more than 10 basis points.

“Of course, higher yields do not have to be negative for stocks. Let’s face it, the stock market has been advancing as these bond yields have bee rising for a full month now,” said Matt Maley at Miller Tabak + Co. “However, given how expensive the market is today, these higher yields could cause some problems for the equity market before too long.”

Exposure to the S&P 500 has reached levels that were followed by a 10% slump in the past, according to Citigroup Inc. strategists. Long positions on futures linked to the benchmark index are at the highest since mid-2023 and are looking “particularly extended,” the team led by Chris Montagu wrote in a note.

“We’re not suggesting investors should start to reduce exposure, but the positioning risks do rise when markets get extended like this,” they said.

The S&P 500 was little changed. The Nasdaq 100 rose 0.1%. The Dow Jones Industrial Average added 0.1%. The Russell 2000 of smaller firms slipped 0.2%. Texas Instruments Inc., which gets almost three-quarters of its revenue from industrial and automotive chips, reports results after the market close.

Treasury 10-year yield was little changed at 4.20%. Oil advanced as traders tracked tensions between Israel and Iran. Gold climbed to a fresh record. Options traders are increasing bets that Bitcoin will reach a record high of $80,000 by the end of November no matter who wins the US presidential election.

The stock market has rallied this year thanks to a resilient economy, strong corporate profits and speculation about artificial-intelligence breakthroughs — sending the S&P 500 up over 20%. Yet risks keep surfacing: from a tight US election to war in the Middle East and uncertainty around the trajectory of Fed easing.

“While recent data indicate a more resilient US economy than previously thought, the broad disinflation trend is still intact, and downside risks — albeit lower — to the labor market remain,” said Solita Marcelli at UBS Global Wealth Management. “We continue to expect a further 50 basis points of rate cuts in 2024 and 100 basis points of cuts in 2025. This should bring Treasury yields lower.”

A string of stronger-than-estimated data points sent the US version of Citigroup’s Economic Surprise Index to the highest since April. The gauge measures the difference between actual releases and analyst expectations.

“On the back of September’s strong economic data, markets have already priced a slower pace of cuts,” said Lauren Goodwin at New York Life Investments. “If the Fed is able to move towards a 4% policy rate — still above the levels most believe represent the ‘neutral’ rate — then the equity market rally can continue. Disruptions to that view make equity market volatility more likely.”

Most Fed officials speaking earlier this week signaled they favor a slower tempo of rate reductions. Policymakers at their meeting last month began lowering rates for the first time since the onset of the pandemic. They cut their benchmark by a half percentage point, to a range of 4.75% to 5%, as concern mounted that the labor market was deteriorating and as inflation cooled close to the Fed’s 2% goal.

“We can point to a few reasons for the rise in global long rates but one possibility is that markets are giving a big thumbs down to central banks easing policy before we’ve seen a sustainable drop in inflation.” said Peter Boockvar author of The Boock Report. “I remain bearish on the long end and bullish on the short end.”

The last time US government bonds sold off this much as the Fed started cutting interest rates, Alan Greenspan was orchestrating a rare soft landing.

Two-year yields have climbed 34 basis points since the Fed reduced interest rates on Sept. 18 for the first time since 2020. Yields rose similarly in 1995, when the Fed — led by Greenspan — managed to cool the economy without causing a recession.

In prior rate cutting cycles going back to 1989, two-year yields on average fell 15 basis points one month after the Fed started slashing rates.

Meantime, the International Monetary Fund said the US election is creating “high uncertainty” for markets and policymakers, given the sharply divergent trade priorities of the candidates. That gap creates the risk of another potential round of volatility on global markets similar to the rattling August selloff.

“Presidents don’t control markets,” said Callie Cox at Ritholtz Wealth Management. “Over time, the stock market’s common thread has been the economy and earnings, not who’s in the Oval Office. Be prepared for mood swings in markets as we get closer to Election Day. But remember that election-fueled storms often dissipate quickly.”

As the earnings season rolls in, US companies are reaping the best stock-market reward in five years for beating profit expectations that were lowered in the run-up to the reporting season.

S&P 500 firms that posted better-than-estimated third-quarter earnings have outperformed the benchmark by a median of 1.74% on the day of reporting results, according to data compiled by Bloomberg Intelligence. That’s the strongest rate in BI’s records going back to 2019.

At the same time, companies missing estimates trailed the S&P 500 by a median of 1.5%, a less severe underperformance than the 1.7% experienced in the second quarter, the data showed.

“This earnings season we are watching what companies are saying about inflation and the economy,” said Megan Horneman at Verdence Capital Advisors. “In addition, their view on interest rates, especially if the Fed cannot be as aggressive as the market is pricing in at this point. It is good to see analysts getting realistic about 2025 earnings growth. However, at 15% earnings growth, we believe it is still too optimistic given the expectation for slower economic growth in 2025.”

Corporate Highlights:

Verizon Communications Inc. reported revenue that missed analysts’ expectations, weighed down by lackluster sales of hardware such as mobile phones.

3M Co. increased the low end of its 2024 profit forecast and reported earnings that topped analyst estimates as a push to boost productivity gained traction.

General Motors Co. signaled solid US demand for its highest-margin vehicles even as the broader market softens, posting better-than-expected results for the latest quarter and raising the low end of its full-year profit forecast.

General Electric Co.’s sales fell short of Wall Street’s expectations last quarter, tempering enthusiasm for its improved profit outlook as the jet engine maker grapples with supply-chain limitations that are weighing on deliveries.

Kimberly-Clark Corp., owner of the Scott toilet paper brand, lowered its full-year organic sales forecast after reporting weaker-than-expected results.

Philip Morris International Inc. forecast higher-than-expected profit this year, citing soaring demand for its Zyn nicotine pouches in the US.

Lockheed Martin Corp.’s third-quarter revenue missed expectations, pulled down by weaker aeronautical sales and ongoing issues with its F-35 fighter jet program.

Zions Bancorp’s third-quarter adjusted net interest income came in ahead of estimates. Morgan Stanley said the results beat across the board and sees the positive trajectory in net interest income continuing into 2025.

L’Oreal SA posted disappointing sales last quarter as the beauty company suffers from worsening consumer demand in China.

An investigation of Huawei Technologies Co.’s latest AI offering has unearthed an advanced processor made by Nvidia Corp. manufacturing partner Taiwan Semiconductor Manufacturing Co., suggesting that China is still struggling to reliably make its own advanced chips in sufficient quantities.

Key events this week:

Canada rate decision, Wednesday

Eurozone consumer confidence, Wednesday

US existing home sales, Wednesday

Boeing, Tesla, Deutsche Bank earnings, Wednesday

Fed’s Beige Book, Wednesday

US new home sales, jobless claims, S&P Global Manufacturing and Services PMI, Thursday

UPS, Barclays earnings, Thursday

Fed’s Beth Hammack speaks, Thursday

US durable goods, University of Michigan consumer sentiment, Friday

Some of the main moves in markets:

Stocks

The S&P 500 was little changed as of 1:47 p.m. New York time

The Nasdaq 100 rose 0.1%

The Dow Jones Industrial Average rose 0.1%

The MSCI World Index fell 0.2%

The Russell 2000 Index fell 0.2%

Currencies

The Bloomberg Dollar Spot Index was little changed

The euro fell 0.1% to $1.0803

The British pound was little changed at $1.2983

The Japanese yen fell 0.1% to 151.02 per dollar

Cryptocurrencies

Bitcoin fell 0.6% to $67,338.79

Ether fell 1.9% to $2,625.07

Bonds

The yield on 10-year Treasuries was little changed at 4.20%

Germany’s 10-year yield advanced four basis points to 2.32%

Britain’s 10-year yield advanced three basis points to 4.17%

Commodities

West Texas Intermediate crude rose 2.3% to $72.21 a barrel

Spot gold rose 1% to $2,748.02 an ounce

This story was produced with the assistance of Bloomberg Automation.

Traders are staring down a series of risks after the stock market’s torrid start to the year, from economic fear, to interest rate uncertainty, to election angst. But perhaps the most important variable for whether equities can keep rolling returns to the spotlight this week: corporate earnings.

The S&P 500 Index has soared roughly 20% in 2024, adding more than $8 trillion to its market capitalization. The gains have largely been driven by expectations of easing monetary policy and resilient profit outlooks.

But the tide may be turning as analysts slice their expectations for third-quarter results. Companies in the S&P 500 are expected to report a 4.7% increase in quarterly earnings from a year ago, according to data compiled by Bloomberg Intelligence. That’s down from projections of 7.9% on July 12, and it would represent the weakest increase in four quarters, BI data show.

“The earnings season will be more important than normal this time,” said Adam Parker, founder of Trivariate Research. “We need concrete data from corporates.“

In particular, investors are eager to see if companies are postponing spending, if demand has slowed, and if customers are behaving differently due to geopolitical risk and macro uncertainty, Parker said. “It is exactly because there is a lot going on in the world that corporate earnings and guidance will particularly matter now,” he said.

Reports from major companies start arriving this week, with results from Delta Air Lines Inc. due Thursday and JPMorgan Chase & Co. and Wells Fargo & Co. scheduled for Friday.

“Earnings seasons are typically positive for equities,” said Binky Chadha, chief US equity and global Strategist at Deutsche Bank Securities Inc. “But the strong rally and above-average positioning going in (to this earnings season) argue for a muted market reaction.”

Obstacles Abound

The obstacles facing investors right now are no secret. The US presidential election is just a month away with Democrat Kamala Harris and Republican Donald Trump in a tight, fierce race. The Federal Reserve has just started lowering interest rates, and while there’s optimism about an economic soft-landing, questions remain about how fast central bankers will reduce borrowing costs. And a deepening conflict in the Middle East is raising concerns about inflation heating up again, with the price of West Texas Intermediate oil rising 9% last week, the biggest weekly gain March 2023.

“The bottom line is that revisions and guidance are weak, indicating lingering concerns about the economy and reflecting some election year seasonality,” said Dennis DeBusschere of 22V Research. “That is helping set up reporting season as another uncertainty clearing event.”

Plus, to make matters more challenging, big institutional investors have little buying power at the moment and seasonal market trends are soft.

Positioning in trend-following systematic funds is now skewed to the downside, and options market positioning shows traders may not be ready to buy any dips. Commodity trading advisers, or CTAs, are expected to sell US stocks even if the market stays flat in the next month, according to data from Goldman Sachs Group Inc. And volatility control funds, which buy stocks when volatility drops, no longer have room to add exposure.

History appears to side with the pessimists, too. Since 1945, when the S&P 500 gained 20% through the first nine months of the year, it posted a down October 70% of the time, data compiled by Bespoke Investment Research show. The index gained 21% this year through September.

Bar Lowered

Still, there’s reason for optimism, specifically a lowered bar for earnings projections that leaves companies more room to beat expectations.

“Estimates got a little bit too optimistic, and now they’re pulling back to more realistic levels,” said Ellen Hazen, chief market strategist at F.L.Putnam Investment Management. “It will definitely be easier to beat earnings because estimates are lower now.”

In fact, there’s plenty of data suggesting that US companies remain fundamentally resilient. A strengthening earnings cycle should continue to offset stubbornly weak economic signals, tipping the scales for equities in a positive direction, according to Bloomberg Intelligence. Even struggling small-cap stocks, which have lagged their large-cap peers this year, are expected to see improving margins, BI’s Michael Casper wrote.

Friday’s jobs report, which showed the unemployment rate unexpectedly declined, quelled some concerns about a soft labor market.

Another factor is the Fed’s easing cycle, which has historically been a boon for US equities. Since 1971, the S&P 500 has posted an annualized return of 15% during periods in which the central bank cut rates, data compiled by Bloomberg Intelligence show.

Those gains have been even stronger when rate-cutting cycles hit in non-recessionary periods. In those cases, large caps posted an averaged annualized return of 25% compared with 11% when there was a recession, while small caps gained 20% in non-recessionary periods compared with 17% when there was a recession.

“Unless earnings are a major disappointment, I think the Fed will be a bigger influence over markets between now and year-end simply because earnings have been pretty consistent,” said Tom Essaye, founder and president of Sevens Report Research. “Investors expect that to continue.”

Sure, investing in these ETFs means you’ll forfeit 15% of your dividends to withholding tax. Yet, for many, it’s a worthwhile trade-off to gain access the most significant U.S. equity index—a benchmark that, according to the Standard & Poor’s Indices Versus Active (SPIVA) report, has outperformed 88% of all U.S. large-cap funds over the past 15 years.

But hold on, these aren’t your only choices. And here’s something you might not know: they aren’t even the cheapest around. Just like opting for no-name brands at the store can offer the same quality for a lower price, other ETF managers have been quietly rolling out competing U.S. equity index ETFs that come with even lower fees. Here’s what you need to know to make an informed choice.

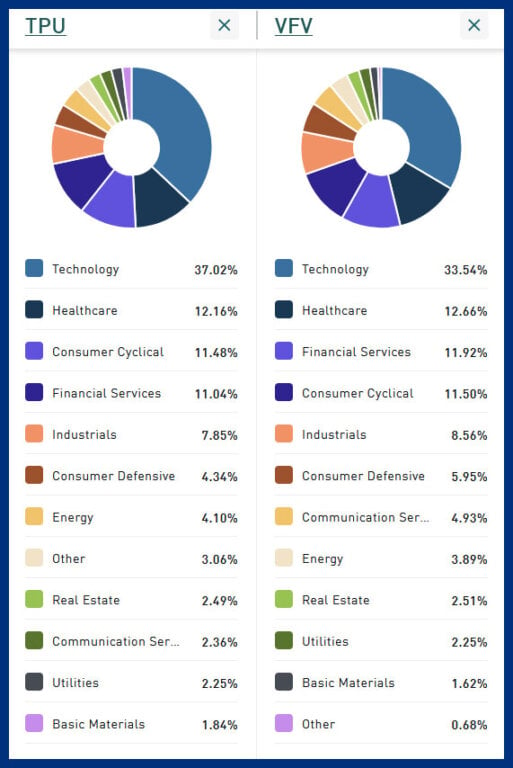

Exploring cheaper alternatives to the well-known S&P 500 ETFs—like VFV, ZSP and XUS—leads us to a pair of lesser known but highly competitive options: the TD U.S. Equity Index ETF (TPU) and the Desjardins American Equity Index ETF (DMEU). Launched in March 2016 and April 2024, respectively, these ETFs track the Solactive US Large Cap CAD Index (CA NTR) and the Solactive GBS United States 500 CAD Index. The “CA NTR” stands for “net total return,” which means the index accounts for after-withholding tax returns, providing a more accurate measure of what Canadian investors might take home.

Essentially, these indices offer U.S. equity exposure without the licensing costs associated with the brand-name S&P 500 index, which is a significant advantage for keeping expenses low. You can think of Solactive as the RC Cola of the indexing industry, and S&P Global as Coca-Cola, and MSCI as Pepsi.

For TPU, the management fee is set at 0.06%, with a total MER of 0.07%. DMEU charges a management fee of just 0.05%. Since it hasn’t been trading for a full year yet, its MER is still to be determined but is expected to be competitively low.

In terms of portfolio composition, there’s scant difference between the these ETFs: VFV, TPU and DMEU. Glance at the top 10 holdings, and you’ll see the weightings of these ETFs reveals very similar exposure, with only minor deviations. Similarly, when comparing sector allocations between TPU and VFV, they align closely, reflecting a consistent approach to capturing the broad U.S. equity market. However, look a bit deeper into the technical aspects, the indices that these ETFs track—the Solactive indices for TPU and DMEU versus the S&P 500 for VFV—exhibit some notable differences.

The S&P 500 is not as straightforward as it might seem, though. It doesn’t just track the 500 largest U.S. stocks. Instead, what is included is at the discretion of a committee, subject to eligibility criteria including market capitalization, liquidity, public float and positive earnings. This makes it more stringent and somewhat more active than you might have thought.

In contrast, the Solactive indices used by TPU and DMEU are more passive. They simply track the largest 500 U.S. stocks by market cap, with minimal additional screening criteria. This straightforward approach lends a more passive characteristic to these indices compared to the S&P 500.

The problem with the AI bubble isn’t that it is bursting and bringing the market down—it’s that the hype will likely go on for a while and do much more damage in the process than experts are anticipating.

Economic analysts, consultants, and business leaders are desperate for anything that will lift productivity growth in the industrialized world. It has been disappointing in the information age, despite all of the glimmer and talk of revolutionary technologies. Total Factor Productivity (TFP)—economists’ favorite measure of macroeconomic productivity which estimates how much aggregate output is growing due to improvements in efficiency and technology—used to grow about 2% a year throughout the 1950s, 60s, and early 70s. Since the 1980s, its growth has been hovering around 0.5%. The promise of an AI-driven productivity boom is music to everyone’s ears.

It isn’t just wishful thinking on the part of businesses. The hype machine of the tech world is powerful. We are told every day in newspapers and social media about the transformative effects of new tools, sparkling with superhuman intelligence.

And of course, the prospect of artificial general intelligence (AGI) appeals to us after decades of Hollywood movies where machines become so capable that they battle it out with humans.

Alas, it seems unlikely that anything of the scale promised by the tech world—such as rapid advances towards singularity where machines can do everything humans can—is even remotely possible. Even more grounded predictions such as those from Goldman Sachs that generative AI will boost global GDP by 7% over the next decade and from the McKinsey Global Institute that the annual GDP growth rate could increase by 3-4 percentage points between now and 2040, may be far too optimistic.

What should we expect from AI?

My own research shows that the effect of the suite of AI technologies is more likely to be in the range of about 0.5%-0.6% increase in U.S. TFP and about 1% increase in US GDP within 10 years. This is nothing to sneer at. Given the state of the economy in the United States and other industrialized countries, we should welcome such a contribution with open arms and do our best so that this potential is realized. Yet, it isn’t transformative.

Where this number comes from is useful to understand, not just to increase our confidence in it but also to know why we could even squander that potential if we give in to the hype.

On its current trajectory and with current capabilities, AI’s biggest impact will come from automating some tasks and making workers a little more productive in some occupations. For now, this can only happen in occupations that do not involve much interaction with the real world (construction, custodial services, and all sorts of blue-collar and craft work are out) and in occupations that do not have a central social element (psychiatry, much of entertainment and academia are out). Even in occupations that fall outside of these categories, getting much productivity growth from AI will be difficult. Physicians could benefit from AI in diagnosis and calibrating their treatment and prescription decisions. But this requires much more reliable AI models—not gimmicks such as large language models that can write Shakespearean sonnets.

Based on the available evidence and these considerations, I estimate that only about 4.6% of tasks in the U.S. economy can be meaningfully impacted by AI within the next decade.

Combine this with existing estimates of how much of a productivity gain businesses can get from the use of generative AI tools, which is on average about 14%, and you come up with a TFP boost of only 0.66% over ten years, or by 0.06% annually.

I readily admit that there is a huge degree of uncertainty. It may well be that generative AI models will make tremendous progress within the next few years and suddenly they can do much more than the 4.6% I currently estimate. Or they could revolutionize the process of science, leading to myriad new materials and products that we could not dream of today and completely change the production process for the better.

But I, for one, don’t think this is the likely outcome. A very tiny percentage of U.S. companies are currently using AI, and it will be a slow process until AI is productively used throughout the economy.

Hype is the enemy

Worse, the hype may be the biggest enemy of getting productivity increases from AI, and the misallocation of resources that it causes could make us lose the modest gains that we can get from AI.

This is for at least three reasons. First, with the hype, there will be a lot of overinvestment in AI. Most business executives, at least until last week’s market correction and soul-searching, were under pressure to jump on the AI bandwagon. If you are not investing in AI massively, you are lagging behind your peers, they were told by journalists, consultants, and tech experts. This leads to efficiency losses not to efficiency gains. In a rush to automate everything, even the processes that shouldn’t be automated, businesses will waste time and energy and will not get any of the productivity benefits that are promised. The hard truth is that getting productivity gains from any technology requires organizational adjustment, a range of complementary investments, and improvements in worker skills, via training and on-the-job learning. The miraculous, revolutionary returns from AI are very likely to remain a chimera.

Second, there will be a lot of wasted resources, investment, and energy, as tech companies and their backers go after bigger and bigger generative AI models. The current market correction will not stop tech leaders from asking for trillions of dollars to buy even more GPU capacity and strive to build bigger models. They may pass on some of these costs by selling their services and technologies to businesses that are not ready to undertake this transition, but as a society, we surely bear the consequences of this overinvestment.

Third and most fundamentally, boosting productivity requires workers to become more productive, gain greater expertise, and use better information in their decision-making and problem-solving. This applies not just to journalists, academics, and office workers—most of what electricians, plumbers, blue-collar workers, educators, and healthcare workers do is tackle a series of problems. The better the information they use, the better they will be at their jobs and the more able they will become to take on more sophisticated tasks. The real promise of AI is as an informational tool: to collect, process, and present reliable, context-dependent, and easy-to-use information to human decision-makers.

But this is not the direction in which the tech industry, mesmerized by human-like chatbots and dreams of AGI and misled by self-appointed AI prophets, is heading.

More must-read commentary published by Fortune:

The opinions expressed in Fortune.com commentary pieces are solely the views of their authors and do not necessarily reflect the opinions and beliefs of Fortune.

Recommended Newsletter: CEO Daily provides key context for the news leaders need to know from across the world of business. Every weekday morning, more than 125,000 readers trust CEO Daily for insights about–and from inside–the C-suite. Subscribe Now.

(Bloomberg) — The world’s largest technology companies got hammered as concern about tighter US restrictions on chip sales to China spurred a selloff in the industry that has led the bull market in stocks.

Most Read from Bloomberg

From the US to Europe and Asia, chipmakers came under heavy pressure. American powerhouses Nvidia Corp., Advanced Micro Devices Inc. and Broadcom Inc. drove a closely watched semiconductor gauge down almost 7% — the most since 2020. Across the Atlantic, ASML Holding NV tumbled over 10% even after the Dutch giant reported strong orders. A plunge in Tokyo Electron Ltd. led the Nikkei 225 Stock Average lower.

Wednesday’s action reprised a recent trend in which capitalization-weighted indexes underperformed the average stock, a consequence of weakness in the megacaps that dominate them. With firms such as Apple Inc. and Microsoft Corp. each making up 7% of the S&P 500, losses are hard to offset even when most of the index’s constituents are up — as they were today.

The Biden administration told allies it’s considering severe curbs if companies like Tokyo Electron and ASML keep giving China access to advanced semiconductor technology. The US is also weighing more sanctions on specific Chinese chip firms linked to Huawei Technologies Co.

“This news on the chip front is the kind of UFO (UnForeseen Occurrence) that could indeed create the kind of selling that could be the catalyst for a tradable correction in the stock market,” said Matt Maley at Miller Tabak + Co. “Broad indices have become very overbought.”

The S&P 500 fell 1.4%. The Nasdaq 100 had its worst day since 2022. A gauge of the “Magnificent Seven” giant companies slipped 3.4%. The Russell 2000 of small firms dropped 1.1%. Wall Street’s “fear gauge” — the VIX — hit the highest since early May. In late hours, United Airlines Holdings Inc. sank on a bearish outlook.

A pair of chipmakers defied the selloff: Intel Corp. and Globalfoundries Inc. And the Dow Jones Industrial Average climbed for a sixth straight day — notching another record. Financial shares outperformed, with U.S. Bancorp surging on solid results.

The bond market saw small moves. The Federal Reserve’s Beige Book showed slight economic growth and cooling inflation. The most-notable speaker on Wednesday was Governor Christopher Waller, who said the Fed is getting “closer” to cutting rates, but is not there yet. The yen led gains in major currencies, up almost 1.5%.

The Biden administration is in a tenuous position. US companies feel that restrictions on exports to China have unfairly punished them and are pushing for changes. Allies, meanwhile, see little reason to alter their policies when the presidential election is just a few months away.

“Normally, the impact of these types of headlines isn’t long-lasting, but in this case, we would note that semis have been underperforming the broader market for the last couple of weeks now,” said Bespoke Investment Group strategists. “So that’s something to watch.”

The tech underperformance is coming after a first half which saw megacaps like Nvidia, Microsoft Corp. and Alphabet Inc. propel the market higher, stretching valuations for these names and leaving them with a tougher setup for the rest of 2024.

Can the market keep powering ahead without tech?

“Much of this year’s equity gains have come from a handful of names currently under direct threat from the political arena,” said Jose Torres at Interactive Brokers. “An important question is if the rest of the market, which generally lacks thrilling tales on a relative basis, can offset the waning momentum in ‘Magnificent Seven’ stocks.”

At Goldman Sachs Group Inc., Scott Rubner says “I am not buying the dip.”

The tactical strategist bets the S&P 500 has nowhere to go from here but down. That’s because this Wednesday, July 17, has historically marked a turning point for returns on the equity benchmark, he said, citing data going back to 1928. And what follows, he says, is August — typically the worst month for outflows from passive equity and mutual funds.

Jonathan Krinsky at BTIG says the market is “nearing the end of the typical bullish window.”

Sentiment remains extremely complacent on the surveys and transactional indicators, he noted.

“While the rotation out of megacap tech into cyclicals and small-caps is encouraging, it felt a bit forced happening in such a short period of time,” Krinsky said. “Even if this is going to be a more long-lasting rotation, we likely won’t be able to see that new leadership until after we see a higher correlation correction and then see what leads coming out of that.”

Corporate Highlights:

Tesla Inc. forming an autonomous taxi platform will be the catalyst for a roughly 10-fold increase in its share price, Ark Investment Management LLC’s Cathie Wood said, echoing years of bullish predictions about a business the carmaker has yet to stand up.

Amazon.com Inc.’s marketing portal for merchants crashed Tuesday night, according to multiple Amazon sellers and consultants, fouling up one of the online retailer’s biggest sales of the year.