SoundHound AI (NASDAQ:SOUN) has staged a remarkable recovery since hitting its April lows, surging 282% to reward patient investors. This ascent — including last year’s 1,024% rise — reflects growing traction for its voice recognition technology, which powers conversational artificial intelligence (AI) across industries. The company has inked a flurry of deals, embedding its solutions in everything from restaurant ordering systems to automotive infotainment.

A prime example came yesterday with a strategic partnership with Telarus, a major tech services distributor. This agreement will roll out SoundHound’s Amelia 7 AI Agent and Autonomics platforms to enterprise customers via Telarus’s global network, targeting sectors like healthcare and finance. Such integrations highlight SoundHound’s push to scale beyond niche applications into broader enterprise adoption, adding to the momentum.

SOUN shares climbed 2%yesterday on its latest deal and is up another 3% at the market open, signaling renewed buyer interest amid the broader AI rally. Investors are eyeing its upcoming third-quarter earnings report on Nov. 6 after the market close, where updates on backlog conversion and revenue acceleration could drive further volatility.

With the stock’s rapid rise underscoring its potential in a booming voice AI market — and following five consecutive days of decline — the question is: should investors jump in before the results?

SoundHound’s core strength lies in its speech-to-meaning technology, which processes voice inputs into actionable intent in milliseconds — far faster than many rivals. This low-latency edge makes it ideal for real-time applications, like drive-thru ordering at quick-service restaurants or hands-free controls in vehicles. The company has secured partnerships with heavyweights in autos, including Stellantis (NYSE:STLA) and Hyundai, and in food service with chains like White Castle. These deals fueled a staggering 217% year-over-year revenue jump to $42.7 million in the second quarter.

A $1.2 billion backlog underscores this momentum, spanning healthcare diagnostics and financial services chatbots. Roughly half of recent growth stems from organic wins, with the rest from smart acquisitions like SYNQ3 for restaurant tech and Amelia for enterprise AI agents.

Management eyes adjusted EBITDA breakeven by late 2025, betting on the voice recognition market’s expansion to $50 billion by 2030.

In a world shifting to voice-first interfaces, SoundHound’s tech positions it as a nimble player in generative AI’s next wave.

Despite the hype, SoundHound grapples with persistent headwinds that temper its appeal. Founded in 2005, the company has never posted an annual profit, racking up widening losses. Q2’s GAAP net loss ballooned to $74.7 million, up sharply from $22.3 million in the first quarter, including a $31 million non-cash charge from the Amelia deal. Core operations continue to bleed, with operating expenses hitting $120 million — outstripping revenue gains and squeezing margins.

Free cash flow tells a stark tale: a $43.7 million burn in the first half of 2025, despite a $230 million cash pile offering just 12 to 18 months of runway. Acquisitions have juiced growth but inflated costs without flipping cash flow positive.

Short interest also tops 32% of the float, fueling volatility. SOUN stock is down 6% year-to-date, even as AI peers soar and its own big run higher. A valuation at 58 times trailing sales — double the software sector’s 8x to 10x norm — requires flawless execution, which is far from guaranteed.

Competition looms large too. Giants like Amazon‘s (NASDAQ:AMZN) Alexa, Alphabet‘s (NASDAQ:GOOG)(NASDAQ:GOOGL) Google Assistant, and Apple‘s (NASDAQ:AAPL) Siri dwarf SoundHound’s $25.8 million quarterly R&D spend with deeper pockets and ecosystems.

Non-GAAP gross margins dipped to 50.8% last quarter, hinting at pricing pressures in a crowded field.

SoundHound AI boasts innovative technology and a solid pipeline in a high-growth market, but its chronic unprofitability, voracious cash burn, and lofty valuation make it a risky bet for long-term holders. While a positive earnings surprise on Nov. 6 isn’t off the table — perhaps from faster backlog conversion — don’t count on profits materializing soon.

I’m bearish overall; this isn’t a core portfolio pick. That said, a small speculative position could pay off if results beat low expectations, offering a quick trade before any post-earnings pullback.

Both SoundHound(NASDAQ: SOUN) and Nvidia(NASDAQ: NVDA) are direct beneficiaries of AI. One produces the chips necessary to make our AI future possible. The other developed its own proprietary AI platform that could power everything from cars to drive-through windows.

If you want to bet on AI, it would make sense to buy stock in both companies. But some serious differences should guide your investment strategy.

Want maximum growth potential?

If you want maximum growth potential, the clear choice is SoundHound. The math isn’t complicated. SoundHound’s market cap is currently around $1.3 billion. Nvidia’s valuation, meanwhile, is closer to $3 trillion. Simply due to size, SoundHound stock has a much better chance of rising another 1,000% than Nvidia. For its stock to rise 10 times in value, Nvidia would need to add more value than Microsoft, Meta Platforms, Apple, and Amazon combined — and then some. SoundHound, meanwhile, would only need to add 0.3% of Nvidia’s current value.

Put simply, SoundHound’s diminutive size gives it more potential upside than Nvidia. But will SoundHound actually be able to realize that potential upside? One factor works heavily in its favor. And that is SoundHound’s platform relevance to a large number of industries.

At its core, the company’s technology enables sound and voice recognition, plus natural language understanding that allows responses via AI. Imagine ordering food through an AI-powered drive-through, chatting with your car about maintenance issues, or simply selecting a song. You might also want to discuss with your television which shows you should watch next. SoundHound actually has contracts with companies working on these very issues, with a total backlog valued at nearly $700 million — that’s up from around $330 million just a year ago.

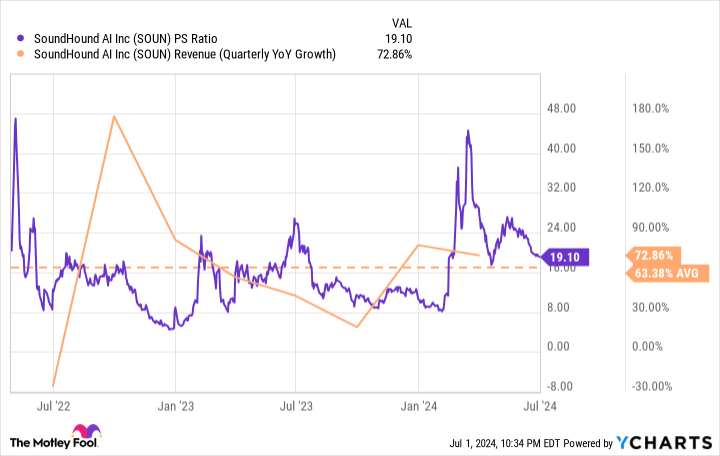

For all its potential, SoundHound stock isn’t priced for perfection. Shares trade at a lofty 19 times sales, but revenue growth rates have averaged roughly 60% per year. There’s a good chance double-digit growth rates will be sustained for another decade or more, a future that would make today’s premium valuation look reasonable in hindsight. Emerging tech companies like this typically show a lot of short-term volatility, but patient investors looking for maximum growth potential should like what they see.

SOUN PS Ratio Chart

Go all-in on artificial intelligence

Nvidia has very little to prove at this point. Over a very short time span, the company has become the largest AI stock in the world, with a huge percentage of its business dependent on growth in the AI industry.

“Back in fiscal 2022 (which ended in January 2022), Nvidia generated 46% of its revenue from its gaming GPUs, 39% from its data center GPUs, and the rest from its professional visualization, auto, and OEM chips,” explains fellow Fool contributor Leo Sun. Oh, how quickly that breakdown changed. For the first fiscal quarter of 2025, Nvidia generated 87% of its revenue from data center chips and just 13% from everything else, gaming included.

“It generated $22.6 billion in data center revenue in that single quarter compared to its total revenue of nearly $27 billion for all of fiscal 2023,” observes Sun. “That breakneck expansion transformed Nvidia from a more diversified GPU maker to an all-in play on AI chips.”

This all-in approach certainly has its risks. Over the past five years, Nvidia’s valuation has gone from around 10 times sales to nearly 40 times sales. The company’s growth rates — revenue grew by 262% year over year last quarter (Q1 of FY 2025) — have more than justified the rise in its multiple. Yet there’s no denying that Nvidia’s stock price is now dependent on two things. First, a continued massive increase in AI spending. Second, its ability to maintain its dominant market lead.

Over the decades, chip wars have produced many repeat winners and losers. Just check out the long-term price charts of AMD, Intel, and Nvidia. The winners and losers of today don’t necessarily stay that way forever, even if it takes years for the transition to occur. AMD’s MI300 Instinct GPUs are already beating Nvidia’s H100 GPUs on several benchmarks, as are Intel’s Gaudi 3 AI accelerators. Nvidia’s next-generation Blackwell chip is heading into the market as we speak, perhaps stemming the tide of rising rivals.

Make no mistake: Nvidia is still a great investment for those bullish on AI. But if you’re looking for the best bang for your buck, don’t ignore lesser-known stocks like SoundHound.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $786,046!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Ryan Vanzo has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Amazon, Apple, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel, long January 2026 $395 calls on Microsoft, short August 2024 $35 calls on Intel, and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Investors are in a feeding frenzy over artificial-intelligence software plays, and you have to think this isn’t going to end well.

You can date the start of the AI stock craze to the Nov. 30 launch of ChatGPT, the generative AI chatbot created by the start up OpenAI. Recent data show that ChatGPT reached more than 100 million users in January, reaching that market faster than other buzzy apps like TikTok.