zimmytws | iStock | Getty Images

Last November’s midterm elections were expected to bring a so-called “red wave” of wins for Republican candidates. But ultimately, voters gave Democrats an edge in some of the most competitive congressional districts.

One deciding factor was candidates’ messages around Social Security and Medicare, which helped sway voters, particularly those ages 50 and up, according to an analysis from AARP following the Nov. 8 election.

Now, as the 2024 presidential election approaches, and GOP hopefuls line up for their party’s nomination, they face new pressure to decide where they stand, particularly with Social Security.

Former President Donald Trump and Florida Gov. Ron DeSantis — who thus far are in the lead in the Republican polls — have so far pledged not to touch the program.

“Under no circumstances should Republicans vote to cut a single penny from Medicare or Social Security to help pay for Joe Biden’s reckless spending spree,” Trump said in January.

In March, DeSantis told Fox News, “We’re not going to mess with Social Security as Republicans.”

Their position matches that of President Joe Biden, who during the State of the Union prompted both sides of the aisle to agree the program is “off the books.”

More from Personal Finance:

This tool lets you play at fixing Social Security woes

Retirement-savings gap may cost economy $1.3 trillion by 2040

How a retirement age change could affect younger Americans

While that stance is popular with the public, some experts say it is ill-advised.

“It’s fundamentally irresponsible to say we’re not going to touch it when everybody who’s ever looked at the finances of the program recognizes that it’s going bankrupt,” said Whit Ayres, president of North Star Opinion Research, a center-right political polling operation.

The situation presents an opportunity for a hero to emerge, one who can put the program on sound financial footing, Ayres said.

One longshot Republican hopeful — former Cranston, Rhode Island, mayor Steve Laffey — plans to enter the race with his own bold plan to reconstruct Social Security as the first priority on his agenda.

“Our biggest problem is this: We as Americans simply don’t directly confront our problems,” Laffey said.

Social Security is the “ultimate example of that,” he said.

A crucial inflection point, particularly for Social Security, is coming, according to the program’s trustees.

Social Security’s combined funds will only be able to pay full benefits until 2034. At that point, just 80% of benefits will be payable if nothing is done sooner.

Lawmakers on both sides of the aisle would need to agree on fixes for the program. These could include benefit cuts, such as raising the retirement age, tax increases or a combination of both.

But with Democrats vowing to protect benefits and Republicans swearing off tax increases, that has thus far left little room for compromise.

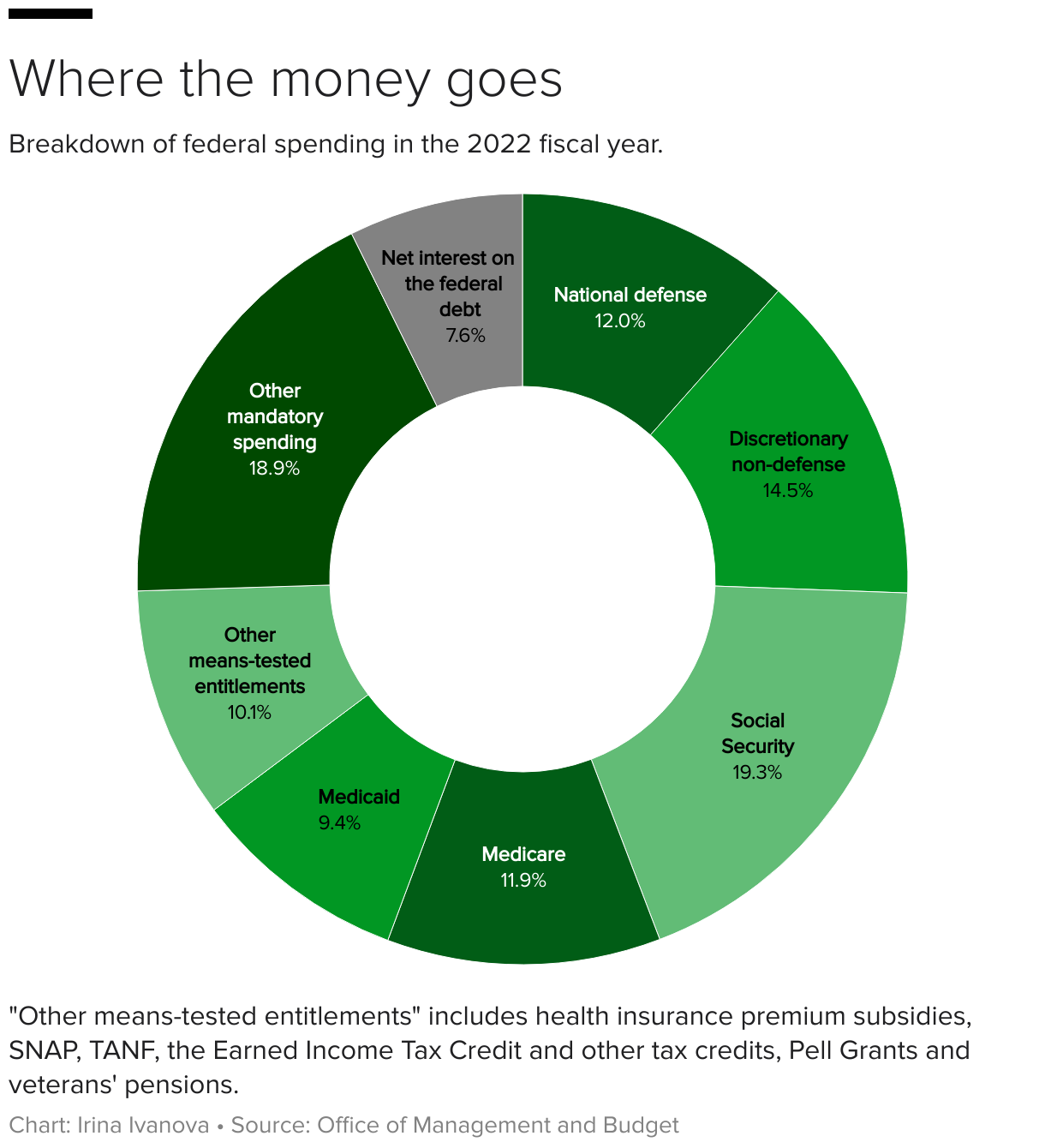

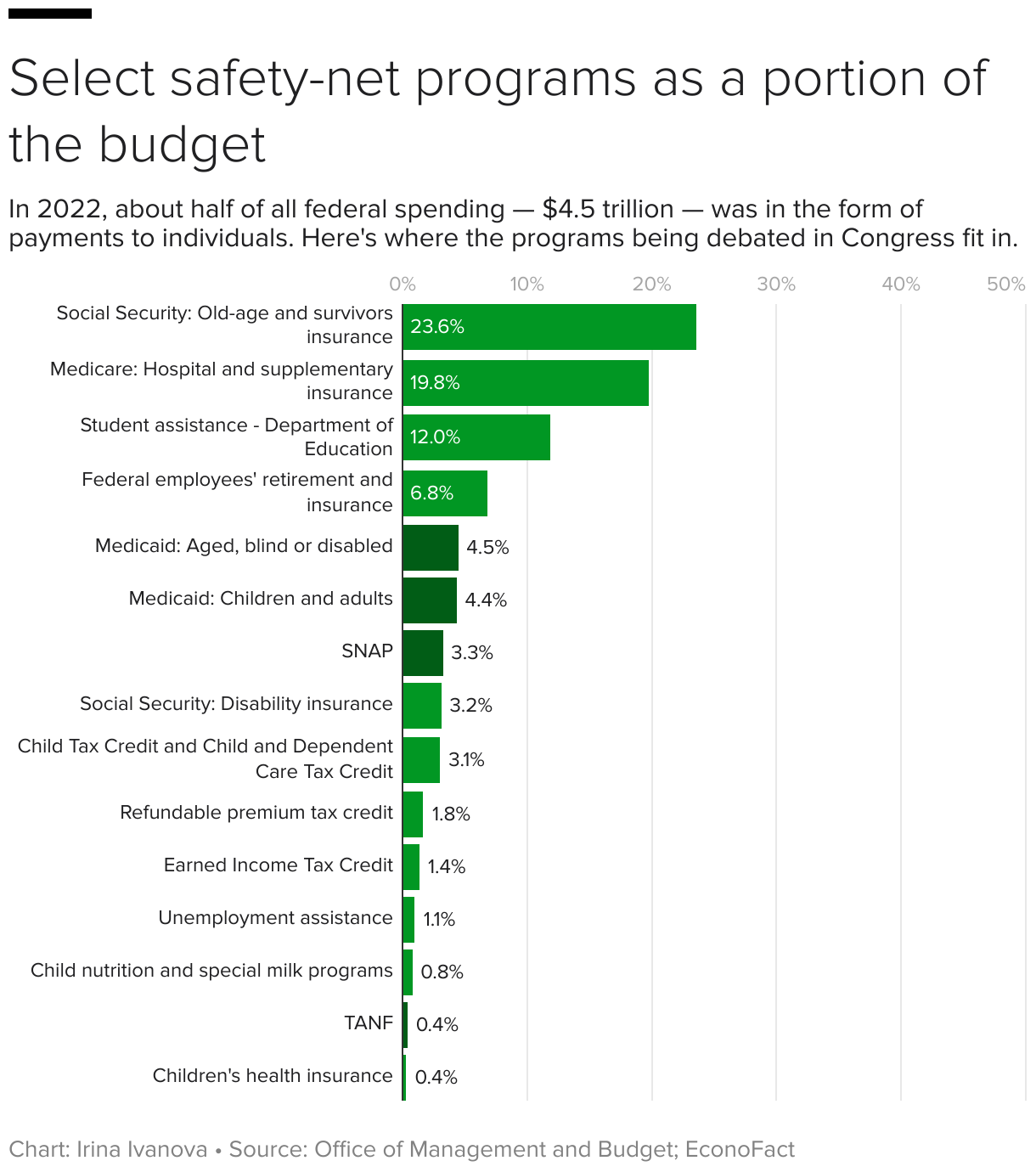

As Washington leaders recently worked out a deal to raise the nation’s debt ceiling for two years, the cost of Social Security and Medicare came under scrutiny.

Both Social Security and Medicare fall under the category of mandatory spending, which altogether represents more than two-thirds of the nation’s budget, according to the Tax Foundation.

Consequently, it is impossible to address the nation’s spending without addressing those programs, according to Tax Foundation economist Alex Durante.

“The longer we push this out, it becomes more difficult to try to protect everyone that receives the benefits,” Durante said. “It’s important that we tackle this sooner rather than later.”

The Social Security plan Laffey would implement throws out the traditional approaches of tax increases or benefit cuts.

Instead, he wants to gradually phase out the FICA tax completely. Currently, workers and employers each pay 6.2% on up to $160,200 in wages toward Social Security.

That would be replaced by new Personal Security System accounts, to which workers would contribute 10% of their pay. Those balances would be invested in a weighted index of global stocks, bonds and other securities.

The plan comes from Laurence Kotlikoff, a Boston University economics professor who has devoted much of his career to helping people get the most from Social Security and demystifying the program’s many rules.

Kotlikoff himself ran for president in 2012 and 2016 as a third-party candidate. In subsequent election cycles, he has urged Laffey to run.

The two met when Laffey was working on “Fixing America,” a 2012 documentary about Americans’ perspectives on fixing the country’s problems post-financial crisis. Laffey wrote and co-produced the documentary, for which he interviewed Kotlikoff.

Laffey, a former Morgan Keegan executive, has mostly been out of politics after serving two terms as mayor of Cranston, Rhode Island.

He ran for a U.S. Senate seat in Rhode Island in 2006 and then in 2014 pursued the Republican nomination for a U.S. House seat representing Colorado, where he now lives. He was unsuccessful in both races.

Republican 2024 presidential hopeful Steve Laffey arrives for an interview at a local TV station in Cranston, Rhode Island, on March 17, 2023.

Ed Jones | Afp | Getty Images

Laffey launched a campaign for mayor at a time when Cranston had the lowest bond rating in America, he said. The big accomplishment he boasts as Cranston mayor is bringing the city’s bond rating up. The city’s S&P rating climbed to an A- in 2006 from a B in 2002, according to a spokesman for Laffey.

The Social Security plan would be a fully funded system, where you get your money back in the form of an inflation-indexed annuity, according to Kotlikoff.

“It’s a modern version of Social Security,” Kotlikoff said.

The goal would be to give beneficiaries a bigger return on the money than they get now.

It also aims to address the program’s current inequities. The government would make matching contributions on behalf of lower earners, the disabled and unemployed. Spouses would share their contributions to the program equally.

The investment strategies would be computerized and custodied by the federal government, not by Wall Street. Everyone would get the same rate of return, Kotlikoff noted.

The expectation is that over a 40-year time horizon the accounts would be able to make up for down years and ultimately provide workers with more money than today’s Social Security program.

The hope is a worker who is 20 years old in 2025 may eventually stand to get $10,000 per month, rather than $2,000, which would be a “lot better,” Laffey said.

The plan coincides with Laffey’s plans to overhaul government spending, such as changing the Federal Reserve’s inflation target to zero, rather than the current goal of 2%, in order to force Congress to work within its budget.

Because any changes to Social Security involve strict emotions, the big question is whether lawmakers and Americans would be ready to embrace a new direction for the program.

The idea of rethinking the way Social Security funds are invested has come up before.

While in office, President George W. Bush had proposed letting Americans save part of their Social Security taxes in personal retirement accounts, referred to as “partial privatization.”

Andrew Biggs, who worked in the White House on Social Security reform at the time and who is now a senior fellow at the American Enterprise Institute, remembers the proposal did not come close to succeeding, even as Social Security still had surpluses and Republicans controlled both houses of Congress.

Consequently, privatization — where personal accounts are funded out of part of the existing payroll tax — would be a long shot, he said.

“If Bush couldn’t do it then, despite a great effort, that’s not happening now,” Biggs said.

But personal accounts funded on top of the existing Social Security program, such as ensuring everyone signs up for a retirement plan at work, could be “more possible,” he said.

Another challenge may be getting Americans to embrace the idea.

The only people who like personalized accounts are affluent, college-educated white men, said Celinda Lake, a Democratic pollster and president at Lake Research Partners, who has conducted focus groups with married couples on the subject.

Women of all ages, who are very worried about the future of the program for their own economic security, are less likely to embrace the idea, she said.

Biden and Trump campaign signs are displayed as voters line up to cast their ballots during early voting at the Alafaya Branch Library in Orlando, Florida, Oct. 30, 2020.

Getty Images

For candidates, taking such a position can also jeopardize their primary and general election viability, Lake said.

Yet Ayres, of North Star Opinion Research, sees an opportunity for reforms much like President Ronald Reagan helped usher in, which put Social Security on sound financial footing for half a century, he said.

That likely won’t come from an “unworkable” overhaul of the program, Ayres said, but instead more marginal changes, such as raising the retirement age by several months and increasing the cap on Social Security earnings.

Like Reagan’s efforts, it would also require bipartisan commissions, he said.

As with the newly inked debt ceiling deal, “both sides are going to have to give a little bit,” Ayres said.

“Just putting your head in the sand and waiting for it to go bankrupt is a fundamentally irresponsible position,” he said.