U.S. stocks rose on Wednesday, with the S&P 500 capping off its biggest three-day percentage-point gain since March after Federal Reserve Chairman Jerome Powell again suggested that rising Treasury yields were likely aiding the central bank’s fight against inflation. This could potentially ease the pressure on the Fed to push interest rates even higher, which helped boost stocks. The S&P 500 SPX finished higher for the third straight day, rising 44.04 points, or 1.1%, on Wednesday to 4,237.84, according to preliminary closing data from FactSet. The index has gained nearly 3% over the last three trading days, its biggest…

Securities and Exchange Commission Chair Gary Gensler has plenty to worry about as he seeks to bring order and fairness to America’s $100 trillion capital markets, and there are few issues that cause him more concern than the spread of artificial-intelligence technology.

In an exclusive interview with MarketWatch, the regulator argued that generative AI technologies in the vein of ChatGPT have the potential to revolutionize the way we invest by leveraging large data sets to “predict things that were unimaginable even 10 years ago,” but that these new powers will come with great risks.

“A growing issue is that [AI] could lead to a risk in the whole system,” Gensler said. “As many financial actors rely on one or just two or three models in the middle … you create a monoculture, you create herding.”

Gary Gensler: AI could pose ‘a risk in the whole system.’

This herding effect can be dangerous if there is a flaw in the model that might reverberate through markets during a time of stress, causing abrupt and unpredictable price changes in markets. Gensler pointed to the examples of cloud computing and search engines as markets for tech products that have quickly become dominated by one or two major players, and he said he worries about similar concentration in the market for AI technology.

The regulator said this issue is especially difficult because of the fragmented nature of the U.S. regulatory apparatus, which relies on the SEC to oversee securities markets while other agencies have responsibility for banks or commodity markets.

“This is more of a cross-entity issue,” Gensler said. “That’s the challenge for these new technologies.”

As SEC chair, Gensler has escalated his regulatory agency’s crackdown on the cryptocurrency industry in 2023 by launching lawsuits against Binance and Coinbase, the two largest digital asset exchanges in the world by trading volume. The SEC alleges the two companies are operating unregistered securities exchanges in the U.S., but the companies say they are not running afoul of securities laws.

But AI is another issue that Gensler is starting to ring alarm bells over. There’s a little bit of irony because the promise of AI has largely been responsible for the S&P 500’s SPX

gains in 2023. The SEC chair said that his agency is already contemplating new rules to regulate artificial intelligence. For example, the SEC proposed a rule this summer to address conflicts of interest associated with stock brokers and investment advisors that leverage algorithms to predict and guide investor decisions through their smartphone applications or web interfaces.

The industry is pushing back on the proposal, arguing that existing rules are sufficient to prevent harm to investors and that a new rule would prevent brokers from using technology to create a better experience for clients.

Gensler said that the SEC benefits from such feedback, but still believes that regulators must be vigilant about the impact of these so-called predictive analytical tools. “If they do that to suggest a certain movie on a streaming app, okay,” he said. “But if they’re doing that about your financial help … we should address those conflicts.”

Federal prosecutors on Monday sought to chip away at FTX founder Sam Bankman-Fried’s credibility, pointing to discrepancies between his public comments and actions taken behind the scenes as the company collapsed.

In a steady drumbeat of questions, Assistant U.S. Attorney Danielle Sassoon tried to paint Bankman-Fried, the 31-year-old former wunderkind of the crypto world, as someone who lied to his customers about the safety of their investments, while secretly raiding their accounts to fund his own risky investments, luxury real estate purchases, costly celebrity endorsements and political contributions.

In his second day of testimony before a jury in his criminal fraud trial in Manhattan’s federal court, Bankman-Fried repeatedly said he couldn’t remember exactly what he had said in numerous media interviews in the days and weeks after FTX had declared bankruptcy and $8 billion in customer deposits had vanished.

He also sought to distance himself from decision-making at FTX’s sister investment firm, Alameda Research, whose risky bets helped bring the crypto trading platform down.

Sassoon pointed to multiple public comments by Bankman-Fried in which he claimed FTX’s risk management protocols made it safer than other crypto currency trading platforms, while the company allowed its own investment arm, Alameda Research to make risky bets without limit.

FTX ultimately collapsed largely as a result of the billions in loans it had extended to Alameda, which prosecutors allege was done using customer money.

Federal prosecutors have alleged that Alameda was effectively granted carte blanche to use FTX customer money to make risky bets. One key element was that certain risk-management systems that FTX used to to liquidate customer accounts that had entered into negative territory were disabled for Alameda, allowing it unfettered ability to make high-risk moves.

Throughout his testimony, Bankman-Fried claimed he had limited visibility as to what was happening at Alameda, which he founded and mostly owned, but which had ceased running day-to-day in 2021, when his ex-girlfriend Caroline Ellison took over as CEO.

He said he only became aware of how bad a liquidity issue Alameda faced well after a financial crisis began sweeping through the crypto industry in the summer of 2022. Bankman-Fried said he had told Ellison, who had pleaded guilty and testified against him, that she should have taken hedge positions earlier to lessen the company’s risk.

But he said he continued to believe up until just days before the companies collapsed, that both Alameda and FTX were on firmer financial footing.

“I viewed Alameda as solvent and FTX as solvent and decently liquid,” he testified. “Had that analysis come up any other way, I would have been in full on crisis mode. But in my view at the time that wasn’t the case.”

Bankman-Fried did admit that he consulted frequently with Ellison about moves that Alameda made and even signed off on several billion-dollar investments.

“I think a few billion of them were my decision,” he said when asked about several large investments made by Alameda in 2021 and 2022.

Bankman-Fried is expected back in court for further cross examination on Tuesday. The judge in the case said he expected the case may go to the jury as early as Friday.

Many people like to feel at least a little bit of fright.

That has been the whole point of Halloween for ages. The spooky traditions might even be a sort of hedge, a way to limit carnage should darker days lurk around the corner.

Where it gets trickier is when fear impacts a nest egg, retirement fund or portfolio holdings. And fear of looming mayhem has been higher in October, with a sharp selloff causing the S&P 500 index SPX

to break below the 4,200 level, landing it in a correction on Friday. It also joined the Nasdaq Composite Index in falling at least 10% from a summer peak.

In addition, a brutal bond-market rout has pushed the 10-year and 30-year Treasury yields BX:TMUBMUSD10Y

up dramatically, with both recently dancing around the 5% level, which can drive up borrowing costs for the U.S. economy and cause havoc in financial markets.

“Round numbers matter,” said Rich Steinberg, chief market strategist at The Colony Group, which has $20 billion in assets under management. He said the backdrop has investors trying to figure out “where to put money” and wanting to know “where can we hide?”

“When you get into a fear cycle, the dynamics can get out of whack with reality,” Steinberg said. He thinks investors won’t go wrong earning roughly 5.5% on shorter term risk-free Treasurys, while penciling in stock prices they like.

“That’s where investors really get rewarded over the long-term,” he said, granted they have enough liquidity to ride out what could be elongated patches of volatility.

Increasingly, investor worries tie back to U.S. government spending, with the Treasury Department early next expected to release an estimated $1.5 trillion borrowing need to accommodate a large budget deficit. That would unleash even more Treasury supply into an unsettled market, and potentially strain the plumbing of financial markets.

Higher U.S. bond yields threaten to make it more expensive for the federal government to service its debt load, but they also can be prohibitive for companies, sparking layoffs and defaults.

Fed decisions, yields

The Federal Reserve is expected to hold its policy interest rates steady on Wednesday following its two-day meeting, keeping the rate at a 22-year high in the 5.25%-5.5% range.

The real fireworks, however, often appear during Fed Chairman Jerome Powell’s afternoon press conference following each rate decision.

“I firmly believe they are done for good,” said Bryce Doty, a senior portfolio manager at Sit Investment Associates, of Fed hikes in this cycle, which he notes should set up bond funds for a banner 2024, after two rough years, given today’s higher starting yields.

Yet, Doty also sees two “wild cards” that could rattle markets. Heavy Treasury debt issuance could overwhelm liquidity in the marketplace, causing yields to go up higher and potentially force the Fed to restart its bond-buying program, he said.

War abroad also could expand, including with the Israel-Hamas conflict, which could spark a flight to quality and push down U.S. bond yields.

With that backdrop, Doty suggests adding duration in bonds BX:TMUBMUSD03M

as longer-term yields rise above short-term yields, and the so-called Treasury yield curve gets steeper. “This is the time,” he said. Investors should “keep marching” out on the curve as it steepens.

“Yields, in my mind, have been the main challenge for the equity market,” said Keith Lerner, chief markets strategist at Truist Advisory Services, while noting that stocks have been wobbly since the 10-year Treasury yield topped 4% in July.

“We’ve had a pretty good reset,” he said, adding that lower stock prices provide investors with “somewhat better compensation” for the uncertainties ahead.

“This is one of the most challenging investment environments we’ve seen in a long time,” said Cameron Brandt, director of research at EPFR, which tracks fund flows across asset classes.

With that backdrop, he expects investors to keep more dry powder on hand through the end of this year than in the past.

The Dow Jones Industrial Average DJIA

shed 2.1% for the week and closed at its lowest level since the March banking crisis. The S&P 500 lost 2.5% for the week and the Nasdaq Composite fell 2.6% for the week.

Another big item on the calendar for next week, beyond the Treasury borrowing announcement and Fed decision Wednesday is the Labor Department’s October jobs report due Friday.

Oil futures dropped Sunday night as markets saw a calm opening following Israel’s launch of a ground offensive in Gaza that drew implied threats from Iran amid market fears of a wider conflict that could disrupt global crude supplies.

Oil declined as Israel “seems to be approaching the situation with caution, which has brought a sense of relief that the worst-case scenarios may not materialize,” said Stephen Innes, managing partner at SPI Asset Management, in a note.

Innes, however, said investors should remember “this is likely to be a long, drawn-out affair with many false dawns.”

West Texas Intermediate crude for December delivery CL00, -1.51%

CLZ23, -1.51%

fell 93 cents, or 1%, to $84.61 a barrel on the New York Mercantile Exchange on Sunday night. December Brent crude BRNZ23, -1.34%,

the global benchmark, was off $1, or 1.1%, at $89.48 a barrel on ICE Futures Europe, dipping back below the $90-a-barrel threshold.

Oil futures jumped nearly 3% on Friday, but suffered weekly declines, eroding the modest risk premium priced into the market.

Israeli solders had moved at least two miles deep into the Gaza Strip as of Sunday, the Wall Street Journal reported, after beginning a delayed ground incursion into the enclave aimed at routing Hamas following its Oct, 7 attack on southern Israel that left more than 1,400 dead and saw more than 200 Israelis taken hostage.

A sustained bombardment of the densely populated Gaza Strip by Israel has resulted in more than 8,000 casualties, according to Palestinian authorities. Israel has been under pressure by the U.S. and others to minimize civilian casualties.

U.S. stock-index futures ticked higher, with S&P 500 futures ES00, +0.32%

up 0.3%, while futures on the Dow Jones Industrial Average YM00, +0.20%

added 68 points, or 0.2%.

The biggest worry among investors is a conflict that sees Iran become more directly involved. Iranian crude exports have rebounded from lows seen after the Trump administration withdrew the U.S. from a nuclear accord with Tehran and reimposed sanctions in 2018.

A renewed crackdown on Iran could take up to 1 million barrels a day of crude off the market, while a spiraling conflict could see Tehran threaten transportation chokepoints, particularly the Strait of Hormuz, or otherwise attack infrastructure in the region, while driving up a fear premium.

Iranian President Ibrahim Raisi, in a post on X written in English, said Saturday that Israel had “crossed the red lines, which may force everyone to take action.”

U.S. warplanes on Friday struck two locations in eastern Syria, which the Pentagon said were linked to Iran’s Revolutionary Guard Corps, following a string of attacks on U.S. air bases in the region that started last week.

U.S. stocks are poised to book another round of monthly losses as October draws to an end, though pressure has been attributed largely to a surge in Treasury yields. The S&P 500 SPX

last week joined the Nasdaq Composite COMP in correction territory, while the Dow DJIA

is down more than 2% year to date.

The rise in yields, which move opposite price, has come as U.S. government debt has failed to attract its usual haven-related buying amid rising Mideast tensions.

A researcher at Two Sigma Investments adjusted the hedge fund’s investing models without authorization, the firm has told clients, leading to losses in some funds, big gains in others and fresh regulatory scrutiny.

The researcher, Jian Wu, a senior vice president at New York-based Two Sigma, was trying to boost his compensation, Two Sigma has told clients, without identifying Wu. He made changes over the past year that resulted in a total of $620 million in unexpected gains and losses, according to people close to the matter and investor letters. Two Sigma has placed Wu on administrative leave.

In 1989, author Marsha Sinetar wrote a bestselling book, “Do What You Love, The Money Will Follow.” She urges readers to pursue a career that stokes their passion.

Many advisers take that advice. They love what they do. And the money follows: Median pay for U.S. financial advisers was $95,390 in 2022, according to the Bureau of Labor Statistics.

Lately, though, the passion is waning for some advisers. They still love the practice of wealth management — customizing financial plans, constructing client portfolios and analyzing the ever-growing menu of investment products.

They’re just not as enamored of their clients’ wealth. Reassuring wealthy retirees that they can afford to buy a second (or third) vacation home has its merits. But helping them accumulate more and more wealth rings hollow after awhile.

Steve Oniya, a Houston-based certified financial planner, works with a diverse mix of clients. He enjoys helping them achieve their goals, regardless of their net worth. “It’s more gratifying helping them get over some hurdles to get to the life that they really want,” he said. “You make more of an impact that way.”

He compares his work to a firefighter’s job. Some days, they rescue people from burning buildings. Other days, they put out a dumpster fire. Yet they’re always driven to excel and perform at a high level.

Nevertheless, if an adviser serves rich clients who hoard their money, don’t give to charity and lack perspective on what matters most in life, a day at the office can feel dispiriting. “Sometimes advisers may be passionately opposed to certain clients’ values,” Oniya said. “In those instances, end the relationship or limit the scope.”

Oniya said he does not find clients’ wealth objectionable. He sees his role as an ally who seeks to understand — and not judge — others’ beliefs and values.

“I like to stay in the neutral camp,” Oniya said. “It’s easy to empathize with another person and see they are a person who needs help just like others. We’re generally here to advise them on how to be more efficient and effective financially in attaining their goals.”

The arc of an adviser’s career comes into play as well. To build a practice, newly minted financial planners might welcome pretty much anyone with sufficient assets.

Once they establish a stable book of business, advisers may get picky in deciding whom to serve. Their onboarding process might get more rigorous in an effort to determine if they’re aligned with a potential client’s aspirations, goals and priorities.

Some advisers shift gears as they gain experience working with different types of clients. They come to realize what they like most about the job and adjust their practice — and the type of clients they serve — accordingly.

“Everyone evolves,” said Angeli Gianchandani, a professor of marketing at University of New Haven’s Pompea College of Business. “Advisers may see there’s a greater reward and opportunity helping people in a different income bracket.”

As a self-test, advisers at a career crossroads might want to ask themselves how they’d respond to two clients. The first one says, “You saved me $5 million. Now I want to save $10 million to buy a bigger yacht.”

The other says, “You helped me pay off my student debt” or “You helped me save enough for a down payment to buy my first house.”

“You may feel more valued and appreciated as an adviser” if you pave the way for someone who lacks vast wealth to build a nest egg for the future, Gianchandani says.

Advisers who have misgivings about helping wealthy people attain greater wealth are not alone. Brooke Harrington, a sociology professor at Dartmouth College, interviewed 65 wealth managers between 2007 and 2015. About one-quarter expressed qualms about helping lower ultra-wealthy clients’ tax liabilities.

Still, another 25% did not feel such qualms. They saw their role as defending their clients from an unjust tax code.

The Nasdaq Composite Index fell into its 70th correction in history on Wednesday, as surging long-term Treasury yields increased borrowing costs and weighed on stocks.

The interest rate sensitive Nasdaq COMP

barreled higher in the year’s first half, in part on optimism about a potential Federal Reserve pivot away from rate hikes to fight inflation, but stocks have been under fire in recent months as the Fed dialed up its message that interest rates could will stay higher for longer.

The tech-heavy equity index fell 2.4% on Wednesday to close below the 12,922.216 threshold, marking a drop of a least 10% from its prior peak, which was set in mid-July at 14,358.02, according to Dow Jones Market Data.

That met the common definition for a correction in an asset’s value and is the Nasdaq’s 70th close in correction territory since the index’s inception in February 1971.

Robert Pavlik, senior portfolio manager at Dakota Wealth Management, said the sharp rise in long-term Treasury yields has spooked investors, especially those in highflying, high-growth technology stocks where rising rates can be particularly corrosive.

Pavlik likened the dynamic to the spending power of a lottery winner hitting a jackpot when rates are at 2% versus someone who wins when rates are closer to 10%.

He also expects the 10-year Treasury yield BX:TMUBMUSD10Y,

which rose to 4.952% Wednesday, to top out at 5.25% to 5.5% and likely complicate any recovery for the Nasdaq.

In the past 20 corrections for the Nasdaq, it took an average of three months for performance to improve, with index then gaining 14.4% on average a year later, according to Dow Jones Industrial Average.

Nasdaq corrections are usually followed by a bounce in a few months

“You’re feeling the pressure in some big-name stocks,” Pavlik said. “But this too will, at some point, end. But concerns about the Fed are still in the forefront of everybody’s minds.”

The Nasdaq was still up 22.5% on the year through Wednesday, while the Dow Jones Industrial Average DJIA

was down 0.3% and the S&P 500 index SPX

was up 9% in 2023, according to FactSet.

Morgan Stanley said late Wednesday that Co-President Edward “Ted” Pick will become its chief executive, effective Jan. 1.

Outgoing Chief Executive James Gorman will become executive chairman, Morgan Stanley said. Pick will also join the firm’s board of directors.

“The board has unanimously determined that Ted Pick is the right person to lead Morgan Stanley and build on the success the firm has achieved under James Gorman’s exceptional leadership,” the company said in a statement.

“Ted is a strategic leader with a strong track record of building and growing our client franchise, developing and retaining talent, allocating capital with sound risk management, and carrying forward our culture and values,” it said.

Pick’s name had been among those in the running. The executive joined Morgan Stanley in 1990, and was promoted to managing director in 2002, according to his bio on the company’s website.

Gorman became CEO in January 2010, having joined the firm in 2006.

The lack of a clear successor at Morgan Stanley has weighed on its stock lately.

The shares are down 24% in the last three months, three times the losses for the S&P 500 index SPX

in the same period. So far this year, Morgan Stanley shares are down 16%, contrasting with an advance of about 9% for the S&P.

The Dow Jones Industrial Average opened higher on Wednesday as a post-earnings rally in shares of Microsoft Corp. MSFT, +3.71%

helped lift the blue-chip gauge while the S&P 500 and Nasdaq Composite sunk. The Dow gained 91 points, or 0.3%, at to trade at 33,218, according to FactSet data. Meanwhile, the S&P 500 SPX, -1.02%

shed 22 points, or 0.5%, to 4,225, and the Nasdaq COMP, -1.43%

fell by 135 points, or 1.1%, to 13,000. The Dow had snapped a four-day losing streak on Tuesday as U.S. stocks rebounded following the worst stretch of the year.

House Republicans on Tuesday night voted for Rep. Mike Johnson to become their latest nominee for speaker of the U.S. House of Representatives, with the Louisiana congressman’s selection capping a tumultuous day in which Rep. Tom Emmer was briefly the nominee.

Johnson, vice chair of the House Republican Conference, picked up support in two rounds of voting and drew a majority votes in a third ballot, topping the number of votes cast for Rep. Byron Donalds of Florida. That’s according to posts on social media by Rep. Elise Stefanik of New York, who as chair of the conference is the No. 4 House Republican.

The GOP-run House wasn’t due to hold a floor vote on the speaker position on Tuesday night, but the chamber could do that Wednesday.

Analysts have been warning that the long process of picking a new speaker is preventing the Republican-run House from addressing crucial matters, such as supporting Israel and passing a budget to avoid a government shutdown next month that could rattle markets SPX.

It has been three weeks since the historic ouster of former Speaker Kevin McCarthy, a California Republican.

The selection of Johnson marks the the fourth time that House GOP lawmakers have picked a speaker nominee this month. Emmer of Minnesota, the No. 3 House Republican, was nominated around mid-day Tuesday, beating out Johnson, but bowed out about four hours later after some colleagues and former President Donald Trump refused to support him.

Rep. Jim Jordan of Ohio secured the nomination on Oct. 13, but was dropped as the nominee last Friday as GOP opposition to him grew over three rounds of voting on the House floor. House Majority Leader Steve Scalise, a Louisiana Republican, was tapped for the post on Oct. 11 but ended his speaker bid a day later due to opposition from fellow Republicans.

McCarthy on Tuesday floated a plan that would reinstall him as speaker and set up Jordan as the assistant speaker, according to an NBC News report citing unnamed sources.

In the third ballot on Tuesday night, Johnson scored 128 votes, Donalds got 29 votes, and 44 lawmakers backed people who weren’t on the ballot, according to multiple published reports. Most of those Republicans supported McCarthy, while one supported Jordan.

Bitcoin surged over 10% on Monday, briefly surpassing $34,500, on continued optimism that an exchange-traded fund investing directly in the cryptocurrency will soon be approved in the U.S.

The largest cryptocurrency BTCUSD, +6.59%

by market cap on Monday reached as high as $34,616, the loftiest level since May 2022, according to CoinDesk data, before falling to around $33,021 by Monday evening. Other major cryptocurrencies also rose, with ether up 5.8% over the past 24 hours to $1,763.

The U.S. Securities and Exchange Commission has repeatedly rejected bitcoin ETF applications in the past, citing risks of market manipulation. But crypto-industry participants are expecting that to change soon.

A U.S. Appeals court on Monday issued a mandate, putting into effect its ruling in August, which overturned the SEC’s rejection of Grayscale Investments’ application to convert its Bitcoin Trust product GBTC

into an ETF. The final ruling on Monday confirmed Grayscale’s win in court.

Meanwhile, BlackRock’s proposed bitcoin ETF has been listed on the Depository Trust & Clearing Corporation. While it doesn’t mean that the ETF is guaranteed to be approved, it shows another step closer for BlackRock to bring the fund to the market.

If bitcoin ETFs are approved, the crypto may see “historical price increases,” with a crypto bull market coming, according to Alex Adelman, chief executive and co-founder of Lolli. “Bitcoin ETFs will give institutional and retail investors new ways to gain exposure to bitcoin within established regulations,” Adelman said.

A Wall Street strategist who foresaw the U.S. stock-market rally in the first half of the year now sees stocks treading water through the end of 2023, unlikely to extend the previous momentum until at least April 2024.

Barry Bannister, chief equity strategist at Stifel, extended his 4,400 target for the S&P 500 SPX

to April 2024 from the end of this year, as higher interest rates could pressure corporate earnings, weighing on stock prices, he said.

“We believe the rally off the Oct. 2022 lows is over, and our view since summer 2023 has been a sideways trading range,” Bannister said in a Monday note. “The updated view is that we now believe our year-end 2023 target of 4,400 applies through Apr. 30, 2024.”

Bannister was one of the few Wall Street strategists who correctly anticipated the U.S. stock-market rally in the first half of 2023. He also said economic risk for equities will rise in late 2023 as stock gains would stall in the second half of the year. He set his 4,400 year-end target for the S&P 500 in May, a roughly 4.3% advance from Monday’s close of 4,217.04, according to FactSet data.

“We traded the relief rally [in early 2023], turned neutral in summer 2023 and discouraged bullishness before the third quarter of 2023,” Bannister said. He said he thinks a new record-high for the S&P 500 by year-end 2023, as some of the most bullish strategists on Wall Street have projected, is “exceptionally unlikely.”

Meanwhile, Bannister thinks the key 10-year U.S. Treasury yield BX:TMUBMUSD10Y

will peak around 5% in the current cycle, but he projects a “normalized” 10-year yield of 5% or 6% in the mid-2020s, which could put pressure on corporate earnings.

The 10-year Treasury yield flirted with 5% on Monday for the first time since 2007, touching an intraday high of 5.02% in the morning trading before retreating to finish the New York session at 4.836%, according to Dow Jones Market Data.

“It is not ‘Fed high for longer’ — the Fed has returned to ‘policy modulation at normalized rates,’” Bannister wrote.

Bannister also pointed to the health of the U.S. labor market as a source of economic resilience and a reason for “the Fed rate normalization,” which could tighten financial conditions and weigh on price-to-earnings ratios for stocks.

The price-to-earnings ratio, sometimes known as the price multiple, is a ratio of a stock price divided by a public company’s yearly earnings per share. It is a way to determine stock valuation.

That’s why the strategist sees the S&P 500 will remain flat or “range-bound” for the rest of the 2020s decade as price-to-earnings ratios across U.S. firms will be halved due to tightening financial conditions, but it could offset growth in earnings-per-share (EPS). Bannister forecasts the S&P 500 EPS will at least double from $156 in 2019 to a range of $300-325 in 2030.

EPS is a company’s net profit divided by the number of common shares it has outstanding, and it usually indicates how much money a company makes for each share of its stock.

U.S. stocks finished mostly lower on Monday, with the Dow Jones Industrial Average DJIA

down 190 points, or 0.6%, to end at 32,936, but the Nasdaq Composite COMP

edged up 0.3%, according to FactSet data.

Bill Gross, a co-founder of fixed-income investing giant Pacific Investment Management Co., said Monday in a post on social-media platform X that the U.S. economy is likely headed for a recession by year’s end.

“Regional bank carnage and recent rise in auto delinquencies to long-term historical highs indicate U.S. economy slowing significantly. Recession in 4th quarter,” Gross said.

Such an outcome would represent a remarkable turnaround, considering the Atlanta Federal Reserve’s GDP Now real-time indicator shows the U.S. economy expanding at a 5.4% annualized clip during the third quarter. Official GDP data is due Thursday, with economists polled by The Wall Street Journal looking, on average, for a 4.5% annualized growth figure.

Many Wall Street economists had anticipated that the U.S. recession would slide into recession earlier this year. However, strength in construction, consumer spending and other areas has helped it defy expectations, as data show it has instead continued to expand at a solid pace.

Revised data released last month by the Commerce Department showed the U.S. economy grew by 2.1% during the second quarter. Typically, investors only become aware of recessions in hindsight after they’ve been officially declared by the National Bureau of Economic Research.

Rising auto-loan delinquencies are an alarming portent of economic pain to come, Gross said, citing data from Fitch Ratings, reported by Bloomberg News on Friday, which showed the percentage of subprime auto loans more than 60 days delinquent surpassed 6% in September. At 6.1%, it’s the highest rate ever recorded by the data series going back to 1994.

As far as how investors might play this, Gross said he’s “seriously considering” investing in shares of regional banks, which have fallen substantially this year: the SPDR S&P Regional Banking ETF KRE,

one popular exchange-traded fund tracking regional players down more than 30% year-to-date. He also touted some merger-arbitrage plays, a strategy he endorsed in a recent investment outlook.

He also recommended betting that the Treasury curve will continue steepening as it looks to break out of negative territory for the first time in more than a year. Rising long-term rates have nearly caught up with short term rates, with the 10-year yield BX:TMUBMUSD10Y

within 30 basis points of the 2-year yield BX:TMUBMUSD02Y

on Monday.

10-year yields have been lower than 2-year yields for 327 days, according to Dow Jones Market Data. That’s the longest stretch since the 444-trading day streak that ended May 1, 1980.

Gross is using interest-rate futures for his steepening trade. He expects the curve will re-enter positive territory before the end of the year as a slowing economy forces investors to adjust their expectations regarding the timing of Federal Reserve interest-rate cuts.

“’Higher for longer’ is yesterday’s mantra,” Gross said.

Following a decadeslong career on Wall Street, Gross announced his retirement a few years back after a stint at Janus Capital Group. He joined Janus after a contentious exit from Pimco.

Nevertheless, Gross has continued to share his views on markets in posts on X, as well as in investing outlook letters published to his website, and during interviews with the financial press.

U.S. stocks are sliding this week, erasing October’s gains, as higher Treasury yields weigh on markets. The Dow Jones Industrial Average DJIA , S&P 500 SPX and Nasdaq Composite COMP were all down heading toward the closing bell on Friday, with each index on pace for a weekly loss. Investors saw this month’s gains evaporate on Thursday, as equities fell under pressure from rising interest rates in the bond market as investors weighed Federal Reserve Chair Jerome Powell’s remarks that another rate hike may be needed to slow the economy and bring down inflation. So far this month, the Dow has slumped 1%, the S&P 500 has…

The 10-year Treasury yield continued to pull back from 5% on Friday after moving tantalizingly close to surpassing that level in the previous session.

The yield touched 5% at 5:02 p.m. Eastern time on Thursday, only to drift back down, according to Tradeweb data. It ended Friday’s New York session down by 6.3 basis points at 4.924%.

Rising Middle East tensions gave way to renewed safe-haven demand in government debt on Friday that not only sent the 10-year yield BX:TMUBMUSD10Y

lower, but dragged down rates on everything from 3-month Treasury bills BX:TMUBMUSD03M

to the 30-year bond BX:TMUBMUSD30Y.

Investors were trying to catch the proverbial falling knife by taking advantage of a cheaper 10-year Treasury note, the product of recent selloffs. Analysts warn that it’s difficult to have much short-term conviction in catching that knife, however, given the likelihood that the selloff could return.

One big reason is the onslaught of new supply from the U.S. Treasury as the result of the government’s growing borrowing needs, which is raising the risk that investors will keep demanding more compensation to hold long-dated debt to maturity.

On Oct. 30 and Nov. 1, which is the same day as the Federal Reserve’s next policy decision, Treasury is expected to provide updated guidance on its borrowing needs and auction sizes. Treasury’s refunding announcement could even upstage the Federal Open Market Committee — creating “fertile ground for a continuation of the selloff in Treasuries,” said BMO Capital Markets rates strategists Ian Lyngen and Ben Jeffery.

Over the next several weeks, “it becomes much easier to envision a surge in Treasury yields in anticipation of the upcoming coupon supply,” they wrote in a note on Friday. While the 10-year yield has stopped shy of 5%, “we continue to expect this milestone will be reached shortly.”

Stock-market investors have been focused on the prospects of a 5% 10-year yield because such a level would dent the appeal of equities and make government debt a more attractive investment by comparison.

As of Friday, the 10-year yield, used as the benchmark on everything from mortgages to student and auto loans, has jumped 163.9 basis points from its 52-week low of almost 3.29% reached on April 5. The 10-year yield hasn’t ended the New York session above 5% since July 19, 2007.

COMP

ended the day lower as the prospects of a widening conflict in the Middle East triggered a flight-to-safety trade into Treasurys.

Taking a step back, a 5% 10-year yield would imply that a Goldilocks-scenario of a U.S. economy — one that’s neither too hot or too cold, and able to sustain moderate growth — “is here to stay for a decade,” or that the Fed’s main interest-rate target needs to be materially higher on average over the next decade, according to BMO’s Lyngen and Jeffery. One of the biggest questions facing policy makers is whether the economy might be moving into a new stage in which even higher interest rates down the road could be required to cool demand and activity.

Though BMO Capital Markets is biased toward lower yields into the weekend given the absence of major economic data on Friday, technical indicators “continue to favor higher rates in the near-term,” and “our conviction that 5% will ultimately be traded through has grown.”

In my day, applying to college meant thumbing through a big paperback encyclopedia of college listings and then pulling out the typewriter and filling in applications. Thirty-some years later as my kid prepares to apply, I need a spreadsheet and access to reams of data that I’m not sure how to process.

I’ve tried doing it the old-fashioned way, by searching through the websites of all the schools my high-school senior is interested in applying to. For each school, you need to find the common data set, a multipage PDF that lists seemingly unrelated stats. Then you need to run the net-price calculator, which attempts to give you a price tag based on the financial information you input. Then you put everything together to try to get some sense of your kid’s chances of getting in and what it might cost you so you can compare the schools to each other.

Of course, there’s an app for that. Well, not so much one app, but several different programs that purport to sort college data in a useful way — some of them free, some by subscription and some through the school. All of it is still confusing and overwhelming for the average family.

Big J Education Consulting is attempting to make it easier with interactive charts, available on its website for free, that allow you to easily sort through data from the common data sets of hundreds of schools, plus some of the company’s own fact-checked and reported updates. Co-owners Jennie Kent and Jeff Levy have been making these charts for years for their own business, and they went high-tech with a new format this year that makes sorting and crunching the data easy enough for a layperson to do.

“People think about that common data set as a snapshot, but it’s really more of a collage,” says Kent. “Admissions fills out part, financial aid fills out part. Sometimes numbers are off, and we reach out to institutions. The best that any of us can do with this is to use the common data set.”

Take, for instance, the sometimes outrageous cost-of-attendance number, a sticker price that includes tuition, room and board, books and fees for one year. At the top of their list is Northwestern University in Evanston, Ill., at a whopping $89,394. Levy and Kent say they are hearing from a number of schools that the price for the upcoming year will be over $90,000, at least for international students.

Need-based and merit aid for the class of 2026, sorted by total cost of attendance for out-of-state students.

Credit: Jennie Kent, Jeff Levy, and Big J Educational Consulting, 2023

You can learn a lot from looking at a chart like this and playing with it according to the choices pertinent to your family. For instance, one thing to note is that if you sort by price, you don’t see prices below $80,000 until you get four pages in. Those are the most expensive 78 out of 427 schools.

To get to the least expensive schools, you have to sort by in-state prices, because most of these will be public institutions that offer special pricing to state residents.

Need-based and merit aid for the class of 2026, sorted by total cost of attendance for in-state students.

Credit: Jennie Kent, Jeff Levy, and Big J Educational Consulting, 2023

Of course, a school’s list price does not tell you how much it will cost your family to send a student there. The price you pay will depend on your own family’s financial situation, and that’s where all the strategizing comes in — and why families sometimes turn to professionals to crunch this data for them.

To get any kind of handle on that, you have to look at the other columns detailed on the chart below that analyze how much need-based aid a school gives and how much it gives out in so-called merit aid, which college finance experts have taken to calling “tuition discounting,” because it really just represents a coupon value off the sticker price.

If your family falls under the threshold of “need,” which varies by school, you can get a decent picture of what your price may be from the net-price calculator. But if you fall outside of those parameters, you’ll want to know how generous a school is with that tuition discounting. You really have to look at two numbers to figure this out, because the average amount of merit aid can be inflated by the small number of students it goes to.

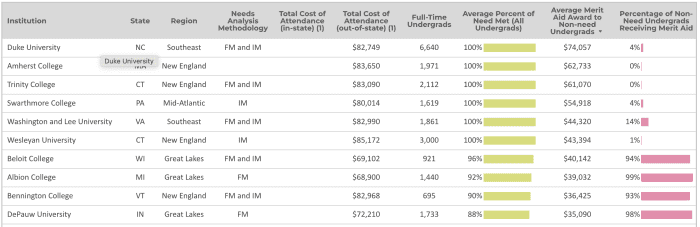

Need-based and merit aid for the class of 2026, average merit aid awarded to non-need undergrads.

Credit: Jennie Kent, Jeff Levy, and Big J Educational Consulting, 2023

For instance, according to common-data-set data compiled by Big J, Duke meets all needs of undergraduates and gives out an average of $74,057 in merit awards to non-need undergrads, but it only gives that out to 4% of its full-pay applicants. Whereas Beloit College meets 96% of need but gives out an average of $40,142 in merit awards to 94% of non-need undergrads. Which sounds like the better chance of getting a discount?

You can input your own selection of colleges into this list and do a comparison that way. I input the top colleges on my child’s list and was able to see how they stacked up against each other in terms of merit aid and tuition price. I found that useful for weeding some out.

Playing the early game

None of the price modeling matters if your child doesn’t get into a school in the first place. That’s where strategizing over what type of application to submit matters. A little data visualization on early admission might help you if you want to play that game. And if you pair it with the financial data, you can get a sense of whether it matters at a particular school to apply early, and what it might cost you — since the decision is supposed to be binding.

The choice of whether to apply for early decision is complicated this year because the federal financial-aid form, FAFSA, is not opening until December, and schools cannot typically finalize their aid packages without it. Plus, more colleges across the spectrum are filling their classes with early admits because it maximizes their yield statistics — that is, the number of students who accept their offers. So competition is fierce.

Early-decision and regular-decision acceptance rates for the class of 2026, sorted by early admits as percent of freshman class.

Credit: Jennie Kent, Jeff Levy, and Big J Educational Consulting, 2023

On the Big J chart for early-decision and regular-decision acceptance rates, the schools making the most of this are filling more two-thirds of their classes with early admits. They are also typically accepting students at a far greater rate from the early-decision pool than they are from the regular-decision pool. At Tulane, for instance, the early-decision acceptance rate is 8.6 times greater than that for regular decisions.

Looking at that data might make you feel a little pressure, but remember, at the end of the day, the only school your child should pick for early decision is one that you can afford and that is a good fit for them.

I recently graduated with my master’s degree and am seeking full-time employment at age 53. I want to know what is the best way to invest some of my earnings when I begin receiving a paycheck. I expect to have an annual salary of between $80,000 and $90,000.

For religious reasons, I cannot invest to earn interest, but business-related ventures such as stocks are acceptable. I am planning to set aside up to $1,000 per month for investment purposes, so that I can build some retirement funds. What are my options?

“You have already made the best investment you can make — one in yourself, your education and your future.”

MarketWatch illustration

Dear First-Time,

Congratulations on your master’s degree. You have already made the best investment you can make — one in yourself, your education and your future. It takes patience, guts and stamina to go back to college in your 50s, and you should be very proud. You were one of about 505,000 students in college ages 50 and over, representing less than 4% of the student population.

Given your faith, CDs and high-yield savings accounts are ruled out. A letter writer recently asked me where he should start looking to invest his $50,000 life savings, and I pointed him in the “make interest off your cash” direction, particularly given the recent rise in interest rates. That won’t work for you, but the good news is that you do have many options.

There are investment vehicles for you. In fact, the Accounting and Auditing Organization for Islamic Financial Institutions sets guidelines for investing in accordance with the Sharia religious code, including rules around companies that derive a percentage of their profits from tobacco and alcohol products. And, yes, it also regards interest as unjust and exploitative.

Saturna Capital has mutual funds that follow Islamic principles. The Amana Income Fund AMANX, which focuses on current income and the preservation of capital, has had an average annual five-year return of 8.8% for investor shares, slightly lower than the 9.9% average return for the S&P 500 SPX

over the same period with dividends reinvested. I suggest this as a guidepost rather than a recommendation.

Similarly, the Knights of Columbus assets are managed by Knights of Columbus Asset Advisors in accordance with Catholic moral principles, which are distilled to six main tenets: “protecting human life, promoting human dignity, reducing arms production, pursuing economic justice, protecting the environment [and] encouraging corporate responsibility.”

Of course, investing along religious principles — similar to ESG investment, which takes environmental, social, and corporate-governance factors into account when deciding what to do with your money — is fraught with complications, contradictions and problems with transparency. Regulators are cracking down on vehicles that “greenwash” their ESG credentials.

A major report by the Organization for Economic Cooperation and Development, an intergovernmental organization with 38 member nations, found that ESG ratings vary strongly depending on the provider, as they commonly use different measures, indicators, metrics, data and qualitative judgments to make decisions about funds and companies.

“Moreover, returns have shown mixed results over the past decade, raising questions as to the true extent to which ESG drives performance,” the OECD said. “This lack of comparability of ESG metrics, ratings, and investing approaches makes it difficult for investors to draw the line between managing material ESG risks within their investment mandates.”

You have many funds to choose from. If you’re Catholic, you could look into the Global X S&P 500 Catholic Values ETF CATH

; the LKCM Aquinas Catholic Equity Fund AQEIX; or Ave Maria, which offers mutual funds for growth AVEGX, value AVEMX and bonds AVEFX AVEFX. You can read more here. Investing based on religious, moral or ethical principles doesn’t guarantee a satisfactory return.

It’s not too late to start investing at 53. With the advice of a financial adviser, your risk profile may need regular adjusting, based on your age and tolerance. But you may work into your 70s and may live into your 80s or 90s, and you will want to find myriad ways to build your wealth throughout your retirement. Cash-hoarding typically gets outdone by inflation.

You may find a job with a 401(k) and an employer match, meaning your employer will contribute an additional sum toward your retirement based on the amount you are contributing every month. You may also consider an IRA. Both account types have “catch-up” contributions for people who are over 50. Annual IRA contribution limits for 2023 are $6,500 for people under 50, but $7,500 for those 50 and older.

You can also use pretax dollars for health savings accounts, which are used to offset the burden of high-deductible healthcare plans. With the latter, you pay a lower premium, but you will be saddled with higher out-of-pocket expenses for medical services should you require them. You can contribute up to $4,150 to an HSA for 2024, up from $3,850 this year.

As for right now? Pay off your credit cards. Don’t let high-interest debt trap you. Warren Buffett said one of the best investments he ever made was buying his Omaha, Neb., home for $31,500 in 1958. It’s worth $1.4 million today. He has said he may have put that money to better use if he had rented instead, but owning your own home will solidify your financial position in retirement.

Investing $1,000 a month may be ambitious. But thinking in the medium to long term — and knowing this is a marathon rather than a sprint, even at 53 — is half the battle. With compounding, or making money off your principal and the increase in value of your initial investment, you could have more than $120,000 in 10 years, and over $600,000 in 30 years.

Bravo on this new chapter. Take it one day, one week and one month at a time, and enjoy your life.

You can email The Moneyist with any financial and ethical questions at qfottrell@marketwatch.com, and follow Quentin Fottrell on X, the platform formerly known as Twitter.

Check out the Moneyist private Facebookgroup, where we look for answers to life’s thorniest money issues. Post your questions, tell me what you want to know more about, or weigh in on the latest Moneyist columns.

The Moneyist regrets he cannot reply to questions individually.