These are tricky times in the stock market, so it pays to look to the best stock-fund managers for guidance on how to behave now. Veteran value investor Bill Nygren belongs in this camp, because the Oakmark Fund OAKMX he co-manages consistently and substantially outperforms its peers.

That isn’t easy, considering how many fund managers fail to do so. Nygren’s fund beats its Morningstar large-cap value index and category by more than four percentage points annualized over the past three years. It also outperforms at five and…

U.S. stocks finished lower on Tuesday with only the Dow clinging to gains for the session as investors digested more earnings reports from major American firms. The S&P 500 SPX shed roughly 3 points, or 0.1%, to finish just shy of 4,017. The Nasdaq Composite COMP dropped by 30 points, or 0.3%, to roughly 11,334. The Dow Jones Industrial Average gained 104 points, or 0.3%, to finish at roughly 33,734. More earnings from major U.S. companies, including Microsoft Corp. MSFT are due out after the bell.

U.S. stocks finished at their highest level in a month on Monday as strong performances by consumer-technology giant Apple Inc. AAPL, +2.35%

and chipmaker NVIDIA Inc. NVDA, +7.59%

pushed the Nasdaq Composite COMP, +2.01%

further into the lead. The Nasdaq gained roughly 223 points, or 2%, to finish at around 11,364, bringing the tech-heavy index’s year-to-date gain to 8.6%, according to FactSet data. The Dow Jones Industrial Average DJIA, +0.76%

gained 254 points, or 0.8%, to close at roughly 33,630. The S&P 500 SPX, +1.19%

gained 47 points, or 1.2%, to 4,020. The Dow is up approximately 1.5% since the start of the year, while the S&P 500 is up roughly 4.7%. The tech-heavy Nasdaq has outperformed the other major U.S. indexes since the start of 2023, a reversal of the trend from 2022, when the value-heavy Dow outperformed the Nasdaq by the widest margin since 2000, according to Dow Jones Market Data. Investors await a batch of earnings from megacap technology stocks this week, including Microsoft Corp MSFT, +0.98%.

Short selling can be controversial, especially among management teams of companies whose stocks traders are betting that their prices will fall. And a new spike in alleged “naked short selling” among microcap stocks is making several management teams angry enough to threaten legal action:

Taking a long position means buying a stock and holding it, hoping the price will go up.

Shorting, or short selling, is when an investor borrows shares and immediately sells them, hoping he or she can buy them again later at a lower price, return them to the lender and pocket the difference.

Covering is when an investor with a short position buys the stock again to close a short position and return the shares to the lender.

If you take a long position, you might lose all your money. A stock can go to zero if a company goes bankrupt. But a short position is riskier. If the share price rises steadily after an investor has placed a short trade, the investor is sitting on an unrealized capital loss. This is why short selling traditionally has been dominated by professional investors who base this type of trade on heavy research and conviction.

Brokers require short sellers to qualify for margin accounts. A broker faces credit exposure to an investor if a stock that has been shorted begins to rise instead of going down. Depending on how high the price rises, the broker will demand more collateral from the investor. The investor may eventually have to cover and close the short with a loss, if the stock rises too much.

And that type of activity can lead to a short squeeze if many short sellers are surprised at the same time. A short squeeze can send a share price through the roof temporarily.

Short squeezes helped feed the meme-stock craze of 2021 that sent shares of GameStop Corp. GME, +10.45%

and AMC Entertainment Holdings Inc. AMC, +2.54%

soaring early in 2021. Some traders communicating through the Reddit WallStreetBets channel and in other social media worked together to try to force short squeezes in stocks of troubled companies that had been heavily shorted. The action sent shares of GameStop soaring from $4.82 at the end of 2020 to a closing high of $86.88 on Jan. 27, 2021, only for the stock to fall to $10.15 on Feb. 19, 2021, as the seesaw action continued for this and other meme stocks.

Naked shorting

Let’s say you were convinced that a company was headed toward financial difficulties or even bankruptcy, but its shares were still trading at a value you considered to be significant. If the shares were highly liquid, you would be able to borrow them through your broker for little or almost no cost, to set up your short trade.

But if many other investors were shorting the stock, there would be fewer shares available for borrowing. Then your broker would charge a higher fee based on supply and demand.

For example, according to data provided by FactSet on Jan. 23, 22.7% of GameStop’s shares available for trading were sold short — a figure that could be up to two weeks out-of-date, according to the financial data provider.

According to Brad Lamensdorf, who co-manages the AdvisorShares Ranger Equity Bear ETF HDGE, -2.65%,

the cost of borrowing shares of GameStop on Jan. 23 was an annualized 15.5%. That cost increases a short seller’s risk.

What if you wanted to short a stock that had even heavier short interest than GameStop? Lamensdorf said on Jan. 23 that there were no shares available to borrow for Carvana Co. CVNA, +10.63%,

Bed Bath & Beyond Inc. BBBY, -12.24%,

Beyond Meat Inc. BYND, +11.31%

or Coinbase Global Inc. COIN, +1.45%.

If you wanted to short AMC shares, you would pay an annual fee of 85.17% to borrow the shares.

Starting last week, and flowing into this week, management teams at several companies with microcap stocks (with market capitalizations below $100 million) said they were investigating naked short selling — short selling without actually borrowing the shares.

This brings us to three more terms:

A short-locate is a service a short seller requests from a broker. The broker finds shares for the short seller to borrow.

A natural locate is needed to make a “proper” short-sale, according to Moshe Hurwitz, who recently launched Blue Zen Capital Management in Atlanta to specialize in short selling. The broker gives you a price to borrow shares and places the actual shares in your account. You can then short them if you want to.

A nonnatural locate is “when the broker gives you shares they do not have,” according to Hurwitz.

When asked if a nonnatural locate would constitute fraud, Hurwitz said “yes.”

How is naked short selling possible? According to Hurwitz, “it is incumbent on the brokers” to stop placing borrowed shares in customer accounts when supplies of shares are depleted. But he added that some brokers, even in the U.S., lend out the same shares multiple times, because it is lucrative.

“The reason they do it is when it comes time to settle, to deliver, they are banking on the fact that most of those people are day traders, so there would be enough shares to deliver.”

Hurwitz cautioned that the current round of complaints about naked short selling wasn’t unusual and even though short selling activity can push a stock’s price down momentarily, “short sellers are buyers in waiting.” They will eventually buy when they cover their short positions.

“But to really push a stock price down, you need long investors to sell,” he said.

Different action that can appear to be naked shorting

Lamensdorf said the illegal naked shorting that Verb Technology Co. VERB, +69.65%,

Genius Group Ltd. GNS, +45.37%

and other microcap companies have been recently complaining about might include activity that isn’t illegal.

An investor looking to short a stock for which shares weren’t available to borrow, or for which the cost to borrow shares was too high, might enter into “swap transactions or sophisticated over-the-counter derivative transactions,” to bet against the stock,” he said.

This type of trader would be “pretty sophisticated,” Lamensdorf said. He added that brokers typically have account minimums ranging from $25 million to $50 million for investors making this type of trade. This would mean the trader was likely to be “a decent-sized family office or a fund, with decent liquidity,” he said.

Elon Musk testified Monday he believed he had funding secured to take Tesla Inc. private, both from a Saudi Arabia investment fund and from his stake in SpaceX.

The Tesla chief executive resumed testimony in a federal trial in San Francisco over investor losses allegedly caused by tweets he fired off in 2018, including his “funding secured” tweet.

Representatives of Saudi Arabia’s investment fund “were unequivocal about moving forward,” Musk said. He also mentioned his large stake in privately held aerospace company SpaceX, and that “alone meant funding was secured.”

Tesla TSLA, +8.48%

stock added to gains as Musk’s testimony got underway, and at last check was up nearly 8% and far outperforming the broader equity indexes.

The stock traded as high as $143.50, its highest intraday since Dec. 20, and was on pace to close at its best since that date.

The CEO told the court that the $420-a-share price on the deal “was a coincidence” as it was roughly a 20% premium over Tesla’s stock price at the time, and “not a joke.”

In certain circles, the number 420 refers to marijuana use.

Lead defense lawyer Nicholas Porritt also asked several questions that led Musk to say he hadn’t talked to major Tesla shareholders such as Baillie Gifford and T. Rowe Price about possibly taking Tesla private. Musk also said he couldn’t recall specifics around speaking with the board about the plan.

Firing off the now famous “funding secured” was a way to stay ahead of a soon-to-be-run Financial Times story about the Saudi fund taking a large stake at Tesla and as a way to keep all Tesla investors informed, Musk said. Moreover, he tweeted that he was “considering” the move, “not saying that it would be done,” Musk told the court.

Musk gave brief testimony Friday before the court adjourned for the day, taking pains to make clear that his tweets are not always taken to the letter. The trial started last week and it is expected to go into February.

“Just because I tweet something, it does not mean people believe it, or act accordingly,” Musk said on Friday to a defense attorney.

The trial revolves around Musk’s tweets from August 2018, including one where he told his millions of Twitter followers he was “considering taking Tesla private at $420” and then added “funding secured.” The plan later fizzled out.

Investor Glen Littleton, the lead plaintiff in the case, alleges he lost money due to the false tweets and is seeking damages.

U.S. District Judge Edward Chen already has ruled that Musk’s tweets about taking Tesla private were not true and that Musk acted with recklessness.

It is still up to jurors to decide, however, if the tweets were material to investors and if the falsehoods caused investor losses.

The CEO and Tesla each were fined $20 million in September 2018 to settle civil charges around the “funding secured” tweets and Musk was stripped of his chairman role at Tesla.

Musk and Tesla agreed to settle the charges against them without admitting to nor denying the SEC’s allegations.

Most investors want to keep things simple, but digging a bit into details can be lucrative — it can help you match your choices to your objectives.

The JPMorgan Equity Premium Income ETF JEPI, +0.20%

has been able to take advantage of rising volatility in the stock market to beat the total return of its benchmark, the S&P 500 SPX, +1.19%,

while providing a rising stream of monthly income.

The objective of the fund is “to deliver a significant portion of the returns associated with the S&P 500 Index with less volatility,” while paying monthly dividends, according to JPMorgan Asset Management. It does this by maintaining a portfolio of about 100 stocks selected for high quality, value and low price volatility, while also employing a covered-call strategy (described below) to increase income.

This strategy might underperform the index during a bull market, but it is designed to be less volatile while providing high monthly dividends. This might make it easier for you to remain invested through the type of downturn we saw last year.

JEPI was launched on May 20, 2020, and has grown quickly to $18.7 billion in assets under management. Hamilton Reiner, who co-manages the fund with Raffaele Zingone, described the fund’s strategy, and its success during the 2022 bear market and shared thoughts on what may lie ahead.

Outperformance with a smoother ride

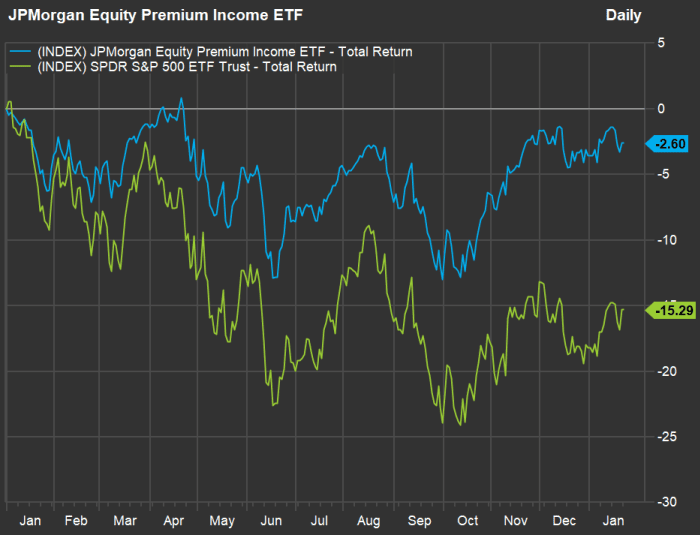

First, here’s a chart showing how the fund has performed from when it was established through Jan. 20, against the SPDR S&P 500 ETF Trust SPY, +1.20%,

both with dividends reinvested:

JEPI has been less volatile than SPY, which tracks the S&P 500.

FactSet

Total returns for the two funds since May 2020 pretty much match, however, JEPI has been far less volatile than SPY and the S&P 500. Now take a look at a performance comparison for the period of rising interest rates since the end of 2021:

Rising stock-price volatility during 2022 helped JEPI earn more income through its covered call option strategy.

FactSet

Those total returns are after annualized expenses of 0.35% of assets under management for JEPI and 0.09% for SPY. Both funds have had negative returns since the end of 2021, but JEPI has been a much better performer.

““Income is the outcome.””

— Hamilton Reiner

The income component

Which investors JEPI is designed for? “Income is the outcome,” Reiner responded. “We are seeing a lot of people using this as an anchor tenant for income-oriented portfolios.”

The fund quotes a 30-day SEC yield of 11.77%. There are various ways to look at dividend yields for mutual funds or exchange-traded funds and the 30-day yield is meant to be used for comparison. It is based on a fund’s current income distribution profile relative to its price, but the income distributions that investors actually receive will vary.

It turns out that over the past 12 months, JEPI’s monthly distributions have ranged between 38 cents a share and 62 cents a share, with a rising trend over the past six months. The sum of the past 12 distributions has been $5.79 a share, for a distribution yield of 10.53%, based on the ETF’s closing price of $55.01 on Jan. 20.

JEPI invests at least 80% of assets in stocks, mainly selected from those in the S&P 500, while also investing in equity-linked notes to employ a covered call option strategy which enhances income and lowers volatility. Covered calls are described below.

Reiner said that during a typical year, investors in JEPI should expect monthly distributions to come to an annualized yield in the “high single digits.”

He expects that level of income even if we return to the low-interest rate environment that preceded the Federal Reserve’s cycle of rate increases that it started early last year to push down inflation.

JEPI’s approach may be attractive to investors who don’t need the income now. “We also see people using it as a conservative equity approach,” Reiner expects the fund to have 35% less price volatility than the S&P 500.

Getting back to income, Reiner said JEPI was a good alternative even for investors who were willing to take credit risk with high-yield bond funds. Those have higher price volatility than investment-grade bond funds and face a higher risk of losses when bonds default. “But with JEPI you don’t have credit risk or duration risk,” he said.

An example of a high-yield bond fund is the iShares 0-5 Year High Yield Corporate Bond ETF SHYG, -0.10%.

It has a 30-day yield of 7.95%.

When discussing JEPI’s stock selection, Reiner said “there is a significant active component to the 90 to 120 names we invest in.” Stock selections are based on recommendations of JPM’s analyst team for those that are “most attractively priced today for the medium to long term,” he said.

Individual stock selections don’t factor in dividend yields.

Covered call strategies and an example of a covered-call trade

JEPI’s high income is an important part of its low-volatility total-return strategy.

A call option is a contract that allows an investor to buy a security at a particular price (called the strike price) until the option expires. A put option is the opposite, allowing the purchaser to sell a security at a specified price until the option expires.

A covered call option is one an investor can write when they already own a security. The strike price is “out of the money,” which means it is higher than the stock’s current price.

Here’s an example of a covered call option provided by Ken Roberts, an investment adviser with Four Star Wealth Management in Reno, Nev.

You bought shares of 3M Co. MMM, +1.63%

on Jan. 20 for $118.75.

You sold a $130 call option with an expiration date of Jan. 19, 2024.

The premium for the Jan. 24, $130 call was $7.60 at the time that MMM was selling for $118.75.

The current dividend yield for MMM is 5.03%.

“So the maximum gain for this trade before the dividend is $18.85 or 15.87%. Add the divided income and you’ll get 20.90% maximum return,” Roberts wrote in an email exchange on Jan. 20.

If you had made this trade and 3M’s shares didn’t rise above $130 by Jan. 19, 2024, the option would expire and you would be free to write another option. The option alone would provide income equivalent to 6.40% of the Jan. 20 purchase price in the period of a year.

If the stock rose above $130 and the option were exercised, you would have ended up with the maximum gain as described by Roberts. Then you would need to find another stock to invest in. What did you risk? Further upside beyond $130. So you would have written the option only if you had decided you would be willing to part with your shares of MMM for $130.

The bottom line is that the call option strategy lowers volatility with no additional downside risk. The risk is to the upside. If 3M’s shares had doubled in price before the option expired, you would still wind up selling them for $130.

JEPI pursues the covered call options strategy by purchasing equity-linked notes (ELNs) which “combine equity exposure with call options,” Reiner said. The fund invests in ELNs rather than writing its own options, because “unfortunately option premium income is not considered bona fide income. It is considered a gain or a return of capital,” he said.

In other words, the fund’s distributions can be better reflected in its 30-day yield, because option income probably wouldn’t be included.

One obvious question for a fund manager whose portfolio has increased quickly to almost $19 billion is whether or not the fund’s size might make it difficult to manage. Some smaller funds pursuing narrow strategies have been forced to close themselves to new investors. Reiner said JEPI’s 2% weighting limitation for its portfolio of about 100 stocks mitigates size concerns. He also said that “S&P 500 index options are the most liquid equity products in the world,” with over $1 trillion in daily trades.

Summing up the 2022 action, Reiner said “investing is about balance.” The rising level of price volatility increased options premiums. But to further protect investors, he and JEPI co-manager Raffaele Zingone also “gave them more potential upside by selling calls that were a bit further out of the money.”

“It’s like being robbed in a library, but you can’t shout ‘Thief!’ because there are ‘Silence, please’ signs everywhere.”

That’s how Roger Hamilton, chief executive of Genius Group Ltd. GNS, +55.02%,

describes the powerlessness he feels as U.S. securities rules prevent him from discussing his company’s share price, even as it comes under attack from a group of naked short sellers.

The Singapore-based education company on Thursday announced it had appointed a former FBI director to lead a task force investigating alleged illegal trading in its stock that it first addressed in early January.

The news sent the stock up a record 290% on Thursday, and it climbed another 59% on Friday. Volume of about 270 million shares traded in Thursday’s session crushed the daily average of about 634,000 — another indicator, Hamilton told MarketWatch in an interview Friday, of wrongdoing, given that the company’s float is just 10.9 million shares. “Clearly, that’s far more shares than we created,” he said.

Genius Group has evidence from Warshaw Burstein LLP and Christian Levine Law Group, with tracking from Share Intel, that certain individuals and/or companies sold but failed to deliver a “significant” amount of its shares as part of a scheme seeking to artificially depress the stock price.

The company is now exploring legal action and is planning an extraordinary general meeting in the coming weeks to get shareholder approval for its planned actions. These include paying a special dividend as a way to flush out bad actors and working with regulators to share information.

Share Intel uses tracking software in real time to determine exactly where there are discrepancies in the market and where brokers are opening large positions, Hamilton said. The software can measure the number of shares that are being naked shorted and has found multiple instances where significant amounts of fake shares were being created, said Hamilton.

Naked short selling is illegal under Securities and Exchange Commission rules, but that hasn’t stopped the practice, which Hamilton said affects far more companies than is generally known.

In regular short trading, an investor borrows shares from someone else, then sells them and waits for the stock price to fall. When that happens the shares are bought cheaper and returned to the prior owner, with the short seller pocketing the difference as profit.

In naked short selling, investors don’t bother borrowing the stock first and simply sell shares with a promise to deliver them at a later date. When that promise is not fulfilled, it’s known as failure to deliver.

By repeating that process again and again, bad actors can generate massive profits and manipulate a stock’s price lower, with an ultimate goal of driving a company to bankruptcy, at which point all the equity is wiped out and the naked shorts no longer need to be covered.

Hamilton said the evidence gathered by Genius Group shows a great deal of the illegal activity is happening on U.S. exchanges, but there’s also activity happening off-exchange and involving dark pools.

The company is fighting back “because we want this to stop,” Hamilton told MarketWatch. “They’re taking value away from our shareholders. They’re predators. They’re doing something illegal, and we want it to stop, whether that means getting regulators to enforce existing regulations or put new ones in place.”

Public companies have to have committees to monitor and report internal fraud to protect shareholders, he said. But there is no such team looking for external fraud and many retail investors see stocks being manipulated, he said.

“Hopefully, regulations will change and regulators will see there are as many, if not more, threats from outside a company,” he said.

Genius Group is not alone, said Hamilton. He cited among other examples Torchlight, an oil- and gas-exploration company that decided to merge with Metamaterial Inc. to thwart a naked-short-selling attack.

The stock rose from 30 cents to $11 in the six months after the deal was completed, and the company was able to raise about $183 million through a combination of convertible debt and equity. An interview Hamilton conducted with Torchlight’s former CEO, John Brda, can be found below.

Then there’s Jeremy Frommer, CEO of Creatd Inc. CRTD, +4.14%,

which aims to unlock creativity for creators, brands and consumers, who is behind Ceobloc, a website that aims to end the practice of naked short selling.

“Illegal naked short selling is the biggest risk to the health of today’s public markets,” is how the site introduces its mission.

On Friday, the stock of Helbiz Inc. HLBZ, +65.48%

joined Genius Group in rocketing higher in high volume, after that company said it, too, was taking on naked short sellers.

The New York–based maker of e-scooters and e-bicyles said that it was following Genius Group’s example and that it believes “certain individuals and/or companies may have engaged in illegal short selling practices that have artificially depressed the stock price.” The stock had plummeted 64% over the three months through Thursday’s close at 12.31 cents.

Genius Group’s stock, which went public in April 2022 at $6 a share, has gained more than 600% this week. The S&P 500 SPX, +1.89%

has gained 1.1% over the same four trading sessions.

The stock of a Singapore-based ed-tech and education company called Genius Group Ltd. rallied more than 200% on Thursday, after it said it appointed a former F.B.I. director to lead a task force investigating alleged illegal trading in its stock that it first disclosed in early January.

The stock was last up 264% to mark its biggest-ever one-day percentage gain. Volume of 197.76 million shares traded crushed the 65-day average of just 634,17. Genius Group GNS, +290.29%

also said it would issue a special dividend to shareholders to help expose the wrongdoing and is considering a dual listing that would make illegal naked short selling more difficult.

The task force will be led by Timothy Murphy, a former deputy director of the F.B.I. who is also on the board. It will include Richard Berman, also a Genius Group Director and chair of the company’s Audit Committee, and Roger Hamilton, the chief executive officer of Genius Group.

“The company has been in communication with government regulatory authorities and is sharing information with these authorities to assist them,” the company said in a statement.

Genius Group said it has proof from Warshaw Burstein LLP and Christian Levine Law Group, with tracking from Share Intel, that certain individual and/or companies sold but failed to deliver a “significant” amount of its shares as part of a scheme seeking to artificially depress the stock price.

It will now explore legal action and will hold an extraordinary general meeting in the coming weeks to get shareholder approval for its planned actions.

Genius’ IPO priced at $6 a share in April of 2022, he wrote in a blog. The company, which aims to develop an entrepreneur education system, then completed five acquisitions of education companies to build out its portfolio and reported more than 60% growth in its last earnings report.

Analysts at Diamond Equity assigned it an $11.28 stock price target, while Zacks assigned it a $19.20 stock price target.

“By all measures, we believed we were doing all the right things to justify a rising share price,” said Hamilton.

The company then announced two funding rounds totaling $40 million to grow its balance sheet to more than $60 million, yet its stock fell to under 40 cents, or less than 25% of the cash raised and less than 20% of its net assets.

“This didn’t happen gradually,” the executive wrote. “It happened in two month intervals from our IPO, in June, August, October and December. Each time, over a period of a few days, massive selling volume that was a multiple of our float (As most of our shares are on lock up, only around 4 million are tradeable) was sold into the market, making our share price drop by 50% or more.”

The company has since drawn on Wes Christian, a short-selling litigator from Christian Levine Law Group, who has helped it understand how naked short selling works, and then Share Intel helped find the proof that that’s what has happened.

Individuals or groups get together and sell shares in a target company that they don’t own, with the aim of getting the share price to fall 50% in a short period. They use small-cap firms that have low buying volume, allowing them to scare off buyers.

“The broker doesn’t bother to find shares to borrow,” said Hamilton. “They simply sell shares they don’t have and after a few days book them as FTDs (failure to deliver) or hide them as long sales instead of short sales. The people who bought the shares have no idea they bought a fake share, and suddenly there’s plenty more shares in the market than there should be.”

If these groups sell 6 million shares from $12 to $6 each, and then buy back over two months at under $6, they double their money. That allows them to make up to $30 million out of thin air. They can then repeat the whole process a few months later.

“If they don’t buy back all the shares, they simply leave them as FTDs or hide them in offshore accounts,” he wrote. “At no point do they need to put up any cash to make this happen, as they’re making money from the moment they start selling fake shares.”

The ultimate goal is to push a company into bankruptcy, where the equity will be wiped out, meaning they never have to cover the short position on the fake shares.

By issuing a special dividend, Genius is hoping to find who is responsible, as all brokers are forced to disclose to the Depository Trust & Clearing Corp. (DTCC) how many shares their clients hold and how many dividends will be paid. Theoretically, that should expose the oversold shares and dishonest brokers will be forced to cover their position, said Hamilton.

In practice, dishonest brokers will not declare the fake shares and just pay the dividend out of their own pockets.

“If you issue a dividend that isn’t straight cash—such as a spinoff of a company so you are issuing shares, or a blockchain based asset, then the brokers can’t do that are a forced to either cover or be exposed,” he wrote.

Embattled crypto lender Genesis announced that it had filed for bankruptcy late Thursday, the latest firm to be taken amid a widespread rout among crypto companies driven by plunging prices and charges of fraud at major players like FTX.

Genesis, which froze customer withdrawals in November following the collapse of FTX, filed for Chapter 11 bankruptcy protection in federal court in Manhattan for its lending units, saying it was the best way for it to achieve “an optimal outcome for Genesis clients.”

“While we have made significant progress refining our business plans to remedy liquidity issues caused by the recent extraordinary challenges in our industry, including the default of Three Arrows Capital and the bankruptcy of FTX, an in-court restructuring presents the most effective avenue through which to preserve assets and create the best possible outcome for all Genesis stakeholders,” said Derar Islim, Genesis’ interim chief executive, in a statement on the company’s website.

According to its bankruptcy filing, Genesis’ lending unit said it had both assets and liabilities in the range of $1 billion to $10 billion and had over 100,000 creditors. The firm said it had about $150 million in cash on hand to support its operations during restructuring.

Genesis was the main partner of Gemini’s “earn” program, in which its retail investors received payments for allowing their crypto assets to be loaned out to others.

Cameron Winklevoss welcomed Genesis’ bankruptcy filing, saying it would provide Gemini a better venue for getting its clients’ money back.

“We will use every tool available to us in the bankruptcy court to maximize recovery for Earn users and any other parties within the bankruptcy court’s jurisdiction,” he wrote in a post on Twitter.

Both Genesis and Gemini were charged by the Securities and Exchange Commission last week with illegally selling securities to investors through the Earn program.

Genesis and its parent company, Digital Currency Group, had said they were seeking outside investment to help bolster the books and pay customers back in the months before filing for bankruptcy.

As part of its restructuring, Genesis said it would seek to possibly sell the company and also continue to look for additional investment.

I recently made a panic decision to withdraw all my money from one retirement account and I am now closing on a house in February (about $200,000). I am 36 years old, married and have a 1-year-old. Half of me is regretting it, and I’m worried about next year’s taxes due to the withdrawal and the 10% penalty I paid.

I have been saving up money with my family in order to buy our first home. Recently, however, interest rates have risen, making me worry that this window to get an affordable house was closing. In a fit of panic, I withdrew all of our $26,000 saved money from my 401(k), putting it in a high-yield savings account (3.75%). We have now chosen a home and will be using around $18,000 of this money for the down payment.

I am now worried that I might have to pay income taxes and a penalty for the withdrawal itself. I am extremely anxious over this situation as I feel I have destroyed our family’s financial future and that we cannot afford to pay taxes on the money I withdrew.

My main concern or question is, is there a way to tell the IRS that this money is being used toward a house? Retroactively?

The first thing you need to do: Take a breath. Most decisions should not be made in a panic, especially when involving money.

Because you withdrew from your 401(k), yes, you will have to pay taxes and a penalty. Had it been a loan, you’d have to pay interest on what you borrowed, but it would be to your own account. Keep in mind however that loans from your employer-based retirement plans are also risky – if you were to separate from your job, for whatever reason, you’d be responsible to pay it back or it would be treated as a distribution.

I understand your sense of urgency in wanting to buy a home during a more favorable market, but your time now should be spent on getting yourself financially situated and saving for the future.

“I wouldn’t advise this or done it this way, but he’s not stuck and it’s not detrimental – it’s just a tough lesson to learn,” said Jordan Benold, a certified financial planner at Benold Financial Planning.

Get very serious about your current finances and find a way to earmark a portion of your income to savings if at all possible. There are a few things you should be doing.

First, assess how much you will be paying in taxes and penalties. I’m not sure what your tax bracket is, but did this distribution push you into a higher tax bracket? You can use a calculator or talk to an accountant to see what that withdrawal will incur in taxes – then make sure you can pay it, or talk to the Internal Revenue Service about an extension. There are penalties for failing to file your taxes or pay them, and you don’t want to add that on top of your stress.

The IRS may not be able to do anything for you in terms of waiving those penalties – though it doesn’t hurt to ask, even if you have to wait on the phone for a while to talk to someone – but communication and attention to detail are key when it comes to your taxes. Getting an IRS agent on the phone and talking through your situation won’t be time wasted. There are so many rules, and an agent can help make sense of your options.

Once you get that sorted, look extremely carefully at whatever money you have coming in and what’s going out. You’re about to close on a home, and that costs money – not just the home itself, but all of the extras associated with closing. You may also need money for insurance, furniture, any repairs and so on if you haven’t factored that in yet, so fit that into your budget for when you sign the papers. Beyond that, list every expense you expect to have for the next 12 months – home insurance and taxes, a mortgage or utilities, groceries, medicine, any other nonnegotiable costs and add it all up. Don’t forget anything – ask your partner if there’s anything you may have forgotten.

Then compare it to your income. Are you under? Are you over? What changes can you make without totally draining your happiness? I always advocate for a balance…yes, in some cases you have to omit a few expenses for the time being when building up an emergency savings account or paying down debt, but don’t completely rob yourself of joy or all of your hard work may backfire. If you really need to buckle down, make a separate list of activities and entertainment you can get for free (or as close to free as possible)—walks in the park or on the beach with your partner and child, museums on free days, pot lucks and at-home movie nights with family and friends and so on.

Want more actionable tips for your retirement savings journey? Read MarketWatch’s “Retirement Hacks” column

Earmark a portion of your income to replenish your retirement savings before you try saving for any other goals. (This is separate from an emergency savings account, however – you should have one of those.) You may do that with payroll deductions in your 401(k), or also by allocating some of your savings to an IRA outside of the 401(k).

Take some time to learn the rules of your retirement plans. For example, an IRA allows an investor to take $10,000 out of the account penalty-free if it’s for a first-time home purchase (whereas a 401(k) does not have that exception). It may be too late for that, but there are other perks with various retirement accounts.

The 401(k) has a higher contribution limit and also comes with the possibility of employer matches (if your company offers it), whereas an IRA allows for penalty-free withdrawals for college. With a traditional IRA, you’d have to pay taxes on the withdrawal, whereas with a Roth IRA you’ve already paid the taxes and won’t have to pay any more for withdrawing from your contributions (you may have to pay taxes on the earnings portion, so follow distribution rules closely).

Remember – you don’t want to make distributions from your retirement savings for just anything. You can borrow money for a home or college, but you can’t borrow money for retirement, so it’s important to protect those accounts. Familiarize yourself with the pros and cons of all accounts so that you can maximize your savings and diversify your withdrawal options when you finally get to retirement.

So just buckle down, get yourself in order and think of the future. “He’s got plenty of time – 30 to 40 years to work,” Benold said. “This might be a distant memory that he hopes he can forget.”

Have a question about your own retirement savings? Email us at HelpMeRetire@marketwatch.com

Readers: Do you have suggestions for this reader? Add them in the comments below.

Many people are good at saving up money for retirement. They manage expenses and build up their nest eggs steadily. But when it comes time to begin drawing income from an investment portfolio, they might feel overwhelmed with so many choices.

Some income-seeking investors might want to dig deeply into individual bonds or dividend stocks. But others will want to keep things simple. One of the easiest ways to begin switching to an income focus is to use exchange-traded funds. Below are examples of income-oriented exchange-traded funds (ETFs) with related definitions further down.

First, the inverse relationship

Before looking at income-producing ETFs, there is one concept we will have to get out of the way — the relationship between interest rates and bond prices.

Stocks represent ownership units in companies. Bonds are debt instruments. A government, company or other entity borrows money from investors and issues bonds that mature on a certain date, when the issuer redeems them for the face amount. Most bonds issued in the U.S. have fixed interest rates and pay interest every six months.

Investors can sell their bonds to other investors at any time. But if interest rates in the market have changed, the market value of the bonds will move in the opposite direction. Last year, when interest rates rose, the value of bonds declined, so that their yields would match the interest rates of newly issued bonds of the same credit quality.

It was difficult to watch bond values decline last year, but investors who didn’t sell their bonds continued to receive their interest. The same could be said for stocks. The benchmark S&P 500 SPX, -0.20%

fell 19.4% during 2022, with 72% of its stocks declining. But few companies cut dividends, just as few companies defaulted on their bond payments.

One retired couple that I know saw their income-oriented brokerage account value decline by about 20% last year, but their investment income increased — not only did the dividend income continue to flow, they were able to invest a bit more because their income exceeded their expenses. They “bought more income.”

The longer the maturity of a bond, the greater its price volatility. Depending on the economic environment, you might find that a shorter-term bond portfolio offers a “sweet spot” factoring in price volatility and income.

And here’s a silver lining — if you are thinking of switching your portfolio to an income orientation now, the decline in bond prices means yields are much more attractive than they were a year ago. The same can be said for many stocks’ dividend yields.

Downside protection

What lies ahead for interest rates? With the Federal Reserve continuing its efforts to fight inflation, interest rates may continue to rise through 2023. This can put more pressure on bond and stock prices.

Ken Roberts, an investment adviser with Four Star Wealth Management in Reno, Nev., emphasizes the “downside protection” provided by dividend income in his discussions with clients.

“Diversification is the best risk-management tool there is,” he said during an interview. He also advised novice investors — even those seeking income rather than growth — to consider total returns, which combine the income and price appreciation over the long term.

An ETF that holds bonds is designed to provide income in a steady stream. Some pay dividends quarterly and some pay monthly. An ETF that holds dividend-paying stocks is also an income vehicle; it may pay dividends that are lower than bond-fund payouts and it will also take greater risk of stock-market price fluctuation. But investors taking this approach are hoping for higher total returns over the long term as the stock market rises.

“With an ETF, your funds are diversified. And when the market goes through periods of volatility, you continue to enjoy the income, even if your principal balance declines temporarily,” Roberts said.

If you sell your investments into a declining market, you know you will lose money — that is, you will sell for less than your investments were worth previously. If you are enjoying a stream of income from your portfolio, it might be easier for you to wait through a down market. If we look back over the past 20 calendar years — arbitrary periods — the S&P 500 increased during 15 of those years. But its average annual price increase was 9.1% and its average annual total return, with dividends reinvested, was 9.8%, according to FactSet.

In any given year, there can be tremendous price swings. For example, during 2020, the early phase of the Covid-19 pandemic pushed the S&P 500 down 31% through March 23, but the index ended the year with a 16% gain.

Two ETFs with broad approaches to dividend stocks

Invesco Head of Factor and Core Strategies Nick Kalivas believes investors should “explore higher-yielding stocks as a way to generate income and hedge against inflation.”

He cautioned during an interview that selecting a stock based only on a high dividend yield could place an investor in “a dividend trap.” That is, a high yield might indicate that professional investors in the stock market believe a company might be forced to cut its dividend. The stock price has probably already declined, to send the dividend yield down further. And if the company cuts the dividend, the shares will probably fall even further.

Here are two ways Invesco filters broad groups of stocks to those with higher yields and some degree of safety:

The Invesco S&P 500 High Dividend Low Volatility ETF SPHD, -0.33%

holds shares of 50 companies with high dividend yields that have also shown low price volatility over the previous 12 months. The portfolio is weighted toward the highest-yielding stocks that meet the criteria, with limits on exposure to individual stocks or sectors. It is reconstituted twice a year in January and July. Its 30-day SEC yield is 4.92%.

The Invesco High Yield Equity Dividend Achievers ETF PEY, -0.70%

follows a different screening approach for quality. It begins with the components of the Nasdaq Composite Index COMP, +1.39%,

then narrows the list to 50 companies that have raised dividend payouts for at least 10 consecutive years, whose stocks have the highest dividend yields. It excludes real-estate investment trusts and is weighted toward higher-yielding stocks meeting the criteria. Its 30-day yield is 4.08%.

The 30-day yields give you an idea of how much income to expect. Both of these ETFs pay monthly. Now see how they performed in 2022, compared with the S&P 500 and the Nasdaq, all with dividends reinvested:

Both ETFs had positive returns during 2022, when rising interest rates pressured the broad indexes.

8 more ETFs for income (and some for growth too)

A mutual fund is a pooling of many investors’ money to pursue a particular goal or set of goals. You can buy or sell shares of most mutual funds once a day, at the market close. An ETF can be bought or sold at any time during stock-market trading hours. ETFs can have lower expenses than mutual funds, especially ETFs that are passively managed to track indexes.

You should learn about the expenses before making a purchase. If you are working with an investment adviser, ask about fees — depending on the relationship between the adviser and a fund manager, you might get a discount on combined fees. You should also discuss volatility risk with your adviser, to establish a comfort level and to try to match your income investment choices to your risk tolerance.

Here are eight more ETFs designed to provide income or a combination of income and growth:

Company

Ticker

30-day SEC yield

Concentration

2022 total return

iShares iBoxx $ Investment Grade Corporate Bond ETF

The following definitions can help you gain a better understanding of how the ETFs listed above work:

30-day SEC yield — A standardized calculation that factors in a fund’s income and expenses. For most funds, this yield gives a good indication of how much income a new investor can be expected to receive on an annualized basis. But the 30-day yields don’t always tell the whole story. For example, a covered-call ETF with a low 30-day yield may be making regular dividend distributions (quarterly or monthly) that are considerably higher, since the 30-day yield can exclude covered-call option income. See the issuer’s website for more information about any ETF that may be of interest.

Taxable-equivalent yield — A taxable yield that would compare with interest earned from municipal bonds that are exempt from federal income taxes. Leaving state or local income taxes aside, you can calculate the taxable-equivalent yield by dividing your tax exempt yield by 1 less your highest graduated federal income tax bracket.

Bond ratings — Grades for credit risk, as determined by ratings agencies. Bonds are generally considered Investment-grade if they are rated BBB- or higher by Standard & Poor’s and Fitch, and Baa3 or higher by Moody’s. Fidelity breaks down the credit agencies’ ratings hierarchy. Bonds with below-investment-grade ratings have higher risk of default and higher interest rates than investment-grade bonds. They are known as high-yield or “junk” bonds.

Call option — A contract that allows an investor to buy a security at a particular price (called the strike price) until the option expires. A put option is the opposite, allowing the purchaser to sell a security at a specified price until the option expires.

Covered call option — A call option an investor writes when they already own a security. The strategy is used by stock investors to increase income and provide some downside protection.

Preferred stock — A stock issued with a stated dividend yield. This type of stock has preference in the event a company is liquidated. Unlike common shareholders, preferred shareholders don’t have voting rights.

These articles dig deeper into the types of securities mentioned above and related definitions:

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

Nearly two years after biotechnology stocks began to tumble, executives at small and midsize companies in the space are finally accepting that share prices aren’t bouncing back anytime soon.

With reality setting in, it’s a buyer’s market for companies looking for acquisitions and partnerships, according to many of the pharmaceutical and medical technology executives who gathered at this year’s

J.P. Morgan

healthcare investor conference, which wrapped up in San Francisco on Thursday.

Pour one out for the beleaguered economists, who for once got an important indicator, the consumer price index, right on the nose, after CPI fell 0.1% in December, while core prices rose 0.3%.

“The 2021 surge in durable goods demand normalized, and the resulting collapse in durable goods price inflation was stunningly fast,” says Paul Donovan, chief economist of UBS Global Wealth Management.

“The commodity wave of inflation is fading, and that leaves the profit margin expansion in focus,” he adds. What a good time for earnings season to be upon us, and what do you know, it is, kicking off with the banking sector on Friday before broadening out next week.

Strategists at Goldman Sachs have a new note out, saying that the market is pricing in a soft landing even though the trend of earnings revisions points to a hard landing.

They’re not that optimistic — even in the soft-landing scenario, the team led by David Kostin say the S&P 500 SPX, +0.40%

will end the year right around current levels, at 4,000. But they identify 46 stocks that could benefit — profitable, cyclical companies that are trading at price-to-earnings valuations below their 10-year median, among other factors.

One name jumps out: Tesla TSLA, -0.94%,

which trades at 22 times forward earnings versus the 10-year median of 117 times. But the other 45 names are less flashy, ranging from Capital One COF, +1.81%

and Carlyle Group CG, +0.54%,

to a host of industrials including 3M MMM, +0.12%,

Parker-Hannifan PH, +0.73%

and Otis Worldwide OTIS, +0.42%.

As a whole, these typically $10 billion companies are trading at 12 times earnings, versus 17 times usually.

In the hard landing scenario, S&P 500 profit margins would shrink by 125 basis points, to 10.9% — about in line with the median peak-to-trough decline during the eight recessions since 1970, which has been 132 basis points. Consensus expectations are for a 26 basis-point margin decline.

The Goldman team also have a 36 stock screen for a hard landing — profitable companies in defensive industries with a positive dividend yield. They’re typically food, beverage and tobacco companies as well as software and services companies — including Costco Wholesale COST, +0.58%,

Kroger KR, -0.99%,

Altria MO, +0.48%,

Tyson Foods TSN, +0.23%,

Microsoft MSFT, +0.30%,

MasterCard MA, -1.13%

and Visa V, -0.25%.

As a whole, these $37 billion companies are trading at 22 times earnings vs. a historical 24 times.

The market

After a 2.3% advance for the S&P 500 SPX, +0.40%

over the last three sessions, U.S. stock futures ES00, +0.39%

JPMorgan shares slumped after forecast-beating earnings, though investment bank revenue came in light of estimates. Delta shares also declined after topping earnings estimates.

Virgin Galactic SPCE, +12.34%

surged after saying it’s on track to launch space-tourism flights in the second quarter.

Apple AAPL, +1.01%

says CEO Tim Cook requested, and received, a pay cut after investor criticism.

The University of Michigan’s consumer-sentiment index is due at 10 a.m. Eastern, and Minneapolis Fed President Neel Kashkari and Philadelphia Fed President Patrick Harker are due to speak.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Katie St. Ores has a 100% track record of getting her tax clients out of paying the steep penalty for missing a required minimum distribution from their retirement funds. That amounts to only two households getting forgiveness, but it represents a lot of dollars, because the fee for any sort of mistake with RMDs is 50% of what’s missing, which could be tens of thousands of dollars.

Now’s the time to make things right if you forgot to make your RMD payment by Dec. 31 for 2022, paid the wrong amount or realized you got it wrong in a past year. The faster you correct it, the more likely the IRS is likely to waive the fines — and your chances are good overall, despite the agency’s stern reputation.

Beware, though, that new rules are going into effect in 2023 that could make the IRS less accommodating. For one thing, the age to start RMDs is going to 73 this year, and then 75 in 2033, which means the government is going to be hungry for the missing revenue. Even more important, the penalty will be reduced to 25% — or 10% if you’re really quick about reporting it.

The IRS doesn’t publicly track how many people miss or make mistakes with their RMDs, but financial advisers and tax professionals say it happens often enough, and they consider the IRS to be quite liberal about granting waivers.

St. Ores, who is a financial adviser and tax preparer based in McMinnville, Ore., thinks the IRS has responded generously so far because they know the rules are complex and mistakes happen.

“They know people are getting up there in age, and so they’ve probably said up to now, let’s just grant it,” says St. Ores.

But the new penalties seem worded to avoid waivers in the future, especially because of the extra reduction to 10% if you act to quickly correct mistakes. Up to now, the IRS has taken pains to point out how to ask for a forgiveness on its website, but now there will be new emphasis on the lower penalties.

“The 50% penalty effectively ‘scared’ taxpayers to withdraw RMDs, so reducing the penalty could reduce the fear of additional tax, leading to more taxpayers missing their RMDs,” says St. Ores. “Between more taxpayers that potentially neglect to take their RMDs because of a not-as-high penalty and confusion over the current required age, the IRS will probably collect more taxes overall.”

What to do about past mistakes

There are a lot of different ways to mess up your required minimum distributions. The amount you’re supposed to pay is calculated according to a formula that takes your account balance of all your qualified tax-deferred accounts and multiplies it by a factor related to your age.

When you get started taking the money out, it works out generally to about 4% of the account value. You keep taking RMDs every year from your designated start time until the accounts are empty (or you die). The beginning age in the past was 70½, then it moved to 72, and now it’s changing to 73.

“These things can get complicated,” says Isaac Bradley, director of financial planning at Homrich Berg, an investment firm based in Atlanta. He advised one couple that accidentally took the distribution from the wrong spouse.

Another easy mistake is taking the wrong amount because of a math error. Sometimes, the problem is just about communication, because people tend to have multiple 401(k)s at old employers or several rollover IRAs that aren’t consolidated. The adviser helping make the calculations might not know of an account held at a different custodian, and that could throw off the whole equation.

David Haas, a financial adviser and president of Cereus Financial Advisors, based in Franklin Lakes, N.J., has had to help family members correct RMDs, mostly having to do with inherited IRA accounts.

“You’re supposed to take RMD for the person who died, if they didn’t already take it,” he says, but a lot of people miss those in the confusion of grief.

Then once you inherit the account, you have to take RMDs over a 10 year period to empty the account.

“With one relative, she just kept on missing it and that was her fault. She didn’t realize what she was supposed to do. People don’t know the law, and it’s very confusing,” Haas says.

The first step is realizing you made a mistake, and then once you know that, pay the amount that’s missing. You need to file a special form with the IRS for the tax year in question (Form 5329), which you can send in at any point — you don’t have to wait until you file your next tax return.

If you want to ask for a waiver, you need to attach a letter explaining the mistake. If your request is not granted, then you pay the penalty.

While the process isn’t excessively complicated, you might want to consult with a tax professional to make sure you’re not making more mistakes in calculating the amount that’s missing. It could turn out to be a lot of paperwork if you have missed multiple years.

Kenneth Waltzer, a financial planner based in Los Angeles, had a client who did not realize he had inherited an IRA and missed the RMDs on it for five years. “He ignored emails about it,” says Waltzer. “When he came to us, it added up to over $100,000.”

For Katie St. Ores, the message going forward is going to be: Get it right the first time. Forgiveness may not be so easy to come by in the future. “I’m trying to stay on top of my clients taking their RMDs on time,” she says.

U.S. securities regulators on Thursday charged Genesis Global Capital and crypto exchange Gemini Trust Co. with offering and selling of unregistered securities to retail investors, bypassing disclosures and other requirements aimed at protecting market participants.

Genesis and Gemini raised billions of dollars’ worth of crypto assets from hundreds of thousands of investors through unregistered offers, using a crypto asset-lending program called Gemini Earn, the Securities and Exchange Commission said.

The complaint seeks the return of any “ill-gotten gains” plus interest, and any civil penalties, the SEC said.

The SEC is also investigating whether other securities-law violations were committed and whether there are other companies or people relating to the alleged misconduct.

The Winklevoss twins were early champions of cryptocurrencies, using the money and fame they won in legal wrangling with Facebook parent Meta Platforms Inc. META, +2.87%

and Meta’s founder Mark Zuckerberg over their role in creating the social-media giant to launch Gemini.

According to the SEC complaint, the Gemini Earn agreement between Genesis, part of a subsidiary of Digital Currency Group, and Gemini started in December 2020.

Gemini customers, including U.S. retail investors, were to have an opportunity to loan their crypto assets to Genesis in exchange for Genesis’ promise to pay a high interest rate.

Gemini deducted agent fees that were as high as 4.29%, the SEC alleges.

“Genesis then exercised its discretion in how to use investors’ crypto assets to generate revenue and pay interest to Gemini Earn investors,” the SEC said.

By November, however, Genesis announced it would not allow the Gemini Earn investors to withdraw their crypto assets because of a liquidity crunch following volatility in the crypto market after FTX’s bankruptcy filing, the SEC said.

At the time, Genesis held about $900 million in investor assets from 340,000 Gemini Earn investors, the SEC said. Gemini ended the Gemini Earn program earlier this month.

“As of today, the Gemini Earn retail investors have still not been able to withdraw their crypto assets,” the SEC said in a statement.

“We allege that Genesis and Gemini offered unregistered securities to the public, bypassing disclosure requirements designed to protect investors,” SEC Chair Gary Gensler said in a statement.

The charges “build on previous actions to make clear to the marketplace and the investing public that crypto-lending platforms and other intermediaries need to comply with our time-tested securities laws,” Gensler said.

The SEC’s complaint was filed in the U.S. District Court for the Southern District of New York.

A mild stock market rally to kick off the new year will be put to the test Thursday when investors face a highly-awaited U.S. inflation reading which could well help determine the size of the Federal Reserve’s next interest-rate increase.

The December CPI reading from the Bureau of Labor Statistics, which tracks changes in the prices paid by consumers for goods and services, is expected to show a 6.5% rise from a year earlier, slowing from a 7.1% year-over-year rise seen in the previous month, according to a survey of economists by Dow Jones. The core price measure that strips out volatile food and fuel costs, is expected to rise 0.3% from November, or 5.7% year over year.

The December CPI will be particularly important for influencing the Fed’s decision in its upcoming meeting which concludes February 1, said economists at Pimco. They expect the inflation and labor market data will have moderated sufficiently will push the central bank to pause rate hikes before their May meeting.

“After hiking 50 basis points at the December meeting, we expect the Fed moves to a 25bp hiking pace in early February, and ultimately pause around 5%,” wrote Pimco’s economists Tiffany Wilding and Allison Boxer, in a Tuesday note.

However, since the Fed’s December meeting, officials have relentlessly signaled the central bank will need to raise interest rates above 5% in order to get inflation to the 2% target, with no interest rate cuts expected this year. Fed funds futures traders now see a 78% likelihood of a 25 basis point hike at its February meeting, and a 68% chance of another in March, which would bring the terminal rate to merely 4.75-5% by mid-year, according to the CME FedWatch tool.

“Inflation swaps currently see inflation falling below 2.5% by the summer of 2023, which seems hopeful,” Kramer said. “This week’s CPI reading will be essential in maintaining that view and could prove disastrous if CPI comes in hotter than expected, veering market-based inflation expectations off course.”

The stock market is looking for an “around 5%” increase in December’s core inflation, said Rhys Williams, chief strategist at Spouting Rock Asset Management. “If you get a number in the low four [percent], the stock-market rally will continue. The market is very hyper-focused on data points.”

U.S. stocks had a positive start to 2023 with hopes that cooling inflation and a potential recession may persuade the central bank to ease off the pace at which it is raising its policy interest rate.

Williams thinks inflation is coming down but it will not hit the central bank’s 2% mark by summer 2023.

“I think at some point the markets will realize, ‘oh we can’t get to 2%,” and then the markets probably do sell off on that. I think maybe in short term [the stocks go] up and then in the second quarter, they go back down as people realize that 2% is not realistic,” Williams told MarketWatch via phone.

U.S. stocks opened higher on Wednesday, building on their gains from the prior session ahead of Thursday’s closely watched inflation report. The S&P 500 SPX, +1.28%

gained 15 points, or 0.4%, to 3,935. The Dow Jones Industrial Average DJIA, +0.80%

rose by 124 points, or 0.4%, to 33,828. The Nasdaq Composite COMP, +1.76%

gained 34 points, or 0.3%, to 10,777.

Trouble may be brewing in the second half of this year, but there’s a window for a stock-market rally during the first six months of 2023, in the view of Stifel chief equity strategist Barry Bannister.

The potential for a rally in equities is based on his expectations for inflation to fall sharply, for the Federal Reserve to pause interest-rate hikes in the second quarter, and for no official recession, as declared by the National Bureau of Economic Research, before midyear, according to a Jan. 9 note from Bannister.

All of that should add up to a lower real yield on the 10-year U.S. Treasury note TMUBMUSD10Y, 3.594%

and to the S&P 500 rising to 4,300 by the end of June, according to the note.

“2023 may be a year of 2 halves, with the S&P 500 peaking mid-2023,” wrote Bannister. “The S&P 500 in late 2023 may give back some or all of 2023 gains.”

During the first half of the year, the equities rally will probably be led by “cyclical growth” and “cyclical value” stocks as hot inflation cools, Bannister wrote. He sees economic risk for equities likely rising again in late 2023, when a recession for U.S. industrial production may already be “locked in” after “long and variable lags” to the Fed’s aggressive rate hikes aimed at bringing down inflation.

Stifel’s earnings-per-share forecast for the S&P 500 features a “major” slowdown in the second half of the year, Bannister said in the note. “Additionally, inflation may turn back up late-2023, causing the Fed to re-tighten financial conditions.”

The downside risk for the S&P 500 may be 3,300, according to Bannister.

STIFEL NOTE DATED JAN. 9, 2023

While Bannister does not yet see a recession in earnings per share, or EPS, for the S&P 500 in the first half of 2023, he cautioned that in the second of the year, the benchmark may face a slowdown in EPS that’s similar to 2012 or 2015-2016.

The S&P 500 closed at around 3,919 on Tuesday, as the U.S. stock market climbed after initially struggling for direction following Fed Chair Jerome Powell’s speech in Sweden.

The S&P 500 SPX, +0.70%

finished 0.7% higher Tuesday, while the Dow Jones Industrial Average DJIA, +0.56%

gained 0.6% and the technology-laden Nasdaq Composite rose 1%, according to FactSet data.

Investors have been anxious about a potential recession in 2023, fearing that the Fed’s rapid pace of rate hikes in 2022 and continued monetary tightening this year could lead to a hard landing for the U.S. economy.

“The Fed drives this bus,” said Bannister. “Real yields were repressed 2000-2020 amid crises, and if hastily normalized, stocks could fall further.”

The U.S. stock market is up so far this year after tumbling in 2022 as the Fed raised its benchmark rate to battle the highest inflation in four decades. The S&P 500 has edged up 2.1% this month based on Tuesday’s close, following a 19.4% drop in 2022 for the index’s worst year since 2008, FactSet data show.

Meanwhile, Stifel has forecast that headline readings from the U.S. consumer-price index (CPI) will fall to 3.5% on a year-over-basis by the end of the third quarter, Bannister’s note said. Headline inflation ran as high as 9.1% in the 12 months through June, falling to 7.1% in November.

The next CPI reading, scheduled for Thursday, will provide details on U.S. inflation data for December.

It took 16 months for inflation to rise to last year’s June peak on a year-over-year basis, according to Bannister, who said Stifel’s measures point to it taking around 16 months to fall to 3.5%.

“Major inflation bursts are symmetrical,” meaning that “up” equals “down,” he said. “Every leading indicator of inflation sub-components now points down.”

It may not have been a surprise to see the consumer discretionary sector of the S&P 500 get hammered last year amid talk of a looming recession while the Federal Reserve jacked up interest rates to push back against inflation.

But the stock market always looks ahead. Following a decline of 19.4% for the S&P 500 SPX, +0.42%

in 2022 and a 37.6% drop for the benchmark index’s consumer discretionary sector, this may be the time to begin looking for bargains.

And now, analysts at Jefferies have lifted the sector to a “bullish” rating.

In a note to clients on Jan. 10, Jefferies’ global equity strategist, Sean Darby, wrote: “A Goldilocks scenario might be unfolding for the U.S. consumer — falling inflation but steady employment conditions.”

He sees consumer confidence improving, in part because “households are still sitting on [about] $1.4 trillion of Covid savings.”

Darby pointed to a list of 18 consumer discretionary stocks favored by Jefferies analysts that was published on Jan. 6. Those are listed below, along with three stocks in the sector the analysts rate “underperform.”

The ratings of the Jefferies analysts for individual stocks is based on their 12-month outlooks for the companies, in keeping with Wall Street tradition.

So we have added another list further down, showing which companies in the S&P 500 consumer discretionary sector are expected by analysts polled by FactSet to increase sales the most through 2024.

The Jefferies 18

Here are the 18 consumer discretionary stocks recommended by Jefferies analysts with “buy” ratings on Jan. 6, sorted by how much upside the firm sees for the shares from closing prices on Jan. 9:

Click on the tickers for more information about the companies.

Click here for Tomi Kilgore’s detailed guide to the wealth of information available for free on the MarketWatch quote page.

The two right-most columns on the table show estimated compound annual growth rates (CAGR) for the companies over the past three calendar years and expected sales CAGR for two years through calendar 2024, based on the companies’ financial reports and consensus estimates among analysts polled by FactSet.

(We used calendar-year numbers, some of which are estimated by FactSet for prior years, because some companies have fiscal years or even months that don’t match the calendar.)

The stock pick with the highest 12-month upside potential, based on Jefferies’ price target, is Topgolf Callaway Brands Corp. MODG, -0.22%.

This company has the highest estimated three-year sales CAGR on the list, and has the third-highest projected sales CAGR through 2024, after Planet Fitness Inc. PLNT, +0.69%

and Chewy Inc. CHWY, +1.63%.

On Jan. 6, the Jefferies analysts also listed three stocks in the sector they rated “underperform.” Here they are, sorted by how much the analysts expect the stocks to decline over the next 12 months:

A look head at which companies are expected to increase sales the most over the next two years might serve as a good starting point for your own research.

Bear in mind that some of the companies in travel-related industries suffered declining sales for three years through 2022 because of the coronavirus pandemic. Some of those are on this new list of 20 stocks in the S&P 500 consumer discretionary sector expected to show the highest two-year sales CAGR through calendar 2024:

Among the companies on this list that didn’t suffer sales declines from 2019 levels, Tesla Inc. TSLA, -1.83%

is expected to achieve the highest two-year sales CAGR through 2022.

Dollar General Corp. DG, -0.26%

is the only company to appear on this list based on consensus sales growth estimates and the Jefferies recommended list.