AI is everywhere these days—and that means so is AI risk.

Among S&P 500 companies, 72% mentioned AI as a material risk on their Form 10-Ks this year, the Conference Board found, up from 58% last year and 12% in 2023. The shift is reflective of how AI use within business has matured from the experimental to the widespread, the organization wrote in a report. (The Conference Board’s report defines “AI” broadly, including not only LLMs but also robotics, automation, machine learning, and other types of AI.)

The companies most likely to disclose AI risk were those in “frontline adopter” industries, such as the finance, healthcare, industrial, IT, and consumer discretionary sectors.

S&P companies were most concerned about the reputational risks of AI, the Conference Board reported; 38% of them disclosed potential reputational threats from AI on their 10-Ks. Forty-five companies mentioned “implementation and adoption” risks, such as overpromising on AI projects or AI not meeting expectations, while 42 stated that consumer-facing AI was a risk. Other reputational risks companies mentioned included privacy and data risks, hallucinations, competitive threats, and issues with bias and fairness.

One in five S&P companies mentioned AI-related threats to cybersecurity as a risk on annual filings. While 40 companies simply stated that cybersecurity in general was a risk, 18 called out third party or vendor risks, and 17 said data breaches were a risk.

Companies also foresaw potential compliance risks from AI. Forty-one listed “evolving regulation and uncertainty” as a risk area, and some specifically referred to the EU AI Act, which has steep penalties for noncompliance.

Fortune Global Forum returns Oct. 26–27, 2025 in Riyadh. CEOs and global leaders will gather for a dynamic, invitation-only event shaping the future of business. Apply for an invitation.

Benzinga and Yahoo Finance LLC may earn commission or revenue on some items through the links below.

A slew of cryptocurrency exchange-traded funds may be set to launch any day now, according to Bloomberg Intelligence Senior ETF Analyst Eric Balchunas.

Balchunas said Monday on X that the approval of pending ETF applications tied to assets such as Cardano, Litecoin, Solana, and XRP was now “100%” guaranteed following the Securities and Exchange Commission’s launch of generic listing standards for cryptocurrency-based ETFs.

Balchunas’ remarks came after the SEC requested that issuers withdraw 19b-4 filings related to their ETF applications.

Don’t Miss:

The 19b-4 is a filing submitted by exchanges, such as the Nasdaq and NYSE, on behalf of issuers outlining a rule change required to list a new ETF. The filing has typically been required for spot cryptocurrency ETF approvals, but it also came with a statutory approval window of 240 days.

According to Balchunas, 19b-4 filings and the “clock” that came with them are no longer necessary for spot cryptocurrency ETF applications thanks to the new generic listing standards. Now only S-1 registration filings are required, he said. S-1 filings submitted by issuers do not come with such deadlines.

“The baby could come any day,” Balchunas said. “Be ready.”

Before the recent shift in the cryptocurrency ETF applications process, the deadline for an SEC decision on ETF applications tied to Litecoin, Solana, and XRP was already concentrated in October.

Of all the pending spot cryptocurrency ETF applications, Balchunas suggested on Monday that Solana-linked products may be the first to be approved. He highlighted that registration statements linked to the products have already undergone four amendments, which typically signals high SEC engagement and progress.

Bitwise investment chief Matt Hougansaid last month that the launch of Solana ETFs would usher in “Solana season.” He cited a convergence of inflows into the products and demand from digital asset treasury companies that are stacking the asset. He said the combination was what sparked Bitcoin’s run from $40,000 in January 2024 to a record of nearly $125,000. He also said it is what has caused Ethereum to rally since April.

The chairman of the Securities and Exchange Commission is weighing a major rule change for public companies. This week, on social media, President Trump said companies should not report earnings quarterly, but instead, just twice a year. SEC Chairman Paul Atkins told CNBC that he welcomes that idea. Wall Street Journal financial reporter Corrie Driebusch joins CBS News to discuss.

President Donald Trump wants corporations to “no longer be forced” to report earnings every quarter.

In a Truth Social post on Monday, he said companies should instead only be required to post earnings every six months, pending the U.S. Securities and Exchange Commission’s approval. This change would break a quarterly reporting mandate that’s been in place since 1970.

“This will save money, and allow managers to focus on properly running their companies,” Trump wrote.

Trump added that China has a “50 to 100 year view on management of a company,” as opposed to U.S. companies required to report four times in a fiscal year. China’s Hong Kong Stock Exchange (HKEX) allows companies to submit voluntary quarterly financial disclosures, but only requires them to report their financial results twice a year.

During his first term, Trump publicly asked the SEC on X, then still known as Twitter, to study shifting company disclosures from a quarterly to semiannual basis, stating business leaders felt less frequent reporting would allow for greater flexibility and long-term planning.

He told reporters at the time that he got the idea from CEOs.

“It made sense to me because, you know, we are not thinking far enough out,” Trump said in 2018. “We’ve been accused of that for a long time, this country. So we’re looking at that very, very seriously.”

No change came from the SEC.

A revived debate

“President Trump has revived an old idea emphasizing the costs of quarterly filings, the distraction from long-term goals, and how they reinforce Wall Street’s obsession with beating short-term expectations,” Usha Haley, a professor at the Barton School of Business at Wichita State University, told Fortune.

For his part, SEC Chair Paul Atkins has explicitly called for more transparency as he’s taken control of the regulatory body this year.

But companies keep pushing back. Last week, the San Francisco-based Long Term Stock Exchange said it planned to petition the SEC to end its quarterly reporting requirement. The exchange lists companies focused on long-term goals.

Critics of the move argue that it might reduce transparency for investors.

Chad Cummings, a CPA and attorney at Cummings & Cummings Law, told Fortune semiannual reporting enables companies to hide “red flags” like deteriorating cash flows or abrupt changes in auditor language, which can lead to unsavory practices like concealment of liquidity crises, accounting fraud, and whistleblower retaliation.

“Removal of quarterly earnings sabotages valuation models and tilts power to insiders,” Cummings, who has active bar admissions in the U.S. Tax and Bankruptcy courts, added.

SEC approval would face internal resistance, statutory barriers, and potential litigation, as the SEC’s investor protection mandate requires “reasonably current” disclosure, Cummings said.

If regulators stopped requiring companies to report earnings every quarter without having clear legal authority, the decision could be challenged in court under the Administrative Procedure Act, a federal law that governs how U.S. administrative agencies create regulations, he warned.

Meanwhile, Haley also said Trump’s nod to China’s financial disclosure mandates misses the point.

“The United States is not China,” she said. “Our markets derive their strength and global dominance through transparency, investor protections, and a long tradition of disclosures… Weakening those guardrails, while invoking efficiency risks, undermines investors’ confidence, the foundation of U.S. capital markets, which China does not have.”

Fortune Global Forum returns Oct. 26–27, 2025 in Riyadh. CEOs and global leaders will gather for a dynamic, invitation-only event shaping the future of business. Apply for an invitation.

The conservative network Newsmax will pay $67 million to settle a lawsuit accusing it of defaming a Denver-based voting equipment company by spreading lies about President Donald Trump’s 2020 election loss, according to documents filed Monday.

The settlement comes after Fox News Channel paid $787.5 million to settle a similar lawsuit in 2023 and Newsmax paid what court papers describe as $40 million to settle a libel lawsuit from a different voting machine manufacturer, Smartmatic, which also was a target of pro-Trump conspiracy theories on the network.

Delaware Superior Court Judge Eric Davis ruled earlier that Newsmax did indeed defame Denver-based Dominion Voting Systems by airing false information about the company and its equipment.

But Davis left it to a jury to eventually decide whether that was done with malice, and, if so, how much Dominion deserved from Newsmax in damages. Newsmax and Dominion reached the settlement before the trial could take place.

The settlement was disclosed by Newsmax on Monday in a new filing with the U.S. Securities and Exchange Commission. It said the deal was reached Friday.

The disclosure came as Trump vowed in a social media post Monday to eliminate mail-in ballots and voting machines such as those supplied by Dominion and other companies. It was unclear how the Republican president could achieve that.

The past week hasn’t been the kindest to the electric vehicle industry. Now, it’s capped off with news that the EV startup Fisker is the subject of an investigation from the US Securities and Exchange Commission (SEC).

reported that SEC officials sent several subpoenas to Fisker. The filing doesn’t specifically say what the subpoenas are asking for or looking into but it’s clear that the SEC has launched an investigation into the floundering EV maker that .

Fisker has been struggling to keep its head above water ever since last year’s disastrous rollout of its Ocean SUV that failed to score more than a few thousands sellers even though it produced well over 10,000 units. Following its Q4 earnings report last year that saw a gross margin loss of 35 percent, the car maker announced it would lay off 15 percent of its workforce the following March as it shifted to a direct-to-consumer sales strategy.

A Fisker spokesperson declined to comment on the matter to TechCrunch saying they could not “comment on the existence or nonexistence of a possible investigation.”

Fisker isn’t the only EV maker to suffer a noticeable setback. Tesla saw a major stumble with .

America’s smallest banks face potentially destructive losses from climate-related weather disasters, according to a first-of-its-kind report from a climate change nonprofit. And they’re not even aware of the risk.

Property damage from floods, wind, storm surges, hail, or wildfires threatens a collective $2.4 billion across nearly 200 national banks, averaging 1.5% of these banks’ total portfolio value, according to First Street. Most of this risk is concentrated amid small regional or community banks. In fact, nearly one in three regional banks face significant climate risk. But large institutions aren’t immune, with one in four facing such risks too, the report found.

“Risk exposure varies, but no matter the size of the institution, all banks had some level of climate risk within their lending footprint,” Jeremy Porter, First Street’s head of climate implications, told Fortune. “The most vulnerable were regional, small, and community banks with highly concentrated portfolios in areas prone to flooding, wildfires, or hurricanes. However, even some of the larger banks faced significant enough risk to merit further scrutiny.”

First Street conducted its analysis by looking at extreme weather risks in banks’ physical locations and using it as a proxy for the commercial and residential properties on which banks have issued loans.

Nearly one-third of the nation’s banks are exposed to climate-related risks that could reduce the value of their holdings by 1%, a threshold the Securities and Exchange Commission has defined as material.

“If you have any line item, as a publicly traded company, with the potential to lose 1% of value… you have to report it,” First Street CEO Matthew Eby said. “On average, every single one of these small banks and community banks hold so much risk, they [would] all have to report it.”

Why banks don’t know

The SEC’s 1% rule is currently on hold while it faces legal challenges—but regardless, it and other financial reporting requirements exempt small banks. Experts say many of these institutions likely don’t know just how risky their portfolios are. And the ballooning costs of weather-related disasters, which are expected to rise dramatically as climate change worsens, show why it’s critical to understand such risks. Since the 1980s, floods, wildfires, hurricanes, and other weather disasters have caused an ever-rising amount of financial damage, much of it in areas previously immune to weather disasters.

Hurricane Debby, which pummeled Florida and the Carolinas last month before moving up the East Coast, caused an estimated $1.4 billion of property losses in the U.S. and over $2 billion in Canada, according to estimates. (It was the costliest event in the history of Quebec, Reinsurance News noted.) But an analysis by First Street found that nearly 8 in 10 of the damage was outside of historical FEMA flood zones, meaning the affected properties were unlikely to have flood insurance, and their owners less able to weather a catastrophic financial loss.

Repeated across hundreds or thousands of properties, such financial losses could spell disaster for small banks that have outstanding loans concentrated in a specific area. One bank flagged as high-risk by First Street has most of its branches across coastal New England, a region that has seen devastating back-to-back floods for the past two years and where climate change is expected to exacerbate extreme weather.

“If you lost, after insurance, 14 or 15% of your residential real estate portfolio or commercial real estate portfolio, there’s no way you have the reserves to withstand that, so you’re talking about potential bank failure,” Eby said.

He added, “financial institutions are really the big concern, because if they fail in financial crises, that impacts everyone else, as opposed to just a company failing by itself.”

Unknown unknowns

While climate risk is a growing concern for banks of all sizes, the smallest institutions are least able to establish and price that risk, said Clifford Rossi, a former Citigroup risk officer who now directs the Smith Enterprise Risk Consortium at the University of Maryland.

“So many other things are affecting small banks—they’re dealing with competitive pressure from the big guys that affect economies of scale, they’re fixated on how they’re managing their assets, interest rates are declining… those things are top of mind,” he said.

Rossi questioned First Street’s methodology and cautioned against putting numerical estimates on bank losses based on branch locations, saying they could provide wildly varying figures.

“There’s certainly a degree of risk in those portfolios, but we don’t know how much,” he said.

Every bank should do a loan-level analysis of their portfolio by putting data on addresses, longitude, latitude, and commercial real estate into a climate model to assess the physical risk, he added.

When it comes to estimates, he warned, “We need to be careful about saying the sky is falling when we still don’t have the best analysis in town.”

But that kind of analysis is time-consuming and difficult, even for the largest institutions. The Federal Reserve this spring published the results of a test to determine how aware America’s six largest banks—Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley, and Wells Fargo—were of their climate risks.

The answer: Not very.

According to the banks, they didn’t have reliable information on the types of buildings they held, their insurance coverage, weather exposure, or climate-modeling data.

The new analysis “underscores the need for all banks, financial institutions, and asset owners to proactively incorporate climate risk into their broader risk management frameworks,” First Street’s Porter said.

“Climate risk is present in these portfolios—and it’s measurable. The Federal Reserve, the SEC, and other regulatory bodies are already acknowledging this risk through stress tests, and it’s only a matter of time before mandatory reporting becomes standard practice.”

Starbucks North America CEO Michael Conway Quits After Just 6 Months In The Position

In a surprising move, Michael Conway, Starbucks (NASDAQ:SBUX) North America CEO, has resigned after only six months in the role.

What Happened: Conway, who took on the position in April, informed the company of his decision last week, as per a Securities and Exchange Commission filing. He will remain with the company until November 30 to assist with the leadership transition, concluding his 11-year tenure at Starbucks, Business Insider reported on Tuesday.

Don’t Miss:

Before his North American CEO role, Conway served as group president of international and channel development and president of Starbucks Canada. His appointment was part of a reorganization effort by former CEO Laxman Narasimhan, Bloomberg noted in March.

Rather than appointing a new CEO for North America, Starbucks announced that Sara Trilling, the company’s North American president, will oversee retail operations across the region. Trilling has been with Starbucks for 22 years and previously managed 3,500 stores as senior vice president of its north division.

The company aims to enhance decision-making efficiency by streamlining its leadership structure, The Wall Street Journal reported. Conway’s departure follows other significant leadership changes, including the recent appointment of Brian Niccol, former CEO of Chipotle, as Starbucks’ new top executive.

Operational challenges have affected Starbucks’ North American stores, with complex drink orders, rising prices, and varying foot traffic impacting staff and profitability. Niccol plans to revamp operations and focus on customer experience, he stated last week.

Why It Matters: This leadership change comes amid a series of strategic shifts at Starbucks. In March, the company announced a new geographic leadership structure to support global functions, appointing Conway as North America CEO to spearhead this initiative.

In August, the appointment of Brian Niccol as the new CEO boosted Starbucks’ valuation by over $15 billion in just one day. Niccol, known for his successful tenure at Chipotle, aims to steer Starbucks through its current challenges and enhance customer experience.

On his second day as CEO, Niccol outlined his vision to reconnect Starbucks with its community coffeehouse roots. He emphasized the need for comfortable seating and a clear distinction between “to-go” and “for-here” services to improve the in-store experience.

Read Next:

Image by Şahin Sezer Dinçer from Pixabay.

Up Next: Transform your trading with Benzinga Edge’s one-of-a-kind market trade ideas and tools. Click now to access unique insights that can set you ahead in today’s competitive market.

Ken Leech, the longtime Western Asset Management chief investment officer, left that role amid probes from the Justice Department and Securities and Exchange Commission into whether some clients were favored over others in allocating gains and losses from derivatives trades.

Leech, who manages some of the largest bond strategies in the US, will take an immediate leave of absence after receiving a Wells notice from the SEC, the company said in a filing Wednesday. Federal prosecutors in New York are conducting a criminal probe into the practice known as “cherry-picking,” where winning trades are credited to favored accounts, according to people familiar with the matter.

“The company launched an internal investigation into certain past trade allocations involving treasury derivatives in select Western Asset-managed accounts,” the firm said. “The company is also cooperating with parallel government investigations.”

Western Asset said Wednesday it’s closing its $2 billion Macro Opportunities strategy and named Michael Buchanan as sole CIO. Shares of parent company Franklin Resources Inc. tumbled 13% to $19.78, the most since October 2020, extending their decline this year to 34%.

Western Asset, with $381 billion in assets, is one of the original California bond giants and once rivaled Pacific Investment Management Co. and BlackRock Inc. in size. Its key funds have struggled in recent years amid the rise in interest rates, leading to outflows in its flagship strategy, which Leech helped run.

Franklin, which has about $1.6 trillion in assets overall, acquired Western as part of the 2020 purchase of Legg Mason.Leech has worked at Western Asset for more than 30 years, serving as CIO for the bulk of that time.

A Wells notice, which isn’t a formal allegation or finding of misconduct, provides a chance to respond to the agency and try to dissuade it from filing a case.

Leech was a star for years. He co-managed the company’s Core Plus fund as it trounced its peers, though it also stumbled in 2018 when the Fed was raising rates. Since 2021, it has been battered by wagering on a pivot by the central bank.

The $19 billion mutual fund, which is up 2.4% this year, is trailing more than 90% of rivals over the last three and five year periods, and investors have yanked money.

That pullback from Western Asset’s fund stands in contrast to rival ones managed by the likes of Pimco, Capital Group Inc. and BlackRock Inc., which have taken in cash this year as the Federal Reserve prepares to cut interest rates.

“At Franklin, it’s somewhat problematic as the whole reason for buying Legg Mason was to help offset the loss of commission-based sales to drive flows,” Greggory Warren, a strategist at Morningstar, said in a phone interview. “Buying Legg was seen helping provide then with more fixed income and institutional client exposure and being less exposed to fee pressures.”

Western had quietly named Buchanan co-chief investment officer alongside Leech in August 2023. John Bellows, who co-managed Core Plus since 2018, abruptly left at the start of May. A spokesperson for Western earlier said that the firm thanked Bellows for his contributions.

Jim Hirschmann, Western’s president and chief executive officer, said in the statement that Buchanan “has played an integral role in Western Asset’s strategy and growth, and we look forward to having him lead the next chapter of our storied investment team.”

Recommended Newsletter: High-level insights for high-powered executives. Subscribe to the CEO Daily newsletter for free today. Subscribe now.

On Wednesday, Judge Analisa Torres brought the first chapter of a major Securities and Exchange Commission crypto case to a close, imposing a $125 million penalty on the digital assets firm Ripple and forbidding the company from violating securities law in the future. The penalty fell fall short of the $2 billion the SEC had sought, causing XRP—the token closely tied to Ripple—to soar more than 20%.

The SEC v. Ripple case, which began in late 2020, has been viewed as a bellwether for how courts will rule on a broader anti-crypto enforcement campaign by the agency—a campaign the industry claims exceeds the SEC’s legal authority. In response to Wednesday’s ruling, Ripple executives and other crypto watchers framed the decision as a victory for crypto firms. In the bigger picture, though, an almost certain SEC appeal—alongside the vague language of the ruling—means that long-awaited regulatory clarity is still a distant dream.

“The immediate decision by Judge Torres on balance is very positive for Ripple,” said Joe Castelluccio, a partner at Mayer Brown and the co-leader of the law firm’s fintech and blockchain practice groups, adding that the decision should still “give the industry and the market a bit of pause.”

The XRP army

Since its founding in 2012, Ripple has carved out a prominent position in the crypto sector through its promise of building a global payments network and its proprietary token, XRP, which has gained a fiercely loyal follower base and an enviable $35 billion market cap. Along with the financial success, Ripple has faced a series of legal challenges, including the 2020 lawsuit filed by the SEC under then-chair Jay Clayton.

Clayton’s successor Gary Gensler inherited the case, which quickly became the agency’s flagship litigation as it pursued a bruising enforcement campaign against the volatile industry. The SEC argued that the company had violated the law by raising over $1.3 billion through an unregistered digital asset securities offering.

After a high-profile court battle, which included the unveiling of internal SEC emails detailing the inner workings of its approach to crypto, Torres issued a surprising decision in July 2023. She found that Ripple’s sales of XRP directly to institutional investors such as hedge funds violated securities laws, but secondary sales of the token on platforms such as exchanges did not. Ripple—and most of the industry—hailed the ruling as a victory, even as the SEC filed to immediately appeal the decision pending a final judgment.

In the time between Torres’s initial decision and her ruling on Wednesday about damages, several other federal judges—including two in Torres’s own district court—have weighed in with crypto-related rulings of their own. These decisions have come to separate and sometimes contradictory conclusions than what Torres found—meaning the legal status of digital token sales has become a ripe legal question for appeals courts, and potentially for the Supreme Court.

A penalty and an injunction

While it is common for government attorneys to ask for greater penalties than are ultimately enforced, Torres’s final figure of $125 million is much closer to Ripple’s ask than what the SEC requested.

“Anyone is going to spin things their own way, but it’s hard not to see it as a win for Ripple,” said a former SEC attorney now working in crypto law, who spoke with Fortune on the condition of anonymity because of their continued work with the agency. They pointed specifically to the fact that the judge denied the SEC’s request for disgorgements from Ripple, meaning the company would not have to pay back any profits it had earned from illegal behavior.

Despite the financial win, Torres also imposed an injunction against Ripple, ordering the company to refrain from further violations of securities laws. In her decision, she points to Ripple’s “willingness to push the boundaries” of the law after the SEC filed its initial lawsuit, arguing that there is a likelihood the company “will eventually (if it has not already) cross the line.”

Because Torres declined to specifically name whether—and how—Ripple had continued to violate securities laws, the question of when digital token sales constitute securities offerings will remain open. “That points to continued guardrails around conduct in the market, and also the fact that this remains an unsettled area of the law,” said Castelluccio.

Even if Torres had been more firm in her language, it would be unlikely to impact the behavior of other companies, given the ongoing litigation by the SEC against crypto firms like Coinbase and Binance. Moreover, because other federal judges have sharply deviated from Torres’s decision—with two in the Southern District of New York finding that secondary sales could also violate securities laws—the disagreements will not be settled until the cases wind their way up to the appellate level.

Given that the SEC already tried—and failed—to file an appeal in the Ripple case before Torres’s final decision, the agency will likely again appeal the ruling, including the matter of secondary sales and the penalty. Even with the market responding positively to the decision—including XRP rallying 20% in price—Castelluccio cautioned that Torres’s decision from last July, and yesterday’s, will not have the impact of “changing the game or changing the market.”

“Those are all significant overstatements,” he added.

A final wildcard in the legal tussle over XRP and other cryptocurrencies is the slow nature of the appeals process, meaning that any higher court ruling in the Ripple case is highly unlikely before 2025 while any Supreme Court ruling would almost certainly have to wait till 2026 or later. In the meantime, the growing interest in crypto on the part of lawmakers means it is possible Congress passes new rules to govern the sector—potentially resolving the legal issues in the cases involving Ripple and Coinbase before the courts do.

Recommended Newsletter:

CEO Daily provides key context for the news leaders need to know from across the world of business. Every weekday morning, more than 125,000 readers trust CEO Daily for insights about–and from inside–the C-suite. Subscribe Now.

BF Borgers, the independent accounting firm for Trump Media & Technology Group, is facing allegations of “massive fraud” from the Securities and Exchange Commission, which on Friday claimed the auditor ran a “sham audit mill” that put investors at risk.

The SEC said Borgers has been shut down, noting that the company agreed to a permanent suspension from appearing and practicing before the agency as accountants. The suspension is effective immediately. Additionally, BF Borgers agreed to pay a $12 million civil penalty, while owner Benjamin Borgers will pay a $2 million civil penalty.

Neither the SEC statement nor its complaint mentioned Trump Media & Technology Group. Borgers didn’t respond to a request for comment.

In an email, Trump Media said it “looks forward to working with new auditing partners in accordance with today’s SEC order.”

The SEC charged Borgers with “deliberate and systemic failures” in complying with accounting standards in 1,500 SEC filings from January 2021 through June 2023, a period during which Borgers had about 350 clients. Trump Media’s March debut as a public company came after that time period, but the social media company said in its 2023 annual report that it had worked with Borgers prior to going public on the Nasdaq stock exchange.

In its report, the company added that an audit committee on March 28 approved Borgers to audit its 2023 and 2022 financial statements.

Among the issues cited by the SEC is that Borgers failed to comply with Public Company Accounting Oversight Board (PCAOB) standards in its audits, even though the regulatory agency requires that public companies’ financial statements meet those standards. Borgers also allegedly falsely told clients that its work would comply with those standards.

The agency claims that at least 75% of the filings that incorporated Borgers’ audits and reviews failed to meet PCAOB standards.

“Ben Borgers and his audit firm, BF Borgers, were responsible for one of the largest wholesale failures by gatekeepers in our financial markets,” Gurbir S. Grewal, director of the SEC’s Division of Enforcement, said in the statement.

He added, “As a result of their fraudulent conduct, they not only put investors and markets at risk by causing public companies to incorporate noncompliant audits and reviews into more than 1,500 filings with the Commission, but also undermined trust and confidence in our markets.”

Aimee Picchi is the associate managing editor for CBS MoneyWatch, where she covers business and personal finance. She previously worked at Bloomberg News and has written for national news outlets including USA Today and Consumer Reports.

Ethereum Spot Exchange-Traded Funds (ETFs) approval odds continue to witness notable pessimism as the cryptocurrency space awaits the United States Securities and Exchange Commission’s (SEC) decision on the products scheduled for May.

The expectation surrounding the SEC’s decision highlights how important ETF approval is in terms of giving conventional investors more convenient access to Ethereum’s spot market. Presently, data from Polymarket, the world’s largest prediction market, shows that ETH ETF approval odds have fallen to a mere 11%.

Pessimism Deepens As Ethereum ETFs Remain Uncertain

As the May deadline draws near, doubt and skepticism loom large on the horizon, casting a dark shadow for the products. One of the most recent figures to voice doubts about the SEC’s willingness to approve the exchange-traded products this May is Nate Geraci, the president of ETF Store.

According to Geraci, the regulatory watchdog is eerily silent on Ethereum spot ETFs. He further suggested that the products might not be approved due to the SEC’s significantly lower level of engagement with ETF issuers than in previous interactions.

“Logic says that is correct, but also wonder if SEC learned a lesson from clown show with spot Bitcoin ETFs,” he added. Thus, he has pointed out two possible options for the products, which are either an approval or lawsuit from the Commission.

Commenting on the president’s insights, a pseudonymous X user questioned if there is a possibility that activities are taking place behind closed doors in order to avoid disrupting the pre-launch market. Geraci responded, saying he believes that could be possible, drawing attention to Van Eck CEO Jan Van Eck’s review, which might prove otherwise.

It is worth noting that Van Eck is one of the earliest firms to submit its application for an Ethereum exchange product. Even though the company was the first to file for an application, Jan Van Eck is pessimistic about the approval of the ETPs, saying they will probably be rejected in May.

He stated:

The way the legal process goes is the regulators will give you comments on your application, and that happened for weeks and weeks before the Bitcoin ETFs. And right now, pins are dropping as far as Ethereum is concerned.

In light of this, investors prepare for an unpredictable result while managing market swings and modifying their investment plans in the face of changing regulations.

ETH Price Sees Positive Movement

While Ethereum ETFs might be experiencing negative sentiment, ETH, on the other hand, has witnessed a positive uptick lately. ETH has revisited the $3,000 level again after falling as low as $2,888 during the weekend.

Today, ETH price rose by over 4%, reaching around $3,234, indicating potential for further price recovery. At the time of writing, Ethereum was trading at $3,215, demonstrating an increase of 1.40% in the past day.

Also, the asset’s market cap and trading volume are up by 1.40% and 5.96% in the last 24 hours. Given the anticipated impact of the recently concluded Bitcoin Halving on cryptocurrencies, ETH could be poised for noteworthy moves in the coming months.

ETH trading at $3,204 on the 1D chart | Source: ETHUSDT on Tradingview.com

Featured image from iStock, chart from Tradingview.com

Disclaimer: The article is provided for educational purposes only. It does not represent the opinions of NewsBTC on whether to buy, sell or hold any investments and naturally investing carries risks. You are advised to conduct your own research before making any investment decisions. Use information provided on this website entirely at your own risk.

Ripple Labs, a leading cryptocurrency payment firm, has been seen moving millions of XRP tokens following the United States Securities and Exchange Commission’s (SEC) recent victory in a legal dispute.

Ripple Moves Millions Of XRP As Price Holds Steady

According to a recent report, Ripple Labs moved a whopping 120 million XRP tokens valued at about $60.8 million. The move has caused quite a stir within the XRP community and heightened sell-off anxiety in the face of increased market volatility.

This comes after the payment firm experienced a legal setback in court on Monday. The SEC’s motion to force Ripple to provide its financial statements for XRP was granted by the Southern US District Court of New York.

It was reported by Bithomp that the aforementioned funds were transferred to a Ripple-related wallet that was used for massive transfers. Data from Bithomp revealed that the wallet address rBg2Fu…uJ4vt5x1o91m moved the funds to a separate wallet address rP4X2hTa7…XvPz7XZ63sKxv3. This indicates that the transaction might include the transfer of such large amounts using other wallets or companies under Ripple’s control.

Furthermore, the transfer might just be connected to Ripple’s payment services. As a result, it will allow banks to utilize XRP to send funds across borders almost instantly and for a minimal cost.

It is noteworthy that the address that received the funds has transferred a notable portion of the XRP tokens. However, the address still contains about 90 million XRP valued at approximately $45 million.

Bithomp also reported that the firm was seen moving about 53.75 million XRP tokens valued at about $27.5 million. Data from the on-chain platform shows that the wallet address rKveEy…ZsoGMb3PEv transferred the funds to another wallet address rPfSrrKY…R7g1tYzDDJoAys.

The Payment Firm Brings XRP To The US Market

Ripple has announced its plan to transform international payments in the US with XRP and its payment services. According to the firm, they will be introducing “new product updates that will cover the majority of US states.”

These fresh products are going to be powered by its Money Transmitter Licenses (MTLs). Initially, Oliver Segovia, Senior Director and Head of Product Marketing for Payments at Ripple, shared the announcement on Linkedin.

Segovia explained that although Ripple’s global headquarters is located in the US, 90% of its businesses serve organizations outside. Specifically, he acknowledges that for the last three years, the firm has remained somewhat quiet in the US market.

Despite these developments, XRP’s price has still been down by 5.42% in the past week, holding steady at $0.50. Interestingly, its trading volume has increased by over 25% in the past 24 hours.

XRP trading at $0.5039 on the 1D chart | Source: XRPUSDT on Tradingview.com

Featured image from iStock, chart by Tradingview.com

Disclaimer: The article is provided for educational purposes only. It does not represent the opinions of NewsBTC on whether to buy, sell or hold any investments and naturally investing carries risks. You are advised to conduct your own research before making any investment decisions. Use information provided on this website entirely at your own risk.

A Colorado pastor of an online church is challenging allegations that he and his wife defrauded parishioners out of millions dollars through the sale of cryptocurrency deemed “essentially worthless” by state securities regulators.

Colorado Securities Commissioner (CSC) Tung Chan filed civil fraud charges against Eligo and Kaitlyn Regalado last week in Denver District Court, according to a statement from the Colorado Department of Regulatory Agencies. The complaint accuses the Regalados of targeting members of the state’s Christian community, enriching themselves by promoting a cryptocurrency token that the Denver couple launched called the INDXcoin.

The couple allegedly sold the “illiquid and practically worthless” tokens from June 2022 to April 2023 through a cryptocurrency exchange they created called Kingdom Wealth Exchange, Commissioner Chan said in the statement. The sales supported the couple’s “lavish lifestyle,” he alleged.

Kingdom Wealth Exchange, the only crypto exchange selling the INDX token was inexplicably shut down on November 1, according to the Denver Post.

“Mr. Regalado took advantage of the trust and faith of his own Christian community and that he peddled outlandish promises of wealth to them when he sold them essentially worthless cryptocurrencies,” Chan said.

Pastor says “God was going to provide”

In a nine-minute long video, Regalado acknowledged on Friday that the allegations that he made $1.3 million from investors “are true.”

“We took God at His word and sold a cryptocurrency with no clear exit,” Regalado said in the video, adding that he had also been divinely instructed to abandon his former business to take over INDXcoin.

“I’m like, well, where’s this liquidity going to come from,’ and the Lord says, ‘Trust Me,’” Regalado said in the video.

“We were just always under the impression that God was going to provide that the source was never-ending,” he added.

Regalado did not immediately return CBS MoneyWatch’s request for comment.

According to the CSC, the Regalados had no prior experience operating a cryptocurrency exchange or creating a virtual token before minting INDX two years ago. Almost anyone can create a cryptocurrency token, the agency noted in its statement.

There are more than 2 million cryptocurrencies in existence, in addition to 701 cryptocurrency exchanges where investors can trade them, according to crypto markets website CoinMarketCap.

Regalado said in the video that he will go to court to address the allegations against him and his wife. “God is not done with this project; God is not done with INDX coin,” he said.

Elizabeth Napolitano is a freelance reporter at CBS MoneyWatch, where she covers business and technology news. She also writes for CoinDesk. Before joining CBS, she interned at NBC News’ BizTech Unit and worked on The Associated Press’ web scraping team.

The Securities and Exchange Commission on Friday rejected a petition from Coinbase, the largest crypto exchange in the U.S., for a separate regulatory framework for the cryptocurrency industry.

“The commission concludes that the requested rulemaking is currently unwarranted and denies the petition,” the SEC wrote in a letter addressed to Coinbase’s chief legal officer, Paul Grewal.

Gary Gensler, the chair of the SEC, cheered on the denial in a separate statement, saying that he supported the commission’s decision because, he argues, existing laws and regulations already apply to crypto, the SEC already addresses the industry through rulemaking, and it’s important for his agency to maintain control over what resources it deploys to oversee its regulatory agenda. “As I said prior to the collapse of one of the largest noncompliant crypto intermediaries that cost investors billions of dollars,” he wrote, “meaningful engagement with the SEC is always welcome.”

Spokespeople for Coinbase did not immediately respond to a request for comment when contacted by Fortune.

The SEC’s ruling on Coinbase’s petition comes more than a year after the company filed its request with the agency, arguing that the “U.S. does not currently have a functioning market in digital asset securities due to the lack of a clear and workable regulatory regime.”

After the collapse of FTX in November 2022 and the subsequent arrest of the exchange’s CEO, Sam Bankman-Fried, the SEC, under the guidance of Gensler, has embarked on an extensive campaign against crypto.

In the first half of 2023, it targeted some of the largest players in the industry, filing suits against Gemini, Genesis, Terraform Labs and founder Do Kwon, as well as Justin Sun and Tron. In June, it launched salvos against two crypto heavyweights, first suing the world’s largest crypto exchange, Binance, and then filing a lawsuit against Coinbase. The SEC’s campaign has continued through the end of the year, with it most recently targeting another industry mainstay, the crypto exchange Kraken.

Most of its lawsuits against the industry’s top players are ongoing, even its litigation against Binance, which recently agreed to a $4.3 billion settlement with the Department of Justice for breaking anti-money laundering laws, among other crimes.

Coinbase, which positions itself as one of the industry’s do-gooders, has cried foul at the SEC’s extensive litigation against crypto, claiming the agency is “regulating through enforcement,” rather than rulemaking. Evidently, the SEC disagrees, and its lawsuit against Coinbase, which it alleges listed unregistered “crypto asset securities,” continues to wind its way through court.

Subscribe to Fortune Crypto to get daily updates on the coins, companies, and people shaping the world of crypto. Sign up for the newsletter for free.

Prominent pro-XRP lawyer John Deaton has launched a scathing critique of the US Securities and Exchange Commission (SEC) in light of the regulatory body’s actions against blockchain company LBRY Inc. Deaton, renowned for representing XRP holders in the Ripple-SEC lawsuit, marked the regulatory body’s conduct as an exhibit of overreach.

“The LBRY case should be taught in law schools across the country,” Deaton asserted on X (formerly Twitter), emphasizing its significance not just in applying “the Howey Test to modern-day blockchain technologies and crypto,” but also as a “specific highlight [of] SEC overreach.”

Pro-XRP Lawyer Deaton Slams SEC

Elaborating further on his stance, Deaton criticized the SEC’s choice to pursue LBRY Inc., a relatively smaller entity, despite there being larger, more questionable activities to scrutinize within the crypto sector. He remarked that the regulatory body “picked a small American Company based out of New Hampshire, threatened to bankrupt it during the investigation, and then proceeded to bankrupt it – in a case where no fraud or misrepresentation occurred.”

Meanwhile, the US Securities and Exchange Commission (SEC) has seemingly turned a blind eye to the real scammers in the crypto ecosystem. Deaton cites “FTX, Celsius Network, Voyager, Luna, Genesis, [other] pump and dumps” as potential targets for the US agency that it could have investigated and stopped to protect US retail investors. Instead, all of these companies caused a massive amount of damage.

Deaton’s tweet came in response to an announcement by LBRY Inc. Marked by a tone of resignation, they unveiled their decision to cease operations amidst unsustainable debts and continuous challenges posed by the SEC. The firm was initially slapped with a $22 million fine, which was later mitigated to $111,000 by the SEC, in cognizance of LBRY’s financial duress.

Following this, the company withdrew its appeal against the SEC and commenced its wind-down procedures, with all executives, employees, and board members tendering their resignations.

Commenting on the LBRY case’s broader implications, Deaton highlighted the expenditure of “millions of dollars” resulting in a $130,000 fine, painting a picture of inefficiency and failure on the part of the SEC.

His condemnation didn’t just pertain to the financial aspects but extended towards the regulatory approach and discernment exercised by the SEC in choosing its battles within the crypto landscape:

After millions of dollars were wasted, the SEC got a $130K fine. This case alone proves the SEC is a broken, failed and inept agency.

Remarkably, the conclusion of LBRY’s journey has elicited a mixture of disappointment and resilience from the crypto community. Despite the unfolding adversities, community members have conveyed their willingness to sustain LBRY’s open-source blockchain network, Odysee, showcasing the persistent spirit of the decentralized ethos.

At press time, XRP was trading at $ and eyed a daily above the 200-day EMA ($0.5172)

Several Wall Street banks were hit with substantial fines by two regulatory agencies on Tuesday for utilizing “off-channel” messaging services and failing to properly preserve the communications wherein deals, trades, and other business were discussed.

The Securities and Exchange Commission (SEC) is imposing fines totaling $289 million across nine firms, while the Commodity Futures Trading Commission (CFTC) is imposing $260 million in fines — resulting in a combined total penalty of $549 million.

The agencies found that employees frequently used personal devices and platforms like iMessage, WhatsApp, and Signal to discuss business matters, according to the complaint, but failed to retain most of the communications, violating securities laws, the SEC press release noted.

The SEC has taken action against 10 broker-dealer firms and one dually registered broker-dealer and investment adviser for “longstanding failures” to “preserve electronic communications” that occurred when discussing business. The SEC’s investigation revealed widespread and prolonged use of unofficial communication channels at all 11 firms.

Among the fined firms, Wells Fargo and its affiliates (Wells Fargo Clearing Services and Wells Fargo Advisors Financial Network) agreed to pay $125 million, while BNP Paribas Securities and SG Americas Securities will pay $35 million each. Other firms facing fines are BMO Capital Markets Corp. and Mizuho Securities USA ($25 million each), Houlihan Lokey Capital ($15 million), Moelis & Company and Wedbush Securities ($10 million each), and SMBC Nikko Securities America ($9 million).

The SEC stresses that adhering to recordkeeping regulations is crucial for safeguarding investors and maintaining well-functioning markets.

“Today’s actions stem from our continuing sweep to ensure that regulated entities, including broker-dealers and investment advisers, comply with their recordkeeping requirements, which are essential for us to monitor and enforce compliance with the federal securities laws,” Sanjay Wadhwa, SEC deputy director of enforcement, said in a statement. “Recordkeeping failures such as those here undermine our ability to exercise effective regulatory oversight, often at the expense of investors.”

The 11 firms involved admitted to violating “crucial requirements” and are taking steps to prevent future violations, Wadhwa added.

Gurbir S. Grewal, director of the SEC’s division of enforcement, advises firms to self-report and rectify to avoid harsher consequences.

“So here are three takeaways for those firms who haven’t yet done so: self-report, cooperate and remediate. If you adopt that playbook, you’ll have a better outcome than if you wait for us to come calling.”

The Securities and Exchange Commission announced charges Wednesday against actor Lindsay Lohan, boxer Jake Paul and a group of rappers and R&B stars, including Soulja Boy, Akon and Lil Yachty.

Abbott Laboratories is facing investigations by the Securities and Exchange Commission and the Federal Trade Commission (FTC) in connection with its formula business, the company revealed in a recent SEC filing.

The developments are the latest in a series of inquiries into the factors that precipitated the company’s Michigan factory shutdown and kickstarted a nationwide formula shortage.

Abbott received a subpoena from the SEC’s Enforcement Division soliciting “information relating to Abbott’s powder infant-formula business and related public disclosures” last December, the company said.

Then, in January, the FTC issued the manufacturer a civil investigative demand connected with an investigation into companies that bid for infant formula contracts with federal nutritional programs such as the Special Supplemental Nutrition Program for Women, Infants, and Children, or WIC, program. That same month, Abbott also confirmed the U.S. Justice Department is investigating operations at its Michigan plant.

Abbott Laboratories made headlines in February 2022 after the FDA sent inspectors to Abbott’s infant formula manufacturing facility in Sturgis, Michigan, to investigate a whistleblower report alleging the company had engaged in activities to cover up substandard cleaning practices at its facilities and had shipped untested and potentially contaminated formula to retailers.

Abbott recalled select Similac, EleCare and Alimentum as well as powdered infant formulas manufactured at the Sturgis plant, and closed down the factory later that month when investigators found evidence of cronobacter sakazakii bacteria at the facility. The recall came shortly after four infants drank Abbott’s formula and contracted cronobacter infections; two of the infants died.

At least two dozen families are now suing Abbott over the allegedly contaminated formula. Abbott’s representatives say there’s no conclusive evidence linking its formula to the infants’ illnesses, as none of the cronobacter strains found at their plant matched samples genetically sequenced from the sick infants.

Food and Drug Administration Commissioner Robert Califf said his agency’s inspections found conditions at Abbott’s Sturgis, Michigan plant “shocking” and “egregiously unsanitary.”

The Michigan plant closure took a massive toll on families nationwide, forcing parents and caregivers to turn to local food pantries to procure formula and spurring collection initiatives at breast milk banks.

Abbott Nutrition, a subdivision of multinational health conglomerate Abbott Laboratories that oversees the conglomerate’s formula business, controlled 40% of the baby-formula market in the U.S. at the time of its Michigan plant shutdown last year.

Public health organizations have for decades criticized formula makers for aggressively marketing their products to the detriment of breastfeeding. The World Health Organization last year detailed how big formula companies use aggressive marketing practices to promote the use of infant formula over breast milk, leaving many families dependent on commercial products and vulnerable to formula shortages. A series of papers published in the medical journal The Lancet this month describes what its authors call the commercial milk industry’s “underhand marketing strategies, designed to prey on parents’ fears and concerns, to turn the feeding of infants and young children into a multibillion-dollar business.”

A Russian millionaire with ties to the Kremlin was convicted Tuesday of participating in an elaborate $90 million insider trading scheme using secret earnings information from companies such as Microsoft that was stolen from U.S. computer networks.

Vladislav Klyushin, 42, who ran a Moscow-based information technology company associated with the Russian government, was found guilty on all charges against him, including wire fraud and securities fraud, after a two-week trial in federal court in Boston.

“The jury saw Mr. Klyushin for exactly what he is — a cybercriminal and a cheat. He repeatedly gamed the system and finally got caught. Now he is a convicted felon. For nearly three years, he and his co-conspirators repeatedly hacked into U.S. computer networks to obtain tomorrow’s headlines today,” Massachusetts U.S. Attorney Rachael Rollins said in an emailed statement.

Klyushin was arrested in 2021 in Switzerland after he arrived on a private jet and just before he and his party were about to board a helicopter to whisk them to a nearby ski resort. Four alleged co-conspirators — including a Russian military intelligence officer who’s also been charged with meddling in the 2016 presidential election — remain at large.

Klyushin’s attorney, Maksim Nemtsev, said in an email that he and his client are disappointed but respect the jury’s verdict. He said they intend to appeal, adding that the case included “novel theories” that have never before been reviewed or adopted by higher courts.

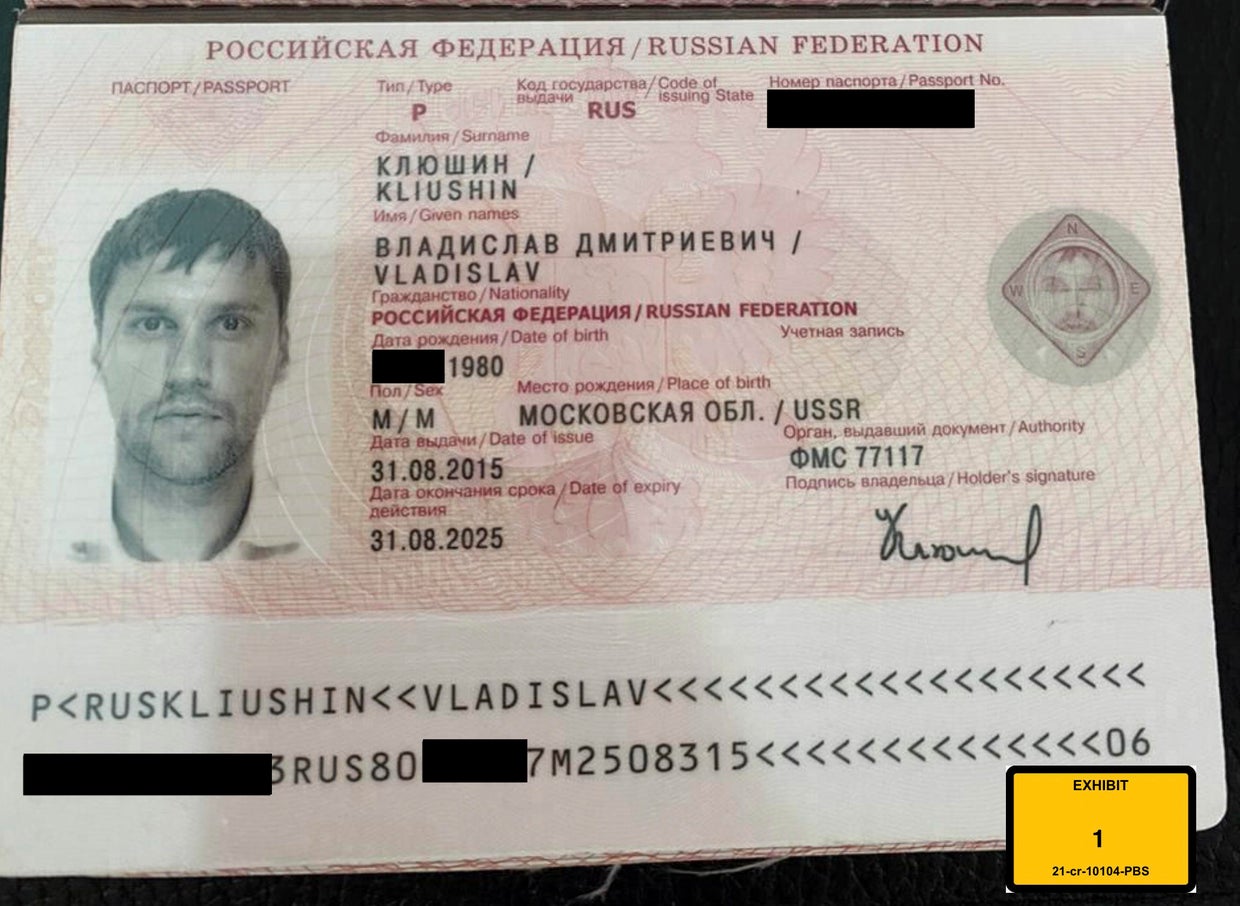

This image provided by the U.S. Attorney’s Office shows the Russian passport of Vladislav Klyushin, part of the U.S. government’s evidence entered into the record during Klyushin’s trial. Klyushin, a Russian millionaire with ties to the Kremlin, was convicted Tuesday, Feb. 14, 2023, of participating in a $90 million insider trading scheme using secret earnings information from companies such as Microsoft that was stolen from U.S. computer networks.

U.S. Attorney’s Office via AP, File

The businessman was owner of a Moscow-based information technology company that purported to provide services to detect vulnerabilities in computer systems. It counted among its clients the administration of Russian President Vladimir Putin and other government entities, according to prosecutors.

Klyushin was also close friends with a Russian military officer who was among 12 Russians charged in 2018 with hacking into key Democratic Party email accounts, including those belonging to Hilary Clinton’s presidential campaign chairman, John Podesta, the Democratic National Committee and the Democratic Congressional Campaign Committee. Ivan Ermakov, who worked for Klyushin’s company, was a hacker in the alleged insider trading scheme, alleged prosecutors. They have not alleged that Klyushin was involved in the election interference.

Stolen credentials

Prosecutors say hackers stole employees’ usernames and passwords for two U.S.-based vendors that publicly traded companies use to make filings through the Securities and Exchange Commission. They then broke into the vendors’ computer systems to get financial disclosures for hundreds of companies — including Microsoft, Tesla, Kohls, Ulta Beauty and Sketchers — before they were filed to the SEC and became public, prosecutors said. Many of the earnings reports were downloaded via a computer server located in Boston, according to prosecutors.

Armed with this insider information, the hackers were able to cheat the stock market, alleged prosecutors. They said that Klyushin personally turned a $2 million investment into nearly $21 million, and altogether, the group turned about $9 million into nearly $90 million.

Klyushin’s attorney denied that his client was involved in the scheme, telling jurors in his opening statement that the government’s case was filled with “gaping holes” and “inferences.”