TOPSHOT – The Manhattan skyline is seen at sunrise from the 86th floor observatory of the Empire … [+] State Building (Photo by Angela Weiss / AFP) (Photo by ANGELA WEISS/AFP via Getty Images)

AFP via Getty Images

In the past years, crowdfunding has gained traction for certain real estate investments. While some platforms are available to all investors, others require individuals to meet certain criteria to participate. The SEC divides investors into two categories: non-accredited and accredited. In my previous article, I discussed the differences between these two, along with some considerations for platforms that accept non-accredited investor funding.

In this piece, we’ll look at crowdfunding for accredited investors. One of the well-known players in this space is CrowdStreet, which has funded more than 750 deals with over $4 billion invested. CrowdStreet requires a minimum investment of $25,000 for most deals.

CrowdStreet recently hit headlines when investor funds went missing. On August 11, Bisnow reported investigations by the DOJ into Nightingale Properties, which allegedly diverted nearly $40 million of equity raised on CrowdStreet into accounts controlled by its CEO. In light of the missing funds, CrowdStreet co-founder Tore Steen left his role as CEO of the company. In a statement published by Crowdfund Insider, CrowdStreet stated that the investments on its platform “are illiquid, with significant risks. These risks are clearly disclosed to investors both when they sign up on the CrowdStreet platform, when they complete a new account agreement, and when they make an offer and fund a specific investment.” The platform has also announced new enhancements, including escrow account funding, individual accreditation verification, and operational improvements aimed to increase investor protections.

Despite recent events, crowdfunding platforms continue to have a presence in the investment world. Another platform open to accredited investors is EquityMultiple, which requires a starting investment of at least $5,000. It focuses on commercial real estate, with opportunities including equity, preferred equity, and senior debt investments. PeerStreet allows accredited investors to start with minimums of $1,000 for debt investments.

Before we go further, I want to point out that it’s essential to consult an attorney before delving into crowdfunding. There are complex regulations in this space, and you’ll want to make sure that everything from the disclosures you provide to the way you file is in line with the SEC requirements. In addition, clearly there are risks involved, and carrying out research and due diligence will be increasingly important amid today’s rising interest rates and higher costs of debt.

Who Qualifies as an Accredited Investor

Individuals who have a net worth of more than $1 million (not including their primary residence) can qualify as accredited investors. Those who have earned $200,000 as a single filer or $300,000 as a couple during the previous two years, with an expectation to continue to make the same going forward, are also included in this category. Households that meet the criteria to be accredited investors are able to invest in certain products and vehicles, including real estate.

As I’ve mentioned previously, when raising capital for an acquisition, you’ll often be reaching out to individuals who could contribute $25,000 or more. In recent years, crowdfunding rules have changed—specifically the JOBS Act of 2012 created avenues for non-accredited investors to participate in fundraising. While some crowdfunding platforms do cater to all investors and accept contributions starting at low figures such as $50, it’s also true that platforms for accredited investors often are looking to fund larger projects.

Factors to Consider before Trying Out Crowdfunding

Crowdfunding platforms are as unique as individual investors—you’ll find that the minimum investment, fees, and listings differ from one site to another. The way that investors are managed through crowdfunding can vary too. Some platforms allow you to own the communication with investors after you raise the money, while others have limitations. You’ll want to find out who is overseeing the investor relationship and how that fits into your business plan.

Like other types of real estate investments, track records and reputation matter. It can be valuable to compare and evaluate different platforms to see how they have performed in the past. The number of years they have operated and the amount of funding they have raised can be a determining factor. Following several platforms over time and paying attention to their social media presence may be helpful as well. Look for the total number of investors and the historical annual returns, along with opportunities to reinvest. Read through reviews and see what others are saying about the sites through online channels. Check how much information is available on the platform: Are there educational resources available? How are opportunities vetted? What can investors expect? Are there ways to communicate and interact personally?

If you’re attempting to raise money for a real estate investment for the first time, relying on crowdfunding might get complicated. In some cases, it could serve to supplement the capital you’re already bringing to the table. However, you’ll want to keep in mind that with so many rules involved, you’ll need to work with professionals including an attorney to make sure you’re proceeding correctly.

Ultimately, you may opt to work with a partner who has experience on these platforms when starting out. Or you might find that your deal team prefers to connect directly with investors, reaching out personally and raising funds on an individual basis. After you’ve carried out several successful deals and are looking for ways to diversify, you might revisit crowdfunding options. Overall, the best opportunities tend to come to those who have an insider’s edge, and that typically requires building relationships and developing a team over time.

Cryptocurrency influencer Richard Heart defrauded investors of millions he obtained through the illegal sale of unregistered crypto asset securities, which he then used to make extravagant purchases, the Securities and Exchange Commission claims.

The YouTuber misappropriated at least $12 million in investor funds, according to the lawsuit filed Monday, funds that he raised through his crypto ventures Hex, PulseChain and PulseX — all three of which he controls. He then spent the money on “exorbitant luxury goods,” including a 555-karat black diamond called The Enigma, worth roughly $4.3 million, the suit claims. His other alleged splurges included a $1.38 million Rolex watch, a $534,916 McLaren sports car and a $314,125 Ferrari Roma, according to the complaint.

“I want to be the best crypto founder that’s ever existed. I like doing – I like owning the world’s largest diamond,” Heart stated in a January 2023 Hex Conference (available on YouTube) cited by the SEC.

On one occasion, Heart “immediately transferred” $217 million of investor assets from PulseChain’s crypto assets account of $354 million, into “a private held wallet,” the complaint states.

Today we charged Richard Heart (aka Richard Schueler) and three unincorporated entities that he controls, Hex, PulseChain, and PulseX, with conducting unregistered offerings of crypto asset securities that raised more than $1 billion in crypto assets from investors.

— U.S. Securities and Exchange Commission (@SECGov) July 31, 2023

One man, three crypto entities

Heart launched Hex, an Etherium-based token, in 2019, aggressively promoting its potential on his Youtube channel as, “the highest appreciating asset that has ever existed in the history of man,” the complaint states.

He began raising funds, between July 2021 and April 2022, for PulseChain and PulseX, two crypto platforms that he “designed, created, and maintained,” and which have their own native tokens.

“Beginning in December 2019, and continuing for at least the next three years, Heart raised more than $1 billion,” operating through the three entities of Hex, PulseChain and PulseX, according to the SEC.

“Although Heart claimed these investments were for the vague purpose of supporting free speech, he did not disclose that he used millions of dollars of PulseChain investor funds to buy luxury goods for himself,” the SEC’s lawyers said in the lawsuit.

Heart also accepted more than 2.3 million ether tokens from December 2019 to November 2020, worth more than $678 million at the time, as noted in the lawsuit. However, 94% to 97% of those tokens were “directed by Heart or other insiders,” enabling them to gain control of a large number of Hex tokens while “creating the false impression of significant trading volume and organic demand” for the tokens.

“Heart pumped Hex’s capacity for investment gain,” the lawsuit states.

Crackdown on unregistered securities

The SEC is also suing Heart for securities registration violations. All three of his crypto projects are considered unregistered securities.

Each of the three tokens is “was, and is, a crypto-asset security,” the SEC’s lawyers allege in the lawsuit, that should have been registered according to the suit, and therefore “violated the federal securities laws through the unregistered offer and sale of securities.”

Regulators from the SEC are cracking down on cryptocurrencies following the high-profile implosions of crypto exchange FTX and the crash of so-called stablecoin TerraUSA and its sister token, luna, last year. SEC Chairman Gary Gensler said at the time that he believes “the vast majority” of the nearly 10,000 tokens in the crypto market at that time were securities.

Bitcoin rose sharply Wednesday and surpassed $30,000 for the first time in months, continuing a days-long increase in the cryptocurrency’s price, despite economic uncertainty and a regulatory crackdown on some crypto exchanges.

The Binance logo is displayed on a screen in San Anselmo, California, June 6, 2023.

Justin Sullivan | Getty Images

Binance.US customers will no longer be able to use U.S. dollars to buy crypto on the platform as early as June 13, hobbling the exchange’s ability to do business in the U.S., after both payment and banking partners “signaled their intent to pause USD fiat channels,” the exchange said.

Binance announced the change late Thursday night on Twitter and blamed the U.S. Securities and Exchange Commission’s “unjustified civil claims against our business.” The exchange said it had preemptively disabled customers’ ability to buy and deposit U.S. dollars.

Binance’s banking transactions are the center of immense scrutiny by the SEC, which filed a civil complaint against the exchange and its founder, Changpeng Zhao, alleging both violated U.S. securities laws.

Zhao’s influence over and ownership of the U.S. and international arms of Binance — an international network of offshore holding companies the SEC alleges have moved billions of dollars of assets between themselves — prompted the SEC to file an emergency motion for a temporary restraining order. That restraining order would have frozen U.S. dollars from the exchange anyway.

Customers won’t lose their money. Those who haven’t withdrawn their money by the shutdown date could still theoretically convert it to a stablecoin such as tether, then withdraw that and convert it back to dollars elsewhere. But it suggests Binance’s banking partners have decided the exchange is too risky a client to keep on, and that the revelations from the SEC case have grown too significant to ignore.

The exchange’s disclosed U.S. banking partners, which have included Axos Bank, Cross River Bank and the failed Silvergate, Signature and Silicon Valley Banks, processed billions of dollars in transactions for the U.S. exchange, according to documents Binance provided to the SEC. Multiple banking partners had already stopped serving Binance and it wasn’t immediately clear which banking partners Binance retained.

The U.S. Securities and Exchange Commission on Monday sued Binance and its CEO, Changpeng Zhao, alleging the cryptocurrency company was effectively operating an illegal exchange and diverted investors’ funds into a trading entity controlled by Zhao.

The lawsuit, filed Monday in federal court in Washington, D.C., claims Binance ran its trading operations without registering with the SEC, as required by law, in order to “evade the critical regulatory oversight” aimed at protecting investors and markets.

Binance, the world’s largest crypto-currency exchange, allegedly commingled and diverted customers’ assets, steps that registered financial firms wouldn’t be able to do, the agency claims. The SEC also charges that Zhao and Binance redirected “billions of U.S. dollars of customer funds” into an account controlled by Zhao.

“Defendants’ purposeful efforts to evade U.S. regulatory oversight while simultaneously providing securities-related services to U.S. customers put the safety of billions of dollars of U.S. investor capital at risk and at Binance’s and Zhao’s mercy,” the lawsuit claims.

The lawsuit also alleges Binance defrauded customers by claiming they had controls in place to monitor “manipulative trading.”

Binance didn’t immediately respond a request for comment.

This is a developing story and will be updated.

Thanks for reading CBS NEWS.

Create your free account or log in for more features.

A former Wells Fargo executive agreed to pay a $3 million penalty to settle Securities and Exchange Commission charges that she misled investors.

From 2014 to 2016, Carrie Tolstedt publicly endorsed a key Wells Fargo metric that measured the bank’s financial success, according to the SEC. But the metric was inflated by accounts and services that were unused, unneeded or unauthorized, the SEC said in a news release this week.

Tolstedt, the longtime head of Wells Fargo’s retail banking division, knew the so-called cross-sell metric wasn’t accurately tracking accounts or products that customers needed or used because she was aware of misconduct at Wells Fargo’s Community Bank, according to the SEC. Bankers were pushing products on customers they did not need or want, including the unauthorized opening of accounts.

Tolstedt, who retired from Wells Fargo in 2016, made misleading public statements to investors at conferences, according to the SEC. She also signed misleading certifications about the accuracy of the bank’s public disclosures when she either knew or was “reckless in not knowing” the disclosures on the cross-sell metric were false or misleading, the SEC said.

The former executive did not admit or deny the SEC’s allegations through the settlement.

A former Wells Fargo executive reached a settlement this week with the Securities and Exchange Commission for $3 million related to allegations of misleading investors. Joshua Komer jkomer@charlotteobserver.com

The SEC will distribute the $3 million settlement plus $2.5 million from a settlement with former Wells Fargo CEO and chairman John Stumpf to harmed investors. That money is in addition to $500 million previously paid by Wells Fargo. Tolstedt also agreed to pay other remedies totaling close to $2 million, according to the release.

“Companies do not act on their own,” said Regional Director Monique Winkler of SEC’s San Francisco office in a statement this week. “Where the facts warrant it, we will hold senior executives accountable for conduct that violates the securities laws.”

Wells Fargo, based in San Francisco, maintains a massive financial and employment presence across the Charlotte area, with some 27,000 employees. It came to North Carolina in 2008 with the purchase of Wachovia.

More on former Wells Fargo executive

Tolstedt, 63, also is facing up to 16 months in prison plus a $100,000 fine and three years of supervised release, The Charlotte Observer reported in March.

Former Wells Fargo community bank head Carrie Tolstedt

In an agreement announced in March in California federal court, Tolstedt agreed to plead guilty to obstructing a government examination of the bank’s misconduct, the Observer reported.

In a separate civil settlement also announced in March, Tolstedt has also been banned from working in the banking industry and must pay a $17 million penalty.

Other Wells Fargo settlements and scandals

Tolstedt’s settlement is the latest consequence of a Wells Fargo sales scandal.

Over more than a decade, hundreds of thousands of Wells Fargo employees took part in sham sales practices, opening millions of fake accounts in customers’ names to meet unreasonably high sales goals, the Observer reported in 2020.

The bank agreed in 2020 to pay a $3 billion fine to federal prosecutors and the SEC for the practices.

In May, Wells Fargo was settling a class-action lawsuit from shareholders for $1 billion over claims the bank misled them about how it was complying with regulators in the aftermath of its fake sales scandal.

This story was originally published June 1, 2023, 11:53 AM.

Related stories from Charlotte Observer

Gordon Rago covers growth and development for The Charlotte Observer. He previously was a reporter at The Virginian-Pilot in Norfolk, Virginia and began his journalism career in 2013 at the Shoshone News-Press in Idaho.

A finance company boasting hundreds of apparently glowing online “customer reviews” and an A+ rating from the Better Business Bureau was this week civilly charged with cheating over 700 investors — many of them senior citizens — out of more than $30 million over 5 years.

El Segundo, Calif.–based Red Rock Secured and its controlling chief executive, Sean Kelly, were accused by the Securities and Exchange Commission of playing on the retirement and tax fears of older investors to sell them gold and silver coins at vastly inflated prices to hold in self-directed IRAs.

The markup on the coins “was almost always above 100 percent, and typically 120 percent or more,” the SEC said in its complaint.

Between 2017 and last year, Red Rock pocketed more than $30 million of the $50 million investors paid for the coins, said the SEC, which also sued two former Red Rock executives.

Attorney Michael Schafler of the Los Angeles law firm Cohen Williams, representing both Red Rock and its CEO, said the company had “nothing to hide” and has been “completely cooperative” with the SEC investigation.

“Red Rock has demonstrated that it is focused on compliance and providing clients with information necessary to make reasoned and informed decisions about purchasing precious metals,” he added. “Red Rock stands by that. It looks forward to the opportunity to defend itself against the government’s allegations in Court.”

According to the SEC, Red Rock used an aggressive marketing campaign to target investors, especially those who were “conservative” or “right wing” politically and “over 59½ [years old].”

Sales personnel played on customers’ fears about government policy, inflation, the stock market and retirement to persuade investors to move IRA funds to Red Rock and invest in gold and silver bullion, according to the SEC. But then, using what the commission calls a “bait and switch,” they persuaded investors instead to buy niche “premium” gold coins with huge, but hidden, markups, which included an 8% sales commission.

These so-called premium coins included an obscure silver Canadian coin for which Red Rock Secured controlled the entire market, allowing it to claim falsely that the “market value” of the coin was more than twice the value of its silver content, the SEC said.

Red Rock Secured salespeople were told to pitch the idea of a “worry-free retirement” to potential clients, while warning them that in the stock market “you could wake up and half your retirement could be gone,” the SEC said.

“The defendants used fear and lies to defraud investors out of millions of dollars from their hard-earned retirement savings,” said Antonia Apps, director of the SEC’s New York office.

There was no hint of any of this in the company’s glowing online “customer reviews.” At Google, Red Rock had an average rating of 4.8 stars out of 5 from 136 self-described customers. At Trustpilot, it got an average rating of 4.8 stars out of 5 from 167 alleged customers. Trustpilot said the rating was “excellent.” At the Better Business Bureau, Red Rock got an average rating of 4.75 stars out of 5 across 96 reviews. At Consumer Affairs it got an average rating of 4.9 stars out of 5.

The Better Business Bureau, contacted by MarketWatch, said it had added an alert to its site about the SEC probe into Red Rock. But, it added, “BBB ratings are not a guarantee of a business’s reliability or performance. BBB recommends that consumers consider a business’s BBB rating in addition to all other available information about the business.”

The organization, which provides information about businesses through a rating system and handles consumer complaints, said its standard policy is to check that all reviews are from legitimate customers by contacting the company being reviewed. The BBB does not possess legal or policing powers.

Business-review platform Trustpilot also told MarketWatch it had added an alert to the Red Rock Secured review page.

“Trustpilot is an open, independent review platform, meaning anyone who has had an experience with a business can leave a review — whether positive or negative — on the business’s Trustpilot profile page,” the company said in a statement “We are currently investigating Red Rock Secured to ensure that they are using our platform in line with our business guidelines, and should we find any evidence they are not, we will take the necessary steps to prevent it.”

Charlie Javice, the 31-year-old founder of now-shuttered student loan software company Frank, has been arrested by law enforcement authorities after being charged with fraud by federal prosecutors.

Javice, whom Forbes named a rising star in its “30 under 30” issue in 2019, was arrested in New Jersey on Monday, the U.S. Department of Justice announced on Tuesday. She faces three charges of fraud and one charge of conspiracy.

Javice was released on $2 million bond Tuesday, and agreed to a curfew and possible electronic monitoring if court officers decide it is necessary. She also agreed not to contact key figures in the case — including investors — except for her mother and her mother’s boyfriend.

The Securities and Exchange Commission also filed a civil complaint alleging that Javice lied about having data on 4 million clients, including making up fake client information, in order to entice JPMorgan Chase to buy her company in 2021 for $175 milliion.

Javice started Frank, a student-aid assistance tool, shortly after graduating from the University of Pennsylvania. As part of the deal to sell the startup to the banking giant, Javice got $21 million for selling her equity stake in Frank, as well as a job as a managing partner at JPMorgan Chase, which came with a $20 million retention bonus, according to the Justice Department. All told, she stood to gain $45 million from the scheme, law enforcement officials said.

“This arrest should warn entrepreneurs who lie to advance their businesses that their lies will catch up to them,” U.S. Attorney Damian Williams said in a statement.

According to the SEC’s complaint, JPMorgan was eager to buy Frank because the company claimed to have contact information — including names, emails and phone numbers — for over 4 million students, a pool of potential new customers the bank wanted to reach.

But those numbers were a lie, authorities allege. Frank only had data for about 300,000 customers, and Javice made up the 4.2 million others with the help of a local data science professor, the SEC’s complaint alleges.

Javice, along with an unnamed Frank executive, “engaged in a months-long scheme to fabricate the data that both of them knew JPMC was paying $175 million to acquire,” the complaint said.

Javice, via a lawyer, denied the allegations.

“Old-school fraud”

The bank discovered the alleged fraud when a test marketing campaign to Frank’s supposed customers flopped. Because JPMorgan Chase had acquired Frank’s internal records as part of the acquisition, it soon found emails in which Javice asked the professor to create “synthetic data” for 4.2 million users and discussed purchasing user databases from a data broker.

“Rather than help students, we allege that Ms. Javice engaged in an old school fraud,” Gurbir Grewal, director of the SEC’s enforcement division, said in a statement. “Even non-public, early-stage companies must be truthful in their representations, and when they fall short we will hold them accountable as in this case.”

Separately, JPMorgan Chase sued Javice last year, alleging fraud, and she countersued. Javice no longer works at the bank.

Federal prosecutors have charged Charlie Javice with fraudulently misrepresenting the value of the college financial aid technology startup she founded by inflating the company’s customer base ahead of a $175 million sale to JPMorgan Chase.

The Securities and Exchange Commission accused Javice on Tuesday of knowingly concealing the number of customers that her New York-based company, Frank, had secured as JPMorgan prepared to acquire the fintech in an attempt to expand in the student financial services industry.

Javice wrongfully received approximately $9.7 million as a result of the transaction as well as “millions more indirectly,” according to a complaint filed by the SEC in the U.S. District Court for the Southern District of New York.

The Department of Justice and the Federal Deposit Insurance Corporation also filed criminal charges against Javice after her arrest last night in New Jersey, accusing the Frank founder of making more than $45 million from the fraudulently negotiated deal, according to a separate statement released on Tuesday.

A lawyer for Javice declined to comment and said in an email that the Frank founder denied the government’s allegations.

The fintech founder allegedly exaggerated the amount of Frank’s 300,000 student loan customers in the months leading up to JPMorgan’s acquisition of the company in September 2021, according to the SEC’s complaint.

Gurbir S. Grewal, director of the SEC’s Division of Enforcement, said in a statement that Javice “lied about Frank’s success” to induce JPMorgan into making a deal.

“Even nonpublic, early-stage companies must be truthful in their representations,” Grewal said.

After launching Frank in 2017 as an online service helping potential and current college students apply for federally disbursed financial aid, the regulator alleged, Javice promoted on the fintech’s website and in deal negotiations throughout 2021 that the company had attracted 4.25 million customers.

After JPMorgan agreed to purchase the fintech, the SEC accused Javice and a high-ranking Frank executive of working together to pay $105,000 and $75,000 to third-party data providers to augment an enlarged list of the company’s customers.

In a lawsuit filed in December, JPMorgan named former Frank chief growth and acquisition officer Olivier Amar as a co-defendant alongside Javice.

A lawyer for Amar did not respond to a request for comment. A spokesperson for JPMorgan declined to comment.

The case raises questions about how banks should conduct due diligence on potential startup acquisitions as lenders increasingly seek to purchase fintechs that have developed lucrative technology or penetrated a market that’s difficult to enter.

During JPMorgan’s fourth-quarter earnings call in January, CEO Jamie Dimon described the acquisition as “a huge mistake.”

Charlie Javice, the 31-year-old founder of now-shuttered student loan software company Frank, has been charged with fraud by the Securities and Exchange Commission.

The SEC filed a complaint Tuesday alleging that Javice lied about having data on 4 million clients, including making up fake client information, in order to entice JP Morgan Chase to buy her company.

Javice started Frank, a student-aid assistance tool, shortly after graduating from the University of Pennsylvania, and sold it to JPMorgan Chase in 2021 for $175 million. As part of the deal, Javice got a $9.7 million payout and a job as a managing partner at JPMorgan Chase, which came with a $20 million retention bonus.

According to the SEC’s complaint, JPMorgan Chase was eager to buy Frank because the tool claimed to have contact information — including names, addresses, emails and phone numbers — for over 4 million students, a base of potential new customers the bank wanted to reach. But the numbers were a lie, the SEC claims. Frank only had data for about 300,000 customers, and Javice made up the 4.2 million others with the help of a local data science professor, the SEC’s complaint alleges.

Javice, along with an unnamed Frank executive, “engaged in a months-long scheme to fabricate the data that both of them knew JPMC was paying $175 million to acquire,” the complaint says.

“Old-school fraud”

The bank discovered the alleged fraud when a test marketing campaign to Frank’s supposed customers flopped. Because JPMorgan Chase had acquired Frank’s internal records as part of the acquisition, it soon found emails in which Javice asked the professor to create “synthetic data” for 4.2 million users and discussed purchasing user databases from a data broker.

“Rather than help students, we allege that Ms. Javice engaged in an old school fraud,” Gurbir Grewal, director of the SEC’s enforcement division, said in a statement. “Even non-public, early-stage companies must be truthful in their representations, and when they fall short we will hold them accountable as in this case.”

Javice, via a lawyer, denied the allegations.

Separately, JP Morgan Chase sued Javice last year, alleging fraud; she countersued. She no longer works at the bank.

The Securities and Exchange Commission announced charges Wednesday against actor Lindsay Lohan, boxer Jake Paul and a group of rappers and R&B stars, including Soulja Boy, Akon and Lil Yachty.

Abbott Laboratories is facing investigations by the Securities and Exchange Commission and the Federal Trade Commission (FTC) in connection with its formula business, the company revealed in a recent SEC filing.

The developments are the latest in a series of inquiries into the factors that precipitated the company’s Michigan factory shutdown and kickstarted a nationwide formula shortage.

Abbott received a subpoena from the SEC’s Enforcement Division soliciting “information relating to Abbott’s powder infant-formula business and related public disclosures” last December, the company said.

Then, in January, the FTC issued the manufacturer a civil investigative demand connected with an investigation into companies that bid for infant formula contracts with federal nutritional programs such as the Special Supplemental Nutrition Program for Women, Infants, and Children, or WIC, program. That same month, Abbott also confirmed the U.S. Justice Department is investigating operations at its Michigan plant.

Abbott Laboratories made headlines in February 2022 after the FDA sent inspectors to Abbott’s infant formula manufacturing facility in Sturgis, Michigan, to investigate a whistleblower report alleging the company had engaged in activities to cover up substandard cleaning practices at its facilities and had shipped untested and potentially contaminated formula to retailers.

Abbott recalled select Similac, EleCare and Alimentum as well as powdered infant formulas manufactured at the Sturgis plant, and closed down the factory later that month when investigators found evidence of cronobacter sakazakii bacteria at the facility. The recall came shortly after four infants drank Abbott’s formula and contracted cronobacter infections; two of the infants died.

At least two dozen families are now suing Abbott over the allegedly contaminated formula. Abbott’s representatives say there’s no conclusive evidence linking its formula to the infants’ illnesses, as none of the cronobacter strains found at their plant matched samples genetically sequenced from the sick infants.

Food and Drug Administration Commissioner Robert Califf said his agency’s inspections found conditions at Abbott’s Sturgis, Michigan plant “shocking” and “egregiously unsanitary.”

The Michigan plant closure took a massive toll on families nationwide, forcing parents and caregivers to turn to local food pantries to procure formula and spurring collection initiatives at breast milk banks.

Abbott Nutrition, a subdivision of multinational health conglomerate Abbott Laboratories that oversees the conglomerate’s formula business, controlled 40% of the baby-formula market in the U.S. at the time of its Michigan plant shutdown last year.

Public health organizations have for decades criticized formula makers for aggressively marketing their products to the detriment of breastfeeding. The World Health Organization last year detailed how big formula companies use aggressive marketing practices to promote the use of infant formula over breast milk, leaving many families dependent on commercial products and vulnerable to formula shortages. A series of papers published in the medical journal The Lancet this month describes what its authors call the commercial milk industry’s “underhand marketing strategies, designed to prey on parents’ fears and concerns, to turn the feeding of infants and young children into a multibillion-dollar business.”

Not six months ago, ether led a recovery in cryptocurrency prices ahead of a big tech upgrade that would make something called “staking” available to crypto investors.

Most people have hardly wrapped their heads around the concept, but now, the price of ether is falling amid mounting fears that the Securities and Exchange Commission could crack down on it.

On Thursday, Kraken, one of the largest crypto exchanges in the world, closed its staking program in a $30 million settlement with the SEC, which said the company failed to register the offer and sale of its crypto staking-as-a-service program.

“This should put everyone on notice in this marketplace,” SEC Chair Gary Gensler told CNBC’s “Squawk Box” Friday morning. “Whether you call it lend, earn, yield, whether you offer an annual percentage yield – that doesn’t matter. If someone is taking [customer] tokens and transferring to their platform, the platform controls it.”

Staking has widely been seen as a catalyst for mainstream adoption of crypto and a big revenue opportunity for exchanges like Coinbase. A clampdown on staking, and staking services, could have damaging consequences not just for those exchanges, but also Ethereum and other proof-of-stake blockchain networks. To understand why, it helps to have a basic understanding of the activity in question.

Here’s what you need to know:

What is staking?

Staking is a way for investors to earn passive yield on their cryptocurrency holdings by locking tokens up on the network for a period of time. For example, if you decide you want to stake your ether holdings, you would do so on the Ethereum network. The bottom line is it allows investors to put their crypto to work if they’re not planning to sell it anytime soon.

How does staking work?

Staking is sometimes referred to as the crypto version of a high-interest savings account, but there’s a major flaw in that comparison: crypto networks are decentralized, and banking institutions are not.

Earning interest through staking is not the same thing as earning interest from a high annual percentage yield offered by a centralized platform like those that ran into trouble last year, like BlockFi and Celsius, or Gemini just last month. Those offerings really were more akin to a savings account: people would deposit their crypto with centralized entities that lent those funds out and promised rewards to the depositors in interest (of up to 20% in some cases). Rewards vary by network but generally, the more you stake, the more you earn.

By contrast, when you stake your crypto, you are contributing to the proof-of-stake system that keeps decentralized networks like Ethereum running and secure; you become a “validator” on the blockchain, meaning you verify and process the transactions as they come through, if chosen by the algorithm. The selection is semi-random – the more crypto you stake, the more likely you’ll be chosen as a validator.

The lock-up of your funds serves as a sort of collateral that can be destroyed if you as a validator act dishonestly or insincerely.

This is true only for proof-of-stake networks like Ethereum, Solana, Polkadot and Cardano. A proof-of-work network like Bitcoin uses a different process to confirm transactions.

Staking as a service

In most cases, investors won’t be staking themselves – the process of validating network transactions is just impractical on both the retail and institutional levels.

That’s where crypto service providers like Coinbase, and formerly Kraken, come in. Investors can give their crypto to the staking service and the service does the staking on the investors’ behalf. When using a staking service, the lock-up period is determined by the networks (like Ethereum or Solana), and not the third party (like Coinbase or Kraken).

It’s also where it gets a little murky with the SEC, which said Thursday that Kraken should have registered the offer and sale of the crypto asset staking-as-a-service program with the securities regulator.

While the SEC hasn’t given formal guidance on what crypto assets it deems securities, it generally sees a red flag if someone makes an investment with a reasonable expectation of profits that would be derived from the work or effort of others.

Coinbase has about 15% of the market share of Ethereum assets, according to Oppenheimer. The industry’s current retail staking participation rate is 13.7% and growing.

Proof-of-stake vs. proof-of-work

Staking works only for proof-of-stake networks like Ethereum, Solana, Polkadot and Cardano. A proof-of-work network, like Bitcoin, uses a different process to confirm transactions.

The two are simply the protocols used to secure cryptocurrency networks.

Proof-of-work requires specialized computing equipment, like high-end graphics cards to validate transactions by solving highly complex math problems. Validators gets rewards for each transaction they confirm. This process requires a ton of energy to complete.

The source of return in staking is different from traditional markets. There aren’t humans on the other side promising returns, but rather the protocol itself paying investors to run the computational network.

Despite how far crypto has come, it’s still a young industry filled with technological risks, and potential bugs in the code is a big one. If the system doesn’t work as expected, it’s possible investors could lose some of their staked coins.

Volatility is and has always been a somewhat attractive feature in crypto but it comes with risks, too. One of the biggest risks investors face in staking is simply a drop in the price. Sometimes a big decline can lead smaller projects to hike their rates to make a potential opportunity more attractive.

The Securities and Exchange Commission on Thursday charged crypto firms Genesis and Gemini with allegedly selling unregistered securities in connection with a high-yield product offered to depositors.

Gemini, a crypto exchange, and Genesis, a crypto lender, partnered in February 2021 on a Gemini product called Earn, which touted yields of up to 8% for customers.

According to the SEC, Genesis loaned Gemini users’ crypto and sent a portion of the profits back to Gemini, which then deducted an agent fee, sometimes over 4%, and returned the remaining profit to its users. Genesis should have registered that product as a securities offering, SEC officials said.

“Today’s charges build on previous actions to make clear to the marketplace and the investing public that crypto lending platforms and other intermediaries need to comply with our time-tested securities laws,” SEC chair Gary Gensler said in a statement.

Gemini’s Earn program, supported by Genesis’ lending activities, met the SEC’s definition by including both an investment contract and a note, SEC officials said. Those two features are part of how the SEC assesses whether an offering is a security.

Regulators are seeking permanent injunctive relief, disgorgement, and civil penalties against both Genesis and Gemini.

The two firms have been engaged in a high-profile battle over $900 million in customer assets that Gemini entrusted to Genesis as part of the Earn program, which was shuttered this week.

Gemini, which was founded in 2015 by bitcoin advocates Cameron and Tyler Winklevoss, has an extensive exchange business that, while beleaguered, could possibly weather an enforcement action.

But Genesis’ future is more uncertain, because the business is heavily focused on lending out customer crypto and has already engaged restructuring advisers. The crypto lender is a unit of Barry Silbert’s Digital Currency Group.

SEC officials said the possibility of a DCG or Genesis bankruptcy had no bearing on deciding whether to pursue a charge.

It’s the latest in a series of recent crypto enforcement actions led by Gensler after the collapse of Sam Bankman-Fried’s FTX in November. Gensler was roundly criticized on social media and by lawmakers for the SEC’s failure to impose safeguards on the nascent crypto industry.

Gensler’s SEC and the Commodity Futures Trading Commission, chaired by Rostin Benham, are the two regulators that oversee crypto activity in the U.S. Both agencies filed complaints against Bankman-Fried, but the SEC has, of late, ramped up the pace and the scope of enforcement actions.

The SEC brought a similar action against now bankrupt crypto lender BlockFi and settled last year. Earlier this month, Coinbasesettled with New York state regulators over historically inadequate know-your-customer protocols.

Since Bankman-Fried was indicted on federal fraud charges in December, the SEC has filed five crypto-related enforcement actions.

Sam Bankman-Fried, the disgraced former CEO of collapsed cryptocurrency exchange FTX, has been formally indicted on charges of fraud, money laundering and others. The unsealed document reveals eight charges from the United States Southern District Court of New York, including:

Conspiracy to commit wire fraud on customers

Wire fraud on customers

Conspiracy to commit wire fraud on lenders

Wire fraud on lenders

Conspiracy to commit commodities fraud

Conspiracy to commit securities fraud

Conspiracy to commit money laundering

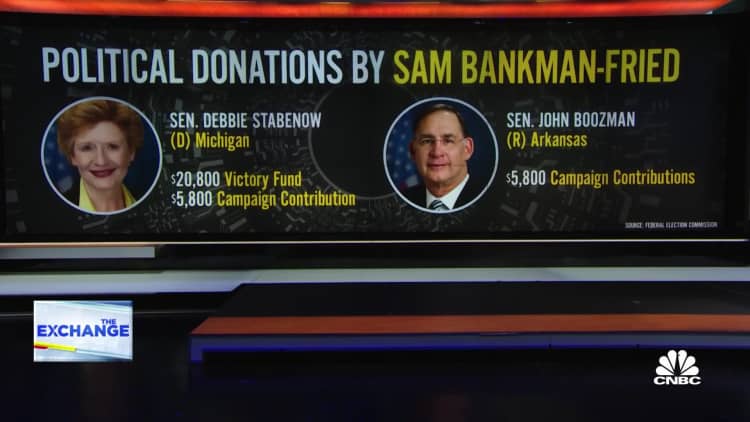

And conspiracy to defraud the United States and violate the Campaign Finance Laws.

This follows Bankman-Fried’s arrest on the night of December 12 in the Bahamas by local authorities, after they had received notification from the U.S. that it had filed criminal charges against SBF.

SBF was also charged with defrauding investors by the U.S. Securities and Exchange Commission, alleging that he diverted customer funds from FTX to Bankman-Fried’s Alameda Research fund while simultaneously raising $1.8 billion with investors.

In addition to the SEC and N.Y. Southern District Court’s charges, the CFTC also filed charges against SBF, Alameda Research and FTX for “fraud and material misrepresentations in connection with the sale of digital commodities.”

The collapse of FTX led to billions of dollars of lost customer funds which have yet to be recovered, and there is no guarantee that will happen. Both FTX and Alameda Research fund are undergoing bankruptcy proceedings. Today’s unsealed indictment shows that the Department of Justice is seeking any profits Bankman-Fried received from these ventures.

The House Financial Services Committee has commenced its investigation into the collapse of FTX, with the current CEO testifying. Bankman-Fried appeared this morning in front of Chief Magistrate Joyann Ferguson-Pratt in Nassau, during which he told the judge that he had not yet had the chance to speak to his lawyer.

FTX CEO Sam Bankman-Fried attends a press conference at the FTX Arena in downtown Miami on Friday, June 4, 2021.

Matias J. Ocner | Miami Herald | Tribune News Service | Getty Images

Sam Bankman-Fried, the disgraced former CEO of FTX — the bankrupt cryptocurrency exchange that was worth $32 billion a few weeks ago — has a real knack for self-promotional PR. For years, he cast himself in the likeness of a young boy genius turned business titan, capable of miraculously growing his crypto empire as other players got wiped out. Everyone from Silicon Valley’s top venture capitalists to A-list celebrities bought the act.

But during Bankman-Fried’s press junket of the last few weeks, the onetime wunderkind has spun a new narrative – one in which he was simply an inexperienced and novice businessman who was out of his depth, didn’t know what he was doing, and crucially, didn’t know what was happening at the businesses he founded.

It is quite the departure from the image he had carefully cultivated since launching his first crypto firm in 2017 – and according to former federal prosecutors, trial attorneys and legal experts speaking to CNBC, it recalls a classic legal defense dubbed the “bad businessman strategy.”

At least $8 billion in customer funds are missing, reportedly used to backstop billions in losses at Alameda Research, the hedge fund he also founded. Both of his companies are now bankrupt with billions of dollars worth of debt on the books. The CEO tapped to take over, John Ray III, said that “in his 40 years of legal and restructuring experience,” he had never seen “such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here.” This is the same Ray who presided over Enron’s liquidation in the 2000s.

In America, it is not a crime to be a lousy or careless CEO with poor judgement. During his recent press tour from a remote location in the Bahamas, Bankman-Fried really leaned into his own ineptitude, largely blaming FTX’s collapse on poor risk management.

At least a dozen times in a conversation with Andrew Ross Sorkin, he appeared to deflect blame to Caroline Ellison, his counterpart (and one-time girlfriend) at Alameda. He says didn’t know how extremely leveraged Alameda was, and that he just didn’t know about a lot of things going on at his vast empire.

Bankman-Fried admitted he had a “bad month,” but denied committing fraud at his crypto exchange.

Fraud is the kind of criminal charge that can put you behind bars for life. With Bankman-Fried, the question is whether he misled FTX customers to believe their money was available, and not being used as collateral for loans or for other purposes, according to Renato Mariotti, a former federal prosecutor and trial attorney who has represented clients in derivative-related claims and securities class actions.

“It sure looks like there’s a chargeable fraud case here,” said Mariotti. “If I represented Mr. Bankman-Fried, I would tell him he should be very concerned about prison time. That it should be an overriding concern for him.”

But for the moment, Bankman-Fried appears unconcerned with his personal legal exposure. When Sorkin asked him if he was concerned about criminal liability, he demurred.

“I don’t think that — obviously, I don’t personally think that I have — I think the real answer is it’s not — it sounds weird to say it, but I think the real answer is it’s not what I’m focusing on,” Bankman-Fried told Sorkin. “It’s — there’s going to be a time and a place for me to think about myself and my own future. But I don’t think this is it.”

Comments such as these, paired with the lack of apparent action by regulators or authorities, have helped inspire fury among many in the industry – not just those who lost their money. The spectacular collapse of FTX and SBF blindsided investors, customers, venture capitalists and Wall Street alike.

Bankman-Fried did not respond to a request for comment. Representatives for his former law firm, Paul, Weiss, did not immediately respond to comment. Semafor reported earlier that Bankman-Fried’s new attorney was Greg Joseph, a partner at Joseph Hage Aaronson.

Both of Bankman-Fried’s parents are highly respected Stanford Law School professors. Semafor also reported that another Stanford Law professor, David Mills, was advising Bankman-Fried.

Mills, Joseph and Bankman-Fried’s parents did not immediately respond to requests for comment.

Bankman-Fried could face a host of potential charges – civil and criminal – as well as private lawsuits from millions of FTX creditors, legal experts told CNBC.

For now, this is all purely hypothetical. Bankman-Fried has not been charged, tried, nor convicted of any crime yet.

Richard Levin is a partner at Nelson Mullins Riley & Scarborough, where he chairs the fintech and regulation practice. He’s been involved in the fintech industry since the early 1990s, and has represented clients before the Securities and Exchange Commission, Commodity Futures Trading Commission and Congress. All three of those entities have begun probing Bankman-Fried.

There are three different, possibly simultaneous legal threats that Bankman-Fried faces in the United States alone, Levin told CNBC.

First is criminal action from the U.S. Department of Justice, for potential “criminal violations of securities laws, bank fraud laws, and wire fraud laws,” Levin said.

A spokesperson for the U.S. Attorney’s Office for the Southern District of New York declined to comment.

Securing a conviction is always challenging in a criminal case.

Mariotti, the former federal prosecutor is intricately familiar with how the government would build a case. He told CNBC, “prosecutors would have to prove beyond a reasonable doubt that Bankman-Fried or his associates committed criminal fraud.”

“The argument would be that Alameda was tricking these people into getting their money so they could use it to prop up a different business,” Mariotti said.

“If you’re a hedge fund and you’re accepting customer funds, you actually have a fiduciary duty [to the customer],” Mariotti said.

Prosecutors could argue that FTX breached that fiduciary duty by allegedly using customer funds to artificially stabilize the price of FTX’s own FTT coin, Mariotti said.

But intent is also a factor in fraud cases, and Bankman-Fried insists he didn’t know about potentially fraudulent activity. He told Sorkin that he “didn’t knowingly commingle funds.”

“I didn’t ever try to commit fraud,” Bankman-Fried said.

Beyond criminal charges, Bankman-Fried could also be facing civil enforcement action. “That could be brought by the Securities Exchange Commission, and the Commodity Futures Trading Commission, and by state banking and securities regulators,” Levin continued.

“On a third level, there’s also plenty of class actions that can be brought, so there are multiple levels of potential exposure for […] the executives involved with FTX,” Levin concluded.

The Department of Justice is most likely to pursue criminal charges in the U.S. The Wall Street Journal reported that the DOJ and the SEC were both probing FTX’s collapse, and were in close contact with each other.

That kind of cooperation allows for criminal and civil probes to proceed simultaneously, and allows regulators and law enforcement to gather information more effectively.

But it isn’t clear whether the SEC or the CFTC will take the lead in securing civil damages.

An SEC spokesperson said the agency does not comment on the existence or nonexistence of a possible investigation. The CFTC did not immediately respond to a request for comment.

“The question of who would be taking the lead there, whether it be the SEC or CFTC, depends on whether or not there were securities involved,” Mariotti, the former federal prosecutor, told CNBC.

SEC Chairman Gary Gensler, who met with Bankman-Fried and FTX executives in spring 2022, has said publicly that “many crypto tokens are securities,” which would make his agency the primary regulator. But many exchanges, including FTX, have crypto derivatives platforms that sell financial products like futures and options, which fall under the CFTC’s jurisdiction.

“For selling unregistered securities without a registration or an exemption, you could be looking at the Securities Exchange Commission suing for disgorgement — monetary penalties,” said Levin, who’s represented clients before both agencies.

“They can also sue, possibly, claiming that FTX was operating an unregistered securities market,” Levin said.

Then there are the overseas regulators that oversaw any of the myriad FTX subsidiaries.

The Securities Commission of The Bahamas believes it has jurisdiction, and went as far as to file a separate case in New York bankruptcy court. That case has since been folded into FTX’s main bankruptcy protection proceedings, but Bahamian regulators continue to investigate FTX’s activities.

Court filings allege that Bahamian regulators have moved customer digital assets from FTX custody into their own. Bahamian regulators insist that they’re proceeding by the book, under the country’s groundbreaking crypto regulations — unlike many nations, the Bahamas has a robust legal framework for digital assets.

But crypto investors aren’t sold on their competence.

“The Bahamas clearly lack the institutional infrastructure to tackle a fraud this complex and have been completely derelict in their duty,” Castle Island Ventures partner Nic Carter told CNBC. (Carter was not an FTX investor, and told CNBC that his fund passed on early FTX rounds.)

“There is no question of standing. U.S. courts have obvious access points here and numerous parts of Sam’s empire touched the U.S. Every day the U.S. leaves this in the hands of the Bahamas is a lost opportunity,” he continued.

Investors who have lost their savings aren’t waiting. Class-action suits have already been filed against FTX endorsers, like comedian Larry David and football superstar Tom Brady. One suit excoriated the celebrity endorsers for allegedly failing to do their “due diligence prior to marketing [FTX] to the public.”

FTX’s industry peers are also filing suit against Bankman-Fried. BlockFi sued Bankman-Fried in November, seeking unnamed collateral that the former billionaire provided for the crypto lending firm.

FTX and Bankman-Fried had previously rescued BlockFi from insolvency in June, but when FTX failed, BlockFi was left with a similar liquidity problem and filed for bankruptcy protection in New Jersey.

Bankman-Fried has also been sued in Florida and California federal courts. He faces class-action suits in both states over “one of the great frauds in history,” a California court filing said.

The largest securities class-action settlement was for $7.2 billion in the Enron accounting fraud case, according to Stanford research. The possibility of a multibillion-dollar settlement would come on top of civil and criminal fines that Bankman-Fried faces.

But the onus should be on the U.S. government to pursue Bankman-Fried, Carter told CNBC, not on private investors or overseas regulators.

“The U.S. isn’t shy about using foreign proxies to go after Assange — why in this case have they suddenly found their restraint?”

Wire fraud is the most likely criminal charge Bankman-Fried would face. If the DOJ were able to secure a conviction, a judge would look to several factors to determine how long to sentence him.

Braden Perry was once a senior trial lawyer for the CFTC, FTX’s only official U.S. regulator. He’s now a partner at Kennyhertz Perry, where he advises clients on anti-money laundering, compliance and enforcement issues.

Based on the size of the losses, if Bankman-Fried is convicted of fraud or other charges, he could be behind bars for years — potentially for the rest of his life, Perry said. But the length of any potential sentence is hard to predict.

“In the federal system, each crime always has a starting point,” Perry told CNBC.

Federal sentencing guidelines follow a numeric system to determine the maximum and minimum allowable sentence, but the system can be esoteric. The scale, or “offense level,” starts at one, and maxes out at 43.

A wire fraud conviction rates as a seven on the scale, with a minimum sentence ranging from zero to six months.

But mitigating factors and enhancements can alter that rating, Perry told CNBC.

“The dollar value of loss plays a significant role. Under the guidelines, any loss above $550 million adds 30 points to the base level offense,” Perry said. FTX customers have lost billions.

“Having 25 or more victims adds 6 points, [and] use of certain regulated markets adds 4,” Perry continued.

In this hypothetical scenario, Bankman-Fried would max out the scale at 43, based on those enhancements. That means Bankman-Fried could be facing life in federal prison, without the possibility of supervised release, if he’s convicted on a single wire fraud offense.

But that sentence can be reduced by mitigating factors – circumstances that would lessen the severity of any alleged crimes.

“In practice, many white-collar defendants are sentenced to lesser sentences than what the guidelines dictate,” Perry told CNBC, Even in large fraud cases, that 30-point enhancement previously mentioned can be considered punitive.

Bankman-Fried could also face massive civil fines. Bankman-Fried was once a multibillionaire, but claimed he was down to his last $100,000 in a conversation with CNBC’s Sorkin at the DealBook Summit last week.

“Depending on what is discovered as part of the investigations by law enforcement and the civil authorities, you could be looking at both heavy monetary penalties and potential incarceration for decades,” Levin told CNBC.

In the most famous fraud case in recent years, Bernie Madoff was arrested within 24 hours of federal authorities learning of his multibillion-dollar Ponzi scheme. But Madoff was in New York and admitted to his crime on the spot.

The FTX founder is in the Bahamas and hasn’t admitted wrongdoing. Short of a voluntary return, any efforts to apprehend him would require extradition.

With hundreds of subsidiaries and bank accounts, and thousands of creditors, it’ll take prosecutors and regulators time to work through everything.

Similar cases “took years to put together,” said Mariotti. At FTX, where record keeping was spotty at best, collecting enough data to prosecute could be much harder. Expenses were reportedly handled through messaging software, for example, making it difficult to pinpoint how and when money flowed out for legitimate expenses.

In Enron’s bankruptcy, senior executives weren’t charged until nearly three years after the company went under. That kind of timeline infuriates some in the crypto community.

“The fact that Sam is still walking free and unencumbered, presumably able to cover his tracks and destroy evidence, is a travesty,” said Carter.

But just because law enforcement is tight-lipped, that doesn’t mean they’re standing down.

“People should not jump to the conclusion that something is not happening just because it has not been publicly disclosed,” Levin told CNBC.

Could he just disappear?

“That’s always a possibility with the money that someone has,” Perry said, although Bankman-Fried claims he’s down to one working credit card. But Perry doesn’t think it’s likely. “I believe that there has been likely some negotiation with his attorneys, and the prosecutors and other regulators that are looking into this, to ensure them that when the time comes […] he’s not fleeing somewhere,” Perry told CNBC.

In the meantime, Bankman-Fried won’t be resting easy as he waits for the hammer to drop. Rep. Maxine Waters extended a Twitter invitation for him to appear before a Dec. 13 hearing.

Bankman-Fried responded on Twitter, telling Waters that if he understands what happened at FTX by then, he’d appear.

Correction: Caroline Ellison is Bankman-Fried’s counterpart at Alameda. An earlier version misspelled her name.

SEC, CFTC reportedly probing FTX over handling of customers’ funds.

Investigations also relate to lending.

SEC probe reportedly predates Binance’s acquisition of FTX.

U.S. financial regulators have apparently been actively following the carnage that’s ensued in cryptocurrency markets over the past couple of days.

According to a report by Bloomberg, people familiar with the matter said the Securities and Exchange Commission and the Commodity Futures Trading Commission are investigating the liquidity crunch at FTX that led to its non-U.S. operations being acquired by competitor Binance, the world’s largest exchange, on Tuesday.

What started as apparently a clash between crypto’s two wealthiest founders quickly spiraled into a deal between them to save FTX from collapse. Binance CEO Changpeng Zhao announced his company would be offloading half a billion dollars worth of the rival’s native token, FTT, which triggered a sharp selloff of the token and culminated in FTX’s Sam Bankman-Fried being rescued out of a “liquidity crunch.”

The regulatory agencies are probing FTX over how it handled customer funds, apparently a key component of the exchange’s liquidity situation.

Watchdogs also seemingly worry about how much of an impact the buyout will have on FTX’s U.S. operations. According to a financial policy analyst at $15.8 billion Cowen, the deal could be treated as a matter of national security by American regulators.

Regulators also seem to be keenly interested in learning more about the flow of funds between two of Sam Bankman-Fried’s businesses, FTX and Alameda.

Hand is turning a dice and changes the direction of an arrow symbolizing that the value of the … [+] crypto currency Ethereum (ETH) is going up (or vice versa)

getty

The week after the Securities and Exchange Commission settled charges against Kim Kardashian for (allegedly) illegally promoting a cryptocurrency, JPMorgan Chase JPM and Ye (formerly Kanye West), much like Kim and Ye, wenttheir separate ways. For very different reasons, both moguls’ mishaps provide an opportunity to discuss what’s wrong with financial market regulation in the United States.

The problems go much deeper than just legacy securities and banking regulation. They even bleed over to the newly forming fintech industry.

While it very well may have been JP Morgan’s intent to steer clear of political controversy by dropping Kanye West as a client, it remains unclear exactly what West did to anger JP Morgan. (For what it’s worth, it does appear that JP Morgan sent their letter to Ye before his recent controversial comments.) Perhaps all the clickbait headlines caused him to launch an alarming anti-inflation tirade in JP Morgan’s headquarters.

But it’s not surprising that some people suspect political motives could be behind the breakup. (Between JP Morgan and Ye, not Kim and Ye.) Again, I have no idea what truly happened and I’m not defending anything he may have said or done.

Regardless, as I’ve pointedout before, the much bigger threat to Americans is how much power federal regulators have over banks, not whether banks can ditch their customers.

Federal regulators can ultimately revoke banks’ federal deposit insurance and shut them down. If regulators deem, for example, that lending to fossil fuel companies puts a bank’s reputation at risk, or that doing so constitutes an unsafe or unsound practice, they can force the bank to change who it does business with. They have enormous leverage to do so.

That sort of leverage has many climate change activists excited, but they should reconsider. As soon as people with different views run the agencies, the very same authority could be used to target today’s popular activities and activists. The United States has spent decades leading most developed nations down the same path, discounting fundamental principles in the name of preventing mistakes, financial crises, money laundering, tax evasion, and terrorist financing.

Federal regulators could easily use their authority to target groups engaged in constitutionally protected political protests. (Fourth Amendment protections, for example, have been severely watered down.)

The details of Kim Kardashian’s mishap are a bit different, especially in that they involve a capital markets regulator.

As reported by the Wall Street Journal, the SEC believes that Kim Kardashian violated securities laws when she used her Instagram page to promote a crypto token (EMAX) without disclosing that she was paid $250,000 for the post. Sometime after her post, EMAX lost most of its value.

To be extra clear: The problem isn’t that EMAX took a deep nosedive, or that Kim promoted a crypto token which (according to the SEC) is a security. The problem is that she didn’t disclose she was being paid to promote EMAX.

Section 17(b) of the Securities Act of 1933 requires any person who gives publicity to the sale of a security to disclose any compensation for doing so. The SEC has enforced this anti-touting rule aggressively, bringing cases against people who have published entirely accurate internet posts about companies in return for undisclosed benefits.

The jurisdictional limits of the SEC allow it to go after her [Kim Kardashian] and Floyd Mayweather, while Matt Damon’s Super Bowl ad for Crypto.com, part of a $65 million campaign, escapes enforcement because it was promoting a platform and not a security.

Setting all these technical and legal arguments aside and ignoring whether securities laws might provide a false sense of security, the bigger problem here is that federal officials have overly broad discretion to act in the name of “protecting” people from making “bad” investment choices. In other words, a guiding principle behind federal securities laws is that federal officials need to prevent Americans from making mistakes and losing money. The SEC has gone way past prosecuting fraud.

Congress should not have given securities regulators so much discretion and it should not have based securities laws on these principles. The same critique applies to U.S. banking law. What Americans have, though, is a complex web of rules and regulations that blunts innovation and competition, as well as the ability to raise private capital.

In the extreme (not theabsurd), the result of this kind of regulatory system is that government officials can allocate credit to politically favored interests.

So, Congress should rethink these principles, but that’s not what they’re doing. Instead, these same ideas, and these same harmful outcomes, are playing out right now as the House tries to craft new stablecoin legislation.

For months, Financial Services chair Maxine Waters (D-CA) and ranking member Patrick McHenry (R-NC) have been negotiating a bill to regulate stablecoins. Negotiations seem to have broken down, and based on the discussion draft, that’s probably a good thing.

During DC Fintech Week, Yahoo!reported that McHenrytold his audience “It [the bill] doesn’t look like a modern regulatory regime. It actually looks pretty retrograde.” He then characterized the “current status of the legislation as an ‘ugly baby,’” and added that “It is a baby nonetheless, and we’re grateful and hopeful it can grow and prosper into something that is a lot more attractive.”

As I and my fellow Cato scholars wrote in early October, the “best part of the draft is that the House…is not trying to enact the President’s Working Group recommendation to ‘require stablecoin issuers to be insured depository institutions.’” The problem, though, is that Congress is arguing over which assets stablecoins should be backed with, who can hold stablecoins, what people can do with stablecoins in their own digital wallets, and which regulator should be in charge.

Congress should write laws to protect Americans from fraud and theft. But that goal does not require Congress to dictate which assets can legally back stablecoins. Let fintech companies and other financial firms experiment, and let people take risks with their own money. Most people aren’t going to use something called a stablecoin if it isn’t stable, so anyone issuing stablecoins better figure out how to make them stable.

Moreover, Congress should not protect legacy firms or the best-connected upstart firms from competition. That’s how free enterprise breaks down, not how it works best for the largest number of people.

Hopefully, McHenry’s wish comes true, and Congress comes up with a bill that’s much more attractive.

Unfortunately, that outcome is wishful thinking unless Congress changes its underlying approach. This time, though, a misstep is likely to keep the U.S. payments system stuck somewhere in the 20th century while the rest of the world races ahead. With or without Kim and Ye.