A car drives through high water from the effects from Hurricane Ian, Friday, Sept. 30, 2022, in Charleston, S.C. Alex Brandon/AP Photo

Besides leaving a path of death and destruction in its wake, Hurricane Ian has another legacy: Catastrophic flooding potentially damaged more than 350,000 vehicles, according to new estimates from Carfax.

Car shoppers need to be aware that these waterlogged vehicles will soon be showing up — in disguise — all over the country. Some shady used car lots (imagine that!) will illegally try to hide these flood-damaged vehicles by obtaining new titles for them, passing them off as pristine.

“Cosmetically these cars might look great, but if you don’t know what to look for, it’s nearly impossible to tell they’re literally rotting from the inside out,” Carfax spokeswoman Emilie Voss said in a press release. “Flood water can cause mechanical, electrical, health and safety issues in a vehicle, even if it was submerged for only a short time.”

Inevitably, thousands and thousands of these cars will be resold to unsuspecting buyers, like the roughly 400,000 flood-damaged cars that Carfax estimates are currently on the road — mostly from other recent hurricanes.

How can you protect yourself if you’re buying a used car? Don’t worry, we’ve got your back.

Flood-Damaged Vehicles: Not Just a Southern Problem

This isn’t just a problem in southeastern states that typically get hit by hurricanes.

Texas and Florida — hurricane magnets — lead the nation when it comes to the number of flood-damaged cars on the road. But Carfax finds that these vehicles also show up in states where hurricane flooding isn’t exactly an issue.

Carfax’s data shows these 10 states have the most flood-damaged autos:

States With the Most Flood-Damaged Autos

State

Flood-Damaged Vehicles

Texas

67,000

Florida

33,500

Kentucky

26,000

Pennsylvania

21,500

New Jersey

18,800

North Carolina

15,600

New York

14,600

California

14,200

Illinois

13,300

Michigan

11,400

Many of these flooded cars are the legacy of Hurricanes Harvey and Irma, which hit Texas and Florida in 2017; and Hurricane Ida, which hit Louisiana in 2021 but also caused massive flash flooding throughout the Northeast.

After Ida passed through, New Jersey and New York saw the biggest one-year spikes in the number of flood-damaged cars, according to Carfax.

How to Avoid Buying a Flood-Damaged Used Car

We rounded up helpful tips from Carfax, the auto inventory website Edmunds and other experts to help you avoid purchasing a vehicle that’s been damaged by flood waters.

Buy From a Reputable Dealer

To avoid being swindled into purchasing a flood-damaged used car, your safest bet is to buy from a trusted dealership. These dealers have a reputation to uphold and will likely provide you with a detailed vehicle history report.

A vehicle history report will include tons of relevant information, like states in which the car has been registered. Edmunds also recommends a cheap ($7 or less) report from the National Motor Vehicle Title Information System, which will detail whether the car has been salvaged, among other key points.

At carfax.com/flood, Carmax has a free “Flood Check” tool where you can simply type in the car’s VIN. It also has a flood damage checklist and a national map that shows where flooded cars are washing up.

Trust Your Senses, but Also a Mechanic’s

When you’re inspecting a used car, watch out for these red flags:

Foul odors, particularly mold and mildew. These smells can signal that a car has been in standing water for a prolonged amount of time.

Discolored carpeting or rusted metal. Stains in carpeting or seat fabrics are also indicators of standing water. Rust on the body or the undercarriage is a sign of excessive water exposure, particularly in newer cars.

Inexplicable dirt build-up, like in the trunk or along the seat tracks. This is a sign that mud got into places where muddy feet typically do not travel.

Water build-up in headlights and taillights. Fogginess in the lighting can also be a sign of prolonged water exposure.

Mismatching parts, like seat materials compared to floor mats. A clever seller may replace a damaged floor mat, hoping you won’t notice that it isn’t a perfect match to the other mats or the seat fabric.

As an added precaution, have a trusted mechanic give the vehicle a once-over before you sign on the dotted line. Avoid any seller who’s uncomfortable with you taking the car to a mechanic.

If you do suspect a dealership or private seller of knowingly selling a flood-damaged vehicle, contact your local authorities or the National Insurance Crime Bureau.

Follow These Tips Every Time

When it comes to used cars, all of this is actually good lifelong advice. Hurricanes Harvey, Irma, Ida and Ian have put hundreds of thousands of flood-damaged vehicles into our nation’s used car lots and onto our roads.

From the looks of things, they won’t be the last major hurricanes to threaten the U.S. this decade. Global warming and all that.

But especially if you’re buying a used vehicle in the next year or so, be on the alert for flooded-out cars.

Mike Brassfield ([email protected]) is a senior writer at The Penny Hoarder. Freelance writer Timothy Moore contributed to this article.

If you’re looking for a way to cut food costs and still eat well, going vegetarian could be the solution — especially if you know what to cook.

Fortunately, we’ve come up with some tasty budget-friendly meatless recipes that you can find by shopping at Trader Joe’s.

It’s not as if being a vegetarian is a new concept — or a fringe idea. Nearly one in four Americans reported eating less meat in the previous year, according to a 2019 Gallup Poll.

And with food prices steadily rising, cutting food costs could offer a major way to save. (Also check out this article on additional ways to save on food costs.)

By incorporating simple ingredients you can find at Trader Joe’s, these vegetarian recipes can help prevent you from getting bored with your food — or breaking the bank.

7 Trader Joe’s Vegetarian Recipes for the Budget Foodie

We’ve found some delicious ways to make simple meatless dishes, whether you’re a committed vegetarian or simply trying to eat less meat than you usually do.

Going vegetarian doesn’t have to mean going all-in organic (though you can check out these seven ways to save on organic food) or spending a bundle on fancy meat substitutes.

To make meals healthy but still delicious, simply include a protein-rich food and look for ways to incorporate vegetables or fruit in every meal.

Here are seven of our favorite meals to make after a shopping trip to Trader Joe’s.

1. Cauliflower Fried “Rice”

Trader Joe’s does the hard part for you — it sells cauliflower that is already “riced” in the frozen vegetable section. Cook the riced cauliflower with minced garlic, ginger, turmeric and salt and pepper. (Trader Joe’s even sells already-prepared frozen vegetable fried rice for $3.)

From there, add your favorite vegetables or whatever you have in your freezer or fridge — think: carrot, celery and onion. You can toss in a scrambled egg for extra protein.

Cauliflower fried rice is surprisingly filling, especially when served with tofu for a protein boost. You’ll get several servings of vegetables with this meal and lots of vitamin C from the cauliflower.

2. Quinoa Cowboy Veggie Burgers With Fries

Although the Trader Joe’s Quinoa Cowboy Veggie Burgers don’t pretend to taste like meat, they’re a pretty good substitute when you’re having a burger craving.

Inspired by cowboy caviar, the patties are filled with quinoa, black beans, peppers and roasted corn. Serve on a whole wheat bun for a boost of fiber, and skip the fries in favor of veggies (or veggie fries!) to make the meal healthier.

You can load up the burger with a tomato, sauteed onion, mayonnaise and cheese — or whatever toppings you’re craving.

This burger is lower in protein (it only has 5 grams on its own; the bun has 5 grams too), but it’s an easy, healthy vegetarian option.

3. Greek Yogurt Parfait

Greek yogurt has an unbelievable amount of protein. The nonfat version has 15 grams in one serving — that goes a long way toward your daily intake. Buy the unflavored Greek yogurt to avoid too much added sugar, then add honey to sweeten to taste. From there, add your favorite toppings; we recommended blueberries and granola.

This Greek yogurt parfait is perfect for breakfast, lunch, snacks — whenever. It resembles a dessert but is seriously protein-packed, and it even has a serving of fruit.

4. Kale and Chickpea Salad

Even if you’re a vegetarian, salads can get a bit boring — and some veggies get a bad rap, like kale. The key is in how you prepare it. Before dressing the salad, go through the kale leaves to remove hard stems.

After rinsing, add a small spoonful of olive oil and gently massage the kale to break it down and remove bitterness. Start with more kale than you want to end up with, because after you’re done massaging it, it shrinks to nearly half its size.

The ingredients for this kale and chickpea salad can be found at Trader Joe’s. The total is $11.26 for four servings. Tina Russell/The Penny Hoarder

Now, the best part. Pour Trader Joe’s Goddess Dressing, a creamy Greek dressing, over the greens (not too much!). Stir to combine. Then top with chickpeas and shredded parmesan cheese. Add salt and pepper to taste. Now, enjoy the best salad you’ve ever had.

5. Tofu and Vegetable Biryani

This is an easy meal to make, but it still packs protein and vegetable servings. It’s the ultimate lazy dinner meal — you can make it in the microwave in under four minutes.

If you’re wondering, “What’s biryani?” It’s a mixed rice dish from India that can have vegetables, meat, eggs or potatoes.

Combine it with Trader Joe’s Sriracha Baked Tofu for protein and to make it a full meal.

Beware of the high sodium content — especially if you’re adding a sauce. This meal will give you 20 grams of protein per serving.

6. Brussels Sprouts With Sweet Potato

For this recipe, pour maple syrup and soy sauce over the Brussels sprouts and then oven-bake until they’re crispy (about 25 minutes at 400 degrees).

Once they’re done, add a sprinkling of goat cheese. The creaminess of the cheese complements the crunchy, sweet flavor of the glazed Brussels sprouts perfectly.

This meal is surprisingly filling, so just add a baked sweet potato to enhance the sweet flavor and add some diversity — and a huge dose of vitamins — to your plate. If sweet potatoes aren’t your thing, cook these Brussels sprouts as a side and add to your other favorite meals.

Brussels sprouts

Goat cheese

Sweet potato

7. Honorable Mention: Tikka Vegetables and Naan Bread

OK, this isn’t the healthiest lunch in the world, but it is quite delicious. Whenever it’s cooking, someone is bound to note how good it smells.

Watch your sodium on days you make these — like most frozen foods, Trader Joe’s Tikka Vegetables contains an unhealthy amount, especially coupled with other processed food. But it’s a nice treat packed with health-benefiting spices, veggies and 4 grams of protein.

It heats up quickly in the microwave and is good to have on hand for emergency lunch situations. If the tikka veggies alone isn’t usually enough to keep you full through dinner, crisp up garlic naan bread in the oven (another 7 grams of protein, and a good source of fiber!) or add on some vegetable samosas (4 grams of protein). This meal is fast and comes in at a few bucks per serving.

Joline Buscemi is a contributor to The Penny Hoarder. Senior editor Johna Strickland contributed.

When someone posted a blood type test kit on a local Buy Nothing Facebook group in Queens, NY, they may have wondered if anybody would want it.

Someone did.

“I think it was leftover from one of those food diet things where you find out what’s best to eat for your blood type,” said Sheri Sayles, who responded to the post and picked up the test kit from her neighbor.

This transaction was part of the gift economy — a way to exchange random items you don’t want with your neighbors who might have a use for them. It’s all free.

Buy Nothing groups on Facebook, the Nextdoor website and app, and other online platforms exist in neighborhoods across the country, helping people get free stuff online — sometimes stuff they never knew they needed.

What is a Buy Nothing Group?

The first question you might have while reading all of this is a simple one: What exactly is a Buy Nothing group?

The initiative started from humble beginnings: Two friends in Bainbridge Island, Wash., began the Buy Nothing Project in July 2013, aiming to save people money and reduce waste. It has since grown to more than 7,500 communities and 6.5 million members, per the project’s website.

Their mission is all about community and gifting: neighbors in hyperlocal areas post what they have to offer and ask for what they need.

While the project initially ran everything through Facebook groups, the company transitioned in recent years to an in-house app, called the BuyNothing app. The platform comes with some distinct benefits: first, users can set their preferred geographic distance, from one mile to six miles. Unlike Facebook, there is no requirement to approve users, eliminating at least a few delays.

But fret not: if you’re a beloved user of Facebook groups, Buy Nothing still exists on the platform. In fact, the site maintains a directory of its groups based on country and state. You can easily find the group closest to you.

How Do They Work?

The basic idea is simple. Someone posts something they want to give away and another person responds if they want it. You can also post when you’re looking for something specific in hopes a neighbor might have it.

But in practice, it isn’t always so clear-cut, especially for high-quality items.

“When you post something, people will then say, ‘I’m interested, I want it, this is why I want it.’ Then you don’t necessarily select the first person who responds. You wait for people to respond in like a 24-hour period and then you select from that list,” said Robin Eiseman, a member of the Buy Nothing group in her Philadelphia neighborhood of Fairmount.

She uses a random number generator to pick who receives her items, but not everyone does.

“I wanted to be as fair and impartial as possible,” Eiseman said.

According to the rules of Buy Nothing, people can only be in one group based on the address where they physically live. The organization also operates under a strict set of community guidelines, found here. First and foremost, posts are separated into three different categories: gifts that must be given for free either to share, to loan or to completely give away. Second is an asking post that asks group members whether they have something to share, loan or give that you need. And third, a post of gratitude is allowed that simply offers gratitude for the community.

Other neighborhood platforms with similar services have seen the demand for free products skyrocket in recent years. Nextdoor, for example, reported that the number of free listings has almost doubled in 2020 since the beginning of the year, which may be a result of the decluttering spree the pandemic has wrought.

What Else is Available (Besides Free Blood Test Kits)?

The Buy Nothing project breaks down possible gifts into categories, and they’re not all items. Members can give gifts of self or talent, which includes things like cooking classes, tutoring or offering rides for an appointment or an evening of babysitting for free. They can also offer what you might expect: gifts of stuff, miscellaneous items that are no longer of use to their owner but might be of use to you.

Nextdoor reports that the most popular categories are usually furniture, garden, and baby and kids items. But 2020 brought with it some changes.

“Throughout 2020 with the COVID-19 pandemic, we’ve observed an increase in requests for items related to DIY projects as people are sheltering in place and taking care of their household projects to do list,” Angold said.

Eiesman has gotten rid of things like a water bottle holder for a kayak that was the wrong size, extras from a monthly subscription box she didn’t care for, a printer that didn’t work (though she told people it didn’t work) and more.

“I’ve picked up from other people some really random stuff like ginger beer, Girl Scout cookies and lots of different things” she said.

After her father died, Sayles gave away some of his things like two nice television sets and some healthcare items.

“I recently posted that I had some sort of adult underwear, and like 10 people wrote to me that they would like it. So here’s something I would think nobody would ever want … and there’s 10 people who need it, so it has been a very good thing.”Sayles said.

Using a Buy Nothing Group vs. Giving Items Away: The Pros and Cons

If you’re reading this and wondering why you shouldn’t just pack up all your stuff and give it away to the nearest nonprofit or thrift store, consider these pros and cons before taking your latest dump to the, well, dump.

Pro: Buy Nothing groups are limited to a local radius, so there’s a higher chance that someone nearby will want your things and get them quickly.

Con: Buy Nothing groups aren’t necessarily about the fastest bidder, so you may have to wait some time to make a decision on who gets your item if you’re in it to be fair.

Pro: Both Eiseman and Sayles say getting rid of items this way is often easier for them than donating them because of limited storage space and the fact people come to pick the items up.

“Many organizations receiving item donations are flooded right now and can’t accept more inventory,” Angold said. “[Nextdoor] For Sale & Free allows members gifting items to get the item in front of thousands of nearby neighbors instantly.”

Con: You’ll have to be responsive. Even if you’re giving your items away for free, people generally have a few questions. What condition is it in? What are its measurements? Be prepared to monitor your social media for a little while. This is a good deed that doesn’t quite go unpunished.

Pro: There’s a certain sense of safety associated with these groups.

“Nobody puts their address on the actual Facebook page [for Buy Nothing]. It’s all done through Messenger,” Sayles said. “I feel perfectly safe, and they’re neighbors generally so you know you see them on the neighborhood Facebook group.”

Nextdoor works to create a sense of security by requiring transparency.

“Since day one, Nextdoor has required people to use their real name and verified address, so members can trust that their Nextdoor neighborhood is made up of real people at real addresses,” Angold said. “Additionally, proximity is incredibly powerful given the current situation. While neighbors around the world are staying closer to home, it becomes increasingly important to have a trusted community to rely on.”

Pro Tip

There’s always the option of meeting someone in a public place to exchange items.

Con: There’s no guarantee someone will take your item. Yes, there’s technically a home out there for everything, but this is not a church thrift shop. It’s essentially an online marketplace—albeit a free one.

Free Exchanging Advice

Veterans of no-sell groups say there are some general do’s and don’ts to follow.

Do: Be creative. Your trash might be someone else’s treasure. “The interesting thing is people post and say, ‘I’m sure nobody wants this but’ and then 30 people say ‘I’ll take it,’” Sayles said.

Don’t: Give away junk. Make sure what you’re giving away is in working order. If it isn’t, let people know that. Giving away junk wastes everyone’s time. “Upload multiple photos with different angles to showcase all the features of your item,” Angold suggests.

Don’t: Offer or ask for anything illegal. Both platforms have lists of what can and cannot be given away. Anything illegal isn’t allowed.

Do: Respond quickly. Like good news, good stuff travels fast. So if it’s something you want, respond as soon as you see it.

Don’t: Take your sweet time picking up your items. People are posting items because they want it out of their houses. If you claim something, go get it as soon as you can.

Do: Be gracious. These are real people behind computer screens. “Not everybody’s going to get the item that they want, and that’s okay. It’s not personal when people decide to give it to one person over another. They’re your neighbors. Don’t do stuff that is going to anger your neighbors. You have to live next to them,” Eiseman advises. Be civil and do not discriminate.

Don’t: Post when no one is online. “Most transactions happen on the weekend, so posting around that time frame is best for visibility,” Angold advises.

Do: Respect the administrators—and everyone. These people are volunteers and neighbors. Treat them as if you will see them again.

Ultimately, the whole idea isn’t just to get things for free.

“[Many people would] rather reuse something instead of going out and buying something new,” Eiseman said. “It’s not a matter of being cheap, but it’s kind of like, well, if you’ve got this and you don’t want it anymore instead of throwing it out, I’m happy to take it.”

Sayles agreed. “I have too much stuff and everyone else has too much stuff and we’re sharing our stuff. It’s great. It’s a very good way to keep it out of the landfill.”

Tiffani Sherman is a Florida-based freelance reporter with more than 25 years of experience writing about finance, health, travel, real estate, and other topics.

Writer Elizabeth Djinis is a contributor to The Penny Hoarder, often writing about selling goods online through social platforms. Her work has appeared in Teen Vogue, Smithsonian Magazine and the Tampa Bay Times.

The cost of living is going up and up thanks to inflation, which rose 8.2% in September compared to the previous year.

You’ve likely felt the financial pinch at the grocery store and when making other everyday purchases.

If you’re looking to stabilize your rising costs, you’re going to have to think a bit differently about the way you shop.

14 Savvy Ways to Fight Price Inflation

Here are savings tips to help you fight price inflation on everyday purchases.

1. Shop Your Pantry

Before you go grocery shopping, make a habit of checking the shelves of your pantry first. Canned goods, pasta and other pantry staples have a tendency to get forgotten in dark corners.

By taking inventory of what you already have at home, you’ll avoid mistakenly buying multiples of the same item. You might be able to shorten your grocery list (and spend less). You’ll also reduce the chance of food going bad before you remember to eat it.

Try a pantry challenge to use up what you’ve already got at home instead of going out and buying overpriced groceries. Don’t just limit your challenge to pantry items. Check what you’ve got in the freezer and what toiletries you already have before buying more of the same stuff.

2. Comparison Shop Before You Head to the Grocery Store

Prices for individual products can vary wildly between retailers, so you can save a lot by switching to the store that charges least for your staples.

After creating a list of your household’s needs, use one of these supermarket comparison spreadsheets or apps to get the most bang for your grocery budget buck — no matter what’s on your list.

3. Do Meal Prep

Planning out your meals and making grocery lists based on a meal plan means you’ll be less likely to waste money on something that looks good in the store but you never get around to eating.

This expert meal prep advice simply lays out how to get started planning your meals in advance.

4. Minimize Food Waste

When you’re paying more for food, the last thing you want is to let it go to waste. It’s like throwing your hard-earned cash in the trash.

Use these tips to reduce food waste so you’ll never have to toss out moldy cheese or stale bread again.

5. Choose Store Brands Over Name Brands

Name brand groceries are already priced higher than their store brand counterparts. And many times, you can barely tell the difference between the two.

With prices going up, switch to generic brands to lower your grocery spending. You may even discover a new favorite.

6. Buy in Bulk

While you’ll pay more money upfront for stuff in larger quantities, it’s actually a smart move to buy in bulk. Typically, you’ll pay less per item.

If you don’t need a three-box bundle of cereal or 10 pounds of macaroni noodles, you could always split your shopping haul with a friend or family member. Or you could just use this as an excuse to do less grocery shopping throughout the month.

7. Cut Back on Meat

Cutting back on meat will have a significant impact on your grocery bill, because beef and pork and chicken tend to be some of the more expensive items in the store — inflation or not.

Going meatless a day or two a week and turning to cheaper alternatives, like beans and lentils, can help you cut costs.

8. Save Money on Produce

Even with prices going up, you can still find ways to save on fruit and vegetables — without growing them in your backyard.

Which is better: Buying something for $5 that you use once and throw away, or purchasing something similar for $10 but that you can reuse over and over again?

Reusable products cost more upfront than their disposable counterparts, but they’re usually a better deal because they last much longer. Being better for the environment is an added plus.

The price at the pump has been on a bit of a roller coaster, whether it’s a production cutback or due to the ongoing war between Russia and Ukraine. And you still have places to go — which means gas is an essential.

Carpooling to the office can help you cut costs. So can signing up for fuel reward programs or using fuel comparison apps to find the lowest gas prices around. This article on how to save on gas has additional advice to lower your spending even as prices rise.

Looking for a credit card that earns you discounts on fuel and puts cash back in your pocket? We rounded up the best gas credit cards.

11. Share Tools and Equipment

Splitting the cost of something you’ll only use occasionally is a better deal than paying full price for something that’ll end up collecting dust most of the time.

Consider sharing pricy tools and equipment — like a stand mixer or a leaf blower — with a neighbor or nearby friend or family member.

12. Learn to Barter

You can also fight price inflation by choosing to barter with a friend or family member, rather than paying full price for goods and services.

Perhaps a friend has extra lumber from a home renovation that you can use in exchange for doing free graphic design work for their small business. Or maybe you can dog sit for a family member while they’re out of town in exchange for a few free meals.

13. Get Free Things from a Buy-Nothing Group

Getting free items from a local Buy Nothing Group, means you can bypass high prices at a store — and you don’t even have to offer up anything in exchange. These groups focus on donations rather than trading or bartering.

Join your local Buy Nothing Group on Facebook.

14. Fight Shrinkflation

“Shrinkflation” is a term coined to describe when companies reduce the size of a product but keep the price the same — it’s companies’ way of still carving out a profit when their production costs rise. You can beat shrinkflation by simply paying more attention while shopping and be willing to change up your habits to become a savvy shopper.

Nicole Dow is a former staff writer at The Penny Hoarder. Deputy editor Tiffany Wendeln Connors updated this post.

A Goodwill store sign is shown in Berkeley, Calif., Tuesday, March 9, 2021. Goodwill Industries International Inc., the 120 year-old non-profit organization that operates 3,300 stores in the U.S., and Canada, has launched an online business as part of a newly incorporated recommerce venture called GoodwillFinds. Jeff Chiu/AP Photo

In big news for thrifters everywhere, Goodwill is going digital. It’s launching GoodwillFinds, a new website that allows you to browse through roughly 100,000 pieces of secondhand merchandise from the comfort of your couch.

Instead of making your way to one of Goodwill’s 3,300 stores, now you can just click on your favorite bargains and have them shipped to you. Because your purchases will come from Goodwill locations across the U.S. and Canada, the shipping costs for each item will vary — but they’ll never be a surprise. At checkout, you’ll be offered shipping options based on your address.

The goal is to list a million items on the site within a few years, said Matthew Kaness, the website’s CEO. Eventually, the plan is for GoodwillFinds to be personalized for shoppers based on each customer’s previous purchases on the site.

For now, there’s a search bar, and you can also browse by category. Do you need women’s clothing, men’s clothing or shoes? Cookware, jewelry or books? Home decor? Collector’s items? It’s all there.

When people donate their secondhand stuff to Goodwill stores, workers will decide which things to list online. They’ll inspect each item, and if it’s dirty or in bad shape, they won’t try to sell it.

Goodwill also says they’ll accept returns for purchases that arrive damaged, or if there’s an incorrect item in your order. GoodwillFinds takes major credit cards and PayPal, but not Apple Pay.

The new website is the brainchild of a coalition of Goodwill leaders from across the country who wanted to bring Goodwill fully into the digital age. It’s an improvement over Goodwill’s previous internet offering, an auction site called ShopGoodwill (which is still operating). You can’t just click-and-purchase on that site — you have to bid on items.

This new Goodwill shopping site comes just in time for the holiday shopping season, too.

And although we’re big fans of putting together affordable Halloween costumes, you’ll need to place your online order for spooky stuff by Oct. 20, according to the website. After that, you’ll need to go to Goodwill in person to throw together a cheap zombie or rocker costume.

Goodwill is a 120-year-old nonprofit organization, the granddaddy of thrift shops everywhere. When you buy from Goodwill — or from GoodwillFinds — the proceeds help fund Goodwill’s community-based social service programs across the U.S. and Canada, like youth mentorship, job placement and professional training.

Also, it’s a good way to save a buck or two.

Mike Brassfield ([email protected]) is a senior writer at The Penny Hoarder.

‘Tis the season for the pumpkin spice latte, or PSL, for short. Starbucks, Panera, Krispy Kreme and a slew of other chains and local coffee shops are serving up the fall favorite.

And it’s got a cult following.

Just how popular is the orange gourd? Pumpkin products — from muffins to pancakes to lattes — brought in $522 million last year, according to Nielsen research. That was a 4.7% increase from the year before.

While “skipping the Starbucks” and other seasonal splurges, are often touted as a way to save money, you can still enjoy this fall rite of passage without blowing your budget. Here’s how to save money on pumpkin spice lattes all autumn long.

How to Save Money on Pumpkin Spice Lattes

1. Join Starbucks Rewards

Join Starbucks Rewards to start getting free drinks — including PSLs. Earn one star per $1 you spend. When you have 150 stars, you can redeem them for a free PSL or any handcrafted drink of your choice.

While that may seem like a good chunk of change to spend to get a reward, remember that it’s pretty easy to rack up a bill at Starbucks without even realizing it. That extra shot of espresso, added flavor and morning bagel all come at a cost. You can even offer to pay for friends and let them Venmo you or pay you back with cash.

Plus there are other perks to the rewards program, such as free refills of brewed coffee or tea.

(And if you just can’t quit Starbucks, these Starbucks hacks can save you money on your habit.)

2. Buy Discounted Starbucks Gift Cards

Websites such as Raise or Gift Card Granny and others can stretch your coffee dollars further. Just buy a gift card for less than its face value, and you’ll get more for your money anywhere making PSLs.

3. Join My Panera

Panera has a perks program, too. Join My Panera to get discounts and other customer rewards such as a free PSL.

4. Join Krispy Kreme Rewards

At Krispy Kreme, dollars equal doughnuts, as well as custom coffees. You get a free doughnut when you join and after about a dozen purchases, you can score a free pumpkin spice latte.

5. Celebrate Your Fall Birthday

If you’re a member of Starbucks Rewards, you’ll enjoy a free drink on your birthday. Why not make it a pumpkin spice latte?

Dunkin Donuts also offers free birthday drinks through its DD Perks Rewards program and has an extensive pumpkin spice menu.

Many other cafes also offer free birthday drinks, so if you find yourself at a coffee shop with pumpkiny concoctions on your birthday, be sure to ask!

Getty Images

6. Make a DIY Pumpkin Spice Latte

Indulge in a pumpkin spice latte anytime with this great do-it-yourself recipe from Farmgirl Gourmet. This recipe makes two 10-ounce lattes, so you can share one with a friend.

Stir the milk, pumpkin puree, sugar, vanilla and pumpkin pie spice together in a pan over medium-high heat. Bring it almost to a boil, but avoid boiling (that will make it too thick). Stir constantly, and it should start to froth in about a minute.

Pour the concoction into two mugs, then slowly add the strong coffee or espresso, pouring it in by the edge of the cup so that the milk stays frothy. Add whipped cream and a dash of pumpkin pie spice on top, and indulge in your homemade creation.

7. Make DIY Pumpkin Spice Coffee Creamer

This simple recipe from Delish requires just five ingredients and produces 1-3/4 cups of pumpkin spice creamer to add to your coffee.

You’ll Need:

1-1/2 cups heavy cream or half-and-half

2 tablespoons pumpkin puree

2 tablespoons pure maple syrup

1/2 teaspoon pumpkin pie spice

1 or 2 cinnamon sticks

Directions:

Whisk together the heavy cream or half-and-half, pumpkin puree, maple syrup and pumpkin pie spice in a small pan over medium heat. Add a cinnamon stick or two and turn the heat up a bit until it boils, whisking occasionally.

After a minute, take it off the heat and let it cool for about five minutes before you add it to your coffee.

According to Delish, the leftover creamer will keep in your refrigerator for a week, but be sure to give it a good shake before using.

Kristen Pope is a former contributor to The Penny Hoarder.

Contributor Katherine Snow Smith is a veteran newspaper reporter and editor who covers lifestyle topics, workplace issues and ways to make money for The Penny Hoarder. She is the author of “Rules for the Southern Rulebreaker: Missteps and Lessons Learned.”

With food costs surging, groceries can quickly eat up your monthly budget. But we all need to eat in the end. So, what can we do?

There are quite a few ways to save money on groceries, but you’ll need to take some time to plan your shopping trips. Coupons can help, but they are no substitute for shopping at the right stores.

We’ll show you how you can save money each month on grocery shopping, as long as you don’t mind putting on your detective hat.

Save Money on Groceries — Every Single Time

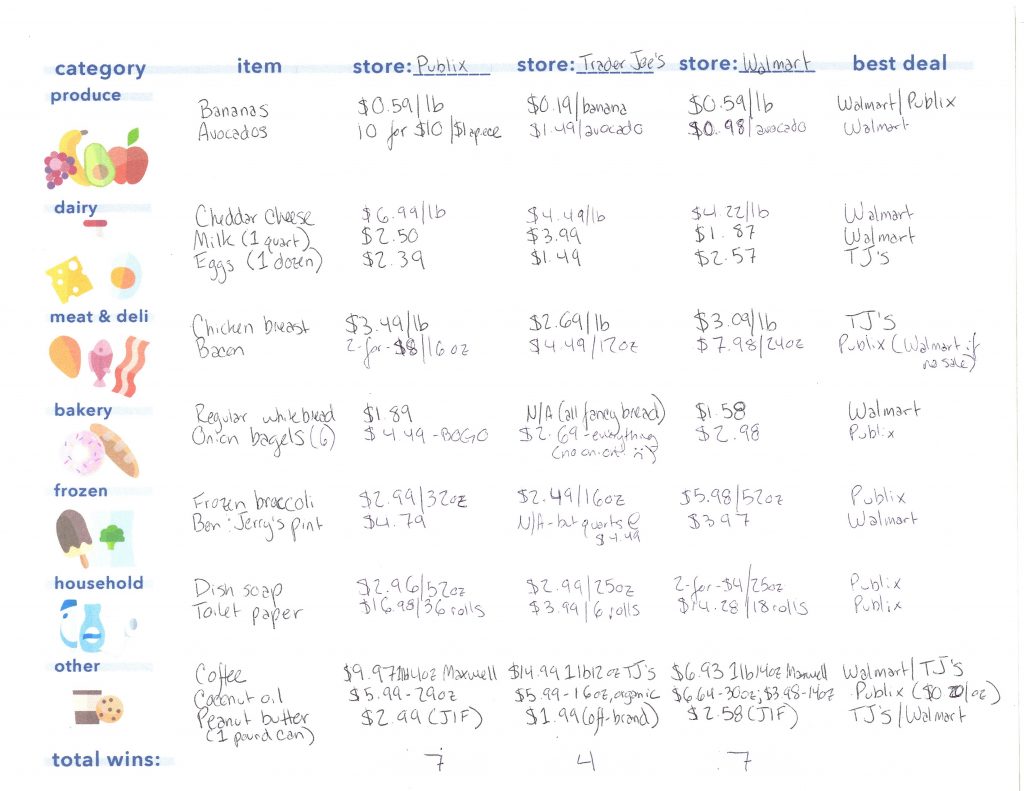

Since prices can vary wildly between retailers, you can save a lot by switching to the store that charges least for your staples.

Everyone’s grocery list is different, so we created a supermarket comparison template for you to print out and complete yourself. This way, you’ll automatically get the most bang for your grocery budget buck — no matter what’s on your list.

Click for a larger version you can print out.

How to Use the Grocery Comparison Worksheet

So, here’s the thing.

Comparing grocery stores is going to take some time and effort upfront. You’ll need to travel to several stores in your area, locate your staples, record their prices and compare costs.

But while doing your supermarket comparison may seem like a chore, it can actually be a lot of fun.

You’ll feel a little bit like a private investigator. And once you’re done, you’ll save money every time you shop — no further thought or effort required.

Automated savings? Yes, please.

It’s super simple! Here’s what to do.

1. List Your Staples

First things first: Make a list of your most commonly purchased items — those things you absolutely always have in the house.

You still want the best price on your one-off treats or occasional buys, of course.

But if the cookies or candy you buy every once in a while are a lot cheaper at a certain store and all your staples are more expensive, you might not see the true winner. So to best automate your savings, stick with the stuff you always have on hand.

We’ve created some suggested categories in our sheet to help get you thinking, but if you don’t eat meat, for instance, no worries — just use those spaces for more veggies, or whatever else you buy.

If you purchase some of your items in bulk, like toilet paper, don’t include them — you’re almost definitely getting a better deal at your warehouse club store.

2. Choose Your Stores

Now that you’ve got your list, it’s time to choose which stores you want to compare.

If some shop 50 miles away has awesome deals, great — but you’ll be cutting into some of your savings by driving so far, to say nothing of the opportunity cost of spending so much time on a weekly necessity.

Plus, when it comes down to a busy Tuesday night when you need to swing by the store because you’re out of milk or toilet paper or insert-essential-here, you’re not going to want to drag yourself all the way across town.

Do yourself a favor and survey only stores within a reasonable distance. Fill in their names along the top of the list — and get ready to figure out which one you’ll start seeing a lot more of!

3. Go Find the Prices

Here comes the time-intensive part.

You have to find time to head to each of your chosen stores, track down those items and write down their prices.

You don’t have to do it all at once, so take your time. Fit it in by doing your normal weekly grocery shopping at each store as needed — just remember to actually write down the prices when you go!

An important note: Remember to write down the amounts of the items, as well.

In some cases, stores won’t carry the same item in the same size. Even if the total sticker price is cheaper, you’re not getting a better deal if you’re getting less product.

By recording the actual amount of each item, you’ll be able to calculate the cost per unit or ounce, so you’ll know exactly how it’s priced.

4. Compare Prices

Once you have all the prices and amounts listed for each of your stores, start comparing those prices and figuring out which store has the best deal.

If it’s a one-for-one comparison (say $3.49 vs. $3.09 for a pound of boneless, skinless chicken breast), it’s easy: Just record whichever store has it cheaper in the column on the right-hand side.

But in some cases, you’ll have to do some math if two stores don’t package the item in the same amounts. For example, check out our sample math to figure out which deal for bacon is best.

Since Publix had 16-ounce packages marked at 2-for-$8, it technically won at 25 cents per ounce.

But if that sale wasn’t going on, Walmart would be the winner — so it’s not always an easy race to judge.

Which brings me to another caveat: Quality matters! Feel free to factor in cases in which you’d rather spend a little bit more per ounce for a product you like better, or for fair trade, organic or humanely raised food items.

5. Name a Victor — and Start Shopping Smarter!

Now look at the right-hand column and count how many times each store’s name appears. Record the total number in the bottom of the store’s column (see the example above).

Whichever store’s name appears the most is where you should shop to save the most money on the bulk of your grocery purchases.

Congrats, you’ve just automated your grocery savings! You can rest assured you’re saving money every time you shop, even if you never clip another coupon.

Of course, markets and prices change, so you’ll want to revisit your comparison fairly regularly.

And besides — just try to tell me you didn’t have fun sneaking around the stores, recording their prices.

And if you really didn’t? I bet your kids would. So next time, recruit some help.

Consider a Grocery Comparison App

If you feel more high-tech, you might consider a grocery store price comparison app. We tested a few offerings in Apple’s App Store and Google’s Play Store and found Basket to be our favorite choice for shoppers.

The Basket app is free and enables you to compare product pricing at different grocery stores (and even grocery delivery services). You can see the best prices for individual items or your overall cart, if you want one-stop shopping.

You can scan any product with a barcode quickly if you don’t feel like typing. You can also put together separate carts for different shopping trips or plan ahead for a big dinner or party you may be throwing.

Basket also surfaces some of the best savings from local grocery stores, displaying current sales and available coupons.

When filling up your shopping cart, stay aware of exactly what you’re taking home. When shopping for perishables, never buy more than you can use before they might expire (no matter how good the deal may be). If possible, purchase nonperishables in bulk.

How Much Should a Single Person Spend on Groceries?

According to the United States Department of Agriculture, the average moderate-cost monthly food plan for an adult (aged 19-50) is $367 for men and $310 for women. More aggressive savings when shopping can bring the price as low as $238.

Is It Cheaper to Eat Out or Buy Groceries?

Due to the additional overhead costs you need to support when dining at a restaurant or grabbing takeout, it is generally always cheaper to buy groceries. Additionally, eating at home will allow you to keep a closer eye on nutrition and what actually goes into your food.

Jamie Cattanach is a former staff writer at The Penny Hoarder.

Michael Archambault is a senior writer for The Penny Hoarder specializing in technology.

New over-the-counter hearing aids are now available without a prescription or medical exam, following a final ruling from the U.S. Food and Drug Administration in August.

These devices will be available online, at pharmacies and in retail stores. Big names like Walgreens, Walmart and Best Buy have already announced plans to carry a selection of products this fall.

The new class of OTC devices — available for adults with perceived mild to moderate hearing loss — will be equipped with the same basic technology as traditional hearing aids but at a fraction of the cost.

Hearing aid devices can cost anywhere from $900 to $4,000 per ear. Many health insurance providers — including traditional Medicare — don’t cover the devices or hearing tests.

The new rule also cuts the red tape plaguing many consumers. Hearing aids are currently only available with a prescription from an audiologist or a hearing health specialist. Multiple appointments are usually required, from consultations to fitting adjustments.

So how are over-the-counter hearing aids different?

Here’s what you need to know.

How Much Will Over-the-Counter Hearing Aids Cost?

Over-the-counter hearing aids are just starting to hit store shelves, so it’s hard to say how much they’ll cost. The White House said it anticipates OTC devices will save Americans as much as $3,000 per pair.

Walgreens announced plans recently to start carrying Lexie Lumen hearing aids in stores nationwide after Oct. 17 for $799.

Consumers will also be able to purchase these hearing aids online through Walgreens Find Care for $39 per month for 24 months ($936 total).

Each pair of hearing aids at Walgreens will also include batteries and accessories as well as a 45-day money-back guarantee.

Walmart also told Reuters it will begin offering over-the-counter hearing aids to adults with mild to moderate hearing impairments without a medical exam after Oct. 17 — but the major retailer declined to say how much they will cost.

Competition from manufacturers is expected to drive prices down on OTC hearing aids. But by how much or how quickly is still anyone’s guess.

Will OTC Hearing Aids Be HSA and FSA Eligible?

You can use a health savings account (HSA) or a flexible spending account (FSA) to purchase OTC hearing aids.

The new category of over-the-counter hearing aids is also expected to qualify.

A health savings account is a tax-advantaged account you and your employer can contribute to that can pay for a long list of eligible medical expenses. An FSA offers similar tax-saving benefits but with different contribution limits and other rules.

Pro Tip

What’s the difference between an HSA and FSA? Learn the pros and cons of both.

Are Over-the-Counter Hearing Aids Right For You?

OTC hearing aids are intended for people 18 or older with mild to moderate hearing loss.

They’re not meant for everyone or every situation, kind of like drugstore reading glasses.

Struggling to understand speech in a phone call, on the television, or when you can’t see who is talking.

Difficulty hearing in noisy environments.

Trouble hearing loud sounds.

Regularly asking others to speak more slowly or clearly, to talk louder, or to repeat themselves.

Getting regular complaints from family or friends that you’ve turned the sound up too loud or aren’t hearing them properly.

If you have severe hearing loss or a specific hearing issue — such as deafness in only one ear — you should consult an audiologist.

Likewise, you should see a doctor right away if you experience dizziness, sudden hearing loss, pain or discomfort in your ear canal as these can be signs of a more serious medical condition.

Visiting a hearing care professional can also be beneficial if you want advice on how to choose the right hearing aid or need help adjusting or repairing your OTC device.

The Hearing Loss Association of America offers this tip sheet to help you decide if OTC hearing aids are right for you. It also includes questions to ask yourself when shopping around for a new device.

How Do You Buy OTC Hearing Aids?

Over-the-counter hearing aids will be advertised and sold in pharmacies, big-box stores, online and through the mail. You won’t need a prescription from a hearing specialist to buy them.

You fit the devices yourself, and you might be able to control and adjust the settings in ways that people with prescription hearing aids cannot.

An automated hearing test may be offered through a smartphone app so you can test your hearing at home.

You’ll probably use a smartphone or computer to install and customize your hearing devices as well.

Companies like Audicus, Bose, Eargo, Jabra, Lexie and Lively are all expected to be big players in the OTC market. Additional manufacturers and devices will also emerge over the next few years.

More consumer guidance on how to buy and use OTC hearing aids is expected in the coming weeks.

The Fight For Affordable Hearing Aids

Lawmakers and advocacy groups like AARP have fought for years to lower the cost of hearing aids and make them more accessible.

Under the current system, audiologists usually buy hearing aids wholesale from manufacturers and then set their own prices.

Five manufacturers control about 90% of the hearing aid market, according to a Senate investigative report released in June. Many policy makers say this lack of competition among prescription devices contributes to higher retail prices.

The actual devices usually account for just a fraction of the total cost. Hearing aids are typically bundled with multiple services, including a hearing exam, fittings, programming and repairs.

The added expense of these professional audiology services is what really drives up the cost for many people, especially older Americans.

Medicare beneficiaries spent an average of $914 out of pocket on hearing services in 2018, according to a report from the nonprofit Kaiser Family Foundation.

Approval for OTC hearing aids has been years in the making.

In 2017, Congress ordered the FDA to craft regulations for over-the-counter devices and the proposal was signed by former president Donald Trump.

Little progress was made after that. In July 2021, President Joe Biden called on the FDA to take action “to promote the wide availability of low-cost hearing aids.”

The FDA reviewed more than 1,000 public comments and tweaked the proposal before approving its final rule Aug. 16, 2022.

Wait, Haven’t OTC Hearing Aids Been Around For a While?

Devices known as personal sound amplification products, or PSAPs, have been on the market for years. The same goes for TV amplifiers, hearing assistive devices and hearing protection devices.

These products help people with normal hearing amplify sounds in specific situations — but they’ve never been approved to help treat hearing loss.

The quality of these consumer electronics also varies widely. Attorneys general in New York, California and Texas have warned consumers about low-quality amplifiers falsely marketed as over-the-counter hearing aids in recent years.

The FDA said it is clamping down on this deceptive advertising.

OTC hearing aids will be regulated as medical devices by the FDA, and must adhere to strict specifications and labeling guidelines.

Rachel Christian is a Certified Educator in Personal Finance and a senior writer for The Penny Hoarder.

You may have Champagne tastes on a boxed wine budget, but that doesn’t mean you have to settle for a bottle of wine that tastes like maroon vinegar. Or just plain vinegar.

Wine can run the gamut from Trader Joe’s Two Buck Chuck all the way to vintages that can cost more than our homes. However, most people who can afford incredibly expensive bottles – like this 2005 Petrus Pomerol that goes for $8,997 at some Total Wine locations – probably aren’t too worried about the cost of their homes.

Total Wine explains the tasting notes, which may be delightful or offensive depending on your appreciation of the words chewy and supercaressing mouthfeel: “Full-bodied, with ultrafine tannins and a supercaressing mouthfeel. Coffee, dark chocolate and berry. Chewy yet balanced. Very long in the mouth.”

But there is something to all of this wine knowledge (chewy just refers to a thicker textured wine) and we’re here to help you find some of the best cheap wines on the market. And by inexpensive we mean less than $15.

We offer suggestions but also ways for you to separate the expensive wines from the best cheap wines when you’re cruising the liquor store aisles. We spoke with some sommeliers to get the tricks of selection and point us to the affordable wine.

The six cheap wines they recommend come from:

But First, a Word on How Wine Is Priced

It’s common that buyers equate quality with cost. Surely, a $35 cabernet is better than one that comes in under $15, right? Not necessarily. Wine is priced using several variables.

Pricing reflects the cost of materials and labor, and also volume. A large vintner like Kendall Jackson produces millions of cases of chardonnay annually. Patz & Hall, another Sonoma County, California, winemaker produces considerably less.

Depending on the year and style, a Kendall Jackson chardonnay can be had for less than $15, sometimes as low as $8 on sale at big-box retailers. Plan to spend at least $30 for a bottle of Patz & Hall chardonnay. The boutique winery releases about 15,000 cases of chardonnay a year. Size does matter when it comes to pricing.

Is the 2017 Patz & Hall chardonnay better than the same vintage of Kendall Jackson? Maybe, maybe not. Sometimes the pricing can be chalked up to perceived value. But the only perception we are concerned with here is where to get the best cheap wine.

Don’t Let a Cute Label or Familiar Name Lead You Astray

A large grocery store stocks hundreds of bottles of wine and the prices are usually reasonable. For many of us, this is our wine store. There are plenty of brands that you recognize: Yellow Tail from Australia; Robert Mondavi out of California and even La Marca from Spain that makes a popular $15 bottle of prosecco perfect for Sunday brunch mimosas.

(Bubbly lesson: The sparkling wine of France is called Champagne. In Italy that’s prosecco, and in Spain it’s cava. Bring on trivia night!)

Rather than recognizing brands, you might believe that France turns out the best red wines and California the best white wine. Again, our perceptions on what’s fancy and what’s not helps set the prices.

Then there are just a lot of cool labels, and that’s how some of us pick wine. Honestly, how can you resist Michael David’s Petite Petit with its circus-themed label and fun name? The mostly sirah blend can be had for $13 or less on sale.

Inexpensive wine is a given at grocery stores and the wine section of Costco, Sam’s Club or Target, but good wine can be harder to pick out among the vast selection.

4 Tips for Scoring Good Cheap Wine

You’ll get more selection guidance at a local wine shop or even a big-box booze store than you at the average grocery store or Costco, but our tips will help you bust out on your own and find plenty of good cheap wine priced below $15 — heck, even around $10.

1. Buy International Wines

The United States — and specifically California — produces a ton of amazing affordable wines, says Vincent Anter, founder and host of the V is for Vino wine show that’s streamed for free on YouTube and various other places.

Because California produces so much wine, he says, it’s more difficult to figure out the good stuff.

However, South American wines tend to be less expensive due to lower labor and land costs with overall good quality. Or, look to Europe, specifically Italy, where costs may be kept lower through several factors, including:

Government assistance for wine producers, which is available in many wine-growing regions.

Regulations that control everything from grape yields to where the grapes come from to the use of additives.

A distribution model that doesn’t vary from state to state and doesn’t include three tiers, with each tier marking up the wines each step of the way.

The production of more entry-level wine, because most Europeans see wine as part of the meal instead of a luxury item.

2. Stay Away From Trendy Wines

Wine, like all things, goes through trends, according to Matt Woodburn-Simmonds, a sommelier who runs The Plate Unknown, a website celebrating world food and drinks.

To pick up a bargain, he suggests avoiding the trends.

“Rather than a New Zealand sauvignon blanc or Argentinian malbec, look for an Argentinian cabernet franc or New Zealand pinot gris,” he says. They will be the same price, but a higher quality, because popularity isn’t driving the price higher. Yes, you can find an Argentinian malbec for $15 but it’s likely that the $15 cabernet franc will be better.

The same applies to lesser-known Eastern European wine-growing countries like Greece, Slovenia and Hungary, all of which are currently turning out great quality wine at pocket-friendly prices, Woodburn-Simmonds said.

3. Don’t Be Afraid of Unusual Wines

Instead of reaching for a California cabernet sauvignon — because the best cabernet grapes grown there go into the more expensive bottles — look for a cabernet from Argentina.

Argentinian wine producers are known for their malbec, not their cabernet, so better quality grapes will likely be in that bottle of cabernet, according to Kathleen Bershad, author of The Wine Lover’s Apprentice and owner of Fine Wine Concierge in New York.

“Along those lines, look for the grape you’ve never heard of,” she said. “While you might love chardonnay, a torrontes can offer a similar feel and flavor, but because it’s not well known, the quality is likely to be better for the price.”

You can easily snag a decent bottle of torrontes for about $5 to $10. Try the Mendoza Station Torrontes ($7 at Totalwine.com).

4. Pay Attention to Where the Wine Comes From

Much of what goes into the cost of a bottle has to do with where the wine is grown and produced, says Melissa Smith, founder of Enotrias Elite Sommelier Service in Oakland, California.

“Have you seen the cost of an acre of land in Napa Valley?” she says. “Between that, French oak barrels starting at $800 a piece and a celebrity winemaker, you can see why a bottle of cabernet might cost $100 per bottle.”

She has suggestions on finding quality wines at a lower price, based on their region:

Watch for regions that don’t typically use fertilizer or pesticides in vineyards. Smith says Europe (look for Bordeaux or Chianti), North Africa (cabernet sauvignon or merlot) and the Middle East (chardonnay and sauvignon blanc) fit this description.

Look for countries where wine is part of daily life. Such is the case in Greece, Spain, Italy and France. A lot of wine in those countries is made in co-ops, where the grapes have passed certain standards and vineyard practices, and in large quantities, keeping the prices low. In other words, classic table wines.

Understand where wine is more labor intensive. For example, machinery can’t be used in vineyards with steep hills or narrow terraces, so those grapes need to be harvested by hand. You’ll know if this was the case if the label says “hand-picked grapes” or “hand harvested.” That wine may not necessarily taste better, but it will increase production costs. As a result, the price of the wine will be higher, according to sommelier Woodburn-Simmonds.

Some of the steepest vineyards in the world are in the Mosel region of Germany. Riesling is the star grape there and it’s not uncommon to see prices of more than $25 a bottle. The Chateau Ste. Michelle Columbia Valley riesling out of Washington State can be had for under $10.

Try These 6 Cheap Wines From Different Regions

This is a starter list of the best cheap wines for wine lovers. Get a taste of them and then start to branch out to other wines from these areas, keeping your wallet in mind all of the time.

Israel

Try this wine — Recanati yasmin red

Taste — This is a bold and complex wine from the grape-growing region around the Sea of Galilee in Israel, says Sneha Saigal, a sommelier in New York who has lived in India and Spain. It is a blend of merlot and cabernet sauvignon.

“It pairs really well with meats and BBQs, and plus, it’s kosher,” Saigal says.

Taste — Chenin blanc grapes have been grown in South Africa since the mid 1600s, and the varietal originated in France, says Gary Schueller, a New York wine buyer. It’s a versatile grape that can make wines of all styles and price points, including sparkling wine.

At the lower price points, chenin blanc is typically a medium-bodied crisp, refreshing wine that’s food friendly, but can easily be enjoyed on its own. It’s noted for flavors of stone fruit, pear, apple and yellow citrus, Schueller says.

“Having tasted hundreds of wines at this price point, it certainly is at the top of the pack,” Schueller says.

Taste — Alicia Ortiz, the strategic communications manager at Sippd, a wine app that matches wine to your budget, recommends this bottle from delle Venezie, Italy. The price is right and its fruit is sourced from some of the top growers in northeast Italy.

You’ll taste hints of apple and mineral in this light-bodied wine. Pair it with grilled fish or a light meal.

Taste — The land-locked Beaujolais region of France produces this deeply flavored gamay. Tasters note hints of raspberries and strawberries in the fruity red. It has low tannin levels and is delicious when slightly chilled and is best served with poultry and mild cheeses.

Taste — California has plenty of delicious summer wines priced at less than $10, says Shana Bull, a wine writer in Sonoma County. This refreshing bottle in particular is great with spring vegetables such as asparagus with grated parmesan cheese or fish tacos.

They also make a canned Bonterra Rose that’s priced under $10 that pairs well with creamy brie cheese and strawberries or melons. Think picnic or beach wine, Bull says.

Taste — Boasting some of the oldest vines in the world, Chile is putting out wines at incredible values that are crowd-pleasing for novices and experienced wine drinkers alike. This specific wine is a $12 bottle made from 35-plus-year-old vines, Schueller says.

Random cool fact: This grape was believed to be extinct until it was rediscovered in Chile in the mid-1990s.

“So this is a grape with a lot of history, but really just in recent years is getting its due and is surging in popularity,” Schueller says.

Danielle Braff is a Chicago writer who specializes in consumer goods and shopping on a budget. Her work has appeared in the New York Times, Washington Post, Real Simple and more. Senior staff writer Robert Bruce contributed.

Note: This article doesn’t contain any depiction of physical or sexual violence, but does detail financial and emotional abuse in relationships.

Lisa Orban was married to her abuser for three years. In 1990, she left after he threatened to kill her and their two young children.

She was 20 years old.

Her financial situation in the marriage? “Bad, in a nutshell,” she recalled.

Her husband was the main breadwinner, and he managed the family’s finances.

“Whenever there was a chance that I might make enough money or make more money than him or do anything to upset his financial apple cart, so to speak, he would come in and sabotage it,” she said.

She lost multiple jobs because of his meddling.

Orban moved with him from her hometown in Illinois to Arizona for college, where she’d won a four-year scholarship to study psychology. Before she could start, he contacted the university and told them she’d decided to drop out.

“Imagine my surprise when I go to registration day and find out that my scholarship is gone,” she said.

He even had control of the mailbox. He took her key, though she thought she’d just lost it, and put off replacing it. That had major, unexpected financial ramifications.

“It wasn’t until after we were divorced that I found out that I had not paid off my student loan,” she said. The $4,000 loan ultimately cost her $38,000 to repay.

The checks Orban thought were going into the mail were not, and the missed payment notices from her loan providers weren’t getting to her.

He kept control of the checking account.

He wouldn’t let her use the car alone.

He knew how much money she earned, and he would accompany her to the bank to deposit her paychecks.

He signed up for credit cards in her name.

By the time Orban left and filed for divorce, she was $80,000 in debt and didn’t even know it.

Domestic violence and abuse comes in many forms, whether it’s physical, emotional, psychological or sexual — but it can also be financial. Likely, it’s some mix of these, but not always all of them.

“Like all abuse, financial abuse takes a lot of forms, but it’s all controlling behavior — power and control,” said Casey Harden, General Secretary of World YWCA. “Imagine tightening the reins on the financial condition of the home, so that there’s limited options.”

Abusers may leave their partner out of major decisions and purchase a home that’s well out of the family’s budget, for example. They may run up credit card debt without their partner’s knowledge or input, lie about paying bills or damage valuable property.

“More often than not, the abuser has made the victim feel as if they are dependent upon the abuser — that without the help of the abuser, the victim could not survive financially in the world, and it is only by the grace of the abuser that the victim has a roof over their head and food on the table,” said Michelle Kuehner, a survivor of domestic violence who is now a financial adviser and author of The Money Diet blog.

If you’re in a bad situation, consider this advice from financial, legal and domestic violence experts on how to leave an abusive relationship when you don’t have any money.

6 Steps to Prepare Your Finances Before Leaving

“The largest hurdle you face in an abusive relationship is getting back your independence,” Kuehner said.

That’s easier said than done.

In addition to the financial hurdles, the most dangerous time for an abused partner is the moment he or she decides to leave.

That’s why before you do anything, we recommend this step:

1. Connect With a Victim Advocate

These people are trained and experienced, so they know how to help you plan to leave safely and quietly. They can point out potential pitfalls and let you know what major financial hurdles to expect.

How to get in touch with local advocates:

You’re the best at assessing your own safety, so listen to your own instincts, work with an advocate and only consider these steps when you feel it’s safe.

2. Save Money

“Be sure you have liquid funds held in an account in your name only,” said Allison Alexander, a financial adviser at Savant Capital Management. She also recommends having credit cards in your name alone.

If you can’t get a loan, see if there are other ways to secure money for yourself that your partner doesn’t have access to.

Here are some creative ways to make extra money:

Keep an eye out for influxes of cash your partner doesn’t know about or have access to.

“A lot of survivors… wait until that tax return comes, and that’s a nice little chunk to get started on,” said Kim Pentico, director of the Economic Justice Program at the National Network to End Domestic Violence.

A bonus at work may be a similar lifeline.

You may be able to work with the human resources department at work to automatically deposit part of your paycheck into a separate bank account.

Catherine Scrivano, a Phoenix–based financial planner, says HR may also be able to help you make an adjustment to your tax withholding to help you receive more money with each paycheck that you can save or invest throughout the year.

3. Make Copies of Important Documents

This includes tax returns, bank statements, investment statements, mortgage or loan information, car titles and pay stubs.

You can simply snap a picture of these documents with your phone and email it to a friend. Or store them in a cloud drive that you — and only you — can access from anywhere, like Google Drive.

4. Cut Ties and Open a New Bank Account

Before opening your own account, Harden recommends obtaining a new mailing address, such as a post office box, and an email address your partner doesn’t know about.

Harden also suggests you contact your bank to update your account’s security questions if your partner has access to an account in your name.

“Your husband of 10, 15 years probably knows the answers to most of your security questions,” she said, “especially if he’s been actively working to know them.”

You can tell your bank the question you want to use. You don’t have to stick with a default question your partner might know the answer to.

If you can, set up separate accounts your partner doesn’t know about, or at least can’t access.

Also, “remove your personal items from a safe deposit box if it is held jointly,” Alexander said. “Establish your own safe deposit box at another bank and place your financial documents and sentimental items, including jewelry, pictures (or) valuables there.”

5. Find a Financial Adviser

If you have the resources to hire a professional financial adviser — who works for you alone, not you and your partner together — great.

If you can’t afford to work with a professional, utilize your local library or domestic abuse support organization. It may have financial literacy classes, support groups and literature to help you.

Even financially savvy friends and family can offer advice.

Pentico often tells survivors, “There’s somebody in your life, more than likely, that seems to know what’s going on when it comes to money and finances, whether it’s a coworker or a family member. Reach out to them.”

6. Find an Attorney

If you are planning to file for divorce, or if you think your partner is planning to file, seek out the help of a lawyer as soon as possible.

If you don’t have money to hire a lawyer or don’t feel safe, a victim advocate can help you find resources.

Getty Images

6 Steps to Rebuild Your Finances After Leaving

Orban didn’t make a plan to leave her abuser. She did what many survivors do: run blindly for their lives.

“They look for a moment — a credit card left unattended, a check that unexpectedly arrives that you somehow got access to, a Christmas bonus from your work that your spouse doesn’t know about,” she says. “These are things you look at, and you go, ‘This is it. This is my chance.’”

And then what?

Once you’ve left and you’re safe, your greatest financial hurdle may be not knowing what you’re working with.

Start by figuring that out.

1. Get a Copy of Your Credit Report

If you haven’t had control of your finances for years, you may have no idea what state they’re in. To create a rebuilding plan, you have to first know what you’re dealing with by reviewing your credit report.

Your credit report will give you this information.

Here’s how to get a free copy of your credit report:

Contact the three major credit reporting bureaus to get a free copy from each. They’re legally required to give you a free credit report once every 12 months, but since the pandemic, all three are offering free weekly credit reports.

To check out your free reports, start at annualcreditreport.com. A banner, front and center, tells you about the new policy with a “request your free credit reports” button.

Your credit history can affect a lot of what you do from now on.

Someone will likely pull it when you apply for an apartment, mortgage, vehicle loan or credit cards, before hiring you for a job or opening a new bank account. It will affect how much you pay to rent a car or get a new cell phone. It could even affect your car insurance rates.

Once you know what’s in your credit history, you can figure out how to fix it.

2. Identify and Work to Pay Off on Lingering Debts

Your credit report will show you all the creditors you owe. Reach out to them directly and ask what you need to do to eliminate those debts.

Scrivano pointed out that a divorce agreement isn’t enough to get you out of debts you shared with your partner. For example, even if the agreement says credit card debt is your ex’s responsibility, the creditor doesn’t know — or care.

Contact your creditors to determine exactly what needs to be done — and what, in the end, is your responsibility.

To prevent your ex from building new debt in your name, you can place a 90-day fraud alert with the major credit bureaus. That way, businesses must verify your identity before issuing credit in your name.

Here’s how to initiate a fraud alert with one of the bureaus:

Pro Tip

You only have to place an initial fraud alert with one bureau. It will contact the others, according to the FTC. You can renew the alert after 90 days, as often as you need.

3. Create a New Budget

Next, Harden said, spend time “learning to budget in the new reality, whatever that new reality is.”

You can set up new savings and investing plans to “become proactive about having full ownership over (your) finances,” not just reactive to your situation.

Orban learned to manage her budget through trial and error. She always kept a detailed budget.

“I ended up itemizing my life on a day-to-day basis and seeing how much I had coming in and how much, realistically, I had to pay out to function in a normal way,” she said.

Read our tips on how to budget if you’ve never done it before:

4. Rebuild Your Credit

Even if you have damaged credit, you’re not doomed.

“Since my credit had been damaged a bit, I wanted to rebuild that as well,” Kuehner says. “Taking out secured loans… was the easiest way I knew. Within a year-and- a-half my credit had been repaired.”

It’s similar to a debit card: You put down a cash deposit and can use that amount in credit.

Unlike a debit card, secured cards report your payments and balance to credit bureaus. So it’s a way to establish a credit history if yours is shot or nonexistent.

Read more tips for rebuilding your credit:

5. If You Need to, Find a New Job and Housing

If your abuser didn’t allow you to keep a job, the effect can ripple beyond your lack of control in the relationship.

“It could interrupt a work history,” Harden said.

If you’ve lost your job or you’ve been out of work for a while, you have options.

Find a bridge job or seasonal job, or pick up a side gig. These may not become your long-term career, but they’ll get some money coming in.

“Your local domestic-violence program has relationships with community resources, so while they may not provide (job placement) themselves, they certainly have built partnerships and relationships with those who do, so reach out to them,” Pentico said.

The final step is refocusing on financial vitality, Harden said.

What does a thriving, successful life look like for you? Is there a business you need to reclaim, a career you need to start over or education you need to finish?

Healing emotionally and financially took a lot of time and work. But a small epiphany late one night made her realize she could do it.

“(I realized) I didn’t have to wait for time to heal all wounds. I could make steps and go forward and go, ‘I am in control of my life now — me — and I can make these changes.’”

If you or anyone you know needs help, contact the National Domestic Violence Hotline to speak with an advocate or be connected with someone in your area: 1-800-799-SAFE (7233) / TTY: 1-800-787-3224.

Contributor Dana Miranda is a Certified Educator in Personal Finance® who has written about work and money for publications including Forbes, The New York Times, CNBC, Insider, NextAdvisor and Inc. Magazine.

Deputy editor Tiffany Wendeln Connors updated this post.

Fewer people are sending items by mail these days opting instead for online bill pay, email and social media. But some prefer the traditional feel of mailing cards, bills or letters, or trust the postal service more than the internet with their correspondence.

If you use a lot of stamps, the cost can quickly add up. As of July 2022, U.S. Forever stamps cost 60 cents each — a 3.4% increase from the previous year. The great thing about Forever stamps is that they don’t list a value on the stamps themselves, so you can stock up and still use them even if the cost of a Forever stamp increases.

But you can get postage stamps for cheaper than face value if you know where to look. Here are a few options to get you started.

Best Places to Buy Stamps at Discounted Prices

Before you start shopping for discounted stamps, it’s important to think critically about the deal you’re getting. According to the United States Postal Inspection Service, the sale of counterfeit stamps is up.

“Is a substantial discount of up to 50% off an order of United States Forever Stamps too good to pass up?” the article asks. Yes, keep scrolling.

USPIS reports that counterfeit Forever stamps are typically sold in bulk with a hefty discount, such as 20-50% off. If you see a deal that looks too good to be true, it probably is. That’s why buying stamps from a random seller on eBay might not be the best decision.

But despite the presence of counterfeit stamps out there, it’s still possible to get a discount on postage stamps; you just need to be vigilant and do your research on the seller to make sure they’re legit before parting with your money.

It’s your birthday and you deserve a gift or two. Check our list of 101 birthday freebies and get your fair share.

Check Stamp Dealers for Discounted Postage

Stamp collecting is a big business. Dealers make a lot of their money buying and selling stamps from collectors, but they also make money selling mint stamps at a lower cost than their worth.

Stamp collectors often buy unique stamps when they come out, thinking they may become valuable someday. But often, they don’t grow in value, and the collector may sell stamps to a dealer at a discount. The dealer then sells these stamps to you, the consumer, at a low cost.

Buying stamps this way might mean you have to use several stamps of random value in order to get to the 60 cents required for regular postage, but it can save you money (and make for a unique envelope to the recipient of your mail).

Look for Deals on Amazon

At first glance, postage stamps on Amazon seem to sell for the same price as at USPS, and in some cases they are more expensive. But if you have patience, you can find good deals on stamps on Amazon.

For example, I stumbled upon a listing selling a roll of 100 stamps for $55.99 on sale, which works out at just under 56 cents per stamp, or an 7.1% discount.