Meta Platforms (META) stock is once again in the limelight after the company reported good earnings results, taking its shares close to record highs. Although Wall Street has generally reacted well to the accelerating revenue growth of Meta Platforms and its aggressive artificial intelligence (AI) plans, at least one major investment firm is cautioning investors not to get overly bullish on the tech giant’s shares. In a recent interview, Needham senior analyst Laura Martin said Meta Platforms is “priced for perfection” but could potentially decline 10% to 15% if growth targets are not met.

META stock has risen 7% in the past month due to Meta’s aggressive AI plans for its advertisements and management’s positive outlook on the business. However, the current high optimism surrounding Meta Platforms shares has led investors to price its growth potential at an unforgiving level. With a massive capital expenditure cycle in place, the market is no longer rewarding good enough execution.

The warning comes at a time when the valuations of other major tech stocks are once again facing challenges due to increasing spending plans and a lower tolerance for margin pressure.

Meta Platforms operates the world’s largest social media platform through its Facebook, Instagram, WhatsApp, and Messenger services, along with its Reality Labs segment dedicated to virtual and augmented reality technologies. With its headquarters in Menlo Park, California, Meta Platforms has a current market capitalization of around $1.8 trillion, making it one of the most valuable companies in the world.

Over the last 52 weeks, the stock has traded between a low of $479.80 and a high of $796.25. This is a reflection of its strong earnings momentum and the volatility of the stock related to the investing cycles of artificial intelligence. META stock is currently trading at $697 and has outperformed the S&P 500 Index ($SPX). Investors have clearly rewarded the company for the acceleration of its growth after the efficiency reset of 2022 to 2023.

https://www.barchart.com

From the perspective of valuation, the stock currently trades at 24 times trailing earnings and 24 times forward earnings. The price-to-sales (P/S) ratio is above 9 times as well. These numbers are at the upper end of the stock’s historical range, further supporting the idea that the good news is already priced into META.

Meta Platforms’ fourth-quarter and full-year 2025 results were undoubtedly strong. Revenue for Q4 was up 24% year-over-year (YOY) and came in at almost $60 billion. This was due to an 18% increase in ad impressions and a 6% increase in average ad price during the period. For the full year, revenue was up 22% YOY and came in at more than $200 billion, reflecting a robust digital advertising environment.

However, the story is not so rosy when looking at expenses. Fourth-quarter expenses went up by 40% YOY while full-year expenses went up by 24% YOY. This is a reflection of the significant investments Meta is making in AI infrastructure and technical talent. The company spent $72.2 billion in capital expenditures in 2025 and is projecting a significant increase in capex in 2026 to between $115 billion and $135 billion. This projected increase in capex is related to the upcoming rollout of Meta’s Superintelligence Labs.

Guidance provided by Meta’s CFO is for revenue growth of 30% or more in Q1 2026 in constant currencies. This rate marks a significant acceleration from prior quarters. While that acceleration is great, it leaves little room for disappointment. The problem that concerns Needham is that much of the expense is irreversible in the near term. This means that Meta Platforms’ margins could compress rapidly if the growth slows.

Analysts assign a “Strong Buy” consensus rating on META stock with a mean price target at $855.88, indicating a potential increase of 23% from the current price. The high price target for META is $1,144 while the lowest target price is $700, showing a wide range of price targets.

Analyst Laura Martin’s bearish view on the company’s shares is noteworthy, as it focuses less on Meta’s competitive position and more on the timing of the firm’s performance. Martin believes that being in front of a capex cycle has historically implied higher downside risk, particularly as returns on invested capital have declined. Needham estimates that Meta’s operating margins may decline from 40% in 2025 to the low 30% range in 2026, a significant reset given the company’s premium valuation.

However, Martin was more positive on the ad-tech space as a whole. The analyst highlighted strong results seen by digital advertising companies in the fourth quarter, seeing positive read-throughs for companies like Alphabet (GOOGL), The Trade Desk (TTD), and Magnite (MGNI), even if there’s weakness for Meta shares.

https://www.barchart.com

On the date of publication, Yiannis Zourmpanos had a position in: META. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

Wall Street just learned an expensive lesson about betting on Washington.

According to a Wall Street Journal report, UnitedHealth Group lost roughly $60 billion in market value on January 27 after the Centers for Medicare & Medicaid Services proposed 2027 payment rates that would barely budge from current levels.

Analysts had expected increases closer to 5%. Instead, CMS suggested a 0.09% bump. UNH stock plunged 19% in a single session, marking its worst day since April 2025.

For income investors who’ve collected UnitedHealth (UNH) dividends through thick and thin, the question isn’t just about recovering the stock price.

It’s whether that dividend check keeps showing up while the company navigates what could be its roughest period in decades.

UNH is dependent on Medicare for long-term growthGetty Images Heather Diehl ·Getty Images Heather Diehl

Here’s the uncomfortable truth:

UnitedHealth has become heavily dependent on Medicare for revenue growth.

The company’s Medicare revenue is now more than double its private insurance revenue.

That worked great when government rates kept climbing. Now it’s a vulnerability.

CEO Steve Hemsley, who came out of retirement to lead the turnaround after the company fired his predecessor last year, tried to project confidence during Tuesday’s earnings call.

Investors didn’t share his enthusiasm as the stock kept falling.

UnitedHealth now expects 2026 revenue to reach roughly $439 billion, a 2% decline from 2025. That’s the first revenue contraction since 1989, back when hardly anyone had heard of managed care.

That’s worse than the company originally anticipated, driven by fierce competition during the annual enrollment period.

Add in expected losses of 565,000 to 715,000 Medicaid members, plus declines across commercial plans, and you’re looking at total membership dropping by 2.3 million to 2.8 million people.

That’s not all bad news, though. UnitedHealth deliberately walked away from unprofitable business, repricing plans to focus on members it can actually serve sustainably. The strategy prioritizes margin recovery over top-line growth.

“We will need very meaningful benefit reductions and to take a hard look at our geographic and product footprint,” Noel said, according to Reuters.

In other words, seniors should expect fewer extras and potentially higher out-of-pocket costs as insurers scramble to protect margins.

This is where dividend investors need to focus.

UnitedHealth expects to generate at least $18 billion in operating cash flow for 2026.

That works out to roughly 1.1 times net income, down from 1.5 times in 2025 but still healthy enough to cover the dividend.

CFO Wayne DeVeydt said the dividend would “remain well supported by earnings and cash flow” this year.

According to data from Tikr.com, between 2026 and 2030, UNH stock is forecast to expand from:

Revenue from $449 billion to $581.8 billion.

Free cash flow from $19.35 billion to $27.80 billion.

Annual dividend from $8.75 per share to $12.72 per share.

Wall Street expects UnitedHealth’s dividend payout ratio to range around 41% over the next four years, which is not too high. In this period, the dividend yield at cost is expected to increase from 3% to 4.5%.

But here’s the catch investors need to understand: DeVeydt made clear the company won’t return to “historical capital deployment practices” until the second half of 2026. That’s corporate speak for “don’t expect share buybacks anytime soon.”

The dividend itself looks safe based on cash flow projections. But growth in the payout? That could slow to a crawl as the company prioritizes balance sheet repair and navigates a hostile regulatory environment.

For 2026, UnitedHealth projects adjusted earnings per share of greater than $17.75, representing growth of at least 8.6% over 2025’s adjusted EPS of $16.35.

That’s solid, but nowhere near the double-digit earnings growth investors had grown used to.

UnitedHealth faces more than just rate pressure. The WSJ report explained:

The Trump administration has shown little appetite for insurance industry lobbying, despite initial expectations that it would take a friendlier approach.

Federal spending cuts remain a priority, and political hostility toward insurers has only intensified.

Two powerful House committees recently grilled insurance CEOs about care denials, business structures, and profits.

President Trump himself has said he wants to meet with insurers to push for lower pricing.

Meanwhile, CMS administrator Mehmet Oz has positioned himself as a “new sheriff in town” ready to crack down on industry billing practices that have drawn scrutiny.

The final 2027 rates won’t be announced until April, giving the industry time to lobby for improvements. But the early signals suggest the government isn’t in a generous mood.

UnitedHealth’s dividend isn’t in immediate danger. Cash flow remains strong enough to support current payouts, and management has explicitly committed to maintaining the dividend.

But this isn’t a growth story anymore, at least not for the next year or two.

The company needs time to stabilize margins, work through membership declines, and adapt to a tougher regulatory environment.

Dividend growth will likely remain minimal until earnings momentum returns, not until 2027 at the earliest.

For conservative income investors looking for steady, growing dividends, UnitedHealth doesn’t fit that profile right now. The dividend is safe, but it’s unlikely to grow at the historical pace.

For more aggressive investors willing to ride out volatility, the 19% selloff could create value. But you’d need patience to wait for the turnaround to gain traction and comfort with the political and regulatory risks that aren’t going away.

Sometimes the best dividend play is the one you don’t make.

Bristol Gate Capital Partners, an investment management company, published its Q3 2025 investor letter for the “US Equity Strategy”. A copy of the letter can be downloaded here. The strategy underperformed the benchmark, the S&P 500® Total Return Index, this quarter, but still surpassed the index in dividend growth. The underperformance was due to a lack of significant exposure to the AI/TMT sector or the Value sector, which provides advantages stemming from the Federal Reserve’s rate cut. The portfolio returned 15% dividend growth over the trailing 12 months, driven by the strong underlying fundamentals. In addition, please check the fund’s top five holdings to know its best picks in 2025.

Prediction Market powered by

In its third-quarter 2025 investor letter, Bristol Gate US Equity Strategy highlighted stocks such as Broadcom Inc. (NASDAQ:AVGO). Broadcom Inc. (NASDAQ:AVGO) is a leading technology company that designs and develops various semiconductor and infrastructure software solutions. The one-month return of Broadcom Inc. (NASDAQ:AVGO) was -8.31%, and its shares gained 50.90% of their value over the last 52 weeks. On December 30, 2025, Broadcom Inc. (NASDAQ:AVGO) stock closed at $349.85 per share, with a market capitalization of $1.659 trillion.

Bristol Gate US Equity Strategy stated the following regarding Broadcom Inc. (NASDAQ:AVGO) in its third quarter 2025 investor letter:

“Broadcom Inc. (NASDAQ:AVGO) reported its third quarter results on September 4, which beat analyst expectations for both revenue and earnings per share. However, the highlight of the quarter was the addition of a fourth significant customer for its XPU (custom AI accelerator) products, who has placed over $10 billion in orders to be shipped in Q326. The combination of continued growth from the existing three customers and the addition of this fourth major customer will drive a material improvement in Broadcom’s AI revenue growth in fiscal 2026 compared to the previous outlook. Management now expects 2026 AI revenue growth to exceed fiscal 2025’s 50-60% rate. In addition to the four customers for which it has secured orders, the company is working on projects with three other hyperscalers. Our “NVDA’s demand today is AVGO’s opportunity tomorrow” thesis continues to play out in the hyperscaler market where demand for custom AI accelerators continues to grow as each of them journeys towards compute self-sufficiency. The company’s overall backlog now stands at $110B, with over 50% from semiconductors.”

AVGO Stock: A Strong Buy Pick Backed by Robust Cash Flow and Dividend Growth

Broadcom Inc. (NASDAQ:AVGO) is in the 12th position on our list of 30 Most Popular Stocks Among Hedge Funds. As per our database, 183 hedge fund portfolios held Broadcom Inc. (NASDAQ:AVGO) at the end of the third quarter, which was 156 in the previous quarter. In the fiscal third quarter of 2025, Broadcom Inc. (NASDAQ:AVGO) reported record revenue of $16 billion, up 22% year-over-year. While we acknowledge the potential of Broadcom Inc. (NASDAQ:AVGO) as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you’re looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on thebest short-term AI stock.

Donald Trump Jr.-backed GrabAGun Digital Holdings Inc. (NYSE: PEW) continues to build momentum amid a challenging industry backdrop. Revenue grew an impressive 10% to $22.3 million in the third quarter, sharply outperforming the U.S. firearms market, which declined 5.3%. The outperformance was driven by PEW’s best-in-class digital platform, which continues to drive market share gains, highlighted by 12% growth in firearms revenue.

KPIs remained strong across the board: Customer lifetime value (LTV) increased 10.8% to $855, while repeat purchase rates rose to 55%. Mobile engagement—one of PEW’s core differentiators—jumped 13% and now accounts for 67% of transactions, underscoring a loyal and expanding digital customer base that supports stronger unit economics.

The company has plenty of gunpowder to support growth in coming quarters. PEW sports a pristine balance sheet with $109.5 million in cash and no debt.

Management expects a strong finish to the year, calling for mid- to high-single-digit revenue growth and modest margin improvement. The stock looks severely undervalued, given a $119 million market cap, not much more than its cash balance.

The full report below provides deeper analysis on valuation, KPI trends, and forward estimates.

Tech giants Apple and Amazon delivered better-than-expected quarterly earnings this week, showcasing resilient growth despite ongoing challenges from tariffs and intensifying competition in artificial intelligence. Both companies beat Wall Street estimates but revealed underlying concerns that tempered investor enthusiasm.

Apple’s Record-Breaking Quarter

Apple reported exceptional third-quarter fiscal 2025 results on Thursday, with revenue surging 10% year-over-year to $94 billion, marking the company’s largest quarterly revenue growth since December 2021. The iPhone maker posted earnings per share of $1.57, significantly exceeding analysts’ expectations of $1.43.

“Today Apple is proud to report a June quarter revenue record with double-digit growth in iPhone, Mac, and Services and growth around the world, in every geographic segment,” said CEO Tim Cook during the earnings call.

China Sales: $15.37 billion (up 4% YoY), beating expectations

Gross Margin: 46.5% vs. 45.9% expected

The standout performer was the iPhone business, with Cook revealing that the iPhone 16 models showed “strong double-digit” growth compared to their predecessors. The company also reached a milestone, shipping its 3 billionth iPhone during the quarter.

However, not all product lines performed equally well. iPad revenue fell to $6.58 billion, missing expectations of $7.24 billion, while the wearables division also saw a year-over-year decline to $7.40 billion.

Amazon’s Mixed Results Spark Concerns

Amazon reported second-quarter results that exceeded expectations but disappointed investors with lighter-than-expected operating income guidance. The e-commerce giant posted earnings per share of $1.68, beating the $1.33 estimate, while revenue reached $167.7 billion, surpassing the $162.09 billion forecast.

Despite the strong numbers, Amazon shares slid more than 7% in after-hours trading as the company provided cautious guidance for the third quarter, projecting operating income between $15.5 billion and $20 billion. CEO Andy Jassy attempted to reassure investors about AWS’s “pretty significant” leadership position in cloud computing.

AI Investments and Competition

Both companies are heavily investing in artificial intelligence capabilities. Amazon has committed to spending up to $100 billion this year on AI infrastructure, including data centers and software development. Meanwhile, Apple faces criticism for its slower AI rollout compared to competitors.

Cook hinted at potential acquisitions, stating Apple is “open to M&A that accelerates our roadmap” and confirmed the company would “significantly grow” its AI investments. Industry analysts have suggested Apple should consider acquiring AI startups to catch up with rivals.

Tariff Impact and Future Outlook

Tariff concerns loomed large in both earnings reports. Apple incurred $800 million in tariff costs during Q3, lower than its initial $900 million estimate. Looking ahead, Cook warned that tariff costs could reach $1.1 billion in the September quarter if policies remain unchanged.

Amazon similarly cited “tariff and trade policies” and “recessionary fears” as factors that could affect future guidance. However, Jassy noted that tariffs haven’t significantly dented demand or driven up prices so far this year.

Looking Ahead

For the upcoming quarter, Apple expects mid- to high-single-digit revenue growth with gross margins between 46% and 47%, including tariff impacts. The company’s services segment faces a potential $20 billion threat if a federal judge rules against Google’s exclusivity deals in an ongoing antitrust case.

Amazon forecast third-quarter revenue between $174 billion and $179.5 billion, representing 10% to 13% year-over-year growth. The company’s cloud division, while still growing, showed signs of deceleration with three consecutive quarters of revenue misses.

Both tech giants demonstrate resilience in navigating a complex landscape of regulatory challenges, AI competition, and economic uncertainty. However, investors remain cautious about the sustainability of growth amid these headwinds, particularly as the companies face increasing pressure to deliver returns on their massive AI investments.

(Bloomberg) — Taiwan Semiconductor Manufacturing Co. raised its target for 2024 revenue growth after quarterly results beat estimates, allaying concerns about global chip demand and the sustainability of an AI hardware boom.

Most Read from Bloomberg

The main chipmaker to Nvidia Corp. and Apple Inc. now expects sales to climb about 30% in US dollar terms this year, up from previous projections for about a mid-20% rise. That’s after TSMC reported better-than-predicted earnings for the September quarter. And it foresees capital expenditure rising in 2025 from roughly $30 billion this year.

TSMC’s outlook should help tamp down concerns that investors mis-judged the AI and semiconductor demand. Those fears crystallized after chip industry linchpin ASML Holding NV stunned markets by reporting about half the orders investors had expected. On Thursday, Chief Executive Officer C. C. Wei sought to dispel those doubts. Shares of the company trading on Tradegate gained 7.4% versus their last close on the German exchange.

Shares of Japanese chip gear makers including Lasertec Corp. pared losses in Tokyo, while Infineon Technologies AG rose in Europe alongside sector peers.

“The demand is real and I believe it’s just the beginning,” Wei said, echoing a number of executives including Nvidia Corp.’s CEO. In terms of overall chip demand, “everything’s stabilized and start to improve.”

TSMC’s shares have surged more than 70% this year, outpacing many of Asia’s biggest tech firms in a reflection of strong sales of the Nvidia chips vital to artificial intelligence development.

For a liveblog on TSMC’s earnings, click here.

Taiwan’s largest company had raised its outlook for 2024 revenue just a few months ago in July, underscoring expectations for spending on AI infrastructure from the likes of Microsoft Corp. and Amazon.com Inc. Steady adoption of artificial intelligence should also help fuel sales of iPhones and other gadgets in the long run.

Still, investors had watched for deviations in TSMC’s outlook after ASML blamed slower-than-expected recovery in the automotive, mobile and PC markets, impacting expansion plans for chip plants. AI remains a bright spot, its executives said.

On Thursday, TSMC reported a better-than-projected 54% rise in September-quarter net profit to NT$325.3 billion ($10.1 billion). And it expects revenue of $26.1 billion to $26.9 billion in the final quarter, beating an estimate for $24.9 billion.

While official trading of the company’s American depositary receipts won’t begin for a while, the ADRs were up about 4.5% on Robinhood’s overnight trading platform. TSMC is popular among US retail investors seeking to bet on the AI theme.

What Bloomberg Intelligence Says

TSMC’s guidance of a 57%+ gross margin, which surpasses consensus, coupled with a fast ramp-up of N3 nodes, indicating continuous robust high-performance computing chips, like AI training chip, production demand from Nvidia and others. This aligns with our expectations. Sales growth should be able to exceed 25% in 2025, supported by strong AI chip demand and TSMC’s leadership in 3- and 5-nm nodes, alongside advanced CoWoS packaging.

– Charles Shum, analyst

Click here for the research.

The world’s largest maker of advanced chips has been one of the biggest beneficiaries of a global race to develop artificial intelligence. Its shares have more than doubled since that boom took off in late 2022 with the debut of OpenAI’s ChatGPT. TSMC’s market capitalization briefly crossed the $1 trillion mark in the US.

Yet even before ASML, some investors have grown cautious about the trajectory of global AI spending. They question whether big tech firms like Meta Platforms Inc. and Alphabet Inc. will continue to splash out on AI chips and data centers without a truly killer AI application.

The risks of data center over-capacity and geopolitical issues have unnerved some investors. Bloomberg reported this week that Biden administration officials have discussed capping sales of advanced AI chips from Nvidia and other American companies on a country-specific basis.

On Thursday, Wei said he expects revenue from AI server processors to more than triple this year, yielding a mid-teens percentage of total sales in 2024.

Longer-term, TSMC is pursuing a rapid international expansion.

It’s planning more plants in Europe with a focus on the market for artificial intelligence chips, according to a senior Taiwanese official. That’s on top of construction underway in Japan, Arizona and Germany.

–With assistance from Vlad Savov, Cindy Wang, Mayumi Negishi and Lianting Tu.

(Updates with shares and executives’ comments from the fourth paragraph.)

The biggest winners in the stock market over the last two years have all been great companies fueling the biggest innovations in artificial intelligence (AI).

Nvidia is the poster child of big AI stock winners. Its GPUs are essential equipment for training and running large language models. It has seen its stock climb 865% over the last 24 months, leading to a 10-for-1 stock split in June.

Nvidia was far from the only AI-fueled stock to split shares this year. It was joined by Broadcom, Super Micro Computer, and Lam Research, which all executed splits.

A stock split isn’t necessarily a catalyst for a stock to zoom higher. The fundamental value of a company doesn’t change when management decides to split its shares. And in today’s age of fractional shares, it only has a minor impact on making the stock more accessible to small investors.

But a stock split is a sign of confidence from management that shares will continue to climb, and few people have more insights into the future of a company and its stock than management.

So, investors are rightly interested in what could be the next stock to undergo a split. One company essential to the supply of AI semiconductors looks like a great candidate: ASML Holding(NASDAQ: ASML). And at today’s share price, investors should be looking to buy the stock before it announces a split.

An ASML machine printing a chip. Image source: ASML.

An essential part of the supply chain

ASML builds and services photolithography machines, which semiconductor manufacturing companies use to produce the chips designed by companies like Nvidia. Basically, without ASML’s machines, there are no AI chips.

It’s the only supplier of extreme ultraviolet lithography (EUV) machinery, a necessary technology for printing the most advanced chips, such as those used in AI data centers for training and running large language models. If a manufacturer is printing a high-end semiconductor, it’s using ASML’s machines.

Customers include Taiwan Semiconductor Manufacturing, Intel, and Samsung. All three revamped their foundries about a decade ago to accommodate ASML’s machinery.

But the company isn’t reliant on selling more machines every year to fuel revenue growth. It receives ongoing revenue from servicing machines already in use and selling replacement parts. The recurring revenue from servicing should grow as more machines are installed in chipmakers’ foundries.

ASML’s revenue from its installed base has grown significantly faster than its system sales over the last 15 years as foundries add more of its equipment to their operations while maintaining and updating old equipment. And given the long lifespans of ASML’s machines (25 to 30 years), that’s a steady and growing source of high-margin revenue.

Newer machines using the latest EUV technology will go into service next year. And the increased complexity of the high-end machines could result in even greater revenue from service and replacement parts relative to older machines.

The future looks bright

ASML referred to 2024 as a transition year. It doesn’t expect any revenue growth, and it forecasts gross margin contraction this year as it gears up to sell its latest EUV machines.

That stands in stark contrast to a company like Nvidia, which has seen revenue and profits continue to soar in 2024. So it’s no wonder investors haven’t been nearly as excited about ASML as they are about big-name chipmakers.

But that could be an opportunity for patient long-term investors. ASML expects 2025 to be a big year. Management’s outlook calls for between 30 billion and 40 billion euros ($33.17 billion to $44.2 billion) in revenue next year as foundry openings using its newest machines go into service. At its midpoint, that represents a 27% increase from 2023.

At its investor day in 2022, management provided an outlook for sales in 2030 of between $48.65 billion and $66.34 billion. Considering that was before the AI boom really took off, it’s a good bet that revenue will come in on the high end. Management might update that outlook to a higher or narrower range at its next investor day in November.

Along with sales growth, management expects strong margin expansion. It sees gross margins between 54% and 56% in 2025 and 56% and 60% by 2030. And while it hasn’t explicitly forecast operating margin expansion, it should see good operating leverage from its research-and-development and selling, general, and administrative expenses as its revenue scales up toward the $66 billion mark.

All of that should translate into very strong profit growth. And considering the technology lead and relationships ASML already has with the largest foundries in the world, there shouldn’t be much standing in the way of achieving those numbers.

Will this be the next big stock split?

ASML currently trades around $835 per share. While that’s well off its all-time high of around $1,100, it’s still quite a lofty price. Stocks have split with far lower prices.

The company last executed forward splits in the late 1990s and the year 2000 amid the dot-com boom. With a strong outlook based on the ongoing spending to build the next generation of AI chips, ASML could be motivated to split its shares in the near future as it sees significant growth ahead.

Even without a stock split, you should consider adding shares to your portfolio. The stock currently trades around 26 times forward earnings expectations. Given the potential for strong and predictable revenue increases and margin expansion for years to come, the company should be able to produce earnings growth that more than justifies that slight premium to the overall S&P 500. And when you compare ASML’s price to other AI stocks, it’s an absolute bargain.

Should you invest $1,000 in ASML right now?

Before you buy stock in ASML, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and ASML wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $765,523!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

Adam Levy has positions in Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends ASML, Lam Research, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom and Intel and recommends the following options: short November 2024 $24 calls on Intel. The Motley Fool has a disclosure policy.

(Bloomberg) — Alibaba Group Holding Ltd. reported a 6.6% rise in revenue after its main e-commerce and cloud businesses managed only modest growth.

Most Read from Bloomberg

Revenue for the three months ended March rose to 221.9 billion yuan ($30.7 billion), compared with analysts’ estimates for 219.8 billion yuan. Net income dived a worse-than-expected 86% after accounting for losses from publicly traded holdings. Its shares slid about 5% in pre-market trading.

Investors are closely watching results from Alibaba, a barometer of Chinese consumer sentiment, amid persistent worries about a loss of business to rivals from PDD Holdings Inc. to ByteDance Ltd. The choppy economic recovery is also roiling the company as it tries to revive growth after a years-long regulatory crackdown that kneecapped China’s private sector.

On Tuesday, the company announced a $4 billion dividend for the fiscal year. Alibaba and Tencent Holdings Ltd. both reported results on Tuesday, offering clues to whether the Hong Kong equity rally has legs. Alibaba, which owns slices of public companies including SenseTime Group Inc. and Sun Art Retail Group Ltd., didn’t disclose which specific losses hammered net income, which came in well below expectations. Its main Chinese commerce division managed just 4% revenue growth, while the cloud arm grew 3%.

Alibaba Chief Executive Officer Eddie Wu and Chairman Joe Tsai, longtime lieutenants of Jack Ma who took the helm from Daniel Zhang in September, are spearheading a turnaround of the e-commerce pioneer. They nixed major initiatives conceived under Zhang including listings logistics arm Cainiao and the $11 billion cloud unit, then decided to refocus on what they dubbed the customer experience and innovation.

Wu took the helm after a period of unprecedented turmoil at Alibaba, which contended with Covid, Beijing’s internet crackdown and then a Chinese economic downturn in rapid succession.

Ma weighed in on Alibaba’s turbulence last month, with a rare memo aimed at shoring up sagging morale among the company’s 200,000-plus employees. He emphasized that growth was returning at the company, despite its recent flip-flops, while acknowledging past mistakes.

Wu this year took direct charge of the company’s e-commerce and cloud services arm, both under pressure after a series of mis-steps and regulatory scrutiny. It’s tried to enhance customer service, beef up its product lineup and introduced features such as easy returns. On the cloud front, the once-promising division is slashing prices to regain clients from state-backed companies such as China Telecom Corp. and the likes of Huawei Technologies Co.

Away from the business, it’s hiving off non-core assets like stakes in streaming platform Bilibili and electric-vehicle maker XPeng Inc. to raise capital. It’s then funneled some of that cash into AI research and fast-growing startups like MiniMax.

(Updates with share action in the second paragraph. A previous story corrected the scale of its net income drop.)

Palantir stock (NYSE:PLTR) dipped by about 16% after its Q1 earnings report, prompting me to ponder whether this downturn presents a buying opportunity. Notably, Palantir showcased yet another quarter of solid revenue growth, promising client base expansion, and strong profitability metrics. That said, concerns persist regarding the stock’s elevated valuation. Consequently, despite my belief in Palantir’s long-term prospects as a shareholder, I maintain a neutral stance towards the stock at present and don’t believe the dip is worth buying.

Accelerating Growth Driven by Government and Commercial Clients

Palantir Q1’s marked a period of accelerating growth, driven by solid performance in both the company’s Government and Commercial segments. Revenues landed at $634.4 million, up 20.8% year-over-year. This implies an acceleration from last year’s growth of 17.7% and the third consecutive quarter of accelerating revenue growth on a sequential basis. Let’s take a deeper look at both Palantir’s segments in Q1 to better understand what precisely drove this result.

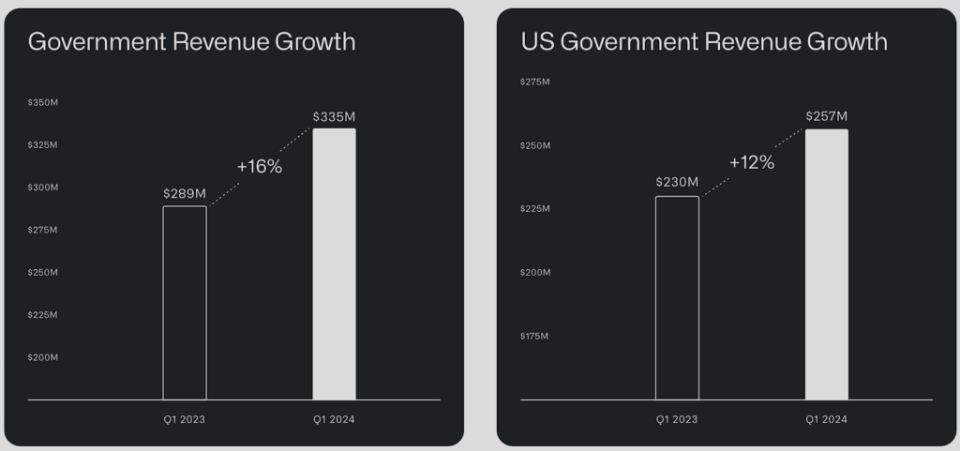

Government Revenue Fueled by Domestic Acceleration, International Expansion

Starting with Palantir’s Government segment, which accounted for about 53% of its Q1 revenue mix, total revenue growth in this segment was 16%, at $335 million. This growth was mainly driven by accelerating revenues in the domestic division and rapid international expansion.

Source: Palantir’s Q1-2024 Investor Presentation

Domestically, revenue growth accelerated in Q1 in the U.S. Government business, increasing by 12% year-over-year and 8% quarter-over-quarter to $257 million. This compares against a 3% quarter-over-quarter increase in Q4, with Palantir’s software becoming increasingly critical for the U.S. Government in today’s unstable geopolitical environment. Palantir’s International Government division further compounded the segment’s growth, with its revenues rising by 33% to $79 million.

An important milestone in Q1 was that the U.S. Army granted Palantir an exclusive prime contract worth over $178.4 million to develop a next-generation targeting node as part of the TITAN program. This marks a historic moment for Palantir, as it became the first software company ever to win a prime contract for a hardware system. This effectively positions Palantir to establish itself as a prime vendor akin to giants like Lockheed Martin (NYSE:LMT) or Northrop Grumman (NYSE:NOC) in the field of weapons and aerospace products.

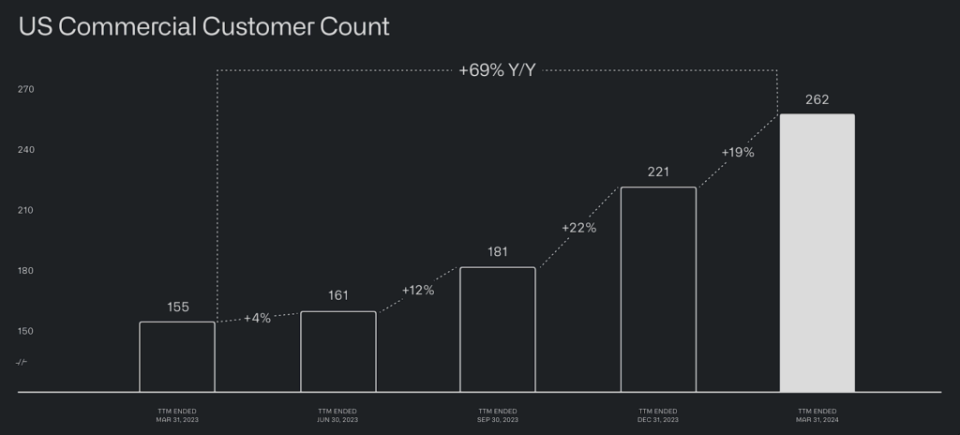

Commercial Revenue Surges Following Rapid Client Base Expansion

Transitioning to Palantir’s Commercial segment, revenues experienced another notable surge, driven by the increasing uptake of its artificial intelligence platform (AIP) and the solid expansion of the company’s clientele.

In a prior update on Palantir, I emphasized the pivotal role of Bootcamps in bolstering Palantir’s corporate customer base. Palantir organizes these hands-on workshops to showcase the capabilities of its software, notably its AIP. Successful demonstrations should allow potential clients to realize the value proposition Palantir offers and potentially commit to a contract.

This strategy seems to be working extremely well for the company. In Q1, Palantir added 41 net new customers in its U.S. Commercial segment (see the image below). This marked a 69% increase in Palantir’s customer count year-over-year and 19% quarter-over-quarter. Palantir also recorded a significant acceleration here, compared to the 8% quarter-over-quarter growth of last year’s Q1.

Source: Palantir’s Q1-2024 Investor Presentation

Rapidly Improving Profitability, But Valuation Concerns Remain

Palantir’s strong revenue growth has gradually allowed the company to record improving unit economics, thus improving its profitability metrics. The company’s adjusted operating margin landed at 36%, up from 34% in the previous quarter and 24% last year, marking the sixth consecutive quarter of expansion. It led to an adjusted operating income of $226.5 million, up 81% compared to last year. Further, Palantir’s adjusted free cash flow came in at $149 million, also achieving a noteworthy margin of 23%.

With additional cash flowing into Palantir’s balance sheet, the company ended the quarter with a record cash position of $3.87 billion, all while maintaining a debt-free status. Nevertheless, investors should still take into account the underlying risks involved in Palantir’s current valuation, no matter how impressive its profitability metrics and robust financial standing are.

At the end of the day, Palantir is still trading at approximately 65 times this year’s expected earnings per share (EPS) and 54 times next year’s expected EPS. Its revenue growth acceleration and ongoing margin expansion may allow the company to grow into these multiples sooner rather than later. Still, Palantir’s investment case offers a notably lower margin of safety compared to last year’s levels, even after the post-earnings dip—and this is coming from a shareholder with high hopes.

Is PLTR Stock a Buy, According to Analysts?

The present sentiment on Wall Street seems bearish, even after Palantir’s post-earnings share price decline. According to Wall Street, Palantir Technologies features a Moderate Sell consensus rating based on two Buys, five Holds, and six Sells in the past three months. At $19.67, the average PLTR stock price target suggests 4.5% downside potential.

If you’re wondering which analyst you should follow if you want to buy and sell PLTR stock, the most profitable analyst covering the stock (on a one-year timeframe) is Mariana Perez from Bank of America (NYSE:BAC) Securities, with an average return of 61.42% per rating and a 92% success rate. Click on the image below to learn more.

The Takeaway

To sum up, Palantir’s Q1 report reflects an ongoing acceleration in revenue growth, evident in both its Government and Commercial segments. With Governments relying increasingly on Palantir’s software during an unstable geopolitical environment and corporate clients gradually realizing the capabilities of AIP, Palantir’s long-term prospects appear more promising than ever.

However, the persistent concern over the stock’s valuation cannot be overlooked. While Palantir shows promise for long-term investors, and I am one of them, a neutral stance on the stock seems reasonable, given its elevated valuation multiples. Accordingly, I wouldn’t buy the stock on this dip if I were looking to initiate a position in Palantir. I’d rather wait for a potentially more attractive entry point.

One of the biggest themes fueling a sharp rebound in the market last year was artificial intelligence (AI). Applications such as ChatGPT have taken the world by storm, and megacap tech companies such as Microsoft, Alphabet, Amazon, and Nvidia are spending billions to gain an edge in the AI arena.

Other software players making inroads in the space are often overlooked in relation to their larger peers. Two such companies in the data analytics space are taking very different approaches to AI. Let’s take a look at how Snowflake(NYSE: SNOW) and Palantir Technologies(NYSE: PLTR) are competing in AI, and assess which company looks like the winner.

Palantir is bringing the heat…

Palantir has long been considered a government contracting business given the company’s close ties to the U.S. military and its Western allies. Although the company develops a host of software products, many Wall Street pundits remained skeptical of Palantir’s tech chops. In fact, a short report published by The Bear Cave nine months ago went as far as labeling Palantir an “AI imposter.”

But in 2023, Palantir caught the bears off guard thanks to the success of its fourth big product: the Palantir Artificial Intelligence Platform (AIP). Since AIP’s commercial launch last April, Palantir has performed nearly 850 demo pilots for the new software platform. By comparison, the company did 92 pilots in 2022.

What’s even more impressive is the rate at which these demos are converting to paid customers. Last year, Palantir grew its customer count by 35% year over year. However, customer growth from its non-government operation was the real winner — increasing by 44%.

In addition to accelerating its top line, Palantir has been demonstrating disciplined financial operation all around. The company has reported profits on a generally accepted accounting principles (GAAP) basis in five consecutive quarters, and its balance sheet ended 2023 with $3.7 billion of cash and equivalents, and no debt.

I see the advent of AIP as a first step in Palantir’s changing investors’ perception of it from a government contractor to an actual software-as-a-service (SaaS) business.

Image source: Getty Images.

…and the snow is melting

Snowflake has almost a polar opposite narrative to that of Palantir. When it was still private, Snowflake attracted some of the world’s most renowned venture capitalists. Moreover, the company’s innovative data warehousing service helped fuel staggering revenue growth for years. Unsurprisingly, Snowflake completed the largest software initial public offering in history in 2020 — and even saw participation from the likes of Warren Buffett.

Nevertheless, since hitting the public exchanges in late 2020, the growth narrative surrounding Snowflake has started to cool. The company’s revenue growth has started to slow down significantly, and while some of this can be attributed to a challenging economy, there is more to the picture than decelerating sales.

One of the most important metrics for SaaS businesses is net revenue retention (NRR), which measures how much revenue is expanding net of any churn the company experiences. If the ratio is above 100%, that implies that the company is outselling its churn.

Indeed, Snowflake’s recent NRR of 131% isn’t anything to cry about. However, what’s concerning is that the company’s NRR has declined in eight consecutive quarters. With revenue growth slowing down, and retention concurrently in decline, it’s no wonder that Snowflake is still hemorrhaging cash — reporting a GAAP net loss of $836 million in 2023.

What’s potentially the most concerning of all is Snowflake’s lack of urgency surrounding AI. In mid-2023, the company acquired a start-up called Neeva, which specializes in generative AI applications geared toward cloud-based data sets. Since the acquisition, Snowflake has been pretty tight-lipped about its AI strategy. And with the company’s CEO resigning on Feb. 28, it seems to me that Snowflake’s future and its place in the AI landscape are enigmatic, at best. Frank Slootman will remain as chairman of the board at Snowflake and Senior Vice President of AI Sridhar Ramaswamy has taken over as CEO.

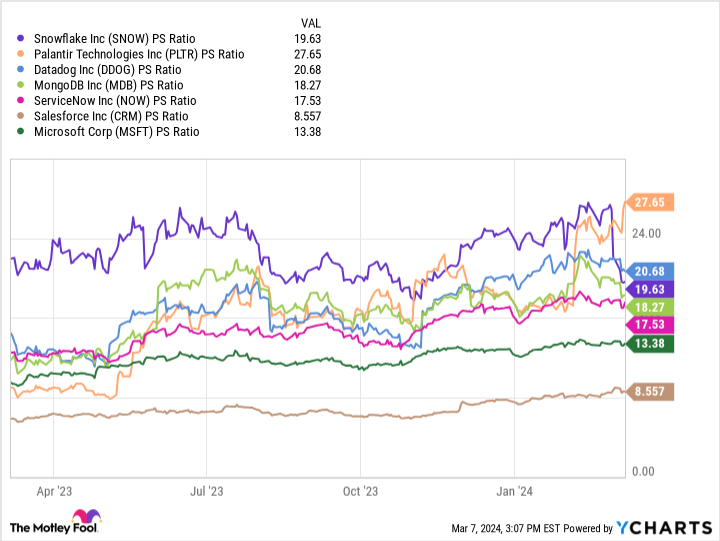

Valuation

The chart below shows the price-to-sales (P/S) ratios for a number of growth SaaS stocks. At a P/S around 28, Palantir is the highest-valued company in this cohort based on this metric. However, it’s important to note that Palantir’s valuation has expanded significantly since its blowout fourth-quarter earnings report last month. I think the company’s premium valuation is warranted, and am bullish about the long-term potential of AIP.

SNOW PS Ratio Chart

On the other hand, I do not see the recent decline in Snowflake’s stock price as an opportunity to buy the dip. The company appears to be at a crossroads, and could very well be falling behind in the AI revolution.

With strong revenue growth, steady profits, accelerated customer acquisition, and a concrete AI vision, I see Palantir as the clear winner compared to Snowflake. A prudent strategy could be to use dollar-cost averaging to start building a position in Palantir, or add to an existing allocation.

Should you invest $1,000 in Palantir Technologies right now?

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Microsoft, Nvidia, and Palantir Technologies. The Motley Fool has positions in and recommends Alphabet, Amazon, Microsoft, Nvidia, Palantir Technologies, and Snowflake. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Tesla (NASDAQ: TSLA) has been one of the best-performing stocks on the market over the last decade as it proved that electric vehicles (EVs) can be a viable business, and even a highly profitable one. However, recently, Tesla stock has been looking surprisingly mortal. The stock trades down by roughly half from its peak in 2021, and its fourth-quarter earnings report shows why the stock has faded.

Tesla’s revenue growth continues to slow and profits are falling, and that pattern continued in Q4. Automotive revenue rose 1% year over year to $21.6 billion, and overall revenue was up just 3% to $25.2 billion. These metrics reflect the impact of lower prices as the company looks to stay competitive, gain market share, and overcome headwinds from higher interest rates.

As a result of lower prices, operating income fell 47% year over year to $2.06 billion, and adjusted earnings per share fell 40% to $0.71. Tesla missed estimates on the top and bottom lines, and it also forecast slower production growth in 2024.

Seemingly, Tesla is less of a millionaire-maker stock than it was two years ago. What’s an ambitious investor to do with this news? If you’re looking for growth stocks that can help make you a millionaire, keep reading.

Image source: Tesla.

Nvidia has powerful tailwinds pushing it higher

Tesla and every other artificial intelligence (AI) stock can’t make their technology without the help of one company, and that’s Nvidia (NASDAQ: NVDA).

Nvidia stock soared over the last year as its chips are in extraordinarily high demand from companies like OpenAI, Oracle, Meta Platforms, and Tesla, among others. Nvidia, which invented the graphics processing unit (GPU), has a significant head start over its rivals. AI systems like OpenAi’s ChatGPT and autonomous vehicle systems like Tesla’s full self-driving rely on massive training models that use the kind of chips and accelerators Nvidia makes.

That strong demand should help power Nvidia stock higher this year as it’s coming off a third quarter in which revenue tripled year over year and its generally accepted accounting principles (GAAP) profit rose by 12x.

As profits have soared, the company’s valuation has come down, and it appears to be set for another strong year in 2024 as cloud infrastructure companies and others are still rapidly building out their AI infrastructure. This should favor Nvidia.

General Motors is more profitable than Tesla

Tesla made its name in electric vehicles, but there are signs of slowing demand for EVs that could spell trouble for Tesla and its peers. It also creates an opening for traditional automakers like General Motors (NYSE: GM) whose stocks got hammered as investors chased EV stocks and abandoned legacy automakers.

As a result, GM stock now trades at a price-to-earnings ratio of just 5. GM may not offer the same growth potential that Tesla does, but the company has a growing EV and autonomous vehicle (AV) business in Cruise, whose rollout has taken a pause after San Francisco regulators suspended operations.

GM remains more profitable than Tesla and is reporting solid growth with a 14% increase in vehicles sold to 2.6 million. That’s a strong growth clip for a mature business and from a stock priced for no growth. Notably, that’s also significantly faster than Tesla’s Q4 revenue growth.

GM’s low valuation also gives the company a greater opportunity to return cash to shareholders. In fact, the company announced a $10 billion accelerated share repurchase program in November and raised its dividend by 33% to $0.12 a share.

Considering the growth in its legacy car business and its investments in electric vehicles and autonomy, GM should be able to bridge the gap with EVs and AVs when the time comes. If GM delivers another strong earnings report, the stock could soar.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Jeremy Bowman has positions in Meta Platforms. The Motley Fool has positions in and recommends Meta Platforms, Nvidia, Oracle, and Tesla. The Motley Fool recommends General Motors and recommends the following options: long January 2025 $25 calls on General Motors. The Motley Fool has a disclosure policy.

(Bloomberg) — Taiwan Semiconductor Manufacturing Co. expects a return to solid growth this quarter and gave itself room to raise capital spending in 2024, suggesting the world’s most valuable chipmaker anticipates a recovery in smartphone and computing demand.

Most Read from Bloomberg

The main chipmaker to Apple Inc. and Nvidia Corp. projected revenue growth of at least 8% to $18 billion to $18.8 billion in the March quarter, versus expectations for around $18.2 billion. And it’s budgeting capital expenditure of $28 billion to $32 billion, potentially up from 2023’s $30 billion.

The Taiwanese company’s outlook, while not quite surpassing the most bullish estimates, comes after a years-long slump in tech demand. But signs of a recovery for the chipmaking sector have emerged in recent weeks. The Semiconductor Industry Association estimated chip sales increased in November after more than a year of declines. Chief Executive Officer C. C. Wei reiterated he expects a return to “healthy growth” this year.

TSMC, which also counts Android chipmaker Qualcomm Inc. among its biggest customers, got a boost from frenzied demand for Nvidia’s artificial intelligence chips in 2023. It reported net income for the fourth quarter of NT$238.7 billion ($7.6 billion), beating the average analyst estimate. Revenue was $625.5 billion, TSMC reported earlier, matching the previous holiday quarter and arresting a series of falls.

“Our business has bottomed out on a year-over-year basis, and we expect 2024 to be a healthy growth year for TSMC,” Wei said.

Click here for a liveblog on the numbers.

What Bloomberg Intelligence Says

TSMC could lead global chip foundries through 2023-24 industry headwinds thanks to growing AI chip demand and migration to next-gen process nodes such as N3 in 2H23 and N2 by 2025. Although the smartphone and PC chip market remains stagnant, TSMC’s advanced packaging tech, both 2.5D and 3D, fortifies its position in the contract-chipmaking market, allowing a potential return to a 53% gross margin following a brief 2H downturn.

— Charles Shum, analyst

Click here for the full research.

TSMC’s revenue should grow in the low- to mid-20% range this year, Wei said. That’s a rebound from the modest decline of last year.

Over the course of 2023, TSMC moderated its capital expenditure plans as the consumer electronics industry grappled with a glut of unsold inventory.

But uncertainty persists. This month, fellow chipmaker Samsung Electronics Co. posted its sixth successive quarter of declining operating profit, as it weathered the impact of muted consumer demand in its own smartphone and memory businesses.

Questions also overshadow China, the world’s largest computing, smartphone, internet and chip market.

Apple — long one of TSMC’s most important customers — faced headwinds with its latest iPhone generation. Several analysts downgraded Apple on expectations of soft demand, and Jefferies has said the iPhone sales slump in China is likely to deepen. The US company has also been hit by a widening ban on foreign-device use among Chinese agencies and state-owned companies.

Advanced Micro Devices (NASDAQ: AMD) has become one of the more notable comeback stories in recent years. Left for dead in the middle of the last decade, it has become a leader in CPU, GPU, and embedded chips under the leadership of CEO Lisa Su.

With it making advancements in the AI field, AMD stock is on an upward trajectory, rising 127% in 2023. However, determining whether the semiconductor stock can mint millionaires from here requires a closer look.

The state of AMD

AMD stock has benefited from a tremendous level of success under Su and has the potential to go much higher. When Su took over in 2014, she limited the company’s focus to CPUs and GPUs. Since product development timelines in the semiconductor industry take at least three years, Su’s vision took time to bear fruit.

Nonetheless, in that time, the company’s CPUs surpassed the performance of those of longtime rival Intel. In the GPU field, it won contracts to power Sony‘s PlayStation and Microsoft‘s Xbox. Additionally, its GPUs have helped it gain traction on Nvidia in some cases, and helped its data center technologies take market share from Intel.

Moreover, just when it looked like Nvidia would dominate AI chips, AMD released its Instinct MI300A accelerator chip and the MI300X GPU, which AMD claims is a faster chip than Nvidia’s H100.

These new offerings have stoked investor optimism, taking the semiconductor stock to 52-week highs in late December. Over the last year, AMD stock has more than doubled.

Why minting millionaires from here may be a struggle

Unfortunately, turning small investors into millionaires would take a level of growth beyond the imaginations of many. With AMD’s recovery, its market cap has reached almost $220 billion, taking it into mega-cap status.

If an investor bought $10,000 worth of AMD stock today, the market cap would have to reach nearly $22 trillion for that position to become $1 million. Currently, the stock with the highest market cap, Apple, has a market cap of around $3 trillion, less than one-seventh that amount.

Also, AMD’s financials would have to make considerable improvements to send the stock into hyperdrive. In the third quarter of 2023, its revenue of $5.8 billion grew 4% year over year, compared with a 9% yearly decline for revenue in the first three quarters of the year.

AMD’s revenue growth should improve. Still, even if it can find a way to match Nvidia’s 206% revenue growth in its third quarter of fiscal 2023 (ended Oct. 29), it will likely not make recent investors with only a few thousand to invest into millionaires .

Millionaire status is more reachable for large investors who bought the stock on Oct. 8, 2014, the day Su became AMD’s CEO. If you’d started a $10,000 position then, it would be worth approximately $414,000 today, meaning if the stock jumps another 127% in 2024, those investors’ original investment would be close to $1 million.

AMD as a millionaire maker

Although AMD can probably help an investor make money on the road to becoming a millionaire, it has probably grown too large to accomplish that feat on its own for small investors. As a mega-cap stock, it is unlikely to achieve the 100-fold or more increases needed to turn $10,000 into $1 million.

Nonetheless, AMD’s performance has far exceeded that of the indexes during Su’s time at the company. Given past successes, that trend is likely to continue. Hence, even if one cannot become a millionaire, an investor could become significantly richer with a long-term investment in AMD stock.

Should you invest $1,000 in Advanced Micro Devices right now?

Before you buy stock in Advanced Micro Devices, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Advanced Micro Devices wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

Will Healy has positions in Advanced Micro Devices and Intel. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Microsoft, and Nvidia. The Motley Fool recommends Intel and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $45 calls on Intel, and short February 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.