[ad_1]

Have questions — or worries — about retirement? Here’s your chance to pose them.

[ad_2]

[ad_1]

Have questions — or worries — about retirement? Here’s your chance to pose them.

[ad_2]

[ad_1]

Why earnings season is one of the most important times for stock investors

[ad_2]

[ad_1]

Coronavirus Update: New York City scraps public-sector-worker vaccine mandate

[ad_2]

[ad_1]

It has become increasingly popular to plan for early retirement. Specifically among younger people. According to a CNBC Make It: Your Money survey in partnership with Momentive, nearly 30% of millennials and 25% of Gen Zers expect to need $1 million or more to retire comfortably.

Additionally, according to Fidelity Investments, retirement can last as long as 25 years.

Of course, meeting this financial goal when 55% of working Americans claim that they are behind on their retirement savings seems impossible. However, don’t get too frustrated if you believe that you’ll never be able to retire early. There’s no reason why you can’t retire at 50, 55, or 60 and have plenty of time left in life to enjoy new experiences. In order to succeed, though, you need to plan carefully and have a strong will.

As a CFP®, there are so many questions that I have before giving you the green light to retire early. These questions include:

Why ask these questions? In my experience, I’ve seen people retire early when they’ve planned well ahead. All projections have been made. Sometimes things go wrong and there’s an emergency, whether it’s a medical one or repairing your car. As a result, they are forced to take money out of their retirement accounts.

Another problem? Underestimating retirement expenses. It’s not for the health stuff either. It’s for selfish reasons. In fairness, I don’t mean selfish in a negative way. You’re probably going to take your family on vacation, buy the latest iPhone, make home improvements, or go out to dinner.

You might burn through your retirement budget if you ignore any of these factors.

When it comes to meeting your financial goals, a good professional can make all the difference. In order to retire early, people must be able to save and invest properly, and most beneficiaries of proper guidance can greatly benefit from it. And, in particular, I’m talking about a CFP®.

You can start by visiting cfp.net. Click on find a CFP professional at the top and then enter your zip code to find a CFP professional near you. You can do this on your phone as well.

Keep in mind that you’ll have to meet certain minimums. You may not be able to work with some investment firms if you don’t have a million dollars, for example. So, I suggest picking two or three that seem to fit with your goals and seem to fit well with your style.

Ideally, you should work with a retirement planning specialist. Specifically, someone knowledgeable about income distribution. Their mission is to help you create a retirement income stream that will last for the rest of your life.

To get an idea of how much you’ll need to save, invest, or diversify to have a steady retirement income, there are several online retirement calculators available. There are many free and easy-to-use calculators available online.

You just need to enter some basic information into the calculator. A few examples would be your annual income and the age at which you plan to retire. After you input these numbers, the calculator crunches them to provide you with a few suggestions about your retirement planning.

While a retirement savings calculator can help you estimate your retirement income needs, it often makes assumptions. It is hard to predict expenses, especially health care costs, and these calculators don’t account for retirees’ ability to adjust to changes in their lives. Rather than draining your savings to cover higher medical expenses one year, you may choose to make cuts elsewhere.

Likewise, the market is beyond your control. It’s impossible to predict what the stock market will do from year to year over a long enough period of time. And, equity returns are just guesses based on historical averages.

If you are not comfortable with retirement savings calculators, Vanguard provides a tool on its website that generates ranges of possible outcomes and probabilities based on your current retirement savings. By running multiple simulations of your inputs and measuring the frequency of each outcome, a Monte Carlo simulation approximates the probability of certain outcomes.

In order to prepare for early retirement, you must also begin saving very early. If you get started sooner, you’ll have to put less effort into it.

As an example, let’s take a look at how it works.

Say you want to retire at 55 and need $1 million. It is estimated that you will earn $100,000 per year between now and retirement.

An average annual rate of return of 7% can be achieved by investing in a blended portfolio of stocks and bonds.

You probably won’t be able to retire at 55 if you’re over 40 and starting from zero. It’d require you to save at least 100% of your income.

Typically, people believe that if they save 10% or 15% of their income, they can retire. If you plan to retire at 55 or even 60 and have 35 or 40 years to invest and save, that may be true.

Saving more money at 50 is necessary if you’re serious about retiring at 50. Your savings might be as much as 20% of your income, or maybe even 25% or 30%. If you intend to retire at 50, you will have to save 40% to 50% of your income if you are older than 25 or 30.

Saving 20% is a good place to start.

Instead of spending the extra money from every pay rise or promotion, put it into your savings. Eventually, you should be able to increase your savings rate to 30% or even higher after a few years of steady pay increases.

You accomplish two very important goals by saving such a large percentage of your income:

When you retire, that second point will be extremely important. Retirement will be quicker and more effective if you have less money to live on now.

Rather than relying only on your ability to build up a massive nest egg to get you to retirement, consider cultivating multiple income streams, suggests Miranda Marquit in an article for Good Financial Cents. You should instead plan to pay off your debt (including your mortgage) by the time you plan to retire early.

“Try to rid yourself of as many obligations as possible, so that you will have fewer expenses during retirement,” Miranda adds. As you prepare for the future, make a plan to pay off this debt. “Figure out how much money you will need each month to support your retirement lifestyle and then begin cultivating different income streams to create that income.”

“While there are rules that allow you to begin withdrawing from an IRA early, you likely won’t have access to Social Security benefits during an early retirement,” says Miranda. If necessary, consider early withdrawals from an IRA, but consider other sources of income as well, such as:

“It is, of course, possible to cultivate a number of income streams at once, diversifying your income sources,” Miranda advises. “Start now to develop these streams so that they are established and mostly automatic by the time you are ready for early retirement.”

It’s pretty much necessary to have a high-risk tolerance when saving for early retirement. If you invest in safe assets, such as certificates of deposit, you won’t reach your goal.

There may be some safe assets you can own, but the majority will need to be riskier investments. In addition to stocks, these include mutual funds and exchange-traded funds (ETFs).

Real estate investment trusts (REITS) may also be included since they often produce returns comparable to stock returns. Ultimately, you’ll have to invest heavily in assets carrying a high level of risk. This may result in a loss of some of your investment.

It is possible to lose money on a stock portfolio at any time. There is even a possibility that you might lose money for two or more years consecutively. That will require some preparation on your part.

In the long run, though, risk assets are a good investment.

A single investment can lose money in a given year, but multi-year investments provide the best returns.

The good news? The numbers work in your favor. Over the past 90 years, the stock market has returned an average of between 9% and 11%.

Do you really want to be aggressive? Invest everything in stocks. You should be able to earn around 10% per year over the course of 20 or 30 years.

If you prefer to play it a little safer, an allocation of 90% stocks will reduce your return to 9%, and an allocation of 80% will bring it to 8%.

The returns on either are, however, still solid. This is particularly true if you invest most of your money in tax-sheltered retirement accounts.

Early retirement planning is hampered by taxes, which are under-estimated obstacles. Taxes not only reduce your income but also decrease your investment returns.

Suppose you earn 10% on your investments, but your tax bracket is 30%, meaning you will only receive 7% in net returns. Consequently, you will have a slower capital accumulation rate.

It is possible, at least partially, to overcome that problem. Contribute as much as you can to your tax-sheltered retirement account.

By doing so, you’ll lower your taxable income from your job. In addition to protecting your investment earnings, you will also receive a 10% return on your portfolio.

The maximum contribution you are allowed to make to your 401(k) plan should be made by you if your employer offers one. A total of $22,500 would be available each year. You may be able to get a matching contribution from your employer.

Additionally, you should contribute to a traditional IRA, even if the contributions won’t be tax-deductible. If you set up a tax-deferred investment account, you can invest and accumulate profits tax-deferred.

In terms of early retirement, there’s a basic problem with retirement savings. When you withdraw from your retirement accounts before you’re 59 ½, you’ll be subject to both income taxes and capital gains taxes.

However, Roth IRAs can solve this problem.

A Roth IRA doesn’t require you to contribute every year to get its benefits. You can convert other retirement accounts, like 401(k)s and traditional IRAs, to a Roth IRA. It’s another good reason to max out your retirement savings — especially if you’re planning on retiring before 60.

When you’re 59 1/2 and have been in the Roth IRA for at least five years, you can withdraw money tax-free from it. There’s also a provision for tax-free withdrawals before age 59 ½.

This is where Roth conversion ladders come in. You can convert money from an IRA, 401(k) or 403(b) into a Roth IRA.

Withdrawals are tax-free once they are made.

You can take withdrawals tax-free and penalty-free from Roth IRA contributions or conversion balances. They’re called Roth IRA withdrawal ordering rules.

According to those rules, Roth IRAs can only withdraw contributions or converted balances first. After those are taken, investment earnings can be withdrawn.

If you want to avoid the 10% penalty, you have to be in the Roth for at least five years. It’s here where the Roth conversion ladder comes in.

For early retirement, you can create a tax-free income source by making annual conversions starting five years before withdrawals are needed.

If you’re planning to retire early the strategy works great.

Because the ladder covers just five years until you can start taking regular withdrawals from your other retirement accounts penalty-free at age 59 ½. it’s perfect for early retirees.

If you do not manage your debt properly, it can undo all of your efforts to retire early. As an example, the fact that you have $500,000 in savings but $100,000 in debt of varying types will do you little good when you reach 50.

Additionally, debt comes with monthly payments that erode your net worth. At 50 you’ll want to retire with as few of those as possible.

Even better? Debt-free living should be the goal.

In order to be debt-free, you need to include your mortgage if you have or plan to have a mortgage. If you plan to retire early, you should include a sub-plan for paying off your mortgage before you do so.

Living below your means is one financial habit you’ll need to develop. So if you make a dollar after taxes, you’d have to live on 70 cents and bank the remainder.

I know it’s difficult to get into that pattern if you’ve never done it before, but it’s vital. After all, early retirement will just be a pipe dream unless you master it.

You’ll need to adopt a few strategies to live within your means:

Having extra money for savings is better than having it go to living expenses.

When you take “Substantially Equal Periodic Payments” (SEPPs) from your qualified accounts (such as 401(k), IRA, Roth IRA, etc.) before age 59 ½, you are not subject to the 10% penalty rule. It’s also known as the “72(t) exception.”

To stay within SEPP rules, you can choose one of three different methods:

Based on your life expectancy and a permitted interest rate, the fixed amortization method determines your annual payment. The IRS recently made changes that have increased the amount that can be withheld without incurring the 10% penalty, so this calculation offers a significant increase.

Why?

Prior to the IRS’s changes, “reasonable interest rates” were calculated using low-interest rates tables published monthly. In December 2022, the rate was 1.52%. Now that the new ruling is in place, the floor rate is 5%. If one wishes to maximize the amount of money they can withdraw penalty-free each year before 5912, this offer is much more appealing.

If you decide how much money you want to withdraw, you have to stick with that method for five years or until you turn 5912. A one-time switch to the RMD method, usually resulting in a smaller payment, is the only exception. You might find this useful if you decide to go back to work and no longer wish to maximize your withdrawals.

Instead of estimating your monthly expenses, it’s recommended that you calculate them. Consider this question: “Am I clear about how much money I need to live comfortably on? “

Knowing how much money you’ll need for retirement can help you determine if your savings will last.

As early as age 62, you can begin receiving Social Security retirement benefits, but your benefits could be reduced by up to 30 percent.

Depending on when you were born, you may be able to receive benefits before you reach full retirement age, which can range from 65 to 67.

Working part-time and taking Social Security will reduce your benefits if you earn too much money. In addition, determine which retirement accounts you need to withdraw money from first in order to avoid tax penalties.

Medicare kicks in at 65, so find out if your employer can provide health insurance during the interim, or if you’ll need private coverage.

Although it is possible to retire on a million dollars, it won’t be easy. In order to ensure that your savings don’t outlive you, you should carefully budget and invest your money. If you plan carefully, you can retire on $1 million comfortably. Despite this, if you do not take care of your finances in retirement, you may struggle.

Having a nest egg that size is necessary to retire with $1 million. To reach your savings goal, you will need to continue saving and working until you reach it. You can start planning your retirement once you have reached your goal.

When planning for retirement, there are a few things to keep in mind. The first thing you need to do is make sure you have enough money saved to cover your expenses. Living expenses, healthcare costs, and other retirement expenses all fall under this category.

Considering your income needs in retirement would also be helpful. Having enough income will allow you to cover your basic living expenses and still have a little left over to enjoy leisure activities and other pursuits.

Last but not least, consider how you may generate income after retirement. Consider part-time work or other income sources, such as pensions or investment earnings, if you need to continue working.

The post Is $1 Million Enough to Retire Early? appeared first on Due.

[ad_2]

Jeff Rose

Source link

[ad_1]

BP reports 4Q underlying replacement cost of $4.8 billion, just shy of forecasts

[ad_2]

[ad_1]

Coronavirus Update: California drops COVID-19 vaccine requirement for students

[ad_2]

[ad_1]

The Baby Boomer Retirement Crisis Is Here. Why the Richest Generation Is Struggling.

[ad_2]

[ad_1]

News flash: We may be in a new bull market.

That’s the good news. The not-so-good news is that the recent rally may have gotten ahead of itself and a pullback would be health-restoring to the bull market.

Read: Jobs report shows blowout 517,000 gain in U.S. employment in January

The…

[ad_2]

[ad_1]

Do you want the good news about the Federal Reserve and its chairman Jerome Powell, the other good news…or the bad news?

Let’s start with the first bit of good news. Powell and his fellow Fed committee members just hiked short-term interest rates another 0.25 percentage points to 4.75%, which means retirees and other savers are getting the best savings rates in a generation. You can even lock in that 4.75% interest rate for as long as five years through some bank CDs. Maybe even better, you can lock in interest rates of inflation (whatever it works out to be) plus 1.6% a year for three years, and inflation (ditto) plus nearly 1.5% a year for 25 years, through inflation-protected Treasury bonds. (Your correspondent owns some of these long-term TIPS bonds—more on that below.)

The second bit of good news is that, according to Wall Street, Powell has just announced that happy days are here again.

The S&P 500

SPX,

jumped 1% due to the Fed announcement and Powell’s press conference. The more volatile Russell 2000

RUT,

small cap index and tech-heavy Nasdaq Composite

COMP,

both jumped 2%. Even bitcoin

BTCUSD,

rose 2%. Traders started penciling in an end to Federal Reserve interest rate hikes and even cuts. The money markets now give a 60% chance that by the fall Fed rates will be lower than they are now.

It feels like it’s 2019 all over again.

Now the slightly less good news. None of this Wall Street euphoria seemed to reflect what Powell actually said during his press conference.

Powell predicted more pain ahead, warned that he would rather raise interest rates too high for too long than risk cutting them too quickly, and said it was very unlikely interest rates would be cut any time this year. He made it very clear that he was going to err on the side of being too hawkish than risk being too dovish.

Actual quote, in response to a press question: “I continue to think that it is very difficult to manage the risk of doing too little and finding out in 6 or 12 months that we actually were close but didn’t get the job done, inflation springs back, and we have to go back in and now you really do have to worry about expectations getting unanchored and that kind of thing. This is a very difficult risk to manage. Whereas…of course, we have no incentive and no desire to overtighten, but if we feel that we’ve gone too far and inflation is coming down faster than we expect we have tools that would work on that.” (My italics.)

If that isn’t “I would much rather raise too much for too long than risk cutting too early,” it sure sounded like it.

Powell added: “Restoring price stability is essential…it is our job to restore price stability and achieve 2% inflation for the benefit of the American public…and we are strongly resolved that we will complete this task.”

Meanwhile, Powell said that so far inflation had really only started to come down in the goods sector. It had not even begun in the area of “non-housing services,” and these made up about half of the entire basket of consumer prices he’s watching. He predicts “ongoing increases” of interest rates even from current levels.

And so long as the economy performs in line with current forecasts for the rest of the year, he said, “it will not be appropriate to cut rates this year, to loosen policy this year.”

Watching the Wall Street reaction to Powell’s comments, I was left scratching my head and thinking of the Marx Brothers. With my apologies to Chico: Who you gonna believe, me or your own ears?

Meanwhile, on long-term TIPS: Those of us who buy 20 or 30 year inflation-protected Treasury bonds are currently securing a guaranteed long-term interest rate of 1.4% to 1.5% a year plus inflation, whatever that works out to be. At times in the past you could have locked in a much better long-term return, even from TIPS bonds. But by the standards of the past decade these rates are a gimme. Up until a year ago these rates were actually negative.

Using data from New York University’s Stern business school I ran some numbers. In a nutshell: Based on average Treasury bond rates and inflation since the World War II, current TIPS yields look reasonable if not spectacular. TIPS bonds themselves have only existed since the late 1990s, but regular (non-inflation-adjusted) Treasury bonds of course go back much further. Since 1945, someone owning regular 10 Year Treasurys has ended up earning, on average, about inflation plus 1.5% to 1.6% a year.

But Joachim Klement, a trustee of the CFA Institute Research Foundation and strategist at investment company Liberum, says the world is changing. Long-term interest rates are falling, he argues. This isn’t a recent thing: According to Bank of England research it’s been going on for eight centuries.

“Real yields of 1.5% today are very attractive,” he tells me. “We know that real yields are in a centuries’ long secular decline because markets become more efficient and real growth is declining due to demographics and other factors. That means that every year real yields drop a little bit more and the average over the next 10 or 30 years is likely to be lower than 1.5%. Looking ahead, TIPS are priced as a bargain right now and they provide secure income, 100% protected against inflation and backed by the full faith and credit of the United States government.”

Meanwhile the bond markets are simultaneously betting that Jerome Powell will win his fight against inflation, while refusing to believe him when he says he will do whatever it takes.

Make of that what you will. Not having to care too much about what the bond market says is yet another reason why I generally prefer inflation-protected Treasury bonds to the regular kind.

[ad_2]

[ad_1]

Right now is a tricky time to manage investments. Stocks, real estate, gold, and crypto are all in bear market territory with a huge chance that the recession will worsen this year.

Due – Due

If you’re looking to make a risky bet, you could consider shorting the market in various capacities.

However, if you’re looking to allocate capital as safely as possible, here are some options with (relatively) high returns.

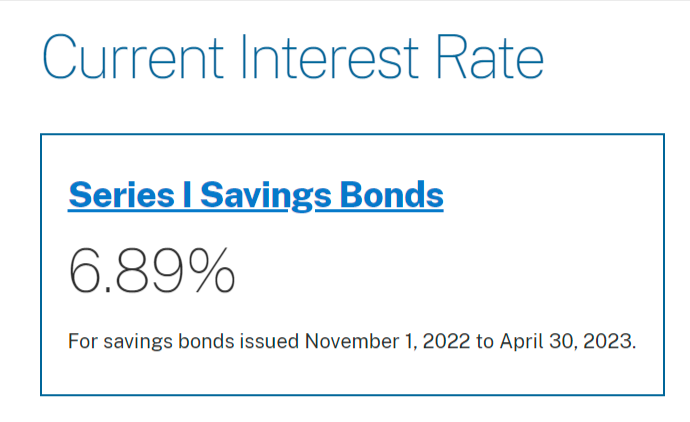

US government-backed bonds are about as safe as it gets. The Series I Savings Bonds accrued at a whopping 9.62% in 2022, and now are offering 6.89%.

Source: TreasuryDirect.com

Interest on the bonds is tax deductible on your federal income taxes. (Though the investment of principle isn’t.)

These interest rates are pegged to inflation, and they change every six months. So if inflation goes up or down, the rates will go up or down, too.

The downsides to this investment involve time and investment caps.

You have to keep the bond for at least one year to gain any interest. If you redeem the bond before holding it for five years, your last three months will not be paid interest as a penalty.

The investment cap is $10,000 per person per year. This is more flexible than it seems.

You’re allowed to invest $10,000 for every person in your household, including minors. So if you have a family of four, you can invest $40,000 per year.

Businesses can also invest up to $10,000. So if you have one or more businesses, that gives you additional investment opportunities as well.

The calendar year limitation is quite flexible too because you don’t have to wait 12 months before making your next investment.

If you already maxed out your I-Bond allocations even as recently as December 2022, you can make your next investment in January 2023.

The traditional inflation hedges, gold and silver, actually declined in price in 2022. So the I-Bond may be your best bet to stay ahead of high inflation.

Source: Photo by Scott Webb from Pexels

This may not be the sexiest investment of the year, but it’s guaranteed to pay off.

If the stock market and other investment markets have a down year, paying off your mortgage may be one of the best returns you can get.

Paying off your mortgage early can save you tens of thousands of dollars in interest. It also decreases your overall financial risk and eliminates what is most likely your biggest monthly bill.

Say you’ve been in your house for three years and have a balance of $300,000 on your home loan at a 3.5% interest rate. The loan term is 30 years.

If you pay an extra $1,000 per month, the loan will be paid off 12 years and 2 months earlier than it would have been.

More importantly, you’ll save $91,824 in interest. (Based on these Calculator.net calculations.)

If you analyze your return on investment, you’ll net 4% per year in annualized returns. (Based on this ROI calculator.)

That may not be record-breaking, but it’s a guaranteed return on an asset that you own 100% of and have insured. Anyone can do it.

Even high net-worth individuals often have huge mortgages, so this advice applies to people across the economic spectrum.

Don’t have a mortgage? The same advice applies to student loans and car loans.

Of course, credit cards are the best debt to pay off because of their high-interest rates. In my opinion, credit card debt should be the first investment priority of anyone who has it.

Fixed-income annuities are like setting up your own private pension plans. You can invest in them while you’re healthy and working, with the expectation that they provide money for you as long as you live.

The biggest financial risk that any of us face is that we’ll outlive both our working years and retirement savings.

Annuities fix this by guaranteeing income for retirement. This is one reason why many economists recommend annuities.

There are many different types of annuities, and like any investment, they can vary quite a bit. Some contain more risk than others.

Still, if you’re looking for an investment alternative to the huge movements in the stock market, annuities offer an opportunity to diversify your portfolio and shield you from market fluctuations.

As with all investment opportunities, you should make sure that you understand what you’re investing in and speak with your financial advisors before proceeding.

Annuities are particularly tricky in this regard because they are usually offered by life insurance salespeople who get huge commissions for selling them. But if an annuity strategy is smartly employed as part of a balanced portfolio, it can offer a consistent retirement income source that few other products can match.

This is an unusual one that is normally reserved for the wealthy.

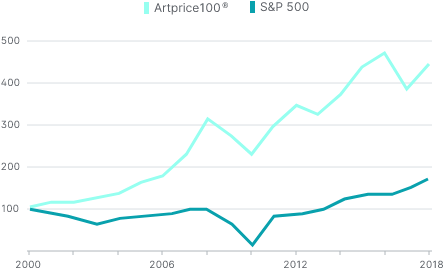

However, as alternative investment platforms like Masterworks and Yieldstreet will tell you, the entire asset class of art has outperformed the S&P 500 by a healthy margin since 2000.

The Artprice100® Index vs. the S&P 500. Source: Yieldstreet

It also has a low correlation to the price movements of stocks and bonds.

Normally the cost and expertise needed to buy a $5,000,000 painting make art inaccessible to the average investor.

However, alternative investment platforms, like those mentioned above, make it affordable for the average investor to buy a share of a valuable piece of art.

One of the main downsides to investing in art is the asset itself. Most asset classes are necessarily boring and unoffensive.

Conversely, many people consider contemporary art to seem silly at best. Or downright repulsive at worst.

Source: Artist JEAN MICHEL BASQUIAT via Masterworks.com

If you can hold your nose regarding the appearance of the asset itself and learn to understand how the art market works, it can be a valuable investment.

Also, keep in mind that this is not a liquid investment. You’ll want to hold onto your ownership shares until the underlying asset gets sold, which could take 1-10 years.

Like art, this one is off the beaten path for the average investor. And historically, it requires large capital investment and considerable expertise to get involved.

Also like art, farmland is now accessible to a wider group of investors through multiple investment platforms. A few platform examples include Acretrader, Farmfolio, FarmTogether, and many more.

Many of these platforms require that you be an accredited investor to invest, but some don’t.

Acretrader claims that farmland has an average 11% historical yield, without the volatility of stocks and real estate.

Source: Acretrader

I was particularly surprised to learn that farmland prices don’t mirror commercial real estate, but it makes sense. Farmland supply and demand differs greatly from commercial buildings and land, which are mostly urban.

It’s important to note that farmland investments do not involve the farm operations themselves.

Many farmers lease their land, and the buildings, livestock, and farming businesses themselves are not part of the investment.

The main downside to farmland is that it’s not liquid. You won’t get your money back until the land is sold years later.

If your investment horizon is at least 5-10 years, then it could be a good option for diversification and safety.

Venture-backed companies typically invest all of their profits back into the company for rapid growth. However, most small businesses don’t operate this way.

If you’re a business owner, now might be the perfect time to think more like a startup and plan your expansion. If your business is in good shape financially, spending on growth could be your smartest investment.

Real business expenses like advertising and inventory are tax deductible, so any new business cost that you take on will lighten your tax burden.

As mentioned earlier, many small business owners don’t allocate capital into their business at the same level they would their own 401(k). Why not?

A smart growth strategy can be your best weapon in protecting your business as the recession gets worse in 2023.

Of course, you don’t want to spend frivolously or on expenses that won’t promote growth.

But if your business has a good track record and you believe in your operation, it could be a solid investment path.

High inflation in 2022 turned off many investors from saving money in a bank account.

On the contrary, I would argue that bolstering your cash reserves may be the smartest move you can make right now.

For starters, interest rates are high. Saving account interest rates are higher than they’ve been in over a decade. Getting 3% interest on savings is entirely doable.

Second, it never hurts to have a lot of cash on hand during a recession. As they say, “cash is king.”

If you lose your job or any of your income sources get jeopardized over the next year, a healthy cash reserve will be your best friend.

Third, and most importantly, there is a very high probability that deflation will set in. There are loads of indicators that the economy will get worse and that markets will continue to tumble.

Why not build your cash reserves to buy back in at the bottom?

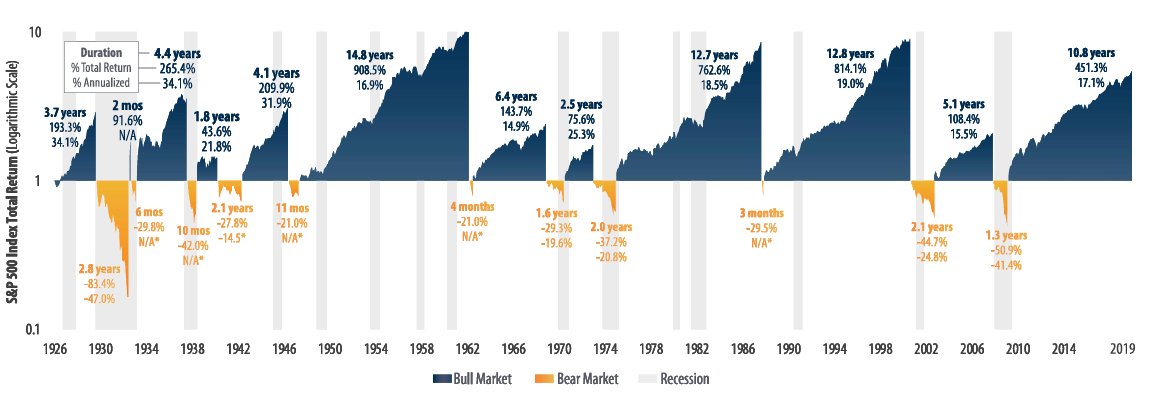

Over the past 100 years, the average stock bear market lasts 1.3 years and has a typical loss of 38%.

Source: First Trust via UIdaho.edu

In more recent years, bear markets have been even longer and lower:

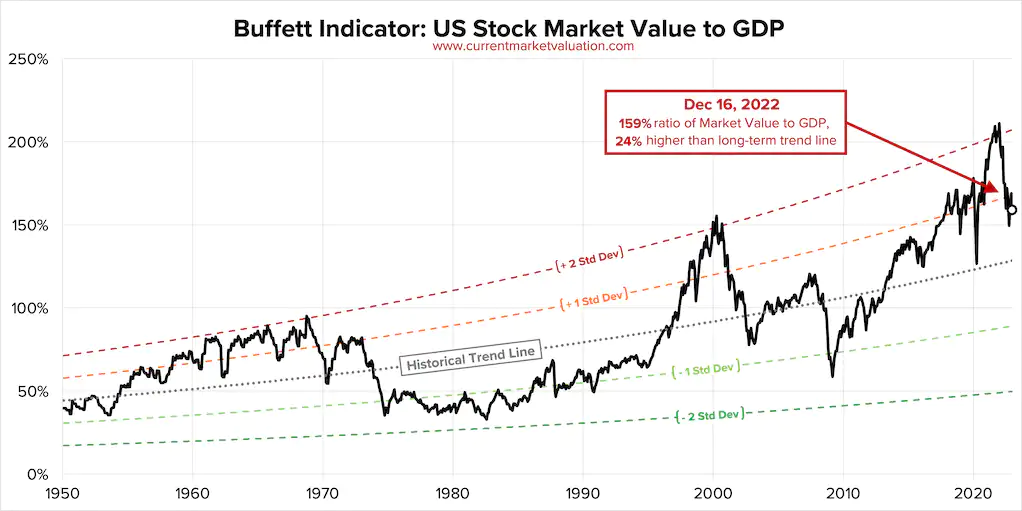

Warren Buffet famously cites the GDP to stock market valuation ratio to measure the state of the overall market. Some people call this the “Buffett Indicator.”

At the time this article was written, markets are “Significantly Overvalued.”

Source: CurrentMarketValuation.com

In 2022, the Federal Reserve demonstrated a high commitment to quashing inflation. They did this by raising interest rates.

If inflation remains the #1 enemy to US economic policymakers in 2023, then the markets will continue to tumble.

What better way to wait out the crash than with a healthy savings account?

None of us have a crystal ball. But the markets and the government policies that affect them typically follow patterns.

One of the most difficult parts of investing is controlling your emotions.

Keep your head. Follow a sound strategy. That’s how you’ll make 2023 a great year for your portfolio.

The post 7 Safe Investments with Relatively High Returns for 2023 appeared first on Due.

[ad_2]

Garit Boothe

Source link