Nvidia Might Have Some Bad News on Gaming. Buy the Stock Anyway?

-

Order Reprints

-

Print Article

Nvidia Might Have Some Bad News on Gaming. Buy the Stock Anyway?

Walt Disney Co. is about to face “perhaps its biggest decision yet” as it charts a future for ESPN, and the path forward initially may be a rocky one, according to an analyst.

Macquarie’s Tim Nollen downgraded Disney shares

DIS,

to neutral from outperform Friday, writing that Disney faces a tricky balance as it tries to set up ESPN for the new reality of media. The downgrade comes after The Wall Street Journal reported a day earlier that Disney was “actively preparing” for a future in which it would offer the flagship ESPN service as a stand-alone streaming service.

“Doing so is inevitable, and it’s hard to see how it will be smooth: steep losses assumed in the pay TV bundle will have to be offset by strong subscriber sign-ups at a presumed high price, and before Disney even gets there it has to negotiate terms with pay TV operators on content, and with the leagues on costs for streaming rights,” Nollen wrote.

Disney already offers the ESPN+ streaming service, but that doesn’t include access to the flagship programming that airs through the traditional cable channel.

Nollen expects that Disney ultimately succeeds with the transition of core ESPN to streaming, though it might require at least a year or two of pain in the interim.

He has concerns about other factors that could weigh on Disney shares as well. For one, the company is making progress in stemming operating losses for its streaming business, but he thinks that “prior guidance of DTC [direct-to-consumer] attaining profitability during FY’24 may now be off the table.”

See also: Disney scraps plans on roughly $1 billion investment at new corporate campus in Florida

Nollen flagged that Disney now looks more likely to buy out Comcast Corp.’s one-third stake in Hulu to take full ownership of the service. That development, which is expected to take place early next year, “along with a slower pace of sub adds (Disney+ may actually lose subs for the 3rd straight quarter in [the fiscal third quarter]) may factor in to extended DTC operating losses beyond [fiscal 2024],” Nollen wrote.

He further noted that growth for Disney’s parks business “is set to slow from here, removing a recent support.”

Disney shares are off more than 2% in afternoon trading Friday.

Also on MarketWatch: Disney’s Star Wars: Galactic Starcruiser experience is closing — here’s what to know if you booked a trip

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

https://www.barrons.com/articles/tesla-stock-price-annual-meeting-elon-musk-772aea70

It was always going to be difficult.

Ramping up production of a new product, using relatively new technology, is a tall order in the best of times. Electric-vehicle startups Rivian Automotive Inc. RIVN, Fisker Inc FSR and Lucid Group Inc. LCID are finding out that it is extra hard in the middle of economic uncertainty, lingering supply-chain worries, rising interest rates and less patient investors.

Earlier…

Icahn Enterprises LP’s stock was trading down 0.7% Thursday, after short seller Hindenburg Research intensified his bearish bet on Carl Icahn’s investing arm, and said he’s now taking aim at its bonds.

Hindenburg, run by Nate Anderson, said the latest disclosures made Wednesday by IEP raised more questions about Icahn’s personal margin loans, or debt, from the company as well as portfolio losses at IEP. The short seller also said disclosures, intended to counter Hindenburg’s May 2 report, failed to address the issues raised.

The original report raised questions about asset valuations and Icahn’s own borrowing from the company using his units as collateral.

Hindenburg Research, which typically aims to profit from the decline in value of the shares of companies that it writes negative reports about, kicked off such a bet against Icahn Enterprise earlier this month but has now also set its sights on the company’s debt.

For more, see: Icahn calls Hindenburg short-seller report self-serving, as market value of his company’s stock plunges by $4 billion

“As noted in our earlier report, Icahn had not disclosed “basic metrics around his margin loans like loan to value (LTV), maintenance thresholds, principal amount, or interest rates.” This is still the case,” said Hindenburg.

IEP has not said why Icahn had borrowed against his holdings. The company didn’t respond to a request for comment on Thursday’s report.

On Wednesday, IEP disclosed a federal probe into its corporate governance and other issues. It is unclear if that investigation by the Southern District of New York is related to Hindenburg’s report and allegations, but the news put further pressure on the stock.

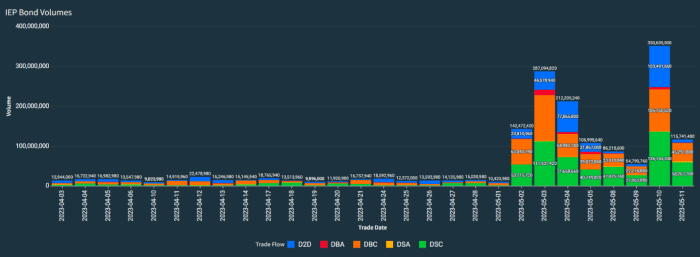

The bonds, which have been more active than usual since the first report, took another leg down on Thursday, as the attached charts from market-data company BondCliQ show, as Hindenburg said it has taken a short position in them.

The longest-dated bonds, the 4.375% notes that mature in February of 2029, were trading at around 75 cents on the dollar, as of midmorning.

Icahn owns 84% of IEP shares and disclosed in a 2022 filing with the Securities and Exchange Commission that he had pledged more than 181 million units, or 60% of his holdings, for margin loans.

On Wednesday, IEP

IEP,

said that pledge had increased to 202 million units, which Hindenburg estimates was valued at $6.5 billion as of Wednesday’s close, based on his calculations.

The battle between the iconic activist investor and the short seller has clobbered IEP’s stock, which has fallen 39% in the month to date at a cost of more than $6 billion of market cap.

Also read: What we know about Carl Icahn’s margin loan

IEP posted an unexpected loss on Wednesday of $270 million, or 75 cents per depositary unit, for the first quarter, after income of $323 million, or $1.06 a unit, in the year-earlier period. The FactSet consensus was for income of 19 cents.

Revenue fell to $2.758 billion from $2.968 billion a year ago, ahead of the $2.559 billion FactSet consensus. Analysts on its conference call didn’t pose any question of executives who briefly outlined the quarterly numbers.

The company on Wednesday also issued a rebuttal of the May 2 report from Hindenburg and said it would “take all appropriate steps to protect our unit holders and fight back.”

Icahn acknowledged that the investment segment has underperformed in recent years, which he blamed on its bearish view of the market and large net short position, which it has now scaled back.

IEP offers exposure to Icahn’s personal portfolio of public and private companies, including petroleum refineries, car-parts makers, food-packaging companies and real estate. Its unit holders are mostly individual investors, which means the market-cap loss prompted by the report has hurt those individual investors, said Icahn.

Lyft Inc. on Thursday reported first-quarter results that beat expectations, but a forecast that fell just shy of analysts’ estimates weighed on the company’s stock.

Lyft shares LYFT fell 15% after hours. They had dropped 1.8% in the regular session to close at $10.69 after a six-day positive streak.

Lyft forecast second-quarter revenue of…

Qualcomm Inc. shares fell in the extended session Wednesday after the chip maker said inventory issues will remain past June because of a downturn in handset demand and the company’s outlook disappointed.

After declining 2.8% to close the regular session $112.83, Qualcomm

QCOM,

shares started sliding after the release of the company’s results at Wednesday’s close, and sank to a deficit of more than 7% after hours by the time the executives’ call with analysts ended. Shares ended the extended trading session down 6.6%.

On the conference call, Qualcomm Chief Executive Cristiano Amon told analysts that the “evolving macroeconomic backdrop has resulted in further demand deterioration, particularly in handsets, at a magnitude greater than we previously forecasted.”

Earlier, Qualcomm had forecast adjusted earnings of $1.70 to $1.90 a share on revenue of $8.1 billion to $8.9 billion for the fiscal third quarter. Analysts had estimated earnings of $2.17 a share on revenue of $9.13 billion for the third quarter.

FactSet

Last quarter, Qualcomm said inventory issues would persist into June, and Wall Street pretty much accepted it. Qualcomm’s inventory problems go back to last year, when the company’s share price fell in November to lows not seen in more than two years after executives said there was up to 10 weeks of inventory in the channel, and forecast a $2 billion shortfall coming off record sales.

A drop in handset demand, however, has extended the time frame of inventory drawdowns considerably past the previously forecast end of June, the company said. As its largest business segment, Qualcomm handset sales fell 17% to $6.11 billion from a year ago.

“As a result, we’re operating under the assumption that inventory drawdown dynamics remain a significant factor for at least the next couple quarters,” Amon told analysts. “Additionally, while expectations are for a rebound in China demand in the second half of the calendar year, we have not seen evidence of meaningful recovery and are not incorporating improvements into our planning assumptions.”

The company reported fiscal second-quarter net income of $1.7 billion, or $1.52 a share, compared with $2.93 billion, or $2.57 a share, in the year-ago period. The chip maker reported adjusted earnings, which exclude stock-based compensation expenses and other items, of $2.15 a share, compared with $3.21 a share in the year-ago period. Total revenue for the quarter fell to $9.28 billion from $11.16 billion in the year-ago period.

Analysts surveyed by FactSet had forecast $2.15 a share on revenue of $9.09 billion, based on Qualcomm’s forecast of $2.05 to $2.25 a share on revenue of $8.7 billion to $9.5 billion.

In Qualcomm’s other end-market segments, auto sales rose 20% to $447 million and Internet-of-Things sales fell 24% to $1.39 billion for the second quarter, the company said.

Late Monday, auto chip supplier NXP Semiconductor NV

NXPI,

topped Wall Street expectations, and shares rallied Tuesday, while last week, another big supplier to the auto market, Texas Instruments Inc.

TXN,

said that sales to the auto industry remained strong.

Qualcomm shares already lag the broader chip sector and market, and were up only 3% year to date at Wednesday’s close. In comparison, the PHLX Semiconductor Index

SOX,

has surged 17%, the S&P 500 index

SPX,

has gained 7%, and the tech-heavy Nasdaq Composite Index

COMP,

has grown 15%.

In other chip earnings, Advanced Micro Devices Inc.

AMD,

shares dropped 9.2% Wednesday after the chip maker’s optimism for the second half of the year late Tuesday did not rub off on analysts.

And last week, Intel Corp.

INTC,

reported its largest quarterly loss ever, but saw its shares rise because PC and data-center sales, while on the decline, had come in better than expected. Intel also lowered expectations on its forecast.

Meta Platforms Inc.’s stock soared more than 10% higher in extended trading Wednesday after the social networking company’s profit declined less than expected in the first three months of 2023, and a revenue forecast pointed toward reinvigorated sales growth.

Facebook’s parent company META racked up fiscal first-quarter net earnings of $5.71 billion, or $2.20 a share, compared with earnings of $2.72 a share in the year-ago quarter. Revenue gained less than 3% to $28.65 billion from $27.91 billion a year ago.

Analysts…

Roku Inc. shares moved 2% higher in Wednesday’s after-hours action as the streaming-media company cited continued ad-market pressures but topped expectations for its latest quarter.

The company reported a first-quarter net loss of $193.6 million, or $1.38 a share, compared with a loss of $26.3 million, or 19 cents a share, in the year-earlier quarter. Analysts tracked by FactSet were expecting a $1.47 loss per share.

Roku…

Netflix Inc.’s stock initially plunged in after-hours trading Tuesday, after the streaming giant posted weaker subscriber growth and forecast a smaller profit than Wall Street expected. But shares later recovered and crossed into positive territory on company disclosures that its new ad-supported service is a success and its crackdown on shared accounts in the U.S. is coming this quarter.

Netflix

NFLX,

reported that subscribers increased by 1.75 million in the first quarter of the year, missing analysts’ average estimate of 2.2 million. Netflix reported fiscal first-quarter net earnings of $1.31 billion, or $2.88 a share, compared with $3.53 a share in the year-ago quarter.

Revenue improved to $8.16 billion from $7.87 billion a year ago. Analysts surveyed by FactSet had expected on average net earnings of $2.86 a share on revenue of $8.18 billion.

For the second quarter, Netflix executives guided for earnings of $2.84 a share on $8.24 billion in revenue, while analysts on average were expecting earnings of $3.07 a share on sales of $8.18 billion. Netflix no longer provides guidance on subscriber additions, a sign its years of rapid growth are clearly cooling.

Shares plunged lower than $300 in after-hours trading immediately following the release of the results, after closing with a 0.3% increase at $333.70. But shares had crossed into positive territory and were recently above $335 in the extended session.

Netflix executives have hoped to goose their financial results with cheaper, ad-supported options and a crackdown on password sharing. In a letter to shareholders Tuesday, company executives said the ads plan in the U.S. “already has a total ARM (subscription + ads) greater than our standard plan.”

At the same time, they disclosed a password crackdown in the U.S. will occur in the second quarter, a bit later from previous expectations.

“We shifted out the timing of the broad launch from late Q1 to Q2,” Netflix executives wrote. “While this means that some of the expected membership growth and revenue benefit will fall in Q3 rather than Q2, we believe this will result in a

better outcome for both our members and our business.”

Additionally, Netflix also announced that it will end the DVD-by-mail business that launched the company into consumers’ homes. Revenue from the DVD business had declined from $911 million in 2013 to $146 million in 2022.

“This a catch-22 environment for streaming companies as they are pivoting from chasing subscribers to chasing profits while at the same time inflation-weary consumers are reassessing their discretionary spending habits,” KPMG U.S. National Media Leader Scott Purdy said, in assessing the results. “Today’s figures, a bellwether for the industry at large, signal that winter is coming for the consumer. All of the subsidies are ending. Consumers can expect to be hit with ads, higher prices, and password sharing crackdown.”

Expectations among investors heading into Netflix’s quarterly report were muted. The focus was on Netflix’s switch toward better monetization with an ad-supported service and a rolling crackdown on shared accounts. Analysts in particular were closely watching the performance of Netflix’s new “Basic with Ads” plan ($6.99 a month) and its effectiveness in stanching the defection of subscribers to competing services from Walt Disney Co.

DIS,

and Apple Inc.

AAPL,

Netflix’s rollout of the ad-supported tier could also have a temporary impact on margins: Netflix reported an operating margin of 21%, compared with about 25% in the year-ago quarter.

At the same time, Netflix put an end to paid shared accounts in some Latin American countries last year, and expanded plans to do so Canada, New Zealand, Portugal and Spain in February.

“In our view, the password-sharing crackdown will result in a greater number of subs as well as revenue because the primary account holder will either pay an additional fee for members who have moved out of the household or those sharing accounts become full subscribers,” Bank of America analysts said in a recent note.

Shares of Netflix have climbed 12% so far this year, while the broader S&P 500 index

SPX,

has advanced 8%.

Shares of American Airlines Group Inc. were rocked Wednesday, after the air carrier raised its profit outlook, but not by enough to match Wall Street expectations.

The company said before the open that it expects first-quarter adjusted earnings per share of 1 cent to 5 cents, compared with a per-share loss of $2.32 a year ago. While that’s better than previous guidance for an “approximately breakeven” quarter, the average EPS estimate of analysts surveyed by FactSet was 5 cents.

The…

Lyft Inc. is bringing in a new chief executive and removing its co-founders from running the ride-hailing company on a day-to-day basis, sending shares more than 3% higher in after-hours trading Monday.

Lyft

LYFT,

announced after markets closed Monday that board member David Risher will take over as CEO, replacing co-founder Logan Green. Green and Lyft’s other active co-founder — John Zimmer, who had been serving as president — will remain on the company’s board as chair and vice chair respectively, but not actively participate in running the company.

“I’m honored and humbled that Logan, John, and the board have trusted me to lead Lyft,” Risher said in a letter to employees. “And I’ll start by saying this: I want Lyft to lead, and I’m thrilled to lead Lyft.”

Risher worked at Microsoft Corp.

MSFT,

in the 1990s before becoming employee No. 37 at Amazon.com Inc.

AMZN,

according to Lyft’s announcement, which noted that he received a permanent thank you on the Amazon website from founder and former chief executive Jeff Bezos upon his departure in 2002. For the past 13 years, he has been in charge of a nonprofit focused on childhood literacy called Worldreader.

“Across all three organizations, I learned of the power of leading with purpose,” he wrote to employees. “Each organization derived tremendous energy through a singleness of purpose. It’s what attracted and retained great people, allowed us to make focused decisions and inspired our customers.”

In an interview with The Wall Street Journal, Risher — who has been on Lyft’s board since 2021 — admitted that Lyft faces competitive issues, seemingly referencing Uber Technologies Inc.

UBER,

He mentioned “a very aggressive — very aggressive — competitor,” while adding, “I think being a strong No. 2 is a good place to be.”

Lyft shares lost more than a third of their value in a single session in February after Green and Zimmer provided a forecast that missed expectations in what one analyst called “a debacle for the ages.” Monday’s announcement reiterated Lyft’s first-quarter guidance and said Lyft expects to report quarterly results in early May.

D.A. Davidson analyst Tom White told MarketWatch on Monday afternoon that the change at the top could be “a potential model positive.”

“A new leader with broader range of experiences could signal increased willingness to broaden Lyft’s strategic aperture a bit as it relates to other possible adjacent products (delivery?), partners, or ways to create value,” he wrote in an email.

Green and Zimmer began developing the company nearly 15 years ago, and launched the service in 2012, according to their separate letters to employees. They have jointly led the company since, including through a 2019 initial public offering that gave them special shares with stronger voting power.

From 2019: 5 things to know about the Lyft IPO

“To say I have loved leading Lyft is an understatement,” Green wrote in his letter to employees. “To say that I will miss working alongside you and this incredible team every day doesn’t even come close. This was an adventure of a lifetime, and I’ve loved every minute of it — the sweetness of the highs, and the pain of the lows that make you appreciate the next win that much more. I’m eternally grateful to this team.”

Lyft shares sold for $72 in its IPO, and closed Monday at $9.60 before moving closer to $10 in the extended session. Lyft stock has plummeted nearly 75% in the past 12 months, dropping 74.4% as the S&P 500 index

SPX,

has declined 12.6%.

Oracle Corp. shares recouped some of their losses in the extended session Thursday after the forecast revenue range bookended the Wall Street consensus, as the software company’s largest business unit topped forecasts, but its others didn’t.

Oracle

ORCL,

shares were down about 3.5% after hours following the forecast. Prior to the forecast, shares had dropped more than 5% and were around those levels when a conference call with analysts began. Oracle shares declined 1.8% in the regular session to close at $86.87.

On the call with analysts, Oracle Chief Executive Safra Catz forecast fourth-quarter earnings of $1.56 to $1.60 a share on revenue growth of 15% to 17%, or $13.62 billion to $13.85 billion. Analysts surveyed by FactSet had estimated $1.47 a share on revenue of $13.75 billion.

That followed fiscal third-quarter results in which Oracle reported net income of $1.9 billion, or 68 cents a share, compared with $2.32 billion, or 84 cents a share, a year ago.

Adjusted earnings, which exclude stock-based compensation expenses and other items, were $1.22 a share, compared with $1.13 a share in the year-ago period.

Revenue rose to $12.4 billion from $10.51 billion in the year-ago quarter.

Analysts had estimated earnings of $1.20 a share and revenue of $12.43 billion for the third quarter.

Oracle’s largest segment, cloud services and license support, rose 17% to $8.92 billion. Cloud license and on-premise license revenue was flat at $1.29 billion from a year ago, while hardware revenue rose 2% to $811 million, and services revenue jumped 74% to $1.38 billion.

Analysts had forecast cloud services and license support revenue of $8.83 billion, cloud license and on-premise license revenue of $1.39 billion, hardware revenue of $815.5 million and services revenue of $1.43 billion.

“Since June of last year when we acquired Cerner, that business has increased its healthcare contract base by approximately $5 billion,” said Larry Ellison, Oracle’s chairman, in a statement. “While we are pleased with this early success of the Cerner business, we expect the signing of new healthcare contracts to accelerate over the next few quarters.”

Oracle’s board also hiked the quarterly dividend 25% to 40 cents a share. The dividend will be paid April 24 to shareholders of record as of April 11.

Oracle shares are up 14% over the past 12 months, versus a 14% decline by the iShares Expanded Tech-Software Sector ETF

IGV,

while the S&P 500 index

SPX,

has dropped 8% and the tech-heavy Nasdaq Composite Index

COMP,

has fallen 14% in that time.

Rising Treasury yields appeared Tuesday to finally catch up with a previously resilient stock market, putting major indexes on track for their worst day so far of 2023.

“Yields are popping across the curve, with the 2-year back to its November highs. This time it seems, market rates are playing catch up with fed funds,” said veteran technical analyst Mark Arbeter, president of Arbeter Investments, in a note.

Since the beginning of the month, traders in fed-funds futures have priced in a more aggressive Federal Reserve after initially doubting the central bank would hit its forecast for a peak fed-funds rate above 5%. A few traders are even pricing in the outside possibility of a peak rate near 6%.

Arbeter noted that markets generally lead fed-funds higher, not the other way around. Meanwhile, the U.S. dollar has also rallied, with the ICE U.S. Dollar Index adding 0.2% to a February bounce.

Arbeter also noted that breadth indicators, a measure of how many stocks are participating in a rally, had previously deteriorated, with some measures reaching oversold levels.

“Just another perfect storm against the equity markets in the short term,” he wrote.

Rising yields can be a negative for stocks, increasing borrowing costs. More important, higher Treasury yields mean that the present value of future profits and cash flow are discounted more heavily. That can weigh heavily on tech and other so-called growth stocks whose valuations are based on earnings far into the future. Those stocks were pummeled heavily last year but have led gains in an early 2023 rally, remaining resilient through last week even as yields extended a bounce.

Yields have been on the rise after a run of hotter-than-expected economic data, which have boosted expectations for Fed rate hikes. Weak guidance Tuesday from Home Depot Inc.

HD,

and Walmart Inc.

WMT,

also contributed to the tone.

Home Depot sank 6.5%, and was the biggest lower on the Dow Jones Industrial Average

DJIA,

after the home-improvement retailer reported a surprise decline in fiscal fourth-quarter same-store sales, guided for a surprise drop in fiscal 2023 profit and earmarked an additional $1 billion to pay its associates more.

“While Wall Street expects resilient consumers following last week’s robust retail sales report, Home Depot and Walmart are much more cautious,” said Jose Torres, senior economist at Interactive Brokers, in a note.

“This morning’s data offers more mixed signals concerning consumer demand, but during a traditionally weak seasonal trading period, investors are shifting toward a glass half-empty view against the backdrop of a year that’s featured the exact opposite so far, a glass half-full perspective,” he wrote.

The Dow remained down nearly 650 points, or 1.9%, while the S&P 500

SPX,

slumped 1.9% to trade at 4,001 after earlier dipping below the 4,000 level for the first time since Jan. 25. The S&P 500 was on track for its biggest daily drop since December. The Nasdaq Composite

COMP,

was down 2.4%.

The losses left the Dow clinging to a 0.1% year-to-date gain, while the S&P 500 remains up more than 4% and the Nasdaq Composite has rallied over almost 10% so far this year.

Arbeter identified a “very interesting cluster” of support just below the Tuesday low for the S&P 500, with the convergence of a pair of trend lines along with the index’s 50- and 200-day moving averages all near 3,970 (see chart below).

“If that zone does not represent the pullback lows, we have more trouble ahead,” he wrote.

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

https://www.barrons.com/articles/stock-market-movers-5b0c54ae

Nvidia

should be insulated from any slowdown in the broader economy by increased spending on artificial intelligence, say analysts at Oppenheimer, who lifted their price target for the semiconductor company.

The heightened interest around artificial-intelligence should set investors’ minds at ease ahead of

Nvidia

‘s earnings next week, say the analysts, with the semiconductor maker’s commentary on data-center spending in focus.

Alphabet Inc.’s stock slipped nearly 5% in extended trading Thursday after the tech giant missed slightly on revenue and earnings in ho-hum quarterly results.

Google’s parent company reported fiscal fourth-quarter total revenue of $76.05 billion, up from $75.3 billion a year ago. Earnings were $13.62 billion, or $1.05 per share, compared with $20.64 billion, or $1.53 per share, last year. Alphabet’s revenue, minus traffic-acquisition costs (TAC), was $63.12 billion, vs. $61.9 billion a year ago.

“We’re on an important journey to re-engineer our cost structure in a durable way and to build financially sustainable, vibrant, growing businesses across Alphabet,” Chief Executive Sundar Pichai said in a statement announcing the results. The company recently announced 12,000 layoffs and has scaled back hires.

In a conference call later with analysts, Google Chief Business Officer Philipp Schindler said a “pullback” in spending by advertisers amid a more challenging economy as well as foreign-exchange headwinds impacted sales.

Analysts polled by FactSet expected Alphabet

GOOG,

GOOGL,

to report total revenue of $76.2 billion and earnings of $1.18 per share, with sales expected to be in line with last year’s results and profit declining from the holiday season a year ago. Revenue, minus TAC, were modeled at $63.2 billion, which also suggests little to no growth from last year.

Google’s total advertising sales slid to $59 billion from $61.2 billion a year ago, missing analysts’ average expectations of $60.44 billion. Google Cloud brought in $7.32 billion, compared with $5.54 billion last year. YouTube ad sales slipped to $7.96 billion from $8.63 billion a year ago.

“The search giant underperformed our expectations across almost all business units, most importantly its core ad-search segment,” Jesse Cohen, senior analyst at Investing.com, said. “Once again, YouTube growth slowed to a crawl amid tough competition from TikTok and other players in the video-streaming space.”

A dip in digital advertising has defined the past few quarters for Google, Meta Platforms Inc.

META,

Snap Inc.

SNAP,

Pinterest Inc.

PINS,

and other companies dependent on ads. Meta’s better-than-expected quarterly report Wednesday was a sign of encouragement after Snap had another desultory quarterly performance.

Indeed, Alphabet shares closed up 7% in Thursday’s regular session, at $107.74, before retreating 5% in after-hours trading.

Read more: Alphabet earnings: What to expect from the Google parent company

“After Alphabet’s advertising revenue cycle reached peak growth” in the second quarter of 2021, revenue for this part of the business is set to decelerate for the sixth quarter in a row, said Monness, Crespi, Hardt analyst Brian White, who forecast a 3% drop in the recently completed quarter.

On Thursday, Alphabet Chief Financial Officer Ruth Porat said that beginning in

the current quarter, AI subsidiary DeepMind will be included in Alphabet’s corporate costs rather than in Other Bets.

Alphabet’s stock has declined 24.7% over the past 12 months. The S&P 500 index

SPX,

is down 6.7% over the past year.

Amazon.com Inc. reported its least profitable holiday quarter since 2014 on Thursday, leading to the biggest annual loss on record for the e-commerce giant, which also disappointed Wall Street with its forecast amid concerns about cloud growth.

Amazon

AMZN,

reported a holiday profit of $278 million, or 3 cents a share, down from $1.39 a share a year ago. Revenue increased to $149.2 billion from $137.41 billion a year ago. Analysts on average were expecting earnings of 17 cents a share on sales of $145.71 billion, according to FactSet.

Shares fell 5% in after-hours trading following the release of the results, after closing with a 7.4% increase at $112.91.

“In the short term, we face an uncertain economy, but we remain quite optimistic about the long-term opportunities for Amazon,” Chief Executive Andy Jassy said in a statement.

Amazon was expected to post a loss for the whole year for the first time since 2014, but worse-than-expected holiday earnings actually led Amazon to the company’s worst annual loss on record. For the year, Amazon produced a net loss of $2.7 billion and revenue of $513.98 billion, up from $469.82 billion a year ago and the company’s first annual sales total to surpass a half-billion dollars. Amazon had never lost more than $1.4 billion in a single year since going public in 1997, according to FactSet records.

Amazon’s fourth-quarter profit was hindered again by the decline of Rivian Automotive Inc.

RIVN,

stock, which cost Amazon $2.3 billion in net income in the quarter. In addition, Amazon recognized many of the costs of its recently announced layoffs and other cost cuts in fourth-quarter results as well — a $2.7 billion impairment charge included $640 million in severance charges related to layoffs and $720 million related to closures and impairment of physical stores, Chief Financial Officer Brian Olsavsky said in a call with reporters.

Without those charges, Amazon would have exceeded expectations, and recognizing them in 2022 leaves a cleaner sheet for this year, when Amazon’s ability to return to strong profitability will be the focus of Wall Street. The end result will likely rest on Amazon Web Services, or AWS, the cloud-computing offering that has supplied the bulk of Amazon’s profit in recent years, including 2022. Last year, AWS had operating profit of $22.84 billion, while the rest of the business produced an operating loss of $10.59 billion.

But cloud-computing growth has slowed, as Microsoft Corp.

MSFT,

displayed in its results and forecast last week, and Olsavsky confirmed the slowdown Thursday after AWS results missed expectations and suggested revenue growth had slowed to mid-teens and could stay there.

“Starting back in the middle of the third quarter of 2022, we saw our year-over-year growth rates slow as enterprises of all sizes evaluated ways to optimize their cloud spending in response to the tough macroeconomic conditions,” he said in a conference call with analysts. “As expected, these optimization efforts continued into the fourth quarter.”

Olsavsky told reporters he expected “slower growth rates for the next few quarters” for AWS, and later disclosed to analysts that revenue growth was in the mid-teens in the first month of this year. He noted that AWS revenue growth rates had been hit by customers looking to cut their cloud spending, and “we expect these optimization efforts will continue to be a headwind to AWS growth in at least the next couple of quarters.”

Opinion: The cloud boom has hit its stormiest moment yet, and it is costing investors billions

Making his first appearance on an earnings call since being named CEO two years ago, Jassy — who led AWS before being promoted to replace Jeff Bezos as CEO — said “if it’s good for our customers to find a way to be more cost effective in an uncertain economy, our team is going to spend a lot of cycles doing that.”

“We’re the only ones that really break out our cloud numbers in a more specific way, so it’s always a little bit hard to answer your question about what we see,” Jassy said to an analyst asking about the larger cloud industry, while referencing rival Microsoft’s refusal to provide full financial information about Azure. “But to our best estimations, when we look at the absolute dollar growth year over year, we still have significantly more absolute dollar growth than anybody else we see in this space.”

In the fourth quarter, AWS produced operating income of $5.21 billion on revenue of $21.38 billion, with sales growing more than 20% and operating income declining slightly. Analysts on average were expecting profit of $5.73 billion on sales of $21.85 billion, according to FactSet.

Any slowdown in AWS would hit Amazon’s bottom line as well as its overall top line, and executives’ forecast for the first quarter shows less optimism than Wall Street expected. Amazon’s guidance calls for operating profit of break-even to $4 billion and revenue of $121 billion to $126 billion, while FactSet recorded an average analyst forecast of $4.04 billion in operating profit on sales of $125.09 billion.

Amazon’s e-commerce business has struggled for growth amid the worst inflation in decades, with Olsavsky saying in a call with reporters that Amazon “saw customers spend less on discretionary items… [while] continuing to spend on everyday essentials.” Amazon recently announced it would start charging for grocery delivery for Prime members, which could increase revenue from sales of fresh food.

For more: Amazon Fresh to start charging Prime customers up to $10 for grocery deliveries

Amazon’s domestic e-commerce business posted an operating loss of $240 million on sales of $93.36 billion, after a $206 million loss on sales of $82.36 billion in the holiday quarter of 2021. Olsavsky said cuts in the company’s physical stores and device businesses would improve operating margins in North America.

Amazon’s international efforts struggled more, with a sales decline and increasing losses, as Olsavsky said the U.K. and other parts of Europe showed slowdowns. Amazon reported an operating loss of $2.23 billion on revenue of $34.46 billion overseas, after a loss of $1.63 billion on sales of $37.27 billion a year ago.

One bright spot in Amazon’s report was a record quarter for its advertising business, which has grown fast in recent years in a challenge to Alphabet Inc.’s

GOOGL,

GOOG,

Google and other online ad giants. Ads brought in $11.56 billion in the holiday quarter, growing nearly 19% from $9.71 billion a year ago and beating the analysts’ consensus.

Amazon stock has fallen more than 25% over the past 12 months, but has experienced a rebound so far in 2023, gaining more than 33% year to date. The S&P 500 index

SPX,

has declined 10.2% in the past year while gaining 7.3% since the calendar flipped to 2023.

In the biggest week of the holiday-earnings season, Big Tech results will receive the spotlight amid thousands of layoffs that could only be the beginning.

After tech stocks were decimated in 2022, investors will be looking for signs of a turnaround in holiday reports and potential forecasts for the year ahead from three of 2022’s top five market-value losers: Amazon.com Inc.

AMZN,

Apple Inc.

AAPL,

and Meta Platforms Inc.

META,

The other two stocks on that list — Microsoft Corp.

MSFT,

and Tesla Inc.

TSLA,

— reported last week, and Microsoft’s results in the wake of a mass-layoffs announcement did not bode well for its Big Tech brethren.

See also: Microsoft could be the cloud sector’s ‘canary in the coal mine’

Those companies — along with Google parent Alphabet Inc.

GOOGL,

GOOG,

— will deliver results after finding themselves in unfamiliar territory: A backdrop of layoffs amid slowing demand for core products like digital ads, electronics and e-commerce, after a two-year pandemic surge and a two-decade-plus honeymoon with investors. Some analysts say the bottom hasn’t arrived, for either their finances or their workforces.

The one Big Tech company that hasn’t taken a sword to its payroll is Apple, which also increased its staff the least among the group during the COVID-19 pandemic. Apple shed $846 billion from its market cap last year, and now reports after its core product was part of the smartphone industry’s worst year since 2013 and worst holiday-season decline on record. The iPhone maker could also face questions from Wall Street about changing up its product sourcing, which has relied heavily on China, a nation whose COVID-19 restrictions have constrained production of some phones.

While the tech-industry layoffs have yet to hit Apple, some analysts say the company is unlikely to be spared, despite Chief Executive Tim Cook requesting and receiving a healthy cut to his compensation.

“Similar to other big technology companies, we expect Apple to adjust its head count to reflect an increasingly challenging global macroeconomic environment,” D.A. Davidson analyst Tom Forte said in a research note Tuesday.

Rivals that have already cut could face more if profit continues to fall along with revenue growth. Alphabet, for instance, is cutting 12,000 employees, but an activist investor has already said that is not enough considering how much the company grew during the pandemic, and the difficulties it now faces in the online-ad sector.

Opinion: Microsoft’s big move in AI does not mean it will challenge Google in search

Analysts have said Meta’s “darkest days” are still ahead, as it navigates a round of more than 11,000 layoffs, competition from TikTok and its early stumbles in the metaverse. While cutting, Chief Executive Mark Zuckerberg has promised to keep spending on metaverse development, even as the efforts slash the Facebook parent company’s previously healthy bottom line.

“In 2023, we expect Meta to remain engulfed in arduous battles inside the Octagon,” Monness Crespi Hardt analyst Brian White said in a research note on Thursday. “In the long run, we believe Meta will benefit from the secular digital ad trend and innovate in the metaverse; however, regulatory scrutiny persists, internal headwinds remain, and we believe the darkest days of this downturn are ahead of us.”

Full Facebook earnings preview: Meta’s ‘darkest days’ are ahead, but some analysts say ad sales are still on track

Online retailer Amazon

AMZN,

was the first Big Tech company to publicly declare cost-cutting was in order a year ago, and still coughed up $834 billion in market value in 2022. It kicked off 2023 with plans to lay off more than 18,000 workers as struggles continued throughout last year, when inflation siphoned away more consumer dollars toward essentials.

Amazon’s own AWS cloud-infrastructure unit has helped to drive sales in years past, as businesses built out their tech infrastructures. But remarks and the outlook from Microsoft executives — the third-biggest market-cap loser of 2022, and a big barometer for tech spending overall — weren’t exactly encouraging for cloud growth: Executives there last week warned of “moderating consumption growth” for its own cloud business.

For more: One company could determine whether U.S. corporate profits rise to a record in 2023

“Sentiment was already bearish on AWS, with investors looking for slowing revenue over the next three quarters, largely confirmed after Microsoft earnings and conversations with industry checks,” Oppenheimer analyst Jason Helfstein said in a note on Wednesday. “Positively, we believe e-commerce revenue has stabilized, and margins should improve from organic scale and announced head-count reductions.”

Layoffs are also starting to spread beyond Big Tech companies that grew fast during the pandemic in response to massive demand spikes. International Business Machines Corp.

IBM,

confirmed plans for 3,900 layoffs as it reported earnings, despite already reducing its workforce by at least 20% during the pandemic.

One sector to watch is semiconductors, where a chip shortage has turned into a glut: Chip-equipment maker Lam Research Corp.

LRCX,

announced layoffs in the past week as Silicon Valley semiconductor giant Intel Corp.

INTC,

displayed “astonishingly bad” results while laying off workers. When Intel rival Advanced Micro Devices Inc.

AMD,

reports this week, it could determine whether there is any silver lining in the semiconductor storm.

Earnings preview: AMD faces even more scrutiny after ‘astonishingly bad’ Intel outlook

Wedbush analyst Daniel Ives said in a Sunday note that a common theme of this week’s Big Tech earnings will be that “tech layoffs will accelerate with more pain ahead to curb expenses,” though he added that “Apple will likely cut some costs around the edges, but we do not expect mass layoffs from Cupertino this week.”

Big Tech earnings were a salve to other problems in the market for the past decade-plus, but with layoffs already under way and doubts about the path forward, don’t expect salvation from their results this week.

For the week ahead, 107 S&P 500

SPX,

companies, including six members of the Dow Jones Industrial Average

DJIA,

will report results, according to FactSet. While more Dow components reported last week, this will be the busiest week for S&P 500 holiday earnings of the season, FactSet senior earnings analyst John Butters confirmed to MarketWatch.

Appliance-maker Whirlpool Corp.

WHR,

reports on Monday, after it forecast fourth-quarter sales that were below expectations, following what it called a “one-off supply-chain disruption” and the pandemic home-renovation boom.

On Tuesday, package-deliverer United Parcel Service Inc.

UPS,

reports, amid questions about holiday-season demand. So does streaming service Spotify Technology,

SPOT,

following its own layoffs and suggestions of possible price hikes, as well as McDonald’s Corp.

MCD,

amid concerns that rising prices are keeping people from dining out. Exxon Mobil Corp.

XOM,

Caterpillar Inc.

CAT,

Snap Inc.

SNAP,

and Pfizer Inc.

PFE,

also report Tuesday.

Earnings outlook: McDonald’s earnings haven’t been hit by higher prices

On Wednesday, T-Mobile US Inc.

TMUS,

reports, in the wake of a data breach and wobbling cellphone demand. Coffee chain Starbucks Corp.

SBUX,

reports on Thursday, with analysts likely to be zeroed in on U.S. demand and China’s reopening, after executives said they were confident that higher prices, along with enthusiasm from younger customers and for customizable drinks, could help them navigate any potholes in the economy.

For the Big Tech companies, Thursday is also the big day: Apple, Amazon and Alphabet will report that afternoon, after Meta reports the prior day.

WWE upheaval: World Wrestling Entertainment Inc.

WWE,

reports earnings on Thursday, as Vince McMahon — who returned to the professional-wrestling organization this month following allegations of sexual misconduct — seeks a buyer or some other so-called “strategic alternative” for the company.

Analysts have speculated how the company’s wrestling events and backlog of media content might be repurposed, with some entertaining the possibility of interest from Amazon or Netflix Inc.

NFLX,

But WWE has struggled to develop story lines that stick with viewers, and has thinned its ranks of wrestlers.

The Wall Street Journal this month reported that McMahon would pay a multimillion-dollar settlement to a former referee who accused him of raping her. Among the changes since McMahon returned was the departure of his daughter, who had been promoted to co-CEO after he stepped down from the role last year.

There isn’t much clarity on whether Vince McMahon will be on Thursday’s earnings call, which was moved from the morning to the afternoon due to a scheduling conflict. But it should offer drama no matter who attends.

GM and Ford auto sales: Auto makers General Motors Co.

GM,

and Ford Motor Co.

F,

will issue results on Tuesday and Thursday respectively, amid signs of waning demand and rising interest rates that have made car loans more expensive. Despite falling new-vehicle sales in the third quarter, GM managed to keep its own sales higher, the AP noted.

Mary Barry, GM’s chief executive, called out the popularity of vehicles like the Escalade, the Chevrolet Bolt EV and some pickups and SUVs during the auto maker’s third-quarter earnings call in October. During that quarter, GM said it completed and shipped nearly 75% of the unfinished vehicles held in its inventory in June. She said supply-chains were opening up again, but added that “short-term disruptions will continue to happen.”

The auto makers report as they try to put a chip shortage and other production constraints behind them. But some forecasts call for 2022 auto sales, or sales volumes, to be the weakest in roughly a decade. Electric vehicle maker Tesla’s recent price cuts could also cut into GM’s and Ford’s own EV sales.

The U.S. House of Representatives voted on Wednesday night to adjourn until 12:30 p.m. Eastern on Thursday, with the move coming as lawmakers have been unable to elect a new speaker for a second day in a row.

That vote came after House Republicans briefly reconvened at 8 p.m. Eastern following a flurry of meetings that attempted to find room for compromise.

Top House Republican Kevin McCarthy keeps hitting resistance in his push to become speaker, falling short of a majority in three rounds of voting on Wednesday afternoon and three earlier rounds of voting on Tuesday.

CNN and Axios reported Wednesday night that McCarthy offered significant concessions to the defecting Republicans but it was unclear if that would be enough to sway enough of their votes. “No deal yet,” McCarthy said after a closed-door meeting Wednesday night, according to the Associated Press, “But a lot of progress.”

The House must kick off the new congressional session with the election of a speaker, and it’s required to keep voting until one is chosen. There hasn’t been a need for multiple votes for a speaker’s election since 1923, when nine rounds of voting were required.

McCarthy can handle no more than four GOP defections given his party’s 222-212 majority, but more than that number have repeatedly opposed the California congressman.

In all three rounds of voting on Wednesday, 20 Republicans opposed him and voted instead for Rep. Byron Donalds of Florida, while Rep. Victoria Spartz of Indiana voted “present” after backing McCarthy on Tuesday.

In Tuesday’s third vote, the number of Republican lawmakers voting against McCarthy rose to 20, up from 19 in the first two rounds. Those 20 backed GOP Rep. Jim Jordan of Ohio on Tuesday, even as Jordan gave a speech in support of McCarthy and didn’t vote for himself.

Analysts have been warning that the tensions over what’s typically a ceremonial election could signal that the GOP-run House will be dysfunctional throughout 2023 —and that might affect markets eventually.

“If the House deadlock continues for weeks — or longer — the markets may have to worry about fiscal policy uncertainty,” said Greg Valliere, chief U.S. policy strategist at AGF Investments, in a note.

“If House Republicans can’t even elect a leader, how will they respond when a debt default crisis looms later this year?”

Former President Donald Trump offered support for McCarthy in a post on Wednesday morning on Truth Social, his social network.

“It’s now time for all of our GREAT Republican House Members to VOTE FOR KEVIN, CLOSE THE DEAL, TAKE THE VICTORY,” Trump wrote.

“DO NOT TURN A GREAT TRIUMPH INTO A GIANT & EMBARRASSING DEFEAT. IT’S TIME TO CELEBRATE, YOU DESERVE IT. Kevin McCarthy will do a good job, and maybe even a GREAT JOB — JUST WATCH!”

Betting market PredictIt on Wednesday evening was giving McCarthy around a 42% chance of becoming speaker, while No. 2 House Republican Steve Scalise’s chances were around 38%.

Related: How betting markets got the midterms wrong, and why Biden’s a ‘great bet’ for 2024

Republicans have taken control of the House thanks to wins in November’s midterm elections, returning to power in that chamber after four years in the minority.

But the GOP’s hopes for a strong red wave two years into President Joe Biden’s term were dashed, as the party has claimed just a small House majority and Democrats have maintained their grip on the Senate.

McCarthy has been drawing opposition from about 10% of his fellow House Republicans in large part because he’s viewed as not having done enough to oppose Democrats — as well as being part of the Washington establishment.

From MarketWatch’s archives (November 2022): McCarthy’s House speaker bid may be in trouble due to Republican objections: ‘He’s not a true conservative’

GOP Rep. Scott Perry of Pennsylvania, who heads the House Freedom Caucus, described voting against McCarthy as a vote against business as usual in Washington.

“Everybody came here because they said to their constituents, “This town is broken, and I want to fix it,’” Perry said, as he gave a speech Wednesday on the House floor.

“Well, how are you going to fix it, if you come to this town and just step right in line and keep doing the same things that everybody has done before?”

The Freedom Caucus, known for helping to bring about former Speaker John Boehner’s departure from his post in 2015, is made up of several dozen of the chamber’s most conservative Republicans.

U.S. stocks

SPX,

DJIA,

closed with gains on Wednesday. The main equity gauges finished lower on Tuesday in 2023’s first session, after the S&P 500 benchmark fell 19% in 2022, hit by the Federal Reserve’s interest-rate hikes as the central bank tries to rein in inflation.

Now read: Isolated and humiliated, Russia is biggest geopolitical threat of 2023, analysts say

Plus: Brace yourself: Your tax refund could shrink in 2023. Here’s why.