[ad_1]

As you’ve probably heard by now, Fitch Ratings late Tuesday cut the U.S. federal government’s credit rating to AA+ from AAA.

Here’s a look at what it means for investors and markets:

What’s a credit rating?

A credit rating is an independent assessment of the ability of an organization, including corporations and governments, ranging from school boards to cities, counties, states and countries, that have issued debt to meet their obligations. Fitch — alongside S&P Global and Moody’s Investors Service — is one of the world’s big three ratings firms.

Need to Know: The U.S. is downgraded. How much does it matter to markets? And the surprise asset that may benefit.

The ratings firms use scales that employ letters, and in Moody’s case also include numbers, to provide a guide to creditworthiness. At the top of the list is the AAA rating from S&P and Fitch, or Aaa, in the case of Moody’s. AA+ is the second-highest rating.

Ratings that employ Cs are at the bottom of the scales, with Fitch and S&P using D ratings in cases of default or bankruptcy.

Any rating below BBB- from Fitch and S&P, or Baa from Moody’s, is considered below “investment grade.” Such debt is often termed “junk.”

Why did the U.S. rating get cut

Fitch had warned in May that a cut was possible, with the ratings firm expressing dismay over what it termed another round of “brinkmanship” around the U.S. government’s debt ceiling. The warning came amid a battle between congressional Republicans and the Biden administration over lifting or suspending the federal government’s debt ceiling.

The limit has been a frequent source of political squabbling. While the showdown was resolved with a two-year suspension of the limit, the battle underlined the high stakes. Failure to reach a deal could have led to a default. In Tuesday’s decision, Fitch said that the past two decades have seen “a steady deterioration in standards of governance” in the U.S., the debt-ceiling agreement notwithstanding.

How does the U.S. rating stack up to other countries

Fitch isn’t the first of the big three ratings firms to strip the U.S. of its AAA rating. S&P did so in 2011, amid an earlier debt-limit battle. That leaves Moody’s as the only firm to still assign the U.S. its top rating.

The pool of triple-A sovereign ratings, meanwhile, continues to dwindle. Only a handful of countries carry triple-A ratings across the board from all three ratings firms.

See: Here are the countries that still have Triple-A credit ratings across the board

What does rating cut mean to investors?

The cut isn’t seen having much lasting effect on investor demand for U.S. Treasurys. The market for Treasurys is the largest and most liquid debt market in the world. Despite the lack of triple-A ratings, Treasurys are viewed and treated by investors as being virtually “risk-free,” or equivalent to cash. Other types of debt are often quoted in terms of the yield premium, or spread, demanded by investors to hold them over Treasurys.

That isn’t going to change overnight. Analysts have emphasized that investors don’t buy Treasurys based on the credit rating. And any outflows from funds that are required to hold only triple-A rated bonds are expected to be limited.

See: $25 trillion Treasury market is in the spotlight as U.S. loses its AAA rating for a second time

“Many major Treasury holders, such as funds and index trackers, have already prepared for the move by changing mandates to specifically refer to Treasurys rather than AAA credit, and are unlikely to be forced into selling given the importance of the asset class,” said Solita Marcelli, chief investment officer for the Americas at UBS Global Wealth Management, in a Wednesday note.

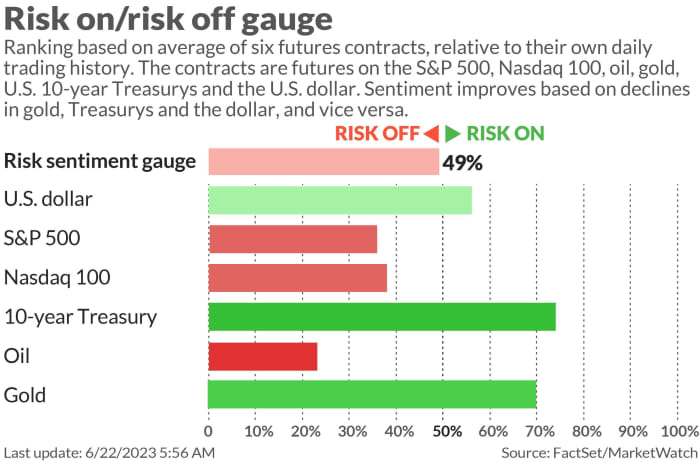

How are markets reacting?

The downgrade was blamed for a weak tone across global equity markets, with U.S. stocks following suit. The Dow Jones Industrial Average

DJIA

dropped around 315 points, or 0.9%, while the S&P 500

SPX

shed 1.3%. The moves come after a strong run of gains, however.

Treasury yields, which move opposite to price, were higher. The selling, however, took hold only after data from ADP that showed a stronger-than-expected rise in private-sector payrolls. Treasurys took the downgrade in stride in earlier trading, with yields moving lower.

The yield on the 10-year Treasury note

BX:TMUBMUSD10Y

was up around 2 basis points near 4.02%.

Marcelli recalled that in 2011 the yield on the 10-year U.S. Treasury fell around 50 basis points, or half a percentage point, in the three days after the S&P downgrade to 2.6% on Aug. 5. Even 15 trading days later, yields were still down 40 basis points from the day of the downgrade, and around 80 basis points lower compared with where they were 15 trading days before the move.

[ad_2]