The below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Analyzing On-Chain Bottom Indicators

In this week’s dashboard release, we highlighted some key on-chain metrics we like to track. In this article, we want to walk through more of those in detail. Across bitcoin’s short history, many on-chain cyclical indicators are currently pointing to what looks to be a classic bottom in bitcoin price. Market extremes — potential tops and bottoms — are where these indicators have proven to be the most useful.

On-chain indicators overlaid with previous bitcoin price bottoms.

However, these indicators need to be considered alongside many other macroeconomic factors and readers should consider the possibility that this could be another bear market rally — as we still sit below the 200-week moving average price of around $24,600. That being said, if price can sustain above $20,000 in the short-term, the bullish metrics paint a compelling sign for more long-term accumulation here.

A major tail risk is a possible market-wide selloff in risk assets that are currently pricing a “soft landing” style scenario along with the potentially incorrect expectations of a Federal Reserve policy pivot in the second half of this year. Many economic indicators and data still point to the likelihood that we’re in the midst of a bear market similar to 2000-2002 or 2007-2008 and the worst has yet to unfold. This secular bear market is what’s different about this bitcoin cycle compared to any other in the past and what makes it that much harder to use historical bitcoin cycles after 2012 as perfect analogues for today.

All that being said, from a bitcoin-native perspective, the story is clear: Capitulation has clearly unfolded, and HODLers held the line.

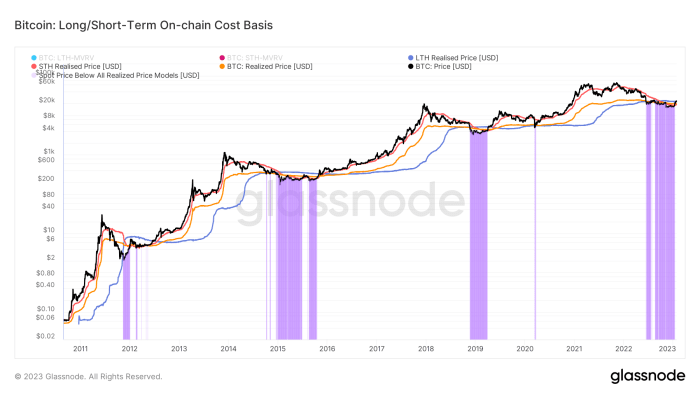

Given the transparent nature of bitcoin ownership, we can view various cohorts of bitcoin holders with extreme clarity. In this case, we are viewing the realized price for the average bitcoin holder as well as the same metric for both long-term holders (LTH) and short-term holders (STH).

The realized price, STH realized price and LTH realized price can give us an understanding of where various cohorts of the market are in profit or underwater.

A look at realized price for short- and long-term holders.

On a monthly basis, realized losses have flipped to realized profits for the first time since last April.

Capitulation and loss taking has flipped to profit realization across the network, which is a very healthy sign of thorough capitulation.

There is a strong case to be made that given the current elasticity of bitcoin’s supply — as evidenced by the historically small number of short-term holders or rather the large number of long-term holders — it will be challenging to shake out current market participants. Especially considering the gauntlet endured over the previous 12 months.

Statistically, long-term bitcoin holders are usually unfazed in the face of bitcoin price volatility. The data shows a healthy amount of accumulation throughout 2022, despite a massive risk-off event in both the bitcoin and legacy market.

While liquidity dynamics in legacy markets should be noted, the supply-side dynamics for bitcoin look to be as strong as ever. All it will take for a significant price appreciation will be a small influx of newfound demand.

Like this content? Subscribe now to receive PRO articles directly in your inbox.

The below is an excerpt from a recent year-ahead report written by the Bitcoin Magazine PRO analysts. Download the entire report here.

Bitcoin Magazine PRO sees incredibly strong fundamentals in the Bitcoin network and we are laser-focused on its market dynamic in the context of macroeconomic trends. Bitcoin aims to become the world reserve currency, an investment opportunity that cannot be understated.

In our year-ahead report, we analyzed seven notable factors that we recommend investors pay attention to in the coming months.

Convicted Bitcoin Investors

We can put investor conviction into perspective by looking at the number of unique Bitcoin addresses holding at least 0.01, 0.1 and 1 bitcoin. This data shows that bitcoin adoption continues to grow with a growing number of unique addresses holding at least these amounts of bitcoin. While it is entirely possible for individual users to hold their bitcoin in multiple addresses, the growth of unique Bitcoin addresses holding at least 0.01, 0.1 and 1 bitcoin indicate that more users than ever before are buying bitcoin and holding it in self-custody.

Unique bitcoin addresses continues to grow across the board.

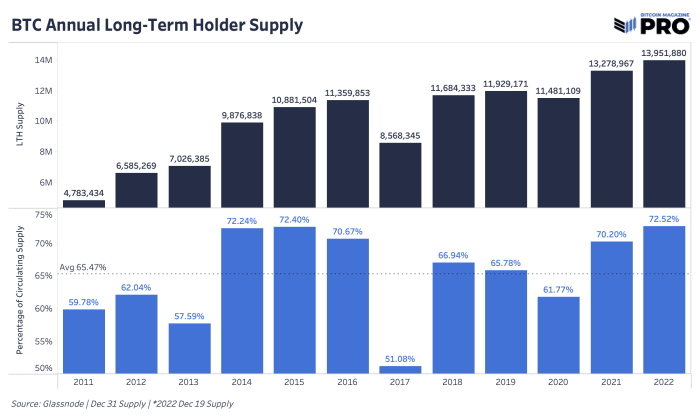

Another promising metric is the amount held by long-term holders, which has increased to almost 14 million bitcoin. Long-term holder supply is calculated using a threshold of a 155-day holding period, after which dormant coins become increasingly unlikely to be spent. As of now, 72.49% of the bitcoin in circulation is not likely to be sold at these prices.

Long-term holder supply reached 72.52% of the circulating bitcoin supply.

There is a large subset of bitcoin investors who are accumulating the digital asset no matter the price. In a December 2022 interview on “Going Digital,” Head of Market Research Dylan LeClair said, “You have people all over the world that are acquiring this asset and you have a huge and growing cohort of people that are price-agnostic accumulators.”

With a growing number of unique addresses holding bitcoin and such a significant amount of bitcoin being held by long-term investors, we are optimistic for bitcoin’s advancement and rate of adoption. There are many variables that demonstrate the potential for asymmetric returns as demand for bitcoin increases and adoption increases worldwide.

Total Addressable Market

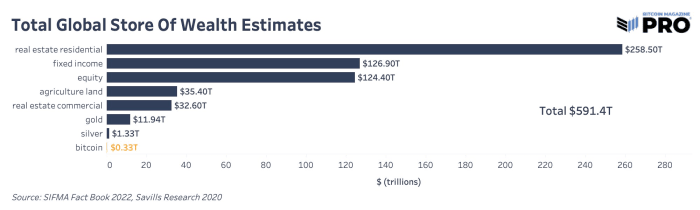

During monetization, a currency goes through three phases in order: store of value, medium of exchange and unit of account. Bitcoin is currently in its store-of-value phase as demonstrated by the long-term holder metrics above. Other assets that are frequently used as stores of value are real estate, gold and equities. Bitcoin is a better store of value for many reasons: it is more liquid, easier to access, transport and secure, easier to audit and more finitely scarce than any other asset with its hard-cap limit of 21 million coins. For bitcoin to acquire a larger share of other global stores of value, these properties need to remain intact and prove themselves in the eyes of investors.

Estimations of global stores of wealth.

As readers can see, bitcoin is a tiny fraction of global wealth. Should bitcoin take even a 1% share from these other stores of value, the market cap would be $5.9 trillion, putting bitcoin at over $300,000 per coin. These are conservative numbers from our viewpoint because we estimate that bitcoin adoption will happen gradually, and then suddenly.

Transfer Volume

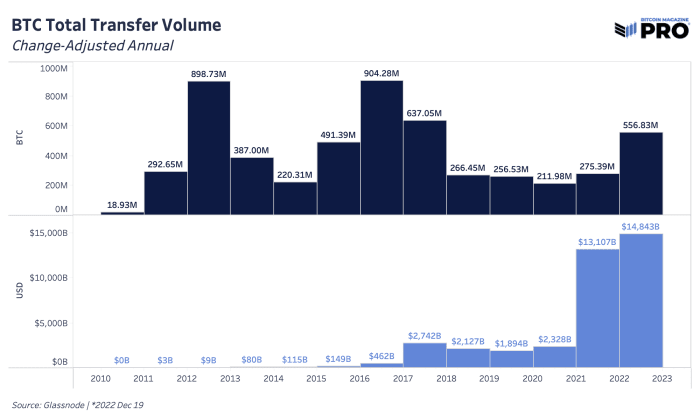

When looking at the amount of value that was cleared on the Bitcoin network throughout its history, there is a clear upward trend in USD terms with a heightened demand for transferring bitcoin this year. In 2022, there was a change-adjusted transfer volume of over 556 million bitcoin settled on the Bitcoin network, up 102% from 2021. In USD terms, the Bitcoin network settled just shy of $15 trillion in value in 2022.

Bitcoin transfer volume was higher than ever in USD terms.

Bitcoin’s censorship resistance is an extremely valuable feature as the world enters into a period of deglobalization. With a market capitalization of only $324 billion, we believe bitcoin is severely undervalued. Despite the drop in price, the Bitcoin network transferred more value in USD terms than ever before.

Rare Opportunity In Bitcoin’s Price

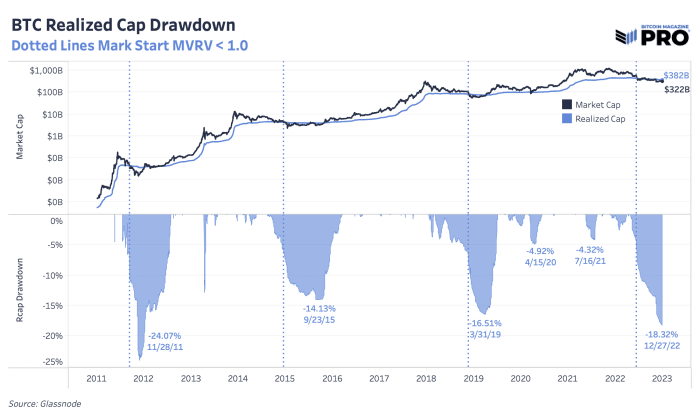

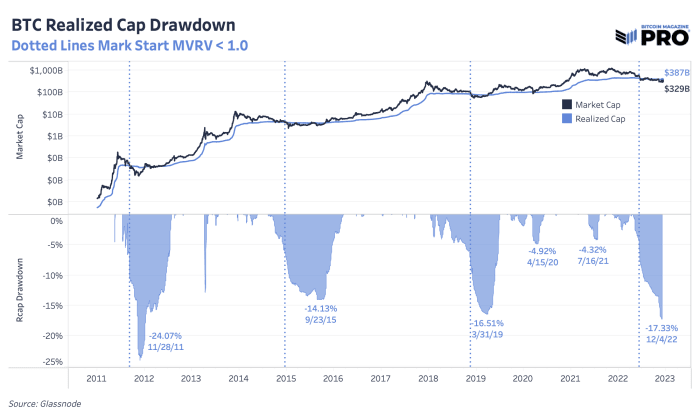

By looking at certain metrics, we can analyze the unique opportunity investors have to purchase bitcoin at these prices. The bitcoin realized market cap is down 18.8% from all-time highs, which is the second-largest drawdown in its history. While the macroeconomic factors are something to keep in mind, we believe that this is a rare buying opportunity.

The realized cap drawdown in 2022 was the second largest in bitcoin’s history.

Relative to its history, bitcoin is at the phase of the cycle where it’s about as cheap as it gets. Its current market exchange rate is approximately 20% lower than its average cost basis on-chain, which has only happened at or near the local bottom of bitcoin market cycles.

Current prices of bitcoin are in rare territory for investors looking to get in at a low exchange rate. Historically, purchasing bitcoin during these times has brought tremendous returns in the long term. With that said, readers should consider the reality that 2023 likely brings about bitcoin’s first experience with a prolonged economic recession.

Macroeconomic Environment

As we move into 2023, it’s necessary to recognize the state of the geopolitical landscape because macro is the driving force behind economic growth. People around the world are experiencing a monetary policy lag effect from last year’s central bank decisions. The U.S. and EU are in recessionary territory, China is proceeding to de-dollarize and the Bank of Japan raised its target rate for yield curve control. All of these have a large influence on capital markets.

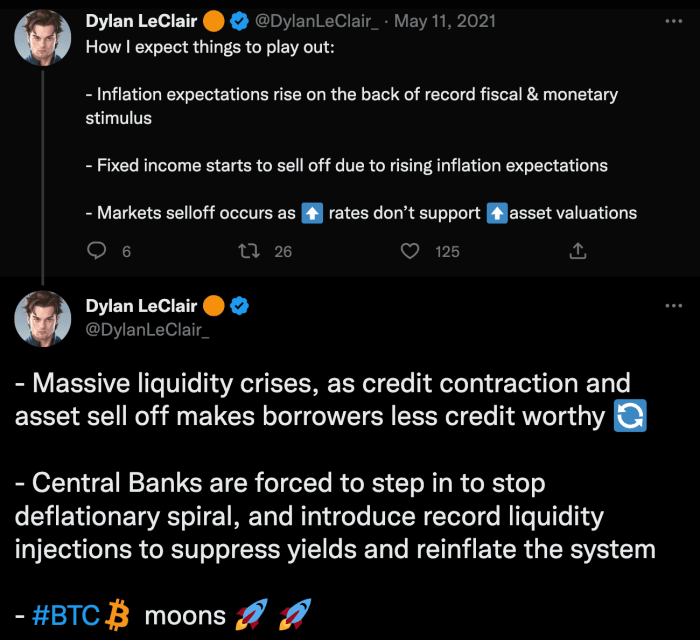

Nothing in financial markets occurs in a vacuum. Bitcoin’s ascent through 2020 and 2021 — while similar to previous crypto-native market cycles — was very much tied to the explosion of liquidity sloshing around the financial system after COVID. While 2020 and 2021 was characterized by the insertion of additional liquidity, 2022 has been characterized by the removal of liquidity.

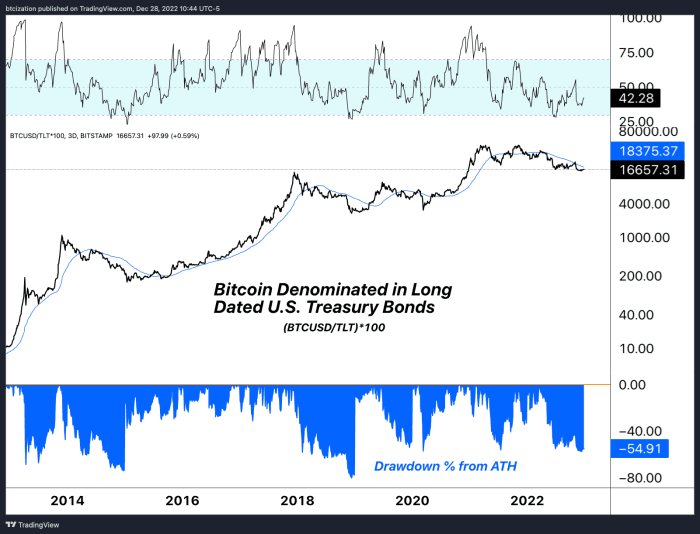

Interestingly enough, when denominating bitcoin against U.S. Treasury bonds (which we believe to be bitcoin’s largest theoretical competitor for monetary value over the long term), comparing the drawdown during 2022 was rather benign compared to drawdowns in bitcoin’s history.

As we wrote in “The Everything Bubble: Markets At A Crossroads,” “Despite the recent bounce in stocks and bonds, we aren’t convinced that we have seen the worst of the deflationary pressures from the global liquidity cycle.”

In “The Bank of Japan Blinks And Markets Tremble,” we noted, “As we continue to refer to the sovereign debt bubble, readers should understand what this dramatic upward repricing in global yields means for asset prices. As bond yields remain at elevated levels far above recent years, asset valuations based on discounted cash flows fall.” Bitcoin does not rely on cash flows, but it will certainly be impacted by this repricing of global yields. We believe we are currently at the third bullet point of the following playing out:

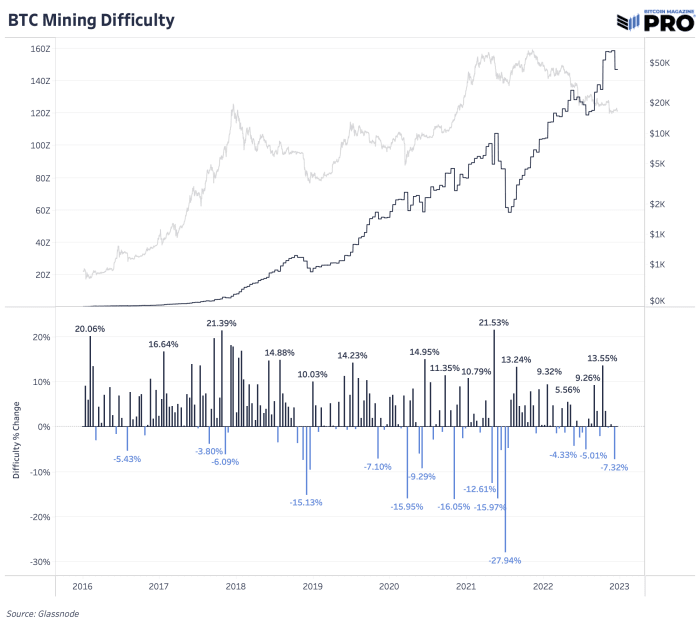

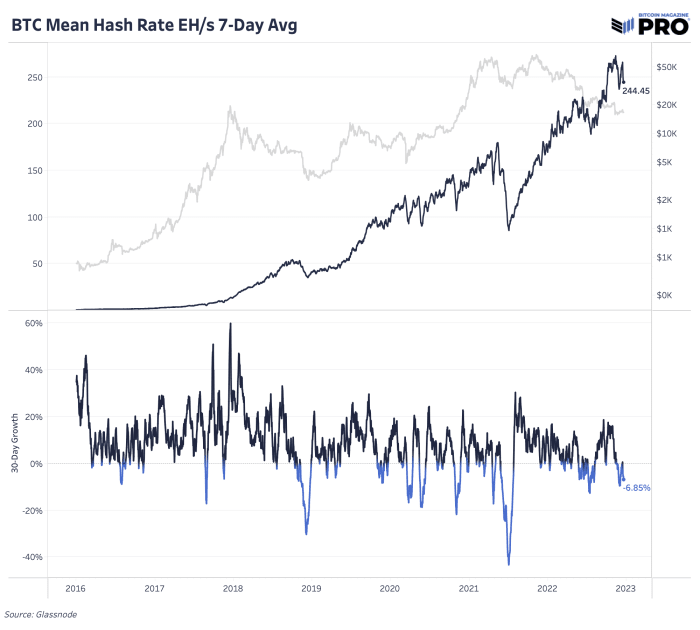

While the multitude of negative industry and worrying macroeconomic factors have had a major dampening on bitcoin’s price, looking at the metrics of the Bitcoin network itself tell another story. The hash rate and mining difficulty gives a glimpse into how many ASICs are dedicating hashing power to the network and how competitive it is to mine bitcoin. These numbers move in tandem and both have almost exclusively gone up in 2022, despite the significant drop in price.

Bitcoin mining difficulty continues to rise.

Bitcoin hash rate continues to rise.

By deploying more machines and investing in expanded infrastructure, bitcoin miners demonstrate that they are more bullish than ever. The last time the bitcoin price was in a similar range in 2017, the network hash rate was one-fifth of current levels. This means that there has been a fivefold increase in bitcoin mining machines being plugged in and efficiency upgrades to the machines themselves, not to mention the major investments in facilities and data centers to house the equipment.

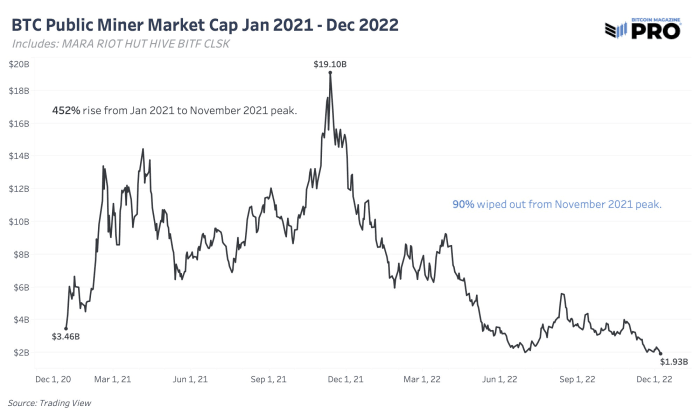

Because the hash rate increased while the bitcoin price decreased, miner revenue took a beating this year after a euphoric rise in 2021. Public miner stock valuations followed the same path with valuations falling even more than the bitcoin price, all while the Bitcoin network’s hash rate continued to rise. In the “State Of The Mining Industry: Survival Of The Fittest,” we looked at the total market capitalization of public miners which fell by over 90% since January 2021.

The market cap of all public mining equities has dropped by 9

We expect more of these companies to face challenging conditions because of the skyrocketing global energy prices and interest rates mentioned above.

Increasing Scarcity

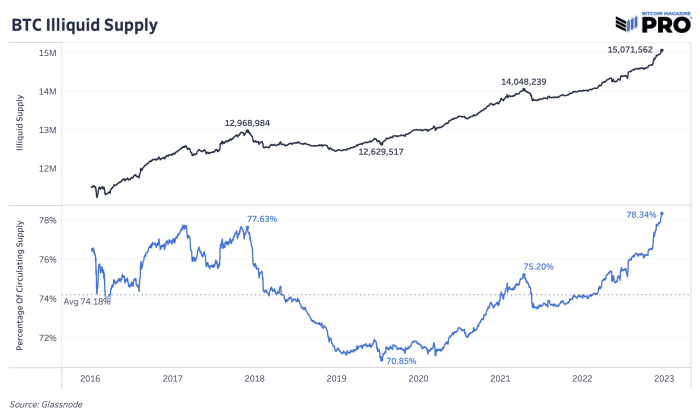

One way to analyze bitcoin’s scarcity is by looking at the illiquid supply of coins. Liquidity is quantified as the extent to which an entity spends their bitcoin. Someone that never sells has a liquidity value of 0 whereas someone who buys and sells bitcoin all the time has a value of 1. With this quantification, circulating supply can be broken down into three categories: highly liquid, liquid and illiquid supply.

Illiquid supply is defined as entities that hold over 75% of the bitcoin they deposit to an address. Highly liquid supply is defined as entities that hold less than 25%. Liquid supply is between the two. This illiquid supply quantification and analysis was developed by Rafael Schultze-Kraft, co-founder and CTO of Glassnode.

Bitcoin’s illiquid supply continues to grow.

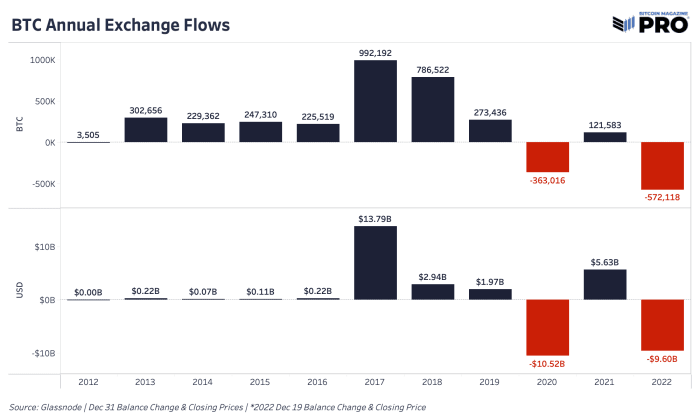

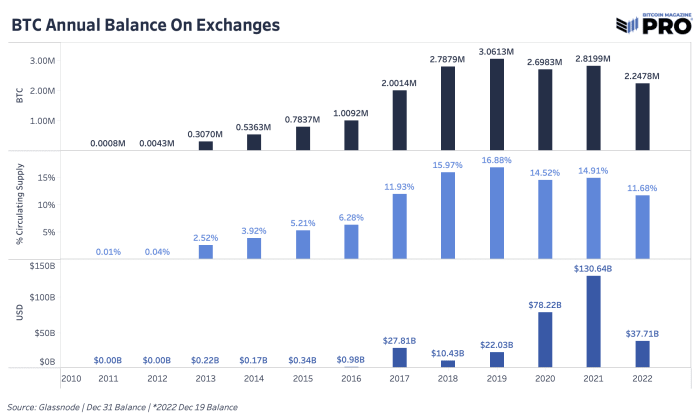

2022 was the year of getting bitcoin off exchanges. Every recent major panic became a catalyst for more individuals and institutions to move coins into their own custody, find custody solutions outside of exchanges or sell off their bitcoin entirely. When centralized institutions and counterparty risks are flashing red, people rush for the exit. We can see some of this behavior through bitcoin outflows from exchanges.

In 2022, 572,118 bitcoin worth $9.6 billion left exchanges, marking it the largest annual outflow of bitcoin in BTC terms in history. In USD terms, it was second only to 2020, which was driven by the March 2020 COVID crash. 11.68% of bitcoin supply is now estimated to be on exchanges, down from 16.88% back in 2019.

Exchanges saw a massive decrease in the bitcoin balances on their platforms.

Bitcoin balance on exchanges decreased in 2022.

These metrics of an increasingly illiquid supply paired with historic amounts of bitcoin being withdrawn from exchanges — ostensibly being removed from the market — paint a different picture than what we’re seeing with the factors outside of the Bitcoin network’s purview. While there are unanswered questions from a macroeconomic perspective, bitcoin miners continue to invest in equipment and on-chain data shows that bitcoin holders aren’t planning to relinquish their bitcoin anytime soon.

Conclusion

The varying factors detailed above give a picture for why we are long-term bullish on the bitcoin price going into 2023. The Bitcoin network continues to add another block approximately every 10 minutes, more miners keep investing in infrastructure by plugging in machines and long-term holders are unwavering in their conviction, as shown by on-chain data.

With bitcoin’s ever-increasing scarcity, the supply side of this equation is fixed, while demand is likely to increase. Bitcoin investors can get ahead of the demand curve by averaging in while the price is low. It’s important for investors to take the time to learn how Bitcoin works to fully understand what it is they are investing in. Bitcoin is the first digitally native and finitely scarce bearer asset. We recommend readers learn about self-custody and withdraw their bitcoin from exchanges. Despite the negative news cycle and drop in bitcoin price, our bullish conviction for bitcoin’s long-term value proposition remains unfazed.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

On-Chain Data Trends

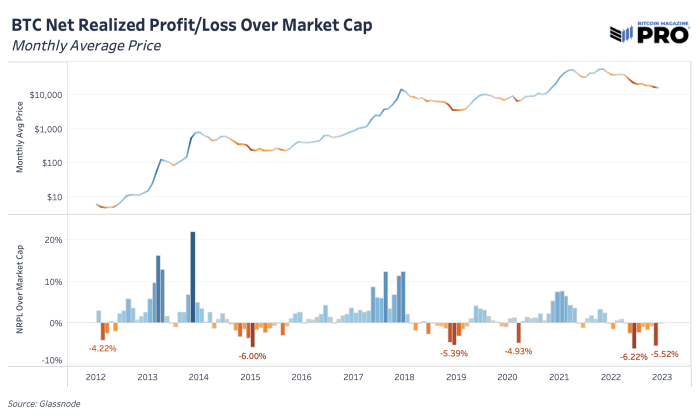

November was a painful month. By looking at on-chain realized profit and loss data, we can see that this was true for many forced-sellers of bitcoin. Before any bitcoin price bottom, a hallmark sign that you want to see is extended periods of forced selling, capitulation and rise in realized losses. One way to view this is by looking at the sum of realized profit and loss for each month relative to bitcoin’s total market cap. We saw these bottom signals in November 2022, and similarly in the July 2022 Terra/LUNA crash, March 2020 COVID fear and December 2018 cycle bottom capitulation events.

Net realized profit/loss over market cap

Looking at the 2018 cycle, the end was marked by excess realized losses, although this was much different with the forced liquidations and cascades of private balance sheet leverage and paper bitcoin unwinding that we saw this year.

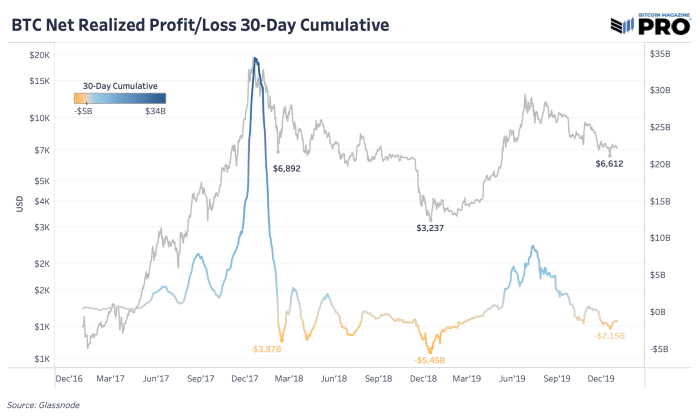

30-day cumulative net realized profit/loss

We’ve talked about the current drawdown in bitcoin’s price and how that compares to previous cycles many times over the last few months. Another way to look at cyclical drawdowns is to focus on bitcoin’s realized market capitalization — the average cost basis of the network which tracks the latest price where each UTXO moved last. With price being more volatile, realized price is a more stable view of bitcoin’s growth and capital inflows. The realized market capitalization is now down 17.33% which is significantly higher than 2015 and 2018 cycles of 14.13% and 16.51%, respectively.

Bitcoin realized cap drawdown

As for duration, we’re 176 total days into the price being below bitcoin’s realized price. Those aren’t consecutive days as price can temporarily go above realized price, but price trends below realized price in bear market periods. For context, trends in 2018 were short-lived at around 134 days and the trends in 2014-15 lasted 384 days.

On one hand, bitcoin’s realized market capitalization has taken a significant hit in the previous round of capitulation. That’s a promising bottom-like sign. On the other hand, there’s a case to be made that price being below realized price could easily last another six months from historical cycles and the lack of capitulation in equity markets is still a major headwind and concern.

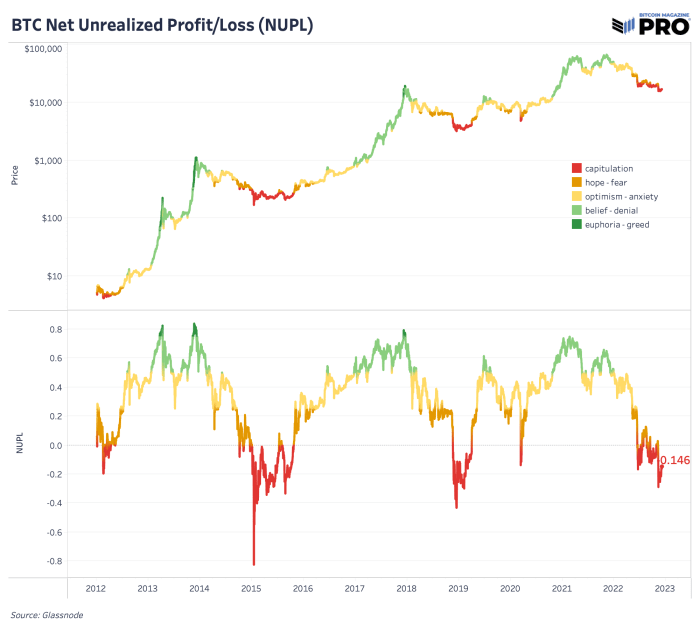

Net unrealized profit/loss

As per the net-unrealized-profit/loss (NUPL) ratio, we are firmly in the capitulation phase. NUPL can be calculated by subtracting the realized cap from market cap and dividing the result by the market cap, as described in this article authored by By Tuur Demeester, Tamás Blummer and Michiel Lescrauwaet.

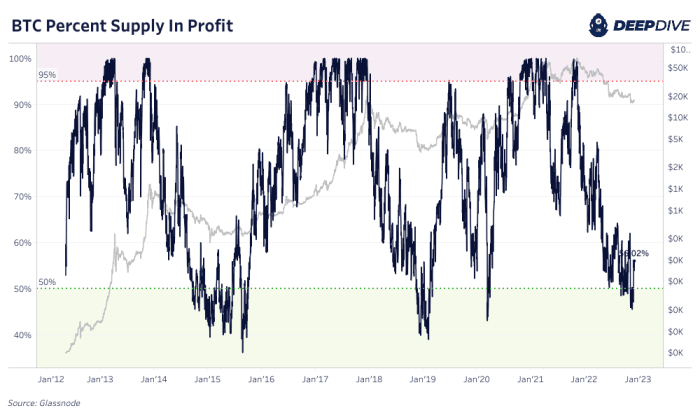

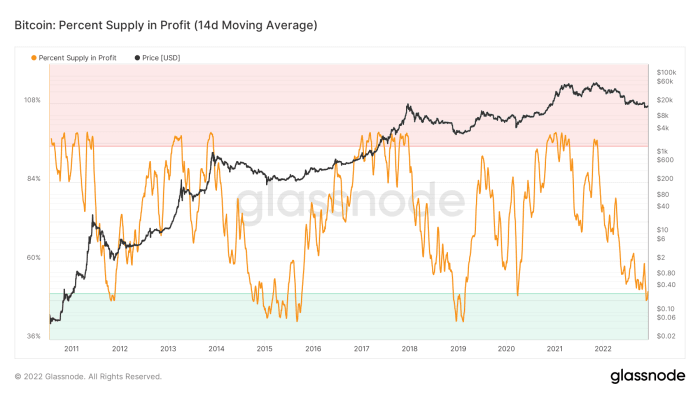

There is no denying it: For bitcoin-native cycles, we are firmly in the capitulation phase. Currently, only 56% of circulating supply was last moved on-chain in profit. On a two-week moving average basis, under 50% supply was last moved above the current exchange rate, which is something that has only ever happened in the depths of previous bear-market lows.

Percent of bitcoin supply in profit

14-day moving average of the percent of bitcoin supply in profit

When thinking of the bitcoin exchange rate, the numerator side of the equation is historically cheap. The Bitcoin network continues to produce a block approximately every 10 minutes in an unabated fashion, as hash rate ticks higher and as the ledger offers an immutable settlement layer for global value. The speculation, leverage and fraud of the previous cycle is washing to shore and bitcoin continues to exchange hands.

Bitcoin is objectively cheap relative to its all time history and adoption phases. The real question over the immediate future is the denominator. We have talked at length about the global liquidity cycle and its current track. Despite being historically cheap, bitcoin is not immune to a sudden strengthening in the dollar because nothing truly is. Exchange rates are relative and if the dollar is squeezing higher, then everything else will subsequently fall — at least momentarily. As always, position sizing and time preference is key for all.

As for the catalyst for a surge higher in the dollar denominator of the bitcoin exchange rate (BTC/USD), there are 80 trillion possible catalysts…

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

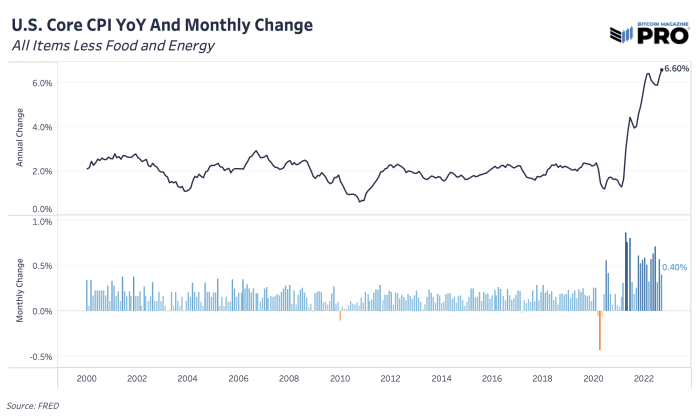

CPI Volatility Doesn’t Disappoint

In the last article, we highlighted a potential for CPI to surprise to the upside and bring more volatility — and that’s exactly what we got and more. We won’t cover the components that drove the surprise in detail since we already highlighted much of that, but the key takeaway is that Core CPI came in hotter than expected at 6.6% year-over-year and 0.4% month-over-month with shelter (rent, housing components, etc) and medical services as key drivers. This is the fastest rate of change in annual headline Core CPI since 1982. To compare the various components over the last three months, check out this chart.

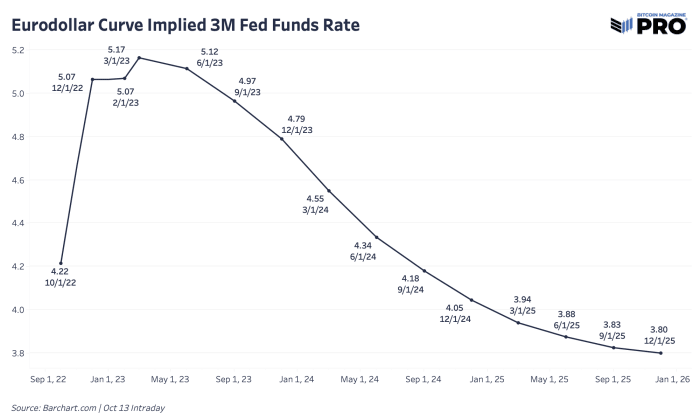

As for the rates, the latest implied federal funds rate from the eurodollar market shows a peak just above 5% in March 2023 before any rate cuts happen at the end of the year.

Where’s The Bitcoin Price Low?

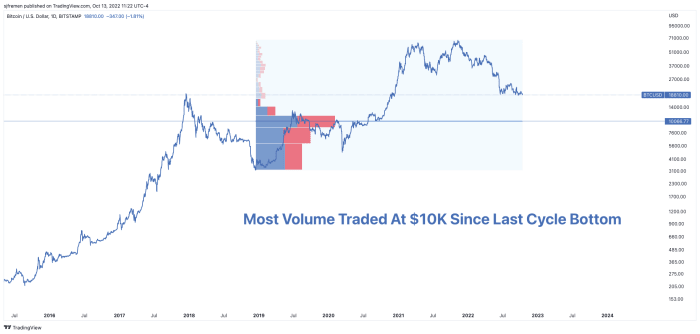

With a fall to $18,000 inching closer and bitcoin facing risks of new year-to-date lows, it’s worth taking a look at a few key bottom price levels to gauge where the price may end up. First, let’s look at the fixed volume range profile of bitcoin since the December 2018 bottom of last cycle. The overwhelming majority of traded volume in the market occurred right around $10,000, also a key psychological level. In a strong downward move, $10,000 is a place where many in the market have their spot cost basis and could start feeling some real drawdown pain or lack of conviction.

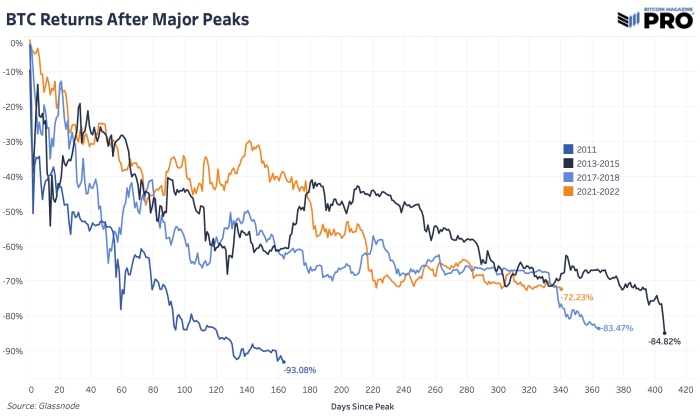

In terms of bear market and cycle duration, let’s revisit the cyclical drawdown chart for bitcoin in current and previous cycles. Currently, we’re right around a 72.23% drawdown from an all-time high closing price of $67,589. If we are going to see a max cycle drawdown come in less than the last two cycles — let’s say around 80% — then we’re looking at a price around $13,500. If we assume that this cycle and popping of valuations will be much worse, let’s say around 85%, then we’re looking at a price around $10,100. The bull case is that we’ve found a durable bottom at $18,000 and we won’t see the max drawdown reach beyond 73%.

From an on-chain perspective, one of the more interesting realized price areas is the realized price held by the cohort of addresses that have 10-100 BTC. Recall that realized price is an estimate of the average cost basis based on the price when UTXOs last moved. This particular group accounts for around 22.6% of all circulating supply. This group would certainly reflect a decent portion of long-term holders and there’s a case to be made that in a deep, prolonged bear market, long-term holders have yet to feel the pain or capitulation that we’ve seen in the past.