Few places present a sense of freedom like the open air. Standing underneath a sweeping sky presents a sense of expansiveness, unboundedness, exhilaration. And while living among the clouds might be nothing more than a flight of fancy, a home can, through its unique location and architecture, capture the all-encompassing sense of peace, possibility, and escape that the wide blue sky promises.

Such a home may be situated on a bluff, on a hilltop, on a mountain, or at the top of an apt-named skyscraper. Or, like this magnificent compound in Charlestown, Rhode Island, it may be set amid private woods and quiet beaches, where there’s nothing to obscure or obstruct the sight lines of the breathtaking horizon, of shooting stars and sunrises. Here are some ways a property can truly take the sky to be its muse.

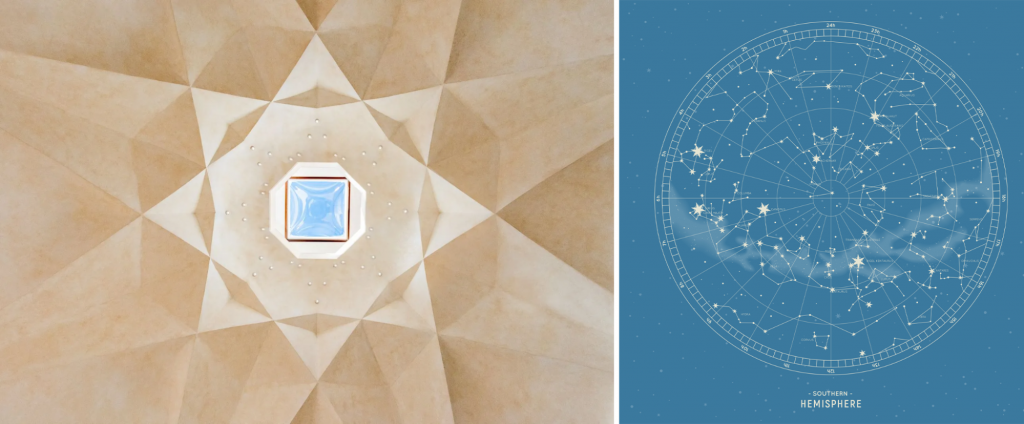

Eyes to the Skies

Nothing says “celestial” like skylights. Throughout this home, windows of different radiating shapes and dimensions crown the pinnacle of each of the peaked roofs, drawing the eye skyward and fostering a perpetual awareness of the sky’s color and closeness. While flat-paned, traditional skylights also feature above the dining room, it’s the faceted dome ceiling in the living room that showcases the most impressive overhead window.

As Above, So Below

Holistically conceived by a single visionary architect, Soheil Tavakoli, the home uses a variety of materials, and synthesizes motifs from both Persian and Native American aesthetics, to bolster its outward and upward views. Azure accents complement and amplify the skylights—from the tile in the kitchen and bathrooms, to the bas-relief interior window and fountain, to the gorgeous geometric pool on the grounds. It goes to show that the sky is best captured through color.

Days in the Sun

To take inspiration from the sky, a home should indulge indoor-outdoor living to the fullest. This property is a masterclass in how to do that, with its picturesque patio, glass-topped gazebo, and fountains and waterfalls spread across its terraces and gardens. A custom-built yoga platform makes it an ideal space for meditation and contemplation, offering fresh air and fresh perspective.

Endless Horizons

Because the skies are increasingly obscured and obstructed by tall towers, industrial infrastructure, and bright lights, location is crucial—and this property is a perfect cloudspotting and stargazing retreat. What better way to enjoy the serenity of the daytime, or the sublimity of the nighttime, than with a leisurely walk across the nearly twenty acres to the exquisite New England shores? Here, there’s nothing between the land, the ocean, and the sky—an elemental experience that eases the mind, even as it quickens the heart.

Ultimately, this unique Rhode Island compound shows that a home doesn’t necessarily have to be in the sky to be inspired by the sky. Brilliant glass surfaces, compatible tones and hues, and distance from urban light and noise pollution allow a property to create an aesthetic of boundless openness, and lift the spirits of those who live there.

It looks more like a project at NASA than a home construction site.

Just outside Austin, Texas, massive machines are squeezing out 100 three- and four-bedroom homes, in the first major housing development to be 3D-printed on site.

One of the nation’s largest homebuilders, Lennar, is partnering with ICON, a 3D printing company, to develop the project. Lennar was an early investor in ICON, which has printed just about a dozen homes in Texas and in Mexico. These homes will go on the market in 2023, starting in the mid-$400,000 range.

“This is the first 100 homes, but we expect to be able to bring this to scale, and at scale we really bring cycle times down and we also bring cost down,” said Stuart Miller, executive chairman of Lennar.

ICON claims it can build the entire wall system of the home, which includes mechanical, electrical and plumbing, two to three times faster than a traditional home and at up to 30% of the cost.

Read more real estate coverage

“We exceed code requirements for all the different kinds of strength, wind, compressive strength by about 4x. We’re about two and a half times more energy efficient,” said Jason Ballard, co-founder and CEO of ICON.

The printers are designed to operate 24 hours a day, but they don’t because of area noise restrictions. They are almost fully automated, with just three workers at each home. One monitors the process on a laptop, and one checks the concrete mixture, which has to be adapted to the current weather conditions. Another works in support, misting the area with water or adding new material into the system.

“The promise of robotic construction is a promise of automation, reducing labor – therefore reducing labor costs,” Ballard said.

ICON aims to get the number of operators down to two over the next 12 months, Ballard added. Eventually, he wants even fewer operators. “I think the sort of Holy Grail is where one person can watch a dozen systems you need one person to watch a dozen systems,” Ballard said.

An ICON 3D printer at a housing development in Georgetown, TX.

Diana Olick | CNBC

The way it works is a digital floor plan is loaded into the software system called Build OS, which then prepares it for robotic construction. It will automatically map out the structural reinforcement, placing the electrical and plumbing outlets during the print. The printers then squeeze out rows and rows of a proprietary concrete mixture that looks much like toothpaste, slowly building up the structure.

Other companies, like California-based Mighty Buildings, are also using 3D printing technology, but they print the homes in a factory and then move them on-site. ICON brings the factory to the site.

“With this project, we’re improving our total house count 400%, and we expect to like continue at least doubling for the next three to five years,” said Ballard. He said he already has plans to work with other large-scale builders. DR Horton is another of ICON’s early investors.

Lennar’s Miller said his primary focus is on bringing more affordable homes to the market, and he sees this as one way to do that. But he knows it’s also still the early stages.

“This is all about innovation. If you go around the country and speak to officials at the local and state level, the single biggest question is: How do we provide workforce housing, affordable housing,” he said.

Lennar began plans on the project with ICON when the housing market was still red-hot, driven by strong demand and record-low mortgage rates. Now mortgage rates are more than double what they were at the start of the year, and demand has fallen off sharply, suggesting their could be added risk to this project.

“We still focus on our core business, making the trains run on time, building homes across the country, and as the market cycles up and cycles down we adjust our business,” said Miller. “Innovation is a cycle as it sits on the side of our business because we know, looking forward, there’s a housing shortage out there.”

WASHINGTON — The average long-term U.S. mortgage rate returned to the 20-year highs of two weeks ago when rates breached 7% for the first time since 2002.

Mortgage buyer Freddie Mac reported Thursday that the average on the key 30-year rate rose to 7.08% from 6.95% last week. A year ago the average rate was 2.98%.

The rate for a 15-year mortgage, popular with those refinancing their homes, climbed to 6.38% from 6.29% last week. It was 2.27% one year ago.

Last week, the Federal Reserve raised its short-term lending rate by another 0.75 percentage points, three times its usual margin, for a fourth time this year as part of its inflation-fighting strategy. Its key rate now stands in a range of 3.75% to 4%.

More increases are likely coming, though there is some hope that the Fed will dial them down as more evidence comes in that prices have peaked.

The Labor Department reported Thursday that consumer inflation reached 7.7% in October from a year earlier, the smallest year-over-year rise since January. Excluding volatile food and energy prices, “core” inflation rose 6.3% in the past 12 months. The numbers were all lower than economists had expected.

Thursday’s report raised the possibility that the Fed could decide to slow its rate hike, a prospect that sent stock prices jumping as soon as the data was released.

Two weeks ago, the average long-term U.S. mortgage rate topped 7% for the first time in more than two decades, which combined with sky-high home prices, have crushed homebuyers’ purchasing power by adding hundreds of dollars to monthly mortgage payments.

Sales of existing homes have declined for eight straight months as borrowing costs have become too big of an obstacle for many Americans already paying more for food, gas and other necessities. Additionally, many homeowners seeking to upgrade or change locations have held off listing their homes because they don’t want to jump into a higher rate on their next mortgage.

The sagging housing market has prompted real estate companies to dial back their financial outlooks and shrink their workforces. Online real estate broker Redfin on Wednesday said it was cutting 862 employees and shutting down its instant-cash-offer subsidiary RedfinNow.

Redfin also laid off 470 employees in June, blaming slowing home sales. Through attrition and layoffs, Redfin has slashed more than a quarter of its workforce on the assumption that the housing downturn will last “at least through 2023,” it said in a regulatory filing.

Another online real estate broker, Compass, has laid off hundreds of workers this year.

While mortgage rates don’t necessarily mirror the Fed’s rate increases, they tend to track the yield on the 10-year Treasury note. The yield is influenced by a variety of factors, including investors’ expectations for future inflation and global demand for U.S. Treasurys.

Hui Ka Yan, a member of the CPPCC National Committee and chairman of Evergrande Group, attends a press conference at the fifth session of the 12th CPPCC National Committee on March 9, 2017 in Beijing, China. (Photo by VCG/VCG via Getty Images)

VCG via Getty Images

Once China’s richest person, Hui falls out of the top 100 for the first time in 14 years.

Hui Ka Yan, the founder of real estate firm China Evergrande Group, has lost nearly all of his once massive fortune. Worth $42.5 billion and ranked the richest person in Asia at his peak in 2017, his wealth has been drastically diminished as debt woes plague the embattled developer. Yet as pressure mounts for the former tycoon to find a concrete way to repay his firm’s debts, analysts say he will certainly lose a lot more.

The 64-year-old, who dropped out of the 2022 ranks of China’s top 100 richest for the first time since his 2007 debut, now has an estimated net worth of $2.9 billion, an amount that is based entirely on the dividends he’s received over the years, though some of it has since been plowed into mansions, jets and a yacht. The number excludes Hui’s 60% stake in Evergrande, whose shares were suspended from trading in March, and still can’t meet the criteria for a resumption. Even before the suspension, the firm had lost about 95% of its peak value.

But even his personal assets are not safe from the firm’s creditors. Hui was forced to use $1 billion of his own cash to pay down Evergrande debt late last year earlier this year, and he sold earlier this year two luxury apartments at a discount–one in the city of Shenzhen and one in Guangzhou–for a combined $50 million (360 million yuan), apparently to help pay off more.

As Evergrande struggles to come up with a plan for restructuring its more than $300 billion in liabilities, which according to one person with knowledge of the matter will probably get delayed again and pushed out into 2023 due to the sheer size and complexity of the matter, more of his remaining trophy assets are likely at risk. Chen Zhiwu, a professor of finance at the University of Hong Kong, says amid China’s drastically changed political environment, the pressure is “really high, if not higher” for Hui to keep paying down corporate liabilities with his own money.

In fact, one of his three homes in Hong Kong’s prestigious The Peak neighborhood was seized by China Construction Bank (Asia) last week in November after Evergrande defaulted on a loan collateralized by the $90 million (estimated market value) property.

“Of course, he would like his personal assets and corporate assets very clearly separated, which officials aren’t willing to accept,” Chen says. “What this means is that when his company debt is in default, some of his personal fortune may have to be used to contribute to the payments to debt holders.”

The facade of 2-8a Rutland Gate, which is thought to be the most expensive home ever marketed in Britain, is recently put on sale by beleaguered billioniare Hui Ka Yan(Photo by Leon Neal/AFP via Getty Images).

AFP via Getty Images

Hui, who according to Evergrandethe company’s website is still a member of the ruling Communist Party, has pledged his two other luxury homes in the same posh Hong Kong locale as collateral for loans from Orix Asia Capital. He is also looking to sell his 45-room Knightsbridge mansion overlooking London’s Hyde Park area, two years after buying it from a Saudi prince for $232 million. And he owns private jets and a $60 million superyacht that he could be forced to sell.

As Evergrande’s revenues have fallen off a cliff (it only recorded $2.5 billion in contracted sales during the first eight months of the year, a plunge of around 96% from the prior year), Hui is unlikely to convince creditors that the company could ever generate enough cash flow for future repayment.

Of course, he would like his personal assets and corporate assets very clearly separated, which officials aren’t willing to accept.

Meanwhile, a nationwide mortgage boycott by angry buyers, who paid for their purchases in full but aren’t getting apartment complexes delivered on time after troubled developers such as Evergrande ran out of money, is putting pressure on the government. To quell public protests, which are rare in China, officials have agreed to issue special loans totaling $27.6 billion (200 billion yuan) to help with this type of work. Victor Shih, an associate professor of political economy at the University of California, San Diego, says banks are likely to have been told to lend to the financing arms of local governments, so that they could buy the unfinished projects from distressed real estate firms at a small discount. Evergrande said in September it had resumed working on 95% of its 706 pre-sold but undelivered construction projects.

But aside from protecting the interests of average homebuyers, few expect Beijing to reverse its course and unveil broader sector bailout measures–which are seen as crucial to restoring offshore creditor confidence. Kaven Tsang, a Hong Kong-based senior vice president at Moody’s Investors Service, says the economic pain inflicted by the real estate meltdown–including defaults, falling sales and rapidly slowing growth–are “within the [government’s] tolerance level.”

“The central government has made it clear in the past that they aren’t going to use the property sector to support the economy,” says Tsang. “We haven’t seen any changes so far.”

An Evergrande residential development under construction in Beijing, China. (Photo by Bloomberg)

Ron Thompson, a Hong Kong-based managing director at consulting firm Alvarez & Marsal Asia, says he thinks it would take at least two years for China’s housing demand to stabilize. Moody’s estimated in October that China’s property sales would continue to decline over the next 12 months, after shrinking 21% in August from the prior year, and 15.3% in September. Default risk remains high, given that the country’s developers have at least a combined $55 billion in bonds due over the next two years, but face weaker sales and limited refinancing options.

Amid this environment, bond investors mired in the restructuring of defaulted developers “aren’t expecting 100 cents on the dollar,” and are likely to demand equity and other collaterals to compensate for their rising losses, says Alvarez & Marsal Asia’s Thompson. Those who have lent specifically to Hui are increasingly taking things into their own hands, with more asset seizures and “wind-up” petitions to liquidate assets due to unpaid financial obligations, says Brock Silvers, a Hong Kong-based chief investment officer at Kaiyuan Capital, which invests in distressed assets.

Evergrande is facing a wind-up hearing in Hong Kong on Nov. 28, which was first brought in June by creditor and Samoa-based investment holding Top Shine Global Limited over $110 million in unspecified financial obligations.

Evergrande’s Hong Kong headquarters, which it acquired for $1.6 billion (HK$12.5 billion) in 2015 from Chinese Estates Holdings, controlled by Hui’s billionaire friend Joseph Lau, has also been seized by creditors and recently put on sale. The 26-story China Evergrande Centre located in Wan Chai now has an estimated value of around $1 billion, and the bidding process, concluded in late October reportedly drew interest from billionaire Li Ka-shing’s CK Asset Holdings.

Evergrande’s Hengchi 5 electric vehicle is on display at Hengchi experience center in Shanghai, China. (Photo by Wang Gang/VCG via Getty Images)

VCG via Getty Images

Hui appears to be pinning his last hope on electric cars. The Hong Kong-listed China Evergrande New Energy Vehicle Group , two thirds owned by parent Evergrande and whose trading has also been suspended since March, announced in late October that it had delivered the $24,700 Hengchi 5 electric sports utility vehicle to the first batch of 100 buyers, constituting a “major milestone” for Hengchi Auto. Parent company Evergrande also said in a July filing that it may offer equity interests in its EV unit as part of a “supplemental credit enhancement” package for restructuring offshore debt.

But Shen Meng, managing director at Beijing-based boutique investment bank Chanson & Co., says the EV deliveries offer little comfort to creditors. The beleaguered Hui, who once cherished ambitions to become the Elon Musk of China and propel Evergrande above Tesla, still has a long way to go before establishing Hengchi as a stable brand.

“The deliveries of the first batch doesn’t mean the maturing of Evergrande’s EV business, as it will take quite some effort to start bigger-scale production and delivery to the mass,” says Shen. “The EV unit is unlikely to be seen as a reliable asset, and it won’t help much with the restructuring process.”

George Hongchoy of Link Asset Management believes that a wide price gap between optimistic sellers and cautious buyers are reducing deals in real estate markets, and someone has to move on pricing.

Designed and crafted to meticulous standards, this distinguished 6.2 acre compound is surrounded by captivating, protected vistas far and wide. In the enduring tradition of the regions’s iconic estates, this extraordinary residence is a place for living life to the fullest, providing an endless source of enjoyment in exquisite indoor/outdoor spaces.

Fine millwork and nine fireplaces underscore the comfortably elegant environment. Rooms for relaxation include a lower-level entertainment (media) room, a wine cellar, and a fitness studio. Wraparound tiered terraces feature a pool and a pool house. Glorious terraced gardens and formal gardens with fountain create a splendid backdrop for the estate. A separate three-bedroom guest house completes the property.

HIGHLAND PARK, IL – OCTOBER 21: A gate with the number 23 controls access to the home of basketball … [+] legend Michael Jordan on October 21, 2013 in Highland Park, Illinois. Twenty-three is the number Jordan wore while playing basketball for the Chicago Bulls. The home which had been offered for sale for $29 million and later dropped to $21 million is scheduled to be sold at auction on November 22. The 32,683-squre-foot home features nine bedrooms, 19 bathrooms, a 15-car attached garage and an “NBA-quality” basketball court. (Photo by Scott Olson/Getty Images)

Getty Images

The careers of most athletes are short-lived. 3.5 years is typically the average number of years WNBA players have to play at a high level. To most athletes, each day isn’t just a chance to get better on the court, but also a day to prepare for what the future may hold.

Liberian-American basketball star Matee Ajavon went on to have an illustrious start to her career by winning the Gold Medal in the Pan-American Games in Rio De Janeiro, Brazil while attending Rutgers University. Her team, led by the famous Coach C. Vivian Stringer also went to the 2007 NCAA Championship Game vs. Tennessee University only to fall short of a win.

When the Houston Comets drafted Matee Ajavon as the fifth overall pick in the 2008 WNBA Draft, she instantly knew she had been given an opportunity that most athletes only dream of throughout their lifetime. Matee was 1 of the 144 women that could actually call themselves a WNBA pro.

Her career beat the odds by lasting for a total of 10 years. Matee played with the Houston Comets (1 year), Washington Mystics (5 years), and Atlanta Dream for the last 4 years of her career. She also played in 5 different countries that included Turkey, Brazil, Israel, Poland and Romania in the off-season. Going overseas allowed some WNBA players to earn up to 10x the salary they would in the WNBA.

LOS ANGELES, CA – JULY 16: Matee Ajavon #10 of the Atlanta Dream handles the ball against the Los … [+] Angeles Sparks in WNBA game at Staples Center on July 16, 2015 in Los Angeles, California. (Photo by Leon Bennett/Getty Images)

Getty Images

In the latter stages of her career, Matee admits that she always felt the need to diversify and invest her earnings. Her search eventually led her to Real Estate Gurus; a company led by Real Estate professional Justin Giles. Giles introduced a then-retired Matee Ajavon to a whole new world by helping her build a real estate investment business.

Giles is a well-known real estate advisor and licensed real estate broker of 17+ years and has been behind the making of quite a few athlete-turned-real estate investors. He utilizes his social media platform on Instagram to educate and connect his many followers on ways to simply start investing in real estate.

His strategies, as explained in two of his books, Zero Down and Learn To Fish And Eat Forever, have also been widely received and critically acclaimed.

The number of former and current athletes investing in real estate has multiplied over time. Roger Staubach, Emmitt Smith, Magic Johnson, Shaquille O’Neal, David Robinson, Alex Rodriguez, & Martin Braithwaite immediately come to mind,

A Familiar Market

Professional athletes, especially in leagues like the NBA, WNBA, or the NFL, are traded quite often from team to team during their careers. This also means they have to purchase or rent properties from different parts of the country.

Athletes rarely have the chance to play for their home teams, which means they are likely to maintain at least two properties at any given time. One of them being their home state and the other being their current location.

While many A-list players may have people who put property deals together for them, most others have to get involved personally. In turn, this puts them squarely in the bustle of the industry. Whether knowing or unknowingly, many athletes end up as real estate investors or somewhat develop an idea or love for the industry.

Senegalese-born former Chicago Bulls star Luol Deng started a real estate symposium to educate players on the value of the sector. At the time he said, “I’ve always had a love for real estate and wanted to do something in Chicago for a long time,”

“We talk about players going broke, but we don’t talk about why that is happening,” Deng says. “The symposiums were a way to teach players about real estate and foster a better understanding of these kinds of investments.”

CHICAGO, IL – MAY 15: Luol Deng #9 of the Chicago Bulls attempts to steal the ball from LeBron … [+] James #6 of the Miami Heat in Game One of the Eastern Conference Finals during the 2011 NBA Playoffs on May 15, 2011 at the United Center in Chicago, Illinois. NOTE TO USER: User expressly acknowledges and agrees that, by downloading and or using this photograph, User is consenting to the terms and conditions of the Getty Images License Agreement (Photo by Jonathan Daniel/Getty Images)

Getty Images

A Low Entrance Bar And High Availability

Few people consider the real estate market as having a low entrance bar because of the high prices quoted for properties. Not every athlete can afford to splash $36 million on a Beverly Hills mansion like LeBron. But according to Giles, they don’t have to;

“Athletes are often looking to invest their earnings and savings into the real estate industry. So they have to learn the art of finding the best deals from anywhere in the country. At every price point, there will always be an available and lucrative property somewhere and also loans available to help anyone acquire properties.”

“Even though some pro-athletes may be familiar with buying and selling properties, they still need to learn the small details of how to actually buy and sell properties as a ‘realbusiness’. The first thing is learning how to find these deals that may not be in plain sight, next how to renovate these properties with the help of contractors, and last and definitely not least, how to turn it into healthy profits.”

The real estate market also offers many options for investment; while athletes like the NFL’s William Sweet buys and rent out their properties, others could choose to flip homes or buy and hold assets as part of their real estate portfolio.

DENVER, CO – AUGUST 29: William Sweet #75 of the Arizona Cardinals walks in the bench area during a … [+] preseason National Football League game against the Denver Broncos at Broncos Stadium at Mile High on August 29, 2019 in Denver, Colorado. (Photo by Dustin Bradford/Getty Images)

Getty Images

“There are properties that are entering foreclosure, and I teach people how to stop a foreclosure even 24 hours before the auction.” Giles explains, “There are houses owned by deceased individuals who passed on without a will. Whenever that happens, there are ways to help their heirs claim these properties and then purchase the properties from them. If you know where to look, properties are always available using these strategies”

Robbie Fowler, an ex-Liverpool Football Club and England FC star who is now estimated to be worth roughly £30 million ($34 million) also opined, “Don’t get me wrong, not everything went into property at the time. And I didn’t just invest on my own, because when I was 18, I was on next to nothing and I couldn’t afford it, regardless of what people think about football players”.

“I invested with partners. It was all through the advice I was given, not because I knew anything or wanted to know it, it was totally by accident”.

He continued, “When you’re 18, I think it is probably the last thing on your mind. You’re obviously signing new contracts and you want to go out, you probably want a new car, and you’ll get all the things that you haven’t had”.

BRISBANE, AUSTRALIA – MARCH 04: Roar coach Robbie Fowler poses during an International Champions Cup … [+] media opportunity, ahead of matches between Crystal Palace FC, West Ham United FC and the Brisbane Roar at Suncorp Stadium on March 04, 2020 in Brisbane, Australia. (Photo by Jono Searle/Getty Images)

Getty Images

“But then all of a sudden, there comes a time when you think: Uh, I need to pull the reins in a little bit here and maybe look after my life after football. When I was 18, that was far from my mind, but over the years, it does materialise that way”.

Passive Income

Every investor’s dream is to have a portfolio that yields more passive income than active income. Athletes and celebrities often invest in stocks and bonds to get passive income, but the fluctuating markets have dissuaded many of them and made real estate investing a bit more attractive. This desire for passive income has led several pro athletes to invest in real estate investment trusts (REITs). While REITs are often considered safe, they are also more of a long-term strategy.

“After the housing crash of 2008, I found myself in so much debt. But somehow, I decided to stick with real estate, and over time I have devised investment strategies that make investing in real estate virtually recession-proof.” Giles believes that there is no such thing as a bad property market.

Justin Giles – The Celebrity-Athlete’s Pathway; Why Professional Athletes Are Investing Heavily Into … [+] Real Estate

REG

If the storied investment successes of NBA greats like Shaquille O’Neal and Magic Johnson are anything to go by, pro athletes will be investing in real estate for quite some time.

A man enters a Bank of America branch in New York.

Scott Mlyn | CNBC

Mortgage rates rose again last week, throwing even more cold water on demand from both current homeowners and potential homebuyers. Weekly application volume fell 0.1% last week from the previous week, according to the Mortgage Bankers Association’s seasonally adjusted index.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) increased to 7.14% from 7.06%, with points increasing to 0.77 from 0.73 (including the origination fee) for loans with a 20% down payment.

“Mortgage rates edged higher last week following news that the Federal Reserve will continue raising short-term rates to combat high inflation. The 30-year fixed rate remained above 7 percent for the third consecutive week, with increases for most loan types,” said Joel Kan, MBA’s deputy chief economist.

Refinance demand, which has been positively crushed by the sharp rise in interest rates, fell another 4% for the week and was down 87% compared with the same week one year ago. Mortgage rates started this year around 3%, so there are very few borrowers left who could benefit from a refinance at today’s higher rates. Refinance demand is now at a 22-year low.

Mortgage applications to purchase a home increased 1% for the week. While that wasn’t a major move, it was the first increase in six weeks. Purchase demand, however, is still down 41% from a year ago and close to a seven-year low.

The adjustable-rate mortgage (ARM) share of activity increased to 12% of all applications. ARMs offer lower interest rates, and while they are considered riskier loans, their rates can be fixed for up to 10 years.

Mortgage rates have been moving sideways to start this week, but that could change Thursday, as investors await the October reading from the government’s consumer price index.

Owning a historic property offers a unique opportunity for an individual to act as a steward of a city’s and nation’s history and to interpret and share that heritage. This early-20th-century landmark in the prestigious San Francisco neighborhood of Pacific Heights affords just such a valued opportunity. Immediately captivating from any vantage point within eyeshot, the striking Tudor Gothic manor has a provenance deeply rooted in the life of “the City by the Bay.” In 1915, one area luminary, M. H. de Young—founder of the paper that came to be known as the San Francisco Chronicle and namesake of the famed museum in Golden Gate Park—commissioned the residence from architect Willis Polk. At the peak of his talents, Polk was widely recognized as one of the city’s most prolific and influential architects and urban planners, a legend in his own right.

While the 8,990-square-foot home has undergone a painstaking renovation by the current owners, vestiges of period aesthetics remain and are readily apparent throughout: the dramatic gray concrete façade, slate-clad gables, stately copper chimneys, an elegantly ornate two-story bay window, diamond-patterned leaded-glass windows and doors, ornamentally detailed fireplaces, intricate moldings, richly hued hardwood floors, and graceful arched doorways. Perhaps its most distinguishing attribute is the curious streetside half arch. Mr. de Young gifted this residence to one of his daughters—Constance Tobin, for whom the manor takes its official name—and intended for a mirroring adjoining home to be constructed for a second daughter, who reportedly chose to live elsewhere, so the twin structure never came to be. The arch still serves a purpose, of course, leading to a breezeway that accesses the rear grounds—roughly an eighth of an acre of verdant lawns, flourishing colorful gardens, and sun-washed terraces.

While the home’s main level is dedicated to entertaining—a light-filled living room, a formal dining room with an eye-catching fireplace, a sitting room with floor-to-ceiling leaded-glass doors opening to the enviable garden, and a spacious modern kitchen with a butcher-block-topped island, plentiful cabinetry and other storage, top-caliber appliances, marble countertops, and a built-in dining banquette—the upper levels, reached via a barrel-vaulted staircase, are devoted to the private quarters.

The peaceful owner’s suite occupies some 1,000 square feet of the second floor and boasts a wall of south-facing windows, a warming wood-burning fireplace, a private terrace, a large library or sitting room, and luxurious bath with a glass-walled shower and a soaking tub. On the third level, two bedroom suites share a lofty sitting room with a vaulted skylit ceiling and useful built-ins; each suite benefits from a walk-in closet and a private terrace for surveying the rarefied environs of Pacific Heights. The lower level is a delightful, versatile space with an entertainment area, a gym or recreation room with a wet bar, an office, abundant storage, and a full bath.

The home’s undeniable classicism notwithstanding, contemporary comforts and conveniences have been attended to: a gym, a wine room, superior appliances, and automatic security gates that offer access to the three-vehicle carport. A multizone alarm system, a sophisticated camera system, and a whole-house sprinkler system provide peace of mind for the discerning buyer who chooses to steward this residence well into the 21st century and its continuing role as a San Francisco landmark.

From a seafront property in Lidingo, Sweden, to an elegant estate in Seattle, Washington, these are this month’s four featured notable properties for sale over $10 million.

This extraordinary ranch estate offers two private lakeshore homes with well over 14,300 square feet of combined luxurious living space, over 1,200 feet of shoreline, and two docks.

King’s View is a luxury home situated on the private south end of Harbour Island. It is a five-minute walk to the famous Pink Sands Beach and a quick drive into town or to any of the other main attractions on the island.

Opinions expressed by Entrepreneur contributors are their own.

As an investor, taking calculated risks is part of your job. Not every investment is profitable, and you can’t always know the risks you’re taking when buying a property. Problems could arise many years down the line. For example, an apparently sound building could develop infrastructure problems after several years of ownership. Or an unpredictable squabble between tenants could turn into a liability issue you couldn’t have foreseen.

For this reason, it’s essential to protect yourself from risk by purchasing insurance. Both you and your tenants should have coverage to protect you should something unpredictable occur. But how much will your coverage cost? Why do your renters need insurance, too?

Let’s explore these questions and discover why insurance policies are critical to your rental business.

Like any insurance coverage, landlord insurance protects you and your rental business against potential losses and liabilities.

Here’s how it works: When you buy a property, you work with an insurance provider to decide which dwelling policy (DP) you want. Dwelling policies are insurance plans for property owners with varying levels of coverage.

For instance, the cheapest dwelling policy might only provide basic coverage for fires or storms. More substantial dwelling policies may add other types of natural damages, lost rent if those disasters make your units uninhabitable or liabilities.

What does landlord insurance cover?

A typical landlord insurance plan covers three types of losses:

Property damage to your building or equipment, including that caused by natural disasters, fires, wind, lightning or criminal break-ins

Lost rent from months wherein your properties are uninhabitable due to any of the above damages

Liabilities, or legal claims (including medical bills, legal fees or court costs) made against you, usually resulting from an injury on the property.

These three types of coverage are standard across many insurance plans. However, you also have the option to purchase additional coverage. These add-on policies may cover vandalism, construction damage, or upgrading to fulfill building or health code policy changes.

Another thing to note is that flood and eviction insurance are not included in a typical landlord dwelling policy. Coverage for these losses must be purchased separately.

When deciding on your coverage, think about where your properties are located. Is the geographical area vulnerable to flooding, wildfires or earthquakes? Is the crime rate in the neighborhood high? If so, you might consider purchasing more comprehensive insurance coverage.

How much does landlord insurance cost?

The average cost of landlord insurance is around $1,200-$1,300 a year, paid in monthly installments. This is approximately 25% more than a typical homeowners insurance policy with the same coverage — because renters tend to introduce more risk.

However, the cost ultimately depends on several factors, including the building’s age, the materials used to construct it, the presence or absence of pets, the dwelling policy you choose and the location of your property.

In general, dwelling policies that use replacement cost value (RCV) are valued higher than those that use actual cash value (ACV). RCV represents the cost of rebuilding your property at today’s construction rates, while ACV represents the current, actual value of your property. Coverage based on RCV will lead to higher premiums.

Why buy landlord insurance?

If you take care of your properties, do you really need to be insured? Landlord insurance is highly valuable and usually worth the monthly fee. Here are some of the top reasons to purchase landlord insurance:

Protect your investment: You can’t predict what might happen to your properties or your tenants. It’s best to be prepared.

Achieve better interest rates on your mortgage: Some lenders require landlord insurance.

Take advantage of tax deductions: Landlord insurance premiums are usually fully deductible as operating expenses that you can subtract from your taxable income.

If landlord insurance protects your properties, what does renters insurance cover? Your landlord coverage won’t cover every loss related to your rental properties. Your renters need insurance coverage for their losses as well.

What does renters insurance cover?

Like landlord insurance, renters insurance typically covers three types of losses:

Personal property and tenant belongings, such as clothes, electronics or valuables

Liabilities due to a tenant’s responsibility for an injury or property damage

Living expenses in the case that a tenant’s unit becomes uninhabitable and they must find other accommodations until repairs are made

You may decide to offer a standard renters insurance package to your tenants, but they might also wish to purchase their own coverage. For instance, if a tenant keeps particularly valuable items in their unit, they may wish to add on scheduled personal property or valuables coverage.

Tenants may also purchase theft extension coverage to cover their cars, boats or trailers; credit card coverage for unauthorized transactions; or other add-on policies.

How much does renters insurance cost?

Renters insurance is relatively inexpensive for tenants. The average cost is around $15 per month. However, this cost varies depending on the coverage level.

Ultimately, the benefits offered by renters insurance are well worth the monthly premium. Your tenants may not appreciate the extra fee up front, but they’ll be thankful they have coverage should something happen.

Why require renters insurance?

Many landlords make renters insurance a requirement to rent their units. This is generally a smart move, and here are our top reasons why:

Prevent resentment for damages: Your tenants are less likely to sue you or pursue litigation if their insurance policy covers the loss.

Be transparent: In the event of a natural disaster, for instance, your tenants may expect that your landlord insurance will cover their belongings. They’ll be surprised to learn that it doesn’t. It’s better to inform your tenants upfront.

Avoid unnecessary complications with your insurance: If an accident occurs on your properties, it’s likely that your tenants’ renters insurance will kick in first. This saves you the trouble of interacting with your insurance company until necessary.

If you’re ready to get started with landlord and renters insurance, here are a few tips and tricks:

If your property management software offers renters insurance as a secondary feature, use it: This saves your tenants the trouble of finding a policy themselves and allows you to determine which type of coverage you think your tenants need.

Track renters insurance policies: Remind tenants to renew their policies before their coverage expires.

Avoid making claims for minor damage: Conserve your coverage for more severe losses and prevent your rate from increasing.

Ask for a discount if you own multiple buildings: You never know which deals are available until you ask.

Disasters and accidents can be entirely beyond your control. However, by preparing for them ahead of time, you’ll know you’re protected in case of a major loss or casualty in your rental business. Both you and your tenants will appreciate the peace of mind and protection offered by insurance.

A home awaits sale at a reduced asking price in Glendale, California.

David McNew | Getty Images

The historic run-up in home prices during the first two years of the pandemic gave homeowners record amounts of new home equity.

Since May, however, about $1.5 trillion of that has vanished, according to Black Knight, a mortgage software and analytics company. The average borrower has lost $30,000 in equity.

Homeowner equity peaked at $17.6 trillion collectively last May, after home prices jumped 45% since the start of the pandemic.

At the end of September, prices were still up 41%, and equity was still quite strong. Borrowers who bought their homes before the pandemic collectively have $5 trillion more than they did before the pandemic hit. That translates to a gain of $92,000 more equity per borrower than in February of 2020.

“While additional declines may be on the horizon, homeowner positions remain broadly strong,” noted Ben Graboske, Black Knight’s president of data and analytics.

But home prices began to weaken as mortgage rates rose in the spring, making it a lot less affordable to buy. The monthly payment on the average home, with a 20% down payment on a mortgage, is up nearly $1,000 since the start of the year.

In 10% of major markets — including Las Vegas, Miami, Los Angeles, Phoenix, Tampa and San Diego — homeowners have to spend twice the long-term average amount of median household income to make their monthly payments.

That’s why home sales began dropping sharply back in May — and why prices have been following suit.

Home prices fell in September on a month-to-month basis for the third month in a row, though the decline wasn’t as steep as in July and August. While prices usually drop from summer to fall due to the seasonal slowdown, they fell much more sharply than usual in 2022.

Prices are now down 2.6% since the end of June, which is the first three-month drop since late 2018 and the steepest such drop since the financial crisis of early 2009. Since July, the median home price is down by $11,560. Prices, however, are still 10.7% higher than they were in September 2021.

As of the end of September, the amount of collective equity available to borrowers while still keeping 20% equity in the home fell by $1.17 trillion since May. That’s the first decline in so-called tappable equity in three years.

The share of borrowers who owe more on their mortgages than their homes are worth is still quite low, at just 0.85%. But the numbers are beginning to rise.

Less than 500,000 borrowers are currently underwater on their mortgages, but that is still double what it was in May. Those who purchased their homes in the past year will be most at risk of going underwater since they bought at the peak of the market.

“This is obviously a situation that demands careful, ongoing monitoring, but to put that into context, just 3.6% of nearly 53 million U.S. mortgage holders are either underwater or have less than 10% equity in their homes roughly half the share coming into the pandemic” Graboske said.

William Beardmore-Gray of the real estate company says some of that decline has already been seen in markets such as New Zealand, Canada and the Nordic region.

Spending a few minutes in a sauna has been known to release endorphins and improve physical and mental health. Whether part of a spa-inspired bath or freestanding in an idyllic backyard, these home saunas are bound to banish the winter blues.

In a pastoral 2.31-acre setting, this impressively scaled estate features a living room with a double-height fireplace, a chef’s kitchen, a sunny breakfast room, a formal dining room, a butler’s pantry with a wine refrigerator, a playroom, a wine cellar, a gym, a golf simulator, a family room with a fireplace, and a backyard patio, pool, spa, grilling area, and fire pit. Of the six bedrooms, the owner’s suite includes a luxurious bath with a soaking tub, a shower, and a sauna.

On the sunny northern slope of San Francisco’s Bernal Heights, this thoughtfully renovated modern home features and open-concept kitchen, dining room, and family room; a separate living room; three decks with views of Twin Peaks, the Golden Gate Bridge, Mt. Tamalpais, and the downtown skyline; and three bedrooms, including a primary suite with a well-outfitted walk-in closet. The professionally designed backyard is an idyllic escape with fruit and maple trees, lavender, herbs, an Adirondack swing, an outdoor shower, and a classic barrel sauna.

Perched high above Pacific Palisades with views of Catalina Island and the Queen’s Necklace, this five-bedroom villa combines modern architecture and Italianate influences. Highlights include formal living and dining rooms, a sunroom, a sunken wet bar, a well-equipped kitchen, and a heated stone terrace with a spa, a built-in grill, burners, an oven, and a beverage refrigerator—all with an ocean view. The primary bedroom is a tranquil getaway boasting a fireplace and a bath with a whirlpool tub, a steamshower, and a therapeutic sauna.

This 5,300-square-foot contemporary home in the Hollywood Hills is an ideal setting for entertaining indoors and out. Its dramatic interiors feature a chef’s kitchen, a spacious media and family room, and walls of glass that open to the refreshing swimming pool and spa, multiple alfresco lounging areas, and an outdoor kitchen with a Viking grill and a pizza oven. Rest and relaxation are assured by the four peaceful bedrooms and a private wood-paneled sauna.

Collin Madden, founding partner of GEM Real Estate Partners, walks through empty office space in a building they own that is up for sale in the South Lake Union neighborhood in Seattle, Washington, May 14, 2021.

Karen Ducey | Reuters

A few things we know about corporate real estate: it’s a focus of cost-cutting for companies, but it’s also probably the last asset you want to sell now in a soft market.

How soft? According to Elizabeth Ptacek, senior director of market analytics at commercial real estate information and analytics company CoStar, there is currently 232 million square feet of surplus commercial real estate up for sub-leasing. To put those numbers into perspective, Amazon’s HQ2 is 8 million square feet. Even more telling, the 232 million square feet is twice the level of surplus from before the pandemic.

CFOs have told us that as their companies go to hybrid work and corporate hub models that make less use, if any use, of satellite offices, there is real estate to be sold. And they aren’t selling it now. Ptacek says that’s the right decision.

The only property owners selling today are either desperate for cash or they are sitting on trophy assets. And those trophy assets are few and far between. Well-leased medical offices and laboratories with high credit score tenants and secure income streams are still attracting plenty of attention from investors, according to CoStar, but that’s about it. Any corporation that has abandoned a satellite office that used to be key for its in-office staff, is sitting on a property that Ptacek says, “no one will buy for anything less than a substantial discount.”

Between the shock to commercial real estate from the remote work trend, followed by the higher interest rates and the prospect of another recession, now is no time to sell even if Ptacek says commercial real estate owners should expect it will get worse yet. CoStar projects that the sub-leasing surplus will persist as companies worry about needing to lay off workers and make other cuts ahead of a recession, and it goes further: the subleasing square footage will never return to the pre-pandemic level, she said.

The slowdown in investment activity that Ptacek described as a gradual slowdown so far, will become a “dramatic slowdown” after the pipeline of deals signed in Q2 and Q3 before rates started to rise are closed. “The bigger impact is ahead of us, and absolutely the higher borrowing cost will have an impact, and in many cases, eliminate the levered investors,” she said.

It’s a bad situation, but she said that for owners of corporate real estate, if the cost of real estate debt is cheap and the balance sheet is solid, sit on the real estate.

With companies still in the early days of their hybrid work experiments, it’s not just economic uncertainty but uncertainty about how in-office occupancy trends over time which should make companies want to hold off pulling the trigger on asset sales. Leases that were up for renewal were an easy call to make (end it), and firms can always sign new leases (likely at even better rates) if and when they need to make that call.

“It’s all still shaking out and you see it, you see the big companies one day fully remote and the next day signing huge leases and telling everyone, ‘Back in the office,’ and then the minute they do employees express consternation and they say, ‘Never mind.’ It’s all very much in flux,” Ptacek said.

Uncertainty is the ultimate deal killer, she said. No one wants to buy assets with the risk of no demand barring rent cuts of 50%. It’s difficult right now, she said, for either buyer or seller to reach what would be defined as a “reasonable price.”

Companies should expect the situation may be even worse a year from now.

“It’s probably a fair assumption that this is not going to be a lot better in a year, in terms of demand,” she said. “There could be another leg down in transactions.”

The wave of distressed sales that usually occur in downturns have not occurred yet, and that is right on schedule, as they tend to lag the start of downturns by a few years. Ptacek noted that after 2008, the peak in the distressed asset sales wave didn’t occur until 2010/2011.

“As loans come due and they have difficulty, it’s refinance or sell,” she said. And more borrowers won’t be able to refinance, and the wave of distressed sales will ensue. “There will likely be some level of distress which will weigh on pricing, so you could as an owner find yourself in a position in a few years where the environment is even less favorable. But it’s not like it’s a good environment today,” she said.

Nick Jones, equity research analyst at JMP securities, joins ‘Power Lunch’ to discuss Opendoor’s warning, the cash needed to navigate near term headwinds and forces needed to normalize the housing market.

A For Sale sign is posted in front of a property in Monterey Park, California on August 16, 2022.

Frederic J. Brown | AFP | Getty Images

After more than two years of a historically lean housing market, listings are starting to rise − and swiftly.

Active inventory nationally jumped 33.5% in October from the same time last year, according to Realtor.com. That puts supply at the highest level in two years.

It’s not that sellers are rushing into the market; newly listed homes dropped 16% from a year ago, and pending listings are down 30%. But supply is growing because the homes that are on the market aren’t selling as fast as they did just six months ago.

The average number of days it takes to sell a home is now 51, up by six days compared with a year ago.

“As the rapid runup in rates reshapes housing market dynamics this fall, both buyers and sellers are taking a step back to recalibrate their plans,” said Danielle Hale, chief economist at Realtor.com.

Mortgage rates have climbed so high and so fast that home shoppers are rushing to the sidelines. Already, affordability was rough with home prices up more than 40% since the start of the Covid-19 pandemic. But with rates now more than twice what they were in January, at just over 7%, potential buyers are looking at a monthly payment that is nearly $1,000 higher than it would have been at the start of the year.

Housing availability varies by city, depending on demand and affordability.

In Phoenix, inventory jumped a striking 174% in October. The city saw a mad rush of buyers over the past two years as employees who could suddenly work from anywhere moved out of pricey markets in California. Now, sales in the city are down more than 30% from a year ago, according to Redfin.

Inventory is also up 167% in Raleigh, North Carolina, and up 145% in Nashville, Tennessee, markets that also saw an influx of buyers during the pandemic. Inventory is still down in Chicago, Milwaukee and Hartford, Connecticut, but those markets did not see the same surge in demand over the last two years.

The slowdown in demand for homes has caused sellers to cut their prices. A full 20% of listings now on Realtor.com have had a price reduction − about twice the share as a year ago.

Still, home prices are not exactly falling yet. The price gains from a year ago are, however, shrinking at the fastest pace on record, according to several surveys.

And with prices still high, more buyers appear to be widening their searches. Just over 60% of listings views on Realtor.com in the third quarter of this year came from shoppers outside of a listing’s area. That’s up from 57% in the second quarter and 52% in the same quarter of 2021.

“For buyers with the flexibility, relocating to a lower-priced market could help offset higher mortgage costs. There’s also a takeaway for sellers in these areas – on a well-priced home, you could still see strong interest from these out-of-towners,” added Hale.

Opinions expressed by Entrepreneur contributors are their own.

Buying a house as an investment or as a place where your family is going to live is as big of a purchase as many people will ever make in their lives. Seattle-based Redfin set out 15 years ago to create a combination tech company and a real estate brokerage to make the industry work better for customers and agents. The technology-powered real-estate company generated $1.9 billion in revenue in 2021 — a 10x increase from 2015. Since launching in 2006, it has saved customers more than $1 billion in commissions. Despite a volatile housing market, it currently boasts 53 million average monthly users on the website and app, serves more than 100 markets across the U.S. and Canada and employs more than 6,000 people.

For my latest episode of Entrepreneur‘s Leadership Lessons series, I had the opportunity to speak with Redfin CEO Glenn Kelman. Before joining the company in 2005, he was a co-founder of Plumtree Software. In his seven years at Plumtree, he at different times led engineering, marketing, product management and business development; he also was responsible for financing and general operations in Plumtree’s early days. Before that, Kelman was one of the first handful of employees at Stanford Technology Group, a startup that was acquired by IBM.

“I started as a web expert, not a real estate expert,” Kelman said during our conversation. “I had no idea how to build such a large organization, but along the way, we’ve learned a lot of valuable lessons. It’s been a wild ride.”

The Seattle-raised leader is one of the most authentic, energetic and unflinchingly honest CEOs I have ever met. He graciously shared 10 valuable leadership lessons with me during our hour-long talk:

1. Business can be a force for good.

Kelman describes himself as an “ex-hippie from UC Berkeley” who thought business was a force of evil as he set out to better the world post-college. How do you improve the world without some kind of business interaction? “That dichotomy made me miserable for the first decade of my professional life,” Kelman admits. But he soon realized that business is only as good or bad as the people who drive it. “An enterprise can give people a common sense of purpose, a sense of belonging and a way to express their ideas and abilities. Most important, we need the industry and commerce of humanity to solve the world’s problems.”

2. Find a support group that knows your value and continually pushes you to realize it.

Kelman’s friends and family never gave up on him. “I was always encouraged and told that if this doesn’t work, I can try something else. It’s never too late to find something you really believe in.”

3. A leader’s path isn’t always in a straight line.

Kelman says he’s thankful for his post-college years of searching for his dream job, including writing a novel and considering a medical career, as these experiences helped develop him into the person he is today.

4. Not everyone has to be Steve Jobs. Just be yourself.

When a friend told Kelman, “You are not Steve Jobs,” he took it as an insult that he wasn’t as brilliant, creative and innovative as his hero. But after taking a step back from the statement, Kelman understood that what his friend really meant was, “Only a genius can be a genius. But any leader can be respectful and kind.”

5. Focus on what customers need and want versus trying to please Wall Street.

Investors have fickle demands. Trying to please Wall Street can tie a leader into knots. The best bet is to tell investors who you are, how you are going to make your customers happy and how that will lead to profitability. “It takes a mature person to be a good leader, because the hardest business problems are often not technical, but rather questions of the soul and heart,” Kelman says.

6. A CEO should love their company more than anyone else.

“If someone was more ambitious for the company, or believed in our mission more than I did, how could I possibly be better qualified than that person to run the company?” Kelman asked me. If self-interest and the biggest paycheck led to you running the company you are running, there will be friction down the line.

7. Don’t let your level of self-esteem ride up and down with the ebb and flow of your finances.

There are always going to be times when war chests are full and other times when cupboards are bare. Your job is to get out of bed and bring the future to life, whatever the current standings.

8. Get enough sleep.

Remembering and tending consistently to the bottom-line fact that you’re a human and that you need things like proper sleep, exercise and time with family and friends will make you the best person you can be and — by extension — the best leader you can be.

9. We all want to be the smartest person in the room, but the best and most valuable trait for a leader is to be humble.

“That’s a skill that’s accessible to all of us,” Kelman says. “It’s one where you can get an ‘A’ for effort. If you let other people flower, you will build a much larger and more successful organization.”

10. A CEO should be the “great exhilarator.”

Writer Robert Louis Stevenson’s wife compared life with him to having lunch on a volcano, but she married him anyway because he was the great exhilarator, Kelman says. “A CEO’s employees will stick with a great leader for the same reason. You can’t be volatile as a CEO, but you can be — and have to be — emotional when the emotions are big and good. You have to make the people you lead feel something big and good.”

For more from my time with Kelman, watch the full webinar here. The growing collection of episodes from our series gives readers access to the best practices of successful CEOs from the biggest brands, including Wayfair, Foot Locker, Heineken, Headspace, Zoom, Chipotle, Warby Parker and ZipRecruiter.

Four acres of beautiful waterfront land in Boca Raton, Florida, is on the market for $43 million.

There’s only one issue—it’s largely underwater.

Image credit: William Swain via The Real Deal

Giving new meaning to the term “underwater mortgage,” real estate manager William Swaim of Waterfront ICW Properties is offering the submerged land for developing single-family homes.

Swaim calls the property a “unicorn” due to its location and relatively inexpensive price tag. The parcel sits along the Intracoastal Waterway, a series of inlets and canals that wealthy residents use to dock their boats and yachts. Home prices in the area have appreciated monthly by more than 10 percent over the past 18 months. A mansion can go for as much as $18 million a pop.

But he also warns that anyone buying the property will have their work cut out for them.

“Submerged parcels are a headache,” Swaim told The Palm Beach Post. “It takes years to clean them up, and most people don’t want to take years to clean them up.”

His company will build a seawall and fill the dirt for an additional $3.5 million.

Why is the property underwater?

Swaim’s land wasn’t always beneath the sea. The property was above ground until 1957, but an apparently greedy neighbor stole the dirt to build a nearby subdivision, Swaim told The Post.

Some local activists are concerned that overdeveloping properties such as these can harm wildlife.

“Manatees are dying at record rates because of impacts to their habitat, and increasing development on submerged lands is only going to compound that problem,” said Everglades Law Center Executive Director Lisa Interlandi.

But a 2018 Army Corps review concluded that developing the land would not adversely affect endangered and threatened sea turtles, smalltooth sawfish, or manatees.