The housing market’s stagnation this year is projected to carry over into 2024. But a forecast published today by Realtor.com identifies metro areas that are poised to see both rising prices and

sales next year, with Toledo, Ohio, leading the way.

Continue reading this article with a Barron’s subscription.

The numbers: U.S. new-home sales fell 5.6% to a seasonally adjusted annual rate of 679,000 in October, from a revised 719,000 in September, the government reported Monday.

Analysts polled by the Wall Street Journal had forecast new-home sales to occur at a seasonally adjusted annual rate of 725,000 in October.

Home prices keep going up, defying mortgage rates at 23-year highs and a housing market that hasn’t been this unaffordable since the 1980s. Everything looks steady on the surface but prolonged national U.S. home price declines could be around the corner for the first time in more than a decade, according to one housing expert.

Continue reading this article with a Barron’s subscription.

The numbers: U.S. pending home sales rebounded in September but remain near a record low as high mortgage rates and low inventory continue to hurt the real-estate sector.

Pending home sales rose 1.1% in September from the previous month, according to the monthly index released Thursday by the National Association of Realtors.

But pending home sales were still depressed on an annual basis due to the dearth of home listings. The September figure was the second-lowest reading since the NAR began tracking the data in 2001.

Transactions were down 11% from last year.

Nonetheless, the sales pace exceeded expectations on Wall Street. Economists were expecting pending home sales to fall 1.5% in September.

Pending home sales reflect transactions where the contract has been signed for the sale of an existing home, but the sale has not yet closed. Economists view it as an indicator of the direction of existing-home sales in subsequent months.

The NAR also released an updated forecast for existing-home sales on Thursday. The group expects sales to fall 17.5% in 2023 to a pace of 4.15 million, which will be the slowest pace since 2008. Yet due to low inventory, the median home price will increase by 0.1% in 2023, the NAR said, to $386,700.

The group expects home sales to rebound in 2024, rising 13.5% to a rate of 4.71 million. Home prices are expected to rise 0.7% next year, to $389,500.

The NAR also expects the 30-year mortgage rate to fall to 6.9% in 2023 and 6.3% in 2024. The 30-year was averaging 7.98% as of Wednesday, according to Mortgage News Daily.

Big picture: The U.S. housing market is dealing with problems on both the demand and supply sides, but the NAR seems confident that the sector will recover in the new year.

At present, not only are rates high enough to discourage home buyers, the lack of inventory is also making homes more expensive, which further spooks buyers. The NAR expects the pace of existing-home sales to fall to the slowest in 15 years, when the U.S. was in the midst of a recession caused by the subprime-lending crisis.

What the realtors said: “Because of home builders’ ability to create more inventory, new-home sales could be higher this year despite increasing mortgage rates,” NAR Chief Economist Lawrence Yun said. “This underscores the importance of increased inventory in helping to get the overall housing market moving.”

The numbers: Home sales in September fell to the lowest level since 2010, as high mortgage rates continue to hammer the housing market.

Aside from low inventory, rising rates are eroding buyers’ purchasing power, and drying up demand. Sales of previously owned homes fell by 2% to an annual rate of 3.96 million in September, the National Association of Realtors said Thursday.

That’s the number of homes that would be sold over an entire year if sales took place at the same rate every month as they did in September. The numbers are seasonally adjusted.

The drop in sales was slightly better than what Wall Street was expecting. They forecasted existing-home sales to total 3.9 million in September.

Compared to September 2022, home sales are down by 15.4%.

Key details: The median price for an existing home in September rose for the third month in a row to $394,300. Prices are up 2.8% from a year ago. That was the highest price for the month of September since NAR began tracking the data.

Home prices peaked in June 2022, when the median price of a resale home hit $413,800.

Around 26% of properties are being sold above list price, the NAR noted.

The total number of homes for sale in September fell by 8.1% from last year, to 1.13 million units. Housing inventory for the month of September was the lowest since 1999, when the NAR began tracking the data.

Homes listed for sale remained on the market for 21 days on average, up from the previous month. Last September, homes were only on the market for 19 days.

Sales of existing homes rose only in the Northeast in September, as compared with the previous month, by 4.2%. The median price of a home in the region was $439,900.

All-cash buyers made up 29% of sales, highest since January 2023. The share of individual investors or second-home buyers was 18%. About 27% of homes were sold to first-time home buyers.

Big picture: The U.S. housing market is in the midst of a serious slowdown that is primarily driven by high mortgage rates. High rates spook home buyers, drying up demand, and high rates also deter homeowners from selling since they may have to purchase another home. For a homeowner with a 3% mortgage rate for the next few decades, there’s little incentive to move.

And the residential sector is likely to see sales fall further in October’s data, as the 30-year mortgage inches even higher. Demand for mortgages has collapsed, and some outlets like Mortgage News Daily are quoting a rate of 8% for the 30-year.

Existing-home sales in 2023 could fall to the slowest pace since the housing bubble burst in 2008, real-estate brokerage Redfin said on Thursday, at a 4.1 million pace.

What the realtors said: “Mortgage rates and limited inventory has been the story throughout this year — no different this month, other than the fact that interest rates are moving higher,” said Lawrence Yun, chief economist at the National Association of Realtors.

“The Federal Reserve simply cannot keep raising interest rates in light of softening inflation and weakening job gains,” he added. “We don’t want the Fed to overdo it and cause great harm to real estate.”

Yun also questioned whether there will be a “fundamental change” or a temporary one to the “American way of life” due to the slowdown in sales.

Market reaction: Stocks were down in early trading on Thursday. The yield on the 10-year note BX:TMUBMUSD10Y

rose above 4.9%.

KB Home shares declined in the extended session Wednesday even after the home builder reported results that topped Wall Street estimates, hiked its revenue forecast for the year and reported steady demand amid rising mortgage rates.

KB Home KBH shares slid more than 2% after hours, following a 0.7% decline in the regular session to close at $48.06.

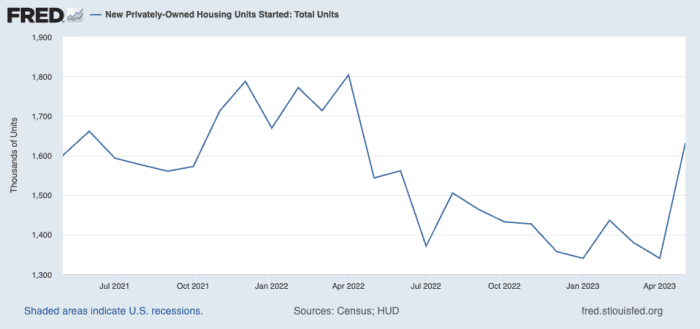

The numbers: Construction of new U.S. homes fell 11.3% in August — falling short of Wall Street expectations — as builders scaled back new projects to focus on completions.

The pace of construction reversed course and fell as mortgage rates stayed over 7%, dampening home-buying demand. The last time construction of new homes was at this level was in June 2020.

So-called housing starts fell to a 1.28 million annual pace from 1.45 million in August, the government said Tuesday. That’s how many houses would be built over an entire year if construction took place at the same rate every month as it did in August.

Economists on Wall Street were expecting a drop in starts to 1.43 million. All numbers are seasonally adjusted.

Housing starts peaked at 1.8 million in April 2022.

The number of homes started in July was revised downwards, to an increase of 2% to 1.45 million, from an initial reading of a 3.9% gain.

New homes have dominated the housing market, but persistently high rates are beginning to spook home builders. In anticipation of waning demand, builders said they’ve started to ramp up price cuts to boost buyer demand in September, according to a survey by the National Association of Home Builders.

Building permits, a sign of future construction, rose 6.9% to a 1.54 million rate. That’s the highest level since October 2022.

Key details: The construction pace of single-family homes fell by 4.3% in August, and apartment-building construction fell by 26.3%.

But home builders ramped up single-family home construction in the South, where starts rose by 8.1% in August.

Housing starts fell the most in the West, by 28.9%.

Permits for single-family homes rose 2% in August, while permits for buildings with at least five units or more surged by 14.8%.

Around 1.69 million homes were under construction as of August.

Big picture: Builders are increasingly concerned about how 7% rates will impact demand, and they’re pulling back on starting new developments as a result.

Builder confidence in September fell to the lowest level in five months, according to the NAHB. Home builders are increasingly offering incentives, including cutting prices. The share of builders cutting prices to boost sales rose to the highest level in nine months, the NAHB noted, going up to 32% in September from 25% the previous month.

Nonetheless, given the long-term need for housing and a decade of underbuilding, builders may not see a sustained drop in demand.

What are they saying? Despite starts falling sharply in August, the uptick in building permits “suggests housing starts could pick up modestly again and today’s data could reflect some volatility,” CIBC Economics said in a note. “Nonetheless, the cooling in building activity is a good sign for the Fed which is expecting to limit housing market activity in an effort to contain inflation.”

Rates have peaked, but “will remain elevated for the rest of the year,” Capital Economics wrote in a note. And this means that with “a slowing economy, we expect this will lead single-family starts to flatten-off at around 900,000 annualised until mid-2024, after which an economic recovery will help spur buyer demand and supporting renewed homebuilder confidence,” they added.

The Federal Reserve’s inflation fight has been particularly brutal for anyone not already a U.S. homeowner before interest rates and mortgage rates rose to 15-year highs.

With mortgage rates around 7.2% to kick off the post–Labor Day period, the difference between the rates on a new 30-year home loan and on all outstanding U.S. mortgage debt (see chart) has not been so wide since the 1980s.

It’s the 1980s again in the U.S. housing market.

Glenmede, FactSet

“Generally, climbing interest rates curb demand and cause housing prices to fall,” Glenmede’s investment strategy team wrote, in a Tuesday client note, but not this time.

Instead, U.S. homes remain in critically low supply after more than a decade of underbuilding, and with most homeowners who already refinanced at low pre-pandemic rates being “reluctant to leave their homes,” wrote Jason Pride, chief of investment strategy and research, and his Glenmede team.

“Until the supply gap is filled by new construction, home prices and building activity are unlikely to decline as meaningfully as they normally would given the headwind from rising rates,” the Glenmede team said.

The Glenmede team, however, does expect more pressure on consumers in the coming months, particularly as student-loan payments resume in October and if the Fed keeps interest rates high for a while, as increasingly expected. The benchmark 10-year Treasury yield BX:TMUBMUSD10Y,

which underpins the U.S. economy, was back on the climb at 4.26% Tuesday.

Meanwhile, shares of home-vacation rental platform Airbnb Inc. ABNB, +7.23%

rose 7.2% on Tuesday, after the Labor Day weekend, and 66.4% higher on the year so far, according to FactSet.

Shares of Invitation Homes Inc. INVH, -0.91%,

which grew out of the last decade’s home-loan foreclosure crisis to become a single-family-rental giant, were up 14.3% on the year, according to FactSet.

Dallas Tanner, CEO of Invitation Homes, said he expected “the rising costs and the burden of homeownership” to continue to benefit his company, in a July earnings call. The company recently bought a portfolio of about 1,900 homes and has been snapping up newly constructed homes. Companies can borrow on Wall Street at much lower rates than individuals.

Stocks closed lower Tuesday, with the Dow Jones Industrial Average DJIA

off 0.5%, and the S&P 500 index SPX

0.4% lower and the Nasdaq Composite Index COMP

down 0.1%, according to FactSet.

Chinese regulators eased the nation’s mortgage requirements to let more home buyers enjoy favorable mortgage conditions that were previously limited to first-time home purchasers, the state-run Xinhua News Agency said on Friday.

China’s central bank, the Ministry of Housing and Urban-Rural Development and the National Financial Regulatory Administration jointly eased the requirements for home buyers who have already purchased homes to boost property sales as the real-estate slump continued, according to Xinhua.

Home buyers who don’t have family members with houses registered under their names can enjoy favorable terms that were previously limited to people buying their first homes, according to Xinhua.

First-home buyers are normally given cheaper mortgage rates than other buyers who have at least one apartment. First-home buyers are also required to make smaller down payments, as low as 20% of the total property value.

Write to Singapore editors at singaporeeditors@dowjones.com

The numbers: Mortgage rates rose for the fourth week in a row to the highest level since 2000, as the economy continues to show strength.

Rates surged as the U.S. economy continued to show signs of resilience, which signal to the market that the U.S. Federal Reserve may not be done with rate increases.

The 30-year was averaging at 7.31%, which in part dampened demand for home-purchase mortgages to the lowest level since April 1995.

Demand for both purchases and refinancing fell. That overall pushed down the market composite index, a measure of mortgage application volume, the Mortgage Bankers Association (M.B.A.) said on Wednesday.

The market index fell 4.2% to 184.8 for the week that ended Aug. 18, relative to a week earlier. A year ago, the index stood at 270.1.

Key details: High mortgage rates are weighing on home buyers’ budgets due to an increase in borrowing costs. Many buyers fled the market as a result of rates rising over the last week. The purchase index, which measures mortgage applications for the purchase of a home, fell 5% from last week.

Rates hold little allure for homeowners hoping to refinance. The refinance index fell 2.8%.

Rates rose across the board.

The average contract rate for the 30-year mortgage for homes sold for $726,200 or less was 7.31% for the week ending August 18. That’s up from 7.16% the week before, the M.B.A. said. The 30-year is at the highest level since December 2000.

The rate for jumbo loans, or the 30-year mortgage for homes sold for over $726,200, was 7.27%, up from 7.11% the previous week.

The average rate for a 30-year mortgage backed by the Federal Housing Administration rose to 7.09% from 6.93%.

The 15-year rose to 6.72%, up from last week’s 6.57%.

The rate for adjustable-rate mortgages rose to 6.5% from last week’s 6.2%. The share of adjustable-rate mortgages rose to 7.6%, the highest level in five months.

The big picture: The housing market continues to be hammered by good economic news, which is pushing rates up and depressing home sales. Higher rates also discourage homeowners from selling, as their purchasing power erodes when they look for homes to buy.

As a result, both home-buying demand and supply of home listings continues to fall, bringing the market to a standstill. Until the economy shows signs of slowing, it’s likely that the housing market will remain in the doldrums.

What the M.B.A. said: “Applications for home purchase mortgages dropped to their lowest level since April 1995, as home buyers withdrew from the market due to the elevated rate environment and the erosion of purchasing power,” Joel Kan, deputy chief economist and vice president at the M.B.A., said in a statement.

Kan added that there was an uptick in people using adjustable-rate mortgages. “Some home buyers are looking to lower their monthly payments by accepting some interest rate risk after the initial fixed period,” he said.

Market reaction: The yield on the 10-year Treasury note BX:TMUBMUSD10Y

was above 4.3% in early morning trading Wednesday.

The average house price in the U.K. fell 1.9%, or 7,012 pounds ($8,938) in the month to August 12–the biggest fall in asking prices in a month since 2018–according to new data from Rightmove released on Monday.

The average price of property coming to the market fell on month to GBP364,895, outpacing the usual summer slowdown of a drop of 0.9% for the month, the online property portal said. On an annual basis, house prices fell 0.1%, swinging from growth of 0.5% in July.

This bigger-than-average dip indicates some sellers are taking the initiative to price competitively, and tempt buyers that might be more preoccupied with holidays, inflation and the highest interest rates since 2008, Rightmove said.

“While a 1.9% drop in just one month seems dramatic, it’s in part an expected seasonal drop as sellers coming to market realise that they have to compromise on price due to the traditionally quieter summer holiday period,” Rightmove property-science director Tim Bannister said.

First-time buyer asking prices slipped 0.9% on month to GBP223,614, and were down 0.2% on year. Second-stepper prices fell 0.8% on month to GBP338,137, while top-of-the-ladder homes fell furthest, slipping 3.4% to GBP664,756.

Agreed sales were 15% behind levels seen in the more normal, prepandemic year of 2019, worse than the month before which was 12% below 2019’s figure. First-time buyer demand, however, is holding up better and is down just 10% compared with 2019, partly due to record rents and scarce rental properties.

“The lower level of agreed sales compared to this time in 2019 indicates the affordability challenges that many buyers currently face. However, with sales holding up more strongly in the typical first-time buyer sector, the prospect [of] owning your own home remains an appealing option for those that can afford it, with the alternative being an extremely frenzied rental market, where rents are at record levels,” Bannister said.

The portal measured 123,692 prices across the U.K. over the period of July 9 to Aug. 12.

The majority of second-quarter earnings season is over, with a handful of major technology and retail names left to report this week. Economists will be focused on any news from an annual gathering of monetary policy thinkers and practitioners in Jackson Hole, Wyoming.

The numbers: Home sales inched up for the first time in four months, even as the U.S. housing market continues to deal with a dearth of listings.

Pending home sales rose by 0.3% in June from the previous month, according to the monthly index released Thursday by the National Association of Realtors.

The figure exceeded expectations on Wall Street. Economists were expecting pending home sales to fall 0.5% in June.

Transactions were still down 15.6% from last year.

Pending home sales reflect transactions where a contract has been signed for the sale of an existing home but the sale has not yet closed. Economists view it as an indicator of the direction of existing-home sales in subsequent months.

Big picture: Home sales rose as the housing market contends with excess buyer demand and a shortfall in the supply of homes for sale.

What the real-estate experts said: “The recovery has not taken place, but the housing recession is over,” NAR chief economist Lawrence Yun said. “The presence of multiple offers implies that housing demand is not being satisfied due to lack of supply.”

The NAR also said it expects rates for 30-year mortgages to average 6.4% this year and to fall to 6% in 2024.

The NAR also expects existing-home sales to fall 12.9% in 2023 from the previous year, to 4.38 million, before recovering in 2024 to a rate of 5.06 million.

The group also expects home prices to hold steady this year, falling only slightly by 0.4% to $384,900, before rising 2.6% next year to $395,000.

“The West — the country’s most expensive region — will see reduced prices, while the more affordable Midwest region is likely to see a small positive increase,” Yun added.

The housing market may feel out of whack to home buyers coping with fast-rising home prices and 7% mortgage rates. But like it or not, the housing market is in the pink of health.

Several economic indicators that measure housing activity — from home prices to sentiment surveys — show that home builders and sellers (the few that are out there) are finding strong demand from home buyers.

News of the housing market’s relative health may be welcome to some — like real-estate agents and investors — but it’s becoming a concern for economists. The more buoyant the housing market, economists say, the more likely the U.S. Federal Reserve will unveil another interest-rate hike, which further heightens the risk of a recession.

“‘The housing market has started to recover, and this is a problem for the Fed because more demand for housing will boost home prices and rents.’”

— Torsten Slok, chief economist at Apollo

“The housing market has started to recover, and this is a problem for the Fed because more demand for housing will boost home prices and rents,” Torsten Slok, chief economist at Apollo, wrote in a note in May. And housing is a big part of how the government measures inflation, he added. This will make it more difficult to reduce inflation from 5% to the Fed’s 2% inflation target, he said.

If the Fed launches another rate hike, it would push mortgage rates, which are already in the 7% range, to go even higher.

“The housing market is in a very — if fragile — recovery,” Mike Simonsen, founder and president of real-estate analytics firm Altos Research, told MarketWatch.

“There appears to be more demand than available supply for homes, especially in the real-estate market,” he explained, which is keeping home prices high, but that doesn’t mean demand could evaporate if the current situation changes. Recall when rates doubled from pandemic-era lows in 2021 to 7% last year, which zapped home-buying momentum.

House hunters have adjusted their expectations. But if rates were to jump from 7% today to even higher levels, “I would not be at all surprised if homebuyers stopped abruptly again,” Simonsen said, stating his thesis for the fragility of the sector. Americans broadly expect rates to go over 8%, according to a March survey by the New York Federal Reserve.

MarketWatch looked at three housing-market indicators — and the picture looks rosier than ever:

Active listings are down — blame interest rates

Redfin’s deputy chief economist, Taylor Marr, said his go-to indicator was active listings.

Active listings are down this spring, compared to the previous year, according to the company’s data. At the end of June, the number of homes listed for sale on the market was down 8.1% over the prior year.

“It really captures that supply is pulling back significantly relative to demand,” Marr said.

Redfin data says that active listings of homes are down.

As a result, the housing market is seeing an excess of demand and not enough supply, which has led to a resurgence of bidding wars in some parts of the U.S.

While this metric is showing signs of the housing market returning to life and heating up amid a shortage of houses for sale, Marr said he’s not yet ready to call it a recovery. “It’s hard to declare completely the bottom of the housing market,” he said.

Still battle-scarred by the housing crash of the Great Recession, Marr said economists “might be hesitant” to say that the housing market is in recovery mode. “We still have a lot of uncertainty with the economy ahead,” he added. “If the economy really takes a turn three or four months from now for whatever reason, it could certainly bring the housing market back lower than it was even last November,” he added.

The price gap between new and existing homes

With a major shortage of resale homes, new-home sales have been taking off.

Home builders, understandably, are thrilled about the inventory shortage.

The National Association of Home Builders measures builders’ sentiment in a monthly index, and that indicator has been very cheery of late. In June, the index turned positive for the first time in nearly a year. Builders were scaling back price reductions; they were happy about current sales conditions as well as sales over the next six months, the NAHB said.

“A bottom is forming for single-family home building as builder sentiment continues to gradually rise from the beginning of the year,” said Rob Dietz, chief economist of the NAHB.

One of the major U.S. home builders, Lennar, also offered some commentary on its second-quarter earnings call last month. The company’s executive chairman, Stuart Miller, said that “the market and the economy will remain constructive for home builders as pent-up demand continues to come to market and consume affordable offerings.”

Miller also doesn’t expect the supply issue to be fixed anytime soon: “We believe that the supply constraint will continue to limit available inventory and maintain supply-demand balance,” he said on the call. “The core elements of the supply shortage will not resolve in the near term as the almost 15-year production deficit will take years to resolve.”

Home-builder confidence, as a result, is signaling high optimism about the future of the housing market, and a return to normalcy.

Builders have ramped up building new single-family and multi-family homes.

Ali Wolf, chief economist at Zonda, looks at how prices of new homes trend relative to resale homes as a key indicator of the health of the housing market. Her conclusion? Housing industry professionals involved in the construction and sale of new homes are out of a recession, given the robust demand.

In fact, demand has been so strong that new homes — generally considered to be more expensive than resales — have become more affordable in home buyers’ eyes given the competition in the existing home space.

Typically, new homes are 20% more expensive than resales, Wolf said. And today? That spread has fallen to 4%.

So what’s going on? Builders are not necessarily slashing prices. Instead, existing home prices have risen as homeowners are reluctant to sell.

That’s a good deal for buyers. New homes, Wolf said, are traditionally considered a “luxury good.” They’re brand new, and buyers can often customize them. They also require less maintenance than older homes.

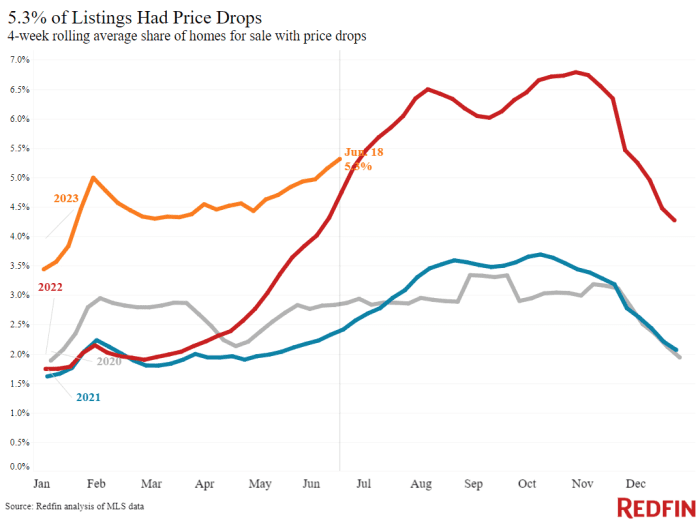

Sellers are holding out on cutting prices

Simonsen, who leads Altos Research, said price cuts were his go-to indicator to gauge the health of the real-estate market. Specifically, price cuts formed a proxy for demand, he explained.

“When the houses are on the market, if there are no buyers for the current houses that are listed, people start taking price cuts,” Simonsen said.

And to be clear, price cuts jumped last year, when rates jumped, he added.

But that dynamic has since changed, as seen in the chart below. “There are currently fewer price reductions now than in 2018 or 2019,” Simonsen said.

Data from Redfin says that homeowners aren’t cutting prices on their homes when selling, possibly due to strong interest from buyers.

And for those of you holding out for home prices to crash? Keep waiting, Simonsen said.

“There’s nothing in the data that shows prices crash,” he said. Even if a recession hits at the end of the year, which results in more job layoffs, demand for home-buying falling, and an increase in foreclosures and distress, that’s still a few years from now, he added.

“There’s no signal of home prices crashing anywhere,” Simonsen added.

If you’re a retiree and you’re trying to square the circle of rising costs, longer lifespans, more expensive medical care and turbulent markets, don’t be afraid to run the numbers on your biggest investment.

That would be your home — if you own it.

U.S. house prices are now so high that it is almost impossible for seniors not to ask themselves the obvious question: “Should we cash in, invest the money, and rent?”

Right now the average U.S. house price is nearly $360,000. That’s about a third higher than just a few years ago, before the COVID-19 pandemic. The lockdowns, the panic, the stimulus checks and 2.5% mortgage rates have all passed into history. But the sky-high prices remain — for now.

After several years of double-digit percentage increases, apartment-rent growth is falling for only the second time since the 2008 financial crisis. WSJ’s Will Parker joins host J.R. Whalen to discuss.

There is a similar story for seniors. Federal data show that the average U.S. house price is now nearly 17 times the average annual Social Security benefit — an even higher ratio than it was in August 2008, just before Lehman Brothers collapsed. At that juncture, the average house price was 15 times higher.

U.S. National Home Price Index vs. average rent of primary residence in U.S. city, according to the U.S. Bureau of Labor Statistics. Indexed: January 1987=100.

S&P/Case-Shiller

Our simple chart, above, compares average U.S. home prices with average U.S. rents, going back to 1987. (The chart simply shows the ratio, indexed to 100.) The bottom line? House prices are very high at the moment compared with rents — again, prices are about where they were in 2006-07.

And the two must run in tandem over the long term, because the economic value of owning a house is not having to pay rent to live there.

If there are times when, in general, it makes more financial sense for seniors to rent than to own, this has to be one of those.

Seniors who own their own homes may think high interest rates on new mortgages don’t affect them. They most likely either already have a mortgage at a lower, older rate or they’ve paid off their home loan. But if you want to sell, you’ll almost certainly be selling to someone who needs a mortgage.

If borrowing costs drive down real-estate prices, seniors who hold off on selling may miss out on gains they may never see again. After the last housing peak, in 2006, it took a full decade for prices to recover fully. Those who sold when the going was good had the chance to buy lifetime annuities at excellent rates or to invest in stocks and bonds that overall rose about 80% over the same period.

Incidentally, there is also an exchange-traded fund that invests in residential REITs, Armada’s Residential REIT ETF HAUS, -0.53%,

though in addition to single-family homes and apartment-complex operators, about 25% of the fund is invested in companies involved in manufactured-home parks and senior-living facilities.

For each person, the math will be different, and there are a number of questions you need to ask. Where do you want to live? How much would you get if you sold your house? How much would you pay in taxes? How much would it cost to rent the right place? Do you want to leave a property to your heirs? And what would be the costs of moving — both financial and emotional?

The conventional wisdom is that you should own your home in retirement.

“I would advise any and all retirees against renting if at all possible,” says Malcolm Ethridge, a financial planner at CIC Wealth in Rockville, Md. “You need your costs to be as fixed as possible during retirement, to match your income being fixed as well. If you choose to rent, you’re leaving it up to your landlord to determine whether and by how much your No. 1 expense will increase each year. And that makes it very tough to determine how much you are able to allocate toward everything else in your budget for the month.”

A key point here, from federal data, is that nationwide rents have risen year after year, almost without a break, at least since the early 1980s. They even rose during the global financial crisis, with just one 12-month period where they fell — and then by only 0.1%.

“My general advice for clients is that owning a home with no mortgage in retirement is the best scenario, as housing is typically the highest cost we pay monthly,” says Adam Wojtkowski, an adviser at Copper Beech Wealth Management in Mansfield, Mass. “It’s not always the case that it works out this way, but if you can enter retirement with no mortgage, it makes it a lot easier for everything to fall into place, so to speak, when it comes to retirement-income planning.”

“Renting comes with a lot of risk,” says Brian Schmehil, a planner with the Mather Group in Chicago. “If you rent, you are subject to the whims of your landlord, and a high inflationary environment could put pressure on your finances as you get older.”

But it’s not always that simple.

“With housing costs as high as they are now though, renting may be a viable solution, at least for the moment,” says Wojtkowski. “We don’t know what the housing-market trends will be going forward, but if someone is waiting for a housing-market crash before they move, they could very likely be waiting for a long time. We just don’t know.”

“Any decision comes with pros and cons,” says Schmehil. “Selling when your home values are historically high and renting allows you to capture the equity in your home, which is usually a retiree’s largest or second-largest financial asset. These extra funds allow you to spend more money on yourself in retirement without having to worry about doing a reverse mortgage or selling later in retirement, when it may be harder for you to do so.”

Renting also allows you to be more flexible about where you live, for example nearer your children or grandchildren, he adds.

And as any experienced property owner knows, renting also brings another benefit: You no longer have to do as much work around the house.

“Renting is great in that you don’t need to maintain a residence,” says Ann Covington Alsina, a financial planner running her own firm in Annapolis, Md. “If the dishwasher breaks or the roof leaks, the landlord is responsible.”

Wojtkowski agrees, noting that many people no longer want to spend time mowing the lawn or shoveling snow in retirement. “Ultimately, one of the things that I’ve seen most retirees most concerned with is eliminating the general upkeep [and] maintenance of homeownership in retirement,” he says.

Several planners — including Covington Alsina and Wojtkowski — note that one alternative to selling and renting is simply downsizing. This can free up capital, especially when home prices are high, like now, without leaving you exposed to rising rents.

Many baby boomers have been doing exactly that.

Meanwhile, I am reminded of my late friend Vincent Nobile, who — after a long and fruitful life owning homes and raising a family — found himself widowed and alone in his 80s. He rented a small cottage on a New England sound and said how glad he was that he never had to worry about maintaining the roof or the appliances, or fixing the plumbing or the heating, or any one of a thousand other irritations. Or paying property taxes — which go down even more rarely than rents.

When the regular drives to Boston got too onerous, he moved into the city and rented there. And he was glad to do it. The money he had made was all in investments — a lot less hassle both for him and his heirs.

I once asked him if he would prefer to own his own home. He shook his head and laughed.

The construction industry posted a slight gain in May as companies and the government increased spending on projects across the U.S.

Spending on construction projects rose 0.9% in May to $1.93 trillion, the Commerce Department reported Monday.

Wall Street was expecting construction spending to rise 0.5% in April.

Construction spending reveals how much the government and private companies spend on projects, from housing to highways. The more the U.S. spends on construction, the higher the level of economic activity.

The government revised spending on construction in April to 0.4% from an initial read of a 1.2% increase.

Over the past year, construction spending was up 2.4%.

In terms of residential real estate, private residential construction fell 11.6% in May as compared to the previous year. It was up 2.2% as compared to April.

Single-family construction rose on a month-over-month basis in May by 1.7%, but fell sharply by 25% from last year.

Multifamily construction fell by 0.1% in May, but increased by 20.4% from last year.

Spending on public residential construction rose by 0.1% from last month, and 12.3% from last year. The U.S. increased spending on public residential construction by 1.1% from last month, and 8.3% over the last year.

The increase in spending May overall was “strong,” Stephen Stanley, chief U.S. economist at Santander U.S. Capital Markets, wrote in a note.

“In particular, new residential activity jumped by 2.2%, reversing the cumulative declines recorded over the three prior months,” he added. “This lines up with the big increase in housing starts in May and adds to the growing body of evidence that the housing sector is bottoming out.”

The numbers: Construction on new American homes jumped 21.7% in May, as homebuilders ramp up building single-family homes to meet strong demand from buyers.

Housing starts rose to a 1.63 million annual pace last month from 1.34 million in April, the government said Tuesday. That’s how many houses would be built over an entire year if construction took place at the same rate in every month as it did in May.

Economists were expecting a slight decline of about 0.8%. The numbers are seasonally adjusted.

This is the second month in a row that starts are up. The pace of construction was the highest since last April, when starts hit a 1.8 million pace.

The surge in construction this spring was led by the Midwest.

Both single and multi-family construction rose in May. Keen interest from would-be home buyers is creating strong demand for new homes. These buyers continue to face a lack of options in the resale market.

Building permits, a sign of future construction, rose 5.2% to a 1.49 million rate.

Key details: As the weather warms up, construction pace has picked up considerably.

The construction pace of single-family homes rose 18.5% in May while apartment building rose 28.1%.

Home builders were most active in the Midwest, where housing starts rose by 67% from the previous month. The Midwest also led the nation in terms of single-family construction.

Permits for single-family homes rose 5.2% in May while permits in buildings with at five units or more rose 7.8%.

Housing starts are up on an annual basis for the first time in nearly a year. The annual rate of total housing starts rose 5.7% from last May.

Big picture: New construction is a bright spot in an otherwise despondent housing market. For the buyers who brave 6% mortgage rates, there are few options in the resale market, which continues to funnel demand for new homes.

Builders also reported that they were feeling upbeat about the housing market for the first time in nearly a year.

What are they saying? “To say that we did not see this one coming would not even come close to capturing the degree to which the May residential construction data caught us off guard,” Richard Moody, senior vice president and chief economist at Regions Financial Corporation, wrote in a note.

“This is without question an exaggeration of the underlying reality and a reminder that the housing starts data are among the most volatile and random of the government’s major economic indicators,” Stephen Stanley, chief U.S. economist at Santander U.S. Capital Markets, wrote in a note.

“Having said that,” he added, “the housing sector broadly appears to be healing remarkably fast after enduring a historic shock in affordability last year, when 30-year mortgage rates more than doubled.”