Hashrate Index has released its 2022 Bitcoin Mining Year In Review, an extensive report on the mining industry and markets surrounding it.

2022 was a difficult year for Bitcoin mining, with the bear market leading to a hashprice all-time low, bankruptcies and losses for miners. Despite this, hash rate still grew 41%, and Bitcoin mining still generated nearly double the rewards compared to the previous three years. The report covers all of these topics and more in detail.

One of the main focuses of the report is the growth of hash rate.

Bitcoin hash rate 2022 vs. 2021 — Source: Hashrate Index

Although the year involved many challenges to the mining industry, from an all-time low hashprice, to several public miner bankruptcies and even an arctic cyclone at the end of the year to top things off, hash rate still climbed, and at a much greater rate than 2021, which was stunted by China’s mining ban.

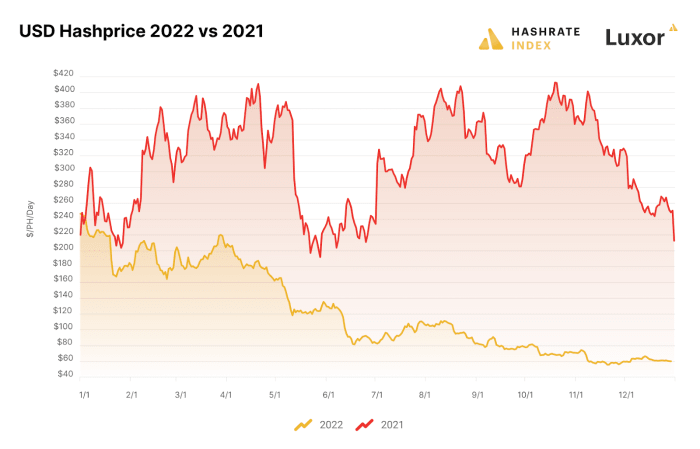

The report also describes a large decline in hashprice, with the high of the year being recorded on January 1 at $246.86/PH/day and only declining from there. Indeed, the year saw an all-time low in hashprice at $55.94/PH/day.

Bitcoin USD hashprice 2022 vs. 2021 — Source: Hashrate Index

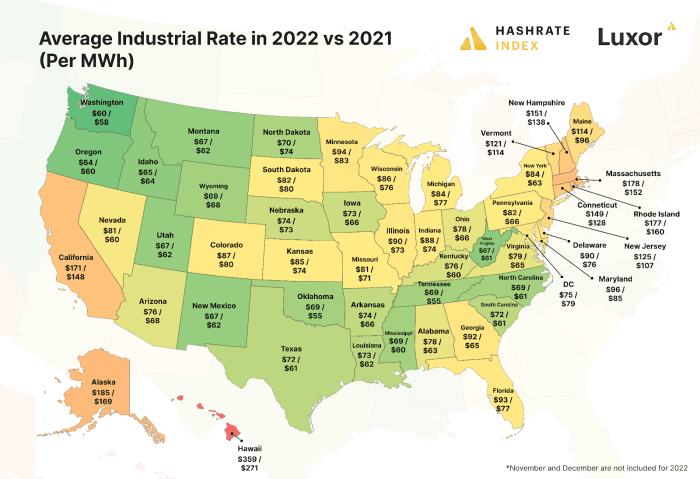

One factor that played into this, according to the report, is increasing industrial electricity rates across the country. But many states have been insulated from this rise in cost through abundant energy production sources like Washington’s hydropower, or other states’ access to natural gas, leading to certain states retaining viable mining operations. The report also notes that “power strategies can take many forms, but a common theme is that miners exploit the unique low-consequence-interruptibility of the bitcoin mining process by adjusting their electricity consumption based on market signals.” This was on display most recently when Texas miners turned off their operations in order to return energy supply to the grid, while getting paid nearly as much as they would have had they continued mining.

Average U.S. industrial power rate 2022 vs. 2021 — Source: EIA.gov

Hashrate Index also highlighted the increase in hosting costs, which prior to 2022, hovered around $0.05-$0.06/kWh. But now, “Anything below $0.075/kWh is considered “a steal” given market conditions.”

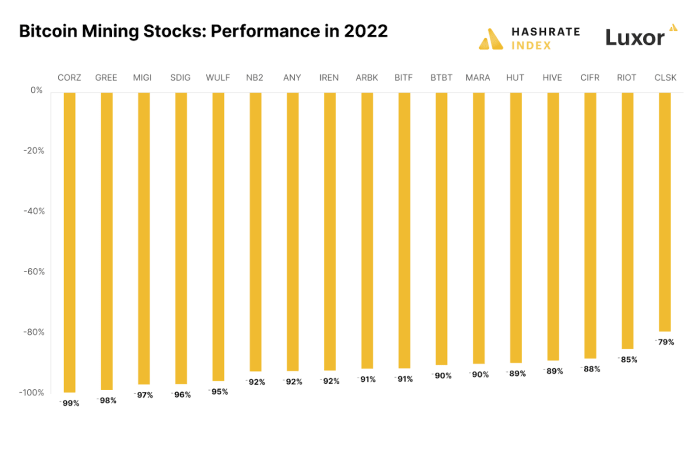

Suffering public miners were also a focal point in the analysis.

Bitcoin mining stock performances in 2022 — Source: TradingView

With the bull market in full swing, public bitcoin miners made big bets with their equipment purchases and expansionary moves. But the bear market hit some larger performers particularly hard, with behemoths like Core Scientific taking losses of nearly 100% — the company is currently undergoing Chapter 11 bankruptcy procedures. These were difficult-to-swallow pills for the market, but public miners did expand in terms of their hash rate dominance, ending the year at 19%.

Overall, the report signified Bitcoin’s resilience in the face of various major headwinds. Macroeconomic pressures, environmental anomalies and major public mining stocks tumbling more than 90% still couldn’t hamper major growth in network hash rate. Apparently, even such horrendous extraneous conditions as those on display in 2022 cannot temper the growth of the Bitcoin mining industry.

Cleanspark, a publicly traded bitcoin miner based in Las Vegas, Nevada, has announced their December 2022 bitcoin mining update, in addition to comments from the CEO reflecting on 2022.

“Among our many accomplishments this year, I’m most proud of increasing our annual bitcoin production by over 200% as we expanded our fleet and the number of mining campuses we own and operate throughout Georgia,” said Zach Bradford, CEO, in the release. “Even in this down market, we are committed to the promise of bitcoin and are proud to be part of the global network that keeps it secure for millions of users across the world.”

The company mined a total of 464 bitcoin in the month of December, to conclude 2022 with a total of 4,621 bitcoin mined. As of December 31, the company held 228 bitcoin while it sold 517 bitcoin in December for operations and growth.

Like other public miners this year, Cleanspark has faced a dramatic downturn in its stock price, just as the price of bitcoin fell similarly. Despite this, when priced in bitcoin, Cleanspark has maintained a relatively steady valuation, and has continued to expand its operations.

In September, mining expert Zack Voell detailed how the energy company turned miner is continuing to grow despite the various headwinds currently present in the bitcoin market. This continued with ASIC acquisitions in the following months, as well as record production of bitcoin in October.

The December report also detailed the company’s operational reactions to the winter storm which ravaged the United States that month, describing how 98% of its machines present in Georgia were powered down due to the conditions. The machines were turned back on as soon as the temperature and humidity levels permitted.

Core Scientific’s lender, B Riley, has stated its intentions of loaning out $72 million to the embattled publicly traded miner. Core Scientific currently has an existing loan with B Riley totaling $42 million. The new $72 million loan would be “on favorable terms,” and aim to provide two years of runway before anticipating profitability from the company.

In the lender’s released statement it described how, “We believe that there is a path forward and have been proactive in working through a solution, specifically by providing debt on a number of unencumbered assets.”

The mining firm has faced various headwinds in recent months. Bitcoin Magazine PRO detailed these back in late October of this year, describing how “Core Scientific is halting all debt service payments; Bitcoin holdings are now 24 — they sold 1,027 over the last month; Cash resources will be depleted by the end of the year or sooner; and Core Scientific claims Celsius owes them $5.4 million.”

In addition to these, last week a lawsuit was filed by Kirby McInerne LLP on behalf of Core Scientific investors.

Despite this and statements by the mining firm that bankruptcy was not off the table, B Riley states that they believe “bankruptcy is not necessary at all.”

The lender explains that the miner’s previous loans “were made when the price of Bitcoin was significantly higher than it is today and the theoretical payoff on miners was significantly faster. These debts were incurred as part of an aggressive, ill-conceived strategy by the Company to continue to build out power facilities and expand miners while never selling Bitcoin on hand and never hedging prices … This decision combined with the fast maturity associated with mining has led the Company to its current position.”

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

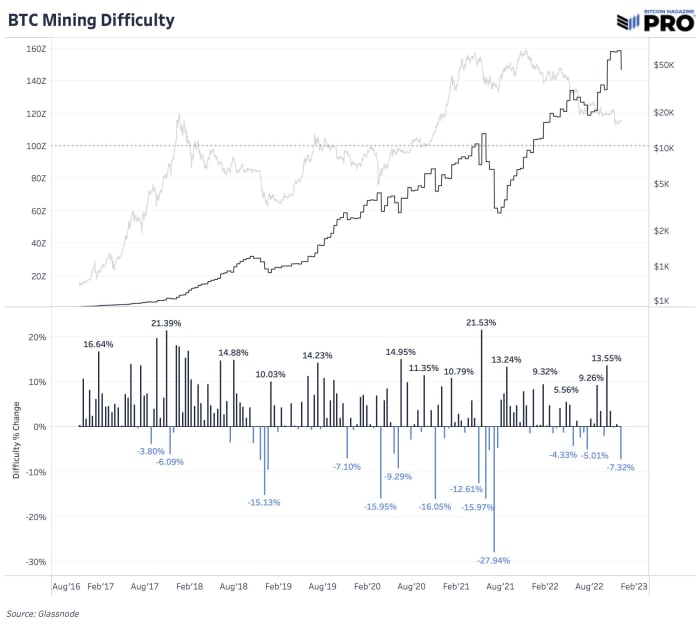

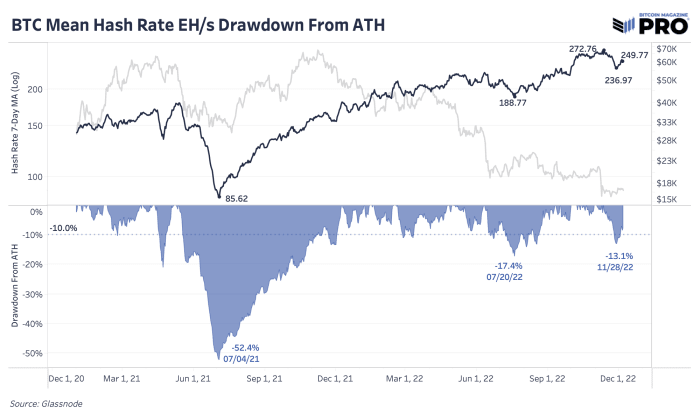

Record Downward Difficulty Adjustment

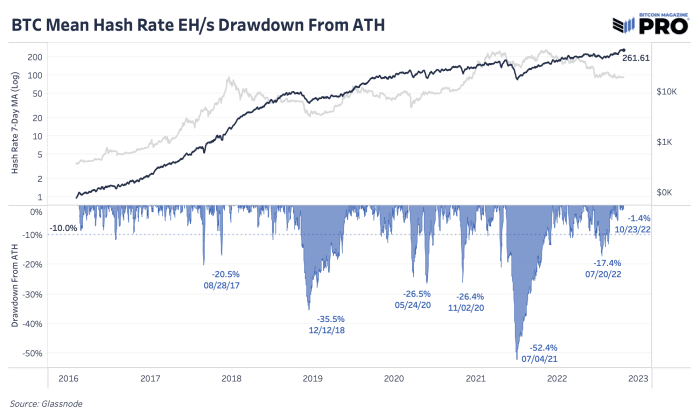

The mining industry continues to take a beating as rising energy inflation, debt burdens and depressed bitcoin prices take their toll. At the end of November, we saw a 13.1% decline in hash rate from all-time highs. However, of the major hash rate declines since 2016, that’s still relatively small compared to the handful of down periods over 15% during that time.

The latest 7.32% downward difficulty adjustment is a direct response to all of that hash rate going offline. As we stand today, the hash rate is right around 250 EH/s and down 7.84% from its all-time high of approximately 273 EH/s. This is the largest downward difficulty adjustment we’ve seen since July 2021, when we saw a series of downward difficulty adjustments following the Chinese mining ban. This should bring some temporary relief to current miners, but it’s too early to say if this trend in declining hash rate has already concluded.

Mining difficulty had its largest drawdown since July 2021

The hash rate drawdown from all-time highs is less than the average bear market

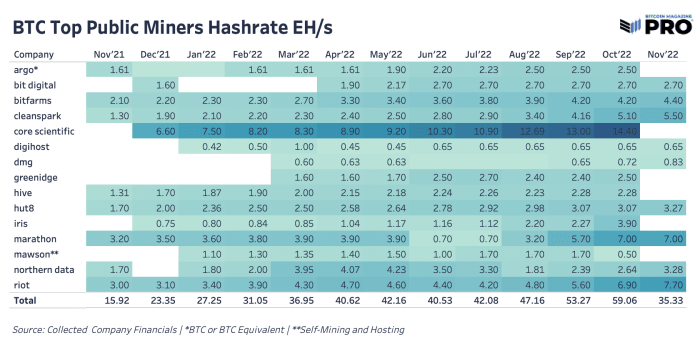

Even with the latest drawdown in hash rate, we’re not seeing announcements come from major public miners. Most public miners’ hash rate is either flat or is growing over the last month.

Public bitcoin miners hash rate remains steady

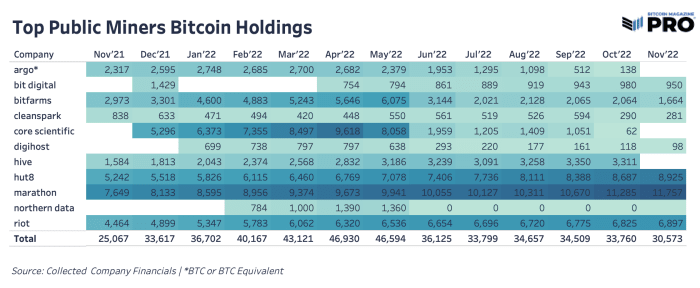

From those who have provided monthly production updates so far, bitcoin holdings are largely rising from the biggest three treasuries across Riot, Marathon and Hut 8 accounting for 27,579 bitcoin. Bitfarms sold a meaningful amount from their treasury which is likely related to paying down their current debt facilities.

Bitcoin holdings are rising from the largest mining companies

In bitcoin terms, miners’ stock performance continues to fall this year when looking at year-to-date returns versus bitcoin performance. The hash price bear market is alive and well, which has been a core thesis for us when evaluating the current prospects of investing in public miners versus bitcoin. Any miner outperformance in bitcoin short-term has proven to be an opportunity in the market to reprice the equity lower.

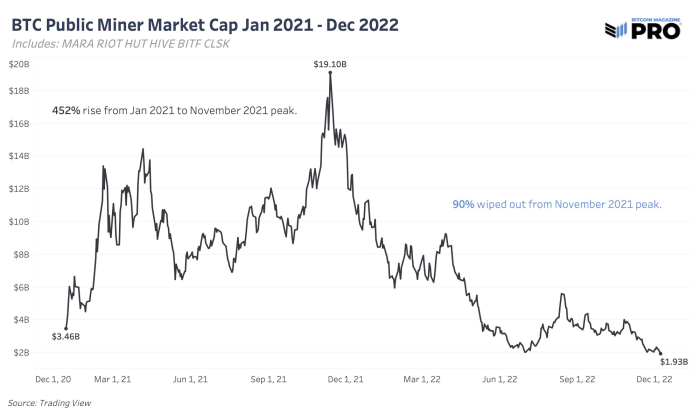

Looking at the market caps of a proxy basket of six public bitcoin miners shows just how much value has been wiped out from 2021. After a 452% rise in value to its November 2021 peak of $19.1 billion, the market wiped out 90% of value in less than a year.

The market cap of public miners has fallen over 90% since all-time highs

While the worst of the drawdown of public miner market capitalizations and hash price (miner revenue per tera hash) has already taken place, we expect that the tough conditions can last for a sustained period of time, squeezing many market participants along the way. The recent downward difficulty adjustment brought about some relief, but it is barely sufficient for many miners who purchased the bulk of their machines in 2021, expecting $30,000 as their “worst-case scenario.”

Throw in an environment where global energy prices and interest rates have skyrocketed and many operations are facing immensely difficult circumstances — particularly hosting facilities where companies serve as intermediaries for customers looking to reap the benefits of mining bitcoin. The elephant in the room for the state of the mining industry is the reality that some of the industry’s biggest hosting facilities are either already bankrupt, teetering on the edge of bankruptcy or are completely out of deployable hash rate for idle ASICs.

We will be intently watching hash rate and the state of the mining industry going forward. Although the industry has been bludgeoned over the course of 2022, we suspect it isn’t out of the woods quite yet.

The beauty of bitcoin and capitalism is that only the strong will survive. Regardless, blocks will continue to be mined every approximately 10 minutes.

On Friday, the trading of shares of Argo Blockchain (NASDAQ: ARBK) was suspended in both the U.S. and U.K.

Particular reasoning for the suspension was not provided.

The suspension could indicate pending updates or changes to the firm.

In the released November operational update, the firm states, “The Company is endeavoring to complete such financing transactions to provide the Company with working capital sufficient for its present requirements.”

The firm is down -94.58% YTD according to NASDAQ, and it mined 198 bitcoin in the month of November. As of November 30, Argo holds 126 bitcoin, “of which 116 were BTC Equivalents.”

Previously, Bitcoin Magazine PRO analysts Dylan LeClair and Sam Rule highlighted Argo as one of several struggling public miners. They noted that a $27 million October fundraise attempt did not go through, which would have been in addition to a preceding $70.6 million loan from NYDIG. Prior to October’s failed raise, in August, Argo used some of its BTC holdings to pay back bitcoin-backed loan obligations from Galaxy Digital.

Bitcoin mining companies continue struggling to survive the ongoing bear market. Dreams of outperforming bitcoin as a public mining company are long gone. Bankruptcies and lawsuits make routine headlines. And even Wall Street analysts that were once bullish on bitcoin mining investment opportunities now say they’re “pulling the plug” until the market improves. But exactly how bad is the current bear market?

It’s always darkest before dawn, as the adage says. And compared to previous bear markets, the mining industry looks much closer to the end of a turbulent market phase than the beginning of it. This article explores a bunch of data sets from the current and previous bear markets to contextualize the state of the industry and how the mining sector is faring. From hardware lifecycles and miner balances, to hash rate growth and hash price declines, all of these data tell a unique story about one of Bitcoin’s most important economic sectors.

Mining Revenue Is Evaporating

When bitcoin’s price drops, it’s not surprising that dollar-denominated mining revenue also drops. But it has – a lot. Roughly 900 BTC are still mined every day and will be until the next halving in 2024. But the fiat price for those bitcoin has plummeted this year, meaning miners have far fewer dollars for expenses like electricity, maintenance and the servicing of loans.

As the chart below demonstrates, in November, the entire bitcoin mining industry earned less than $500 million from processing transactions and issuing new coins. The bar chart below shows this monthly revenue compared to the past five years. November mining revenue marks a two-year low for monthly earnings.

This past month marked a two-year low for Bitcoin mining company revenue.

Potential Hash Rate Uptrend Reversal

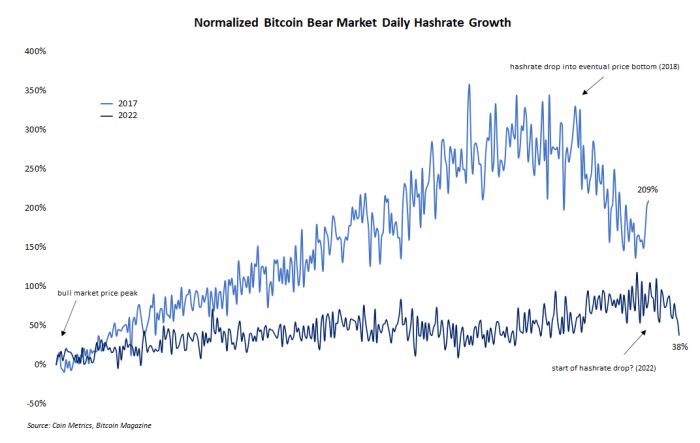

Comparing the current bear market to the previous one in 2018 offers some interesting insights into how the mining industry has changed and how it has remained the same. One such comparison is hash rate growth during downward price trends. It’s not uncommon to see hash rate grow during bear markets. The annotated line chart below shows normalized hash rate growth during the 2018 and 2022 bear markets from bitcoin’s price peak to the drawdowns’ history (or current) lows.

So far in this bear market, Bitcoin hash rate has only grown.

But one thing that is obviously missing from the above chart is a correction in hash rate growth during the later period of the bearish phase. In 2018, for example, the growth trend clearly changed course and dropped as the market eventually found a low for bitcoin’s price. But in the current market, hash rate has only grown. Perhaps a slight drop in hash rate through late November signals a trend change, but the question is still open.

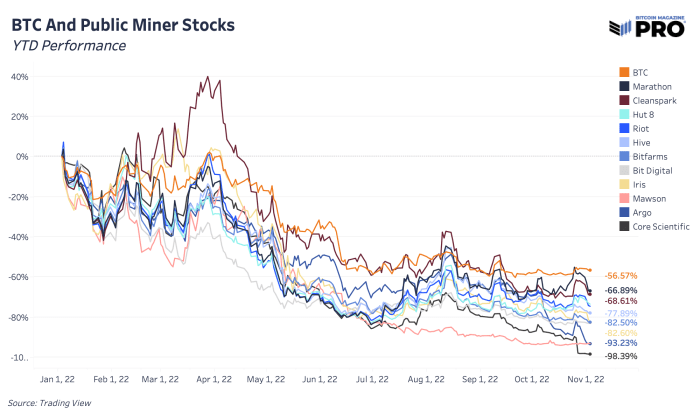

Collapse Of Public Mining Companies

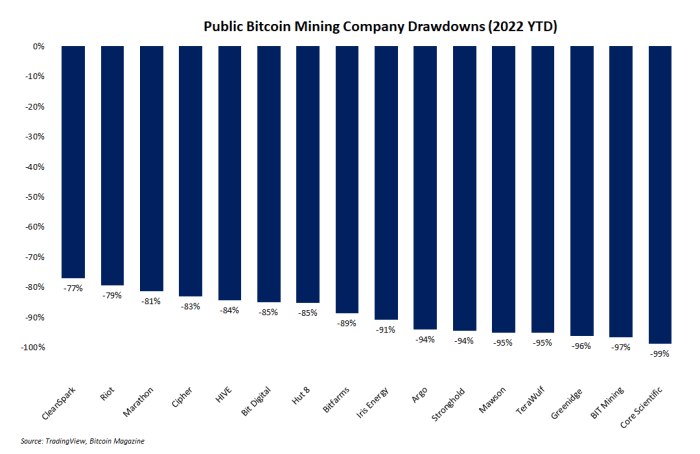

Perhaps the most brutal bitcoin mining chart of all shows the drawdowns of publicly-traded mining companies this year. It’s no secret that the past year has been brutal for bitcoin, other cryptocurrencies, and the global economy in general. But mining companies in particular have been clobbered. Over half of these companies have seen their share prices fall over 90% since January. Only two — CleanSpark and Riot Blockchain — have not dropped more than 80%.

Mining companies in general are often considered to be a high-beta investment in bitcoin, meaning when bitcoin goes up, mining stock prices go up more. But this market dynamic cuts both ways, and when bitcoin falls, the downside for mining stocks is even more brutal. The bar chart below shows the massacre these stocks have endured.

Bitcoin mining stocks have been massacred.

The Rise And Fall Of Bitcoin Mining’s ‘AK-47’

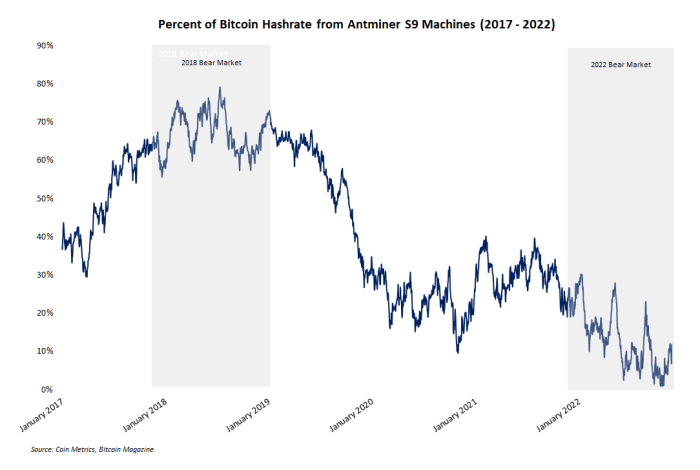

An underappreciated hallmark of the current bitcoin bear market is the precipitous decline in hash rate contributed by Bitmain’s Antminer S9 machines. This model of mining machine is occasionally referred to as the “AK-47” of mining because of its durability and reliable performance. And at one point in the 2018 bear market, the S9 was king. Nearly 80% of Bitcoin’s total hash rate came from this Bitmain model during the depths of the previous bear market.

But the current bear market tells a completely different story. Thanks to new, more efficient hardware and a vice-grip squeeze on mining profit margins, the percentage of hash rate from S9s dropped below 2% in early November. The annotated line chart below shows the rise and fall of this machine.

The Antminer S9 has seen a remarkable fall.

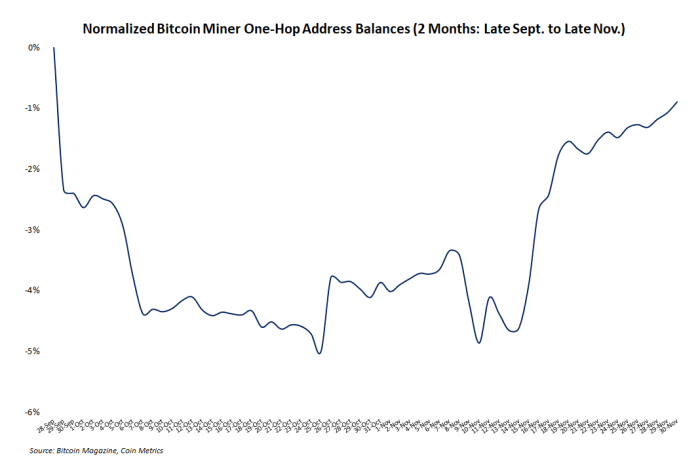

Miner Balance Retraces Its Sell Off

The past few months have been disastrous for the “crypto” industry as exchange wars, insolvent custodians and other forms of financial contagion swept the market. Many bitcoin investors like to assume their segment of the industry is mostly insulated from the chaos of the rest of “crypto,” but this is usually false. In the case of miners, who are notoriously bad at timing the market, some panic was evident as address balances and miner outflows appeared to drop and spike, respectively.

But this activity was short lived. The line chart below shows that miner address balances have almost fully retraced their drop from late September through October. In short, miners appear to be back in HODL mode, impervious to exogenous market events. Whether the bear market is over or not is unknown. But miners seem to be accumulating more than selling.

Miners appear to be back in HODL mode.

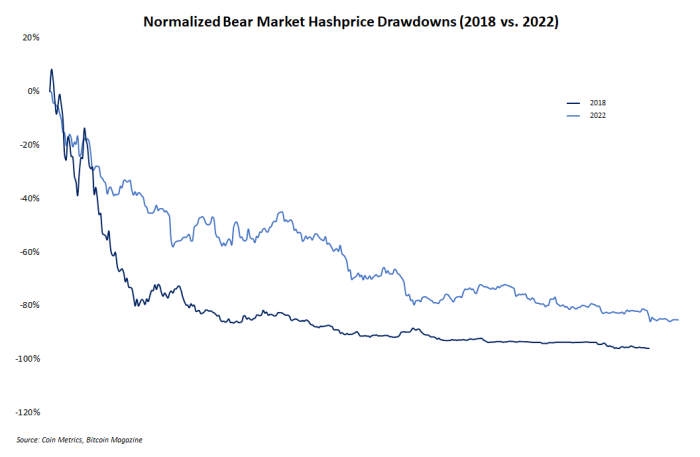

Hash Price Drop Today Vs. 2018

Hash price is one of the most popular economic metrics for miners to track, even though few people outside of the mining sector understand it. In short, this metric represents the dollar-denominated revenue expected to be earned per marginal unit of hash rate. And like everything else in the bear market, hash price has fallen significantly. But its decline is not unusual, especially when it’s compared to the hash price decline in 2018.

Shown in the chart below are normalized hash price drawdowns from 2018 and 2022. Readers will notice the fairly similar slope and size of the drawdowns. 2018 was slightly steeper. 2022 to date has been shallower but longer. But both were and are brutal for fledgling mining operations.

This 2022 hash price drawdown has been shallower but longer than its 2018 equivalent.

The Next Phase Of Mining

Boom and bust cycles are a natural series of events for any properly functioning market. The bitcoin mining sector is no exception. For the past year, mining has seen its weaker, unprepared operators weeded out as the excesses from the bull market are brought to account. Now, in the depths of a bearish period, the real builders can continue to expand their operations and build a solid foundation for the next phase of euphoric bullishness.

This is a guest post by Zack Voell. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Riot Blockchain has released its unaudited production and operations updates for November 2022. According to the release, the company produced 521 BTC, a 12% increase on its November 2021 production of 466 BTC. It sold 450 BTC, generating net proceeds of $8.1 million, and had a deployed fleet of 72,428 miners with a hash rate capacity of 7.7 exahashes per second (EH/s) on 30 November.

Jason Les, CEO of Riot stated, “Riot again achieved a new record for total hash rate capacity during the month of November, resulting in our highest monthly bitcoin production figure to date.” He did caveat this positivity, saying, “Despite this new level of production, expected production was approximately 660 bitcoin given our operating hash rate over the month, assuming normalized performance of the mining pool we participate in. Variance in a mining pool can impact results and while this variance should balance out over time, can be volatile in the short term. This variance led to lower bitcoin production than expected in the month of November, relative to our hash rate.”

To better formulate an outlook on their production, Les stated in the release, “In order to ensure more predictable results going forward, Riot will be transitioning to another mining pool which offers a more consistent reward mechanism, so that Riot will fully benefit from our rapidly growing hash rate capacity as we work towards our goal of reaching 12.5 EH/s in the first quarter of 2023.”

The report did not specify which mining pool Riot will now point its miners towards.

Looking ahead, Riot seeks to achieve a total self-mining hash rate capacity of 12.5 EH/s during Q1 2023, assuming full deployment of approximately 115,450 Antminer ASICs.

However, this does not include any potential incremental productivity gains from the company’s utilization of 200 MW of immersion-cooling infrastructure. The majority of Riot’s self-mining fleet will consist of the latest S19-series miners. In addition to its self-mining operations, the company hosts approximately 200 MW of institutional Bitcoin mining clients.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Latest Public Miner Developments

After writing on the potential for public miner capitulation and covering Core Scientific’s possible bankruptcy route, there’s been a wave of miner announcements and developments that show industry-wide risks taking more shape. The major risk is miners’ accumulated debt and lack of cash flow to afford the interest rate on that debt as profit margins are squeezed. The other risk is hash rate (ASIC mining machines) that has been used as collateral to secure this debt financing.

Public miners across the board continue to heavily underperform bitcoin in year-to-date performance. That’s not a new trend but now, as miners start to fall and the survivors emerge, the performance gap starts to widen in a big way. Miners on the edge of going under are down over 90% while the market’s chosen “stronger” miners are more in the 60-70% drawdown range.

Public miner stocks priced in bitcoin

Starting with Core Scientific, there’s a laundry list of firms that are owed money, including BlockFi, NYDIG and Anchor Labs. In total, creditors are owed around $1 billion and even MassMutual Barings (an investment firm owned by Mutual Life Insurance Co.) is on the short list.

Argo Blockchain is one of those at the bottom, now down 93.23% this year. They released the biggest mining news of the week after announcing that a planned $27 million fundraise didn’t go through. Earlier this year, NYDIG agreed to a $70.6 million loan with Argo. Argo also used some of its bitcoin holdings in August to reduce their BTC-backed loan obligations from Galaxy Digital as well.

Iris Energy highlighted in a financing update this week that the company is “currently capable of generating an indicative $2 million of Bitcoin mining monthly gross profit, compared to aggregate required monthly principal and interest payment obligations of $7 million.” After borrowing $71 million from NYDIG which was secured by ASIC machines for one of their outstanding loans and at risk of needing a debt restructuring, Iris has nearly 36,000 machines that may change hands fairly quickly. The company would default on these loans unless they can find a new agreement by November 8.

Stronghold Digital Mining just this week closed on their debt restructuring deal with NYDIG, delivering a fleet of 26,200 miners in exchange for the wipeout of $67.4 million in debt. Stronghold also extended another tranche of debt to be repaid over 36 months instead of 13 to buy more cash runway. The moves have been a strategic action to “rapidly de-lever our balance sheet and enhance liquidity”.

CleanSpark, who’s been in a place of growth and able to buy ASICs at lower prices recently, ended up selling more of their bitcoin holdings (mined 532 BTC and spent 836) last month to support growth and operations. Although many major miners are still maintaining their HODL strategies and bitcoin balances, strong miners will tap into those holdings for growth opportunities or funding operations when absolutely needed.

TeraWulf, another bitcoin miner down 92.38% year-to-date, runs a relatively high debt-to-equity ratio compared to other miners (86%) and has $120 million in debt to start being paid back in spring 2023 at an 11.5% interest rate.

As larger private lenders like BlockFi and NYDIG don’t disclose how much mining debt is on their balance sheets, it’s impossible to know for sure how exposed some of these lenders are to broader mining industry bankruptcy risk on the horizon. These loans may be a reasonable portion of broader financing activities and well equipped to handle the default risk, but it’s a dynamic worth highlighting and to better understand as we expect more miners to face pressure of debt default and/or restructuring over the next few months.

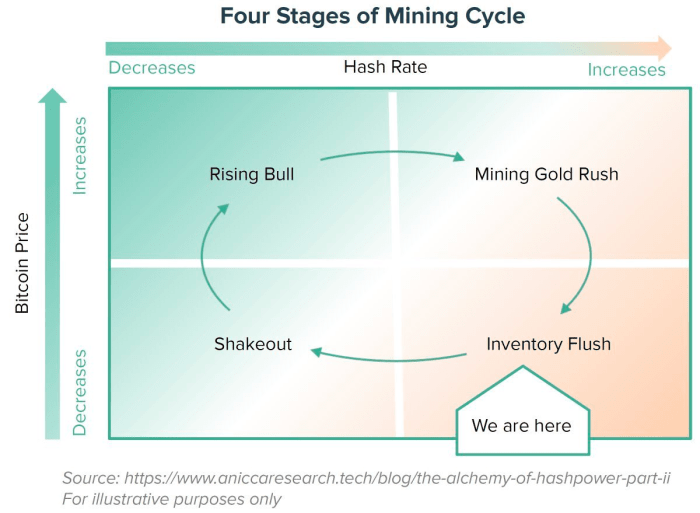

One opinion from Marathon Digital Holdings CEO Fred Thiel, ballparks that 20 or so public miners could be at risk of going bankrupt in what he deems a perfect storm for the industry. There’s no doubt that larger, better positioned miners are looking for potential, favorable acquisition deals to arise fairly soon. Like every other industry before it, major industry consolidation is inevitable and public bitcoin mining looks primed to go through that next phase of its lifecycle. It’s likely we move to a world where there are only a few major bitcoin miner giants with a handful of much smaller miners behind them.

Similarly, it’s entirely possible that as this cycle moves from the bottom right quadrant to the bottom left, cash rich energy producers at both the public and private level start scooping up ASICs to deploy in preparation for the next bull phase.

The biggest risk inherent to the bitcoin market today remains the weak players hanging by a thread underneath the surface. The lack of meaningful price volatility in this $20,000 range is certainly encouraging from the standpoint of buyers and sellers finding a temporary equilibrium. But as the frequency of miner troubles continues to rise, along with the possibility of more fund-based leverage still in the market, max pain unequivocally is lower for industry participants. The brunt of the selling has taken place with bitcoin now at $20,000, but one has to question whether the marginal buyer is of sufficient size to stem the potential selling pressure on the horizon.

We suspect that the pressure is beginning to ramp up on the crypto lenders that did survive the summer contagion, due to the increasing headwinds certain miners are facing in this environment.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Core Scientific Capitulation

We’ve been highlighting the case for more public miner capitulation over the last few months. News shows that Core Scientific, the largest publicly traded mining company by hash rate and miner fleet, may face bankruptcy. The highlights from their SEC filing are the following:

Core Scientific is halting all debt service payments.

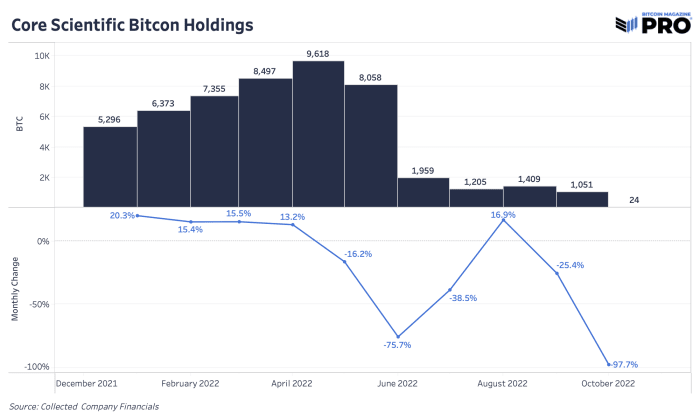

Bitcoin holdings are now 24; they sold 1,027 over the last month.

Cash resources will be depleted by the end of the year or sooner.

Core Scientific claims Celsius owes them $5.4 million.

A giant in the mining space, holding over 9,600 bitcoin at its peak, Core Scientific has now nearly depleted its entire treasury. Month-over-month growth in holdings is now worse than the summer capitulation and selloff we saw back in June 2022. Yet, in June the selloff was much larger in size (6,099 bitcoin). It’s not necessarily the Core Scientific treasury we are concerned about now but rather the treasuries and holdings of all other bitcoin miners if this is a bigger warning sign for the industry.

Core Scientific’s bitcoin holdings went from a whopping 9,618 in May to only 24 in October

Core Scientific was able to drive higher bitcoin production and share of the hash rate by having the largest debt-to-equity ratio in the space at 3.5. Now that debt is coming due during the worst time to try and raise more equity, with depressed prices and lack of financial appetite in the market.

Currently, the company’s liquidity situation is dependent on two variables: the bitcoin price going higher and electricity costs coming down. Our view is that it will be incredibly lucky for either to materialize as a stagnating bitcoin price continues and electricity prices, especially for hosting bitcoin miners, is only trending higher. Looking at Q2 earnings, Core Scientific’s cost of revenues went from 67% to 92% compared to last year. Higher power consumption costs played a significant factor.

The biggest risk associated with mining equities and the rising hash rate is not only if companies can survive and get to the other side; some will and some won’t. Rather, the question you need to ask yourself as an investor is whether your stake in the company will get significantly diluted along the way.

For now, we think broad-based underperformance of miners relative to bitcoin itself can be expected.

Let’s now turn our attention to the potential for a capitulation across the ASIC market, as Core Scientific, the world’s largest publicly traded mining firm by hash rate faces liquidity/solvency worries.

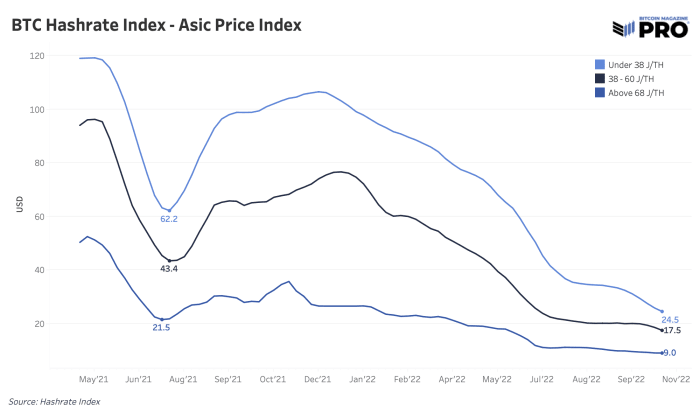

Even without recent developments, ASIC prices were already in fire sale-like territory and are at new all-time lows. Luxor’s Hash Rate Index shows just how depressed prices have become across machine efficiency types in the chart below. As miners have gone to the latest, more efficient rigs, that’s put further downward price pressure on older mining models. As there’s more demand for newer rigs like the S19 XP and other brand new hardware to stay competitive, selling pressure rises for older models that are unviable or unprofitable even with the cheapest energy costs. In the worst case, older machines are just given away for free.

Although Core Scientific will have many options such as debt restructuring, Chapter 11 bankruptcy or a potential merger on the table; selling off and liquidating a part of their 130,000 miner fleet may be another option. Increased selling pressure by miners will only add more strain to depressed prices. Further declines in ASIC prices also impact all miners who are collateralizing or financing their ASICs as the value of ASIC prices can drop further. Now, we await what strain this will have on hash rate over the medium term and if we’re to see a significant falloff in hash rate over the next three to six months. We do not believe this cycle ends without a 20% fall in peak-to-trough hash rate.

ASIC prices are in free-fall mode as hash rate continues to increase while price stays stagnant

Final note: Bitcoin mining is a brutal business, and the current state of these conditions is the last remaining bear to slay in regards to the conclusion of this bearmarket cycleand the rebirth of the next bull market.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

As Hash Rate Soars, Parallels to 2018 Arise

On October 23, bitcoin mining difficulty saw an upwards adjustment of 3.44% (after the previous adjustment of 13.55%), pushing mining difficulty to yet another all-time high as hash rate continues to soar. With the price of bitcoin stagnating at $20,000 give or take for the last few months, we have noticed some parallels between the market cycle of 2018 and the one in front of us today.

The rising hash rate dynamic seen throughout 2022 while the bitcoin price has fallen has put a lot of pressure on both public and private mining operations. Throughout the year, we have seen public miners capitulate on their bitcoin holdings, as diminishing revenue and treasury values have placed increasing pressure on balance sheets.

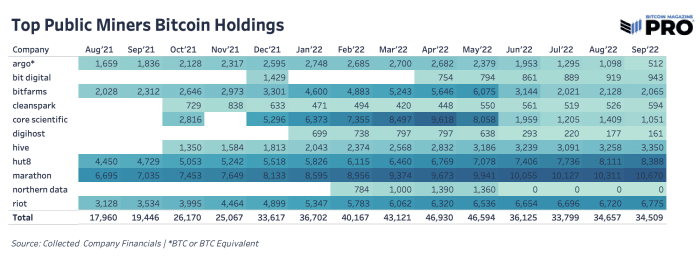

At their peak, public miners’ bitcoin holdings reached over 46,000 BTC but have since fallen 26% as bitcoin treasuries were sold out of necessity to access more capital, pay down debt and fund operations and expansion plans. Although estimated and rough numbers, the top public miners make up over 20% of all Bitcoin’s network hash rate. Moves from public miners to not only sell bitcoin holdings but also to expand and contract their hash rate have a significant impact on the market.

Bitcoin holdings from the top publicly traded bitcoin mining companies

As hash price continues to trend to all time lows, the probability of a miner capitulation/liquidation event probabilistically increases until a drawdown in hash rate, as certain entities cease mining and liquidate their assets (in the form of both bitcoin and ASICs).

Barring the China mining ban during 2021, the largest peak-to-trough drop in hash rate (7d MA) in the history of bitcoin was approximately 35%. In our opinion, this bear market cycle won’t end until a flush of the weakest miner participants has occurred, which will be observable by a temporary yet meaningful fall in hash rate and will subsequently decrease mining difficulty, easing conditions for the surviving participants.

While there was already a “capitulation” per se earlier this summer during the initial cryptocurrency market deleveraging in June, hash rate has since gone vertical, with new fleets of the newest Bitmain Antminer S19 XP, an industry-leading miner, just now being deployed en masse by the largest miners.

Given the current state of hash rate and difficulty, we believe that the pressure is indeed building, but the figurative burst has yet to occur.

The Mechanics Of A Race To The Bottom

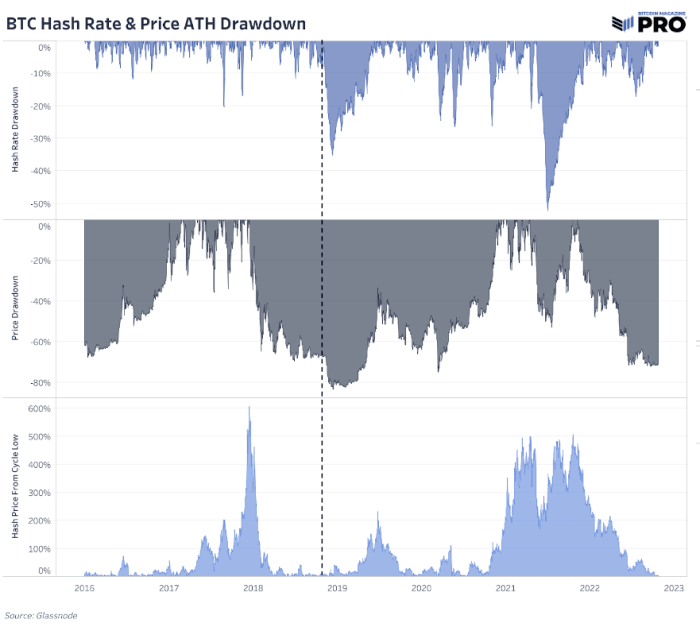

We could easily see a scenario where further bitcoin price and miner industry revenue pressures force more of that held bitcoin back into the market along with a significant drawdown in hash rate. Below charts show the comparison of hash rate, price trajectory and percentage drawdown from 2018 and present day.

The comparison of hash rate, price trajectory and percentage drawdown from 2018

The current comparison of hash rate, price trajectory and percentage drawdown

If there is a case for the last last leg lower, this is it, and our data-driven approach has us leaning towards this having a decent likelihood of playing out. In the chart below, observe what happened to the bitcoin market the last time there was a price stagnation following a drawdown of this caliber as hash rate soared to daily new highs (hint: the dotted line).

The last time there was a price stagnation following a major hash rate drawdown

While history doesn’t repeat, it often rhymes, and our data-driven approach has our team on increasing alert about the pressure this mining industry and subsequently the bitcoin market will face over the short term.

While we are in no way saying this occurs with certainty, the higher that hash rate goes while bitcoin the asset itself trades with increasingly muted levels of volatility -71% from its previous all-time high (around when some of the largest CapEx investments made into mining infrastructure took place), then it is increasingly probable a final miner-induced capitulation event will occur. This is not a prediction, but rather an observation based on the data currently in front of us.