U.S. stock futures were mixed Thursday as Nvidia results boosted tech but debt ceiling concerns weighed on the Dow.

How are stock-index futures trading

S&P 500 futures ES00, +0.67%

rose 21 points, or 0.5%, to 4147

Dow Jones Industrial Average futures YM00, -0.14%

fell 107 points, or 0.3%, to 32747

Nasdaq 100 futures NQ00, +1.83%

jumped 225 points, or 1.6%, to 13875

On Wednesday, the Dow Jones Industrial Average DJIA, -0.77%

fell 256 points, or 0.77%, to 32800, the S&P 500 SPX, -0.73%

declined 30 points, or 0.73%, to 4115, and the Nasdaq Composite COMP, -0.61%

dropped 76 points, or 0.61%, to 12484.

What’s driving markets

Recurring fiscal concerns are battling with a nascent technological paradigm for the market’s lead. Fears about the looming debt-ceiling deadline is counteracted by ebullience over AI to deliver a stark bifurcation.

Futures for the Dow Jones Industrial Average — a gauge arguably currently more sensitive to broader economic conditions — were under pressure early Thursday, while futures for the tech-rich Nasdaq 100 — powered by optimism over a secular AI shift — surged strongly.

“The prospect of the U.S. government being unable to meet its financial obligations continues to be a key influence on investor sentiment in global equity markets,” said Derren Nathan, head of equity research at Hargreaves Lansdown.

Ructions at the short end of the Treasury market — where some 1-month bill yields TMUBMUSD01Y, 5.174%

broke above 7% — illustrate trader anxiety that unless Congress can reach an agreement to extend the debt-ceiling the U.S. government may technically default at the beginning of June.

Ratings agency Fitch late Wednesday said it was placing Washington’s AAA credit rating on watch for a possible downgrade given what it termed the debt ceiling “brinkmanship”.

However, results and comments from chipmaker Nvidia NVDA, -0.49%,

whose stock is soaring 25% in premarket action, have boosted hopes that AI will deliver the next period of strong growth for a number of tech companies.

“The AI revolution may be making a lot of noise but results from microchip firm Nvidia hint at some substance behind the hype,” said Russ Mould, investment director at AJ Bell.

CS.ai Inc. AI, +2.54%

and Advanced Micro Devices AMD, +0.14%

were among those bathing in Nvidia’s AI glow early Thursday.

The optimism over semiconductors bade well for the wider tech sector, according to Mark Newton, head of technical strategy at Fundstrat: “Semis in relative terms to broader technology, have the potential to break back out to new all-time highs this week on a ratio basis. That would be important and positive for this leading sector to show such strength.”

U.S. economic updates set for release on Thursday include the weekly initial jobless claims data and the second reading of first quarter GDP, both at 8:30 a.m. Eastern. Pending home sales for April will be published at 10 a.m..

Fed officials making comments include Richmond Fed President Tom Barkin speaking at 9:50 a.m. and Boston Fed President Susan Collins talking at 10:30 a.m.

Nvidia Corp. headed toward market-capitalization gains of nearly $200 billion in after-hours trading Wednesday, which could put the chip maker within sight of becoming only the seventh U.S. company to top a valuation of $1 trillion.

Nvidia ended Wednesday’s session with a market cap — the total value of all shares in existence — of roughly $754.3 billion, according to FactSet. A 25% increase would add nearly $189 billion to that total, putting the company within striking distance of $1 trillion. Only six U.S. companies have ever attained a $1 trillion market cap: Apple Inc. AAPL, +0.16%

and Microsoft Corp. MSFT, -0.45%

are currently worth more than $2 trillion apiece; Google parent Alphabet Inc. GOOGL, -1.35%

and Amazon.com Inc. AMZN, +1.53%

have valuation of more than $1 trillion; and Facebook parent Meta Platforms Inc. META, +1.00%

and Tesla Inc. TSLA, -1.54%

have both touched the $1 trillion plateau previously.

Nvidia’s market cap was ahead of both Meta and Tesla as of Wednesday’s close, with both worth less than $650 billion, showing the potential fleeting nature of such a valuation. Nvidia’s record market cap is $834.4 billion, established on Nov. 29. 2021, according to Dow Jones Market Data.

If Nvidia’s gains hold through Thursday’s trading session, the company could challenge for the largest one-day market-cap gain in history. The biggest currently on record was Amazon’s $191.2 billion increase on Feb. 4, 2022, according to Dow Jones Market Data, followed closely by a $190.9 billion gain by Apple on Nov. 10, 2022. Nvidia also stands to gain more than rival Advanced Micro Devices Inc. AMD, +0.14%

is worth in total — AMD ended Wednesday’s session with a market cap of $174.4 billion.

Nvidia is closing in on the rare $1 trillion plateau because of huge gains in its stock this year, as hopes and hype about generative AI have flooded the tech sector. After OpenAI debuted its ChatGPT AI offering, and investor Microsoft quickly integrated the chatbot into many of its services, expectations for the technology have exploded.

Despite the hype, most companies have avoided providing hard figures for revenue gains expected from AI. Nvidia’s fiscal second-quarter forecast — which calls for roughly $11 billion in sales, nearly 33% higher than Nvidia’s previous quarterly record of $8.28 billion — could be seen as the first sign of a wave of fresh spending coursing through the tech sector.

Other companies have indicated that they will be forced to spend to develop their technology before reaping large financial rewards from it. Microsoft, for example, disclosed to investors last month that capital expenditures are increasing as it builds AI capabilities into its Azure cloud-computing platform — spending that is largely going toward Nvidia.

That is a rather typical path for large jumps in tech spending: Companies that make the necessary hardware see gains before the companies that use that gear can develop offerings that take advantage of it. Other gear makers joined Nvidia in the sharp move higher in after-hours trading Wednesday, including AMD, which gained more than 10%; chip maker Marvell Technology Inc. MRVL, -1.31%,

which increased more than 5%; and networking specialist Arista Networks Inc. ANET, +0.53%,

which added about 5%.

Alphabet and Microsoft stocks both increased around 2% in after-hours trading, and software companies that have made AI a core part of their offerings also saw gains. Palantir Technologies Inc. PLTR, -3.24%

and C3.ai Inc. AI, +2.54%

shares both increased more than 8%, for example.

Oil demand is likely to hold up longer than many people expect during the anticipated transition to electric vehicles. And changes in the industry point to oilfield services companies as good long-term growth investments as offshore production ramps up.

Below is a list of oil producers and related companies favored by two analysts who have followed the industry for decades.

David Rosenberg honestly doesn’t want to be bearish on stocks or bash the Federal Reserve. The veteran market strategist will get no satisfaction if he’s right about Americans having to slog through recession and consequently endure deflation, job losses and a wallop to the stock market.

“As I play the role of economic detective, I can see the smoking gun,” says Rosenberg, a former chief North American economist at Merrill Lynch and now president of Toronto-based Rosenberg Research.

Opinions expressed by Entrepreneur contributors are their own.

Investing in emerging music artists might be the perfect opportunity if you’re looking for an innovative and rewarding move to diversify your portfolio.

The music industry has always been a lucrative and exciting space for investors. Music can captivate an audience, evoke emotions and inspire us in ways no other art form can. Putting money into emerging musicians is an opportunity to get in on the ground floor and potentially reap large returns, thanks to the power of discovery.

Whether you’re a music industry veteran, a fan, or just someone looking for a savvy investment, investing in emerging musicians will diversify your financial portfolio and have fun doing so.

Here are the top benefits you can expect from investing in emerging music artists.

Investing in emerging music artists is a great way to generate passive income with unstoppable growth. You may have never thought this way, but every time you hear the most overplayed song, its songwriters and artists get a payout.

Luckily, the power of the internet and the ever-changing landscape of the music industry has made it easier than ever to find and invest in upcoming music talent. Simultaneously, new artists have more possibilities to reach a larger audience and build a successful career with the rise of streaming services like Spotify. That’s why investing in emerging music artists is such an attractive option.

Once an artist has established themselves and their music is being streamed or purchased, they can begin to generate revenue — and you’ll get a share of the profits. Music royalties can also bring in a consistent stream of income and potential performance royalties.

Investing in emerging music artists is your chance to enter the protected asset class in a market known for record-high content creation and exponential growth. The music industry seems to have finally found a technology-based model that works for artists, consumers, and businesses.

As an investor, you can use your influence to help your favorite artists grow and become successful. For example, you can introduce them to new contacts, help them with their marketing strategies, and generally be a support system—and yield great rewards in return.

The music industry is constantly evolving, so investing in emerging music artists can be a great way to stay ahead of the curve and capitalize on new trends. With this approach, you can get in on the ground floor of a potential breakout and enjoy a larger return on your investment than if you had waited until the artist was an established star.

Investing in an artist early can help them develop their sound and build their fan base while also financing their career. This can result in a much bigger pay-off down the road.

Emerging music artists often have the potential to become superstars, and when they do, their music sales and streaming figures can skyrocket. Ultimately, the return on your investment could be significantly higher than that of more established artists.

3. A true sense of fulfillment

Investing in emerging music artists isn’t just about money. It is an excellent way to support the career of an artist you truly believe in and help them reach their full potential.

When you invest in emerging music artists, you help create a platform for them to share their music with the world. You give them a chance to be heard and make a real impact in the music industry. You are ultimately enabling them to make a living doing something they love.

As such, it’s safe to say that investing in music can be an act of true passion and advocacy. The experience can be incredibly rewarding, as you can be part of an artist’s journey and watch them grow and develop their art. It’s a great way to support the arts, help new artists get their start and contribute to shaping the future of the music industry. It will give you a feeling of pride and satisfaction that goes beyond any financial gain.

With the new wave of digital music streaming and the ever-evolving music industry, more and more individuals and businesses are looking for ways to diversify their investments and maximize returns.

Investing in emerging music artists offers a unique opportunity to do that. It can provide a great hedge against market volatility, opening the door to interesting diversification opportunities.

For starters, you can benefit from the financial growth of your chosen artist. As the artist’s visibility and success increase, so does their financial value. This means your investment can grow alongside the musician’s success, generating a steady and reliable income stream.

More importantly, investing in emerging music artists can provide you with a level of diversification that other investments may not offer. Music is an ever-changing and ever-evolving industry, so the success of any one artist can be unpredictable. By investing in different music artists, you can spread the risk across multiple assets and ensure that if one artist fails, the other investments will provide you with some support.

The bottom line

As the music industry continues to expand and evolve, so do the opportunities for investors to benefit from the success of up-and-coming artists.

Investing in emerging music artists can be a smart move for investors looking to reap the rewards of a growing industry. Not only can investing in music be lucrative, but it can also be a great way to support and empower the artists you believe in.

In addition to diversifying your portfolio and getting involved in something you are passionate about, you can get in on the ground floor of a potentially lucrative venture.

That said, successful investment in music talent requires having a good understanding of what’s hot and what’s not, along with a keen eye for potential. Any individual or entity looking to make their first investment in an up-and-coming music artist must perform a risk analysis and determine an ideal time horizon, meaning how much they can safely invest and how long they’ll be willing to get a return.

If you invest in dividend stocks, you are probably looking for long-term growth to go with the income. Otherwise you might be content to hold one-month U.S. Treasury bills, which yield 4.5% or park your money in an online savings account for a yield close to 4%.

Below is screen of stocks with current dividend yields ranging from 4.14% to 8.46%. What sets these apart from other stocks with high dividend yields is that their payout increases are expected to accelerate in 2023 and 2024 from those in 2022.

On Tuesday, S&P Dow Jones Indices said in a press release that it expected dividend payments by publicly traded U.S. companies to continue to hit record levels in 2023. But Howard Silverblatt, a senior index analyst with the firm, said that the pace of dividend increases in the first quarter had slowed and that he expected this year’s increases to be “at half the pace of the double-digit 2022 growth.”

Silverblatt also said current events in the banking industry were “expected to negatively impact future spending from both consumers and companies, which in turn may curtail corporate dividend growth.”

For many banks, there’s another big item on the table. A focus on share buybacks in recent years is very likely to end — this is a use of cash that can raise earnings per share if the share count is reduced, but there can be consequences, especially after a year of rising interest rates that pushed down the market value of banks’ investments in bonds.

In a note to clients on March 16, Dick Bove, a senior research analyst with Odeon Capital, predicted that stock repurchases in the banking industry would be “meaningfully cut back if not flat out eliminated.” He made three general points about buybacks in the banking industry:

Buybacks remove working capital that would otherwise provide returns to a bank.

Buybacks mean a bank’s board of directors is “in favor of flat-out giving capital away to investors that want nothing to do with the bank — they are selling its stock.”

Buybacks do “nothing to increase bank stock prices – many bank stocks are selling at below their prices of five years ago.”

A company might find it much easier to curtail or stop buying back shares to preserve cash than it is to cut regular dividends. Preserving and increasing the dividend over time has been correlated with good performance for stocks over time. These articles provide examples of how dividend compounding is correlated with long-term growth as income streams build up:

The S&P Dow Jones Indices report raises the question of which stocks might buck the trend.

Starting with the S&P 500 SPX, -0.50%,

there are 71 companies stocks with current dividend yields of at least 4.00% indicated by annual payout rates. Among these companies, 68 increased dividends during 2022, according to data provided by FactSet.

Then we looked at the pace of dividend increases in 2022 and the consensus estimates for dividends paid during 2023 and 2024, among analysts polled by FactSet. Among the remaining 68 companies, there are 29 for which the estimated 2023 dividend increase is higher than the 2022 dividend increase. Narrowing further, there are 14 for which the estimated 2024 dividend increases are higher than the estimated 2023 dividend increases.

Here are the 14 stocks that passed the screen, sorted by current dividend yield:

Click here for Tomi Kilgore’s detailed guide to the wealth of information available for free on the MarketWatch quote page.

Any stock screen is limited, but can be useful as a starting point or supplement to your own research. If you see any companies of interest, do some research to form your own opinion of how likely they are to remain competitive over the next decade, at least.

Be careful what you wish for. U.S. job openings dropped below 10 million, a symbolic sign that the Federal Reserve’s efforts to combat inflation by sapping labor-market demand was working — and U.S. stocks promptly fell. Perhaps the bigger issue is that investors were not willing to push stocks out of the 3,800 to 4,200 range the S&P 500 SPX, -0.48%

has been trading in for months.

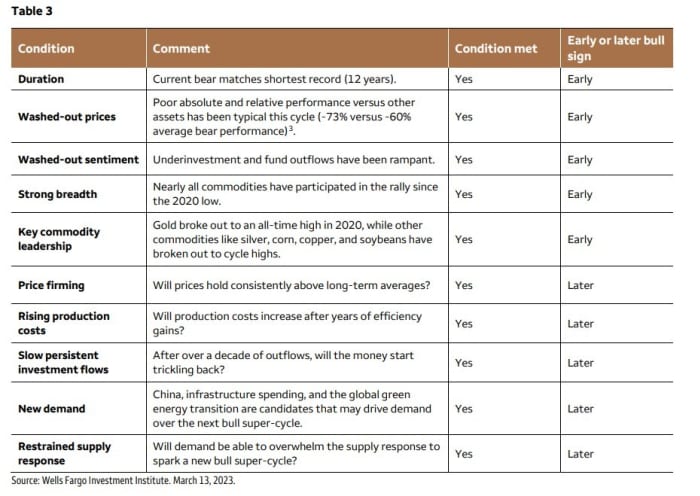

It might not be the most obvious time to be discussing a commodity supercycle, with recession talk growing, but then that’s what makes this call more interesting. Strategists at Wells Fargo investment Institute argue it’s year three of a commodity supercycle, which they say has plenty more room to run.

John LaForge, head of real asset strategy, and Mason Mendez, investment strategy analyst, say commodities are like black holes, in that escaping the gravity of a supercycle is difficult for any individual commodity. They point to this chart, looking at commodity momentum since 1800, plotted in 10-year moving averages, which shows that food, energy and the commodity complex as a whole tend to follow each other around.

Right now nearly all the signs, both technical and fundamental, point to a commodity bull market, they say. The early signs are mostly shifting prices and technical indicators, and the latter signs are more fundamental in nature, like restrained supplies. “The bottom line is that the key early technical indicators are confirming to us that a new supercycle likely began in 2020.”

The analysts went further into depth on what they call washed-out sentiment. They say the process goes something like this: near the end of a commodity bull supercycle, prices go so high that oversupplies become rampant and need to be worked off, which results in investment stopping to flow into production. They say that in both corn C00, +0.80%

and gold GC00, -0.17%

— not commodities with much in common — supply growth rates have turned negative in recent years. Both showed similar conditions at the start of the last supercycle, in 1999.

They advise using commodities as portfolio diversifiers, which certainly would have helped last year, when both stocks and bonds fell but the Bloomberg commodity index rose nearly 16%. They highlight commodity prices typically move differently than stocks or bonds over the long run. And they say that supercycles have historically lasted a decade or longer, and the shortest commodity bull market on record was nine years.

One caveat: the speed of technology advances. Sometimes technology can help fuel demand, but conversely, to the extent technology can make commodities easier to extract, it can also buoy supplies. The obvious example here, not pointed out in the note, is the shale-oil revolution. There’s an interesting article in The Economist (subscription required), how copper has yet to be the beneficiary of a technology boost.

NQ00, -1.08%

edged lower. Oil prices CL.1, -0.62%

fell but held over $80 per barrel. The yield on the 10-year Treasury TMUBMUSD10Y, 3.295%

turned lower after the latest jobs data.

Overseas, New Zealand’s central bank made a larger-than-expected 50 basis point rate hike, while a joint forecast of Germany’s leading institutes upgraded its view on the eurozone’s largest economy, now expecting a 0.3% advance.

Alphabet’s GOOGL, -0.63%

Google says its chips are faster and more power efficient than comparable chips from Nvidia NVDA, -3.41%.

Western Alliance Bancorp WAL, -16.47%

shares fell in premarket trade after the regional lender detailed the latest losses in its portfolio of loans and securities.

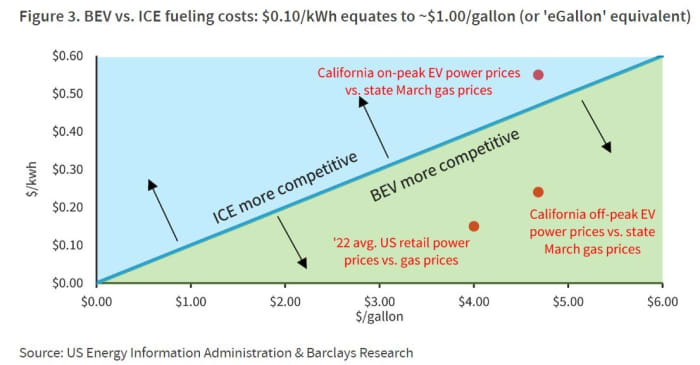

Sure, higher gasoline prices naturally drive demand for electric vehicles. But at what point do high electricity prices make it more cost-effective to buy old gas guzzlers? This chart from Barclays breaks it down — roughly, 10 cents per kilowatt hour equates to $1 per gallon. Right now it’s cheaper to fill a car at the pump than recharge at peak hours.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

Norway’s sovereign wealth fund had a 1.49% stake in Credit Suisse Group AG at the end of 2022 and a 3.31% stake in UBS Group AG, holdings that remain “approximately unchanged,” it said Monday.

UBS yesterday agreed to take over Swiss rival Credit Suisse for more than $3 billion as regulators pushed for the deal in an effort to calm declining confidence in the global banking system.

Credit Suisse shareholders will receive one UBS share for every 22.48 Credit Suisse shares held, but holders of around $17.3 billion of additional tier 1 bonds, or AT1s, will receive nothing.

Norges Bank Investment Management, the arm of Norway’s central bank that manages the sovereign-wealth fund, commonly known as the oil fund, said that it doesn’t hold any Credit Suisse AT1 bonds.

Write to Dominic Chopping at dominic.chopping@wsj.com

David Rosenberg, the former chief North American economist at Merrill Lynch, has been saying for almost a year that the Fed means business and investors should take the U.S. central bank’s effort to fight inflation both seriously and literally.

Rosenberg, now president of Toronto-based Rosenberg Research & Associates Inc., expects investors will face more pain in financial markets in the months to come.

“The recession’s just starting,” Rosenberg said in an interview with MarketWatch. “The market bottoms typically in the sixth or seventh inning of the recession, deep into the Fed easing cycle.” Investors can expect to endure more uncertainty leading up to the time — and it will come — when the Fed first pauses its current run of interest rate hikes and then begins to cut.

Fortunately for investors, the Fed’s pause and perhaps even cuts will come in 2023, Rosenberg predicts. Unfortunately, he added, the S&P 500 SPX, -0.61%

could drop 30% from its current level before that happens. Said Rosenberg: “You’re left with the S&P 500 bottoming out somewhere close to 2,900.”

At that point, Rosenberg added, stocks will look attractive again. But that’s a story for 2024.

In this recent interview, which has been edited for length and clarity, Rosenberg offered a playbook for investors to follow this year and to prepare for a more bullish 2024. Meanwhile, he said, as they wait for the much-anticipated Fed pivot, investors should make their own pivot to defensive sectors of the financial markets — including bonds, gold and dividend-paying stocks.

MarketWatch: So many people out there are expecting a recession. But stocks have performed well to start the year. Are investors and Wall Street out of touch?

Rosenberg: Investor sentiment is out of line; the household sector is still enormously overweight equities. There is a disconnect between how investors feel about the outlook and how they’re actually positioned. They feel bearish but they’re still positioned bullishly, and that is a classic case of cognitive dissonance. We also have a situation where there is a lot of talk about recession and about how this is the most widely expected recession of all time, and yet the analyst community is still expecting corporate earnings growth to be positive in 2023.

In a plain-vanilla recession, earnings go down 20%. We’ve never had a recession where earnings were up at all. The consensus is that we are going to see corporate earnings expand in 2023. So there’s another glaring anomaly. We are being told this is a widely expected recession, and yet it’s not reflected in earnings estimates – at least not yet.

There’s nothing right now in my collection of metrics telling me that we’re anywhere close to a bottom. 2022 was the year where the Fed tightened policy aggressively and that showed up in the marketplace in a compression in the price-earnings multiple from roughly 22 to around 17. The story in 2022 was about what the rate hikes did to the market multiple; 2023 will be about what those rate hikes do to corporate earnings.

“ You’re left with the S&P 500 bottoming out somewhere close to 2,900. ”

When you’re attempting to be reasonable and come up with a sensible multiple for this market, given where the risk-free interest rate is now, and we can generously assume a roughly 15 price-earnings multiple. Then you slap that on a recession earning environment, and you’re left with the S&P 500 bottoming out somewhere close to 2900.

This is just pure mathematics. All the stock market is at any point is earnings multiplied by the multiple you want to apply to that earnings stream. That multiple is sensitive to interest rates. All we’ve seen is Act I — multiple compression. We haven’t yet seen the market multiple dip below the long-run mean, which is closer to 16. You’ve never had a bear market bottom with the multiple above the long-run average. That just doesn’t happen.

David Rosenberg: ‘You want to be in defensive areas with strong balance sheets, earnings visibility, solid dividend yields and dividend payout ratios.’

Rosenberg Research

MarketWatch: The market wants a “Powell put” to rescue stocks, but may have to settle for a “Powell pause.” When the Fed finally pauses its rate hikes, is that a signal to turn bullish?

Rosenberg: The stock market bottoms 70% of the way into a recession and 70% of the way into the easing cycle. What’s more important is that the Fed will pause, and then will pivot. That is going to be a 2023 story.

The Fed will shift its views as circumstances change. The S&P 500 low will be south of 3000 and then it’s a matter of time. The Fed will pause, the markets will have a knee-jerk positive reaction you can trade. Then the Fed will start to cut interest rates, and that usually takes place six months after the pause. Then there will be a lot of giddiness in the market for a short time. When the market bottoms, it’s the mirror image of when it peaks. The market peaks when it starts to see the recession coming. The next bull market will start once investors begin to see the recovery.

But the recession’s just starting. The market bottoms typically in the sixth or seventh inning of the recession, deep into the Fed easing cycle when the central bank has cut interest rates enough to push the yield curve back to a positive slope. That is many months away. We have to wait for the pause, the pivot, and for rate cuts to steepen the yield curve. That will be a late 2023, early 2024 story.

MarketWatch: How concerned are you about corporate and household debt? Are there echoes of the 2008-09 Great Recession?

Rosenberg: There’s not going to be a replay of 2008-09. It doesn’t mean there won’t be a major financial spasm. That always happens after a Fed tightening cycle. The excesses are exposed, and expunged. I look at it more as it could be a replay of what happened with nonbank financials in the 1980s, early 1990s, that engulfed the savings and loan industry. I am concerned about the banks in the sense that they have a tremendous amount of commercial real estate exposure on their balance sheets. I do think the banks will be compelled to bolster their loan-loss reserves, and that will come out of their earnings performance. That’s not the same as incurring capitalization problems, so I don’t see any major banks defaulting or being at risk of default.

But I’m concerned about other pockets of the financial sector. The banks are actually less important to the overall credit market than they’ve been in the past. This is not a repeat of 2008-09 but we do have to focus on where the extreme leverage is centered.

It’s not necessarily in the banks this time; it is in other sources such as private equity, private debt, and they have yet to fully mark-to-market their assets. That’s an area of concern. The parts of the market that cater directly to the consumer, like credit cards, we’re already starting to see signs of stress in terms of the rise in 30-day late-payment rates. Early stage arrears are surfacing in credit cards, auto loans and even some elements of the mortgage market. The big risk to me is not so much the banks, but the nonbank financials that cater to credit cards, auto loans, and private equity and private debt.

MarketWatch: Why should individuals care about trouble in private equity and private debt? That’s for the wealthy and the big institutions.

Rosenberg: Unless private investment firms gate their assets, you’re going to end up getting a flood of redemptions and asset sales, and that affects all markets. Markets are intertwined. Redemptions and forced asset sales will affect market valuations in general. We’re seeing deflation in the equity market and now in a much more important market for individuals, which is residential real estate. One of the reasons why so many people have delayed their return to the labor market is they looked at their wealth, principally equities and real estate, and thought they could retire early based on this massive wealth creation that took place through 2020 and 2021.

Now people are having to recalculate their ability to retire early and fund a comfortable retirement lifestyle. They will be forced back into the labor market. And the problem with a recession of course is that there are going to be fewer job openings, which means the unemployment rate is going to rise. The Fed is already telling us we’re going to 4.6%, which itself is a recession call; we’re going to blow through that number. All this plays out in the labor market not necessarily through job loss, but it’s going to force people to go back and look for a job. The unemployment rate goes up — that has a lag impact on nominal wages and that is going to be another factor that will curtail consumer spending, which is 70% of the economy.

“ My strongest conviction is the 30-year Treasury bond. ”

At some point, we’re going to have to have some sort of positive shock that will arrest the decline. The cycle is the cycle and what dominates the cycle are interest rates. At some point we get the recessionary pressures, inflation melts, the Fed will have successfully reset asset values to more normal levels, and we will be in a different monetary policy cycle by the second half of 2024 that will breathe life into the economy and we’ll be off to a recovery phase, which the market will start to discount later in 2023. Nothing here is permanent. It’s about interest rates, liquidity and the yield curve that has played out before.

MarketWatch: Where do you advise investors to put their money now, and why?

Rosenberg: My strongest conviction is the 30-year Treasury bond TMUBMUSD30Y, 3.674%.

The Fed will cut rates and you’ll get the biggest decline in yields at the short end. But in terms of bond prices and the total return potential, it’s at the long end of the curve. Bond yields always go down in a recession. Inflation is going to fall more quickly than is generally anticipated. Recession and disinflation are powerful forces for the long end of the Treasury curve.

As the Fed pauses and then pivots — and this Volcker-like tightening is not permanent — other central banks around the world are going to play catch up, and that is going to undercut the U.S. dollar DXY, +0.70%.

There are few better hedges against a U.S. dollar reversal than gold. On top of that, cryptocurrency has been exposed as being far too volatile to be part of any asset mix. It’s fun to trade, but crypto is not an investment. The crypto craze — fund flows directed to bitcoin BTCUSD, +0.35%

and the like — drained the gold price by more than $200 an ounce.

“ Buy companies that provide the goods and services that people need – not what they want. ”

I’m bullish on gold GC00, +0.22%

– physical gold — bullish on bonds, and within the stock market, under the proviso that we have a recession, you want to ensure you are invested in sectors with the lowest possible correlation to GDP growth.

Invest in 2023 the same way you’re going to be living life — in a period of frugality. Buy companies that provide the goods and services that people need – not what they want. Consumer staples, not consumer cyclicals. Utilities. Health care. I look at Apple as a cyclical consumer products company, but Microsoft is a defensive growth technology company.

You want to be buying essentials, staples, things you need. When I look at Microsoft MSFT, -0.61%,

Alphabet GOOGL, -1.79%,

Amazon AMZN, -1.17%,

they are what I would consider to be defensive growth stocks and at some point this year, they will deserve to be garnering a very strong look for the next cycle.

You also want to invest in areas with a secular growth tailwind. For example, military budgets are rising in every part of the world and that plays right into defense/aerospace stocks. Food security, whether it’s food producers, anything related to agriculture, is an area you ought to be invested in.

You want to be in defensive areas with strong balance sheets, earnings visibility, solid dividend yields and dividend payout ratios. If you follow that you’ll do just fine. I just think you’ll do far better if you have a healthy allocation to long-term bonds and gold. Gold finished 2022 unchanged, in a year when flat was the new up.

In terms of the relative weighting, that’s a personal choice but I would say to focus on defensive sectors with zero or low correlation to GDP, a laddered bond portfolio if you want to play it safe, or just the long bond, and physical gold. Also, the Dogs of the Dow fits the screening for strong balance sheets, strong dividend payout ratios and a nice starting yield. The Dogs outperformed in 2022, and 2023 will be much the same. That’s the strategy for 2023.

Opinions expressed by Entrepreneur contributors are their own.

Crafting a successful product portfolio might sound daunting, and it certainly can be if you’re not well-prepared. But in reality, it doesn’t have to be an overwhelming process. With the right strategies and knowledge, you can create and maintain a strong product portfolio that meets your customers’ needs and stands out from the competition.

In this article, we’ll walk through the steps necessary to craft a successful product portfolio.

Before you start creating your product portfolio, you must do some research and understand the market landscape. Gather as much information as possible about your potential customers, competitors, and industry trends. This will help you develop a compelling product roadmap and ensure your products stay on top of the latest technological advances.

Consider using various research methods such as surveys, interviews, focus groups or observation studies to gain insights into customer needs and preferences. Other data sources include industry reports, competitive analysis, analytics from existing products or customer feedback from existing users. Take the time to analyze all available data points to get a complete picture of the current market environment and identify growth opportunities.

Once you’ve done your research, it’s time to set goals for your product portfolio. Think about what success looks like for each product and establish clear objectives with measurable metrics such as customer satisfaction scores or user engagement numbers. To ensure accuracy, break down objectives into smaller tasks and milestones that can be tracked more easily over time. This will enable teams to assess progress regularly while also allowing flexibility should plans need to change due to unexpected circumstances or new requirements arising mid-way through development cycles.

Consider long-term implications such as future expansion plans or scalability issues when setting goals. This will ensure that products remain relevant in the years ahead, even if certain technologies become obsolete or new solutions enter the market.

Design with intent

When designing product features, take the time to think through their purpose and how they can benefit users. Consider who is using the product and why they may want or need certain features or functionality. This could range from simple usability enhancements for novice users to advanced capabilities for more experienced ones. Keep an eye out for any gaps between user intent and existing features that a new offering in your portfolio could fill. This could open up opportunities for growth while also providing value to users at the same time.

Try to incorporate design elements that resonate with different types of customers — whether visual design styles that match branding guidelines or interactive components that are easily accessible regardless of experience level with a certain type of device or technology platform.

No matter how well-planned a project may be, ultimately, its success hinges on execution. Develop an agile workflow that allows fast iterations while preserving quality standards, making progress visible throughout development cycles. This will enable teams to make quick decisions based on feedback from stakeholders and changing market conditions without compromising overall results.

Utilize feedback from customers and other stakeholders along the way. This can help identify problems before too many resources have already been invested in a particular direction. It also ensures that all points of view are considered when making decisions about feature development or improvement. This will help create products that truly meet customer needs rather than just incorporating features because they sound good on paper but don’t necessarily deliver real value in practice.

Strive for transparency throughout every stage of development. This will build trust amongst stakeholders involved in the project and make it easier for everyone involved to keep track of the progress being made against established milestones & objectives.

A successful product portfolio requires careful planning, research, intentional design and effective execution. By investing the time to do these tasks correctly, you can create products that meet customer expectations and deliver significant value in return. Whether you’re looking to launch a new product or revamp your existing one, following these steps will ensure that your portfolio is strong and positioned for success.

These are tricky times in the stock market, so it pays to look to the best stock-fund managers for guidance on how to behave now. Veteran value investor Bill Nygren belongs in this camp, because the Oakmark Fund OAKMX he co-manages consistently and substantially outperforms its peers.

That isn’t easy, considering how many fund managers fail to do so. Nygren’s fund beats its Morningstar large-cap value index and category by more than four percentage points annualized over the past three years. It also outperforms at five and…

Even during a year in which the S&P 500 index declined 19%, with 72% of its stocks in the red, there were plenty of winners.

Before showing you the list of the best performers in the benchmark index, let’s look at a preview: Here’s how the 11 sectors of the S&P 500 SPX, -0.25%

performed for the year:

Index

2022 price change

Forward P/E

Forward P/E as of Dec. 31, 2021

Energy

59.0%

9.7

11.1

Utilities

-1.4%

18.9

20.4

Consumer Staples

-3.2%

21.0

21.8

Health Care

-3.6%

17.6

17.2

Industrials

-7.1%

18.3

20.8

Financials

-12.4%

11.9

14.6

Materials

-14.1%

15.8

16.6

Real Estate

-28.4%

16.5

24.2

Information Technology

-28.9%

20.1

28.1

Consumer Discretionary

-37.6%

21.3

33.2

Communication Services

-40.4%

14.3

20.8

S&P 500

-19.4%

16.8

21.4

Source: FactSet

Maybe you aren’t surprised to see that the energy sector was the only one to increase during 2022. But it might surprise you to see that despite the sector’s weighted price increase of 59%, its forward price-to-earnings ratio declined and remains very low relative to all other sectors.

It might also surprise you that West Texas Intermediate crude oil CL.1, +2.69%

gave up most of its gains from earlier in the year:

FactSet

The reason investors are still confident in energy stocks is that oil producers have remained cautious when it comes to capital spending. They don’t want to increase supply enough to cause prices to crash, as they did in the run-up to the summer of 2014, after which prices fell steadily through early 2016, causing bankruptcies and consolidation in the industry.

Now the oil companies are focusing on maintaining supply, raising dividends and buying back shares, as Occidental Petroleum Corp.’s OXY, +1.14%

chief executive explained in a recent interview with Matt Peterson. Click here for more about Occidental and the long-term supply/demand outlook for oil.

Best-performing S&P 500 stocks of 2022

Here are the 20 stocks in the benchmark index that rose most during 2022, excluding dividends. Proving that there are always exceptions, not all of them are in the energy sector.

Harris Kupperman, the president of Praetorian Capital, made a couple of interesting calls heading into 2022. He predicted that stocks of the giant tech-oriented companies that led the bull market would be sold off, and that oil prices would continue to rise through the end of 2022.

The first prediction came true, while the second one for oil prices fizzled. After rising to $130 in March, oil prices have fallen back to where they started the year. Then again, that second prediction still could have made you a lot of money because the share prices of oil companies kept rising anyway.

That leads to a new prediction for 2023 and a related stock screen below.

Here’s a chart showing the movement of front-month contract prices for West Texas Intermediate (WTI) crude oil CL.1, -0.62%

since the end of 2021:

FactSet

Even though Kupperman didn’t get his oil price call right, the energy sector of the S&P 500 SPX, -1.20%

was up 60% for 2022 through Dec. 27, excluding dividends. That is the only one of the 11 S&P 500 sectors to show a gain in 2022. And the energy sector is also cheapest relative to earnings expectations, with a forward price-to-earnings ratio of 9.8, compared with 16.7 for the full S&P 500.

WTI pulled back from its momentary peak at $130.50 in early March, but that didn’t reverse the long-term trend of low capital spending by oil and natural gas producers, which has given investors confidence that supplies will remain tight.

Vicki Hollub, the CEO of Occidental Petroleum Corp. OXY, -3.50%

— the best-performing S&P 500 stock of 2022 — said during a recent interview that there was “no pressure to increase production right now,” citing a $40 per barrel break-even point for oil prices.

At the end of November, these 20 oil companies stood out as reasonable plays for 2023 based on expectations for free-cash-flow generation and dividend payments.

For this next screen, we are only looking at ratings and consensus price targets among analysts polled by FactSet.

There are 23 energy stocks in the S&P 500, and you can invest in that group easily by purchasing shares of the Energy Select SPDR ETF XLE, -2.24%.

We can expand the list of large-cap names by looking at the components of the iShares Global Energy ETF IXC, -1.91%,

which holds all the energy stocks in the S&P 500 plus large players based outside the U.S.

Prices on the tables in this article are in local currencies.

IXC holds 51 stocks. To expand the list for a stock screen, we added the energy stocks in the S&P 400 Mid Cap Index MID, -1.24%

and the S&P Small Cap 600 Index SML, -1.89%

to bring the list up to 91 companies, which we then pared to 83 covered by at least five analysts polled by FactSet.

Here are the 20 companies in the list with at least 75% “buy” or equivalent ratings that have the most upside potential over the next 12 months, based on consensus price targets:

Following a sharp and sustained rise in interest rates, U.S. stocks have taken a broad beating this year.

But 2023 may bring very different circumstances.

Below are lists of analysts’ favorite stocks among the benchmark S&P 500 SPX,

the S&P 400 Mid Cap Index MID

and the S&P Small Cap 600 Index SML

that are expected to rise the most over the next year. Those lists are followed by a summary of opinions of all 30 stocks in the Dow Jones Industrial Average DJIA.

Stocks rallied on Dec. 13 when the November CPI report showed a much slower inflation pace than economists had expected. Investors were also anticipating the Federal Open Market Committee’s next monetary policy announcement on Dec. 14. The consensus among economists polled by FactSet is for the Federal Reserve to raise the federal funds rate by 0.50% to a target range of 4.50% to 4.75%.

A 0.50% increase would be a slowdown from the four previous increases of 0.75%. The rate began 2022 in a range of zero to 0.25%, where it had sat since March 2020.

A pivot for the Fed Reserve and the possibility that the federal funds rate will reach its “terminal” rate (the highest for this cycle) in the near term could set the stage for a broad rally for stocks in 2023.

Wall Street’s large-cap favorites

Among the S&P 500, 92 stocks are rated “buy” or the equivalent by at least 75% of analysts working for brokerage firms. That number itself is interesting — at the end of 2021, 93 of the S&P 500 had this distinction. Meanwhile, the S&P 500 has declined 16% in 2022, with all sectors down except for energy, which has risen 53%, and the utilities sector, which his risen 1% (both excluding dividends).

Here are the 20 stocks in the S&P 500 with at least 75% “buy” or equivalent ratings that analysts expect to rise the most over the next year, based on consensus price targets:

Most of the companies on the S&P 500 list expected to soar in 2023 have seen large declines in 2022. But the company at the top of the list, EQT Corp. EQT,

is an exception. The stock has risen 69% in 2022 and is expected to add another 62% over the next 12 months. Analysts expect the company’s earnings per share to double during 2023 (in part from its expected acquisition of THQ), after nearly a four-fold EPS increase in 2022.

Shares of Amazon.com Inc. AMZN

are expected to soar 50% over the next year, following a decline of 46% so far in 2022. If the shares were to rise 50% from here to the price target of $136.02, they would still be 18% below their closing price of 166.72 at the end of 2021.

You can see the earnings estimates and more for any stock in this article by clicking on its ticker.

Click here for Tomi Kilgore’s detailed guide to the wealth of information available for free on the MarketWatch quote page.

Mid-cap stocks expected to rise the most

The lists of favored stocks are limited to those covered by at least five analysts polled by FactSet.

Among components of the S&P 400 Mid Cap Index, there are 84 stocks with at least 75% “buy” ratings. Here at the 20 expected to rise the most over the next year:

Among companies in the S&P Small Cap 600 Index, 91 are rated “buy” or the equivalent by at least 75% of analysts. Here are the 20 with the highest 12-month upside potential indicated by consensus price targets:

Despite worries about inflation and an impending recession, there is at least one sign that some bullish market technical analysts might latch onto.

An upbeat golden cross appears to be forming in the Dow Jones Industrial Average DJIA, -0.90%,

more than nine months after a bearish death cross formed back in March, as the hawkish agenda of the Federal Reserve shattered bullishness on Wall Street.

A golden cross occurs when the 50-day moving average for an asset price trades above the 200-day MA, while a death cross, comparatively, is when the 50-day falls below the long-term average.

The 50-day moving average for the Dow stands at 32,200.32, at last check Friday afternoon, while the 200-day sits at 32,460.71, a roughly 260-point difference that could be traversed in the coming week or two, based on its current trajectory.

FactSet

A golden cross would mark the first for the Dow industrials since 2020 of August, according to Dow Jones Market Data.

The bullish chart formation also would appear at an odd time for investors, with an apparent uptrend materializing in the stock market, even as the threat of a recession in 2023 grows.

On top of that, MarketWatch columnist Mark Hulbert concludes that the U.S. stock market on average has performed no better in the wake of a golden crosses as it did at other times.

In many cases, a golden cross can help put an asset’s move into perspective, however, they tend to be well telegraphed.

Interestingly, the recession is also being widely predicted and some don’t think investors are getting the memo. As BlackRock notes, investors aren’t reflecting the damage that is to come, particularly as earnings expectations from American companies are right-sized.

So, it might be worth it for investors to take any golden crosses in assets with a grain of salt.

So far, the Dow industrials have outperformed over the past three months, up about 5%, compared with a decline of 2.5% for the S&P 500 SPX, -0.73%

and an 8.2% drop for the Nasdaq Composite COMP, -0.70%.

Over the past three months, the Dow industrials have recent in aggregate on the back of gains in shares of Caterpillar CAT, -1.56%,

Boeing Co. BA, +0.20%

Merck & Co. MRK, -1.86%,

IBM IBM, -0.47%

and Travelers Cos. TRV, -1.10%.

For the year so far, the Dow is down 7%, while the S&P 500 is off 17% and the Nasdaq is down nearly 30%.