[ad_1]

Meet the Suspicious 8: Dividends Over 6% With Plenty of Problems

[ad_2]

[ad_1]

I recently graduated with my master’s degree and am seeking full-time employment at age 53. I want to know what is the best way to invest some of my earnings when I begin receiving a paycheck. I expect to have an annual salary of between $80,000 and $90,000.

For religious reasons, I cannot invest to earn interest, but business-related ventures such as stocks are acceptable. I am planning to set aside up to $1,000 per month for investment purposes, so that I can build some retirement funds. What are my options?

First-Time Investor

MarketWatch illustration

Congratulations on your master’s degree. You have already made the best investment you can make — one in yourself, your education and your future. It takes patience, guts and stamina to go back to college in your 50s, and you should be very proud. You were one of about 505,000 students in college ages 50 and over, representing less than 4% of the student population.

Given your faith, CDs and high-yield savings accounts are ruled out. A letter writer recently asked me where he should start looking to invest his $50,000 life savings, and I pointed him in the “make interest off your cash” direction, particularly given the recent rise in interest rates. That won’t work for you, but the good news is that you do have many options.

There are investment vehicles for you. In fact, the Accounting and Auditing Organization for Islamic Financial Institutions sets guidelines for investing in accordance with the Sharia religious code, including rules around companies that derive a percentage of their profits from tobacco and alcohol products. And, yes, it also regards interest as unjust and exploitative.

Saturna Capital has mutual funds that follow Islamic principles. The Amana Income Fund AMANX, which focuses on current income and the preservation of capital, has had an average annual five-year return of 8.8% for investor shares, slightly lower than the 9.9% average return for the S&P 500

SPX

over the same period with dividends reinvested. I suggest this as a guidepost rather than a recommendation.

Similarly, the Knights of Columbus assets are managed by Knights of Columbus Asset Advisors in accordance with Catholic moral principles, which are distilled to six main tenets: “protecting human life, promoting human dignity, reducing arms production, pursuing economic justice, protecting the environment [and] encouraging corporate responsibility.”

Related: How do I know if my ESG investments are doing any good?

Of course, investing along religious principles — similar to ESG investment, which takes environmental, social, and corporate-governance factors into account when deciding what to do with your money — is fraught with complications, contradictions and problems with transparency. Regulators are cracking down on vehicles that “greenwash” their ESG credentials.

A major report by the Organization for Economic Cooperation and Development, an intergovernmental organization with 38 member nations, found that ESG ratings vary strongly depending on the provider, as they commonly use different measures, indicators, metrics, data and qualitative judgments to make decisions about funds and companies.

“Moreover, returns have shown mixed results over the past decade, raising questions as to the true extent to which ESG drives performance,” the OECD said. “This lack of comparability of ESG metrics, ratings, and investing approaches makes it difficult for investors to draw the line between managing material ESG risks within their investment mandates.”

You have many funds to choose from. If you’re Catholic, you could look into the Global X S&P 500 Catholic Values ETF

CATH

; the LKCM Aquinas Catholic Equity Fund AQEIX; or Ave Maria, which offers mutual funds for growth AVEGX, value AVEMX and bonds AVEFX AVEFX. You can read more here. Investing based on religious, moral or ethical principles doesn’t guarantee a satisfactory return.

It’s not too late to start investing at 53. With the advice of a financial adviser, your risk profile may need regular adjusting, based on your age and tolerance. But you may work into your 70s and may live into your 80s or 90s, and you will want to find myriad ways to build your wealth throughout your retirement. Cash-hoarding typically gets outdone by inflation.

You may find a job with a 401(k) and an employer match, meaning your employer will contribute an additional sum toward your retirement based on the amount you are contributing every month. You may also consider an IRA. Both account types have “catch-up” contributions for people who are over 50. Annual IRA contribution limits for 2023 are $6,500 for people under 50, but $7,500 for those 50 and older.

You can also use pretax dollars for health savings accounts, which are used to offset the burden of high-deductible healthcare plans. With the latter, you pay a lower premium, but you will be saddled with higher out-of-pocket expenses for medical services should you require them. You can contribute up to $4,150 to an HSA for 2024, up from $3,850 this year.

As for right now? Pay off your credit cards. Don’t let high-interest debt trap you. Warren Buffett said one of the best investments he ever made was buying his Omaha, Neb., home for $31,500 in 1958. It’s worth $1.4 million today. He has said he may have put that money to better use if he had rented instead, but owning your own home will solidify your financial position in retirement.

Investing $1,000 a month may be ambitious. But thinking in the medium to long term — and knowing this is a marathon rather than a sprint, even at 53 — is half the battle. With compounding, or making money off your principal and the increase in value of your initial investment, you could have more than $120,000 in 10 years, and over $600,000 in 30 years.

Bravo on this new chapter. Take it one day, one week and one month at a time, and enjoy your life.

You can email The Moneyist with any financial and ethical questions at qfottrell@marketwatch.com, and follow Quentin Fottrell on X, the platform formerly known as Twitter.

Check out the Moneyist private Facebook group, where we look for answers to life’s thorniest money issues. Post your questions, tell me what you want to know more about, or weigh in on the latest Moneyist columns.

The Moneyist regrets he cannot reply to questions individually.

Previous columns by Quentin Fottrell:

‘I’m tired of feeling like I am in hell’: My boss tears into me almost daily. He says I’m worthless. What can I do?

I earn $210,000 and I’m 59. My wife and I want to move to Hawaii. Is it too late to get a mortgage?

[ad_2]

[ad_1]

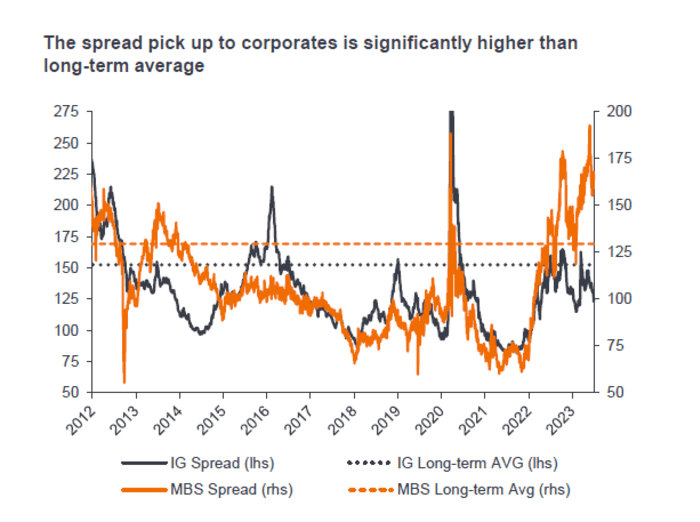

U.S. homes may be wildly unaffordable for first-time buyers, but mortgage bonds backed by those same properties could be dirt cheap.

Shocks from the Federal Reserve’s dramatic rate increases have walloped the $8.9 trillion agency mortgage-bond market, the main artery of U.S. housing finance for almost the past two decades.

Spreads, or compensation for investors, have hit historically wide levels, even through the sector is underpinned by home loans that adhere to the stricter government standards set in the wake of the subprime-mortgage crisis.

Bond prices also have tumbled, sinking from a peak above 106 cents on the dollar to below 98, despite guarantees that mean investors will be fully repaid at 100 cents on the dollar.

Bloomberg, Goldman Sachs Global Investment Research

“It’s really, really struggled,” Nick Childs, portfolio manager at Janus Henderson Investors, said of the agency mortgage-bond market during a Thursday talk on the firm’s fixed-income outlook.

Yet Childs and other investors also see big opportunities brewing. While mortgage bonds have gotten cheaper with the sector’s two anchor investors on the sidelines, the stalled housing market should breed scarcity in the bonds, which could help lift the sector out of a roughly two-year slump.

Prices have tumbled since rate shocks hit, but also since the Fed continued winding down its large footprint in the sector by letting bonds it accumulated to help shore up the economy roll off its balance sheet.

Banks awash in underwater securities have pulled back too. The repricing of similar bonds helped hasten the collapse of Silicon Valley Bank in March.

“Banks have been not only absent, but selling,” said Childs, who helps oversee the Janus Henderson Mortgage-Backed Securities exchange-traded fund

JMBS,

an actively managed $2 billion fund focused on highly rated securities with minimal credit risk.

“But we’re moving into an environment where supply continues to dwindle,” he said, given anemic refinancing activity and the dearth of new home loans being originated since 30-year fixed mortgage rates topped 7%.

The bulk of all U.S. mortgage bonds created in the past two decades have come from housing giants Freddie Mac

FMCC,

Fannie Mae

FNMA,

and Ginnie Mae, with government guarantees, making the sector akin to the $25 trillion Treasury market. But unlike investors in Treasurys, investors in mortgage bonds also earn a spread, or extra compensation above the risk-free rate, to help offset its biggest risk: early repayments.

While homeowners typically take out 30-year loans, most also refinanced during the pandemic rush to lock in ultralow rates, instead of continuing to make three decades of payments on more expensive mortgages. If someone refinances, sells or defaults on a home, it leads to repayment uncertainty for bond investors.

“To put this another way, the biggest risk to mortgages is now off the table, yet spreads are at or near historic wides,” said Sam Dunlap, chief investment officer, Angel Oak Capital Advisors, in a new client note.

That spread is now far above the long-term average, topping levels offered by relatively low-risk investment-grade corporate bonds.

Janus Henderson Investors

Agency mortgage bonds typically are included in low-risk bond funds and can be found in exchange-traded funds. While they have been hard hit by the sharp selloff in long-dated Treasury bonds

BX:TMUBMUSD10Y

BX:TMUBMUSD30Y,

there has also been hope that the worst of the storm could be nearly over.

Goldman Sachs credit analysts recently said they favored the sector but warned in a weekly client note that it still faces “high rate volatility and a dearth of institutional demand.”

As evidence of the U.S. bond selloff, the popular iShares 20+ Year Treasury Bond ETF

TLT

recently sank to its lowest level in more than a decade. It also was on pace for a negative 10% total return on the year so far, according to FactSet. Janus Henderson’s JMBS ETF was on pace for a negative 2.7% total return on the year through Friday.

“Frankly, why they fit portfolios so well is that because the government backs agency mortgages, there is no credit risk,” Childs said. “So if a borrower defaults, you get par back on that. It just comes through as a typical payment.”

[ad_2]

[ad_1]

Some say it’s the fear of stagflation.

Some say it’s chaos on Capitol Hill.

Some say it’s turmoil in the Middle East.

But we all know the real reason the stock market is so crummy, right?

It’s October! Of course stocks are down!

It is a bizarre, inexplicable, and yet undeniable, fact that, throughout history, Wall Street has produced almost all of its gains during the winter months of the year — from Nov. 1 to April 30. It is an even more bizarre, inexplicable and yet undeniable fact that the rest of the world’s stock markets have done the same thing.

The so-called summer months, meaning the half of the year from May 1 to Halloween, have generally given you bupkis or worse.

Around the world, over the course of centuries of recorded financial history, stock-market returns have averaged four full percentage points higher from November to April than from May to October, report researchers Ben Jacobsen at Tilburg University and Cherry Yi Zhang at Nottingham University’s Business School in China. This so-called Halloween Effect seems “remarkably robust,” they concluded, after studying the financial returns of 114 different countries going back as far as they could find reliable monthly data — starting with the stock market in 1693 London.

Even more extreme: In the 65 countries for which they had extensive data both about the stock market and about short-term interest rates, it’s fair to say you would have been better off selling your stocks on May 1, putting the money in the bank, then taking it out again at the end of October and buying back your stocks (ignoring fees and taxes, of course).

“In none of the 65 countries for which we have total returns and short-term interest rates available — with the exception of Mauritius — can we reject a Sell in May effect based on our new test. Only for Mauritius do we find evidence of significantly positive excess returns during summer.”

Italics mine. Mauritius?

The Dow Jones Industrial Average

DJIA

is now lower than it was at the end of April. So is the Russell 2000

RUT

index of small-cap U.S. stocks. The benchmark international stock index, the MSCI EAFE, is down about 6%. Japan’s Nikkei

NIY00,

is slightly up, as the yen has tanked.

The S&P 500

SPX

is hanging on to a small gain, but that is only because of the early summer gains of a few tech titans. The average S&P stock is down about 2.5% since the end of April — while an investment in no-risk Treasury bills is up more than 2%.

Meanwhile, let the record show that, over the same period, according to the record keepers at MSCI, the stock market in Mauritius is up 12%.

Booyah!

Every time I write about this Halloween or “sell in May” effect, I make the same two points, and I make no apologies for repeating them here, because they are unavoidable.

The first is that, every spring, after looking at this data, I am tempted to sell all my stocks at the end of April, and every year I don’t, because I think it’s absolutely ridiculous. (And someone on Wall Street who is much smarter than me usually persuades me not to.) And most years I end up kicking myself for not doing it.

The second is to recall the old economists’ joke: “I don’t care if it works in practice! Does it work in theory?” Selling in May — or, sure, the Halloween Effect — has absolutely no reason that anyone can find for working in theory. But apparently, it works in practice — which is pretty much where we are now.

Does this mean stocks are going to rally? It’s anyone’s guess. It would be crazy if it were that simple. But, then, the whole Halloween Effect is crazy.

If history is any guide, now is the time to buy stocks, not sell them, because the next six months are likely to be the time when they make you money. And if history isn’t any guide, well, aren’t we all sunk anyway?

[ad_2]

[ad_1]

Nvidia Corp.’s revenue doubled while its cost of goods barely crept up, so there must be something fishy, right? A company is using their Nvidia graphics processing chips as collateral for billions in loans — that doesn’t sound right, does it?

As Nvidia NVDA shares fell 3.1% to close at $470.61 on Wednesday, Bernstein analyst Stacy Rasgon must have been hearing from clients all day who were worried after reading the most recent conspiracy theory on why Nvidia’s 222% year-to-date stock gain must somehow be fixed.

“Recently…

[ad_2]

[ad_1]

U.S. exchange-traded funds that invest in Chinese stocks notched their best day in a month after China ramped up its efforts to support the country’s flagging currency as investors’ concerns over the economic weakness persist.

The People’s Bank of China said Friday it will lower the amount of foreign-exchange deposits financial institutions are required to hold for the first time in 2023, a move seen as a bid to shore up the Chinese yuan, which has tumbled this year as the world’s second largest economy has faltered due to a property-market downturn, sluggish domestic consumption, and the ballooning local government debt pile.

The Invesco Golden Dragon China ETF

PGJ,

which tracks the American depositary shares of companies based in China, rose 3% on Friday, while the KraneShares CSI China Internet ETF

KWEB,

which offers exposure to Chinese software and information technology stocks, gained 3.5%. The iShares MSCI China ETF

MCHI

advanced nearly 2.2% and the SPDR S&P China ETF

GXC

surged 2%, according to FactSet data.

The iShares MSCI China ETF and the KraneShares CSI China Internet ETF booked their biggest daily percentage advance since August 3, according to FactSet data.

China’s central bank will cut the foreign-exchange reserve requirement ratio to 4% from 6% beginning Sept. 15. The move is expected to increase the supply of foreign currencies available in local markets, making the Chinese yuan more appealing for domestic investors.

See: China’s central bank to cut FX reserve ratio

Based on about $822 billion foreign-exchange deposits in July, the 200-basis-point cut in the reserve requirement ratio could release about $16 billion, which will improve the supply of the U.S. dollar onshore, and could move spot USDCNY lower, said strategists at Citigroup led by Johanna Chua, chief Asia economist.

“In a broader picture, this can be also seen as part the current round of accelerated policy rollout which works more directly on asset markets. If the accelerated pace [of policy rollout] continues, it may help stabilize sentiment to some extent and prevent outsized bearish moves on China risk assets including the RMB FX,” they wrote in a Friday note.

The onshore yuan

USDCNY,

weakened around 1.7% against the dollar in August, extending its losses for the year to nearly 5%, according to FactSet data. The offshore yuan

USDCNH,

was trading at 7.27 per dollar Friday afternoon.

See: Chinese Property Stocks Gain on Stimulus Measures

Friday’s change to reserve requirement ratio came a day after Chinese authorities announced that homebuyers’ minimum down payment will be reduced to 20% for first-time home purchases, and 30% for second-home purchases nationwide, according to a joint statement from the People’s Bank of China and National Administration of Financial Regulation late Thursday.

Currently, homebuyers in largest cities such as Beijing and Shanghai have a 30% down payment ratio for first homes, and 40% or more for second homes.

Separately, big banks, such as Industrial & Commercial Bank of China

601398,

and Bank of China

601988,

have said they would cut their one-year yuan deposit rate by 10 basis points to 1.55% and their two-year yuan deposit rate by 20 basis points to 1.85%. The banks also plan to cut mortgage rates to boost consumption and aid the troubled property sector.

The broader U.S. stock market finished mostly higher on Friday as traders weighed the latest jobs report to conclude the final trading day before the Labor Day holiday weekend. The S&P 500

SPX

was up 0.2%, while the Dow Jones Industrial Average

DJIA

advanced 0.3% but the Nasdaq Composite

COMP

ended nearly flat.

[ad_2]

[ad_1]

Investors should think twice before picking an actively managed mutual fund according to its style category. By “style category,” I’m referring to the widely used method of grouping mutual funds according to the market-cap of the stocks they invest in and where those stocks stand on the spectrum of growth-to-value.

This matrix traces to groundbreaking research in 1992 by University of Chicago professor Eugene Fama and Dartmouth College professor Ken French, and has since been popularized by investment researcher Morningstar in the form of its well-known style box.

In urging you to think twice before picking a fund based on this matrix, I’m not questioning the existence of important distinctions between the various styles. Fama and French’s research convincingly showed that there are systematic differences between them. My point is that there also are huge differences within each style as well. You can pick a style that outperforms all others on Wall Street and still lose a lot of money, just as you can pick the worst-performing style and turn a huge profit.

This points to the two types of risk you face when picking an actively managed fund. You have the risk associated with the fund’s style (category risk) and you also have the risk associated with the particular stocks that the fund’s manager selects (so-called idiosyncratic risk). Idiosyncratic risk often overwhelms category risk, especially over shorter periods.

To illustrate, consider the midcap-growth style. As judged by the Vanguard Mid-Cap Growth ETF

VOT,

this style produced a 28.8% loss in 2022. Yet, according to Morningstar Direct, the best-performing actively managed midcap-growth fund last year produced a gain of 39.5%, while the worst performer lost 67.0%.

This best-versus-worst performance spread of over 100 percentage points is illustrated in the accompanying chart. Notice that the comparable spread was almost as wide for many of the other styles as well. Though I haven’t done the research to compare 2022’s spreads with those of other calendar years, I have no reason to expect that they on average were any lower.

“ The only way to eliminate idiosyncratic risk when investing in particular styles is to invest in an index fund.”

The only way to eliminate idiosyncratic risk when investing in particular styles is to invest in an index fund benchmarked to the style in question. If you are enamored of a particular fund manager and willing to bet he will significantly outperform the category average, just know that you also incur the not-significant idiosyncratic risk that the fund will lag by a large amount.

The bottom line? By investing in an actively managed fund in a style category, you will be incurring the risk not only of that category itself but also the not-insignificant idiosyncratic risk of that particular fund. Fasten your seatbelt if that’s the path you take.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com

[ad_2]

[ad_1]

With the release this weekend of the new “Barbie” movie starring Margot Robbie and Ryan Gosling, there’s growing attention being paid to the world of Barbie collectibles. As in the hundreds of dolls that have been released over the years, to say nothing of such accessories as Barbie outfits and furniture.

But there’s one collectible above all — the holy grail of Barbies, if you will. We’re referring to Barbie No. 1, the first doll ever released by Mattel to bear the Barbie name, dating from 1959.

Barbie fanatics speak of it in reverent terms. “I lost sleep over this doll,” one collector said in a YouTube

GOOGL,

GOOG,

video that documented the arrival and unboxing of a Barbie No. 1.

Needless to say, collectors will pay a pretty penny for a Barbie No. 1. Prices can easily reach $10,000-plus, according to Barbie experts. The original doll sold for about $3, but there’s a Barbie No. 1 doll on eBay

EBAY,

currently going for $25,000.

But before you plunk down five figures for an investment-grade doll, we figured you might want to know a little more about this one-of-a-kind Barbie. Here goes:

Obviously, it’s all about being the first of its kind, not unlike a baseball player’s rookie card (the 1952 Mickey Mantle card is often considered the holy grail of sports collectibles, though that can sell for millions of dollars). It’s also about rarity. Experts say around 300,000 to 350,000 of those debut Barbies were sold in 1959, but the number of Barbie No. 1s that survived throughout the years — dolls are sold as toys, after all, not necessarily collectibles — is considerably less.

(Mattel

MAT,

reportedly now releases about 60 million Barbies annually, but the company didn’t respond to a MarketWatch request for comment and information.)

There’s also something to be said for No. 1’s distinct look, marked by what veteran Barbie appraiser Dr. Lori Verderame describes as its “deep profile” with a protruding nose and high forehead. It’s a design very much inspired by the German-made Bild Lilli dolls that intrigued Barbie creator Ruth Handler.

Red-headed Barbie No. 1s are known to exist. Marl Davidson, a Barbie dealer based in Bradenton, Fla., says she once sold one for $50,000, and perhaps the holiest of holy grails is a salesman’s Barbie sample case dating from the doll’s early years. Davidson says she believes only two or three are around. And one surfaced? “It could go for $1 million,” she says.

As with almost any collectible category, it’s all about condition. Barbie buyers are looking for a No. 1 that’s as close to mint condition as possible, with all the original items — namely, the box, black stand, sunglasses, shoes, brochure and zebra-striped swimsuit. (There are also outfits and accessories dating from Barbie’s early years, but these were sold separately; Verderame says a popular outfit from this period can sell for $150 to $200.)

Ironically, if the Barbie has stayed in the original box, it may affect the condition — Verderame explains that the packaging is acidic so it can “damage the piece over time,” but she says collectors still “want it in the box.”

Then, there’s the hair color. The original Barbie came in both blonde and brunette versions. Verderame says the blondes are generally more sought after since that’s what most people think of as the Barbie classic. But Davidson says brunettes can actually have value since there were fewer made of them. Then again, she says, the collectors “who can afford it will have one of everything.”

There are various elements that will signify an original Barbie — most notably, a marking on the doll’s, um, right buttock (this also applies to later Barbies, though). Also look for holes in the feet and what the Doll Reference site describes as “tight curly bangs,” among other identifiers. It’s worth keeping in mind that you might find an original No. 1 doll, but with other parts that are not original — say, a replacement stand.

It’s soaring because of the movie, Verderame says. She notes that Barbie No. 1s that went for $10,000 as recently as three months ago are now selling in the $15,000-$25,000 range. Verderame anticipates the market will cool off after the fervor for the Warner Bros.

WBD,

film dies down. But Davidson remains bullish on Barbie’s longer-term prospects because of the doll’s iconic appeal: “The price can only go up,” she says.

Davidson says collectors can also consider Barbie No. 3 as a collectible. It’s a very early model, but it has a far more approachable price — Davidson says collectors can find one between $1,000 and $3,000.

If you want something way more affordable that still has potential to appreciate, Verderame says to consider iconic Barbies from the 1990s and 2000s that are currently selling for between $50 and $150.

But if you insist on a Barbie No. 1, Davidson says you can always buy one in lesser condition for a lesser price. Still, even a bald Barbie No. 1 won’t come cheap, she warns. “It’s going to go for a couple of grand,” she says.

[ad_2]

[ad_1]

Why isn’t gold dead yet?

It hasn’t served a vital economic function since the government stopped treating it as money back in 1971. Actually, you could argue it stopped being necessary long before that.

Yes, some people prefer it in jewelry. It is used in some technological equipment, and sometimes, still, in dentistry. But so what? According to authoritative data from the World Gold Council, even all those uses only account for about half of the world’s supply each year. Logically, this should mean that there is a gigantic glut of gold and that its price would be in free fall.

But it isn’t. Gold is beating U.S. stocks and bonds this month. And this isn’t even a rarity. I’ve run some numbers and have found a couple of things that could be very important to retirees, and for all of us suckers saving for retirement.

Even though, according to traditional financial theory, they really make no sense at all.

Don’t miss: Gold headed for best week since March after U.S. inflation reports

Also see: Why gold will beat the stock market in the coming weeks

The first thing is that over the past century including some gold in your portfolio alongside stocks and bonds has genuinely added value. It has produced higher average returns, less volatility and fewer of those disastrous “lost decades” where your portfolio ended up whistling Dixie.

The second thing is that this peculiarity has been showing no signs of letting up in recent years or decades — even though, if anything, gold makes even less sense today than it used to.

Let me explain.

As usual, I’ve tapped the excellent database maintained by the NYU Stern School of Business, which tracks asset values going back to 1928.

Over that period, a conventional so-called balanced portfolio invested 60% in the S&P 500

SPY,

index of large-company stocks and 40% in U.S. 10-year Treasury bonds

TMUBMUSD10Y,

has generated an average return of 4.9% a year in “real” terms, meaning above inflation.

A portfolio that’s 60% invested in the S&P 500, 30% in the bonds and 10% in gold

GC00,

earned a slightly higher average, 5.1% a year in real terms. But the volatility was lower: The portfolio that included the gold had a lower standard deviation of returns, and a much higher “median” return, meaning the middlemost return if you ranked all the years from best to worst. The portfolio including gold beat the traditional one by five full percentage points in total over the typical 10-year period, and failed to keep up with inflation for 10 years on only five occasions — half as often as the portfolio consisting exclusively of stocks and bonds.

Nor is this just about olden times. The portfolio including 10% gold has beaten the traditional 60/40 by an average of 0.4 percentage point a year since President Richard Nixon finally killed the gold standard in 1971. And it has beaten the traditional portfolio by the same amount, an average of four-tenths of a percentage point, so far this millennium. (The 60/40 portfolio has done better if you start measuring only in 1980, as that ignores the golden 1970s but includes the long bear market for gold of the 1980s and 1990s.)

And gold has added value in five of the last seven years (while in the other two it was effectively a tie).

It’s not so much that gold is a great long-term investment on its own. It’s that gold has seemed to shine when others, specifically stocks and bonds, have failed. And it still does. It held up during the crash of 1929-32. But it also held up during the crash in 2002. And in 2008. And 2020.

A financial expert told me this was “hindsight bias.” But so is most financial analysis.

When your financial adviser tells you what you might reasonably expect from large stocks, small stocks, international stocks, real estate and so forth in the decades ahead, he or she is basing that on history. (In some cases this has been downright hilarious, as when advisers said you should still expect “average” historical returns of 5% a year from Treasurys, even when they had only a 2% yield.)

I’m danged if I know why. But so far this year, once again, you’ve been better off in a portfolio of 60% stocks, 30% bonds and 10% gold than in just 60% stocks and 40% bonds. Make of it what you will.

[ad_2]

[ad_1]

If you’re a retiree and you’re trying to square the circle of rising costs, longer lifespans, more expensive medical care and turbulent markets, don’t be afraid to run the numbers on your biggest investment.

That would be your home — if you own it.

U.S. house prices are now so high that it is almost impossible for seniors not to ask themselves the obvious question: “Should we cash in, invest the money, and rent?”

Right now the average U.S. house price is nearly $360,000. That’s about a third higher than just a few years ago, before the COVID-19 pandemic. The lockdowns, the panic, the stimulus checks and 2.5% mortgage rates have all passed into history. But the sky-high prices remain — for now.

At these levels, analysts at Realtor.com — which, like MarketWatch, is owned by News Corp.

NWSA,

— say that in 45 out of 50 major U.S. metropolitan areas it is cheaper to rent than it is to buy a starter home. The Atlanta Federal Reserve Bank says national housing affordability is abysmal — about where it was in 2006 and 2007, during the big housing bubble.

There is a similar story for seniors. Federal data show that the average U.S. house price is now nearly 17 times the average annual Social Security benefit — an even higher ratio than it was in August 2008, just before Lehman Brothers collapsed. At that juncture, the average house price was 15 times higher.

S&P/Case-Shiller

Our simple chart, above, compares average U.S. home prices with average U.S. rents, going back to 1987. (The chart simply shows the ratio, indexed to 100.) The bottom line? House prices are very high at the moment compared with rents — again, prices are about where they were in 2006-07.

And the two must run in tandem over the long term, because the economic value of owning a house is not having to pay rent to live there.

If there are times when, in general, it makes more financial sense for seniors to rent than to own, this has to be one of those.

Seniors who own their own homes may think high interest rates on new mortgages don’t affect them. They most likely either already have a mortgage at a lower, older rate or they’ve paid off their home loan. But if you want to sell, you’ll almost certainly be selling to someone who needs a mortgage.

If borrowing costs drive down real-estate prices, seniors who hold off on selling may miss out on gains they may never see again. After the last housing peak, in 2006, it took a full decade for prices to recover fully. Those who sold when the going was good had the chance to buy lifetime annuities at excellent rates or to invest in stocks and bonds that overall rose about 80% over the same period.

As I mentioned recently, there is a broad basket of real-estate trusts on the stock market that are publicly traded landlords. You can sell your home and invest in thousands at a click of a mouse.

But should you?

Incidentally, there is also an exchange-traded fund that invests in residential REITs, Armada’s Residential REIT ETF

HAUS,

though in addition to single-family homes and apartment-complex operators, about 25% of the fund is invested in companies involved in manufactured-home parks and senior-living facilities.

For each person, the math will be different, and there are a number of questions you need to ask. Where do you want to live? How much would you get if you sold your house? How much would you pay in taxes? How much would it cost to rent the right place? Do you want to leave a property to your heirs? And what would be the costs of moving — both financial and emotional?

The conventional wisdom is that you should own your home in retirement.

“I would advise any and all retirees against renting if at all possible,” says Malcolm Ethridge, a financial planner at CIC Wealth in Rockville, Md. “You need your costs to be as fixed as possible during retirement, to match your income being fixed as well. If you choose to rent, you’re leaving it up to your landlord to determine whether and by how much your No. 1 expense will increase each year. And that makes it very tough to determine how much you are able to allocate toward everything else in your budget for the month.”

A key point here, from federal data, is that nationwide rents have risen year after year, almost without a break, at least since the early 1980s. They even rose during the global financial crisis, with just one 12-month period where they fell — and then by only 0.1%.

“My general advice for clients is that owning a home with no mortgage in retirement is the best scenario, as housing is typically the highest cost we pay monthly,” says Adam Wojtkowski, an adviser at Copper Beech Wealth Management in Mansfield, Mass. “It’s not always the case that it works out this way, but if you can enter retirement with no mortgage, it makes it a lot easier for everything to fall into place, so to speak, when it comes to retirement-income planning.”

“Renting comes with a lot of risk,” says Brian Schmehil, a planner with the Mather Group in Chicago. “If you rent, you are subject to the whims of your landlord, and a high inflationary environment could put pressure on your finances as you get older.”

But it’s not always that simple.

“With housing costs as high as they are now though, renting may be a viable solution, at least for the moment,” says Wojtkowski. “We don’t know what the housing-market trends will be going forward, but if someone is waiting for a housing-market crash before they move, they could very likely be waiting for a long time. We just don’t know.”

“Any decision comes with pros and cons,” says Schmehil. “Selling when your home values are historically high and renting allows you to capture the equity in your home, which is usually a retiree’s largest or second-largest financial asset. These extra funds allow you to spend more money on yourself in retirement without having to worry about doing a reverse mortgage or selling later in retirement, when it may be harder for you to do so.”

Renting also allows you to be more flexible about where you live, for example nearer your children or grandchildren, he adds.

And as any experienced property owner knows, renting also brings another benefit: You no longer have to do as much work around the house.

“Renting is great in that you don’t need to maintain a residence,” says Ann Covington Alsina, a financial planner running her own firm in Annapolis, Md. “If the dishwasher breaks or the roof leaks, the landlord is responsible.”

Wojtkowski agrees, noting that many people no longer want to spend time mowing the lawn or shoveling snow in retirement. “Ultimately, one of the things that I’ve seen most retirees most concerned with is eliminating the general upkeep [and] maintenance of homeownership in retirement,” he says.

Several planners — including Covington Alsina and Wojtkowski — note that one alternative to selling and renting is simply downsizing. This can free up capital, especially when home prices are high, like now, without leaving you exposed to rising rents.

Many baby boomers have been doing exactly that.

Meanwhile, I am reminded of my late friend Vincent Nobile, who — after a long and fruitful life owning homes and raising a family — found himself widowed and alone in his 80s. He rented a small cottage on a New England sound and said how glad he was that he never had to worry about maintaining the roof or the appliances, or fixing the plumbing or the heating, or any one of a thousand other irritations. Or paying property taxes — which go down even more rarely than rents.

When the regular drives to Boston got too onerous, he moved into the city and rented there. And he was glad to do it. The money he had made was all in investments — a lot less hassle both for him and his heirs.

I once asked him if he would prefer to own his own home. He shook his head and laughed.

[ad_2]

[ad_1]

If there were no tax cheats in America, there would be no Social Security crisis. Benefits could be paid, and payroll taxes kept the same, for the next 75 years.

That’s not me talking. That’s math. It comes from the number crunchers at the Social Security Administration and the Internal Revenue Service.

And it explains why those of us who support Social Security should be pounding the table in outrage over one clause of the Biden-McCarthy debt ceiling deal: The part where the president has to retreat from his crackdown on tax cheats just so McCarthy and the House Republicans would agree to prevent America defaulting on its debts.

It’s just two years since the administration got into law an extra $80 billion for the IRS to beef up enforcement. That was supposed to include hiring an estimated 87,000 IRS agents.

OK, so nobody likes paying taxes and nobody likes the IRS. Cue the inevitable critiques of an IRS tax “army,” and so on. But this isn’t about whether taxes should be higher or lower. It’s about whether everyone should pay the taxes that they owe.

After all, if we’re going to cut taxes, shouldn’t they apply to those of us who obey the laws as well as those who don’t? Or do we just support the “Tax Cuts for Criminals” Act?

Why would any voter rally around a platform of “I stand with tax cheats?”

The Congressional Budget Office calculated that the extra funding for the IRS would have reduced the deficit, because it would more than pay for itself. But it’s now been cut by an estimated $21 billion out of $80 billion.

If this seems abstract, consider the context and how it affects you and your retirement — and the retirements of everyone you know.

Social Security is now running at an $80 billion annual deficit. That’s the amount benefits are expected to exceed payroll taxes this year. (So say the Social Security Administration’s trustees.)

Next year, that deficit is expected to top $150 billion. By 2026, we’re looking at $200 billion and rising. The trust fund will run out of cash by 2034, and without extra payroll taxes will have to slash benefits by a fifth or more.

Over the next 75 years, says the Congressional Budget Office, the entire funding gap for the program will average about 1.7% of gross domestic product per year.

Meanwhile, how much are tax cheats stealing from the rest of us? A multiple of that.

According to the most recent estimates from the IRS, tax cheats steal about $470 billion a year. And that figure is four years out of date, relating to 2019. That’s the figure after enforcement measures.

Oh, and the Treasury Inspector General for Tax Administration says that’s a lowball number.

But it still worked out at around 12% of all the taxes people were supposed to pay (including payroll taxes). And around 2.3% of GDP.

Over the next 10 years, based on similar ratios to GDP, that would come to another $3.3 billion.

Sure, Social Security’s trust fund is theoretically separate from the rest of Uncle Sam’s finances. But that’s an accounting issue: A distinction without a difference.

Social Security is America’s retirement plan. Few could retire in dignity without it. Yet it is facing a fiscal crisis. By 2034, without changes, the program will be forced to cut benefits — drastically.

Some people want to cut benefits. Others want to raise the retirement age, which also means cutting benefits. Others want to raise taxes on benefits — which also means cutting benefits. Others want to hike payroll taxes, either on all of us or (initially) only on very high earners.

At last — just 40 or so years out of date — some are starting to talk about investing some of the trust fund like nearly every other pension plan in the world, in high-returning stocks instead of just low-returning Treasury bonds.

(It is hard for me to believe that it’s now almost 16 years since I first wrote about this ridiculously obvious fix And, yes, I’ve been boring readers on the subject ever since, including here and most recently here, and, no, I have no plans to stop.)

But if investing some of the trust fund in stocks is a no-brainer, so, too, is insisting everyone obey the law and pay the taxes they actually owe each year. I mean, shouldn’t we do that before we think about raising taxes even further on those who abide by the law?

How could anyone object? Any party that believes in law and order would support enforcing, er, law and order on tax evasion. And any party of fiscal conservatism would support measures, like tax enforcement, to narrow the deficit.

And, actually, any party that truly supported lower taxes for all would be tough on tax evasion: It is precisely this $500 billion in evasion by a small, scofflaw minority that forces the rest of us to pay more. We have, quite literally, a tax on obeying the law.

One of the many arguments in favor of taxing assets or wealth, instead of just income, is that enforcement would be easier and evasion much harder.

Washington, D.C., seems to be a place where people come up with complex proposals just so they can avoid the simple, fair ones.

[ad_2]

[ad_1]

A finance company boasting hundreds of apparently glowing online “customer reviews” and an A+ rating from the Better Business Bureau was this week civilly charged with cheating over 700 investors — many of them senior citizens — out of more than $30 million over 5 years.

El Segundo, Calif.–based Red Rock Secured and its controlling chief executive, Sean Kelly, were accused by the Securities and Exchange Commission of playing on the retirement and tax fears of older investors to sell them gold and silver coins at vastly inflated prices to hold in self-directed IRAs.

The markup on the coins “was almost always above 100 percent, and typically 120 percent or more,” the SEC said in its complaint.

Between 2017 and last year, Red Rock pocketed more than $30 million of the $50 million investors paid for the coins, said the SEC, which also sued two former Red Rock executives.

Attorney Michael Schafler of the Los Angeles law firm Cohen Williams, representing both Red Rock and its CEO, said the company had “nothing to hide” and has been “completely cooperative” with the SEC investigation.

“Red Rock has demonstrated that it is focused on compliance and providing clients with information necessary to make reasoned and informed decisions about purchasing precious metals,” he added. “Red Rock stands by that. It looks forward to the opportunity to defend itself against the government’s allegations in Court.”

According to the SEC, Red Rock used an aggressive marketing campaign to target investors, especially those who were “conservative” or “right wing” politically and “over 59½ [years old].”

Sales personnel played on customers’ fears about government policy, inflation, the stock market and retirement to persuade investors to move IRA funds to Red Rock and invest in gold and silver bullion, according to the SEC. But then, using what the commission calls a “bait and switch,” they persuaded investors instead to buy niche “premium” gold coins with huge, but hidden, markups, which included an 8% sales commission.

These so-called premium coins included an obscure silver Canadian coin for which Red Rock Secured controlled the entire market, allowing it to claim falsely that the “market value” of the coin was more than twice the value of its silver content, the SEC said.

Red Rock Secured salespeople were told to pitch the idea of a “worry-free retirement” to potential clients, while warning them that in the stock market “you could wake up and half your retirement could be gone,” the SEC said.

“The defendants used fear and lies to defraud investors out of millions of dollars from their hard-earned retirement savings,” said Antonia Apps, director of the SEC’s New York office.

There was no hint of any of this in the company’s glowing online “customer reviews.” At Google, Red Rock had an average rating of 4.8 stars out of 5 from 136 self-described customers. At Trustpilot, it got an average rating of 4.8 stars out of 5 from 167 alleged customers. Trustpilot said the rating was “excellent.” At the Better Business Bureau, Red Rock got an average rating of 4.75 stars out of 5 across 96 reviews. At Consumer Affairs it got an average rating of 4.9 stars out of 5.

The Better Business Bureau, contacted by MarketWatch, said it had added an alert to its site about the SEC probe into Red Rock. But, it added, “BBB ratings are not a guarantee of a business’s reliability or performance. BBB recommends that consumers consider a business’s BBB rating in addition to all other available information about the business.”

The organization, which provides information about businesses through a rating system and handles consumer complaints, said its standard policy is to check that all reviews are from legitimate customers by contacting the company being reviewed. The BBB does not possess legal or policing powers.

Business-review platform Trustpilot also told MarketWatch it had added an alert to the Red Rock Secured review page.

“Trustpilot is an open, independent review platform, meaning anyone who has had an experience with a business can leave a review — whether positive or negative — on the business’s Trustpilot profile page,” the company said in a statement “We are currently investigating Red Rock Secured to ensure that they are using our platform in line with our business guidelines, and should we find any evidence they are not, we will take the necessary steps to prevent it.”

Alphabet unit

GOOG,

GOOGL,

Google and Consumer Affairs could not be reached for comment.

[ad_2]

[ad_1]

When it comes to investing, some people don’t think in terms of thousands of dollars, tens of thousands, or even millions.

They think in hundreds of millions, or even billions. They have so much money they actually set up a private company, known as a “family office,” to manage all the loot.

And now Goldman Sachs, one of the bankers to the…

[ad_2]

[ad_1]

Many Americans dream of

saving $1 million for retirement. Most fall far short of that.The typical family’s 401(k) and IRA-type accounts come to less than half that goal in the years approaching retirement age, according to the nonprofit Employee Benefit Research Institute. Total household balances in retirement accounts for those 55 to 64 years old are $413,814 on average, according to its estimates based on 2019 data, the most recent available.

[ad_1]

Short selling can be controversial, especially among management teams of companies whose stocks traders are betting that their prices will fall. And a new spike in alleged “naked short selling” among microcap stocks is making several management teams angry enough to threaten legal action:

Taking a long position means buying a stock and holding it, hoping the price will go up.

Shorting, or short selling, is when an investor borrows shares and immediately sells them, hoping he or she can buy them again later at a lower price, return them to the lender and pocket the difference.

Covering is when an investor with a short position buys the stock again to close a short position and return the shares to the lender.

If you take a long position, you might lose all your money. A stock can go to zero if a company goes bankrupt. But a short position is riskier. If the share price rises steadily after an investor has placed a short trade, the investor is sitting on an unrealized capital loss. This is why short selling traditionally has been dominated by professional investors who base this type of trade on heavy research and conviction.

Read: Short sellers are not evil, but they are misunderstood

Brokers require short sellers to qualify for margin accounts. A broker faces credit exposure to an investor if a stock that has been shorted begins to rise instead of going down. Depending on how high the price rises, the broker will demand more collateral from the investor. The investor may eventually have to cover and close the short with a loss, if the stock rises too much.

And that type of activity can lead to a short squeeze if many short sellers are surprised at the same time. A short squeeze can send a share price through the roof temporarily.

Short squeezes helped feed the meme-stock craze of 2021 that sent shares of GameStop Corp.

GME,

and AMC Entertainment Holdings Inc.

AMC,

soaring early in 2021. Some traders communicating through the Reddit WallStreetBets channel and in other social media worked together to try to force short squeezes in stocks of troubled companies that had been heavily shorted. The action sent shares of GameStop soaring from $4.82 at the end of 2020 to a closing high of $86.88 on Jan. 27, 2021, only for the stock to fall to $10.15 on Feb. 19, 2021, as the seesaw action continued for this and other meme stocks.

Let’s say you were convinced that a company was headed toward financial difficulties or even bankruptcy, but its shares were still trading at a value you considered to be significant. If the shares were highly liquid, you would be able to borrow them through your broker for little or almost no cost, to set up your short trade.

But if many other investors were shorting the stock, there would be fewer shares available for borrowing. Then your broker would charge a higher fee based on supply and demand.

For example, according to data provided by FactSet on Jan. 23, 22.7% of GameStop’s shares available for trading were sold short — a figure that could be up to two weeks out-of-date, according to the financial data provider.

According to Brad Lamensdorf, who co-manages the AdvisorShares Ranger Equity Bear ETF

HDGE,

the cost of borrowing shares of GameStop on Jan. 23 was an annualized 15.5%. That cost increases a short seller’s risk.

What if you wanted to short a stock that had even heavier short interest than GameStop? Lamensdorf said on Jan. 23 that there were no shares available to borrow for Carvana Co.

CVNA,

Bed Bath & Beyond Inc.

BBBY,

Beyond Meat Inc.

BYND,

or Coinbase Global Inc.

COIN,

If you wanted to short AMC shares, you would pay an annual fee of 85.17% to borrow the shares.

Starting last week, and flowing into this week, management teams at several companies with microcap stocks (with market capitalizations below $100 million) said they were investigating naked short selling — short selling without actually borrowing the shares.

This brings us to three more terms:

A short-locate is a service a short seller requests from a broker. The broker finds shares for the short seller to borrow.

A natural locate is needed to make a “proper” short-sale, according to Moshe Hurwitz, who recently launched Blue Zen Capital Management in Atlanta to specialize in short selling. The broker gives you a price to borrow shares and places the actual shares in your account. You can then short them if you want to.

A nonnatural locate is “when the broker gives you shares they do not have,” according to Hurwitz.

When asked if a nonnatural locate would constitute fraud, Hurwitz said “yes.”

How is naked short selling possible? According to Hurwitz, “it is incumbent on the brokers” to stop placing borrowed shares in customer accounts when supplies of shares are depleted. But he added that some brokers, even in the U.S., lend out the same shares multiple times, because it is lucrative.

“The reason they do it is when it comes time to settle, to deliver, they are banking on the fact that most of those people are day traders, so there would be enough shares to deliver.”

Hurwitz cautioned that the current round of complaints about naked short selling wasn’t unusual and even though short selling activity can push a stock’s price down momentarily, “short sellers are buyers in waiting.” They will eventually buy when they cover their short positions.

“But to really push a stock price down, you need long investors to sell,” he said.

Lamensdorf said the illegal naked shorting that Verb Technology Co.

VERB,

Genius Group Ltd.

GNS,

and other microcap companies have been recently complaining about might include activity that isn’t illegal.

An investor looking to short a stock for which shares weren’t available to borrow, or for which the cost to borrow shares was too high, might enter into “swap transactions or sophisticated over-the-counter derivative transactions,” to bet against the stock,” he said.

This type of trader would be “pretty sophisticated,” Lamensdorf said. He added that brokers typically have account minimums ranging from $25 million to $50 million for investors making this type of trade. This would mean the trader was likely to be “a decent-sized family office or a fund, with decent liquidity,” he said.

Don’t miss: This dividend-stock ETF has a 12% yield and is beating the S&P 500 by a substantial amount

[ad_2]

[ad_1]

Cheesecake Factory appears to be “running the same play,” wrote J.P. Morgan analyst John Ivankoe in a recent restaurant industry outlook. I don’t think he meant it as a compliment—the stock, he noted, trades where it did in 2004, adjusted for splits.

Why the long stall-out? My first thought was that maybe hitting the mall for a hypercaloric sit-down meal off a menu the size of a Gutenberg Bible has fallen out of favor over the years. But no: Sales have bounced back and then some from the Covid pandemic, with plenty of takeout business and dessert orders. The average

Cheesecake Factory

(ticker: CAKE) restaurant does more than $10 million in yearly sales, or twice as much as an Olive Garden.

[ad_2]

[ad_1]

Investors love dividend stocks but there are different ways to look at them, including various “quality” approaches. Today we are focusing on high yields.

A high dividend yield can be a warning that investors have lost confidence in a company’s ability to maintain its dividend payout. But there are always exceptions, some of which can be brought about by market events — some investors remain skeptical of energy stocks, for example, after so much pain before this year’s outstanding performance for the sector.

Below is a screen of stocks that have high dividend yields and are favored by analysts. The screen has no financial quality filters.

For investors who are interested in dividend stocks but wish to focus on quality and total returns, this recent look at the S&P Dividend Aristocrats (companies that have raised dividends consistently for many years) might be of interest. For those looking for income but also worried about dividend cuts, here is a list of stocks with dividend yields of at least 5% whose payouts are expected to be well-covered by free cash flow in 2023.

If you are looking for higher yields with moderate risk, you should at also learn about funds that use covered-call option strategies to enhance income.

For a broad screen of stocks with high dividend yields that are favored by analysts, we began with the S&P Composite 1500 Index

SP1500,

which is made up of the S&P 500

SPX,

the S&P 400 Mid Cap Index

MID,

and the S&P 600 Small Cap Index

SML,

The S&P indexes exclude energy partnerships, so we added the 15 stocks held by the Alerian MLP ETF

AMLP,

to the list. Energy partnerships tend to have high distribution yields, in part because they pass most earnings through to investors. But they also can make tax preparation more complicated. They can also be volatile as oil

CL00,

CL00 and natural-gas

NG00,

prices swing.

The S&P indexes also exclude business development companies, or BDCs, so we expanded our initial screen to include the 24 stocks held by the VanEck BDC income ETF

BIZD,

BDCs are specialized leveraged lenders that make loans with high interest rates, mainly to middle-market companies. They often take equity stakes in the companies they lend to, for a venture-capital-type of investment style. The BDC space features several stocks with very high dividend yields, but is also known for volatility.

You have been warned — this particular stock screen focuses only on high yields and favorable ratings among analysts working for brokerage firms. There is no look back at dividend cuts and no cash-flow analysis as featured in other dividend-stock articles. If you see anything of interest resulting from the screen, you need to do your own research to consider whether or not a long-term commitment to one or more of these companies is worth the risk as you seek high income.

Starting with the S&P Composite 1500 and the components of AMLP and BIZD, there are 68 stocks with dividend yields of at least 8%, according to data provided by FactSet.

Among the 68 companies, 55 made the first screen, because they are covered by at least five analysts polled by FactSet.

Among the 55 companies, 11 have “buy” or equivalent ratings among at least 70% of analysts.

Here they are, ranked by upside potential implied by analysts’ consensus price targets:

| Company | Ticker | Dividend yield | Share “buy” ratings | Dec. 20 price | Consensus price target | Implied 12-month upside potential |

| Energy Transfer LP |

ET, |

9.08% | 95% | $11.68 | $16.24 | 39% |

| Enterprise Products Partners LP |

EPD, |

8.12% | 79% | $23.39 | $31.69 | 35% |

| Barings BDC Inc. |

BBDC, |

11.67% | 86% | $8.14 | $10.75 | 32% |

| Redwood Trust Inc. |

RWT, |

13.45% | 80% | $6.84 | $8.92 | 30% |

| Crestwood Equity Partners LP |

CEQP, |

9.75% | 100% | $26.86 | $35.00 | 30% |

| KKR Real Estate Finance Trust Inc. |

KREF, |

11.90% | 71% | $14.45 | $18.50 | 28% |

| Owl Rock Capital Corp. |

ORCC, |

11.21% | 91% | $11.78 | $14.73 | 25% |

| Sixth Street Specialty Lending Inc. |

TSLX, |

10.48% | 82% | $17.18 | $20.90 | 22% |

| Oaktree Specialty Lending Corp. |

OCSL, |

9.97% | 100% | $6.77 | $7.75 | 14% |

| Ares Capital Corp. |

ARCC, |

10.45% | 93% | $18.38 | $20.87 | 14% |

| BlackRock TCP Capital Corp. |

TCPC, |

10.25% | 71.43% | $12.49 | $14.00 | 12% |

| Source: FactSet | ||||||

One way to begin your own research into any company listed here is to click on the ticker for more information.

You should also read Tomi Kilgore’s detailed guide to the wealth of information available free on the MarketWatch quote page.

[ad_2]

[ad_1]

We all make mistakes in planning for our golden years. But which are the worst, which are the most common, and which ones do we all need to watch out for?

Financial planners have weighed in with the top 10 they see among clients. It’s emerged in a survey conducted by money managers Natixis and just released. And it’s a terrific checklist for anyone who wants to see how they’re doing, and what they need to change.

The…

[ad_2]

[ad_1]

Might the bear market’s losses at its recent low have gotten so bad that it was actually good news?

Some eager stock bulls I monitor are advancing this convoluted rationale. The outline of their argument is that when things get bad enough, good times must be just around the corner.

But their argument tells us more about market sentiment than its prospects.

At the market’s recent closing low, the S&P 500

SPX,

had dropped to 25% below its early-January high. According to one version of this “so-bad-it’s-good” argument, the stock market in the past was a good buy whenever bear markets fell to that threshold. Following those prior occasions, they contend, the market was almost always higher in a year’s time.

This is not an argument you’d normally expect to see if the recent low represented the final low of the bear market. On the contrary, it fits squarely within the third of the five-stage progression of bear market grief, about which I have written before: denial, anger, bargaining, depression and acceptance.

With their argument, the bulls are trying to convince themselves that they can survive the bear market, rationalizing that the market will be higher in a year’s time. As Swiss-American psychiatrist Elisabeth Kübler-Ross put it when creating this five-stage scheme, the key feature of the bargaining stage is that it is a defense against feeling pain. It is far different than the depression and eventual acceptance that typically come later in a bear market.

Though not all bear markets progress through these five stages, most do, as I’ve written before. Odds are that we have two more stages to go through. That suggests that the market’s rally over the past couple of weeks does not represent the beginning of a major new bull market.

Further support for this bearish assessment comes from the discovery that the bulls’ argument is not supported historically. Only in relatively recent decades was the market reliably higher in a year’s time following occasions in which a bear market had reached the 25% pain threshold. It’s not a good sign that the bulls are basing their optimism on such a flimsy foundation.

Consider what I found upon analyzing the 21 bear markets since 1900 in the Ned Davis Research calendar in which the Dow Jones Industrial Average

DJIA,

fell at least 25%. I measured the market’s one-year return subsequent to the day on which each of these 21 bear markets first fell to that loss threshold. In seven of the 21 cases, or 33%, the market was lower in a year’s time.

That’s the identical percentage that applies to all days in the stock market over the past century, regardless of whether those days came during bull or bear markets. So, based on the magnitude of the bear market’s losses to date, there’s no reason to believe that the market’s odds of rising are any higher now than at any other time.

This doesn’t mean that there aren’t good arguments for why the market might rise. But the 25%-loss concept isn’t one of them.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com.

[ad_2]

[ad_1]

You probably already know that because of market-capitalization weighting, a broad index such as the S&P 500

SPX,

can be concentrated in a handful of stocks. Index funds are popular for good reasons — they tend to have low expenses and it is difficult for active managers to outperform them over the long term.

For example, look at the SPDR S&P 500 ETF Trust

SPY,

which tracks the S&P 500 by holding all of its stocks by the same weighting as the index. Five stocks — Apple Inc.

AAPL,

Microsoft Corp.

MSFT,

Amazon.com Inc.

AMZN,

Alphabet Inc.

GOOG,

GOOGL,

and Tesla Inc.

TSLA,

make up 21.5% of the portfolio.

But there are other considerations when it comes to diversification — namely, factors. During an interview, Scott Weber of Vaughan Nelson Investment Management in Houston explained how groups of stock and commodities can move together, adding to a lack of diversification in a typical portfolio or index fund.

Weber co-manages the $293 million Natixis Vaughan Nelson Select Fund

VNSAX,

which carries a five-star rating (the highest) from investment-researcher Morningstar, and has outperformed its benchmark, the S&P 500.

Vaughan Nelson is a Houston-based affiliate of Natixis Investment Managers, with about $13 billion in assets under management, including $5 billion managed under the same strategy as the fund, including the Natixis Vaughan Nelson Select ETF

VNSE,

The ETF was established in Sept, 2020, so does not yet have a Morningstar rating.

Weber explained how he and colleagues incorporate 35 factors into their portfolio selection process. For example, a fund might hold shares of real-estate investment trusts (REITs), financial companies and energy producers. These companies are in different sectors, as defined by Standard & Poor’s. Yet their performance may be correlated.

Weber pointed out that REITs, for example, were broken out of the financial sector to become their own sector in 2016. “Did that make REIT’s more sensitive to interest rates? The answer is no,” he said. “The S&P sector buckets are somewhat better than arbitrary, but they are not perfect.”

Of course 2022 is something of an exception, with so many assets dropping in price at the same time. But over the long term, factor analysis can identify correlations and lead money managers to limit their investments in companies, sectors or industries whose prices tend to move together. This style has helped the Natixis Vaughan Nelson Select Fund outperform against its benchmark, Weber said.

Getting back to the five largest components of the S&P 500, they are all tech-oriented, even though only two, Apple and Microsoft, are in the information technology sector, while Alphabet is in the communications sector and Tesla is in the consumer discretionary sector. “Regardless of the sectors,” they tend to move together, Weber said.

Exposure to commodity prices, timing of revenue streams through economic cycles (which also incorporates currency exposure), inflation and many other items are additional factors that Weber and his colleagues incorporate into their broad allocation strategy and individual stock selections.

For example, you might ordinarily expect inflation, real estate and gold to move together, Weber said. But as we are seeing this year, with high inflation and rising interest rates, there is downward pressure on real-estate prices, while gold prices

GC00,

have declined 10% this year.

Digging further, the factors also encompass sensitivity of investments to U.S. and other countries’ government bonds of various maturities, credit spreads between corporate and government bonds in developed countries, exchange rates, and measures of liquidity, price volatility and momentum.

The largest holding of the Select fund is NextEra Energy Inc.

NEE,

which owns FPL, Florida’s largest electric utility. FPL is phasing-out coal plants and replacing power-generating capacity with natural gas as well as wind and solar facilities.

Weber said: “There’s not a company on the planet that is better at getting alternate (meaning solar and wind) generation deployed. But because they own FPL, some of my investors say it is one of the largest carbon emitters on the planet.”

He added that “as a consequence of their skill in operating, they re generating amazing returns for investors.” NextEra’s share shave returned 446% over the past 10 years. One practice that has helped to elevate the company’s return on equity, and presumably its stock price, has been “dropping assets down” into NextEra Energy Partners LP

NEP,

which NEE manages, Weber said. He added that the assets put into the partnership tend to be “great at cash-flow generation, but not on achieving growth.”

When asked for more examples of stocks in the fund that may provide excellent long-term returns, Weber mentioned Monolithic Power Systems Inc.

MPWR,

as a way to take advantage of the broad decline in semiconductor stocks this year. (The iShares Semiconductor ETF

SOXX,

has declined 21% this year, while industry stalwarts Nvidia Corp.

NVDA,

and Advanced Micro Devices Inc.

AMD,

are down 59% and 60%, respectively.)

He said Monolithic Power has been consistently making investments that improve its return on invested capital (ROIC). A company’s ROIC is its profit divided by the sum of the carrying value of stock it has issued over the years and its current debt. It doesn’t reflect the stock price and is considered a good measure of a management team’s success at making investment decisions and managing projects. Monolithic Power’s ROICC for 2021 was 21.8%, according to FactSet, rising from 13.2% five years earlier.

“We want to see a business generating a return on capital in excess of its cost of capital. In addition, they need to invest their capital at incrementally improving returns,” Weber said.

Another example Weber gave of a stock held by the fund is Dollar General Corp.

DG,

which he called a much better operator than rival Dollar Tree Inc.

DLTR,

which owns Family Dollar. He cited DG’s roll-out of frozen-food and fresh food offerings, as well as its growth runway: “They still have 8,000 or 9,000 stores to build-out” in the U.S., he said.

In order to provide a full current list of stocks held under Weber’s strategy, here are the 27 stocks held by the the Natixis Vaughan Select ETF as of Sept. 30. The largest 10 positions made up 49% of the portfolio:

| Company | Ticker | % of portfolio |

| NextEra Energy Inc. |

NEE, |

5.74% |

| Dollar General Corp. |

DG, |

5.51% |

| Danaher Corp. |

DHR, |

4.93% |

| Microsoft Corp. |

MSFT, |

4.91% |

| Amazon.com Inc. |

AMZN, |

4.90% |

| Sherwin-Williams Co. |

SHW, |

4.80% |

| Wheaton Precious Metals Corp. |

WPM, |

4.76% |

| Intercontinental Exchange Inc. |

ICE, |

4.52% |

| McCormick & Co. |

MKC, |

4.48% |

| Clorox Co. |

CLX, |

4.39% |

| Aon PLC Class A |

AON, |

4.33% |

| Jack Henry & Associates Inc. |

JKHY, |

4.08% |

| Motorola Solutions Inc. |

MSI, |

4.08% |

| Vertex Pharmaceuticals Inc. |

VRTX, |

4.01% |

| Union Pacific Corp. |

UNP, |

3.99% |

| Alphabet Inc. Class A |

GOOGL, |

3.03% |

| Johnson & Johnson |

JNJ, |

2.98% |

| Nvidia Corp. |

NVDA, |

2.92% |

| Cogent Communications Holdings Inc. |

CCOI, |

2.81% |

| Kosmos Energy Ltd. |

KOS, |

2.68% |

| VeriSign Inc. |

VRSN, |

2.15% |

| Chemed Corp. |

CHE, |

2.06% |

| Berkshire Hathaway Inc. Class B |

BRK.B, |

2.00% |

| Saia Inc. |

SAIA, |

1.97% |

| Monolithic Power Systems Inc. |

MPWR, |

1.96% |

| Entegris Inc. |

ENTG, |

1.93% |

| Luminar Technologies Inc. Class A |

LAZR, |

0.96% |

| Source: Natixis Funds | ||

You can click on the tickers for more about each company. Click here for a detailed guide to the wealth of information available free on the MarketWatch.com quote page.

The Natixis Vaughan Select Fund was established on June 29, 2012. Here’s a 10-year chart showing the total return of the fund’s Class A shares against that of the S&P 500, with dividends reinvested. Sales charges are excluded from the chart and the performance numbers. In the current environment for mutual-fund distribution, sales charges are often waived for purchases of new shares through investment advisers.

Here’s a comparison of returns for 2022 and average annual returns for various periods of the fund’s Class A shares to that of the S&P 500 and its Morningstar fund category through Oct. 18:

| Total return – 2022 through Oct. 18 | Average return – 3 Years | Average return – 5 Years | Average return – 10 years | |

| Vaughan Nelson Select Find – Class A | -20.2% | 11.8% | 10.8% | 13.0% |

| S&P 500 | -21.0% | 9.4% | 9.7% | 12.0% |

| Morningstar Large Blend category | -20.3% | 8.1% | 8.2% | 10.7% |

| Sources: Morningstar, FactSet | ||||

[ad_2]