[ad_1]

TikTok could face U.S. ban as bipartisan Senate bill takes shape

[ad_2]

[ad_1]

Norfolk Southern announces six-point safety plan following Ohio derailment

[ad_2]

[ad_1]

Stock market faces crucial test this week: 3 Q’s that may decide rally’s fate

[ad_2]

[ad_1]

Washington

CNN

—

More than 40 million federal student loan borrowers could be eligible for up to $20,000 in debt forgiveness, but they will likely have to wait several more months before the Supreme Court rules on whether President Joe Biden can implement his proposed relief program.

The Supreme Court heard oral arguments last week in two cases challenging Biden’s student loan forgiveness program, but justices aren’t expected to issue their decision until late June or early July.

When the ruling comes will also determine when federal student loan payments, which have been paused due to the pandemic since March 2020, will restart.

Some borrowers have been anxiously waiting for years to see if Biden would fulfill his campaign pledge to cancel some federal student loan debt. The president finally announced a forgiveness plan last August.

But after 26 million people applied, the program was blocked by lower courts in November – before any debt could be canceled.

“In some ways, it feels like we are one step closer now that they’ve heard the oral arguments, but until a decision is made, it still feels like we are in limbo,” said Lindsay Clausen, who has about $68,000 in student loan debt and works as an instructional designer at a university.

Clausen, 33, filed for relief from Biden’s forgiveness program last fall as soon as the application was open, hoping the forgiveness would help her and her husband save for a new home and expand their family.

“I felt relief, and then it was like a rug was pulled from underneath me,” Clausen said.

“Whichever way SCOTUS (Supreme Court of the US) decides to rule, it will at least be nice to have an answer,” she added.

The Biden administration has estimated that more than 40 million federal student loan borrowers would qualify for some level of debt cancellation, with roughly 20 million who would have their balance forgiven entirely, if the forgiveness program is allowed to move forward.

But not everyone with a federally held student loan would qualify.

Individual borrowers who earned less than $125,000 in either 2020 or 2021 and married couples or heads of households who made less than $250,000 annually in those years could see up to $10,000 of their federal student loan debt forgiven. Those with higher incomes would be excluded.

If a qualifying borrower also received a federal Pell grant while enrolled in college, the individual is eligible for up to $20,000 of debt forgiveness. Pell grants are a key federal aid program that help students from the lowest-income families pay for college, but these borrowers are still more likely to struggle paying off their student loans.

Student debt cancellation would deliver financial relief to millions of Americans, potentially helping them buy their first homes, start businesses or save for retirement.

But those who have already paid off their student loans, or chose not to borrow money to go to college to begin with, would get nothing. And the estimated $400 billion cost of canceling some debt would shift to all taxpayers.

At last week’s hearing, several of the conservative justices questioned whether that tradeoff is fair, while liberal Justice Sonia Sotomayor pushed back, arguing how many borrowers “don’t have friends or families or others who can help them make these payments.”

The back-and-forth on fairness touches on one of the biggest complaints about the nation’s higher education system: many people feel they need to go to college, and as a result borrow money, to get ahead.

Angel Enriquez, a 30-year-old meteorologist with about $61,000 in student loan debt, is one of those people.

His parents, immigrants from Mexico, couldn’t afford to help him pay for college. Enriquez was wait-listed at a state school that had a meteorology program, so he instead enrolled at a more expensive school out of state. He is now pursuing a master’s degree, which he felt he needed to stand out in a competitive industry.

“When you talk about fairness, it’s a complicated argument,” Enriquez said.

“But if you talk to someone who comes from poverty, or someone who’s a person of color, they are going to benefit from the forgiveness program the most because they’re the ones that have to jump through extra financial hoops in order to get where everyone else in the educated country is,” he said.

For some students, college degrees do not deliver the step up in the world they hoped for.

Even though Blake Goddard worked part-time jobs while in college, he still had to borrow nearly $90,000 for his bachelor’s degree in network communications management from DeVry University. In an effort to land a higher-paying job in the information technology industry, he then earned his master’s degree, borrowing another $44,000.

Despite those degrees, most of his jobs have been temporary contract positions, and many of his co-workers opted for getting lower-cost IT industry certifications rather than a four-year degree.

Meanwhile, the Department of Education has found that DeVry University, a for-profit college, misled at least 1,800 borrowers with false advertising about job placement rates.

While Goddard, 45, considers himself “one of the lucky ones” who would qualify for $20,000 of debt relief, the cancellation wouldn’t make too much of a dent in his more than $150,000 balance.

His debt, Goddard said, is “so detrimental” to his American dream, which was to buy a house and have a family.

“I was stupid enough to fall for it,” Goddard said about taking out student loans.

“I wish we could make it so nobody else in this country falls into the same trap,” he added.

Now, he’s committed to helping others avoid borrowing so much money for college and volunteers with an organization that helps students pursue careers in STEM fields.

One criticism of Biden’s one-time forgiveness program is that it would do nothing to address the cost of college for future students.

A more permanent solution to the college affordability problem would have to be created by Congress, but lawmakers have failed to pass any sweeping measure. A provision to make community college free was dropped from Biden’s Build Back Better agenda before it came to a vote in the House in 2021.

The Biden administration is also working on changes to existing federal student loan repayment plans, which don’t need congressional approval, and that aim to make it easier for borrowers to pay for college.

The Department of Education is currently finalizing a new income-driven repayment plan to lower monthly payments as well as the total amount borrowers pay back over time. In contrast to the one-time student loan cancellation program, the new repayment plan could help both current and future borrowers.

Additionally, in July, changes will be made to the Public Service Loan Forgiveness program, which allows certain government and nonprofit employees to seek federal student loan forgiveness after making 10 years of qualifying payments. The changes will make it easier for some borrowers to receive debt forgiveness.

If the Supreme Court ultimately gives the student loan forgiveness program the green light, it’s possible the government will begin issuing some debt cancellations fairly quickly. The administration has said it already approved 16 million applications for relief.

But several of the conservative justices expressed skepticism last week about whether Biden has the power to implement his student loan forgiveness program.

Lawyers for the government have remained confident that their plan is legal. They point to a 2003 law passed after the September 11, 2001, terrorist attacks that grants the secretary of education power to make sure people are not worse off in respect to their student loans in the event of a national emergency.

“I’m confident we’re on the right side of the law,” Biden told CNN a day after the oral arguments when asked if he was confident the administration would prevail in the case. “I’m not confident of the outcome of the decision yet.”

If the Supreme Court strikes down Biden’s student loan forgiveness program, it could be possible for the administration to make some modifications to the policy and try again – though that process could take months.

The pandemic pause on payments will remain in effect until either 60 days after the Supreme Court’s decision, or late August – whichever comes first.

[ad_2]

[ad_1]

New York

CNN

—

The US Supreme Court decided this week to hear a case that will consider the constitutionality of funding for the Consumer Financial Protection Bureau and, in doing so, test the constraints of US regulators’ power. The case would be heard in the fall, with a decision likely by summer 2024.

But what is the CFPB? How does its work affect your wallet? And why is its future potentially at risk?

The agency was created after the 2008 financial meltdown, as part of the Dodd-Frank Wall Street Reform and Consumer Protection Act. That law was passed in the wake of the 2007 subprime mortgage crisis and the Great Recession that followed.

The broad purpose of the CFPB is to protect consumers from financial abuses and to serve as the central agency for consumer financial protection authorities.

Prior to its creation, as the agency notes on its site, “[c]onsumer financial protection had not been the primary focus of any federal agency, and no agency had effective tools to set the rules for and oversee the whole market.”

The CFPB has regulatory authority over providers of many types of financial products and services, including credit cards, banking accounts, loan servicing, credit reporting and consumer debt collection.

It is charged with implementing and enforcing consumer protection laws, making rules and issuing guidance for consumer financial institutions. And it is the place consumers can go to lodge complaints about financial products and services.

Importantly, Dodd-Frank also gave the agency new authority to determine whether any given consumer financial product or service is unfair, deceptive or abusive and therefore unlawful.

While there are critics of the agency’s current structure and funding, it has saved consumers money, made it easier for them to seek redress and to get better clarity and more tailored responses from companies when they have a problem with their accounts, loans or credit reports.

“It has completely changed the consumer financial marketplace. Overall it has had a tremendous impact on making it more fair and transparent,” said Lauren Saunders, associate director of the National Consumer Law Center.

For instance, the CFPB has taken action against bank overdraft policies. “Arguably, the focus on overdraft practices has led some banks to eliminate or reduce their overdraft fees,” said Christine Hines, legislative director of the National Association of Consumer Advocates.

And it has gone after institutions for saddling consumers with pointless products, excessive fees and punitive terms.

Both Hines and Saunders made a special note of CFPB’s actions against Wells Fargo, after the agency found the bank had been engaging in multiple abusive and unlawful consumer practices across several financial products between 2011 and 2022 — from auto loans to mortgage loans to bank accounts.

Last month, the agency required the bank to pay more than $2 billion to customers who were harmed by such practices, plus a $1.7 billion fine that will go into a relief fund for victims.

“More than 16 million accounts at Wells Fargo were subject to their illegal practices, including misapplied payments, wrongful foreclosures, and incorrect fees and interest charges,” the agency said in a blog post.

In the area of mortgages, “CFPB has written rules to implement new protections so that mortgage lenders don’t make loans with tricks and traps that lead people to lose their homes,” Saunders said.

It also has created other safeguards, including rules on how service providers should communicate with borrowers who want to find alternatives to foreclosure, Hines noted.

Currently, the agency is in the midst of an effort to curb excessive or “junk” fees on a range of consumer financial products, such as credit card late fees.

Critics of the CFPB have been trying for years to limit its power and independence, attacking the way the agency is structured and funded. Like federal banking regulators, its funding is not determined by lawmakers in Congress as part of the annual appropriations process. Rather, it gets its money from the Federal Reserve System’s earnings.

“This nontraditional funding source limits congressional oversight of the agency and is the subject of legal challenges,” according to the Congressional Research Service.

The latest challenge — arising from a federal appeals court ruling that CFPB’s funding violates the Constitution’s Appropriations Clause and separation of powers — is what the Supreme Court will take up in its October term.

While it’s impossible to predict how the justices will rule, should they decide to uphold the appeals court ruling, that will put in doubt how the agency will be funded going forward, and whether it can continue to function effectively.

It’s also unclear whether the agency’s actions and rule-making over the past 11 years would be invalidated, nor what impact it would have on banks and other financial institutions that have set up systems to be in compliance with CFPB rules and safe harbors.

“The agency would be unable to do anything if the funding is invalidated. And prior rules could be challenged as the agency did not have a legal funding source that it could use to write those rules,” Cowen Washington Research Group analyst Jaret Seiberg said in a note to clients.

[ad_2]

[ad_1]

Biden had cancerous lesion removed, no further treatment required, doctor says

[ad_2]

[ad_1]

Morsa Images | Digitalvision | Getty Images

In 2019, about 5% of full-time work was done from home. The share ballooned to more than 60% in April and May 2020, in the early days of the Covid-19 pandemic, said Nicholas Bloom, an economist at Stanford University who has researched remote work for two decades.

That’s the equivalent to almost 40 years of pre-pandemic growth virtually overnight, his research shows.

The share of remote work has steadily declined (to about 27% today) but is likely to stabilize around 25% — a fivefold increase relative to 2019, Bloom said.

“That’s huge,” he said. “It’s almost impossible to find anything in economics that changes at such speed, that goes up by 500%.”

Initially, remote work was seen as a necessary measure to contain the spread of the virus. Technological advances — such as videoconferencing and high-speed internet — made the arrangement possible for many workers.

Both employees and companies subsequently discovered benefits beyond an immediate health impact, economists said.

Employees most enjoy having a reduced commute, spending less time getting ready for work and a having a flexible schedule that more easily allows for doctor visits and picking up kids from school, Bloom said.

Some workers have shown they’re reluctant to relinquish those perks. Companies such as Amazon and Starbucks, for example, recently faced a backlash from employees after announcing stricter return-to-office policies.

Employers enjoy higher employee retention and can recruit from a broader pool of applicants, said Julia Pollak, chief economist at ZipRecruiter. They can save money on office space, by recruiting from lower-cost areas of the country or by raising wages at a slower pace due to workers’ perceived value of the work-at-home benefit, she said.

It’s almost impossible to find anything in economics that changes at such speed.

Nicholas Bloom

economist at Stanford University

For example, job seekers polled by ZipRecruiter say they’d be prepared to take a 14% pay cut to work remotely, on average. The figure skews higher — to about 20% — for parents with young children.

Twitter recently shut its Seattle offices as a cost-cutting measure and told employees to work from home, a reversal from an earlier position that employees work at least 40 hours a week in the office.

“The benefits for employers are pretty substantial,” Pollak said.

Momo Productions | Digitalvision | Getty Images

Most companies have turned to a “hybrid” model, with a work week split between maybe two days from home and three in the office, economists said.

That arrangement has yielded a slight boost in average worker productivity, Bloom said. For one, the average person saves 70 minutes a day commuting; roughly 30 minutes of that time savings is spent working more, he said.

“Hybrid is pretty much a win-win,” Bloom said.

About 39% of new hires have jobs with a hybrid work arrangement, while 18% of new jobs are fully remote, according to ZipRecruiter. Both shares are up relative to their pre-pandemic levels (28% and 12%, respectively).

“It’s still an evolving trend, but the movement is very much toward increased remote work,” Pollak said.

Of course, not all workers have the option to work remotely. About 37% of jobs in the U.S. can plausibly be done entirely at home, according to a 2020 study by Jonathan Dingel and Brent Neiman, economists at the University of Chicago.

There are large variations by occupation and geography. For example, jobs in retail, transportation, hospitality and food services are far less likely than those in technology, finance, and professional and business services to offer work-from-home arrangements.

Not everyone agrees that the benefits of working from home outweigh costs.

Evidence suggests employee mentoring, innovation and company culture may suffer if jobs are fully remote, Bloom said. Workers cite face-to-face collaboration, socializing and better work-life balance as top benefits of in-office work, his research finds.

Companies that are fully remote often have in-person gatherings or retreats as a way to build company culture, Bloom said.

Workers have enjoyed a high degree of bargaining power due to a hot labor market characterized by low unemployment and ample job openings. If the economy cools and their bargaining power dissipates, it’s unclear whether some employers would introduce stricter work-from-home policies, economists said.

For one, employers may see remote work as a useful way to trim labor costs in the face of recession, Bunker said. The more likely scenario is on the margin: perhaps three or four days in the office instead of one or two, he said.

The technology sector is a useful indicator, he said. Tech job postings have fallen this year amid industry struggles, but the share of Indeed job ads offering a remote work benefit has remained constant, Bunker said.

“It’s been quite sticky in the face of hiring pullbacks,” he said.

[ad_2]

[ad_1]

The ISM service-sector index held at a robust 55.1% in February, a positive sign

[ad_2]

[ad_1]

Like it or not, financial pitfalls are a part of life. Financial mistakes can happen even with the best of intentions. However, it is not all about making mistakes. It’s also about the opportunities you don’t take advantage of.

Even so, it’s never too late to learn from these mistakes, and it’s never too soon to avoid them. With that said, in this article, we’ll look at 25 ways you’re killing your savings and how to avoid them.

All of us have been guilty of putting off things until another day, whether it was starting a workout regimen or saving money. The problem with the “I’ll do that later” philosophy? You may never follow through — despite your best intentions.

Additionally, you may have missed some opportunities to plan your financial future. And, even worse, you’re missing out on the power of compounding.

Consider, for example, investing $1,000 and earning a 7% return annually. Your account would be valued at $1,070 after year one if you earned $70. Your account would be worth $1,144.90 in year two after earning $74.90. By year three, you would have earned $80.14, bringing your total to $1,225.04.

In time, this can snowball and potentially add up to a large amount if your account continues to grow in this manner.

Simply put, putting off financial chores only contributes to an ever-growing to-do list. Delaying time-sensitive tasks like paying off debt or planning for retirement could cost you more in the long run.

How can you avoid procrastination? Make managing your finances easier by breaking them down into manageable chunks. While you don’t have to organize your finances overnight, ignoring your to-do list won’t make it disappear. Consider setting aside time once a week or once a month to monitor your finances and accomplish important tasks.

Losing one dollar at a time can result in a lot of financial losses. You may not think it’s a big deal to order a double-mocha cappuccino, go out to dinner, or watch a pay-per-view movie. But it adds up.

Consider this. Americans spend an average of $2,375 per year on dining and takeout. These funds could be used to pay off a credit card debt or pad your savings.

It’s very important to avoid this mistake if you are experiencing financial hardship. When a few dollars separate you from foreclosure or bankruptcy, every dollar counts. If you aren’t in that bad of financial shape, consider dining out or getting takeout less often. When you do, look for deals or have lunch instead of dinner.

Chances are you’re living above your means if you’re sweating over money. To be sure though, take a look at these five signs that you’re heading for trouble.

Do not mistake living below your means for being a cheapskate or skipping out on life’s experiences. Instead, it “simply means that you’re spending less or equal than you’re making each month,” explains Deanna Ritchie in a previous Due article. “As a result, you aren’t putting yourself into debt by living off of plastic. And more importantly, this will help you create a more stable financial future.”

“Of course, living within your means requires discipline and a little sacrifice,” adds Deanna.

Of course, covering a friend’s dinner is very different from helping to pay their rent. Even if you have the money currently, you’re playing with fire if they have a poor track record when it comes to managing their finances.

For example, what if they don’t pay you back and you lose your job or have a medical expenses? The cash you were supposed to have will run out. If you can’t find the money from other sources, you may be forced to borrow it.

Helping someone out can take many forms. It may be as simple as bringing them lunch until they are stable or helping them update their résumés.

According to Bankrate: 60 percent of Americans have helped out a friend or family member by lending cash with the expectation of being paid back, while 17 percent have lent their credit card and 21 percent have co-signed for a financial product like a loan or rental

“An emergency fund pertains to the amount set aside to maintain financial security,” explains Chris Porteous in a previous Due article. “In essence, this is the portion of your savings that you should only spend for emergencies.”

This money can be used for urgent expenses during times of financial hardship. By creating a safety net, you prevent yourself from withdrawing money from your primary savings account. As a result, you are prevented from relying on costly alternatives such as bank loans, payday loans, or credit cards. “Hence, your retirement fund will remain untouched.”

Most emergency funds consist of liquid assets. These are assets that are easily convertible into cash. In order to cover urgent expenses, you must have the means to do so. Some examples are your investments in financial markets and your receivables from debtors. Even when earnings are inconsistent, they provide an instant cushion to keep you afloat.

“When you build an emergency fund, do not save a considerable portion of your income right away.” Chris adds. “Only set aside the amount that will not hurt your financial growth since you have constant expenses.” However, make sure you have enough money to handle future mishaps. This may include unplanned hospitalizations, unannounced layoffs, and property damage.

Perhaps the most common money mistake is not sticking to a budget. In fact, according to a survey by loan servicing company OppLoans, 73% of Americans do not regularly adhere to a budget.

Why’s that concerning? We often burn holes in our pockets with little luxuries that we don’t even notice. These could include gym memberships, nights out, and impulsive purchases. There is nothing wrong with making these purchases every now and then. It becomes problematic when they become a habit and don’t fit within your monthly budget.

“Do you need to track every single dollar coming in and out? Absolutely not,” says Aja Evans, a licensed mental health counselor who specializes in financial therapy. “A budget is for making sure you have a plan or understand where your money is going.”

Along with the hassle of tracking expenses, budgeting is “hard for people psychologically,” because they associate them with self-denial. Budgets aren’t just about restrictions, Evans says. Additionally, you can prioritize things you enjoy, like dining out or vacationing.

As Millennials and Gen Z workers enter the job market, they are more concerned with paying off their student loans than saving for retirement. After all, in the early years of one’s career, 65 may seem far away. In the long run, however, money saved early will grow into a much larger nest egg.

As an example, let’s say that start contributing $2,000 annually to an IRA with a 6 percent annual return at age 25. At 65, your investment will be worth $328,095 (40 x $2.000).

What if you started your $2,000 annual contribution at 30? After investing $70,000 (35 times $2,000), you’ll only receive $236,242.

Overall, the sooner you start saving, the better.

Insurance pays for contingencies because people don’t want to spend money on anything without a guarantee of return.

It is possible to ruin your finances without insurance if you do not have enough cash to cover a large medical bill, car accident, house fire, or theft. It’s a small price to pay for ample protection.

Conversely, paying for redundant or unnecessary insurance coverage can drain your bank account. You may be able to secure rental car insurance through your credit card or auto insurance, for example.

With an increase in income, you tend to spend more on your lifestyle. Often, you don’t even notice this type of waste of money until it’s too late.

To be fair, when you can afford certain items, it may be worth spending more on them. The long-term cost of well-made clothes is lower than that of cheap ones, for instance.

You can often live comfortably even when you make less money if you buy things and live the way you did when you made less money. It will not make you happier or enhance your quality of life if you increase your spending.

Spend your extra income on things you really need instead of on fancier things. Among the possibilities are saving more, increasing your retirement contributions, or paying off debt. If all that’s in order, consider buying an annuity.

With annuities, you can save your money tax-deferred until you receive retirement income. You won’t have to worry about outliving your retirement savings with them. In addition, they can provide for your family after you die or for your own long-term care if the need arises.

When you have student loans, a car payment, credit card debt, and a mortgage, it can be difficult to know where to start. In spite of this, financial advisors caution you to prioritize paying off your debts carefully.

It is more common for people to pay extra on their mortgage, which has a 3% interest rate. In contrast, they don’t pay high-interest rates on their student loans or car loans.

Whenever you plan to pay off your debt, start by writing down all your balances and the interest rates associated with them. Debt with the highest interest rate should be tackled first, such as credit cards, before moving on to the debt with lower interest rates.

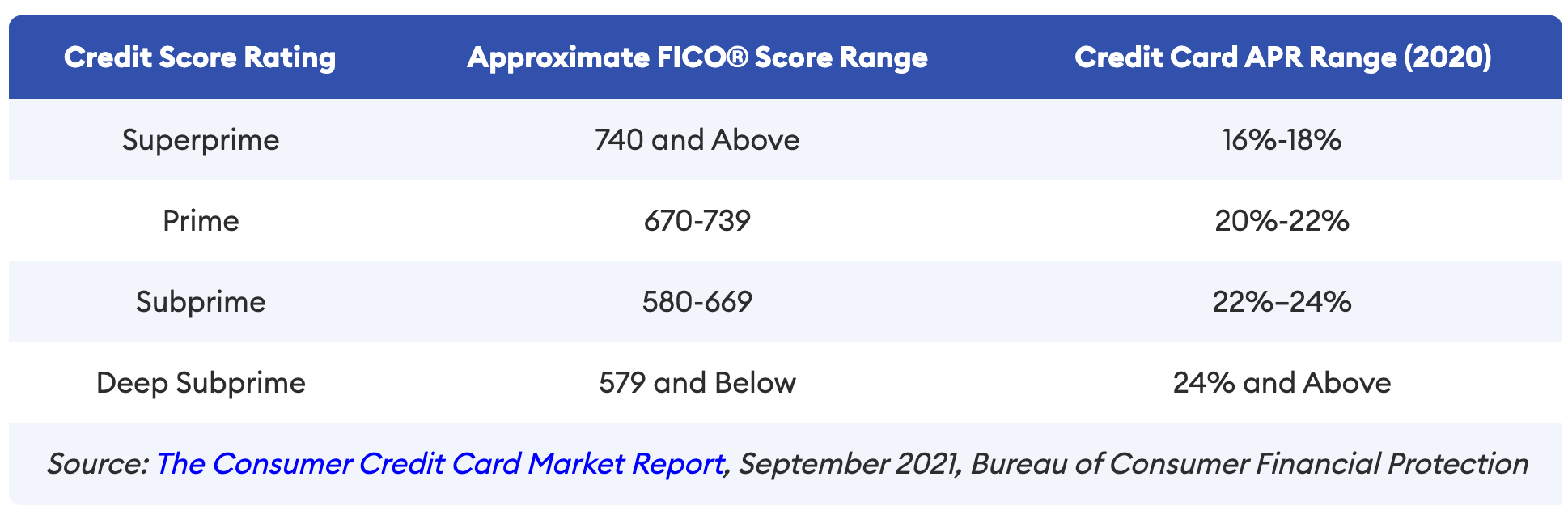

If you are experiencing [credit card] debt, you need to handle it urgently, possibly even delaying retirement contributions while you get your balances under control. When you pay off your debts, you will not only improve your credit score, but you will also have more money to invest and save. In particular, this is true when the average credit card interest rate is 23.77%, according to Forbes Advisor.

Your bank account isn’t the only reason you should make money in your free time. A little extra income can be the difference between achieving your long-term financial goals and not achieving them. In addition, it gives you the extra funds to treat yourself when it’s time.

Also, don’t think you can just make money on the side of your wallet. You can enhance your career prospects by having a side hustle, which will impress potential employers as this can develop your skills.

It doesn’t matter if it’s pet sitting, starting your own business, selling photos online, or any other passive income idea, every little bit helps.

A new car’s value drops the minute you drive it off the lot. It differs from car model, make, upkeep, and other factors, but the depreciation rate of a new car can be as high as 20% (or even more) after one year and reach around 40% after five years.

For this reason, used cars may be a good option if you need new wheels. Depreciation has already been paid for by the previous owner – not you. If you sell your vehicle after three to six years, you’ll gain more money than if you sell it after one to three.

The act of refinancing and withdrawing cash from your house means you are giving away ownership to another person. If you’re able to lower your rate or refinance and pay off high-interest debt, refinancing might make sense.

Alternatively, you can open a home equity line of credit (HELOC). A HELOC, is a revolving credit line secured by your home that can be used for large expenses or to consolidate higher-interest rate debt from other loans, such as credit cards. In addition to having a lower interest rate than some other common types of loans, a HELOC may also be tax deductible.

In the event that all of your savings are invested in one type of investment and it performs poorly, you will lose money. The best thing to do is to spread your money among a few different accounts. Your investment portfolios should be managed by the same financial planner or held in the same blanket account – with varying levels of risk and reward.

Using this strategy, you can grow your wealth while maintaining stability in lower-risk investments while capturing some of the benefits of riskier investments.

Late fees, damaged credit scores, and other negative financial consequences may result from falling behind or missing bill payments. Your credit score can be damaged if you fail to meet your monthly obligations as well. In some cases, as little as two late payments can result in a permanent mark on your credit report.

The easiest solution? Streamline the process of paying your monthly bills by setting up an automatic payment through your online checking account, brokerage account, or mutual fund.

Consumer Affairs reports that “Less than a third (32%) of respondents were able to save money consistently, while just over a quarter (26%) were able to invest. About a fifth said their ability to afford bills worsened due to inflation.”

Do you max out your workplace retirement plan (401k, etc)? Is your employer offering a matching contribution?

It applies specifically to you if you answered yes to both questions.

Why? It is possible that you are missing out on free money. Moreover, it could be free money accumulating over a 30-year period.

There are many types of workplace retirement plans out there, such as 401k plans, 403b plans, and 457 plans. Even so, 17% of employees have access to employer-sponsored benefits but do not contribute. MagnifyMoney found that 12% of employees who do not return company matching funds leave the funds on the table, totaling 17.5 million people.

Considering opting into an auto-escalation feature at your employer can increase your retirement savings. As a result of this feature, your savings rate will automatically be boosted each year by 1% or 2%.

For anyone under the age of 50 in 2023, the contribution limit will be $22,500. A contribution limit of $30,000 applies to people 50 and older. Having an employer who matches your contributions AND maxing out your 401k plan before the end of the year can also present a problem. After maxing out your 401k plan, you must stop contributing. If you stop contributing, your employer will not match your contributions.

When you use your credit card as free money instead of using what you have, you are on the fast track to financial ruin. In this regard, treat your credit card just as you would a debit card.

Have you been thinking about getting that new iPhone? Rather than putting it straight on your credit card, only use it if you’re confident you’ll be able to pay for it immediately. After all, even at a somewhat reasonable 16.99% APR, a $1,000 balance would result in monthly interest charges of $14.06.

Likewise, buying now, and paying later services like Klarna is a also big no-no. According to a Consumer Reports survey, 11 percent of people who use buy now, pay later services miss at least one payment, often because they lose track of when it’s due or don’t know when it’s due. Others said they thought they’d set up automatic payments only to discover they weren’t. They later discovered that their payments had still gone through, even though they thought they had canceled their purchase.

In addition to late fees and interest charges, people who miss buy now, pay later payments may have their credit history affected.

Furthermore, 5 percent of people who used a buy now, pay later service said they couldn’t otherwise afford the purchase. That can cause trouble: People say they miss payments mostly because they thought they had the money but didn’t.

TL;DR: Make sure you only purchase what you can afford.

Having the ability to pay off your credit card or other credit every month is essential. Having missed payments on your credit report can adversely affect your ability to obtain loans or mortgages in the future.

Have you ever thought about how your credit score can affect your life? A credit score is important when you want to borrow money, buy a house, or even rent an apartment. If you discover any problems or errors with your credit profile, you can work with your lenders to correct them.

Because of their importance, it’s vital that you regularly check your credit score.

Additionally, Equifax® credit reports are free each year if you create a myEquifax account. To get your free Equifax credit report and VantageScore® 3.0 credit score based on Equifax data, click “Get my free credit score” on your myEquifax dashboard. Credit scores come in many forms, including VantageScores.

The personal saving rate in the United States decreased from 7.5 percent in December 2021 to 3.4 percent in December 2022. Due to this, it should not be surprising to learn that many households live paycheck to paycheck. As a consequence, you cannot prepare for an unforeseen problem, which has the potential to become a disaster.

As a result of overspending, people are put in a precarious position, one where they can’t afford to miss a paycheck. In the event of an economic recession, you do not want to find yourself in this position. Thankfully, there will be very few options available to you if this happens.

The advice of many financial planners is to keep three months’ worth of expenses in a quick-access account. Changing economic conditions or loss of employment could drain your savings and place you in a debt cycle. If you don’t have a three-month buffer, you may lose your home.

Even if cryptos or fad investments do make you a lot of money in a short period of time, the disruption to your investing strategy can cause you to lose money long-term. To put it another way, you should stick to investments that have a proven track record or only invest money you’re willing to lose.

Or, in the words of Paul Samuelson, “Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.”

If you do not pay your tax debt, you will be charged penalties and interest every month. A lingering balance is going to cost you more money in the long run.

The good news? A tax debt reduction or installment agreement are two methods the IRS offers for settling delinquent balances. An experienced tax professional can guide you through the process, typically at no cost.

It is time to put an end to staying loyal to banks and energy providers. You might think you’re getting a great deal if you’ve been a customer for a long time. In most cases, it will be the exact opposite.

People tend to think that switching utilities are a hassle, so banks and other utility providers know this. As a result, they rely on your laziness to keep your business and your money.

However, switching bank accounts is mostly automated today. For new customers, some banks offer great cash rewards and interest rates on savings accounts. When you think you could find a better deal, it’s definitely worth shopping around.

Your career is your most important financial asset. Since the average American can expect to earn around $1.7 million in their lifetime, it’s no wonder. That comes out to just under $42,000 per year. However, if you start at $40,000 today and earn 3% pay increases over 45 years, you will earn over $3.7 million.

In short, you can lose millions of dollars if you don’t work hard to maximize your income.

So, if you want to avoid this bad money mistake, you simply need to develop and implement a career plan to maximize your earnings. Also, do not quit your job without a backup plan. The stress of working at your current job is nothing compared to the stress of worrying about how you’ll pay for essential expenses.

According to one study, medical reasons may account for two-thirds of bankruptcies in the United States. Even if that statistic is skewed, we all know how difficult it can be for families to pay for medical costs.

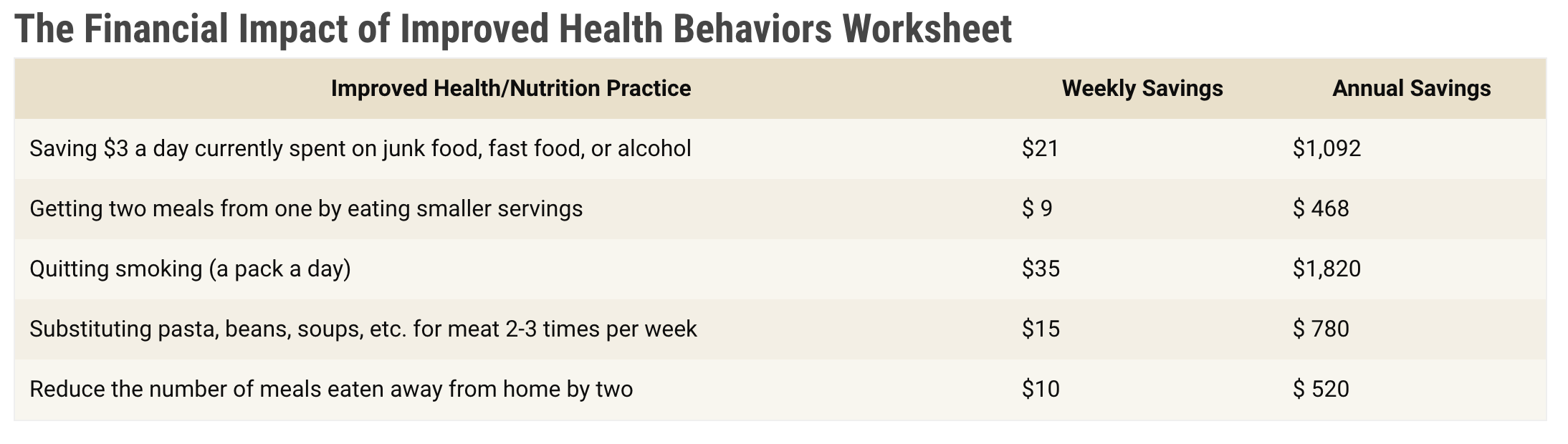

Aside from that, unhealthy habits cost a lot of money. For example, if you give up smoking or junk food for $10 a day, you can save $3,650 a year, plus interest. And, those are just the immediate savings.

Long-term savings can also be made over the course of a person’s life. Overweight people could save between $2,200 and $5,300 on their lifetime medical costs if they lost 10% of their weight. Increased medical costs can be reduced by thousands of dollars per year by delaying the onset of diabetes.

Additionally, employers are increasingly recognizing the benefits of healthy employees. In the end, healthy employees take fewer sick days, so the company pays less out of pocket for health insurance. As such, companies may offer financial bonuses for not smoking or discounts for gym memberships.

Almost no personal finance education is offered in public schools, so many Americans rely on what they learned from their parents. Despite thinking you’ve got things under control, you can avoid many financial mistakes by learning financial literacy and best practices.

The good news? Learning how to become a financial master has never been so easy. Educating yourself is the best way to avoid making financial mistakes, whether you watch videos, read blogs, or listen to podcasts.

Budgeting and planning your finances can be daunting. Taking the time to look back at your past spending habits is a real moment of honesty. Do it anyway.

To get started, try the 50/20/30 system.

Your money is divided into three categories: 50 percent for essential expenses (rent, utilities, car payment), 20 percent for savings, and 30 percent for flexible spending. That’s all there is to it. If you’re single and tend to spend most of your meals out rather than in, the flex percentage works well for you.

The answer depends on the situation. In contrast to credit card debt or what is often called “bad debt,” student loans are considered “good debt.” This is due to the fact that student loan debt has a lower interest rate and that getting a degree will lead to a higher-paying job.

Try to keep your credit usage to 30 percent or less. In general, your debt should be less than 20 percent (including car loans, real estate loans, and personal loans).

Are you still unsure? The following questions will help you gauge how you’re doing:

You should come up with a dedicated plan if one or more of your credit cards are maxed out. Prioritize paying off the card with the highest interest rate first, and then pick off the rest one by one.

The ability to lease a car, take out a loan, or rent an apartment requires a good credit score. All of these things are pretty essential. Credit collectors are trained to increase your anxiety levels to sky-high levels when you have bad credit.

Make sure you pay off your credit card each month. Get in touch with your creditor if the debt seems impossible to pay. Perhaps you can work out a revised payment plan and save a ton of money on interest.

According to financial circles, three to six months’ post-tax income is a good starting point. The ideal is six months, but most of us don’t have any emergency savings, so even half that is a reasonable start.

As soon as possible. As a result of compound interest, the earlier you start saving, the more you will accumulate.

In the absence of a 401k or similar model at your employer, consider setting up a personal retirement account. You must participate in your employer’s retirement plan if it is an option. As a side note, if they offer matching, make sure to take advantage of it every time.

It is also worth researching IRA options, including Roth IRAs as well as Traditional IRAs. You may also want to learn about mutual funds, bonds, and more if you’re more advanced in your retirement savings.

The post 25 Ways You’re Killing Your Savings: STOP Making These Mistakes appeared first on Due.

[ad_2]

John Rampton

Source link

[ad_1]

Stock futures are leaning higher Friday as the S&P 500 looks for a winning week

[ad_2]

[ad_1]

Stocks on the move early Friday: C3.ai surges, but ChargePoint and Zscaler dive

[ad_2]

[ad_1]

Ready for an 8-week stock rally? This strategist lists 6 reasons it will happen.

[ad_2]

[ad_1]

I’m 66 years and 4 months old.

My Social Security payments start next month at $3,300 a month. I’m currently working part-time, three days per week, as a professional engineer for $95/hour for my long-time regular full-time employer of 28 years. (I want to leave this position ASAP or sooner.)

I currently have about $1.6 million in retirement accounts. My wife (60 years old) has about $600,000 in various regular and retirement accounts. We have a 16-year-old daughter at home attending high school and college in a dual enrollment program. If she stays with the program she’ll have her bachelors at 19. While in high school she takes college classes and we pay no tuition while she’s in high school.

Our monthly expenses are about $9,000-10,000 per month including health insurance for my wife and daughter. We own our modest single-family home with no mortgage. Taxes and insurance are currently about $6,000 per year. We currently have no debt, aside from an American Express and Visa that we pay off every month.

I’m on Medicare. I get walloped for a double premium for part “B” because I’m considered a high-wage earner. The two of us are in reasonable/normal health for a couple of old farts.

I want to throw in the towel on May 5 and play more golf. Can we do it?

See: We’re in our 60s and have lost $250,000 in our 401(k) plans — can we still retire?

Dear reader,

Congratulations on saving so much for your retirement. That’s a wonderful accomplishment alone!

Because I don’t have all of your financials in front of me, nor am I a financial planner building a comprehensive plan for your retirement, I can’t say for certain if you can retire. However, it does obviously sound like you’re doing well and that you’ve been planning. Instead of telling you to go for it or not, I’m going to offer a few things to consider before you pick up your mid irons.

More than $2 million (you and your wife’s savings combined) is a lot of money — I’m not suggesting otherwise — but when it comes to retirement, it doesn’t mean you’re automatically good to go once you hit the million-dollar mark. There are so many factors, some of which you mentioned like healthcare and debt, as well as saving and spending.

I harp on spending analysis a lot but to me, it’s so crucial when deciding if and how to retire. Why? Because this is something that, for the most part, you can control. That’s a pretty powerful feeling.

So my first suggestion: Review those AMEX and Visa statements, as well as money that comes out of any checking accounts, and make sure that you’re spending the way you want and need to spend. When you retire, you won’t have that part-time income anymore, and while you may be itching to get on the green, you’ll also be stressing out if you don’t have enough green in a decade or two. You’ve told me what your Social Security benefits will be and what your average monthly spending is, but I would suggest really poring over your spending and assessing how comfortable you’ll be if you continue to spend that way when you retire.

Check out MarketWatch’s column “Retirement Hacks” for actionable pieces of advice for your own retirement savings journey

There’s a second part to that analysis, which is how much money you intend to withdraw from your retirement accounts. I’m not sure if your wife is still working, but regardless, the more money you take out of those accounts every month, the less there is available to grow over time. Taxes also play a part here, depending on if you’re withdrawing from a traditional or Roth-style account. Those taxes could take a larger chunk out of your spending money, as well as potentially give you a heftier tax bill come tax time.

Think about this when your daughter goes off to college, too. She may not be there long if she continues with her hybrid high school and college courses (which is wonderful, by the way), but do you plan to pay for her tuition, and if so, where is that money coming from? Advisers tell me all the time: you can take a loan for college, but you can’t take one for retirement. It might be beneficial to have a separate savings account earmarked for education, if you don’t already have one of those or some sort of college savings account like a 529 plan, so that you’re not draining your retirement account for a tuition bill.

One last bit about that — plan for the unexpected. What will you do if a major expense arises? Will that money also come from a retirement account, or do you have an emergency account set aside to cover it? Saving a lot of money for retirement is amazing, but it’s not the only task individuals need to manage… coming up with a Plan B, and maybe even a Plan C and Plan D, is necessary too.

Also see: Are you planning for retirement all wrong?

Next, before retiring, check the way your money is invested. What’s your asset allocation like, and does it need to change? Don’t make alterations just to make them — and definitely don’t make them just because you read the markets weren’t doing so hot that day — but keep in mind this money does need to grow for decades to support you and your wife, so you will need to strike that balance. Reaching out to a qualified financial professional, such as a certified financial planner, can help you make sense of what the best investment mix is, but at the least, log in to your account or call up the firm where your accounts are located and check that asset allocation.

Also, you mentioned you’re already on Medicare. I would suggest taking the time now — well before open enrollment — to review your current and expected future health expenses, and then assess how helpful your current coverage is for you. I know you mentioned you and your wife are in reasonable health, but if there are any operations or services you think you may need next year, it’s better to start reviewing what plans provide you the best coverage for your situation so that you’re not paying more out of pocket than necessary. This is an exercise you don’t need to do immediately, but it will certainly help you feel more prepared come the end of the year when it’s time to keep your current plan or switch for something else.

As an aside, you’ll eventually pay less in Medicare Part B premiums when your modified adjusted gross income declines. Those premiums are based on your tax returns from two years prior.

You sound like you are on the right track, which is wonderful. I would just caution you to tie up a few loose ends before resigning so that you can tee up without worrying.

Readers: Do you have suggestions for this reader? Add them in the comments below.

Have a question about your own retirement savings? Email us at HelpMeRetire@marketwatch.com

[ad_2]

[ad_1]

Asian stocks following U.S. markets higher as interest-rate fear turns to hope

[ad_2]