This is an opinion editorial by Ruda Pellini co-founder and president of Arthur Mining, an ESG-focused bitcoin mining company.

I recently saw an article that cited the level of leverage and debt of the world’s leading Bitcoin mining companies. Since they are listed companies, it is easy to find their financial statements and prove the obvious: this is a counter-cyclical business that requires a lot of efficiency and professional management.

For those who are still wondering what mining is, let me quickly explain: the term mining makes an analogy to the process of extracting gold and metals, since bitcoin miners are the “producers” of this digital commodity. In practice, mining consists of allocating computing power and electricity to ensure the bitcoin network functions, validating transactions and serving as the backbone of this decentralized system.

Investing in bitcoin mining is different from buying the asset directly. On the one hand, when investing in mining you have constant and predictable cash flow and physical assets that can be liquidated in the event of market stress, making the investment more attractive to more cautious investors accustomed to investing in cash flow generating businesses. On the other hand, besides the risk related to the asset, there are also risks of the operation itself.

Currently, bitcoin is down more than 65% from its November 2021 peak. Moments like this generate apprehension and make the investors ask themselves: is it an opportunity to increase my investments or a risk?

For bitcoin mining operations with structured cash, the moment represents a great opportunity! To quote Warren Buffet: “It’s only when the tide goes out do you learn who was swimming naked.”

The Impact Of Bitcoin Price On Mining

In general, bitcoin miners have their cash flow reduced as the price of bitcoin falls, so at first glance it is counterintuitive that lower prices are beneficial to a mining company.

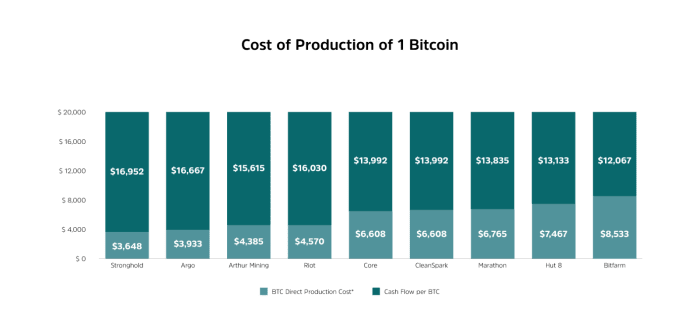

However, since we are talking about an industry, more important than the market price is the cost of production.

Within the production costs, the biggest cost is the cost of electricity, which is the main input for this data processing activity. Therefore, those who can get a good price for energy and efficiency can remain profitable even in unfavorable market conditions.

Since not all miners can achieve this same level of efficiency, in scenarios like this one many end up having their production cost very close to the market price of the asset, leading them to liquidate their assets and exit the market.

Because of this, as in most commodity markets, this market is also counter-cyclical, and these down times are the best times to expand operations. There is a positive correlation of the price of mining computers with the price of Bitcoin, where the price ends up being adjusted in a greater variation than the asset itself.

While the price of bitcoin fell about 47% from April to August of this year, the price of computers used in mining fell about 60% in the same period.

(Source: Arthur Mining)

The Bitcoin Mining Companies

Particularly, I understand the mining industry in much the same way as the network infrastructure (cable) industry of the 1990s, where there were basically three major cycles of expansion and consolidation.

The first cycle was marked by geeks and technology enthusiasts, who started internet businesses and literally cabled and set up the first network infrastructures. This has also happened with bitcoin miners since 2009.

In the second cycle, we had the entry of players interested in maximizing capital quickly, ignoring the importance of efficiency by focusing only on the accelerated expansion of their structures and on short-term results.

In the third cycle, we had the consolidation of the industry, with the entry of players focused on efficiency and long-term vision, encouraging the entry of venture capital and the professionalization of the market. In the United States, the 50 largest cable companies of the late 1990s were consolidated into four by the end of 2010.

Most of today’s large mining companies entered the second cycle, with too much focus on the short term and not enough efficiency. This results in businesses that are not very robust and are very vulnerable to times of stress.

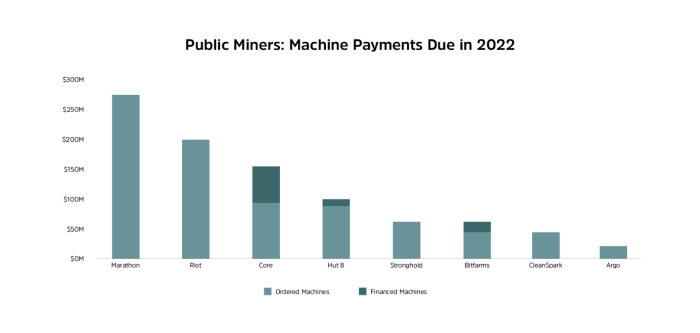

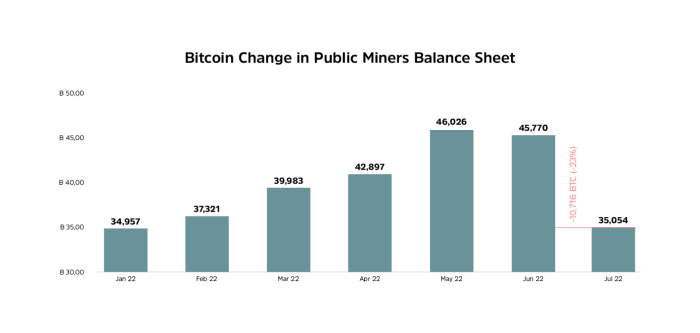

During bitcoin’s big up cycle between 2020 and 2021, many mining companies took advantage of rising margins to leverage themselves and expand their operations. This is very common in many industries, but in this case in addition to leveraging in dollars, a good portion of the listed miners ended up keeping their cash in bitcoin in an attempt to maximize their results.

According to estimates from Luxor Technologies, estimates indicate that listed mining companies have between $3 and $4 billion in loan agreements used to finance infrastructure expansion and computer purchases.

Mistakenly, these players did not consider that, as in any commodity producer, if you are able to increase your production capacity, it makes sense to sell the stock you produce and reinvest it, rather than keeping the asset you produce on your balance sheet.

In order to be able to honor these commitments, mining companies began to liquidate their liquid assets first, in this case the bitcoins held on the balance sheet. This move further increased the selling pressure during June and July, pushing prices to new lows.

Basically, the result of the cash management strategy adopted by these mining companies was to mine high and sell low, resulting in further financial losses in addition to the operational losses caused by the bitcoin price declines.

After selling the bitcoin from the balance sheet, the less efficient mining companies will need to sell computers to honor payments and maintain the operation, opening up space for more efficient mining companies to incorporate these assets and operations.

As with other commodities, bitcoin mining is an anti-cyclical business. As a result, the best time to grow is during periods of low prices, when inefficient miners face problems and exit the market.

At the current moment the equipment is at a great discount and the investments made now will bring returns faster. So, despite the negative news and the last few months of falling prices, this is a moment of great asymmetry, with reduced risk and high potential returns to make investments in bitcoin mining.

We are in a moment of great opportunities and those who invest now will be winners in the long run. In short, for businesses that are well structured and have strategic advantages that ensure efficiency, all the turbulence of this harsh winter points in the direction of a very favorable spring for growth.

This is a guest post by Ruda Pellini. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Let me tell you a story about what happens when you, and others, leave your bitcoin on exchanges. You might be surprised to hear what that means for your holdings. It might sound a lot like your own.

Let’s call our character Bill. Bill has been cautiously watching bitcoin for years, hearing about it in passing and reading a few articles. After inadvertently saving a lot of cash due to lockdowns, he decided to dive into bitcoin at last. A friend told him to check out Coinbase, Binance or another popular and “trusted” exchange in order to buy his first chunk of bitcoin.

So, Bill created an account and uploaded his face, ID, social security number, address and every other relevant detail about his life until he finally reached the “Buy Bitcoin” screen. He picked up a fraction of a bitcoin, but after all that trouble, he thought to himself:

“I don’t need to learn all these complicated technical details about hardware wallets and self custody — I just want my bitcoin safe.”

Bill reviewed the exchange’s website and decided that the security experts at the exchange, with their wiz-bang cold storage and state-of-the-art encryption, would be better at securing his bitcoin than he himself would be.

Bill was very pleased with himself after making that decision — not only did this exchange make investing in bitcoin simple, it gave him peace of mind knowing that someone else was responsible for keeping his assets safe from any kind of theft or malicious activity. After all, why should he have to worry about such things when there were professionals available who could handle them instead?

Bill has since become quite comfortable with the idea of trusting exchanges with his bitcoin — his coins are now safe from his own mistakes!

When Trust Disappears: The Fall Of FTX

When Bill turned on the news one morning and found out that the massive crypto exchange FTX had just paused withdrawals and seemed to “accidentally” lose $10 billion, roughly a third of its market cap, he was shocked.

How could a firm with its logo on the side of a major sports stadium and a CEO who appeared on CNBC, Bloomberg and in front of the U.S. Congress(!) to talk about digital assets and regulation have lost — or likely stolen — so much from right under everyone’s nose?

Now Bill was stuck between a rock and a hard place. He was suspicious of his own exchange, but setting up his own hardware wallet seemed so difficult and scary. It would require him to invest in a physical device, acquire the necessary knowledge to secure it properly and keep track of his seed phrase backup. Even if he figured out the basics, there was still the risk of misplacing his device or improperly storing his backup and losing access to his bitcoin.

FTX was shocking, but surely Bill’s exchange would never conduct itself the same way. People would see it before it was coming, and he’d have time to get out, right?

Reasons To Take Your Bitcoin Off Exchanges

It’s clear that trusting your bitcoin to an exchange brings with it the risk that you’ll log in one morning to find that your bitcoin just isn’t there. If you hold your bitcoin yourself using a hardware wallet, this can’t happen.

However, there’s another big reason it’s important to take your bitcoin off exchanges: the bitcoin price.

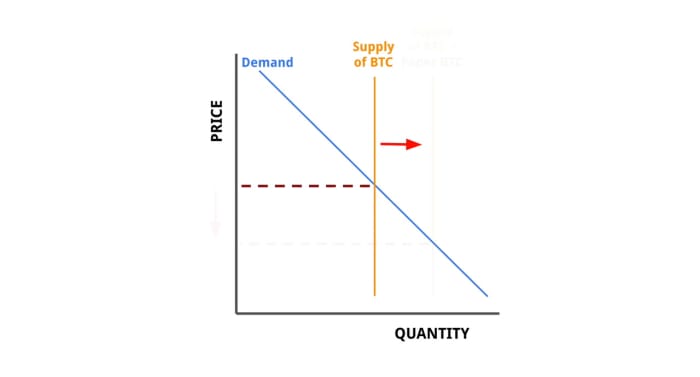

How could self custody affect bitcoin’s price? Everything in economics says that buying and selling affect the market price for a good, not who holds it. However, self custody is very important to price — and it has to do with something I’ll call “paper BTC.”

Introducing The Next Big Thing: Paper BTC

Let’s look at how an exchange works by considering a hypothetical exchange called ExchangeCorp, owned and operated by a jolly entrepreneur named Bernie. ExchangeCorp built an uncomplicated way to buy bitcoin, and hired a team of security experts to make sure hackers are kept at bay. Over time and through great marketing campaigns, ExchangeCorp built trust with traders and investors, drawing many in to store their bitcoin on the exchange.

When users keep their bitcoin with ExchangeCorp, the CEO Bernie and his team maintain control over those coins. Customers simply have a claim on their coins: they can log in and see their balance as well as request to withdraw their coins. However, if Bernie wants to transfer those coins owed to his customers to other Bitcoin addresses, he’s technically able to do so without any customer’s permission.

When Bernie kicks up his feet and looks at the balances in ExchangeCorp’s vault, he’s pleased to see tens of thousands of bitcoin that his customers have deposited sitting pretty. Since ExchangeCorp is doing well, more bitcoin are always coming in than going out.

So Bernie gets a wise idea. He could lend out some of those customer coins, earn some interest, and get the coins back without anyone noticing. He would get richer, and the risk of enough ExchangeCorp customers asking for withdrawals at one time to draw its vault’s massive balance down to zero is miniscule. So Bernie loans out thousands of coins here and there to hedge funds and businesses.

Now there’s another set of claims to consider. Customers have a claim on their bitcoin at ExchangeCorp, but ExchangeCorp no longer has the actual bitcoin — they only have a claim on the coin they lent out. What customers now have is a claim on Paper BTC held by ExchangeCorp, with the real bitcoin in the hands of borrowers.

This is where things get weird. All of ExchangeCorp’s customers still think they have a direct claim on real bitcoin held safely by ExchangeCorp. However, that real bitcoin is in fact in the hands of those who borrowed from ExchangeCorp, and those entities are selling it out in the market.

What happens when ExchangeCorp lends out a large quantity of the bitcoin its customers deposited? A lot of extra bitcoin starts to float around in the market, because investors who think they’re holding actual bitcoin are only holding paper BTC. All of that extra supply of bitcoin in the market absorbs buy pressure, which suppresses the price of bitcoin.

Let’s look at simple supply and demand here:

When paper BTC comes into the market, because market participants are unaware that this new supply is not real bitcoin, it has the same effect as increasing the supply of real bitcoin — until the fraud is uncovered.

Does this hypothetical story sound anything like the recent news around FTX?

The Paper BTC At The Center Of The FTX Fraud

The story of ExchangeCorp and Bernie is exactly the story of FTX and its founder Sam Bankman-Fried, with some save-the-world complexes, study drugs and polyamorous orgies redacted.

By lending out customer funds, FTX essentially inflated the supply of bitcoin by taking advantage of the trust users placed in FTX to safeguard their funds. FTX created tons of paper BTC.

Just how much paper BTC might FTX have created? We cannot be sure of the exact amounts given its absolutely horrid bookkeeping, but the estimate below suggests FTX had 80,000 paper BTC on its books — bitcoin owed to customers that is not backed by real bitcoin.

That would represent a staggering 24% of the roughly 330,000 new bitcoin that were created over the past year through the predictable mining issuance process. That is a ton of extra bitcoin entering the market that nobody — aside from a small group of insiders at FTX — knew about!

It’s impossible to tell where the price would have gone without that extra bitcoin supply entering the market, but we can be almost certain that the price would have climbed higher than it did in 2021.

While the FTX collapse is recent and still unfolding, history has a few cautionary tales to tell about the dangers of paper assets and price manipulation. The story of gold’s failure to resist centralized capture, for instance, can tell us where Bitcoin is headed if we continue to trust exchanges and third parties to hold our bitcoin for us.

The Fall Of Gold

Gold was once used in daily transactions — it takes no more than a visit to a museum of ancient history to see the collections of old gold coins once circulating in local markets. The traditional view of the demise of gold as a transactional currency was that it became too cumbersome or too valuable to continue to function well as a means to buy groceries and beer.

However, this story omits a few key components that only reveal themselves when we trace the evolution that societies took from gold coins to paper bills and digital bank accounts.

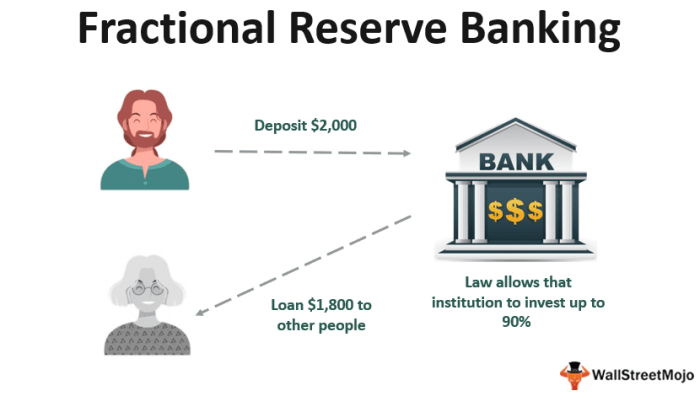

Centuries ago, banks started taking customer’s gold in exchange for bank notes — giving customers a measure of security for their gold and a more convenient means of transacting. However, entrusting a bank with your precious metal meant the bank was able to lend it out or make bad investments without the depositor’s consent. When a bank was caught between bad loans and a high rate of depositor withdrawals, they had to declare bankruptcy and shut down — leaving many depositors penniless, holding paper claims on gold now worth nothing at all.

Then central banks came along to “fix” the problem of bankrupt banks leaving depositors penniless. Central banks held gold for people and commercial banks, giving them banknotes from the central bank as receipts for their gold. By 1960, central bank official holdings accounted for about 50% of all aboveground gold stocks, with their banknotes circulating freely. Commercial banks and individuals didn’t mind, since each note was convertible to a set weight of gold by the central bank that issued it.

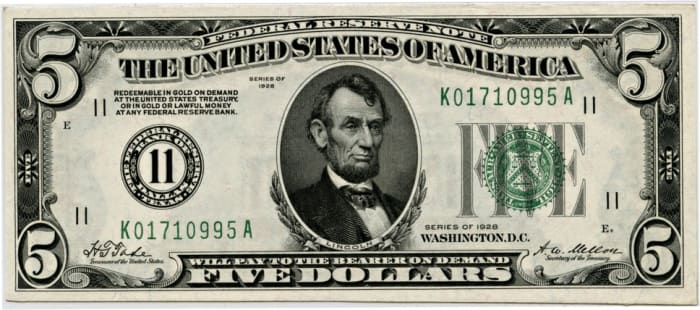

Notice the note in the upper left? This $5 Federal Reserve note — also known as a $5 bill — is redeemable in gold. Source

This would have worked well, except that central banks — especially the Federal Reserve in the U.S. — started creating more bills than they had gold to back. Creating more bills than the Fed had gold to back was essentially creating paper gold, since each bill was a claim on gold. Doing this in secret meant the Fed was manipulating the price of gold, given the extra circulating supply which the market was not aware of. When many depositors of gold at the Federal Reserve — like the French government — started questioning the Fed’s gold holdings and creating the threat of a run on gold in the U.S., the U.S. government had to intervene.

In 1971, this came to a head with the Nixon shock. One night, President Nixon announced the U.S. would temporarily stop allowing depositors to trade in their Federal Reserve notes for the gold they promised.

This temporary halt in withdrawals was never lifted. Since all currencies were connected to gold through the U.S. dollar under the Bretton Woods agreement, the Nixon Shock meant that the entire world went off the gold standard at once. All currencies were now just pieces of paper, instead of notes giving the holder a claim on a quantity of gold.

This was only achievable because gold, over time, was deposited into commercial banks and then to central banks. Once central banks held most of the gold, they could manipulate the price of gold and remove it entirely from daily commerce. Everyday people chose the convenience of paper notes over the security of holding gold, and paid the price.

Instead of a neutral money backed by a precious metal that is difficult to dig up and impossible to synthesize, currencies became easy to print and thus highly politicized. Keeping the dollar at the top of the food chain no longer required restraint and good stewardship to ensure its backing in gold. Instead, it required military expeditions and strong policing to ensure global governments and citizens continued to use the dollar to transact.

A return to gold at this point would be impractical — the world’s commercial networks span too great a distance with transactions happening at too high a speed. With paper currency and eventually digital banking systems, what we gained in speed and convenience we lost in soundness and neutrality. We lost our savings, our social cohesion and our political institutions as a result.

Preventing Bitcoin’s Fall

Taking your bitcoin off of your exchange is not just good practice for your own security, it’s protecting the price of your bitcoin as well. Our freedoms depend on individuals having control over their own wealth. When we entrust our wealth to companies or states, we go down the path we witnessed with gold.

Thanks to bitcoin’s divisibility and digital nature, it overcomes the hurdles that held gold back from supporting our modern, interconnected economy. Bitcoin can support a global marketplace, but it will only get there if we each hold our own bitcoin.

Don’t let the banksters and bureaucrats manipulate the price of your bitcoin: take it off the exchange and get it on your own hardware wallet.

This is a guest post by Captain Sidd. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

A laboratory technician works at a health and science centre in Bangkok, Thailand. It is a WHO Collaborating Centre for research and training on viral zoonoses. Credit: WHO/P. Phutpheng

Opinion by Roopa Dhatt – David Bryden – Gill Adynski (washington dc/ chapel hill, north carolina/ geneva)

Inter Press Service

WASHINGTON DC/ CHAPEL HILL, NORTH CAROLINA/ GENEVA, Dec 19 (IPS) – Health services don’t deliver themselves. It is the nurse who triages in the emergency department, the midwife who delivers babies and cares for mothers, the community health worker who gives babies vaccines, the care assistant who bathes someone at home, the surgeon who performs the operation, the anesthetist who blocks the pain, the pharmacist who matches the script to the medication, and the physiotherapist who restores movement.

Universal Health Coverage Day on 12 December is the annual rallying point for the growing movement for health for all. It marks the anniversary of the United Nations’ historic and unanimous endorsement of universal health coverage in 2012.

With Universal Health Coverage Day (December 12) just behind us, it is critical to recognize the contribution of health workers, most of whom are women, and call for political leaders to urgently recognize and address the escalating resignations, shortfalls, and staff movements putting health security at all levels, from local to global at risk.

Listening to organizations who represent frontline health workers, community health workers, nurses, family doctors, and health professionals, we hear that after nearly three years of a pandemic there is worker burnout, staff shortages, migration of health workers, increasing reports of danger and violence at work, and rising mental health concerns.

Taken together, there are four alarming trends currently affecting health workers’ ability to deliver health services for all and hindering our advancement towards UHC.

Global shortage of health workers

WHO figures released in April this year estimated a projected global shortage of 10 million health workers in 2030 based on current trends (mostly depicting a pre-COVID-19 situation). Since then, in the US alone, the US Bureau of Labor Statistics now estimates that more than 200,000 registered nurse positions are projected to be vacant annually over the next decade and WHO points out the largest shortages will be in Africa and Southeast Asia.

Globally, burnout levels among doctors and nurses have been estimated at 66 percent, a figure that doesn’t bode well for future health worker retention or indeed the ability to attract new recruits. Lack of available health workers, particularly in the global south where disease burden is higher, was the biggest obstacle to maintaining health services and delivering vaccines during COVID-19, according to WHO.

Protection of health workers

The pandemic stretched already understaffed and under-resourced health systems, increasing pressure and danger. Too often women were issued medical personal protective equipment (PPE) designed for male bodies that left them at risk. Health workers were sent door-to-door to enforce lockdowns or do contact tracing or give vaccines with no added protection, facing angry, confused, or frightened people.

They worked extra shifts under horrendous conditions, many with little or no extra pay. It is no wonder that the International Council of Nurses described the COVID-19 effect as a “mass traumatization of the world’s nurses.” The average prevalence of PTSD among global health workers is estimated to be around 17 percent, but this figure is much higher for women frontline workers, at 31 percent.

Advocates for health equity have a responsibility too, to bring the same passion that we see, for instance, in the global struggle for access to COVID vaccines, to the cause of equity and fairness for health workers who deliver these vaccines.

Women are disadvantaged in promotions too: despite 70 percent of health workers and 90 percent of frontline health workers being women, men hold around three quarters of the leadership positions. Historically female professions, like nursing and midwifery, have workers of all genders but they face difficulties advancing into leadership positions due to historical biases against them as caring and nurturing professions, where they are not seen as leaders.

The “Great Resignation” in health

Unsurprisingly, there is a Great Resignation in health–worldwide we see a flood of women health professionals who are planning to or have already left their jobs. In the summer of 2021, in the UK alone, more than 27,000 staff voluntarily resigned from the NHS amid burnout caused by a combination of pandemic pressures and staff shortages. In Ghana, most health workers experienced high levels of stress (68 percent) and burnout (67 percent) citing lack of preparedness as a key factor.

A billboard on a Nairobi freeway advertises for nurses to move to Germany. On Facebook pages, we find hundreds of advertisements for health workers to move to the UK. The incentive for international moves is fast-track visas and better pay. And why wouldn’t health workers give serious consideration to moving somewhere with better pay or more training or the chance to earn enough to send money back to their families?

There are serious implications as nurses from low-income countries leave their health systems to prop up others in wealthier countries that have failed to train health workers of their own. It is estimated that this Great Migration of health workers costs LMICs an estimated $15.85 billion annually in excess mortality.

While any individual has the right to migrate freely, recruiting companies actively recruit nurses while violating the Global Code of Practice on International Recruitment of Health Personnel, further exacerbating health worker shortages in areas that need health workers most.

Africa has only four percent of all health workers in the world, but more than 50 percent of the 10 million health workforce shortage is in Africa. With the Great Resignation and the Great Migration, these are serious concerns and were pointed out by Heads of State at the U.S.-Africa Leader’s Summit last week.

Universal health coverage should not just be about individuals and communities getting better and more affordable health services, it should also be about recognising health workers, their roles, and their needs. Health workers need safe working environments free of violence and harassment that give them all the resources they need to do their jobs well.

Appreciation isn’t just about applause. It’s about governments, which are responsible for the health of their citizens, ensuring systems are properly resourced–from hospitals to home aid. From guaranteeing equity in pay to properly paid work. From provision of proper PPE to safety at work in all conditions. And making sure that career choices and promotions are open to all, regardless of gender.

If global leaders are serious, then it’s time they do more, as they have promised, and accelerate their efforts to achieve universal health coverage and the 2030 Agenda for Sustainable Development. The Working for Health 2022-2030 Action Plan sets out how countries can support each other to build and strengthen their health and care workforce.

Our overburdened health workers have signaled that they have had enough. They have continued to protect us despite the shortages, lack of protection and problems related to pay, but they are burnt out. It is time we moved from applause to action and begin finally, to address the known problems plaguing global health systems.

This is an opinion editorial by Mark Maraia, author of “Rainmaking Made Simple” and Holly Young, a builder within the Portuguese Bitcoin community.

We’ve all been there. You’re at a social event and a friend, acquaintance or relative comes up to you and says “you were into Bitcoin, right?” You know you only have a brief period of their attention to give them an overview and pique their interest. So how can you give them an intelligible take on such a complex, multifaceted subject?

Here are a few ideas for you to pick and choose from for the next time you find yourself in that situation!

Centralisation Is The Enemy Of Property

Any currency which is centralized can be taken away from you in two ways. It can be done directly, by simply skimming it off your bank account as happened in Greece when people lost 20% of whatever was on their account to a government haircut in 2015 and 16, or by cutting your access to your own assets, as has just been shown by America and the U.K. doing this to Russian corporations or individuals during the current crisis in relations around the Ukraine. Secondly, because all our fiat currencies are centralized, this can be done through inflation — the government simply prints more money which means that whatever you have in your bank account will lose its value — also effectively robbing you of your purchasing power.

Bitcoin is a new kind of digital money that will never be issued or controlled by a corporation or government. It is a new form of money, unlike anything we’ve ever seen before and is a 21st century hedge against inflation and central bank money printing. Unlike the US dollar, it is a provably scarce digital asset that is backed by a wall of encrypted real world energy. These coins reached parity with the U.S. dollar ten years ago and are now worth 20,000 times more than the dollar.

Because it is both scarce and totally decentralized, it is deflationary, and no one can take it away from you as long as you keep it in a storage which is not connected to the internet.

What Is Bitcoin?

The term bitcoin can really mean two things: bitcoin the asset (currently worth 20,000 times more than the USD) and Bitcoin the network which is growing faster than the internet or Facebook or Amazon. Bitcoin the asset travels along digital rails (a shared distributed ledger where a record of all the Bitcoin transactions is kept) that are decentralized onto tens of thousands of devices and computers. This digital asset is a 21st century savings technology which uses military grade encryption and permits you to store value and wealth on a smartphone or hardware device called a wallet.

It allows those who buy it to store the fruit of their labor (or life force) and wealth using software, math and energy that is almost impossible to steal directly or indirectly (through inflation) Once you learn the language of bitcoin, you realize that anyone holding government issued currency (which is all of us) is watching their wealth melt like an ice cube in the sun as the fiat value inflates, and hyperinflated when measured against bitcoin. Anyone who cares about keeping their wealth in the future ( and that should be all of us, especially those of us who have children and intend to leave them an inheritance) needs to wake up and smell the coffee. Fiat currencies are losing their value fast, and although Bitcoin is still volatile, everything points towards it holding its value long term.

The Bitcoin Network Has Never Been Hacked

In 13 years. The Bitcoin network is rock solid.

How Bitcoin Works In A Nutshell

Bitcoin runs on a blockchain. As its name suggests, a blockchain is made up of blocks. Each time a new block is confirmed it gets added to the blockchain. Bitcoin blocks are confirmed by computers known as miners and each time a miner solves the math problem which confirms a block, it gets a reward in new Bitcoin, a process written into the original Bitcoin code. This takes a lot of energy and is the system which keeps the Bitcoin blockchain safe.

Bitcoin mining is the energy intensive process which both creates new coins and maintains a log of all transactions performed on the bitcoin network since its inception. Bitcoin miners take real world energy (stranded and renewable) and convert it into monetary energy that will outlive your grandchildren. The more energy used by bitcoin miners, the more secure and unhackable the network becomes.

The protocol has a fixed supply schedule that issues 6.25 coins into the network about every 10 minutes. In 2024 the supply issuance will be cut in half to 3.125 coins every 10 minutes.

Each time a Bitcoin transaction is made, it’s recorded into the next block. Once that block is confirmed and added to the blockchain it can never be deleted.

Who Uses Bitcoin?

More and more individuals are using Bitcoin. It’s been estimated that in the first half of 2021, the number of people using Bitcoin grew by just under 165 per minute (“How Fast Is Bitcoin Growing?”). That’s a lot of people and a lot of growth.

Bitcoin is the first and only digital asset to be named as legal tender by a nation state. Bitcoin is the first and only asset in history to be named a primary treasury reserve asset by a Fortune 500 company, Microstrategy, an intelligence software company.

Here’s what their CEO, Michael Saylor, had to say about it:

“We converted our balance sheet from a depreciating asset to an appreciating asset. So we have two businesses. One is enterprise software business and the other is digital property business. So why did we do it? Defensively, I don’t want to lose money or destroy the value of the company. Wealth is destroyed. Stage two is opportunistic, we could buy high quality property. Digital property is better than analog property. Stage three is strategic. It’s a good idea to buy up cyber Manhattan before everyone else moves here. If bitcoin is appreciating at 100% per year and I can borrow fiat at 5% then my arbitrage is 95%. Why would I NOT do it?”

There’s A Lot Of Negativity About Bitcoin In The Press

If we look back at history, it’s been pretty rare for a king to be deposed from his throne by a newcomer without putting up a bit of a fight. The fiat banking system has been king almost since its invention by the Medici. It’s not going to go quietly. The fiat system has been able to dictate the terms and its employees profit massively from doing so. Until, that is, Bitcoin came along, the upstart King Arthur who, against all odds, has pulled the sword from the stone. And do the central banks and the governments like that? They do not.

It’s a key reason why central bankers attack and spread untruths about bitcoin.

What are those lies? It’s not backed by anything. It wastes energy. It’s volatile. It is controlled by billionaires. It has no practical uses. It’s primarily used by criminals and terrorists. It’s a Ponzi scheme.

Rubbish. Bitcoin has the potential to upset the current status quo — hence why it’s so maligned by those currently holding the microphone.

You Can Buy A Fraction Of A Bitcoin

Sure, most of us don’t have 20,000 odd dollars just lying around which we could spare to buy a whole Bitcoin with. One Bitcoin divides into one hundred million Satoshis – which means that you can invest 10 dollars in Bitcoin as a start investment, should you so desire.

“Bitcoin is our peaceful weapon of choice against central bank driven time theft.” — Ross Stevens

“Bitcoin is a currency for the people backed by the people.” — Sylvain Laurel

This is a guest post by Mark Maraia and Holly Young. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

When you hear or read about an investing expert’s outlook for the year ahead, bear one thing in mind: Every forecast about 2022 was wrong.

Not just a bit amiss, but complete, total busts.

Oh, some strategists will claim victory for saying the stock market SPX, -1.11%

would be down in 2022 or that Treasury bonds TMUBMUSD10Y, 3.488%

would have yields north of 3%. Or that the yield curve would invert or that inflation would be stickier than anticipated. But they don’t deserve laurels for that.

No one said the market would peak on the first day of the calendar year and go downhill from there and, ultimately, that’s the only tale of 2022 that investors will remember.

Expect forecasts for 2023 to be equally miscalculated.

That doesn’t mean investors should ignore or dismiss the exercise of experts offering outlooks, but it’s why you should question the motives of the soothsayers and revisit one of the greatest market forecasts of all time that’s well on its way to becoming true no matter what the market dishes out next year.

Face it, market strategists and economists don’t make forecasts because they want to, but rather because they have to. Keeping their jobs depends on making mostly lame predictions.

Say something memorable, and the expert and firm might be held accountable for it; pabulum, however, gets overlooked when it’s wrong.

Obvious observations

Thus, forecasts lack insight, gravitating toward the middle ground, to obvious observations on the effect of economic and stock market cycles.

“It looks bad if they don’t have an opinion, but worse when they get something wrong, so most forecasts say as little as possible,” said Jeff Rosenkranz, a fixed-income portfolio manager at Shelton Capital Management, after we finished an interview last week for my podcast, “Money Life with Chuck Jaffe.” “You’re not getting much insight — if they have really valuable insights, this isn’t where they want to tell the world — so most forecasts just aren’t worth much.”

Adds Howard Yaruss, a New York University professor and author of the recent book “Understandable Economics”: “If you are talking about a fine-tuned forecast about stocks and asset values, I don’t see how anyone could go there; accurate predictions aren’t going to happen, or will be luck if they turn out true. Their statements are more about marketing than the market.”

One of Wall Street’s best-known prognosticators says credibility is impossible without accountability, but he acknowledges the tightrope experts walk if they say too much.

Bob Doll, chief investment officer at Crossmark Global Investments, started making forecasts — 10 specific prognostications covering markets, the economy, politics and more — in the 1990s while working for Oppenheimer. He carried the exercise with him during well-chronicled career stops at BlackRock BLK, +0.29%,

Nuveen and elsewhere, and historically has been right on north of 70% of his calls.

‘Wordsmithing’

“There’s wordsmithing going on; you word them so that you have a noticeably higher than 50% chance of getting them right, and then say a few things you truly believe in that will make you look really smart if they happen without making you look dumb for believing it,” Doll says.

Good forecasts are not just an academic, rote exercise, Doll says, provided that they’re relevant, prompt thoughtful reactions from the audience and that the expert stands by them. Doll revisits his forecasts every quarter and doesn’t alter them in response to current events.

“You call the beast as you see it,” he says, “and then you stand by it and live with it, and you don’t worry about getting them all right because if you haven’t gotten something wrong, you’ve only said the obvious.”

Wildest market forecast

Which leads to what I think is the best, wildest market forecast of all time, even if it’s more obvious than it appears: Dow DJIA, -0.85%

116,200.

If that sounds far-fetched with the Dow Jones Industrial Average standing at roughly 33,500 — and down about 8% since the start of the year — consider that the prognostication was made in 1995 with the index hovering around 4,500.

Also, the call was for the benchmark to hit that level in 2040.

Bill Berger, founder of the Berger Funds — which merged into the Janus funds in 2002 — made the call at the first Society of American Business Editors & Writers Conference on Personal Finance in Boston, giving one of the best talks I’ve ever heard, mostly railing against forecasting and the habit of making too much of market milestones.

(If the Dow 116,200 prediction rings familiar to you, chances are you learned about it from me, as I raised it periodically while working as senior columnist for MarketWatch between 2003 and 2017. Today marks the return of my column to this site, and I’m glad to be back.)

Berger cited what he called “the two rules of forecasting.”

Rule 1: For each forecast, there is an equal and opposite forecast.

Rule 2: Both of them are wrong.

Ironically, 116,200 sounds implausible, but looks dead solid perfect.

By 1995, Berger had worked in investments for 45 years; when he got started, the Dow was below 200. Mathematically, he saw the Dow’s future as reflecting the past; repeating the growth he’d lived through would push the benchmark to 116,200 over the next 45 years.

A septuagenarian at the time, Berger wryly suggested that if he was proved wrong, people come find him to discuss it; sadly, he died a few years later.

The long game

Despite the outlandishness of the forecast, Morningstar calculates that hitting the target would have required an annualized gain of roughly 7.35% over the 45 years. When the Dow peaked on Jan. 4, 2022, the necessary gain was down to 6.33% annualized.

As of Dec. 1, Morningstar calculates that hitting 116,200 in the fall of 2040 will take a 7.07% annualized gain, which feels like a safe bet.

Thus, 2022’s disappointments haven’t derailed long-term investors any more than they’ve crashed the greatest-ever market forecast.

That’s the lesson to remember when confronted with 2023 forecasts; neither the market’s issues nor experts’ ability to diagnose them will derail long-term financial plans or make lifetime goals unreachable.

NEW YORK, Dec 16 (IPS) – The writer is Deputy Director, Bureau for Policy and Programme Support, UNDPClimate change is the defining issue of our time. In the words of the UN Secretary General at COP27, “we are on a highway to climate hell with our foot still on the accelerator.” Cutting greenhouse gas emissions to net-zero by 2050 is crucial when it comes to meeting the 1.5 degrees Celsius target.

At the same time, if we don’t effectively deal with corruption in climate action, it will severely impede our abilities to fight the climate crisis through scaled-up adaptation and mitigation efforts.

According to Transparency International, up to 35 percent of climate action funds, depending on programme, have been lost to corruption in the last five years.

Corruption and the climate crisis reinforce each other

On the one hand, corruption fuels the climate crisis by depriving countries of much-needed revenues to act on climate change and build resilience, while also significantly altering the efficient allocation and distribution of resources to achieve development objectives.

For example, according to the U4 Anti-corruption Resource Centre, the top recipients of climate finance are among the riskiest places in the world for corruption.

On the other hand, climate impacts reinforce corruption by creating economic and social instability and inequality, fostering an environment more conducive to corruption and misuse of funds, that ultimately deprives the poorest and hardest hit.

Overcoming corruption in the race against the climate crisis requires collective action and bold partnerships between government, private sector, and civil society to recognise and combat the issue through more effective management of resources and programmes.

This calls for:

• Governments to step up their efforts in environmental governance,

• Businesses to strengthen business integrity,

• Media, youth, and communities to continue to advocate against corruption.

The three immediate actions that require commitment from all actors:

1. Management of funds: A much greater transparency and accountability is needed in the use and management of climate finance in adaptation and mitigation programmes.

Access to finance is often presented as the main obstacle to achieving a just transition and transformative climate action, but that’s only one side of the problem. The other side is to make sure that the much-needed resources to address climate crisis are not lost due to corruption and mismanagement.

One good example is that of the Colombian climate finance tracking system, which provides updated data on domestic, public, private, and international climate funding.

It is one of the first countries in the world to have developed a comprehensive Monitoring, Reporting and Verification (MRV) framework to transparently track the inflow and outflow of climate finance from public, private and international sources.

2. Voice and Accountability: This means leveraging the power of advocacy and accountability mechanisms, and providing civic spaces for meaningful participation of society, empowering them to hold policy makers and private sector accountable.

For example, UNDP is empowering communities in Uganda and Sri Lanka, to use digital tools to mainstream integrity and transparency in environmental resource management. In Sri Lanka,

UNDP has launched a digital platform, in collaboration with the Ministry of Wildlife and Forest Conservation and other partners, for citizens to engage and monitor illicit environmental activities. The initiative is supported through UNDP’s Global Project – Anti-Corruption for Peaceful and Inclusive Societies (ACPIS) funded by the Norad— Norwegian Agency for Development Cooperation.

Meanwhile, in Uganda, UNDP and the National Forestry Authority have launched the Uganda Natural Resource Information System (NARIS), designed to monitor and mediate deforestation throughout Uganda to protect the country’s forests and biodiversity.

In the climate change agenda, fighting corruption is not only about the money. It is also about building trust in institutions and restoring hope in the future. Studies show that ‘eco-anxiety’ is increasing, particularly amongst young people.

A global study of 10,000 youth from 10 countries in 2021 found that over 50 percent of young people felt sad, anxious, angry, powerless, helpless, and guilty about climate change. But we have also seen youth, civil society and communities taking action against the environmental damage and climate change from Serbia to India.

3. Private sector has a key role to play: Public capacity needs to be strengthened to implement policies to regulate private sector activities to protect the environment. At the same time, businesses should also play their part with fair, human-rights based business practices, business integrity, and environmental sustainability goals.

4. The normative framework to protect human rights: An intensified focus on ‘environmental justice’ at global and national level is needed. On 28 July 2022, the UN General Assembly adopted a historic resolution that gave universal recognition to the human right to a clean, healthy, and sustainable environment (R2HE). UNDP promotes responsible business by strengthening human rights standards across 17 countries, with support from Japan.

UNDP has supported over 100 national human rights institutions to address the human rights implications of climate change and environmental degradation. In Tanzania, UNDP has supported the ‘Commission for Human Rights and Good Governance’ to manage disputes related to environmental human rights violations. In Chile, UNDP has supported an ongoing process of constitutional reform which includes strong references to environmental rights.

The development community needs to ensure integrated approaches and break the siloes between the governance and environmental communities; and between public and private sectors to tackle the interlinked crises of corruption and climate change.

This is an opinion editorial by Mitchell Askew, a Christian, conservative Bitcoiner who produces Bitcoin-related research and social media content for Blockware Solutions.

“You don’t change Bitcoin, Bitcoin changes you.”

This is one of many mantras circulating around the Bitcoin community. I am two years removed from the start of my Bitcoin journey and can personally attest to the legitimacy of this statement. While my experience in Bitcoin is relatively short-lived, people can grow a great deal in two years, especially those in their early 20s. Bitcoin is a never-ending quest for knowledge and anyone who joins the expedition will in due time find themselves embracing the cardinal virtues.

The cardinal virtues, deeply rooted in Christianity and among philosophers such as Plato and Aristotle, represent a universal foundation of moral guidance. The virtues are prudence, temperance, justice and fortitude. They were dubbed “cardinal” from the Latin root “cardo,” which means “hinge,” as in: all other virtues hinge (rely) upon the four cardinal virtues.

I have outlined how anyone in honest pursuit of the Bitcoin mission to separate money and state is strongly incentivized to behave according to the cardinal virtues.

Bitcoin Instills Prudence

Acting with or showing care and thought for the future.

You will not understand what Bitcoin is the first time you hear about it. Nor will you have a firm grasp the second, third or fourth time. In today’s fast-paced world, few have put in the hours necessary to have a solid understanding of how Bitcoin functions, technically. Of those that have, even fewer have taken the time to study all of the encompassing domains of Bitcoin, including but not limited to economics, personal finance, computer science, energy markets, the history of money and geopolitical game theory.

To say that Bitcoin will have a profound impact on the world is an understatement. To begin having the slightest understanding of what the impact will be requires prudence. In the words of Michael Saylor “there are no informed critiques.” Those who immediately dismiss Bitcoin as a Ponzi scheme no different than those of Bernie Madoff or Sam Bankman-Fried, are simply exposing their intellectual sloth.

A common theme among Bitcoiners, popularized by Austrian economists such as Saifedean Ammous, is the concept of time preference. To have a low time preference means that you are willing to place more emphasis on your future wellbeing relative to your present wellbeing; this quite literally is the definition of prudence. Those who engage in the speculative markets of altcoins, or attempt to trade bitcoin’s unpredictable short-term volatility, rather than HODL the least uncertain asset of all time, are inherently imprudent.

By putting in the hours necessary to have a basic understanding of Bitcoin’s technical fundamentals and its broad implications on society, you have exhibited prudence.

Bitcoin Instills Temperance

Habitual moderation in the indulgence of the appetites or passions.

Similar to prudence, Bitcoiners achieve temperance through low time preference behavior.

Contrary to common FUD propagated among no-coiners, Bitcoin is not full of whales seeking to dump their positions in pursuit of fiat-denominated profit. Moreover, the exponentially-increasing adoption of Bitcoin coupled with its immutably scarce supply means that each wave of newcomers are met with the realization that it is wise to acquire as much bitcoin as possible before the rest of the world catches on.

When bitcoin becomes your individual unit of account, you begin weighing every potential purchase or experience against the opportunity cost of acquiring more bitcoin. This has led to many Bitcoiners, including myself, embracing minimalist lifestyles. The key point here is that this declination of materialistic goods in pursuit of more bitcoin, though perhaps initially sparked by a desire to satisfy future greed, brings forth the realization that an abundance of materialistic goods is unnecessary.

By eliminating many of the “wants” from your personal budget, i.e., moderating the indulgence of appetites or passions, and limiting yourself to “needs” in order to save wealth in bitcoin, you are embracing the cardinal virtue of temperance.

Bitcoin Instills Justice

Just dealing or right action; giving each person his or her due.

The biggest financial fraud of all time is the fiat monetary system. For far too long, the existence of central banks has provided governments with the ability to fund the ideals of the ruling class at the expense of cash savings and future economic productivity. Prior to the rapid acceleration of inflation during the past couple of years, most Westerners were completely unaware of the backdoor thievery that occurs with the expansion of the money supply.

Bitcoin grants inalienable property rights to all of its users. No government agency or corporation has the power to dilute the value of each unit in the network and, when stored properly, BTC is virtually impossible to confiscate. Bitcoin is an open, neutral network that does not discriminate based on religion, ethnicity, sex, race or vaccination status. Nobody is restricted from running a node to audit the authenticity of each transaction on the ledger.

By guaranteeing irrefutable access to an unconfiscatable and undilutable form of property, Bitcoin represents the most just asset and monetary network in the history of mankind.

Bitcoin Instills Fortitude

Courage in pain or adversity.

Bitcoiners develop fortitude in two ways.

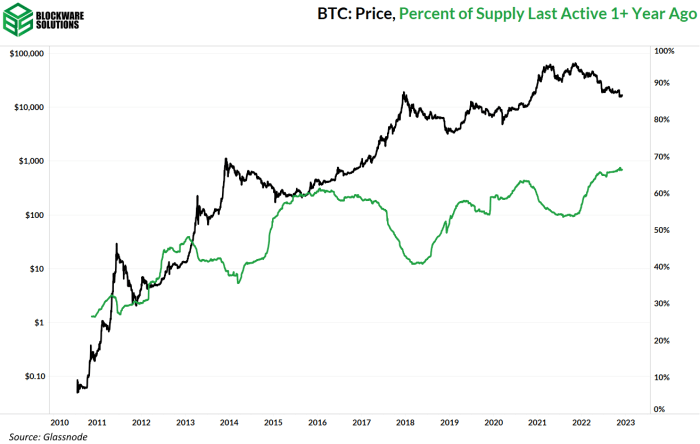

The first way is by encouraging HODLing through volatility. At the time of this writing, bitcoin is down by over 70% from its all-time high. This is the fourth time in Bitcoin’s thirteen-year history that we have experienced a drawdown of this magnitude. Bitcoiners are clearly exhibiting courage in the face of this adversity as evidenced by on-chain data. An all-time high of over 66% of Bitcoin’s supply has not moved in one year or longer. This fortitude is not unprecedented either, as this metric has hit all-time highs during previous bear markets as well.

I sense that a positive feedback loop is occurring here. When you can see for yourself that other bitcoin holders are undisturbed by the extreme drawdowns in price, it enables one to become more confident in the future of the network, and thus continue HODLing themselves.

The second way in which Bitcoiners develop fortitude is by encouraging Bitcoiners to take an action akin to the founding fathers signing of the Declaration Of Independence. While holding bitcoin is not outright illegal in most countries, it certainly does not put you in a favorable standing with the most powerful entities in the world.

History has shown that regimes in control of the global reserve currency do not take kindly to that position being usurped. As such, there is a non-zero chance that Bitcoiners could be declared treasonous in a dramatic, last-chance attempt by the United States government to maintain control over the monetary system.

However, this extremity can be avoided by winning the race of adoption as Cory Klippsten, CEO of Swan Bitcoin, eloquently describes in this article.

This is a guest post by Mitchell Askew. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

This is an opinion editorial by Leon Wankum, one of the first financial economics students to write a thesis about Bitcoin in 2015.

Evolutionary psychologists believe that the ability to “preserve wealth” gave modern humans the decisive edge in evolutionary competition with other humans. Nick Szabo wrote an interesting anecdote about how in his essay “Shelling Out: The Origins of Money.” When homosapiens displaced homo neanderthalensis in Europe circa 40,000 to 35,000 B.C., population explosions followed. It’s difficult to explain why, because the newcomers, homosapiens, had the same size brain, weaker bones and smaller muscles than the neanderthals. The biggest difference may have been wealth transfers made more effective or even possible by collectibles. Evidence shows homosapiens sapiens took pleasure in collecting shells, making jewelry out of them, showing them off and trading them.

It follows that the capability to preserve wealth is one of the foundations of human civilization. Historically, there have been a variety of wealth preservation technologies that have constantly changed and adapted to the technological possibilities of the time. All wealth preservation technologies serve a specific function: storing value. Chief among the early forms is handmade jewelry. Below I will compare the four most commonly used wealth preservation technologies today (gold, bonds, real estate and equities) to bitcoin to show why they underperform and how efficiently bitcoin can help us save and plan for our future. For equities, I focus specifically on ETFs as equity instruments used as a means of long-term savings.

Detail of necklace from a burial at Sungir, Russia, 28,000 BP. Interlocking and interchangeable beads. Each mammoth ivory bead may have required one to two hours of labor to manufacture.

What Makes A Good Store Of Value?

As explained by Vijay Bojapati, when stores of value compete against each other, it is the unique attributes that make a good store of value that allows one to out-compete another. The characteristics of a good store of value are considered to be durability, portability, fungibility, divisibility and especially scarcity. These properties determine what is used as a store of value. Jewelry, for example, may be scarce, but it’s easily destroyed, not divisible, and certainly not fungible. Gold fulfills these properties much better. Gold has over time replaced jewelry as humankind’s preferred technology for wealth preservation, serving as the most effective store of value for 5,000 years. However, since the introduction of Bitcoin in 2009, gold has faced digital disruption. Digitization optimizes almost all value-storing functions. Bitcoin serves not only as a store of value, but also as an inherently digital money, ultimately defeating gold in the digital age.

Bitcoin Versus Gold

Durability:Gold is the undisputed king of durability. Most of the gold that has been mined remains extant today. Bitcoin are digital records. Thus it is not their physical manifestation whose durability should be considered, but the durability of the institution that issues them. Bitcoin, having no issuing authority, may be considered durable so long as the network that secures them remains intact. It is too early to draw conclusions about its durability. However, there are signs that, despite instances of nation-states attempting to regulate Bitcoin and years of attacks, the network has continued to function, displaying a remarkable degree of “anti-fragility”. In fact, it is one of the most reliable computer networks ever, with nearly 99.99% uptime.

Portability: Bitcoin’s portability is far superior to that of gold, as information can move at the speed of light (thanks to telecommunication). Gold has lost its appeal in the digital age. You can’t send gold over the internet. Online gold portability simply doesn’t exist. For decades, the inability to digitise gold created problems in our monetary system, historically based on gold. With the digitization of money, over time it was no longer comprehensible whether national currencies were actually backed by gold or not. Also, it is difficult to transport gold across borders because of its weight, which has created problems for globalised trade. Due to gold’s weakness in terms of portability, our current fiat-based monetary system exists. Bitcoin is a solution to this problem as it is a native digital scarce commodity that is easily transportable.

Fungibility: Gold can be distinguished for example by an engraved logo, but can be melted down and is then fully fungible. With bitcoin, fungibility is “tricky”. Bitcoin is digital information, which is the most objectively discernible substance in the universe (like the written word). However, since all bitcoin transactions are transparent, governments could ban the use of bitcoin that has been used for activities deemed illegal. Which would negatively impact bitcoin’s fungibility and its use as a medium of exchange, because when money is not fungible, each unit of the money has a different value and the money has lost its medium of exchange property. This does not affect bitcoin’s store-of-value function, but rather its acceptance as money, which can negatively impact its price. Gold’s fungibility is superior to bitcoins, but gold’s portability disadvantages make it useless as a medium of exchange or a digital store of value.

Scarcity: Gold is relatively scarce, with an annual inflation rate of 1.5%. However, the supply is not capped. There are always new discoveries of gold and there is a possibility that we will come across large deposits in space. Gold’s price is not perfectly inelastic. When gold prices rise, there is an incentive to mine gold more intensively, which can increase supply. In addition, physical gold can be diluted with less precious metals, which is difficult to check. Furthermore, gold held in online accounts via ETCs or other products often has multiple uses, which is also difficult to control and negatively impacts the price by artificially increasing supply. The supply of bitcoin, on the other hand, is hard-capped, there will never be more than 21,000,000. It is designed to be disinflationary, meaning there will be less of it over time.

Bitcoin’s annual inflation rate is currently 1.75% and will continue to decrease. Bitcoin mining rewards are halved roughly every 4 years, according to the protocol’s code. In 10 years, its inflation rate will be negligible. The last bitcoin will be mined in 2140. After that, the annual inflation rate of bitcoin will be zero.

Auditability: This is not a unique selling proposition for a store of value, but it is still important because it provides information about whether a store of value is suitable for a fair and transparent financial system.

Bitcoin is perfectly audible to the smallest unit. No one knows how much gold exists in the world and no one knows how much US dollars exist in the world. As pointed out to me by Sam Abbassi, bitcoin is the first perfectly, publicly, globally, auditable asset. This prevents rehypothecation risk, a practice whereby banks and brokers use assets posted as collateral by their clients for their own purposes. This takes an enormous amount of risk out of the financial system. It allows for proof of reserves, where a financial institution must provide their bitcoin address or transaction history in order to show their reserves.

In 1949 Benjamin Graham, a British-born American economist, professor and investor, published „The Intelligent Investor“, which is considered one of the founding books of value investing and a classic of financial literature. One of his tenets is that a “balanced portfolio” should consist of 60% stocks and 40% bonds, as he believed bonds protect investors from significant risk in the stock markets.

While much of what Graham described then still makes sense today, I argue that bonds, particularly government bonds, have lost their place as a hedge in a portfolio. Bond yields cannot keep up with monetary inflation and our monetary system, of which bonds are a part, is systematically at risk.

This is because the financial health of many of the governments that form the heart of our monetary and financial system is at risk. When government balance sheets were in decent shape, the implied risk of default by a government was almost zero. That is for two reasons. Firstly, their ability to tax. Secondly, and more importantly, their ability to print money to pay down its borrowings. In the past that argument made sense, but eventually printing money has become a “credit boogie man”, as explained by Greg Foss,

Governments are circulating more money than ever before. Data from the Federal Reserve, the central banking system of the US, shows that a broad measure of the stock of dollars, known as M2, rose from $15.4 trillion at the start of 2020 to $21.18 trillion by the end of December 2021. The increase of $5.78 trillion equates to 37.53% of the total supply of dollars. This means that the dollar’s monetary inflation rate has averaged well over 10% per year over the last 3 years. U.S. Treasury Bonds are yielding less.

For the past 50 years, when equities have sold off, investors fled to the “safety” of bonds which would appreciate in “risk off” environments. This dynamic built the foundation of the infamous 60/40 portfolio — until that reality finally collapsed in March 2020 when central banks decided to flood the market with money. The attempt to stabilize bonds will only lead to an increased demand for bitcoin over time.

Graham’s philosophy was first and foremost, to preserve capital, and then to try to make it grow. With bitcoin it is possible to store wealth in a self sovereign way with absolutely zero counterparty or credit risk.

Bitcoin Versus Real Estate

Given the high levels of monetary inflation in recent decades, keeping money in a savings account is not enough to preserve the value of money. As a result, many hold a significant portion of their wealth in real estate, which has become one of the preferred stores of value. In this capacity, bitcoin competes with real estate, the properties associated with bitcoin make it an ideal store of value. The supply is finite, it is easily portable, divisible, durable, fungible, censorship-resistant and noncustodial. Real estate cannot compete with bitcoin as a store of value. Bitcoin is rarer, more liquid, easier to move and harder to confiscate. It can be sent anywhere in the world at almost no cost at the speed of light. Real estate, on the other hand, is easy to confiscate and very difficult to liquidate in times of crisis, as recently illustrated in Ukraine, where many turned to bitcoin to protect their wealth, accept transfers and donations, and meet daily needs.

In a recent interview with Nik Bhatia, Michael Saylor detailed the downsides of real estate as a store of value asset. As explained by Saylor, real estate in general needs a lot of attention when it comes to maintenance. Rent, repairs, property management, high costs arise with real estate. Commercial real estate for example, is very capital intensive and therefore uninteresting for most people. Furthermore, attempts to make the asset more accessible have also failed, with second tier real estate investments such as real estate investment trusts (REITs) falling short of actually holding the asset.

As Bitcoin (digital property) continues its adoption cycle, it may replace real estate (physical property) as the preferred store of value. As a result, the value of physical property may collapse to utility value and no longer carry the monetary premium of being used as a store of value. Going forward, bitcoin’s return will be many times greater than real estate, as bitcoin is just at the beginning of its adoption cycle. In addition, we will most likely not see the same type of returns on real estate investments as we have in the past. Since 1971, house prices have already increased nearly 70 times. Beyond that, as Dylan LeClair points out in his article-turned podcast, “Conclusion Of The Long-Term Debt Cycle”, governments tend to tax citizens at times like this. Real estate is easily taxed and difficult to move outside of one jurisdiction. Bitcoin cannot be arbitrarily taxed. It is seizure and censorship resistant outside of the domain of any one jurisdiction.

Exchange-traded funds (ETFs) emerged out of index investing, which utilizes a passive investment strategy that requires a manager to only ensure that the fund’s holdings match those of a benchmark index. In 1976, Jack Bogle, founder of the Vanguard Group, launched the first index fund, the Vanguard 500, which tracks the returns of the S&P 500. Today, ETFs manage well over $10 trillion. Bogle had a tenet: active stock picking is a pointless exercise. I recall him stating multiple times in his interviews that over a lifespan, there is only a 3% chance that a fund manager can consistently outperform the market. He concluded that average investors would find it difficult or impossible to beat the market, which led him to prioritize ways to reduce expenses associated with investing and to offer effective products that enable investors to participate in economic growth and save. Index funds require fewer trades to maintain their portfolios than funds with more active management schemes and therefore tend to produce more tax-efficient returns. The concept of an ETF is good, but bitcoin is better. You can cover a lot of ground through an ETF, but you still have to limit yourself to one index, industry, or region. However, when you buy bitcoin, you buy a human productivity index. Bitcoin is like an “ETF on steroids”. Let me explain :

The promise of Bitcoin should at least be on everyone’s lips by now. A decentralized computer network (Bitcoin) with its own cryptocurrency (bitcoin), which, as a peer-to-peer network, enables the exchange and, above all, the storage of value. It is the best money we have and the base protocol for the most efficient transaction network there is (Lightning Network). It is very likely that Bitcoin will become the dominant network for transactions and store of value in the not too distant future. At that point, it will act as an index of global productivity. The more productive we are, the more value we create, the more transactions are executed, the more value needs to be stored, the higher the demand for bitcoin, the higher the bitcoin price. I’ve come to the conclusion that instead of using an ETF to track specific indices, I can use bitcoin to participate in the productivity of all of humanity. As you might expect, bitcoin’s returns have outperformed all ETFs since its inception.

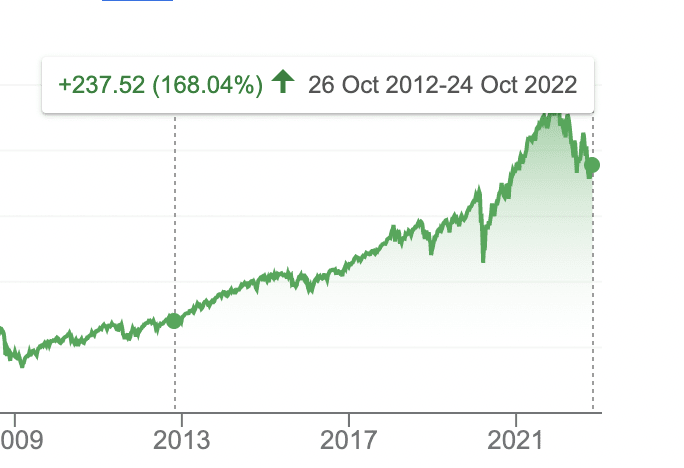

Bitcoin Returns Versus ETFs Returns

The SPDR S&P 500 ETF Trust is the largest and oldest ETF in the world. It is designed to track the S&P 500 stock market index. The performance over the last decade (October 26, 2012 to October 25, 2022) was 168.0%, which translates to an average annual return of 16.68%. Not bad, especially given that all an investor had to do was hold.

However, over the same period, bitcoin‘s performance was: 158,382.362%. More than 200% per annum. We’ve all heard the phrase that past performance is no indicator of future performance, that may be true. But that is not the case with bitcoin. The higher a stock goes the riskier it becomes, because of the P/E ratio. Not bitcoin. When bitcoin increases in price, it becomes less risky to allocate to, because of liquidity, size and global dominance. The Bitcoin Network has now reached a size where it WILL last (Lindy Effect).

We can therefore conclude that bitcoin is likely to continue to outperform ETFs going forward.

Bitcoin has other advantages over an ETF. First, it has a lower cost structure. Second, the latter is a basket of securities held by a third party. You are not free to dispose of your ETFs. If your bank, for whatever reason, decides to close your account, your ETFs are gone too. Bitcoin, on the other hand, cannot be taken away from you or denied access so easily. Additionally, bitcoin can be moved across the internet at will at the speed of light, making confiscation nearly impossible.

Conclusion

Bitcoin is the best wealth preservation technology for the digital age. An absolutely scarce digital native bearer asset with no counterparty risk that cannot be inflated and is easily transportable. A digital store of value, transferable on the world’s most powerful computer network. Considering that the Bitcoin network could theoretically store all of the world’s wealth (Global wealth reached a record high of $530 trillion in 2021, according to the Boston Consulting Group), it may well be the most efficient way we humans have found to store value ever. By holding bitcoin your wealth is going to be protected, likely increasing it by 10x,100x, maybe 500x, during this early monetization process. If you hold out for the next few decades.

In closing, I’d like to revisit Jack Bogle, who was a huge influence on me. As described by Eric Balchunas, Bogle‘s life work is addition by subtraction. Getting rid of the management fees, getting rid of the turnover, getting rid of the brokers, getting rid of the human emotion and the bias. His entire life’s work had been in a similar direction, and as such, I think bitcoin fits well with his investment ethos. Bogle’s primary philosophy was “common sense” investing. He told Reuters in 2012. “Most of all, you have to be disciplined and you have to save, even if you hate our current financial system. Because if you don’t save, then you’re guaranteed to end up with nothing.” Bitcoin is very similar to what Bogle envisioned with passive mutual funds. A long term savings vehicle for investors to place their disposable income with low cost and little risk. Don’t be distracted by bitcoin’s volatility or negative press, to quote Jack Bogle: stay in the course. We’re just getting started, stay humble and stack sats. Your future self will thank you.

UNITED NATIONS, Dec 15 (IPS) – To commemorate the seventy-seventh UN Day, the United Nations Asia Network for Diversity & Inclusion (UN-ANDI) held a panel discussion on the topic “Making the UN Charter a reality”. The discussion took place virtually on 27 October, and the event was attended by diverse participants from around the world.

The keynote speaker, Ambassador Anwarul Chowdhury, former Permanent Representative of Bangladesh to the United Nations (1996–2001), highlighted the need for the UN to be “proactive in oversight, accountability and transparency” and the importance of “practically ensuring gender diversity”.

UN-ANDI is a network of like-minded Asians of the UN system who strive to promote a more diverse and inclusive culture and mindset within the UN. This interest group was created in May 2021 after several years of groundwork.

UN-ANDI is the first ever effort to bring together the diverse group of personnel (i.e., current and former staff, consultants, interns, diplomats, etc.) from Asia and the Pacific (nationality/origin/descent) in the UN system.

Gender, geographical and regional diversity

“Keeping in mind the event’s theme, ‘Making the UN Charter a reality’, I would underscore that the UN Charter is the first international agreement to affirm the principle of equality between women and men with explicit references in Article 8 asserting the unrestricted eligibility of both men and women to participate in various organs of the UN.

It would therefore be most essential for the UN to ensure equality, inclusion, and diversity in its staffing pattern in a real and meaningful sense”, said Chowdhury, former Under-Secretary-General and High Representative of the UN (2002–2007).

Antonia Kirkland, who is the Global Lead on Legal Equality and Access to Justice at Equality Now, said “to keep the noble purpose of the UN and its Charter alive – encouraging respect for human rights and for fundamental freedoms for all – we must continue to hold the UN accountable to do even more to cultivate a culture of equality and non-discrimination internally and externally, including by ensuring a work environment free of sexual harassment and abuse”.

“As we celebrate UN Day, we are hoping to inspire, raise awareness, and fight for a more inclusive, just, and transparent Organization. One of the UN core values is respect for diversity. It is important to have UN staff and personnel from different backgrounds (i.e., nationality, ethnicity, culture, religion/faith, etc.)”, declared Yuan Lin, one of the UN-ANDI coordinators.

“However, the UN hierarchy and staffing currently do not reflect this reality. UN personnel of Asian nationality, origin, or descent are not properly represented, especially at the senior management level. This glass ceiling has deprived the Organization of meaningful contribution from our community and created an unjust and discriminatory work environment”, said Lin, who is serving in the UN peacekeeping mission in the Democratic Republic of the Congo as Chief of the Business Relationship Management Unit.

In November this year, the world’s population reached 8 billion. The Asia-Pacific region is home to around 4.3 billion people, which is equivalent to 54 percent of the total world population.

Article 101 (3) of the UN Charter affirms that “due regard shall be paid to the importance of recruiting the staff on as wide a geographical basis as possible”.

The largest numbers of unrepresented (17) and underrepresented (8) countries were in Asia and the Pacific. In 10 or more organizations with no formal guidelines for geographical distribution, 25 countries in Asia and the Pacific were not represented among staff.

The majority of senior and decision-making posts are held by staff from the global North. Most internships and JPO programs favor the global North, and this contributes to the issue further, as these are entry points to regular jobs in the UN system.

Among promotions to the P-5, D-1, and D-2 levels, only 14.5 percent were from Asia-Pacific States during the period 2018–2020.

Racism and racial discrimination

The issue of racism in the UN system is deep-rooted with many forms and dimensions. There are also structural issues in the policies of the UN system enabling this situation.

Article 1 (3) of the UN Charter asserts that one of the purposes of the UN is to promote and encourage respect for human rights and for fundamental freedoms for all without distinction as to race, sex, language, or religion.

Aitor Arauz, President of the UN Staff Union and General Secretary, UN International Civil Servants Federation (UNISERV), pointed out that “creating an actively anti-racist work environment is not a passive gain – it requires active engagement and daily work to understand each other, value the cultural wealth that our differences bring to the UN, and overcome the biases we all inevitably have. Surveys and direct interaction with constituents reveal that UN personnel of Asian descent face specific forms of bias and discrimination that must be actively addressed.”

He renewed the Staff Union’s commitment to the cause of anti-racism.

Tamara Cummings-John, Steering Committee member of the UN People of African Descent, who is a Senior Human Resources Officer at the World Food Programme in Kinshasa, said, “There is still so much for us to do – and there is so much for us to learn from the outside world, particularly the private sector and above all by listening to our personnel to address the issues relating to racism and racial discrimination in the UN system.”