The Federal Trade Commission is set to file an antitrust lawsuit against Amazon.com Inc. AMZN, -0.62%

in September after the two sides could not reach a settlement over antitrust claims, according to a Wall Street Journal report, citing people familiar with the matter. Members of Amazon’s legal team held a video call with FTC officials on Aug. 15 during a so-called last-rites meeting, but were unable to agree on concessions, the report said. Amazon declined comment on the report.

U.S. stocks closed lower Tuesday after the long Labor Day weekend, as bond yields and oil prices climbed. The Dow Jones Industrial Average DJIA shed about 195 points, or 0.6%, ending near 34,642, according to preliminary FactSet data. The S&P 500 index SPX dropped about 0.4% and the Nasdaq Composite Index COMP fell 0.1%. Investors returned from the long weekend in a less bullish mood on weaker economic data from China and Europe, but also with more clouds on the horizon in oil markets. Oil prices CL00 closed at the highest level since November on Tuesday, after Saudi Arabia and Russia opted to extend oil supply production…

Looking to spend your entertainment dollars wisely in September? Watch Hulu and read a book or two.

That pretty much sums up a hugely underwhelming lineup from streaming services, which burned through their best shows in the spring and have little to offer for the start of the traditional fall TV season. That’s not to say there aren’t a handful of promising shows — there are — but is one decent new show per service worth the price of multiple monthly subscriptions? Almost certainly not.

Shares of investment giant Blackstone Inc. and vacation-home rental platform Airbnb Inc. rallied after hours on Friday after both won the nod to join the S&P 500 index SPX

later this month.

The announcement, from S&P Dow Jones Indices, said that the change would take hold before the start of trading on Monday, Sept. 18. The move, among others announced Friday, will “ensure each index is more representative of its market-capitalization range,” according to a release.

Airbnb ABNB, +0.87%

currently has a market value of $83.98 billion, and its shares are up 64.7% so far this year. Blackstone BX, -1.77%,

currently worth $129.29 billion, has seen its stock rise 43.6% year-to-date.

Shares of Airbnb and Blackstone were up 5.7% and 4.8%, respectively, after hours on Friday.

Blackstone and Airbnb will replace Lincoln National Corp. LNC, +2.14%

and Newell Brands Inc. NWL, +1.23%

in the index, S&P Dow Jones Indices said on Friday. In the process, Lincoln and Newell will join the S&P SmallCap 600.

“We’ve established an unparalleled global platform of leading business lines, offering over 70 distinct investment strategies,” Chief Executive Stephen Schwarzman told analysts. “We believe our clients view us as the gold standard in alternative asset management.”

Meanwhile, Airbnb last month said that travelers were seeking longer stays and bigger properties in pricier areas, as the rebound in travel endures despite a tidal wave of inflation last year. The company’s second-quarter results and third-quarter sales forecast topped Wall Street’s estimates.

Meanwhile, S&P 500 member Deere & Co. DE, +1.94%

will replace Walgreens Boots Alliance Inc. WBA, -7.43%

in the S&P 100, S&P Dow Jones Indices said on Friday. That change also takes hold on Sept. 18. S&P Dow Jones Indices said Walgreens “is no longer representative of the megacap market space” but will stay in the S&P 500.

Shares of Deere fell 0.2% after hours. Walgreens stock was up 0.4%.

More than a year ago, the Federal Trade Commission sued Intuit Inc., the maker of TurboTax, for allegedly tricking people into thinking they could file their income taxes for free with the tax-preparation giant.

Now, an administrative judge inside the agency has ruled against Intuit — and the company said in a Friday afternoon SEC filing that it’s going to keep fighting the case, even if that means incurring “significant costs.”

“We expect to appeal this decision to the FTC Commissioners and, if necessary, then to a federal court of appeals. We intend to continue to defend our position on the merits of this case,” the company said in its 10-K filing.

“There is no monetary penalty, and Intuit expects no significant impact to its business,” Intuit spokesman Rick Heineman said in a statement. The company will appeal “this groundless and seemingly predetermined decision by the FTC to rule in its own favor,” he said.

Intuit already reached a $141 million settlement with state attorneys general about the allegations of deceptive advertising. The company says it has been clear and upfront with customers about costs. It did not admit liability in the settlement.

The FTC could not be immediately reached for comment Friday afternoon.

In March 2022, the regulator sued Intuit in federal court to immediately stop commercials that repeated “free” over and over. Intuit pulled some of the advertising and after filing season ended, a San Francisco federal judge said the FTC bid for emergency halts didn’t need to happen under the circumstances.

FTC lawyers also lodged an internal administrative complaint. “Intuit widely disseminated ads on television, on the radio, and online that gave consumers the impression that they could use TurboTax for free, even though two-thirds of taxpayers don’t qualify for Intuit’s free TurboTax offerings,” they wrote in administrative complaint proceedings.

The ongoing legal fight is happening while the broader fight over of free tax preparation is heating up. The Internal Revenue Service is planning to test its own pilot program in the upcoming filing season where taxpayers can file their taxes directly with the IRS instead of through tax preparation companies or individual preparers.

TurboTax and the tax software industry oppose the proposed IRS direct file system. So do Congressional Republicans.

One sticking point in the looming government shutdown is how much money the IRS should be getting in its budget. The House appropriations bill would forbid the IRS from using any money to build the direct file system.

Intuit Inc. INTU, +1.44%

shares closed 1.4% higher Friday, at $549.60, and the disclosure didn’t seem to be having much effect on the shares in after-hours trading. Shares are up 41% year to date, while the Dow Jones Industrial Average DJIA

is up 5% and the S&P 500 SPX

is up 17.6%.

Shares of Robinhood Markets Inc. HOOD, +2.62%

galloped 2.6% higher Friday, after the trading app disclosed that it bought back 55.3 million of its shares from the U.S. Marshal Service. The company said it paid $605.7 million for the shares, which represents 6.1% of the company’s market capitalization of $9.93 billion at Thursday’s close. The shares were originally acquired through Emergent Fidelity Technologies Ltd. by Sam Bankman-Fried, founder of failed cryptocurrency exchange FTX that collapsed last year. The shares were seized and transferred to the custody of the U.S. Robinhood’s stock has rallied 20.7% over the past three months through Thursday, while the S&P 500 SPX, +0.24%

has gained 6.8%.

U.S. stocks finished higher on Friday, helping the Nasdaq Composite and S&P 500 clinch their first weekly gain after three weeks of losses. The S&P 500 SPX, +0.67%

gained 29.40 points, or 0.7%, to 4,405, according to preliminary closing data from FactSet. It finished 0.8% higher on the week, snapping a three-week losing streak. The Nasdaq Composite COMP, +0.94%

gained 126.67 points, or 0.9%, to 13,590.65. The Dow Jones Industrial Average DJIA, +0.73%

rose by 247.48, or 0.7%, to 34,346.90, but notched a 0.5% loss on the week, for its third weekly loss in four. Federal Reserve Chairman Jerome Powell delivered a speech at the Kansas City Fed’s annual symposium in Jackson Hole that moved markets on Friday, although stocks managed to shrug off initial losses to climb higher during the session.

Wall Street looks ready to build on Monday’s gains, the first in five sessions for the S&P 500 SPX

and Nasdaq Composite COMP.

That’s as expectations build around Nvidia, which has had a lackluster August, to knock it out of the park with earnings on Wednesday.

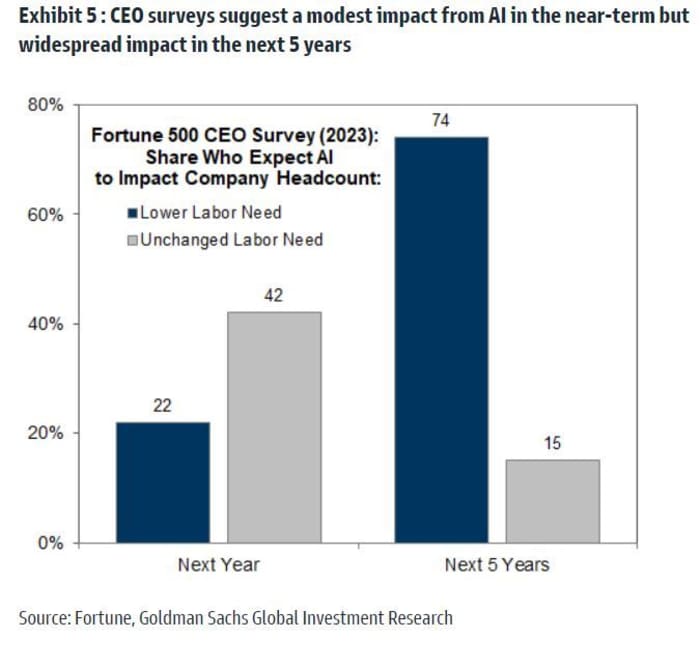

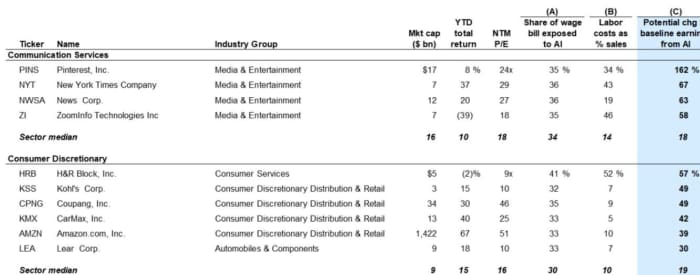

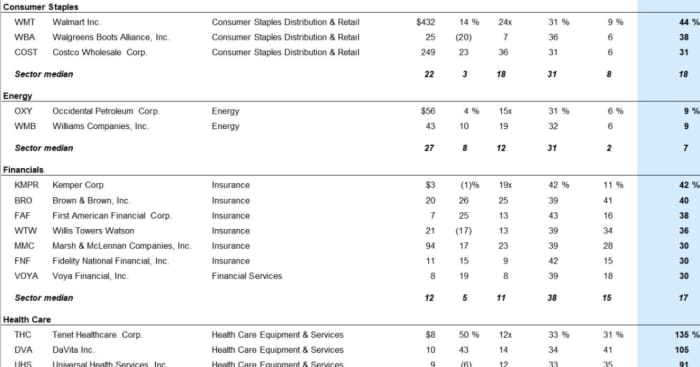

Investors have had months to focus on AI darlings such as Nvidia. In our call of the day, Goldman Sachs takes a look at stocks to trade after the big AI trade. A team led by strategists Ryan Hammond and David Kostin complied a basket of companies with the biggest potential long-term earnings per share boost from the impact of AI adoption on labor productivity.

Their analysis indicates that following widespread AI adoption, EPS for the median stock in that basket could be 72% higher than the baseline, versus 19% for the median Russell 1000 stock.

“We estimate the potential productivity-related EPS boost from increased revenues or increased margins, using a combination of company-level estimates of the share of the wage bill exposed to AI automation and the labor cost to revenue ratio,” said the Goldman team.

Since early 2023, when AI emerged as a theme for investors, they note their long-term basket of stocks has outperformed the equal-weight S&P 500 by just 6 percentage points, far less than near-term beneficiaries such as Nvidia NVDA, -0.49%,

Microsoft MSFT, +0.94%

or Meta META, +0.51%.

Goldman Sachs Investment Research

“The estimated AI-driven earnings boost is likely to occur over the next few years, but should be reflected in stock valuations sooner. However, the eventual share price impact will depend on the ability of companies to use AI to enhance earnings,” said Goldman.

While unable to pin it exactly, Goldman expects AI adoption will start to a have a “meaningful macro impact” between 2025 and 2030, with regulatory constraints and data privacy concerns likely to slow widespread adoption. Nearly 75% of CEOs see AI take-up impacting companies or cutting labor needs within the next five years, even if they don’t right now.

Firms with the biggest workforce exposure to AI and larger and more innovative ones, will likely adopt generative AI earlier than others, say the strategists. They say to “expect valuation multiples for these companies to increase first as the adoption timeline crystallizes, even if actual adoption and the associated EPS boost is occur later.”

Goldman’s estimates on the potential earnings boost for those long-term AI beneficiaries consist of several factors: the share of each company’s wage bill exposed to AI automation, how much of a company’s wage bill is exposed to AI automation and labor cost as a share of revenue.

“For the typical Russell 1000 stock, 33% of the wage bill is potentially exposed to AI automation and labor costs currently represent 14% of total sales. The potential boost from higher sales would increase earnings by 11% and reduced labor costs would increase earnings by 26%, all else equal,” say the strategists.

Here is a taster of their long-term AI beneficiaries basket:

The world’s biggest miner BHP BHP, -0.98%

reported a 58% slump in annual profit amid tumbling commodity prices in part due to China’s economic troubles. U.S.-listed shares are up 4%.

Arm Holdings filed its long-awaited IPO, which could be the year’s biggest. The chip designer aims to raise up to $10 billion with a valuation of $60 billion to $70 billion.

Existing home sales for July are due at 10 a.m., with several Fed speakers throughout the day: Richmond Fed President Tom Barkin at 7:30 a.m. and Chicago Fed President Austan Goolsbee and Fed. Gov. Michelle Bowman both at 2:30 p.m.

Is tech dancing to the beat of its own drum? The Chart Report flagged this one from Scott Brown, founder of Brown Technical Insights, showing performance of the Technology Select Sector SPDR ETF XLK

:

@scottcharts

“It’s only been a week, but consensus and conventional wisdom suggest higher yields are bad for Growth/Tech stocks. Meanwhile, Tech is acting like it never got the memo. It’s still too early to tell if Tech is trying to tell us something, but Scott points out that the sector is facing a crucial test this week at the March 2022 highs (around $163). $XLK is solidly above $163 after today’s bounce, but where it ends the week will likely hinge on $NVDA, as the company releases earnings on Wednesday evening,” says Patrick Dunuwila, editor and co-founder of The Chart Report.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

The so-called Magnificent Seven grouping of technology stocks lost some of its luster this week after four of the seven moved into correction territory, meaning their stocks have fallen at least 10% from their recent peaks.

The corporate-bond market, in contrast, seems to like all seven names.

One caveat: Tesla has no outstanding bonds. In the past, the electric-car maker issued convertible bonds, but they have all been converted into equity.

The group is credited with helping drive the stock market’s gains in the first half of the year, driven by excitement about artificial intelligence. But the rally has stalled in recent weeks as investors have fretted over the potential for U.S. interest-rate increases, surging Treasury yields and China worries, with property developer Evergrande filing for U.S. bankruptcy protection late Thursday.

On Thursday, Meta followed Apple, Microsoft and Nvidia into correction territory, as MarketWatch’s Emily Bary reported. Tesla, meanwhile, is in a bear market, meaning it’s down more than 20% from its recent peak.

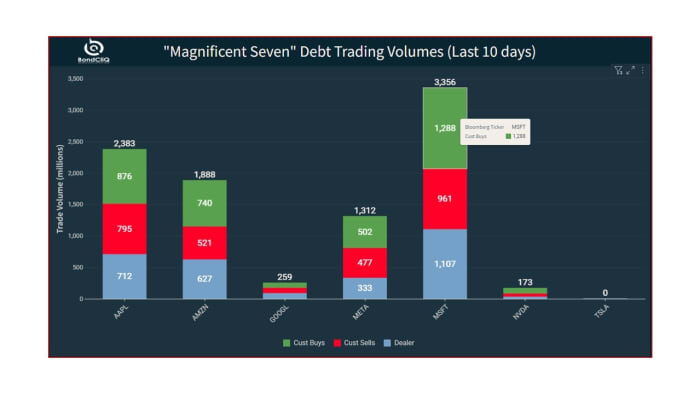

The following series of charts from data-solutions provider BondCliQ Media Services show how many bonds each company has issued by maturity and how they have traded as the stocks have pulled back.

The first chart shows that Microsoft has by far the most bonds, mostly in the 30-year bucket. The software and cloud giant has more than $50 billion in long-term debt, according to its 2023 10-K filing with the Securities and Exchange Commission.

Outstanding Magnificent Seven debt by maturity bucket.

Source: BondCliQ Media Services

This chart shows trading volumes over the last 10 days, divided by trade type. The green shows customer buying, while the red is customer selling. The blue shows dealer-to-dealer flows. Microsoft, for example, has seen almost $1.3 billion in customer buying from dealers in the last 10 days and $960 million in customer sales to dealers.

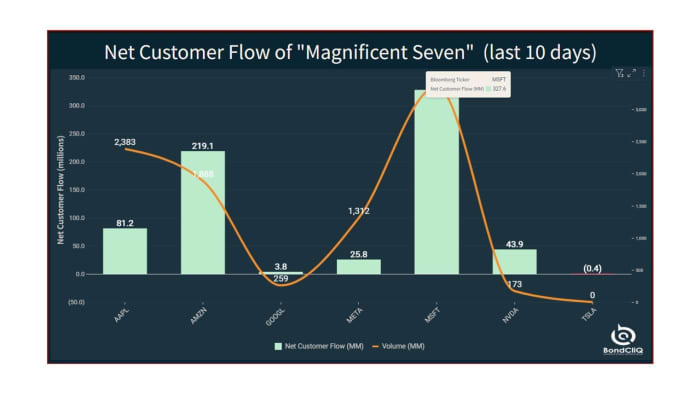

This chart shows that every name in the group has enjoyed better net buying in the last 10 days, with Microsoft leading the way.

Net customer flow of Magnificent Seven debt (last 10 days).

Source: BondCliQ Media Services

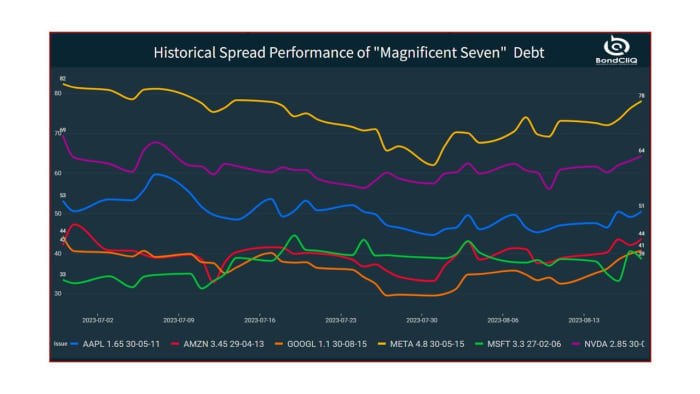

This chart shows spread performance over the last 50 days for an intermediate-term bond from each of the seven issuers. Most have tightened or remained steady over the period.

Historical spread performance of Magnificent Seven debt.

Apple’s stock entered correction Wednesday upon falling more than 10% from its July 31 peak of $196.45. The company sells mainly discretionary products, and right now “consumers are still being pinched” and thinking more carefully about where they spend their money, according to Matt Stucky, senior portfolio manager for equities at Northwestern Mutual Wealth Management.

The stupidest story of the summer may be over. Finally, mercifully.

Mark Zuckerberg, billionaire and chief executive of Meta Platforms Inc. META, -1.34%,

on Sunday appeared to pull the grown-up card — or at least the less-immature card — to scuttle a cage fight with Elon Musk, the even richer billionaire, Tesla Inc. TSLA, -1.10%

CEO and X owner.

From the start, it was a story that appeared to live mostly in Musk’s imagination. Yet it still sparked a media frenzy, as the prospect of two emotionally stunted billionaires publicly pummeling each other was not without some appeal.

But the proposed MMA-style fight apparently met its demise the same way it was born — through a lot of online bluster.

Author and journalist Walter Isaacson — who is currently writing a biography of Musk — tweeted a text exchange Sunday that he said Musk had sent him.

“Wanna do a practice bout at your house next week?” a text apparently from Musk reads. The reply, purportedly from Zuckerberg: “If you still want to do a real MMA fight, then you should train on your own and let me know when you’re ready to compete. I don’t want to keep hyping something that will never happen, so you should either decide you’re going to do this and do it soon, or we should move on.”

Zuckerberg later posted a more public burn on Meta’s Threads — the Twitter/X rival that sparked this whole thing to begin with — saying: “I think we can all agree that Elon isn’t serious and it’s time to move on…If Elon ever gets serious about a real date and official event, he knows how to reach me. Otherwise, time to move on. I’m going to focus on competing with people who take the sport seriously.”

It was unclear what the two billionaires now plan to do with their spare time, if not fight each other.

Shares of Alibaba Group Holding Ltd. were rallying more than 2% in Thursday’s premarket trading after the Chinese e-commerce giant topped expectations with its latest revenue and earnings.

The company notched fiscal first-quarter net income of RMB34.3 billion ($4.6 billion), or RMB13.30 per American depositary share, compared with net income of RMB22.7 billion, or RMB8.51 per ADS, in the year-before period.

On an adjusted basis, Alibaba BABA, +0.67%

earned RMB17.37 per ADS, while the FactSet consensus was RMB14.59 per share. Revenue rose to RMB234.2 billion from RMB205.6 billion, where analysts had been modeling RMB224.7 billion.

Chief Executive Daniel Zhang said the company’s reorganization was “beginning to unleash new energy across our businesses.” Alibaba recently realigned into six units with their own CEOs and boards of directors, and the ability to pursue independent fundraising.

“Through this self-driven transformation, we aim to catalyze innovation, promote vitality in our organization and enable businesses to focus on long-term growth,” Zhang continued. “We look forward to positive impacts on our business, including strengthening competitiveness, sustainable growth and shareholder value creation.”

Overall revenue for the company’s Taobao and Tmall Group, which represents the company’s core e-commerce marketplaces in China, rose to RMB115.0 billion from RMB102.5 billion.

Within that group, customer management revenue was up 10% to RMB79.7 billion, “primarily due to the increase in merchant’s willingness to invest in advertising” and an increase in the volume of online physical goods generated on the platforms.

Alibaba bought back $3.1 billion worth of ADRs during the June quarter, “which is supported by our continuous generation of strong free cash flow,” Chief Financial Officer Toby Xu said in the release. Free cash flow was RMB39.1 billion in the quarter, up 76% from a year earlier.

U.S.-listed shares of Alibaba are up about 8% so far this year.

““We are actively exploring ways to address account sharing and the best options for paying subscribers to share their accounts with friends and family.””

— Disney CEO Bob Iger

Pour another one out for streaming freeloaders.

Netflix Inc. NFLX, -2.14%

has been cracking down on account-sharing, and now Walt Disney Co. DIS, -0.73%

is likely to follow suit.

Bob Iger, the media giant’s chief executive, said Wednesday that the company was “actively exploring” how to tackle the fact that many streaming subscribers on Disney+, Hulu and ESPN+ share passwords and accounts with loved ones.

“Later this year, we will begin to update our subscriber agreements with additional terms on our sharing policies, and we will roll out tactics to drive monetization sometime in 2024,” he said, according to a transcript provided by AlphaSense/Sentieo.

Whereas Netflix suggested that it could be housing 100 million global account borrowers, Iger declined to put a number on Disney’s own base of password sharers, “except to say that it’s significant.”

“What we don’t know, of course, is as we get to work on this, how much of the password-sharing, as we basically eliminate it, will convert to growth” in subscribers, he said. “Obviously, we believe there will be some, but we’re not speculating.”

The company plans to “get at this issue” next calendar year, and the initiative could have some impact on Disney’s business in that period.

“It’s possible that we won’t be complete or the work will not be completed within the calendar year, but we certainly have established this as a real priority, and we actually think that there’s an opportunity here to help us grow our business,” Iger continued.

Disney is making a big push to improve the financials of its streaming business, after spending the stay-home pandemic era focused on raw subscriber growth. Now the company is targeting streaming profitability by the end of fiscal 2024, and it just announced a new round of price hikes in pursuit of that goal.

“We grew this business really fast, really before we even understood what our pricing strategy should be or could be,” Iger commented. In the past six months, the company has started to pursue a pricing strategy “that’s really aimed at enabling us to improve the bottom line, ultimately to turn this into a growth business.”

Netflix is farther along in its efforts, and it’s won praise from Wall Street for them. Executives at the streaming giant indicated early success with Netflix’s broad password-sharing crackdown, though it will take time for the impact to fully manifest in the company’s financials.

Analysts got to the point early and often during a conference call late Wednesday: What are Disney Chief Executive Robert Iger’s M&A plans, particularly following reports that former Disney executives Kevin Mayer and Tom Staggs, now co-CEOs of Blackstone-backed Candle Media, have been retained in a “consulting capacity” to decide ESPN’s fate?

The prospect of an Apple-Disney combo seems far-fetched in a heated regulatory climate, where the Federal Trade Commission is attempting to crack down on Big Tech acquisitions, but it could happen should Disney sell off assets and Apple gobbles up Disney’s direct-to-consumer business that includes streaming service Disney+, some media analysts speculate. Apple could conceivably even buy ABC, which reportedly is on the block. But the path is long and circuitous.

Yet the rumors persist, dating back to Apple co-founder Steve Jobs’ reverence for the Disney brand, and the increasingly overlapping businesses of both companies over the years.

When pressed by analysts during a conference call late Wednesday, Iger declined to discuss the future of Disney’s structure or possible asset sales. When asked if Disney might “plausibly” be snapped up by one company — read Apple — an exasperated Iger said he would not “speculate” on the sale of Disney to a technology company or anyone else, given the current global stance of regulators. The FTC has aggressively challenged mergers from the likes of Microsoft Corp. MSFT, -1.17%

and Facebook parent Meta Platforms Inc. META, -2.38%,

with limited success.

Since Iger hinted at the potential sale of Disney’s assets in an interview with CNBC last month, rumors have swirled around ESPN.

ESPN and related properties likely could command at least one-third of Disney’s current depressed market cap of about $150 billion, say some media watchers, though Iger has denied ESPN is for sale. He has acknowledged “the sports leader” is seeking “strategic partners” — possibly with the NFL, MLB, NBA and NHL — to generate revenue. Late Tuesday, ESPN stuck up a deal with Penn Entertainment Inc. PENN, +9.10%

to create ESPN Bet, a digital sportsbook to launch in the fall in 16 states.

Another possible property being dangled is ABC. But with rights to the NBA Finals and two Super Bowls in the next eight years, it is unclear who would acquire the network and how Disney would replace lucrative sports revenue.

Other properties on the block include cable channels Freeform and Disney Channel, according to a report by the Wall Street Journal.

“If an asset sale happens, will the proceeds be deployed into fortifying its balance sheet or beefing up its remaining operations?” Rick Munarriz, senior media analyst at The Motley Fool, said in an email.

Disney, which is in the midst of a $5.5 billion cost-cutting campaign, is exploring several avenues to prop up sales as linear TV ads shrink, Disney+ subscriptions decline and attendance at Walt Disney World wanes.

Shares of Disney are trading at half their highs from a few years ago, in large part because of dwindling sales and profits at ESPN and Disney’s other cable networks.

Enter Mayer, who previously ran Disney’s strategic planning group for years and engineered a trifecta of mega deals: The acquisition of the aforementioned Pixar Animation Studios from Steve Jobs for $7.4 billion in 2006, the purchase of Marvel Entertainment for $4 billion in 2009, and the acquisition of Lucasfilm for $4.05 billion in 2012. Mayer also led the $71.3 billion acquisition of 20th Century Fox’s entertainment assets in 2019, which has drawn mixed reviews.

Walt Disney Co.’s stock dipped in after-hours trading Wednesday after the company posted mixed quarterly results roughly in line with analysts’ expectations amid a cost-cutting frenzy.

Separately, Disney said it is hiking prices on almost all of its streaming packages in an aggressive push to boost its bottom line. Commercial-free Disney+ will cost $13.99 per month, a 27% increase, beginning Oct. 12. Ad-free Hulu will increase 20% to $17.99 per month. A new Disney+ and Hulu Bundle ad-free plan launches Sept. 6 for $19.99.

The media giant DIS, -0.73% reported a fiscal third-quarter loss of $460 million, or 25 cents a share, mostly because of restructuring and impairment charges. After adjusting for restructuring costs and other effects, Disney reported earnings of $1.03 a share. Revenue grew 4% to $22.3 billion from $21.5 billion a year ago.

Analysts surveyed by FactSet had on average expected adjusted earnings of 96 cents a share on revenue of $22.5 billion. Disney shares declined about 3% in after-hours trading immediately following the release of the report, after dropping 0.7% to $87.52 in the regular session.

“Our results this quarter are reflective of what we’ve accomplished through the unprecedented transformation we’re undertaking at Disney to restructure the company, improve efficiencies and restore creativity to the center of our business,” Disney Chief Executive Robert Iger said in a statement announcing the results. Disney is in the midst of a $5.5 billion cost-cutting plan overseen by Iger, who returned to the CEO position to right the ship in late 2022.

Direct-to-consumer (DTC) sales, which includes streaming services and some international products, hauled in $5.5 billion, compared with analysts’ forecast of $5.7 billion on average and last year’s total of $5.05 billion. The division did reduce its quarterly losses to $512 million, compared with $1.06 billion a year ago. Analysts were expecting a loss of $758 million.

Still, the company has lost more than $10 billion in its DTC segment since launching Disney+ in late 2019. Disney had told investors for three years it expects Disney+ to be profitable by September 2024. During a conference call with analysts late Thursday, Iger said Disney is “actively exploring” options to crack down on account sharing when the company updates subscriber agreements later this year and will “roll out tactics to drive monetization” in 2024.

The company’s iconic theme parks around the world and product-sales business increased to $8.3 billion in revenue from $7.4 billion a year ago. The average analyst estimate was $8.1 billion.

Disney’s largest business segment, media and entertainment distribution, raked in $14 billion during the quarter, down from $14.1 billion a year ago. Analysts on average predicted $14.3 billion, according to FactSet.

Disney’s television networks generated sales of $6.7 billion, while analysts’ average estimates called for $6.74 billion. Content sales and licensing, a category that includes Disney’s film business, reported revenue of $2.1 billion, compared with analysts’ expectations of about $2.15 billion.

In the weeks leading up to Disney’s results, there has been a whirlwind of fear and doubt over the current state of the company’s streaming services — including ESPN — as well as linear-TV ad sales, the actors’ and writers’ strikes that have shut down Hollywood, Disney’s theme parks and its legal and political battle with Florida Gov. Ron DeSantis.

Front and center is the health of Disney+ as it battles streaming rivals like Apple Inc. AAPL, -0.90%,

Netflix Inc. NFLX, -2.14%,

Amazon.com Inc. AMZN, -1.49%,

Warner Bros. Discovery Inc. WBD, -2.15%

and Comcast Corp. CMCSA, -0.26%.

Macquarie Equity Research analyst Tim Nollen believes in Disney’s streaming services over the long term but said “we see too many near-term issues to overcome to support a more constructive view.”

Disney+ had 146.1 million subscribers globally, 7% fewer than the 157.8 million it had in the previous quarter. The decline mostly came from India, where Disney lost the rights to stream a popular cricket league last year.

Disney and DeSantis, who is running for the 2024 Republican presidential nomination, have filed dueling lawsuits that stem from the company’s criticism last year of a Florida law that bans classroom discussion of sexuality and gender identity with younger children. Earlier this week, a group of mostly former Republican high-level government officials called DeSantis’s takeover of Disney World’s governing district “severely damaging to the political, social, and economic fabric” of Florida.

The somber vibe prompted Deutsche Bank analysts on Tuesday to lower their price target on Disney shares 8% to $120, with “lower advertising revenue, underperformance at the box office, and lighter parks attendance in Orlando” chief among their concerns.

“This is Iger’s most important earnings call since returning to Disney late last year. He came in with a punch list that was too long to realistically knock off in two years,” Rick Munarriz, an analyst at the Motley Fool, said in an email. “Now the board has given him four years, and every word he uses during Thursday afternoon’s earnings call has to carry some serious heft.”

Disney’s call was to start at 4:30 p.m. Eastern.

Shares of Disney have inched up 0.7% this year, while the S&P 500 SPX

has climbed 16%.

Online sports-betting company Penn Entertainment Inc. sealed a $1.5 billion deal with Walt Disney Co.’s DIS, +1.50%

ESPN to launch ESPN Bet, a branded sportsbook for fans in the U.S., and pivoted away from Barstool Sports on Tuesday, selling the platform back to founder Dave Portnoy.

Penn Entertainment PENN, -0.68%

will rebrand its current sportsbook and relaunch as ESPN Bet in the fall in 16 legalized-betting states where Penn is licensed.

The rebrand — which includes the mobile app, website, and mobile website — sent Penn’s stock soaring 13% in after-hours trading Tuesday. ESPN Bet will benefit from exclusive promotional services across ESPN’s platforms, including access to ESPN talent, the companies said.

Penn will pay ESPN $1.5 billion over 10 years as part of the strategic partnership, and will grant ESPN $500 million of warrants to purchase about 31.8 million Penn common shares, with additional bonus warrants possible.

“Together, we can utilize each other’s strengths to create the type of experience that existing and new bettors will expect from both companies, and we can’t wait to get started,” Penn Entertainment Chief Executive Jay Snowden said in a release.

Penn also said it has divested 100% of its stake in Barstool Sports to Portnoy, allowing the sports media platform “to return to its roots of providing unique and authentic content to its loyal audience without the restrictions associated with a publicly traded, licensed gaming company.”

For Penn, the ESPN partnership represents “a clear step up from Barstool in terms of mass appeal…and minimal regulatory risk,” according to Wells Fargo analyst Daniel Politzer, who said it was a “nearly impossible challenge for a publicly traded, licensed gaming company” to own “a media platform that thrived on viral/provocative content.”

Still, he said in a note to clients that “it’s premature to conclude this is a game change” since past partnerships between online sports-betting companies and media players have come up short of what initial fanfare would’ve suggested.

The news sent rival DraftKings Inc. shares DKNG, +0.25%

sinking about 5% in after-hours trading.

The decline in DraftKings shares comes as they’ve advanced 178% so far in 2023, through Tuesday’s close. Two analysts upgraded DraftKings’ stock just this week.

Upstart Holdings Inc. has struggled to contend with a tougher lending environment, and the company indicated Tuesday that its challenges are expected to continue.

The financial-technology company, which uses artificial intelligence to inform lending decisions, delivered a lower-than-expected forecast for the current quarter, as Chief Executive David Girouard called out high interest rates and “an environment where banks continue to be super cautious about lending.”

For the third quarter, Upstart UPST, -0.42%

expects $140 million in revenue, while analysts had been anticipating $155 million. The company also models $5 million in adjusted earnings before interest, taxes, depreciation and amortization (Ebitda), while analysts were looking for $9.6 million in adjusted Ebitda.

Upstart shares tumbled more than 19% in Tuesday’s after-hours action.

Chief Financial Officer Sanjay Datta, meanwhile, explained that the “ongoing supply of loans on offer in the secondary markets by sellers anxious for liquidity contributes to a challenging market dynamic, with loan books being sold at bargain prices and creating no shortage of buying opportunities for selected investors.”

“Our view is that it will take some time for the market to work its way through this surplus of cheap available yield,” he said. “Despite this, we continue to pursue a number of promising discussions with prospective funding partners, aimed at bringing more committed capital to the platform, and believe that we will be well positioned once the loan market returns to a more traditional state of pricing equilibrium.”

Though Datta said Upstart moved in a “promising direction this past quarter,” he also acknowledged there’s “much work to be done to restore our business to the scale and growth that we aspire to.”

The company reported a second-quarter net loss of $28.2 million, or 34 cents a share, compared with a loss of $29.9 million, or 36 cents a share, in the year-earlier period. On an adjusted basis, Upstart earned 6 cents a share, whereas analysts tracked by FactSet were modeling a 7-cent loss per share.

Revenue fell to $136 million from $228.2 million. The FactSet consensus was for $135.2 million. The company generated $144 million in fee revenue, compared with the $131 million that analysts were expecting.

Upstart’s lending partners originated 109,447 loans across its platform in the second quarter, totaling $1.2 billion. Conversion on rate requests was 9%, down from 13% in the same period a year prior.

Though Upstart beat on adjusted earnings, it “signaled that macro pressure is not set to abate in Q3, with credit performance and the funding markets still buffeted by a challenging economic environment,” Barclays analyst Ramsey El-Assal wrote in a note to clients Tuesday. “With a new Q3 guide that came in below Street estimates, we expect shares to be down in tomorrow’s tape.”

Shares of Upstart have rocketed 291% so far in 2023, through Tuesday’s close, as the S&P 500 SPX

has risen 17%.

For weeks, Wall Street had been closely eyeing the performance of Amazon Web Services: Would it rise more than 10% in year-over-year sales?

It did, and then some, on Thursday when Amazon.com Inc. AMZN, +0.55%

announced its quarterly results, boosting company shares more than 9% in after-hours trading.

Sales for Amazon’s market-leading AWS jumped 12%, to $22.1 billion, offering proof of its “stabilization” after several rough quarters, Jefferies analyst Brent Thill told CNBC late Thursday. More important, it signals healthier days — for now — in the cloud market amid a stampede for generative-AI services and concerns about Amazon’s place in it.

“I am bullish on AWS’s growth,” Amazon Chief Executive Andy Jassy said in a conference call with analysts late Thursday, in which he predicted AWS would become a $100 billion business within several years.

Last week, Microsoft Corp. MSFT, -0.26% said it expected revenue growth from Azure and other cloud services to continue cooling in the current quarter. Meanwhile, Alphabet Inc.’s GOOGL, +0.05%

GOOG, +0.10%

Google Cloud revenue grew 28%, topping Wall Street estimates.

Maribel Lopez, founder and principal analyst at Lopez Research, called Amazon’s cloud revenue “surprising” and resilient despite costoptimization among enterprise buyers.“Upcoming AI workloads should keep [Amazon] in a similar top-line growth trajectory, but the challenge will be keeping the cost to serve down,” she said in an email. “The new chipsets will assist with cost containment. Overall, the AI business will provide a bright light in the cloud market.”

Although Thill and other analysts openly wonder how AWS will adapt in the age of AI, the company’s second-quarter sales figures heartened Amazon’s top boss, who knows a thing or two about the cloud-computing industry.

“Our AWS growth stabilized as customers started shifting from cost optimization to new workload deployment, and AWS has continued to add to its meaningful leadership position in the cloud with a slew of generative AI releases that make it much easier and more cost-effective for companies to train and run models,” the embattled Jassy, who previously ran AWS, said in a statement Thursday, announcing the results.

Underscoring the importance of AWS, it was mentioned 49 times in Amazon’s second-quarter earnings release, mostly cited in customer use cases.

Shopify Inc. easily topped adjusted profit expectations for its latest quarter, though shares of the e-commerce marketplace were headed lower in Wednesday’s after-hours action.

The e-commerce company reported a comprehensive loss of $1.30 billion, or $1.02 a share, whereas it logged a loss of $1.21 billion, or 95 cents a share, in the year-earlier period.

On an adjusted basis, Shopify SHOP, -7.44%

earned 14 cents a share, whereas analysts tracked by FactSet were anticipating 6 cents a share.

Revenue jumped to $1.69 billion from $1.30 billion a year prior, while the FactSet consensus was for $1.63 billion.

Gross merchandise volume, or the dollar value of orders facilitated through Shopify’s platform, came in at $53.5 billion. Analysts had been modeling $55.0 billion. The company also posted $31.7 billion in gross payments volume.

For the third quarter, Shopify anticipates a revenue growth percentage in the low-20s on a year-over-year basis. The company also expects free cash flow in the third quarter to exceed the first-half total.

Shopify generated $97 million in free cash flow during the second quarter, beating the $27 million FactSet consensus and bringing its first-half haul to $183 million. Analysts were expecting $96 million in free cash flow for the third quarter.

“We’re not just shipping products faster, but we are also expanding our global merchant base, all while improving our ability to generate greater free cash flow,” President Harley Finkelstein said in a release.

PayPal Holdings Inc. edged above expectations with its quarterly revenue and earnings outlook Wednesday, though the company fell short of a margin metric and disappointed Wall Street with its take rate.

Shares of PayPal PYPL, -3.08%

fell 7% in after-hours trading after the payment-technology company reported an adjusted operating margin of 21.4% for the second quarter, below the 22% outlook that the company had given previously.

In its investor deck, the company attributed the shortfall to its credit portfolio, where PayPal generated less revenue than it had anticipated and increased its loss provisions.

“There’s no other items that really contributed to that miss,” Acting Chief Financial Officer Gabrielle Rabinovitch said on the earnings call, noting that PayPal specifically saw pressure related to business loans.

Analysts also flagged concerns about PayPal’s transaction take rate, which came in at 1.74%, while consensus expectations were for about 1.9%.

PayPal’s revenue for the second quarter increased to $7.29 billion from $6.81 billion, whereas analysts were modeling $7.27 billion. But Wolfe Research analyst Darrin Peller noted that while revenue was up 7%, gross profit increased only 1%.

“We believe investor focus will remain on gross-profit growth dynamics given the mismatch [between] revenue and gross-profit growth,” he wrote in a note to clients.

Rabinovitch said on the earnings call that PayPal expects continued pressure on transaction-margin performance in the third quarter before conditions improve in the fourth quarter. Over the long haul, she anticipates that PayPal’s transaction margins “will certainly be benefited” by factors such as accelerations in branded checkout and e-commerce growth, improved cross-border trends, and new value-added services.

The payments company reported second-quarter net income of $1.03 billion, or 92 cents a share, whereas it recorded a net loss of $341 million, or 29 cents a share, in the year-earlier period. On an adjusted basis, PayPal earned $1.16 a share, up from 93 cents a share a year prior, while the FactSet consensus was for $1.15 a share.

PayPal logged $376.5 billion in total payment volume for the period, while analysts had been expecting $368.9 billion.

Chief Executive Dan Schulman told MarketWatch that PayPal was seeing encouraging spending trends throughout the business and in the industry, as e-commerce growth picks up, discretionary purchasing improves and consumers start to rebalance their preferences once again after dramatically weighting their dollars more toward travel and services when the economy initially reopened.

A better balance of spending on goods versus services helps drives e-commerce growth, and “any uptick in e-commerce is going to accelerate our growth as well,” Schulman said.

Amid concerns from some corners of Wall Street about Apple Pay’s advancement, Schulman was confident in the state of PayPal’s branded checkout business.

“In our view we would expect that our branded checkout would be at or above the growth of e-commerce levels going forward,” he said.

PayPal still expects to drive at least 100 basis points of operating-margin expansion for the full year, and it also continues to anticipate about $4.95 in adjusted EPS for 2023. PayPal expects second-half revenue to at least match its first-quarter revenue total.

For the third quarter, PayPal expects $1.22 to $1.24 in adjusted earnings per share, along with revenue of about $7.4 billion. The FactSet consensus was for $1.21 in adjusted EPS and $7.3 billion in revenue.

There are two certainties in the tech world when it comes to digital advertising: Google and Meta. And then there’s everyone else.

Through economic thick and thin, Google and Meta are the gold standards by virtue of broad reach (billions of people globally), product dominance (in search and social media, respectively) and in their positions in the lightning-fast AI race. This week’s earnings results for Alphabet Inc. GOOGL, +2.46%

Both companies rebounded from recent wobbly digital ads sales of their own through giganticconsumer reach and aggressive plans to parlay AI into ad sales. Google has developed (or dabbled) in some form of AI for at least seven years, and in a conference call with analysts Wednesday, Meta Chief Executive Mark Zuckerberg said his company will focus in the near term on AI to develop agents, ad features in existing products like Instagram and Reels, and internal productivity and efficiency. “We want to scale them, but they are hard to forecast,” he admitted.

“We continue to believe it will take multiple quarters of improved execution for many investors to get more comfortable with the story longer term,” JP Morgan analysts said in a note on Snap earlier this month.

Digital-advertising leader Google sought to remind everyone it has been doing AI a long time while Microsoft Corp. MSFT, +2.31%,

a major investor in ChatGPT pioneer OpenAI, tempered its approach, Josh Wetzel, chief revenue officer at OneSignal, said in an interview. “AI’s greatest immediate value may be for Facebook advertising,” he said, pointing to it as an efficient and effective tool after Facebook encountered issues with data-privacy changes Apple Inc. AAPL, +1.35%

made to mobile devices.

“Meta’s solid quarter adds further evidence to the view that advertisers are choosing to spend their budget on the so-called market leaders, such as Facebook and Instagram, at the expense of the smaller social-media networks, like Snap,”said Jesse Cohen, senior analyst at Investing.com.

Jon Oberlander, executive vice president of social at digital-marketing agency Tinuiti, added: “It is, to some extent, still Meta/Google’s game, especially for performance advertisers, as the ROI and scale advertisers can find in the mid-lower funnel gap above other platforms.”

At the same time, Forrester analyst Kelsey Chickering said linear television ad revenue will slow between now and 2027 to about $65 billion from $70 billionas traditional TV continues to lose the under-25 crowd that has fled to streaming services and creator-heavy platforms like Snapchat and TikTok.

Digital advertising is on track to grow in the high single digits, or more, in 2023, slightly ahead of June’s forecast estimates from GroupM and Magna of around 8% each, according to Brian Wieser, head of Madison and Wall, a media and advertising consultancy for investors.

Most of that growth will benefit Google, Meta, and Microsoft’s LinkedIn, according to data from Emburse. Conversely, Emburse found ad spending on Twitter/X has plunged 54% from a year ago in May, before Elon Musk bought the company.

“Google, Meta and LinkedIn are platforms where people go to consume information, search for ideas, or give context to what they experiencing in their personal or work lives,” Emburse Chief Experience Officer Johann Wrede said.

While Alphabet CEO Sundar Pichai boasted Wednesday of “continued leadership in AI and our excellence in engineering and innovation are driving the next evolution of Search” and other services, as well as improved YouTube ad sales, Meta’s addition of potential X-killer Threads could dramatically inflate its ad sales going forward.

Zuckerberg sees potential in Threads long term despite a plunge in its user sign-ups because X is hemorrhaging advertising clients, and this week reportedly slashed ad costs to lure business customers.

“The launch of Threads holds great promise for Meta. While there are currently no ads on the app, it’s inevitable that they will come and the ability to use data from other Meta properties for targeting is a highly lucrative proposition for brands,” Aaron Goldman, chief marketing officer at Mediaocean, said in an email.

That translates to more near-term pain for smaller platforms such as Snap and X, which are posting negative growth, Michael Nathanson of SVB MoffettNathanson warned in a note Wednesday.

“The truth is that Alphabet started integrating machine learning and artificial intelligence into their products and ad solutions close to a decade ago,” he said. Snap and others are scrambling to catch up.