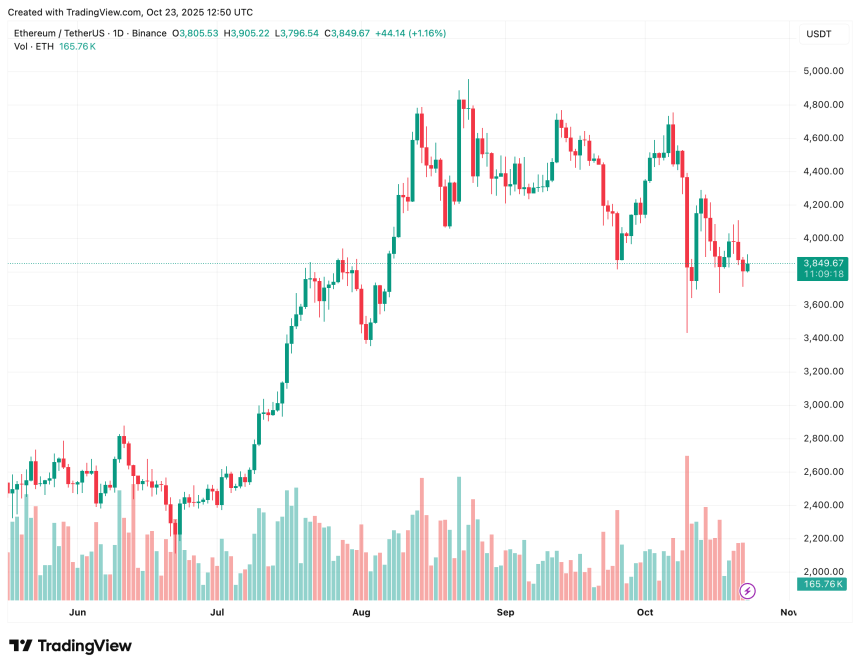

Ethereum (ETH), the second-largest cryptocurrency by market cap, continues to trade slightly below the psychologically important $4,000 price level, following the brutal drawdown on October 9, which saw the digital currency test the support at around $3,435.

According to a CryptoQuant Quicktake post by contributor TeddyVision, Ethereum is trading above its Realized Price at approximately $2,300. Dubbing the price level a “fundamental support zone,” the analyst said that historically, any dips below this level have marked a capitulation phase.

Related Reading

For the uninitiated, Realized Price represents the average cost basis of all ETH holders, calculated by dividing the total value of all ETH at the time they last moved on-chain by the current circulating supply.

Realized Price effectively shows the “true” average price investors paid, serving as a key indicator of whether the market is in profit or loss. As long as ETH trades above Realized Price, the market structure is likely to remain bullish.

The analyst also highlighted Ethereum’s Market Value to Realized Value (MVRV) ratio. Notably, ETH holders are currently, on average, at 67% profit relative to their cost basis. This metric gives two major hints about the current market.

First, it shows that although the market is profitable, it is still far from “overheated” levels. Second, it indicates that market participants are confident about the market’s upward momentum, but not quite euphoric.

To explain, the MVRV ratio compares the market value of an asset to its realized value. A higher MVRV indicates holders are sitting on larger unrealized profits – often signaling potential overvaluation – while a lower MVRV suggests undervaluation or market fear.

Further, TeddyVision noted Ethereum’s reaction from the Upper Realized Price Band, which is currently located around $5,300. The analyst remarked:

Price pulled back before reaching the “Overheating Zone. This isn’t a reversal – it’s a consolidation phase after distribution, a healthy cooldown without structural damage.

Finally, spot inflows of ETH to crypto exchanges are also slowing down, hinting that the next leg up for the digital asset will likely depend on fresh liquidity, and not leverage. To sum it up, Ethereum is slowly moving from the distribution phase to the consolidation phase.

Is It A Good Time To Buy ETH?

While providing reliable future predictions in the crypto market remains a challenging task, fresh on-chain and exchange data point toward ETH regaining its bullish momentum. For instance, Binance funding rates recently hinted that ETH could surge to $6,800.

Related Reading

Similarly, ETH reserves on exchanges continue to fall at a rapid pace. Earlier this month, ETH supply on exchanges hit a multi-year low, increasing the probability of a potential “supply crunch” that can dramatically increase ETH’s price.

That said, crypto analyst Nik Patel recently cautioned that ETH’s price correction may not yet be fully over. At press time, ETH trades at $3,849, up 0.3% in the past 24 hours.

After the massive crash on October 10 – which saw Bitcoin (BTC) touch $102,000 before recovering some losses – some analysts now predict that the top cryptocurrency may be on the verge of another bullish rally as it enters the ‘disbelief phase.’

Bitcoin In Disbelief Phase – Trouble For Bears?

According to a CryptoQuant Quicktake post by contributor Darkfost, Bitcoin appears to be entering the disbelief phase, which increases the possibility of a rebound to the upside. The contributor emphasized the slightly negative funding rate to support their analysis.

Related Reading

For the uninitiated, the Bitcoin disbelief phase occurs when a new uptrend begins, but most investors remain skeptical after a recent correction, doubting that the recovery is real. During this phase, lingering bearish sentiment and short positions often act as fuel for a stronger rally once confidence returns.

Darkfost stated that investors’ skepticism toward BTC returning to bullish mode can be gauged through BTC funding rates in the derivatives market. Funding rates remained negative at -0.004% on the exchange for six out of seven days over the past week, indicating traders are still slightly bearish.

The likely reason behind traders’ short bias is the October 10 crypto market crash that led to a liquidation worth $19 billion. Since then, traders have consistently chosen to short the market instead of getting trapped in another price pullback.

However, the longer BTC remains in the disbelief phase, the stronger the potential for an explosive upside move becomes. Darkfost added:

If the current uptrend continues to establish itself, the growing pile of short positions against it could become a powerful fuel for the next leg higher. As these shorts get liquidated, it would drive prices upward, triggering a short squeeze.

If a short squeeze happens, then BTC could quickly rally to major liquidity zones around $113,000 level, and even as high as $126,000 region, where significant short orders liquidations are clustered.

The analyst shared two previous instance where such a pattern played out. In September 2024, BTC fell to $54,000 before surging to a new all-time high beyond $100,000.

Similarly, in April 2025, the flagship digital asset rallied from $85,000 to $111,000, before climbing even higher to $123,000. To conclude, the Bitcoin market may be on the verge of another short squeeze, fueled by investors’ skepticism.

BTC Investors Need To Be Cautious

Although BTC is giving hints of a looming short squeeze, investors should still exercise some caution before entering the market in hopes of an instant turnaround in sentiment. For example, Bitcoin activity recently slumped below its 365-day average, raising fears of a loss of momentum.

Related Reading

That said, some crypto analysts forecast that BTC is likely done with the price correction and is set to surge in the coming days. At press time, BTC trades at $110,814, up 2.8% in the past 24 hours.

Bitcoin (BTC) witnessed a slight surge earlier today, climbing from $113,000 to around $117,000 at the time of writing, in contrast to expectations of several crypto analysts who were predicting a decline in risk-on assets due to the US government shutdown.

Bitcoin Rises Despite US Government Shutdown

The US federal government shut down at midnight on September 30, as President Donald Trump and Congress failed to reach a deal on funding. Specifically, the two camps were at odds over enhanced Obamacare subsidies, with neither party willing to take the blame.

Related Reading

However, Bitcoin made a surprise move to the upside despite the uncertain environment created by the US government shutdown, recording strong gains earlier today. CryptoQuant analyst Kripto Mevsimi stated that September saw deeper losses among short-term holders (STH), as their Spent Output Profit Ratio (SOPR) fell as low as 0.992.

As a result, most of September was marked by STH continuing to sell their BTC holdings at a loss. However, the metric recovered slightly to 0.995, although it is still below August’s reading of 0.998.

The current STH-SOPR reading is showing signs of stabilization after a period of depression. It is interesting to note the timing of this recovery, as it occurred at a time when BTC is trading in the high $110,000 range, slightly below a heavy resistance zone.

Past data shows two potential scenarios that can happen following such a reset in the STH-SOPR. First, it could be early warning signs of a weakening momentum for BTC, as extended loss realization can precede corrective phases where weak hands capitulate.

The other, more bullish scenario, is that it could be a healthy reset. Quick absorption of realized losses often paves the way for more sustainable rallies, which could catapult BTC to new all-time highs (ATH) in the near term. The CryptoQuant analyst added:

With BTC consolidating under resistance, this rebound in STH-SOPR is a key barometer of market health. If buyers continue to absorb weak-hand selling, it could mirror past resets that paved the way for the next leg higher.

Will BTC Decline In Q4 2025?

While the dwindling active circulating supply of Bitcoin offers some hope to the bulls, others are not as optimistic. According to recent analysis by fellow CryptoQuant contributor Axel Adler, demand for BTC cooled after it failed to hold above $115,000.

Related Reading

Meanwhile, crypto analyst Doctor Profit recently remarked that BTC is likely to experience another 20% decline from its current price, reaching his projected target range between $90,000 – $94,000. At press time, BTC trades at $117,226, up 3.5% in the past 24 hours.

The below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Analyzing On-Chain Bottom Indicators

In this week’s dashboard release, we highlighted some key on-chain metrics we like to track. In this article, we want to walk through more of those in detail. Across bitcoin’s short history, many on-chain cyclical indicators are currently pointing to what looks to be a classic bottom in bitcoin price. Market extremes — potential tops and bottoms — are where these indicators have proven to be the most useful.

On-chain indicators overlaid with previous bitcoin price bottoms.

However, these indicators need to be considered alongside many other macroeconomic factors and readers should consider the possibility that this could be another bear market rally — as we still sit below the 200-week moving average price of around $24,600. That being said, if price can sustain above $20,000 in the short-term, the bullish metrics paint a compelling sign for more long-term accumulation here.

A major tail risk is a possible market-wide selloff in risk assets that are currently pricing a “soft landing” style scenario along with the potentially incorrect expectations of a Federal Reserve policy pivot in the second half of this year. Many economic indicators and data still point to the likelihood that we’re in the midst of a bear market similar to 2000-2002 or 2007-2008 and the worst has yet to unfold. This secular bear market is what’s different about this bitcoin cycle compared to any other in the past and what makes it that much harder to use historical bitcoin cycles after 2012 as perfect analogues for today.

All that being said, from a bitcoin-native perspective, the story is clear: Capitulation has clearly unfolded, and HODLers held the line.

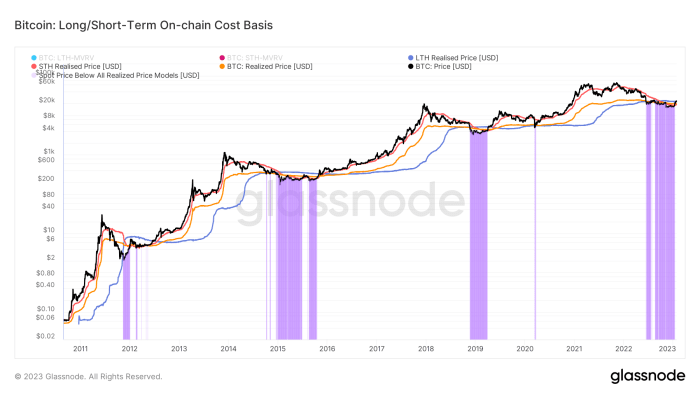

Given the transparent nature of bitcoin ownership, we can view various cohorts of bitcoin holders with extreme clarity. In this case, we are viewing the realized price for the average bitcoin holder as well as the same metric for both long-term holders (LTH) and short-term holders (STH).

The realized price, STH realized price and LTH realized price can give us an understanding of where various cohorts of the market are in profit or underwater.

A look at realized price for short- and long-term holders.

On a monthly basis, realized losses have flipped to realized profits for the first time since last April.

Capitulation and loss taking has flipped to profit realization across the network, which is a very healthy sign of thorough capitulation.

There is a strong case to be made that given the current elasticity of bitcoin’s supply — as evidenced by the historically small number of short-term holders or rather the large number of long-term holders — it will be challenging to shake out current market participants. Especially considering the gauntlet endured over the previous 12 months.

Statistically, long-term bitcoin holders are usually unfazed in the face of bitcoin price volatility. The data shows a healthy amount of accumulation throughout 2022, despite a massive risk-off event in both the bitcoin and legacy market.

While liquidity dynamics in legacy markets should be noted, the supply-side dynamics for bitcoin look to be as strong as ever. All it will take for a significant price appreciation will be a small influx of newfound demand.

Like this content? Subscribe now to receive PRO articles directly in your inbox.

The below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

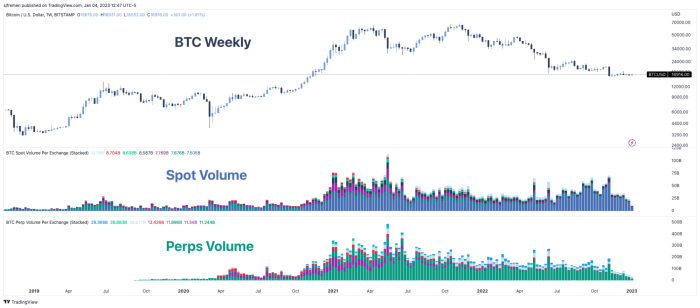

As we head into 2023, we want to highlight the latest state of bitcoin’s volume and volatility after a recent wave of capitulation. Last time we touched on these dynamics was in “The Bitcoin Ghost Town” in October, where we highlighted that an extremely low volume and low volatility period in bitcoin price, GBTC and the options market was a concerning sign for the next leg lower. This played out in early November.

Fast forward and the trends of declining volume and low volatility are back once again. Although this could be indicative of another leg lower to come in the market, it’s more likely indicative of a complacent and decimated market that few participants want to touch.

Even during the November 2021 capitulation period, there was a historically low period of volatility. Sometimes the most market pain can be felt when having to wait for a clear change in trends. The bitcoin price is providing that pain as we’ve yet to see the type of explosion in market volatility that has defined market pivots and major directional moves in the past.

SPX Bottoms

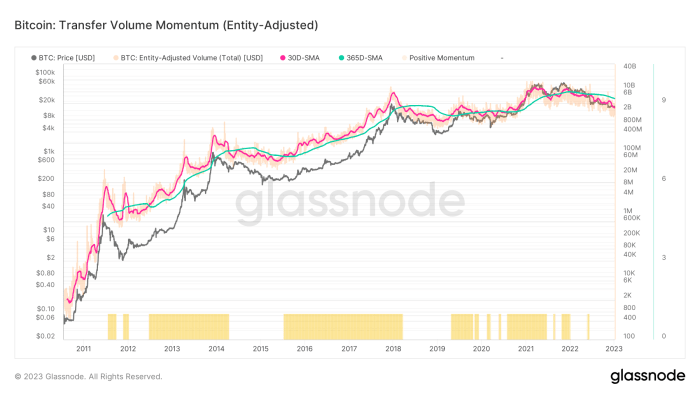

While there are many different ways to define, classify and estimate bitcoin volume in the market, they all show the same thing: September and November 2021 were the peak months of action. Since then, volume in both the spot and perpetual futures markets have been in steady decline.

Bitcoin volume across spot and perpetual futures markets

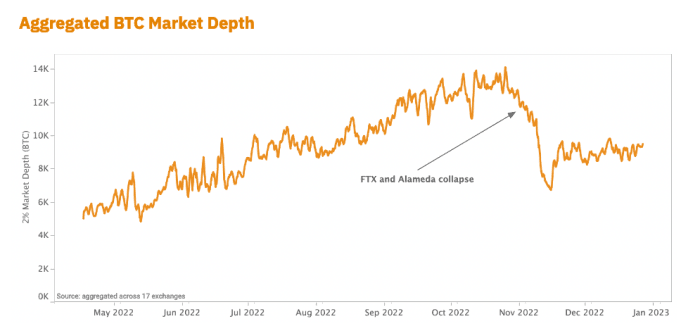

Overall market depth and liquidity has also taken a major hit after the collapse of FTX and Alameda. Their destruction has led to a large liquidity hole, which is yet to be filled due to the lack of market makers currently in the space.

By far, bitcoin is still the most liquid market of any other cryptocurrency or “token,” but it’s still relatively illiquid compared to other capital markets since the whole industry has been crushed over the last few months. Lower market depth and liquidity means assets are prone to more volatile shocks as single, relatively large orders can have a greater impact on market price.

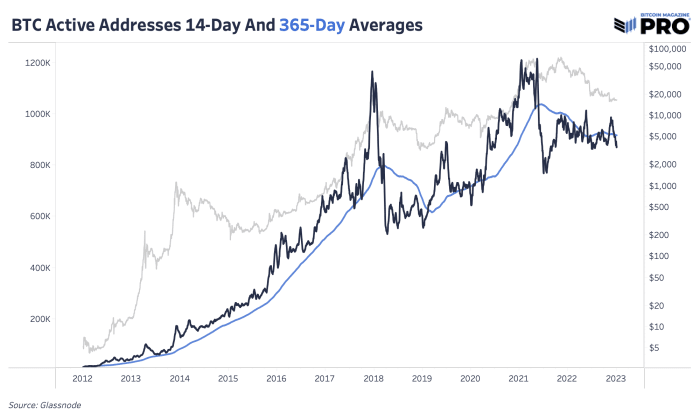

As expected in the current environment, we’re also seeing more market complacency when looking at on-chain data. Although continuing to rise over time, the number of active addresses — unique addresses active as either a sender or receiver — remain fairly stagnant over the last few months. The chart below highlights the 14-day moving average of active addresses falling below the running average over the last year. In previous bull market conditions, we’ve seen growth in active addresses outpace the existing trend fairly significantly.

Moving averages of active bitcoin adresseses

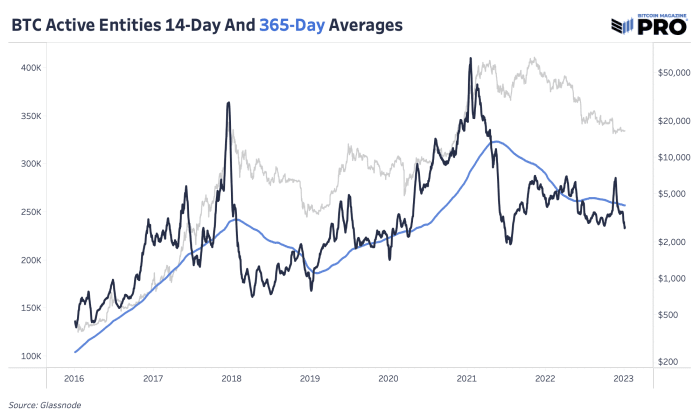

Since address data has its flaws, looking at Glassnode’s data for active entities shows us the same trend. Overall, bear markets reversing are the result of many factors, including growth in new users and an increase in on-chain activity.

Moving averages of active bitcoin entities

Bitcoin transfer volume momentum

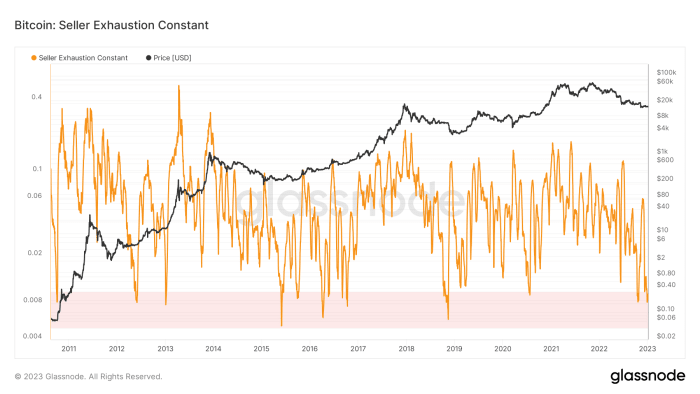

Bitcoin seller exhaustion levels

In our July 11 release “When Will The Bear Market End?”, we made the case that the brunt of the price-based capitulation had already been felt, while the real pain ahead was in the form of a time-based capitulation.

“A look at previous bitcoin bear market cycles shows two distinct phases of capitulation:

“The first is a price-based capitulation, through a series of sharp selloffs and liquidations, as the asset draws down anywhere from 70 to 90% below previous all-time-high levels.

“The second phase, and the one that is spoken of far less often, is the time-based capitulation, where the market finally begins to find an equilibrium of supply and demand in a deep trough.” — Bitcoin Magazine PRO

We believe time-based capitulation is where we stand today. While exchange rate pressures can certainly intensify over the short term — given the macroeconomic headwinds that remain — the conditions that look likely to persist over the short and medium term look to be a sustained period of chop with extremely low levels of volatility that leave both traders and HODLers questioning when volatility and exchange rate appreciation will return.

Like this content? Subscribe now to receive PRO articles directly in your inbox.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

On-Chain Data Trends

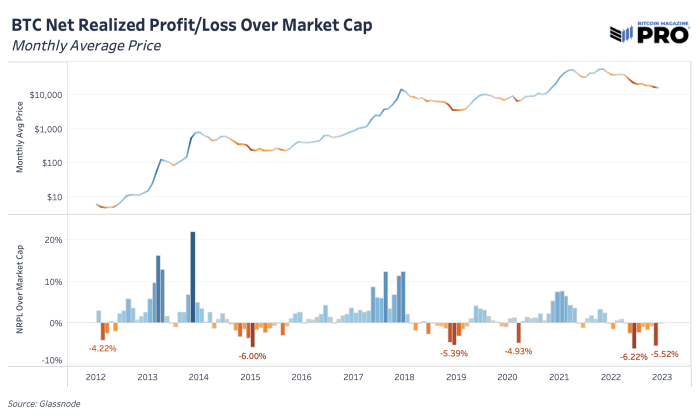

November was a painful month. By looking at on-chain realized profit and loss data, we can see that this was true for many forced-sellers of bitcoin. Before any bitcoin price bottom, a hallmark sign that you want to see is extended periods of forced selling, capitulation and rise in realized losses. One way to view this is by looking at the sum of realized profit and loss for each month relative to bitcoin’s total market cap. We saw these bottom signals in November 2022, and similarly in the July 2022 Terra/LUNA crash, March 2020 COVID fear and December 2018 cycle bottom capitulation events.

Net realized profit/loss over market cap

Looking at the 2018 cycle, the end was marked by excess realized losses, although this was much different with the forced liquidations and cascades of private balance sheet leverage and paper bitcoin unwinding that we saw this year.

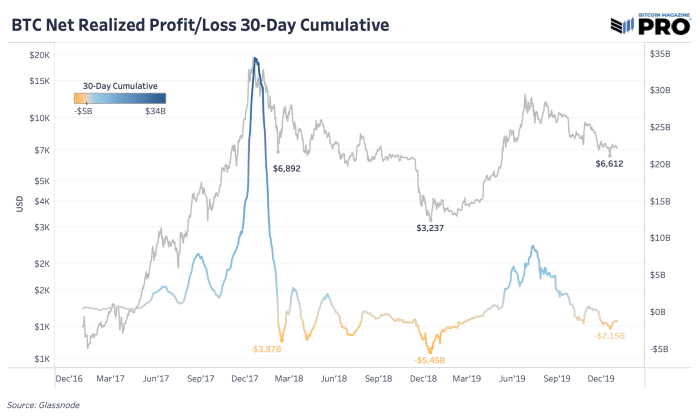

30-day cumulative net realized profit/loss

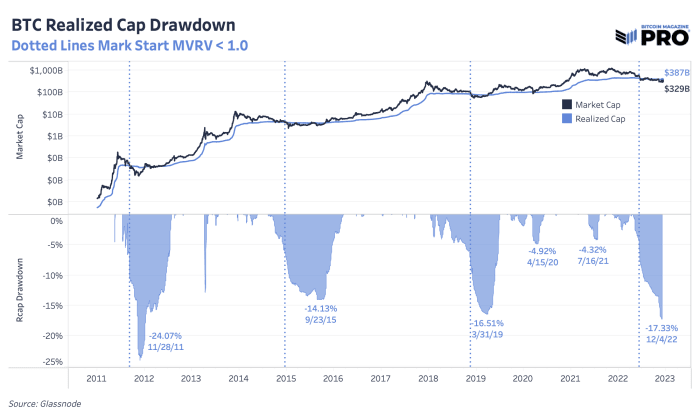

We’ve talked about the current drawdown in bitcoin’s price and how that compares to previous cycles many times over the last few months. Another way to look at cyclical drawdowns is to focus on bitcoin’s realized market capitalization — the average cost basis of the network which tracks the latest price where each UTXO moved last. With price being more volatile, realized price is a more stable view of bitcoin’s growth and capital inflows. The realized market capitalization is now down 17.33% which is significantly higher than 2015 and 2018 cycles of 14.13% and 16.51%, respectively.

Bitcoin realized cap drawdown

As for duration, we’re 176 total days into the price being below bitcoin’s realized price. Those aren’t consecutive days as price can temporarily go above realized price, but price trends below realized price in bear market periods. For context, trends in 2018 were short-lived at around 134 days and the trends in 2014-15 lasted 384 days.

On one hand, bitcoin’s realized market capitalization has taken a significant hit in the previous round of capitulation. That’s a promising bottom-like sign. On the other hand, there’s a case to be made that price being below realized price could easily last another six months from historical cycles and the lack of capitulation in equity markets is still a major headwind and concern.

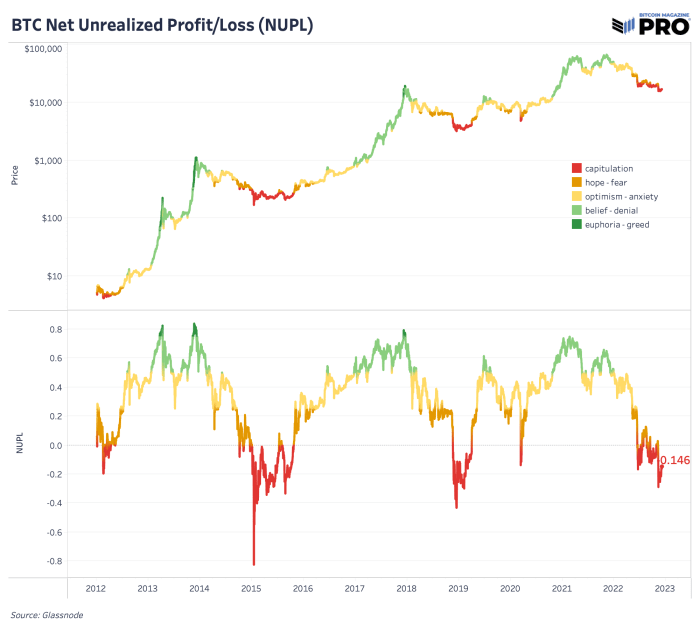

Net unrealized profit/loss

As per the net-unrealized-profit/loss (NUPL) ratio, we are firmly in the capitulation phase. NUPL can be calculated by subtracting the realized cap from market cap and dividing the result by the market cap, as described in this article authored by By Tuur Demeester, Tamás Blummer and Michiel Lescrauwaet.

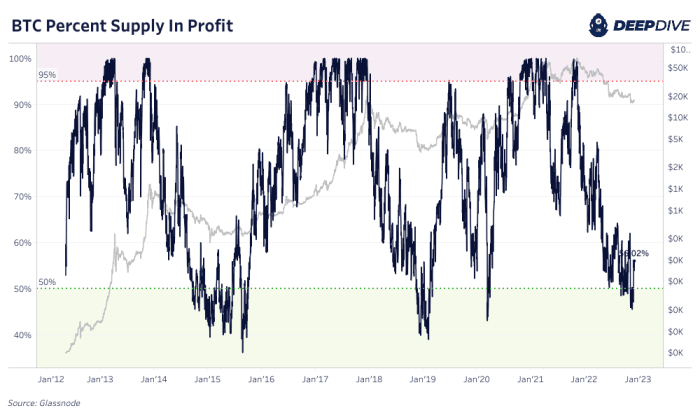

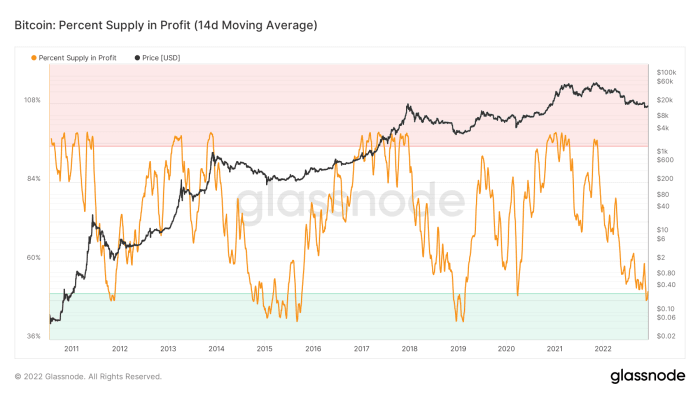

There is no denying it: For bitcoin-native cycles, we are firmly in the capitulation phase. Currently, only 56% of circulating supply was last moved on-chain in profit. On a two-week moving average basis, under 50% supply was last moved above the current exchange rate, which is something that has only ever happened in the depths of previous bear-market lows.

Percent of bitcoin supply in profit

14-day moving average of the percent of bitcoin supply in profit

When thinking of the bitcoin exchange rate, the numerator side of the equation is historically cheap. The Bitcoin network continues to produce a block approximately every 10 minutes in an unabated fashion, as hash rate ticks higher and as the ledger offers an immutable settlement layer for global value. The speculation, leverage and fraud of the previous cycle is washing to shore and bitcoin continues to exchange hands.

Bitcoin is objectively cheap relative to its all time history and adoption phases. The real question over the immediate future is the denominator. We have talked at length about the global liquidity cycle and its current track. Despite being historically cheap, bitcoin is not immune to a sudden strengthening in the dollar because nothing truly is. Exchange rates are relative and if the dollar is squeezing higher, then everything else will subsequently fall — at least momentarily. As always, position sizing and time preference is key for all.

As for the catalyst for a surge higher in the dollar denominator of the bitcoin exchange rate (BTC/USD), there are 80 trillion possible catalysts…

This is an opinion editorial by Shane Neagle, the editor-in-chief of “The Tokenist.”

Macroeconomic headwinds are continuously adding to a bearish narrative across all markets, including bitcoin.

As of October 2022, bitcoin is down more than 60% since the start of the year, yet bitcoin’s trading volume remains fairly consistent since July 2022. Does that mean the majority of holders are giving up on the prospect of bitcoin and opting to sell?

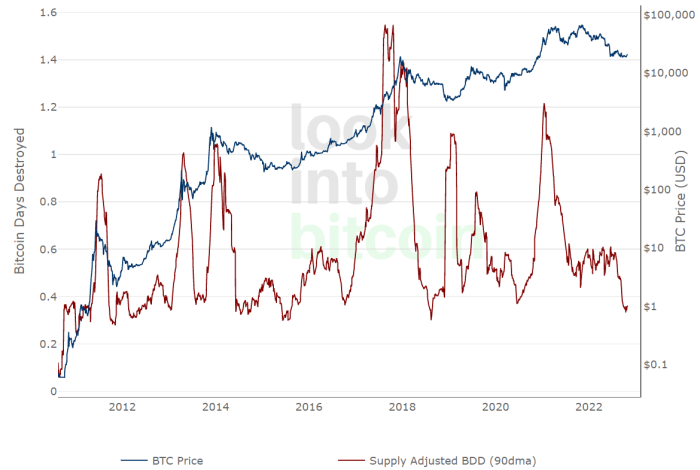

This is a complex topic to dive into, but there’s one indicator that can help us paint a picture of what’s taking place behind the noise: coin days destroyed (CDD).

What Are Coin Days Destroyed?

Throughout the course of an asset’s trading history, there is a significant difference if the buying price was on the lower or higher end of the price spectrum. In the case of bitcoin, that spectrum is relatively short — just 13 years — but quite variable in terms of price (ranging from $0-$69,000). The original cryptocurrency has undergone four major bull and bear cycles, but when zooming out, has continuously trended upwards.

The implication of this long-term, upward trajectory is clear. Investors who were the earliest to buy bitcoin have the most to gain by selling, even in bear markets. Likewise, investors who took the opportunity to purchase bitcoin early and at a lower cost, had the opportunity to buy much more bitcoin for the same amount of fiat currency compared to prices later in bitcoin’s history.

In turn, bitcoin that were mined and purchased earlier have different value significance than newer bitcoin released into the circulating supply. If these “aged” bitcoin are held in the same wallet for an extended period of time, such on-chain activity would suggest a strong conviction held by the owner in terms of bitcoin’s long-term value proposition. Such activity sends a strong signal to the Bitcoin network.

In addition, a long-term holder of dormant bitcoin has an increased likelihood of experiencing multiple bear and bull market cycles, which further amplifies the significance of old bitcoin moving.

The metric of coin days destroyed measures this significance. According to Glassnode, “Coin days destroyed is a measure of economic activity which gives more weight to coins which haven’t been spent for a long time.” CDD is calculated by multiplying the number of coins in a given transaction by the number of days since they last moved from a wallet.

Bitcoin is often critiqued for its high levels of volatility. Yet there’s clear demand for bitcoin in long-term investments, even in traditional IRAs. CDD is a popular on-chain indicator used to measure the sentiment maintained by long-term holders — individuals who see value in the long-term prospects of bitcoin.

So, what does the current CDD level suggest?

Bitcoin’s CDD Has Been Quite Low

At 0.36, the 90-day moving average of bitcoin’s CDD in October 2022 hit one of the lowest values throughout its history. This particular range was only visited previously in 2018, 2015 and late 2011. As the supply-adjusted bitcoin days destroyed (BDD) chart below shows, the highest BDD upticks happened during bull run peaks, which is to be expected as long-term holders lock in their profits.

In other words, long-term Bitcoiners — in the context of the asset’s historical selling activity — are continuing to hold bitcoin in large numbers. This could be one of the reasons why bitcoin’s price activity has been relatively stable. Such holders could be acting as safeguards against selling pressure.

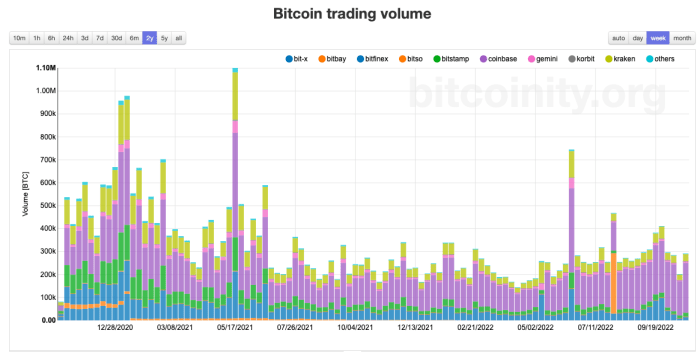

If we turn to bitcoin’s trading volume, do we see a similar pattern?

The above chart shows bitcoin’s trading volume from October 2020 to October 2022. What’s noted here is fairly steady and consistent trading volume from roughly July 2021 to October 2022. We do not see a drop, which resembles the activity from CDD.

The combination of data from these two indicators — a low CDD with steady and consistent trading volume — further suggests that most of the bitcoin traded was by short-term holders. In fact, bitcoin from 2010/2011, purchased at well under the $100 range, have moved the least.

Overall, according to Glassnode data, just over 60% of circulating BTC haven’t moved in over a year. This holding trend also contributed to bitcoin’s exceptionally low volatility. Comparatively, in 2018, a similar price volatility was followed by a 50% drop in a single month, from $6,408 in November to $3,193 in December.

Is it likely we will see a new bottom even with long-term Bitcoiners holding the line?

Additional Bitcoin Sell-Off Pressures

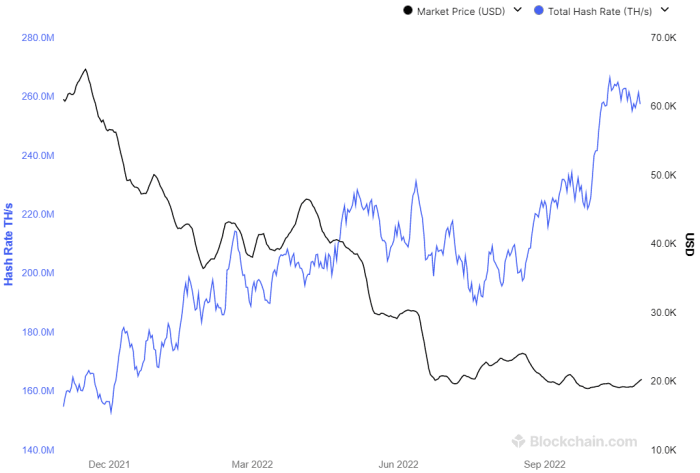

Presently, bitcoin’s price is inversely related to its record-high hash rate. This is not good news considering miners have to service their debts by selling mined bitcoin, even at their bottom price point in this bear cycle.

Argo Blockchain (ARBK) shares the same fate, having fallen by 91.56% and is unable to sell enough assets to cover the costs. According to an operational update from Argo in October 2022:

“Should Argo be unsuccessful in completing any further financing, Argo would become cash flow negative in the near term and would need to curtail or cease operations.”

Although these mining companies will likely end up lowering the Bitcoin hash difficulty, in a game of survival of the fittest this has the potential to cause another contagion spiral. This time around, vulnerability and market sell-offs could come from remaining centralized platforms that are lending dollars to bitcoin mining companies. Going back to the ongoing macroeconomic headwinds, how the market interprets the Federal Reserve’s next moves may end up raising the price of bitcoin just enough for miners to stay above water.

Because the Fed increases the cost of capital and borrowing, making the dollar stronger in the process, this typically makes investors leave risk-on assets, such as bitcoin. When investors forecast a recession, the dollar reigns even stronger, as investors dive into cash as a safe harbor.

With that said, the so-called “Fed pivot” should not be understood as a return to lower interest rates, but as a deceleration to potentially hiking only 50 basis points in December (if incoming inflation data favors it). Nonetheless, in the current fearful market environment, that may be sufficient for a short-term rally, or at least, the avoidance of a new bitcoin bottom.

Despite the many factors pushing investors away from risk-on assets — the Fed battling 40-year-high inflation, a looming energy crisis in Europe, ongoing global supply chain issues and even Bitcoin’s mining difficulty — data from CDD and bitcoin trading volume provides us with an interesting observation. Long-term holders seem more confident than ever in the long-term value proposition that bitcoin provides. Such holders are currently selling bitcoin at one of the lowest rates we’ve seen in the history of the Bitcoin network.

This is a guest post by Shane Neagle. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.