The adoption of artificial intelligence (AI) is continuing at a brisk pace, but some are waiting for the other shoe to drop. A strengthening U.S. economy and robust quarterly results from several AI-related companies helped push the Nasdaq Composite to a new record high last week. Yet these same factors have some investors wondering if the bull market has gone too far, too fast.

Nvidia(NASDAQ: NVDA) has become the de facto standard bearer for the generative AI industry. The company is scheduled to report its fiscal 2025 third-quarter results in less than three weeks, and it’s not an exaggeration to suggest that Wall Street is on pins and needles waiting for the clues that report will offer about the state of AI adoption. Nvidia’s sales have surged since the start of last year, driving the stock up 833% (as of this writing). It’s also less than 5% off the all-time high it touched late last month.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

There’s a lot riding on Nvidia’s upcoming financial report, and many shareholders are wondering whether the stock can possibly continue its breathtaking run. Is it worth picking up shares ahead of its financial report on Nov. 20? Fortunately for investors, data has begun to pile up that could help answer that question.

Image source: Getty Images.

The key to Nvidia’s astounding successes of the past couple of years has been the performance of its graphics processing units (GPUs), which are the best chips for supplying the specific type of computational horsepower necessary for generative AI, as well as other types of cloud computing needs. The necessary resources and the sheer magnitude of data involved limit the top-tier AI models to the world’s largest technology companies and cloud providers — most of which are Nvidia customers. Comments made in conjunction with those tech giants’ recent quarterly results provide some insights about the state of the AI revolution — and the evidence is clear.

For example, Microsoft(NASDAQ: MSFT) said it spent heavily to advance its AI agenda in its fiscal 2025 first quarter (which ended Sept. 30). The company had capital expenditures (capex) of $20 billion, which primarily went to support “cloud and AI-related” demand. CFO Amy Hood expects Microsoft’s spending spree to continue: “We expect capital expenditures to increase on a sequential basis given our cloud and AI demand signals,” she said.

During Alphabet‘s (NASDAQ: GOOGL)(NASDAQ: GOOG) third-quarter earnings call, CEO Sundar Pichai said, “Realizing [the opportunity] of AI requires … meaningful capital investment.” The company revealed capex of $13 billion during the quarter and suggested there would be “substantial increases in capital investment … going into 2025.”

Rounding out the big three cloud providers is Amazon(NASDAQ: AMZN). During its Q3 earnings call, CEO Andy Jassy called generative a “maybe once-in-a-lifetime type of opportunity … we’re aggressively pursuing it.” CFO Brian Olsavsky put that in context, saying Amazon’s capex would amount to roughly $75 billion this year, with much of that going toward cloud computing and AI infrastructure. The company also said it would unveil “100 new cloud infrastructure and AI capabilities” at AWS re:Invent later this month.

Finally, there’s Meta Platforms(NASDAQ: META). While it isn’t a cloud provider, the company’s social media sites attract 3.29 billion people every day, giving Meta vast volumes of user data. The company increased its full-year capex outlook to roughly $39 billion, and CFO Susan Li said, “We continue to expect significant capital expenditures growth in 2025.” She previously noted this was “to support our AI research and product development efforts.”

The trend of accelerating capex to support the growing demand for AI is clear. Additionally, a large fraction of that money will be spent on the data centers and servers needed for cloud computing — where the majority of generative AI software lives. As such, Nvidia will likely be the recipient of a good deal of this spending.

Nvidia has historically kept mum about its biggest customers, but that hasn’t stopped Wall Street from doing some digging. Analysts with Bloomberg and Barclays Research have run the numbers and come to the conclusion that Nvidia’s four biggest customers — generating a total of 40% of its sales — are:

Microsoft: 15%

Meta Platforms: 13%

Amazon: 6.2%

Alphabet: 5.8%

Each of these companies has left no question about their plans to spend heavily on capital expenditures, and in particular to spend heavily on infrastructure to support their cloud computing and AI aspirations. As the leading provider of data center GPUs, Nvidia will likely continue to top the list of beneficiaries of that spending.

Nvidia will deliver its next set of quarterly results on Nov. 20. After achieving triple-digit-percentage year-over-year growth for five consecutive quarters, the company has tried to rein in the market’s expectations, suggesting that its revenue growth this time will only clock in at about 79%. While that would be a deceleration, it would also still be remarkable growth by any stretch of the imagination.

Investors looking to make money over the coming three weeks might be disappointed. No one can say for sure how Nvidia stock will react to the report — even if the company exceeds expectations.

For a reminder of the difficulties involved in short-term prognostication, investors need only look back to this summer, when, starting in mid-June, Nvidia stock lost as much as 27% of its value on fears that its next-generation Blackwell AI processors would be delayed — only to come roaring back. It was an illustration that with this stock, volatility is part of the cost of admission. That said, both the comments made by its big tech customers and their historical spending patterns suggest that Nvidia has further strong growth ahead.

For investors looking for stocks to hold for years and decades rather than weeks and months, Nvidia is a clear choice to benefit from the AI revolution. And trading at roughly 32 times next year’s earnings, it’s still attractively priced. I can’t say for sure what the stock will do between now and Nov. 20. What I can say — with a fair degree of confidence — is that investors who buy Nvidia stock soon and hold it for three to five years or more will be very glad they did.

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $829,746!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Danny Vena has positions in Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Expectations were high heading into Nvidia‘s (NASDAQ: NVDA) fiscal 2025 second-quarter financial report. The company has become the de facto standard bearer for the artificial intelligence (AI) revolution. Its graphics processing units (GPUS) provide the computational horsepower necessary to create the large language models (LLMs) that make generative AI possible.

The surging demand for AI has propelled Nvidia’s stock into the stratosphere. The stock has gained more than 150% so far this year and more than 750% since the accelerating adoption of AI kicked off early last year (as of this writing).

In recent weeks, however, investors have become concerned that Nvidia has simply come too far, too fast, and they are wondering whether the hectic pace of AI adoption could continue. Nvidia answered that question with a resounding “yes,” but given the stock’s parabolic gains, blockbuster results simply weren’t enough.

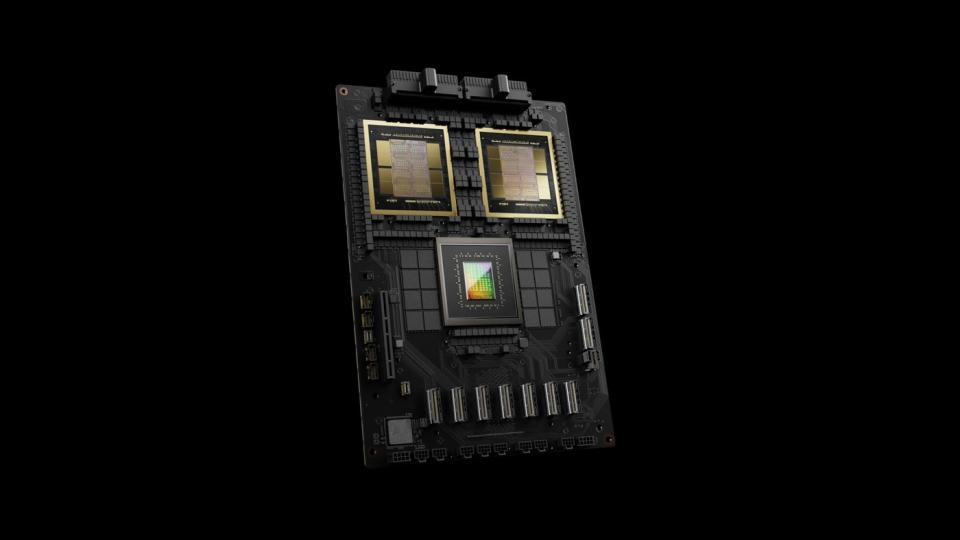

Nvidia’s GB200 Grace Blackwell AI Superchip. Image source: Nvidia.

By the numbers

In the second quarter, Nvidia generated record revenue of $30 billion, which surged 122% year over year and 15% quarter over quarter. This gave rise to adjusted earnings per share (EPS) of $0.68. The results sailed past analysts’ consensus estimates for revenue of $28.6 billion and EPS of $0.64. Revenue also eclipsed management’s forecast of $28 billion.

The headliner was Nvidia’s data center segment — which includes chips used for AI — as revenue of $26.3 billion soared 154% year over year and 16% sequentially, fueled by strong AI adoption among cloud computing and hyperscale data center operators.

It wasn’t just AI that fed Nvidia’s growth, though the data center segment dwarfed results from the company’s other segments (all segment gains year over year):

The gaming segment grew 16% to $2.9 billion.

The professional visualization segment jumped 20% to $454 million.

The auto segment climbed 37% to $346 million.

Original equipment manufacturer increased 33% to $88 million

Nvidia’s gross margin of 75.1% was up compared to 70.1% in the prior year quarter, largely due to the company’s enormous pricing power. That said, the measure edged lower sequentially from 78.4% in Q1. The company had previously signaled margins would moderate throughout the remainder of the year. CFO Colette Kress cited inventory provisions for its Blackwell chips and product mix for the decline.

What the future holds

CEO Jensen Huang noted that demand for its current Hopper chip “remains strong,” calling anticipation for its next-generation Blackwell architecture “incredible.” He went on to note that in recent industry testing, Nvidia’s Hopper H200 and the Blackwell B200 chips “swept” the MLPerf benchmark results for AI inference. Despite the best efforts of its rivals, Nvidia chips remain the gold standard for processing AI.

Media reports suggested that the new Blackwell chips might be delayed by as much as three months due to design flaws, but Nvidia put those fears to rest. “We shipped customer samples of our Blackwell architecture in the second quarter. We executed a change to the Blackwell GPU mask to improve production yield. Blackwell production ramp is scheduled to begin in the fourth quarter and continue into fiscal 2026.”

Another by-product of Nvidia’s growth trajectory is the tremendous amount of cash the company is generating, as free cash flow more than doubled to $13.5 billion. As a result, Nvidia is increasing its returns to shareholders. The board of directors approved an additional $50 billion in share buybacks, adding to the $7.5 billion remaining on its existing authorization.

These factors have combined to fuel a robust outlook for the third quarter. Management is guiding for revenue of $32.5 billion, which would represent year-over-year growth of 80%. That’s a deceleration from the triple-digit growth Nvidia has delivered in each of the past five quarters — but investors have long known that growth of that magnitude couldn’t continue indefinitely. Yet, the numbers show investors were seemingly disappointed.

Nvidia stock was down roughly 7% in after-hours trading (as of this writing,) but it’s too early to tell what tomorrow will bring. Taking a step back, the company’s results continue to defy the odds, but a deceleration in its parabolic growth rate was inevitable. Nvidia’s star is still burning brightly, and the long-term investing thesis is intact.

Taken together, Nvidia’s durable competitive advantage, strong results, and robust outlook show the company still has a long runway for growth ahead.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $786,169!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

Artificial intelligence (AI) is one of the hottest industries for investors right now. Semiconductor darling and data center specialist Nvidia(NASDAQ: NVDA) is considered by many on Wall Street to be a lucrative opportunity for AI enthusiasts.

With shares of Nvidia up over 170% so far in 2024, some investors may think they’ve missed the boat.

Let’s take a look at what is going on at Nvidia, and assess if now is still a reasonable time to scoop up some shares.

Nvidia’s hot start to 2024

2023 marked a new age for the technology industry. Behemoths such as Microsoft, Alphabet, and Amazon all made a series of splashy investments revolving around AI applications.

Some of the bigger investments these tech giants made were buying AI-powered semiconductor chips, as well as ramping up data center services. Considering Nvidia has an estimated 80% share of the AI chip market, these moves by big tech undoubtedly served as a big boost to the company.

The strong momentum from last year’s AI euphoria carried into 2024, and Nvidia investors haven’t stopped buying up the stock. To put this into context, shares of Nvidia have increased almost 800% since January 2023.

What’s incredible is that much of the narrative surrounding Nvidia deals with the company’s chip business. Indeed, its H100 and A100 graphics processing units (GPUs) are used by companies all around the world — including Meta Platforms and Tesla.

Moreover, Nvidia is continuing to lead the innovation front in the GPU realm with the introduction of its new Blackwell and Rubin chips.

With that said, it’s important to understand that Nvidia makes money from other products and services as well. In fact, one of its lesser-known growth opportunities is outside of hardware.

Nvidia’s compute unified device architecture (CUDA) software platform is already proving to be a lucrative business. Essentially, CUDA is a programming tool that is meant to be used in parallel with Nvidia’s GPUs. So, in a sense, the company is attempting to build out an end-to-end AI ecosystem encompassing both hardware and software.

One of the big reasons CUDA is going to be important for Nvidia is due to competition in the chip space. Companies such as AMD, Intel, and even Amazon and Meta are all working on competing GPUs to that of Nvidia.

Although it’s too early to get a sense of how these competing products will impact Nvidia, I think it’s reasonably safe to say that the company will eventually lose some of its pricing power in the chip space. As a result, Nvidia’s profit margins are likely to take a hit at some point in the future. However, some of this margin deterioration should be mitigated so long as CUDA continues to thrive. The reason is because software products tend to carry much higher margins than hardware.

Is now a good time to invest in Nvidia stock?

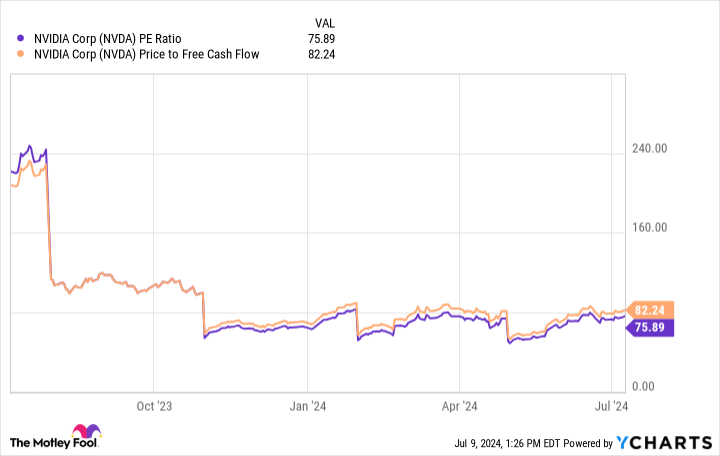

The chart below illustrates Nvidia’s price-to-earnings (P/E) and price-to-free-cash-flow (P/FCF) multiples over the last 12 months. While a P/E of 75.9 and a P/FCF of 82.2 may look pricey, there are a couple of ideas to explore here.

NVDA PE Ratio Chart

First, both Nvidia’s P/E and P/FCF multiples are lower than they were a year ago. In other words, despite the rapid ascent of the stock price, Nvidia’s earnings and cash flow are accelerating at a faster rate — therefore, Nvidia stock is technically less expensive today than it was 12 months ago.

Moreover, Nvidia’s commanding lead in the chip space and its under-the-radar software services should be analyzed further. The company is an investor in Databricks, one of the most valuable AI start-ups in the world. Nvidia is also an investor in Figure AI — a developer of humanoid robotics.

I do not think that opportunities in robotics and AI software are priced into Nvidia stock yet. I think many of these applications are currently overshadowed by the performance of the chip business, and many investors are discounting the potential Nvidia has in other areas in the AI arena.

Long-term investors have an opportunity to gain exposure to many different aspects of AI simply through Nvidia. Despite the meteoric rise in share price, the valuation analysis above, as well as some of the other growth opportunities explored make a compelling case that Nvidia stock is a good buy right now and significant upside could very much be in store.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $791,929!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel, long January 2026 $395 calls on Microsoft, short August 2024 $35 calls on Intel, and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Fool.com contributor Parkev Tatevosian compares Tesla(NASDAQ: TSLA) with Nvidia(NASDAQ: NVDA) to determine which is the better artificial intelligence (AI) stock to buy today to prepare your investment portfolio for 2024.

*Stock prices used were the afternoon prices of Dec. 21, 2023. The video was published on Dec. 23, 2023.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

Parkev Tatevosian, CFA has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia and Tesla. The Motley Fool has a disclosure policy. Parkev Tatevosian is an affiliate of The Motley Fool and may be compensated for promoting its services. If you choose to subscribe through his link, he will earn some extra money that supports his channel. His opinions remain his own and are unaffected by The Motley Fool.