[ad_1]

Many people are searching for investments that create passive income — assets that will distribute cash to them on a regular basis, hopefully in growing amounts over the years. You can achieve passive income from your stock market investments by buying shares of companies that pay dividends. The problem is, most stocks have fairly meager dividends today, or don’t pay them at all.

Illustrating that point, the average dividend yield for the stocks in the broad-market S&P 500 index is only 1.35%. If you want more passive income than that, you might be better off buying short-term U.S. Treasuries or parking cash in a high-yield savings account. To build a passive income dividend portfolio, investors need to pick individual stocks with durable and high dividend yields.

Two stocks with high dividend yields today are Altria Group (NYSE: MO) and Philip Morris International (NYSE: PM). Both are tobacco giants and, funnily enough, used to be parts of the same company back in the day. One stock yields 8.6%, while the other yields 5.2%. But which is a better passive income play now?

Altria Group: High yield from legacy tobacco

Altria Group owns Philip Morris USA, which is a leading tobacco/nicotine company in the United States. Tobacco stocks have been some of the market’s strongest performers over the last few decades due to how cash-generating the cigarette business is. The company has had to deal with declining sales volumes in the cigarette business, but it has counteracted the impact of that by steadily raising cigarette prices. Last quarter, Altria management estimated that industrywide, total estimated domestic cigarette industry volume fell by 9% year over year. But Altria’s revenues net of excise taxes only fell by 2.2% year over year.

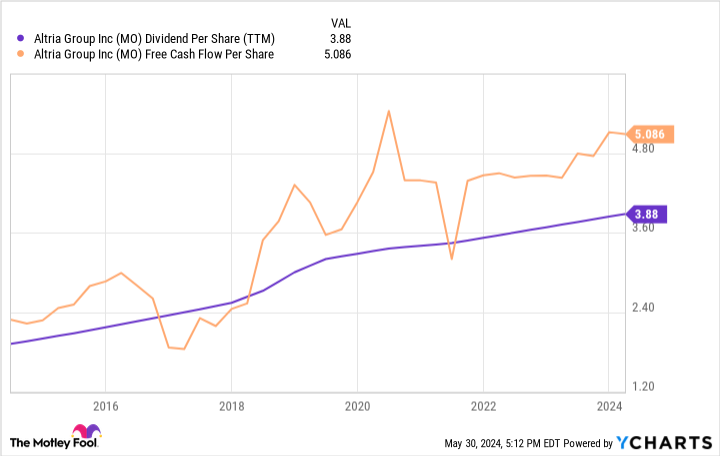

The combination of price hikes and volume declines has led to consistent earnings growth. Free cash flow per share has grown by 122% over the last 10 years. One driver of this has been Altria’s stock-buyback program, which helps juice free cash flow per share. The number of shares outstanding has fallen by 13.4% over the last 10 years, and the company has accelerated its repurchases in recent quarters.

Free cash flow is what companies prefer to tap for dividend payments, and it has fueled the growth of Altria shareholders’ payouts. Currently, its annual dividend payment is $3.88 per share, well below its trailing free cash flow of $5.09 per share. That dividend yields an appetizing 8.6% at the current share price.

Philip Morris International: Growth in new nicotine products

The international part of the Philip Morris operation is owned — unsurprisingly — by Philip Morris International. The company sells cigarettes and tobacco products essentially everywhere but the United States. However, unlike Altria Group, Philip Morris is not experiencing huge volume declines in its cigarette business. Last quarter, its combustibles sales volume only shrank by 0.4% year over year.

On top of this, Philip Morris International is the leader in new-technology nicotine products. It owns the top heat-not-burn tobacco brand, Iqos, which is growing like wildfire in Europe and Japan. In the United States, it has the Zyn nicotine pouch brand, which has grown volumes from essentially zero six years ago to 443 million cans over the last 12 months. These developments drove overall shipment volumes up 3.6% last quarter, and revenue rose by 11% due to price hikes.

The company currently pays a dividend of $5.17 per share, which is only slightly below its free cash flow of $5.76 per share. That narrow gap is something that income investors should consider. At current share prices, the stock’s dividend yields about 5.2%.

Which is the better dividend stock?

Altria and Philip Morris International both have positives and negatives for income investors. Altria has a higher yield and more room to raise its dividend, based on its free cash flow numbers. However, it is facing faster volume declines in the United States market.

Philip Morris International pays a smaller dividend and only has a little room to grow it based on its free cash flow. Despite this, I think Philip Morris International is the better stock to buy for dividend investors over the long term. Sales of new-technology nicotine products are growing quickly, and should start generating healthy amounts of cash flow for Philip Morris over the next few years. Cigarette consumption outside the United States is much more durable as well, which should allow it to achieve better revenue and earnings growth. This combination should lead to faster dividend growth for Philip Morris International over the long haul.

Altria Group should do fine for investors for the next five to 10 years. But the better passive income bet that you can “set and forget” in your portfolio is Philip Morris International.

Should you invest $1,000 in Altria Group right now?

Before you buy stock in Altria Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Altria Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $671,728!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 28, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool recommends Philip Morris International. The Motley Fool has a disclosure policy.

1 Stock Yielding 8.6% vs. 1 Stock Yielding 5.2%: Which Is Better for Passive Income Investors? was originally published by The Motley Fool

[ad_2]