BERLIN — News this month that the number of German soldiers declaring themselves conscientious objectors rose fivefold in the wake of Russia’s full-scale invasion of Ukraine created little more than a ripple in Germany.

For many Germans it’s perfectly natural for members of the Bundeswehr, the army, to renege on the pledge they made to defend their country; if Germans themselves don’t want to fight, why should their troops?

Indeed, in Germany, a soldier isn’t a soldier but a “citizen in uniform.” It’s an apposite euphemism for a populace that has lived comfortably under the U.S. security umbrella for more than seven decades and goes a long way toward explaining how Germany became NATO’s problem child since the war in Ukraine began, delaying and frustrating the Western effort to get Ukraine the weaponry it needs to defend itself against an unprovoked Russian onslaught.

The latest installment in this saga (it began just hours after the February invasion when Germany’s finance minister told Ukraine’s ambassador there was no point in sending aid because his country would only survive for a few hours anyway) concerns the question of delivering main battle tanks to Ukraine. Germany, one of the largest producers of such tanks alongside the U.S., has steadfastly refused to do so for months, arguing that providing Ukraine with Western tanks could trigger a broader war.

Chancellor Olaf Scholz has also tried to hide behind the U.S., noting that Washington has also not sent any tanks. (Scholz has conveniently ignored the detail that the U.S. has provided Ukraine with $25 billion in military aid so far, more than 10 times what Germany has.)

Germany’s allies, including Washington, often ascribe German recalcitrance to a knee-jerk pacifism born of the lessons learned from its “dark past.”

In other words, the German strategy — do nothing, blame the Nazis — is working.

Of course, Germany’s conscience doesn’t really drive its foreign policy, its corporations do. While it hangs back from supporting Ukraine in a fight to defend its democracy from invasion by a tyrant, it has no qualms about selling to authoritarian regimes, like those in the Middle East, where it does brisk business selling weapons to countries such as Egypt and Qatar.

Despite everything that’s happened over the past year, Berlin is still holding out hope that Ukraine can somehow patch things up with Russia so that Germany can resume business as usual and switch the gas back on. Even if Germany ends up sending tanks to Ukraine — as many now anticipate — it will deliver as few as it can get away with and only after exhausting every possible option to delay.

Much attention in recent years has focused on Nord Stream 2, the ill-fated Russo-German natural gas project. Yet tensions between the U.S. and Germany over the latter’s entanglement with Russian energy interests date back to the late 1950s, when it first began supplying the Soviet Union with large-diameter piping.

Throughout the Cold War, Germany’s involvement with NATO was driven by a strategy to take advantage of the protection the alliance afforded, delivering no more than the absolute minimum, while also expanding commercial relations with the Soviets.

In 1955, the weekly Die Zeit described what it called the “fireside fantasy of West German industry” to normalize trade relations with the Soviet Union. Within years, that dream became a reality, driven in large measure by Chancellor Willy Brandt’s détente policies, known as Ostpolitik.

Joe Biden, eager to reverse the diplomatic damage inflicted during the Trump years, reversed course and has gone out of his way to show his appreciation for all things German | Thomas Lohnes/Getty Images

That’s one reason the Germans so feared U.S. President Ronald Reagan and his hard line against the Soviets. Far from welcoming his “Mr. Gorbachev, tear down this wall” demand, both the German public and industry were terrified by it, worried that Reagan would upset the apple cart and destroy their business in the east.

By the time the Berlin Wall fell a couple of years later, West German exports to the Soviet Union had reached nearly 12 billion deutsche mark, a record.

That’s why Germany’s handling of Ukraine isn’t a departure from the norm; it is the norm.

Germany’s dithering over aid to Ukraine is a logical extension of a strategy that has served its economy well from the Cold War to the decision to block Ukraine’s NATO accession in 2008 to Nord Stream.

Just last week, as the Russians were raining terror on Dnipro, the minister president of Saxony, Michael Kretschmer, called for the repair of the Nord Stream 1 pipeline, which was blown up by unknown saboteurs last year, so that Germany “keeps the option” to purchase Russian gas after war ends.

One can’t blame him for trying. If one accepts that German policy is driven by economic logic rather than moral imperative, the fickleness of its political leaders makes complete sense — all the more so considering how well it has worked.

The money Germany has saved on defense has enabled it to finance one of the world’s most generous welfare states. When Germany was under pressure from allies a few years ago to finally meet NATO’s 2 percent of GDP spending target, then-Vice Chancellor Sigmar Gabriel called the goal “absurd.” And from a German perspective, he was right; why buy the cow when you can get the milk for free?

Of course, the Germans have had a lot of help milking, especially from the U.S.

American presidents have been chastising Germany over its lackluster contribution to the Western alliance going as far back as Dwight D. Eisenhower, only to do nothing about it.

The exception that proves the rule is Donald Trump, whose plan to withdraw most U.S. troops from Germany was thwarted by his election loss.

Joe Biden, eager to reverse the diplomatic damage inflicted during the Trump years, reversed course and has gone out of his way to show his appreciation for all things German.

Biden’s decision to court the Germans instead of castigating them for failing to meet their commitments taught Berlin that it merely needs to wait out crises in the transatlantic relationship and the problems will fix themselves. Under pressure from Trump to buy American liquefied natural gas, then-Chancellor Angela Merkel agreed in 2018 to support the construction of the necessary infrastructure. After Trump, those plans were put on ice, only to revive them amid the current energy crisis.

By virtue of its size and geographical position at the center of Europe, Germany will always be important for the U.S., if not as a true ally, at least as an erstwhile partner and staging ground for the American military.

Who cares that the Bundeswehr has become a punchline or that Germany remains years away from meeting its NATO spending targets?

In Washington’s view, Germany might be a bad ally, but at least it’s America’s bad ally.

And no one understands the benefits of that status better than the Germans themselves.

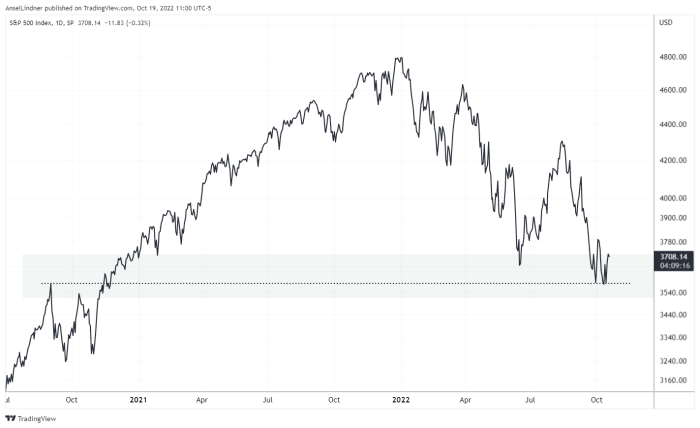

Even during a year in which the S&P 500 index declined 19%, with 72% of its stocks in the red, there were plenty of winners.

Before showing you the list of the best performers in the benchmark index, let’s look at a preview: Here’s how the 11 sectors of the S&P 500 SPX, -0.25%

performed for the year:

Index

2022 price change

Forward P/E

Forward P/E as of Dec. 31, 2021

Energy

59.0%

9.7

11.1

Utilities

-1.4%

18.9

20.4

Consumer Staples

-3.2%

21.0

21.8

Health Care

-3.6%

17.6

17.2

Industrials

-7.1%

18.3

20.8

Financials

-12.4%

11.9

14.6

Materials

-14.1%

15.8

16.6

Real Estate

-28.4%

16.5

24.2

Information Technology

-28.9%

20.1

28.1

Consumer Discretionary

-37.6%

21.3

33.2

Communication Services

-40.4%

14.3

20.8

S&P 500

-19.4%

16.8

21.4

Source: FactSet

Maybe you aren’t surprised to see that the energy sector was the only one to increase during 2022. But it might surprise you to see that despite the sector’s weighted price increase of 59%, its forward price-to-earnings ratio declined and remains very low relative to all other sectors.

It might also surprise you that West Texas Intermediate crude oil CL.1, +2.69%

gave up most of its gains from earlier in the year:

FactSet

The reason investors are still confident in energy stocks is that oil producers have remained cautious when it comes to capital spending. They don’t want to increase supply enough to cause prices to crash, as they did in the run-up to the summer of 2014, after which prices fell steadily through early 2016, causing bankruptcies and consolidation in the industry.

Now the oil companies are focusing on maintaining supply, raising dividends and buying back shares, as Occidental Petroleum Corp.’s OXY, +1.14%

chief executive explained in a recent interview with Matt Peterson. Click here for more about Occidental and the long-term supply/demand outlook for oil.

Best-performing S&P 500 stocks of 2022

Here are the 20 stocks in the benchmark index that rose most during 2022, excluding dividends. Proving that there are always exceptions, not all of them are in the energy sector.

Harris Kupperman, the president of Praetorian Capital, made a couple of interesting calls heading into 2022. He predicted that stocks of the giant tech-oriented companies that led the bull market would be sold off, and that oil prices would continue to rise through the end of 2022.

The first prediction came true, while the second one for oil prices fizzled. After rising to $130 in March, oil prices have fallen back to where they started the year. Then again, that second prediction still could have made you a lot of money because the share prices of oil companies kept rising anyway.

That leads to a new prediction for 2023 and a related stock screen below.

Here’s a chart showing the movement of front-month contract prices for West Texas Intermediate (WTI) crude oil CL.1, -0.62%

since the end of 2021:

FactSet

Even though Kupperman didn’t get his oil price call right, the energy sector of the S&P 500 SPX, -1.20%

was up 60% for 2022 through Dec. 27, excluding dividends. That is the only one of the 11 S&P 500 sectors to show a gain in 2022. And the energy sector is also cheapest relative to earnings expectations, with a forward price-to-earnings ratio of 9.8, compared with 16.7 for the full S&P 500.

WTI pulled back from its momentary peak at $130.50 in early March, but that didn’t reverse the long-term trend of low capital spending by oil and natural gas producers, which has given investors confidence that supplies will remain tight.

Vicki Hollub, the CEO of Occidental Petroleum Corp. OXY, -3.50%

— the best-performing S&P 500 stock of 2022 — said during a recent interview that there was “no pressure to increase production right now,” citing a $40 per barrel break-even point for oil prices.

At the end of November, these 20 oil companies stood out as reasonable plays for 2023 based on expectations for free-cash-flow generation and dividend payments.

For this next screen, we are only looking at ratings and consensus price targets among analysts polled by FactSet.

There are 23 energy stocks in the S&P 500, and you can invest in that group easily by purchasing shares of the Energy Select SPDR ETF XLE, -2.24%.

We can expand the list of large-cap names by looking at the components of the iShares Global Energy ETF IXC, -1.91%,

which holds all the energy stocks in the S&P 500 plus large players based outside the U.S.

Prices on the tables in this article are in local currencies.

IXC holds 51 stocks. To expand the list for a stock screen, we added the energy stocks in the S&P 400 Mid Cap Index MID, -1.24%

and the S&P Small Cap 600 Index SML, -1.89%

to bring the list up to 91 companies, which we then pared to 83 covered by at least five analysts polled by FactSet.

Here are the 20 companies in the list with at least 75% “buy” or equivalent ratings that have the most upside potential over the next 12 months, based on consensus price targets:

Following a sharp and sustained rise in interest rates, U.S. stocks have taken a broad beating this year.

But 2023 may bring very different circumstances.

Below are lists of analysts’ favorite stocks among the benchmark S&P 500 SPX,

the S&P 400 Mid Cap Index MID

and the S&P Small Cap 600 Index SML

that are expected to rise the most over the next year. Those lists are followed by a summary of opinions of all 30 stocks in the Dow Jones Industrial Average DJIA.

Stocks rallied on Dec. 13 when the November CPI report showed a much slower inflation pace than economists had expected. Investors were also anticipating the Federal Open Market Committee’s next monetary policy announcement on Dec. 14. The consensus among economists polled by FactSet is for the Federal Reserve to raise the federal funds rate by 0.50% to a target range of 4.50% to 4.75%.

A 0.50% increase would be a slowdown from the four previous increases of 0.75%. The rate began 2022 in a range of zero to 0.25%, where it had sat since March 2020.

A pivot for the Fed Reserve and the possibility that the federal funds rate will reach its “terminal” rate (the highest for this cycle) in the near term could set the stage for a broad rally for stocks in 2023.

Wall Street’s large-cap favorites

Among the S&P 500, 92 stocks are rated “buy” or the equivalent by at least 75% of analysts working for brokerage firms. That number itself is interesting — at the end of 2021, 93 of the S&P 500 had this distinction. Meanwhile, the S&P 500 has declined 16% in 2022, with all sectors down except for energy, which has risen 53%, and the utilities sector, which his risen 1% (both excluding dividends).

Here are the 20 stocks in the S&P 500 with at least 75% “buy” or equivalent ratings that analysts expect to rise the most over the next year, based on consensus price targets:

Most of the companies on the S&P 500 list expected to soar in 2023 have seen large declines in 2022. But the company at the top of the list, EQT Corp. EQT,

is an exception. The stock has risen 69% in 2022 and is expected to add another 62% over the next 12 months. Analysts expect the company’s earnings per share to double during 2023 (in part from its expected acquisition of THQ), after nearly a four-fold EPS increase in 2022.

Shares of Amazon.com Inc. AMZN

are expected to soar 50% over the next year, following a decline of 46% so far in 2022. If the shares were to rise 50% from here to the price target of $136.02, they would still be 18% below their closing price of 166.72 at the end of 2021.

You can see the earnings estimates and more for any stock in this article by clicking on its ticker.

Click here for Tomi Kilgore’s detailed guide to the wealth of information available for free on the MarketWatch quote page.

Mid-cap stocks expected to rise the most

The lists of favored stocks are limited to those covered by at least five analysts polled by FactSet.

Among components of the S&P 400 Mid Cap Index, there are 84 stocks with at least 75% “buy” ratings. Here at the 20 expected to rise the most over the next year:

Among companies in the S&P Small Cap 600 Index, 91 are rated “buy” or the equivalent by at least 75% of analysts. Here are the 20 with the highest 12-month upside potential indicated by consensus price targets:

Income-seeking investors are looking at an opportunity to scoop up shares of real estate investment trusts. Stocks in that asset class have become more attractive as prices have fallen and cash flow is improving.

Below is a broad screen of REITs that have high dividend yields and are also expected to generate enough excess cash in 2023 to enable increases in dividend payouts.

REIT prices may turn a corner in 2023

REITs distribute most of their income to shareholders to maintain their tax-advantaged status. But the group is cyclical, with pressure on share prices when interest rates rise, as they have this year at an unprecedented scale. A slowing growth rate for the group may have also placed a drag on the stocks.

And now, with talk that the Federal Reserve may begin to temper its cycle of interest-rate increases, we may be nearing the time when REIT prices rise in anticipation of an eventual decline in interest rates. The market always looks ahead, which means long-term investors who have been waiting on the sidelines to buy higher-yielding income-oriented investments may have to make a move soon.

During an interview on Nov 28, James Bullard, president of the Federal Reserve Bank of St. Louis and a member of the Federal Open Market Committee, discussed the central bank’s cycle of interest-rate increases meant to reduce inflation.

When asked about the potential timing of the Fed’s “terminal rate” (the peak federal funds rate for this cycle), Bullard said: “Generally speaking, I have advocated that sooner is better, that you do want to get to the right level of the policy rate for the current data and the current situation.”

Fed’s Bullard says in MarketWatch interview that markets are underpricing the chance of still-higher rates

In August we published this guide to investing in REITs for income. Since the data for that article was pulled on Aug. 24, the S&P 500 SPX, -0.29%

has declined 4% (despite a 10% rally from its 2022 closing low on Oct. 12), but the benchmark index’s real estate sector has declined 13%.

REITs can be placed broadly into two categories. Mortgage REITs lend money to commercial or residential borrowers and/or invest in mortgage-backed securities, while equity REITs own property and lease it out.

The pressure on share prices can be greater for mortgage REITs, because the mortgage-lending business slows as interest rates rise. In this article we are focusing on equity REITs.

Industry numbers

The National Association of Real Estate Investment Trusts (Nareit) reported that third-quarter funds from operations (FFO) for U.S.-listed equity REITs were up 14% from a year earlier. To put that number in context, the year-over-year growth rate of quarterly FFO has been slowing — it was 35% a year ago. And the third-quarter FFO increase compares to a 23% increase in earnings per share for the S&P 500 from a year earlier, according to FactSet.

The NAREIT report breaks out numbers for 12 categories of equity REITs, and there is great variance in the growth numbers, as you can see here.

FFO is a non-GAAP measure that is commonly used to gauge REITs’ capacity for paying dividends. It adds amortization and depreciation (noncash items) back to earnings, while excluding gains on the sale of property. Adjusted funds from operations (AFFO) goes further, netting out expected capital expenditures to maintain the quality of property investments.

The slowing FFO growth numbers point to the importance of looking at REITs individually, to see if expected cash flow is sufficient to cover dividend payments.

Screen of high-yielding equity REITs

For 2022 through Nov. 28, the S&P 500 has declined 17%, while the real estate sector has fallen 27%, excluding dividends.

Over the very long term, through interest-rate cycles and the liquidity-driven bull market that ended this year, equity REITs have fared well, with an average annual return of 9.3% for 20 years, compared to an average return of 9.6% for the S&P 500, both with dividends reinvested, according to FactSet.

This performance might surprise some investors, when considering the REITs’ income focus and the S&P 500’s heavy weighting for rapidly growing technology companies.

For a broad screen of equity REITs, we began with the Russell 3000 Index RUA, -0.04%,

which represents 98% of U.S. companies by market capitalization.

We then narrowed the list to 119 equity REITs that are followed by at least five analysts covered by FactSet for which AFFO estimates are available.

If we divide the expected 2023 AFFO by the current share price, we have an estimated AFFO yield, which can be compared with the current dividend yield to see if there is expected “headroom” for dividend increases.

For example, if we look at Vornado Realty Trust VNO, +1.03%,

the current dividend yield is 8.56%. Based on the consensus 2023 AFFO estimate among analysts polled by FactSet, the expected AFFO yield is only 7.25%. This doesn’t mean that Vornado will cut its dividend and it doesn’t even mean the company won’t raise its payout next year. But it might make it less likely to do so.

Among the 119 equity REITs, 104 have expected 2023 AFFO headroom of at least 1.00%.

Here are the 20 equity REITs from our screen with the highest current dividend yields that have at least 1% expected AFFO headroom:

Click on the tickers for more about each company. You should read Tomi Kilgore’s detailed guide to the wealth of information for free on the MarketWatch quote page.

The list includes each REIT’s main property investment type. However, many REITs are highly diversified. The simplified categories on the table may not cover all of their investment properties.

Knowing what a REIT invests in is part of the research you should do on your own before buying any individual stock. For arbitrary examples, some investors may wish to steer clear of exposure to certain areas of retail or hotels, or they may favor health-care properties.

Largest REITs

Several of the REITs that passed the screen have relatively small market capitalizations. You might be curious to see how the most widely held REITs fared in the screen. So here’s another list of the 20 largest U.S. REITs among the 119 that passed the first cut, sorted by market cap as of Nov. 28:

Editor’s Note: Adjoa Adjei-Twum. She is the Founder & CEO of the Africa-focused and UK-based advisory firm Emerging Business Intelligence and Innovation (EBII) Group for global investors interested in Africa and emerging markets. The opinions expressed in this article are solely hers.

CNN

—

The recently-concluded COP27 was dubbed the “African COP” – with the continent center stage in the global effort to fight the causes and effects of climate change.

As negotiations in the Egyptian resort of Sharm el-Sheikh spilled over into the weekend, there was a significant breakthrough on one of the most fractious elements – creating a fund to help the most vulnerable developing nations hit by climate disasters.

The backdrop for COP27 was a series of catastrophic global weather events including record-breaking floods in Pakistan and Nigeria, the worst droughts in four decades in the Horn of Africa, and severe European heatwaves and hurricanes in the US.

The loss and damage fund – to pay for the sudden impacts of climate change which are not avoided by mitigation and adaptation – has been a major obstacle in COP talks.

The richest, most polluting nations have been reluctant to agree to a deal, worried that it could put them on the hook for costly legal claims for climate disasters.

I welcome progress here, as African nations are bearing the brunt of climate change. The continent contributes around 3% of global greenhouse gas emissions, according to the UN Environment Programme and the International Energy Agency (IEA).

Climate change is estimated to cost the continent between $7bn and $15bn a year in lost economic output or GDP, rising to $50bn a year by 2030, according to the African Development Bank (AfDB).

But my joy is muted – the devil is in the detail, as ever. As an African diaspora entrepreneur whose work focuses significantly on the impact of climate change on the risk profile of African financial institutions and nations, I am concerned about the lack of detail about how the fund would work, when it will be implemented, and the timescale. I fear these could take years.

During a recent visit to the US, I discussed reparation money with US Democrat Congresswoman Rep. Ilhan Omar. She said it was important for the US and other countries to make heavy investments, which could come in the form of reparations.

She spoke about the importance of consulting impacted communities in Africa to avoid exploitation and the need for countries such as the US and China to end fossil fuel expansion and phase out existing oil, gas, and coal in a way that is “fair and equitable.”

Adaptation is Africa’s big challenge – the AFDB estimates that the continent needs between $1.3 to $1.6 trillion by 2030 to adapt to climate change.

The bank’s Africa Adaptation Acceleration Program, in partnership with the Global Center on Adaptation (GCA), aims to mobilize $25bn in finance for Africa, for projects such as weather forecasting apps for farmers and drought-resistant crops.

It is now time for African nations to levy a climate export tax on commodities, such as cocoa and rubber, to help pay for climate adaptation. But it still falls short of the money Africa needs.

Adaptation is all about building resilience and capacity, and I believe our governments, banks, and businesses must also adapt.

I am calling on our governments, institutions, and companies to boost efforts to attract green finance and make Africa more resilient by improving governance, tax systems, anti-corruption efforts, and legal compliance.

Sustainability is not a business tax, it is essential for business survival. Only companies focused on the changing world around us – from regulation to consumer and investor attitudes – will survive the climate crisis.

Businesses that ignore this can expect fines, boycotts, and limited access to funding. Banks will suffer too. So the financial sector must be better prepared and more agile.

This message will be reinforced when I meet CEOs, banking executives, and Nigeria’s central bank at the 13th Annual Bankers’ Committee Retreat, organized by the Nigerian Bankers Committee, in Lagos next month. The aim is to support the country’s biggest banks as they navigate new international sustainability rules.

Increasingly, investment funds must conform to green taxonomies – a system that highlights which investments are sustainable and which are not. In other words, banks will only support investments by institutions in G20 countries if they conform to national or supranational rules, such as the European Union’s Green Taxonomy.

This will not only help tackle greenwashing but also help companies and investors make more informed green choices. Additionally, G20 countries are asking their banks to forecast how risky their loans are due to climate change.

African nations must implement robust systems to mobilize private capital and foreign direct investment in key sectors. Governments must ensure they have an enabling environment for increased green investments.

Regulators must strengthen their capacity to develop and effectively enforce climate-related rules. Companies, especially banks, should strengthen climate risk management teams, regulatory compliance expertise, and preparation of bankable projects for international climate finance. This is the foundation for a successful transition to a low–carbon economy.

Looking ahead, there are other actions we can take. The African Continental Free Trade Area (AfCFTA) – the world’s largest free trade area and single market of almost 1.3bn people – could protect Africa from the adverse impacts of climate change, such as food insecurity, conflict, and economic vulnerability.

It could lead to the development of regional and continental value chains, inter-Africa trade deals, job creation, security, and peace. A single market could drive less energy-intensive economic growth while keeping emissions low, for example by developing regional energy markets and manufacturing hubs.

But we need much better pan-Africa coordination, like the European Union, to accelerate the AfCFTA. I urge our governments to work together and take swift and concrete actions to ensure the full and effective implementation of the AfCFTA. There is no time to waste.

This will not be popular with some African regimes because they will be forced to be more transparent and accountable with their public finances.

This year’s COP may have been marred by chaos, rows between rich and poorer nations, and broken multi-billion-dollar pledges by developed countries who created the climate crisis.

Many observers point out the final deal did not include commitments to phase down or reduce the use of fossil fuels.

But, the deal to create a pooled fund for countries most affected by climate change is significant, and as UN secretary general António Guterres warned, it was no time for finger-pointing.

It is also no time for the blame game. It is a wake-up call for African governments, banks, institutions, and companies to unite, step up, and adapt to a new climate reality.

The EU is under immense pressure to cap the price of imported natural gas to contain energy costs — but many of the companies making a fortune selling cheap U.S. gas to the Continent at eye-watering markups are European.

The liquefied natural gas (LNG) loaded on to tankers at U.S. ports costs nearly four times more on the other side of the Atlantic, largely due to the market disruption caused by a near-total loss of Russian deliveries following the invasion of Ukraine.

The European Commission has come under fierce pressure to sketch out a gas price cap plan, but some countries, led by Germany, worry such a measure could prompt shippers to send gas cargoes elsewhere. The Commission is also reluctant, and its proposal issued Tuesday sets such demanding requirements that they weren’t met even during this summer’s price emergency.

But a large part of the trade is in European hands, according to America’s biggest LNG exporter.

“Ninety percent of everything we produce is sold to third parties, and most of our customers are utilities — the Enels, the Endesas, the Naturgys, the Centricas and the Engies of the world,” said Corey Grindal, executive vice president for worldwide trading at Cheniere Energy, rattling off the names of big-name European energy providers.

Cheniere, which this year saw 70 percent of its exported LNG sail to Europe, sells its gas on a fix-priced scheme based on the American benchmark price, dubbed Henry Hub, which is currently at about $6 per million British thermal units.

On average, the price across all Cheniere contracts is 115 percent of Henry Hub plus $3, Grindal said. That works out to about €33 per megawatt-hour. For comparison, the current EU benchmark rate, dubbed TTF, is €119 per MWh.

It’s a big markup for whoever is reselling those LNG cargoes into Europe’s wholesale market, profiting from fears that there may not be enough gas to last the winter.

Despite fears that any EU cap will send gas to higher bidders in Asia and result in bloc-wide shortages, Grindal gave a resounding “no” when asked if a cap would have any impact on how Cheniere does business with European companies.

“Our balance sheet is underpinned by those long-term contracts,” he added.

Translation: If buyers choose to trade their precious cargoes away for higher profits beyond Europe once they receive them, that’s their decision.

Blame game

“The United States is a producer of cheap gas that they are selling us at a high price … I don’t think that’s friendly,” said French President Emmanuel Macron | Ludovic Marin/AFP via Getty Images

The difference between U.S. and EU gas prices hasn’t gone unnoticed by European politicians — but most of the finger-pointing has been at American producers rather than the resellers closer to home.

“In today’s geopolitical context, among countries that support Ukraine there are two categories being created in the gas market: those who are paying dearly and those who are selling at very high prices,” French President Emmanuel Macron told a group of industrial players last week. “The United States is a producer of cheap gas that they are selling us at a high price … I don’t think that’s friendly.”

Macron’s dig conveniently ignored that the largest European holder of long-term U.S. gas contracts is none other than France’s own TotalEnergies.

At the company’s latest earnings call last month, TotalEnergies CFO Jean-Pierre Sbraire trumpeted the fact that the firm’s access to more than 10 million tons of U.S. LNG annually “is a huge advantage for our traders, who can arbitrage between the U.S. and Europe.”

“And now, given the price of LNG, each cargo represents something like $80 million, even $100 million. So, when we are able reroute or to arbitrage between the different markets, of course, it’s a very efficient way to maximize the value coming from that business,” Sbaire added. “Cash flow generation of this order of magnitude marks the start of a new era for the company.”

Spain’s Naturgy — which has some 5 million tons of U.S. LNG a year from Cheniere under contract — has also earned nearly five times more trading gas so far this year compared with 2021 thanks to “the increased spread between [Henry Hub] and TTF,” it wrote in its half-year report.

Long-term contracts with the U.S. weren’t always so profitable. In fact, from 2016 to at least 2018, buyers were mostly losing money on the fixed deals, leading some to sell them off.

In 2019 Spain’s Iberdrola, for example, pawned off its 20-year Cheniere contract to Asian trader Pavilion Energy, which is now benefiting from selling into a high-priced global market.

In the U.K, Centrica tried — and failed — to sell off its LNG portfolio in 2020 when government-ordered lockdowns drove real-time prices through the floor. That included a 20-year fixed Cheniere contract set to run through 2038.

Now that real-time prices have shot back up, Centrica — part of Shell-owned British Gas — is reaping the rewards and eagerly snapping up more long-term contracts, most recently a 15-year deal with U.S. LNG exporter Delfin beginning in 2026.

“This is a really important profit stream for us,” Centrica CFO Chris O’Shea told investors on a Friday trading update call.

Unlike some producers — for example in the Middle East — which restrict the final destination of the LNG to consumers in Asia and prevent it being sold onward at a higher price, American gas changes ownership the minute it’s loaded onto a ship and comes with no strings attached.

That leaves buyers free to redirect the precious supply wherever it’s most profitable — sometimes at the expense of their downstream clients, if it’s cheaper to break those pre-existing domestic delivery commitments.

“We can only control what we can control,” said Cheniere’s Grindal. “U.S. LNG is destination-free.”

But as far as getting it on the ship at previously agreed prices, “our focus is being that reliable supplier, being committed to the obligations that we’ve made to our customers, and we’re committed to doing everything that we can to help the EU in this situation.”

More than 1 million barrels a day of Russian oil exports are set to be upended by Western sanctions expected to come into force within weeks, shipments Moscow will struggle to redirect elsewhere which threatens to further tighten global energy markets, the International Energy Agency said Tuesday.

Russian crude oil exports, including to the European Union, were largely unchanged last month, despite the prospect of an imminent EU ban on Russian crude oil imports and a separate plan to cap prices for Russian crude oil sales, the Paris-based agency said in a monthly report.

Russian exports to the EU were 1.5 million barrels a day in October, of which 1.1 million barrels a day will be halted when the bloc’s ban comes into effect on December 5, the IEA said.

It was unclear how much of those supplies Russia would be able to redirect to customers elsewhere in the world, the IEA said. India, China and Turkey have snapped up discounted Russian crude shipments, but buying from those nations has stabilized in recent months, the IEA said. Meanwhile, the volume would be too large for the remaining nations to absorb, the agency said.

The warning comes as the IEA predicted additional demand this year and next would come from China as the nation slowly eases its Covid-19 lockdown measures–though global demand growth will be sluggish as economies are expected to struggle.

The agency upped its 2022 global oil demand forecasts by 170,000 barrels a day to 99.8 million barrels a day. For 2023, the IEA raised its oil demand forecasts by 130,000 barrels a day to 101.4 million barrels a day.

Russia’s declining oil output will drag on global supplies which will grow at an anemic rate next year, failing to keep pace with growing oil demand. The IEA said global oil supplies would rise to 100.7 million barrels a day in 2023, 100,000 barrels a day more than it was forecasting last month, but still 700,000 barrels a day short of the world’s expected appetite for oil CL.1, -0.85%

Iran is preparing to hand the Kremlin the blueprints for its most effective weapon against the West: the underground financial network it relies on to evade sanctions.

For years, the Islamic Republic has frustrated American efforts to isolate it and starve its economy by constructing a parallel universe of front companies and foreign banks — including major financial institutions based in Europe and the U.S. — that Iranian companies use to evade international controls and conduct business abroad.

As Russia faces increasing international isolation over the war in Ukraine, Iran, which is already providing Moscow with weapons, has offered to share its expertise in the art of sanctions evasion, Western diplomats say. A series of recent meetings between senior Russian and Iranian officials, including Iranian central bank chief Ali Salehabadi and Deputy Economy Minister Ali Fekri, involved laying the groundwork for that collaboration, the diplomats argue.

If Moscow manages to copy the Iranian system it could hope to blunt the impact of many of the sanctions it faces, especially in its oil and gas sector, which forms the backbone of its economy. Such a system would give Russian President Vladimir Putin much more flexibility — and time — to continue to wage his war against Ukraine by keeping oil revenue flowing.

“Anyone interested in changing the Russian state of mind should understand that paralyzing the Russian-Iranian financial abilities is essential,” one of the Western officials said.

The diplomats who issued the warning on sanctions evasion techniques also noted that Western banks, such as Germany’s Commerzbank and Deutsche Bank, as well as Citigroup in the U.S., played a role in helping Iran continue to rake in export earnings through underground transactions. The risk is that the same Western banks — either wittingly or unwittingly — could be sucked into the same style of trade by Russia.

Trans-Caspian comrades

Over the summer, Tehran and Moscow held talks about using Iran as a backdoor for Russian oil once Tehran and world powers went back to a nuclear deal, under which the Islamic Republic would rein in its atomic program in return for sanctions relief. But amid the Iranian regime’s brutal crackdown on protestors in recent weeks and growing skepticism about renewing the accord in Washington, the likelihood of a breakthrough has faded.

Relations between Russia and Iran, which collaborated in Syria to support the regime of Bashar al-Assad in that country’s civil war, have intensified on other fronts, however. Iran has become a major supplier of the “kamikaze” drones Russia is using in Ukraine, for example. Meanwhile, Tehran asked the Kremlin for help in advancing its nuclear program, CNN reported last week, citing U.S. intelligence.

Iran has decades of experience in finding ways to avoid American sanctions but made particular strides since 2018 after U.S. President Donald Trump withdrew from the nuclear deal and reimposed restrictions. Trump argued that the arrangement with Iran was insufficient to prevent Tehran from building a bomb. European countries, led by Germany and France, objected to the U.S. decision but were powerless to stop it.

Even before Trump’s move, however, European banks and companies had been reluctant to reengage with Iran because many U.S. sanctions remained in place and most firms assessed the risk of U.S. legal exposure as too high.

Iran’s remedy was to go underground.

A cache of recent transaction data reviewed by POLITICO between Iranian clearing houses and foreign-registered front companies controlled by the regime suggests that the volume of sanctions-evading transactions handled by the network is at least in the tens of billions of dollars annually. The data, authenticated by Western officials, underscores the degree to which Iran succeeded in circumventing the so-called “maximum pressure campaign” Washington initiated in 2018.

Iran resisted re-entering the nuclear deal with the Wset despite significant concessions by the administration of U.S. President Joe Biden | Atta Kenare/AFP via Getty Images

“This explains how Iran won the maximum pressure campaign,” one of the Western officials said.

It might also explain why Iran, despite significant concessions by the administration of U.S. President Joe Biden, resisted re-entering the nuclear deal. The talks reached a stalemate even before the recent surge in protests in Iran.

While American sanctions have taken a toll on Iran’s economic output, Tehran’s shadow financial network has ensured the economy continues to fire, if not on all cylinders, then at a pace that keeps it moving, while also securing the elite’s privileges. Though inflation and unemployment in Iran are high — factors that have contributed to unrest — its economy has recently shown signs of life, growing by more than 4 percent in the last fiscal year alone, according to the World Bank.

While Iran’s oil exports have roughly halved under the sanctions to about 1 million barrels per day, it has succeeded in maintaining robust trade in other areas, such as petrochemicals and metals. At about $100 billion last year, Iran’s foreign trade reached its highest level since the U.S. reimposed sanctions. Despite the drop in oil volumes, the country has recently benefited from rising prices, with export revenue last year more than doubling to about $19 billion. What’s driving Iran’s oil recovery, according to the World Bank, are “indirect exports to China.”

Iranian oil is attractive to China, mainly because it’s relatively cheap. The illicit nature of sanctioned Iranian crude means it sells at a steep discount to market prices.

Financial frontmen

That’s where Iran’s secret network of front companies comes in.

The oil itself is fairly easy to deliver under the radar by using ship-to-ship transfers in open water and then blending it in foreign ports with other crude to disguise its origin. The greater difficulty for Iran is getting paid for the sales without triggering red flags in the international financial system, which from a regulatory perspective is dominated by the United States. Instead of selling the oil directly to the end buyer, it is sold via front companies, often to other front companies.

Just last week, the U.S. sanctioned the members of what it described as an Iranian-backed oil smuggling ring that Washington accused of funneling money to Hezbollah, the Lebanese-based terror group supported by Tehran.

“The individuals running this illicit network use a web of shell companies and fraudulent tactics including document falsification to obfuscate the origins of Iranian oil, sell it on the international market, and evade sanctions,” Brian Nelson, a senior official at the U.S. Treasury involved in the investigation, said in a statement announcing the new sanctions.

The ability to quietly finance terror is only one of the myriad benefits Iran draws from its underground financial system, however. The biggest advantage is that it gives the country’s battered economy access to hard foreign currency without a single dollar entering Iran’s own banking system. Though most of the funds generated through the network remain abroad, local companies can use the revenue they generate there as collateral at home.

Iran’s surreptitious financial system is built on what are known in the country as “money exchange houses.” The organizations, which number in the dozens, are Iran-based clearinghouses that operate a network of front companies abroad, typically registered in China, UAE and Turkey. The houses are under the close supervision of the regime.

If an Iranian firm needs to undertake a foreign transaction prohibited by sanctions, its local bank can turn to one of the houses to filter the payment through a labyrinth of front companies, making it extremely difficult to trace the true origin, Western diplomats say.

Sanctions smokescreen

A less-known aspect of this underground trade is the central role played by major Western banks. Many of the transactions, which involve everything from oil to scrap metal, are denominated in either euros or dollars. That means that settlement, the final step in the transaction, requires the involvement of a European or U.S. bank, depending on the currency.

According to Iranian exchange house data reviewed by POLITICO, major EU-based banks, such as Germany’s Commerzbank and Deutsche Bank as well as U.S. banks, including Citigroup, have been used by Iran to settle these transactions. Under U.S. sanctions rules, domestic banks and foreign banks that do business in the U.S. are prohibited from conducting almost all financial dealings that involve Iran.

The diplomats said the exchange data showed illicit Iranian export earnings being swilled through the international banking system, but there is no evidence the banks were aware that those transactions were part of Tehran’s scheme to keep the oil income flowing. If the front companies named in the transactions haven’t been specifically designated by the U.S. government, the banks often fail to detect the suspect activity.

Although banks have stringent due diligence requirements to trace the origins of funds, the Iranians have become masters at hiding where cash comes from. Nothing on the clearing data reveals an Iran connection. The transactions in question often involve the same group of companies and banks, based in China, Turkey the UAE, Singapore and India, and range in value from a few thousand dollars to millions.

The lion’s share of transactions passes through the United Arab Emirates, the diplomats said. The UAE’s proximity to Iran and light-touch regulatory environment make it an attractive place for Tehran to conduct business, they said. Those same attributes have also put the country in the sights of European officials. In the coming days, the European Commission is expected to place the UAE on its list of “high-risk” countries concerning money laundering and the financing of terrorism

One of the companies that appears frequently in the transaction records is Hong Kong-registered Hua Gong HK Trading Ltd. It was founded in October of 2018, shortly after the U.S. began to reintroduce sanctions against Iran. Western diplomats say the firm is a front company operated by Tahayyori Guarantee Society, one of Iran’s biggest exchange houses.

Deutsche Bank adopted a policy 15 years ago to reject “any business with parties in Iran” | Armando Babani/AFP via Getty Images

Hua Gong transactions over the past year reviewed by POLITICO passed through both Deutsche Bank and Citibank via Chinese banks. The recipients of the funds it transferred included firms in Hong Kong, Italy and Singapore.

POLITICO was unable to reach Hua Gong for comment.

POLITICO also contacted the Western banks and asked about the Iranian exchange house data. The European banks in question declined to comment on whether they were aware that Iranian entities were behind the transactions highlighted.

“Commerzbank AG takes its obligations and responsibilities under applicable sanctions laws and regulations seriously,” the Frankfurt-based lender said in a statement. “The bank has implemented measures in line with industry standards to ensure that its activities are conducted in compliance with applicable sanctions, including those implemented by the U.N., EU, U.S. and U.K.”

Deutsche Bank adopted a policy 15 years ago to reject “any business with parties in Iran,” a spokesman said, adding that the bank also applies “strict controls globally to prevent and detect evasion of sanctions, wherever possible.”

A spokesman for Citigroup said the New York-based bank “takes financial crimes compliance very seriously, diligently monitoring and adhering to guidance from relevant governments and other verified sources to assist in protecting the international financial system from abuse by illegitimate front companies or other illicit actors.”

Hard to police

Yet executives close to the banks say privately that policing is easier said than done. The banks have invested billions in sophisticated computer systems to root out suspect transactions and have hired armies of financial crimes specialists. Still, the Iranians are often one step ahead of them.

“It’s difficult to know when we’re being abused,” an executive at one of the banks acknowledged. “The people that do this professionally know the jurisdictions that don’t cooperate with U.S. authorities, so there’s regulatory arbitrage here as well.”

It’s not clear to what degree the specific transactions reviewed by POLITICO may have breached American sanctions.

A spokeswoman for the U.S. Treasury did not comment on the specific banks cited by POLITICO, but said that the authority has a long record of closely monitoring compliance with American sanctions against Iran and Russia and would continue to do so, including where it concerns financial institutions.

“Treasury will continue to target these sanctions evasion efforts to hide and move money through the international financial system, and financial institutions should continue to be vigilant against such schemes,” she said.

Violating U.S. sanctions has been extremely costly for European banks in the past. In 2014, for example, France’s BNP was fined $8.9 billion for running afoul of American sanctions against Iran and other countries.

The EU lifted most financial sanctions against Iran as part of the 2015 nuclear deal, which European powers continue to observe. Nonetheless, for the most part, European banks have steered clear for fear of exposure to U.S. sanctions.

While national regulators in Europe are responsible for overseeing their banks, it’s up to the European Central Bank as steward of the common currency to police euro-denominated transactions that run through its settlement system, known as TARGET2.

Critics accuse the central bank of turning a blind eye to abuse of its settlement system. Asked by POLITICO how the ECB policed its settlement network and if the bank was aware of illicit activity involving Iranian front companies and eurozone banks, a spokesman said: “The ECB enforces EU sanctions, and not sanctions imposed by non-EU jurisdictions. As regards EU sanctions, the ECB ensures that TARGET2 does not settle transactions that fall under the sanctions.”

Yet even if undertaking financial transactions with Iranian interests isn’t a violation of EU sanctions, European regulations aimed at combating money laundering require banks to conduct thorough checks into the identity of their customers, a standard called “know your customer.” The EU’s deficiencies in that regard have been apparent for years. In September, the European Banking Authority, which coordinates regulation in the sector, said that officials across the region “need to do more” to combat illicit activity in Europe’s financial system.

Until that happens, Western diplomats say, Iran will continue to use Europe’s financial infrastructure without fear of detection, an example they say Russia is bound to follow.

“This is not a loophole in the wall,” one of the officials said. “There is no wall.”

This article is part of POLITICO Pro

The one-stop-shop solution for policy professionals fusing the depth of POLITICO journalism with the power of technology

A Bahraini man examines a natural gas pipe in Manama, Bahrain on November 3, 2002 (Photo: Joe … [+] Raedle/Getty Images)

Getty Images

The small Gulf country of Bahrain said it had made two natural gas discoveries, but it is not yet clear how large they are or whether they are commercially viable.

Sheikh Nasser bin Hamad Al-Khalifa, chairman of the country’s main energy company Nogaholding, gave a briefing about the finds to his father King Hamad bin Isa Al-Khalifa in a meeting at Sakhir Palace on November 8.

The two unconventional gas reservoirs, Al-Juba and Al-Jawf, are located under the existing onshore gas-producing fields of Al-Khuf and Al-Onaiza.

The official Bahrain News Agencysaid initial evaluations of the discoveries were “encouraging in terms of quantity and production opportunities” and cited Sheikh Nasser describing them as “significant”. However, the authorities have not yet given any indication of the size of the discoveries or how quickly they might be brought online.

The authorities will be hoping the latest finds will be easier to exploit than the offshore Khaleej Al-Bahrain field discovered in 2018. That holds an estimated 80 billion barrels of shale oil and 20 trillion cubic feet of gas, but the cost and complexity of trying to extract them has meant no decision has yet been made on whether to start production.

Natural gas is seen by many as a viable ‘transition fuel’ to help wean the global economy off hydrocarbons and move to cleaner, greener fuels. However, countries may find that, unless they move quickly, some resources could become stranded as pressure grows to reduce carbon emissions.

U.S. special presidential envoy for climate John Kerry recently told a meeting at the Chatham House think-tank in London recent that countries would have to find a way to capture carbon emissions from gas projects in the longer-term.

“Gas is going to be part of the transition,” he said, but added “You can’t pretend that building out 30- to 40-year infrastructure to have a major gas facility is somehow going to be ok, unless you can capture the emissions.”

US Special Presidential Envoy for Climate John Kerry, speaking at the Chatham House think-tank in … [+] London, UK on October 27, 2022

Dominic Dudley

Bahrain’s Crown Prince Salman Bin Hamad (another son of King Hamad) has been in the Egyptian resort town of Sharm El-Sheikh for the UN climate change summit COP27 in recent days, where he talked about Bahrain’s commitment to global initiatives to mitigate climate change.

Bahrain has set itself a target of achieving carbon neutrality by 2060. As part of that it is also seeking to develop a new national energy strategy and recently appointed Boston Consulting Group to work on the plans.

Vicki Hollub’s Occidental Petroleum controls the biggest piece of the most important area for oil production in the United States. Not so long ago, an oilman in a position like that—and it would’ve been a man, before Hollub came along—would have gone for broke, turning up production to its physical limits.

Not Hollub. Occidental produces on average the equivalent of about 1.15 million barrels of oil a day, and that’s more than enough to turn a profit. The company can make money as long as oil prices are above $40 a barrel. They’ve been above $80 for almost all of this year, as the war in Ukraine takes a toll on global markets and the Saudi-led oil cartel OPEC now slashes production.

“We don’t feel like we’re in a national crisis right now,” Hollub told MarketWatch in an interview. And that means Hollub can keep executing on her plans: making shareholders happy by paying down debt and buying back shares. “When you have such a low break-even, to me there’s no pressure to increase production right now, when we have these other two ways that we can increase shareholder value,” Hollub said.

That market-focused logic puts her at odds with President Biden, who is acting like there is a national energy crisis ongoingprecisely because of what oil CEOs like Hollub are doing. The size of oil companies’ profits is outrageous, Biden said Monday. They’re raking in cash not because of innovation or investment but as a windfall from the war in Ukraine, Biden said. “Rather than increasing their investments in America or giving American consumers a break, their excess profits are going back to their shareholders and to buying back their stock, so the executive pay is — are going to skyrocket,” Biden said. He has ordered releases from the Strategic Petroleum Reserve to keep down gas prices and asked Congress to tax oil-company profits.

But Hollub is single-mindedly focused on seizing the moment to improve the company’s financial position. Occidental still has significant debt left over from a challenging acquisition Hollub spearheaded before the pandemic. In the second quarter alone, the company used its windfall to repay $4.8 billion in debt. If Biden called, she’d listen, but she hasn’t spoken to him one-on-one. Hollub said she’d spoken to the administration through Energy Secretary Jennifer Granholm. (“She doesn’t know the industry very well right now, but it’s because she hasn’t been in her job very long,” Hollub said.) The White House and the Department of Energy did not return requests for comment.

Hollub says she’s just following the market. “If demand goes down, we reduce production, if it goes up, we increase.” Oil prices have fluctuated rapidly over the year, and with a recession widely anticipated in the near future, demand could drop, Hollub said. Biden’s releases of oil from the SPR, she added, may have reduced gasoline prices, but at a cost to national security. “The SPR should be reserved for emergency situations, and you never know when those might come,” Hollub said.

Hollub’s message may not be politically convenient, but it’s exactly what her shareholders want to hear. Occidental OXY, -2.29%

is America’s hottest stock and has returned 150% this year, making it the top-performing company in the S&P 500 SPX, -0.65%.

Investors who bought shares of Occidental in January and held them through today would have more than doubled their money, even as the broader market has crashed. Warren Buffett’s Berkshire Hathaway has gone on a buying spree this year, and now owns more than 20% of Occidental’s shares. How Hollub got here constitutes America’s greatest corporate saga in recent years, from her 2019 debt-fueled decision to buy bigger rival Anadarko Petroleum over the vocal objections of activist investor Carl Icahn, to the pandemic-induced collapse in oil prices that almost bankrupted Occidental, and Buffett’s extension, removal, and re-extension of support.

With Occidental now on solid financial footing, Hollub is continuing to leave a mark on the oil industry and the world, landing her on the MarketWatch 50 list of the most influential people in markets. Hollub’s tangles with the wise men of Wall Street have left her savvier about how to manage her business. Stung by previous boom-and-bust cycles, Hollub has helped lead America’s oil frackers away from being “swing producers” that could counter the war-driven increase in energy prices, as she paid down debt and returned cash to shareholders through dividends and stock buybacks instead of plowing some of that money into shale oil fields. She is also pushing investment into Occidental’s massive new carbon-capture effort.

More than anything, Hollub is focused on guys like Bill Smead, founder of Smead Capital Management, who is a long-term investor in Occidental and a Hollub fan. “She’s somebody that we have a great deal of respect for and appreciate all the money she’s making us,” he said.

With that kind of backing, Hollub is planning to put Occidental in the driver’s seat of the massive national economic transition induced by climate change. She is positioning Occidental to be the company of the energy transition, one geared not to the free-for-all economy of the last century or some carbonless vision of the next, but the oil company for right now. She might even stop drilling new oil wells entirely.

“Now we feel like we control our own destiny,” Hollub said.

For the chief executive of a company that’s having a banner year on Wall Street while investors choke down generational losses, Hollub seems to constantly be on the alert for threats. Talking through the company’s prospects, she repeats a certain phrase: “I know that this will ultimately get me in trouble, but…”

Trouble? Hollub and Occidental have known their share.

The drama surrounding Occidental’s 2019 acquisition of Anadarko would make for a good boardroom thriller—or at least a lively business-school case study. Anadarko had big assets in the crucial Permian Basin region of Texas and New Mexico, where horizontal drilling in shale rock had reinvigorated an aging oil field into the nation’s biggest production zone.

Hollub and her team made an offer to buy Anadarko after months of research. She thought she had a deal locked, only to hear on the radio that Anadarko had announced plans to combine with Chevron. She nearly drove off the road, Texas Monthly recounts.

Hollub turned to Buffett for help. He agreed to what was effectively a $10 billion loan at 8% interest, in the form of preferred shares, along with warrants that allow Berkshire Hathaway, Buffett’s company, to buy more common stock. That got Hollub what she wanted, but many on Wall Street hated it. “The Buffett deal was like taking candy from a baby and amazingly she even thanked him publicly for it!” Icahn wrote in a letter to his fellow shareholders. Icahn had bought a slug of Occidental’s shares and, in the ensuing months, the billionaire investor led a shareholder campaign against Hollub, insisting that she needed stronger board oversight. Icahn allies were made Occidental directors.

In 2020, as COVID-19 flattened the global economy, deeply indebted Occidental was forced to cut its dividend for the first time in decades. Buffett sold his stock. At Icahn’s urging, the company issued 113 million warrants to its shareholders, allowing them to buy shares at $22, at a time when the stock was trading at $17. Gary Hu, one of the Icahn directors on Occidental’s board, pointed to those warrants as evidence of their success. “Our involvement in Occidental represented activism at its finest,” said Hu.

Hollub flatly disagrees. Icahn saw an opportunity to make an easy profit in derailing the Anadarko deal, Hollub said. “And what he expected is that we would lose and he would benefit from that. Since that didn’t happen, he managed to maneuver his way onto the board.” Icahn’s representatives on the board came to Hollub with a number of plans, including the warrants. She felt that one wouldn’t do any harm. “So that’s what we agreed to, but yeah, the other 10 or so weird things, we didn’t do.”

““She’s somebody that we have a great deal of respect for and appreciate all the money she’s making us.””

— Bill Smead, founder of Smead Capital Management

Former Occidental CEO Stephen Chazen returned to chair the board at Icahn’s insistence. Icahn and Occidental ultimately reached a settlement. His board members left, and the activist sold his common shares earlier this year. Chazen passed away in September. The experience embittered both sides, but there is one point of agreement: Hollub will do as she sees fit. “We were clearly wrong about the board’s ability to restrain Vicki’s ambitions,” Hu said.

Icahn made a $1.5 billion profit. At a MarketWatch event in September, Icahn said he still holds the warrants. But he hasn’t let go of the issues that motivated him to push into Occidental in the first place, though he insists he has no problem with Hollub personally. He likened her to a kid who got lucky gambling in Vegas. “The system allowed her to do it. And she’s just one small example of what is wrong with corporate governance.”

But as Icahn has himself shown, the system of corporate money in America is malleable. Its players can learn the rules of the game and adapt. Quarter after quarter since the dark days of the pandemic, Hollub turned up on corporate earnings calls pledging to keep cash flows strong, to invest in the highest-returning assets, and not to fall into the trap of overinvesting in debt-fueled or expensive production capacity, as so many failed shale producers have done in the past. She’s driven the company’s debt from nearly $40 billion following the Anadarko acquisition to less than $20 billion today. She increased the company’s dividend earlier this year. Along the way she transformed from market pariah to textbook CEO.

Hollub and other CEOs who run America’s biggest shale-oil producers have learned from the industry’s past mistakes. After proving a decade ago they could successfully extract shale oil, many U.S. oil producers were cheered on by growth and momentum stock investors as they borrowed billions to ramp up production, only to have those same investors abandon them after Saudi Arabia induced a plunge in oil prices. In the years that followed, U.S. shale-oil producers cultivated a new set of more value-oriented shareholders by promising they would share in profits through dividends and stock buybacks. Hollub and many of those other CEOs are not interested in chasing unrestrained growth again.

The world’s most famous value investor is now also on board. For Buffett, an earnings call Hollub led in February was the turning point. “I read every word, and said this is exactly what I would be doing. She’s running the company the right way,” Buffett told CNBC. Berkshire Hathaway BRK.A, +0.15%

started buying Occidental stock soon after. In August, federal regulators gave Buffett’s company permission to buy up to half of the company. (Asked for comment, a representative of Berkshire Hathaway asked for questions by email but did not respond to them.)

The markets are rife with speculation that Buffett will go all the way and purchase the entire company, though neither Hollub nor Berkshire have said as much. Hollub said simply that Buffett is bullish on oil, so she expects him to invest for the long haul. A Buffett buyout wouldn’t necessarily be a win for the investors who’ve hung on as Occidental’s stock price has recovered. “I’d probably make more money if he doesn’t buy it,” said Smead.

Warren Buffett is back to betting on Hollub and bought 20% of Occidental’s stock this year.

Johannes Eisele/Agence France-Presse/Getty Images

Where Hollub might cause real trouble is in the fight to keep carbon dioxide out of the earth’s atmosphere. That’s not because she’s a climate-denier. Far from it. Like many of her fellow oil-and-gas CEOs in recent years, Hollub has come to see climate change not as a threat to the business, but as an opportunity to be managed.

“I know some people don’t want oil to be produced for very long, but it’s going to be,” Hollub said. For that to change, people have to start using less oil. “It’s not that the more supply we generate, then the more that people are gonna use. It’s all driven by demand,” she said. And even with an electric vehicle in every driveway, we’d still need to extract oil to produce plastics and to create airplane fuel, among other projects that fall under the category of hard-to-abate emissions.

Hollub’s plan for Occidental is to wrap the company around that lingering stream of demand for hydrocarbons. She says Occidental is now in the business of carbon management, a euphemism that glides over the messiness of the climate transition and companies’ role in it. Companies need to show anxious shareholders that they’re serious about reducing their carbon emissions, but they also need to keep operating in an economy that is still seriously short on meaningful alternatives to fossil fuels. Occidental is here to help, spurred along by a series of state and federal incentives that the company lobbied for over years, culminating in the passage this year of the Inflation Reduction Act.

Climate advocates have for years tried to make the use of fossil fuels reflect their full cost on the environment. That has put them deeply at odds with oil-and-gas executives like Hollub, who opposes carbon taxes. It’s also left U.S. climate policy stalled as the planet warms. But the IRA tries something else. “I do not see the IRA as a handout to the energy industry,” said Sasha Mackler, executive director of the energy program at the Bipartisan Policy Center, a D.C. think tank. Rather than making dirty energy more expensive, the IRA tries to make clean energy cheaper, Mackler said. And that’s something Hollub can get on board with. She’s selling the idea that a barrel of oil can be clean.

Getting to a net-zero barrel of oil, as Hollub calls it, involves literally rerouting the route carbon dioxide takes through the world. For companies like Occidental, CO2 isn’t just a planet-destroying waste product. It’s a critical input to the process of oil production. Engineers can use CO2 to essentially juice aging oil wells by pumping it underground to displace hydrocarbons. The process is called enhanced oil recovery, or EOR. Occidental is the industry leader, producing the equivalent of 130,000 barrels per day of EOR oil and gas as of 2020. And that oil can, in theory, be less impactful on the climate. “We have it documented that it takes more CO2 injected into the reservoir than what the incremental barrels from that CO2 that are produced will emit when they’re used,” she said.

The trick is where that injected CO2 comes from. The Permian is crisscrossed with thousands of miles of pipelines that bring CO2 to oil fields from as far away as Colorado. At the moment, the vast majority comes from naturally occurring reservoirs or as a byproduct of the production of methane. One of the strangest ironies of modern oil production is that companies like Occidental don’t actually have enough CO2. “There’s two billion barrels of resources remaining to be developed in our conventional reservoirs using CO2,” Hollub said.

So she and her team went out looking for more. Eventually they hit on the idea that’s encapsulated in the IRA. Instead of pulling CO2 out of the ground only to put it back, Occidental could divert some of the CO2 that’s being produced by so-called industrial sources, companies that would otherwise be dumping it into the atmosphere because, of course, there’s no business reason not to.

Finding companies that wanted to do the right thing with their waste CO2 turned out to be harder than Hollub thought. “We knocked on the doors of a lot of emitters,” Hollub said. They found one taker—a Texas ethanol producer that was willing to try a pilot. It was a decent start but not enough to unlock all those buried barrels.

That may soon change, driven by the IRA. The law puts new financial incentives behind those conversations Occidental was having with CO2 emitters. The IRA significantly beefed up the so-called 45Q tax incentive for companies to put CO2 permanently in the ground. Occidental can get $60 a ton in tax credits if the CO2 is stored in the process of pumping more oil for EOR, or $85 if the company just buries it.

There’s also a higher tier of incentives if companies obtain that CO2 using an experimental technology called direct air capture. Occidental is spending $1 billion to build what would be the world’s largest direct-air-capture facility in Texas, which you can loosely think of as a giant fan to suck ambient CO2 directly out of the atmosphere. Hollub plans to build as many as 70 by 2035.

The problem some see with this plan, and with Hollub and others’ efforts to shape legislation around it, is it tightens the economy’s dependence on fossil fuels rather than loosening it. Americans will now effectively pay Occidental to pursue more enhanced oil recovery. Those net-zero barrels of oil—should they materialize—might be better in climate terms than a traditional barrel. But that’s not the only alternative. Dollar for dollar, public money would be better spent on solar energy and other low-carbon options than on EOR, said Kurt House, who knows as much because he’s tried it. House got a Ph.D. at Harvard in the science of carbon capture and storage more than a decade ago and co-founded a company to put the idea into practice. “It is bad, bad economics,” he said. “If you pay people a million dollars a ton of CO2 sequestering, they will sequester a lot of CO2. But it’ll cost us. It’ll make solving global warming much, much, much, much, much more expensive.”

But Hollub isn’t likely to change course. “I would say to those who don’t like what we’re doing, who do they want to do this? Tell me who have they gotten to, that will commit to take CO2 out of the atmosphere?” she said. “This climate transition cannot happen as fast as some people want it to happen because the world can’t afford it,” Hollub said. “We’re looking at, you know, $100 to $200 trillion for this climate transition. We cannot spend that kind of money to make this transition happen without help from diverting some of the CO2 to enhanced oil recovery, which enables then the technology to be developed and to be built at a faster pace.” And in the meantime, Occidental can sell carbon offsets to companies like United Airlines, which is supporting the direct-air-capture facility.

Those companies can choose whether they want the CO2 Occidental is capturing to be buried, full stop, or used for more oil production. But it’s clear Hollub thinks EOR is a big part of the future for Occidental. She has often said that the last barrel of oil should come from EOR. “I think there could be a world where we do stop drilling new wells,” she said. “To increase recovery from the remaining conventional reservoirs is something that’s kind of like a best kept secret for the United States. Nobody very much realizes that, but that is there. And that gives us that longevity beyond what some people are forecasting,” Hollub said.

Hollub is well-aware of her critics. Perhaps that’s why she keeps looking around for signs of trouble. But even if it finds her, she doesn’t plan to change much. “I have no regrets,” she said.

The British Navy stands accused by the Russian government, without evidence, of blowing up the Nord Stream natural gas pipeline under the Baltic Sea, a claim the U.K. rejected as “false.”

“According to available information, representatives … of the British Navy took part in the planning, provision and implementation of a terrorist attack in the Baltic Sea on September 26 this year — blowing up the Nord Stream 1 and Nord Stream 2 gas pipelines,” the Russian Defense Ministry said on Saturday, according to media reports.

The accusation did not include any further information or evidence to support claims of state sabotage. The Russian government also said that U.K. operatives helped plan a drone attack on its fleet at the Black Sea port of Sevastopol in Crimea on Saturday.

The U.K. Defense Ministry quickly denied Moscow’s claim.

“To detract from their disastrous handling of the illegal invasion of Ukraine, the Russian Ministry of Defense is resorting to peddling false claims of an epic scale,” the British ministry said in a tweet. “This invented story says more about arguments going on inside the Russian government than it does about the West.”

Russia had already blamed the West in general terms for undersea explosions that damaged the Nord Stream pipes last month. Those blasts have likely rendered the energy infrastructure unusable, according to the German government.

An investigation by Danish and Swedish authorities is ongoing into the explosions, which took place inside the two countries’ exclusive economic zones close to the Baltic Sea island of Bornholm.

Russia had already stopped gas transit through the pipeline sparking concerns earlier this year that it would use gas supply to blackmail Europe as its brutal war on Ukraine continues.

While the first phase of Nord Stream had been operating for nearly 11 years, the second phase of the project — dubbed Nord Stream 2 — had not yet been brought into commercial operation.

This photo illustration taken on March 31, 2022 in Moscow, shows gas burning on a domestic hob. – … [+] President Vladimir Putin on March 31 warned “unfriendly” countries, including all EU members, that they would be cut off from Russian gas unless they opened an account in rubles to pay for deliveries. Western countries have piled crippling sanctions on Moscow since it moved troops into Ukraine, including the freezing of its $300 billion of foreign currency reserves. While the United States banned the import of Russian oil and gas, the European Union — which received around 40 percent of its gas supplies from Russia in 2021 — has retained deliveries from Moscow. (Photo by Natalia KOLESNIKOVA / AFP) (Photo by NATALIA KOLESNIKOVA/AFP via Getty Images)

AFP via Getty Images

Britain’s new Prime Minister Rishi Sunak reinstated the country’s ban on hydraulic fracturing (a.k.a. fracking) on Wednesday. That means no UK fracking for for oil and gas.

It’s not surprising given that the vast majority of British people likely don’t know they are already consuming literal boat loads of fracked natural gas from the U.S.

Yet here we are with Britain thinking its doing the environmentally suitable thing by not fracking and at the same time benefiting from the fruits of this energy extraction technique.

Approximately two thirds of natural gas sold in the U.S. is extracted using fracking methods, according to the American Petroleum Institute. That means it is almost a certainty that two thirds of the gas Britain purchases from America is fracked, or approximately 26% of household use via electricity consumption. Stovetop gas use likely adds more.

Of course, no one blames people for wanting to keep warm in the northern hemisphere’s winter. It can be chilly to the extent that people die without heat.

However, what seems hypocritical is the willingness of Brits to use fracked gas as long as it isn’t from Britain.