Exchange-traded fund inflows have already topped monthly records in 2024, and managers think inflows could see an impact from the money market fund boom before year-end.

“With that $6 trillion plus parked in money market funds, I do think that is really the biggest wild card for the remainder of the year,” Nate Geraci, president of The ETF Store, told CNBC’s “ETF Edge” this week. “Whether it be flows into REIT ETFs or just the broader ETF market, that’s going to be a real potential catalyst here to watch.”

Total assets in money market funds set a new high of $6.24 trillion this past week, according to the Investment Company Institute. Assets have hit peak levels this year as investors wait for a Federal Reserve rate cut.

“If that yield comes down, the return on money market funds should come down as well,” said State Street Global Advisors’ Matt Bartolini in the same interview. “So as rates fall, we should expect to see some of that capital that has been on the sidelines in cash when cash was sort of cool again, start to go back into the marketplace.”

Bartolini, the firm’s head of SPDR Americas Research, sees that money moving into stocks, other higher-yielding areas of the fixed income marketplace and parts of the ETF market.

“I think one of the areas that I think is probably going to pick up a little bit more is around gold ETFs,” Bartolini added. “They’ve had about 2.2 billion of inflows the last three months, really strong close last year. So I think the future is still bright for the overall industry.”

Meanwhile, Geraci expects large, megacap ETFs to benefit. He also thinks the transition could be promising for ETF inflow levels as they approach 2021 records of $909 billion.

“Assuming stocks don’t experience a massive pullback, I think investors will continue to allocate here, and ETF inflows can break that record,” he said.

The notion that the Federal Reserve will soon slow, or perhaps even end, its program of quantitative tightening is increasingly being talked about on Wall Street like a foregone conclusion.

But while investors wait to hear more on the subject from Fed Chair Jerome Powell during next week’s post-meeting press conference, they could be forgiven for asking themselves some questions.

What might an imminent taper of the Fed’s balance-sheet runoff look like? Why has it suddenly become so urgent? What might it mean for the six or so interest-rate cuts investors are expecting from the Fed this year, as well as for markets more broadly?

We aim to answer these questions below.

What inspired talk of tapering QT?

It wasn’t until the minutes from the Federal Reserve’s December policy meeting were published earlier this month that investors started to take the notion of the Fed declaring “mission accomplished” on QT seriously.

The minutes revealed that a number of senior Fed officials felt it was nearly time to “begin to discuss” the technical factors that would govern the Fed’s decision to slow the runoff of maturing bonds from its balance sheet.

Shortly after the minutes’ release, several senior Fed officials came forward to discuss the importance of ending the balance-sheet runoff. Dallas Fed President Lorie Logan, the first senior Fed official to expand on what was noted in the minutes, said earlier this month that the Fed should start to slow the pace of its balance-sheet shrinkage once assets locked up in the Fed’s reverse-repo facility fell below a certain level.

According to Logan, senior Fed officials had been unsettled by the drain of $2 trillion in assets from the RRP facility last year.

But there was another issue that was also likely bothering monetary policymakers heading into the Fed’s December meeting.

Sudden spikes in overnight repo rates late last year drew uncomfortable comparisons to the repo-market crisis of September 2019, which foreshadowed the end of the Fed’s previous attempt at tapering its balance sheet, according to TS Lombard’s Steve Blitz.

What is the Fed’s ‘lowest comfortable level of reserves’?

A re-run of the repo-market crisis of 2019 is what the Fed is presumably trying to avoid. Economists are so concerned the central bank might accidentally bump up against the lower bound for reserves in the banking system, that they have come up with a name for the concept: They’re calling it the “lowest comfortable level of reserves.”

According to this idea, strain in overnight-financing markets should emerge once reserves in the banking system retreat below a certain threshold. This would, in turn, likely force the central bank to scale back or even reverse quantitative tightening immediately, according to several economists.

In order to avoid such a risk, Jefferies economist Thomas Simons said in a note to clients earlier this month that he expects the Fed will announce plans to start tapering QT after its March meeting.

Across Wall Street, most economists expect the Fed will begin by tapering the pace at which Treasurys are redeemed from its balance sheet — perhaps cutting it in half to start, from $60 billion a month to $30 billion a month. Reducing the pace at which mortgage-backed securities are running off won’t matter as much until prepayments begin to climb.

Going even further, economists at Evercore ISI said in a report shared with MarketWatch earlier this week that they expect the tapering to begin around the middle of 2024 and continue potentially through 2025, until the Fed has succeeded in reducing the size of its balance sheet to about $7 trillion.

The balance sheet presently stands at $7.7 trillion, according to data published by the Fed. It peaked at nearly $9 trillion in April 2022.

However, one key issue may complicate the Fed’s efforts to ascertain the “LCLoR.” According to Jefferies’ Simons, the amount of banking-system reserves counted as liabilities on the Fed’s balance sheet has been more or less steady since the Fed started its latest round of balance-sheet tapering. It stood at roughly $3.3 trillion recently, according to Fed data cited by Jefferies.

Why stop at $7 trillion if bank reserves haven’t been all that heavily impacted by QT anyway? It’s probably worth noting that, whatever happens, nobody on Wall Street expects the Fed would attempt to shrink the size of its balance sheet back toward pre-crisis levels, when the amount of bonds on its balance sheet was miniscule compared to today.

Why? Because there is simply too much debt sloshing around the global financial system to justify such a withdrawal of support, according to Steven Ricchiuto, chief economist at Mizuho Americas.

“The Fed is not in a position to remove all that extra liquidity because now the system needs it just to function,” Ricchiuto said.

What does this mean for markets?

Because quantitative tightening is a hawkish policy stance, its rolling back should be bullish for stocks and bonds. But there are other considerations that could impact the outcome, market strategists said.

Not only would a reduction in the pace of the Fed’s monthly runoff introduce a fresh dovish tilt to the Fed’s monetary policy, but by reducing the amount of bonds it allows to roll off its balance sheet every month, the Fed would become more active in the Treasury market, said James St. Aubin, chief investment officer at Sierra Investment Management, during an interview.

There are also a few contextual factors that could impact how the equity market reacts. For example, as St. Aubin pointed out, context is equally as important as the nature of the decision itself. Should the Fed decide to end QT abruptly because the U.S. economy is sliding into a recession, then the decision could hurt stocks.

Another issue, raised by a different market strategist, is the notion that the Fed could decide to start tapering QT in lieu of cutting interest rates — or at least in lieu of cutting them as quickly as investors expect. This could buy the central bank more time to press its battle against inflation while mitigating the risks that it could hurt the economy by keeping policy uncomfortably tight for too long, economists said.

Ben Jeffery, U.S. interest-rate strategist at BMO, said in a recent note to clients that, based on Logan’s comments from earlier this month, he would lean toward this being the most likely scenario. Additionally, he said, tapering QT could potentially impact the Treasury’s refunding announcement due in May.

Jeffery calculated that the Fed tapering QT by $20 billion beginning in April would save the Treasury from issuing nearly $250 billion in bonds compared to if the Fed had continued with its balance-sheet runoff apace.

This should lead to lower Treasury yields, all else being equal. And lower long-dated Treasury yields are typically seen as beneficial for stocks, according to Callie Cox, a U.S. equity strategist at eToro.

Although, once again, the outcome for markets would likely depend on the specific context.

“Higher yields probably aren’t a good thing for stock investors these days, but in particular environments, higher yields and less Fed intervention could hint that the economy is healing,” Cox said.

Treasury yields tested their highest levels in more than a dozen years on Thursday as investors continued to absorb the Federal Reserve’s message of higher-for-longer interest rates.

What’s happening

What’s driving markets

Treasury yields continued to climb on Thursday as investors continued to absorb the Federal Reserve’s projections, delivered Wednesday, that suggested another interest-rate increase this year and that borrowing costs were likely to be cut in 2024 by less than previously thought.

Neuberger Berman, an asset manager with eight decades under its belt, is on the lookout for cracks in credit markets from the Federal Reserve’s rate-hiking campaign.

Erik Knutzen, chief investment officer of multi asset, worries that several factors could be a tipping point for the economy, from an economic slowdown in China to U.S. consumers finally becoming exhausted by higher rates.

Yet Knutzen expects the high-yield, or junk bond, market to serve as the “canary in the coal mine” for broader market volatility, acting as “perhaps the most visible threat, and therefore one we think could be priced in sooner than later.”

The Bloomberg U.S. High Yield Bond Index has returned 6.4% through the end of August, producing one of the year’s highest gains in fixed income, helped along by a “resilient U.S. economy coupled with still-available financial liquidity,” according to the Wells Fargo Investment Institute.

But Knutzen worries that as the high-yield maturity wall draws closer, “the first policy rate cuts get priced further and further out, raising the threat of expensive refinancings.”

Starting next year, some $700 billion of high-yield bonds are set to mature through the end of 2027, with a big slice of the refinancing need coming from companies with riskier credit ratings below the top BB ratings bracket.

The junk-bond maturity wall.

Bloomberg, Wells Fargo Investment Institute, Moody’s Investors Service

The two big U.S. exchange-traded funds linked to junk bonds are the SPDR Bloomberg High Yield Bond ETF JNK

and the iShares iBoxx $ High Yield Corporate Bond ETF HYG,

both up 1.8% and 1.5% on the year through Monday, respectively, while offering dividend yields of more than 5.8%, according to FactSet.

Of note, fixed-income strategists at the Wells Fargo Investment Institute also said they see risks emerging in junk bonds for companies rated B and below, particularly with spread in the sector trading less than 400 basis points above the risk-free Treasury rate since July. Spreads are the premium that investors are paid on bonds to help compensate for default risks.

Top corporate executives appear hopeful that the Federal Reserve will cut rates sooner than later. Fed Chairman Jerome Powell said in Jackson Hole, Wyo., in August that the central bank is prepared to keep its policy rate restrictive for a while to get inflation down to its 2% target.

To that end, Neuberger Berman, which has roughly $443 billion in managed assets, sees several sources of volatility lurking through year’s end, and has a “defensive inclination” in equity and credit, favoring high-quality companies with plenty of free cash flow, high cash balances and less expensive long-term debt.

U.S. stocks booked gains on Monday after a week of losses, with the S&P 500 index SPX

and Nasdaq Composite Index COMP

scoring their best daily percentage gains in about two weeks. The Dow Jones Industrial Average DJIA

advanced 0.3%.

The IMF’s Managing Director Kristalina Georgieva tells CNBC’s Martin Soong that the World Bank and IMF are complementary but yet have differing expertise. “The world needs institutions to work together,” she said in an exclusive CNBC interview on the sidelines of the G20 leaders’ summit.

Another big corporate borrowing blitz to kick off September has gotten under way, but this one isn’t looking like the rest.

Instead, the flurry of new bond issues shows how the Federal Reserve’s higher interest rate environment has begun to seep in a year later, by making major companies far more hesitant to tap credit for longer stretches.

A worsening U.S. fiscal situation caught stock and bond investors off guard in the past week and now a round of approaching government auctions is about to provide a crucial test for Treasurys.

The question in the days ahead is whether risks to the demand for U.S. government debt are growing. If so, that could put upward pressure on Treasury yields, which would undermine the performance of stocks. However, if investors end up caring less about the fiscal situation than they do about the possibility of slowing economic growth and decelerating inflation, government debt’s safe-haven appeal could be reinforced, putting a limit on how high yields might go.

Concern about the deteriorating fiscal outlook was a factor behind the past week’s rise in long-term Treasury yields. Ten- BX:TMUBMUSD10Y

and 30-year yields BX:TMUBMUSD30Y

respectively jumped to 4.188% and 4.304% on Thursday, the highest levels since early November, as investors sold off long-term government debt — which took the shine off U.S. stocks. By Friday, though, a moderating pace of U.S. job creation for July sent yields into reverse, giving equities a temporary lift during the final trading session of the week.

At issue is the extent to which potential buyers of Treasurys may be deterred by Fitch Ratings’ Aug. 1 decision to cut the U.S. government’s top AAA rating, at a time when the government is about to unleash what Barclays rates strategists describe as a “tsunami” of supply. A total of $103 billion in 3-, 10-and 30-year Treasurys come up for sale between Tuesday and Thursday. In addition, a spate of Treasury bills are scheduled to be auctioned starting on Monday.

Gene Tannuzzo, global head of fixed income at Boston-based Columbia Threadneedle Investments, said that while he and his team still have room to add T-bills to the government money-market funds they oversee during the week ahead, they haven’t made up their minds about whether to buy more longer-dated maturities for their bond funds.

“While we are comfortable that the Fed is at or near the end of its rate hikes, there are a lot more questions about the durability of the economic recovery, the degree that inflation will remain low, and the risk premium that needs to be put in at the long end,” Tannuzzo said via phone.

Treasury’s $1 trillion third-quarter borrowing plans, along with some technical issues and the Bank of Japan’s decision to switch to a more flexible yield-curve control approach, might reduce demand for U.S. government debt, he said. Columbia Threadneedle managed $617 billion as of June.

“One can’t ignore the risk of an unruly rise in yields, but our view is that this is a low risk and what the Treasury auctions may produce instead is ‘indigestion,’ driven by poor technicals and low liquidity, Fitch’s downgrade, and the Bank of Japan action — and by the end of August, we should be past much of this,” he told MarketWatch.

Risks to the demand for Treasurys may become obvious soon, given Tuesday-Thursday’s $103 billion in total sales of 3-, 10- and 30-year securities, according to analyst John Canavan of U.K.-based Oxford Economics. The main “question mark” for the market’s ability to absorb the increased Treasury issuance will be whether or not domestic investment funds continue to show interest, Canavan wrote in a note distributed on Friday.

Source: Oxford Economics.

“ ‘My suspicion is that with higher rates comes equally solid demand’ at upcoming auctions.”

— John Flahive, head of fixed income at BNY Mellon Wealth Management

Market players have had little difficulty absorbing Treasury coupon issuances in recent years because of flight-to-safety trades made after the U.S. onset of the Covid-19 pandemic in 2020. Now, however, increased auction sizes are being accompanied by still-elevated inflation, better-than-expected economic growth, and the possibility of more rate hikes by the Federal Reserve — which is likely to complicate the market’s ability to absorb the increased supply “without hiccups,” Canavan said.

On the flip side of the debate is John Flahive, head of fixed income at BNY Mellon Wealth Management in Boston, which managed $286 billion in assets as of June. He said equity markets will continue to be much more focused on economic developments and earnings. And as long as the latter of the two remains robust, stocks “can grind higher in a low-volatility environment,” Flahive said via phone.

Saying he does not expect his team to be a major participant in the Treasury auctions, Flahive said that the bond market’s reaction in the past week was “a little overdone” and “we always felt that there was a limited to how much yields could go up to reflect more government debt.”

“My suspicion is that with higher rates comes equally solid demand” at upcoming auctions, he said. “I’m still optimistic about rates going back down over time as the result of a slowing economy and decelerating inflation. We continue to like the bond market and see a better-than-even chance that yields go down as the economy continues to weaken in the quarters ahead.”

Friday’s reaction to July’s official jobs report, which showed the U.S. added a modest 187,000 new jobs, provided a breather from the past week’s run-up in Treasury yields.

On Friday, the 30-year Treasury yield fell 9 basis points to 4.214%, yet still ended with its biggest weekly gain since early February. The 10-year rate, which dropped 12.8 basis points to 4.06%, finished with a third straight week of advances.

Stocks fell Friday, leaving major indexes with weekly declines. The Dow Jones Industrial Average DJIA

posted a 1.1% weekly fall, while the S&P 500 SPX

shed 2.3% and the Nasdaq Composite COMP

retreated 2.9%. The soft start to August comes after a run of sharp gains for equities. The S&P 500 remains up 16.6% for the year to date.

The economic calendar for the week ahead includes U.S. inflation updates.

On Monday, June consumer-credit data is set to be released. Tuesday brings the NFIB’s small business optimism index, plus data on the U.S. trade balance and wholesale inventories. Then on Thursday, weekly initial jobless claims and the July consumer-price index are released. That’s followed on Friday by the producer-price index for last month and an August consumer-sentiment reading.

Meanwhile, portfolio manager and fixed-income analyst John Luke Tyner at Alabama-based Aptus Capital Advisors, which manages roughly $5 billion in assets, said he plans to follow the Treasury auctions, but doesn’t usually participate in them.

“One of the biggest trends we’ve seen is the continued increase in the issuance amounts from Treasury. Whatever we are budgeting for is never enough, which justifies the Fitch downgrade,” Tyner said via phone. “It’s tough to say people aren’t going to buy U.S. debt, but you’ve got to entice them to buy duration and take the risk.

“The U.S. is not an emerging market, but ultimately we are going to see the market rate that participants require be higher, with a notable uptick in term premia,” he said. “What we could see in the face of all this issuance is a grind up in yields on an auction-by-auction basis. If I look at the technicals, a 4.9%-5% yield on the 10-year note seems in the cards,” and “it will be difficult for stocks to hold or expand from full valuations as rates run up.”

Stocks fell on Wednesday, a day after Fitch Ratings lowered its U.S. debt ratings to AA+ from the top AAA category, pointing to its growing debt burden and “erosion of governance” over the past two decades. The S&P 500 SPX, -1.38%

fell about 63 points, or 1.4%, ending near 4,513, booking its biggest daily percentage decline since April 25, according to preliminary Dow Jones Market Data. The Dow Jones Industrial Average DJIA, -0.98%

shed about 1%, while the Nasdaq Composite Index COMP, -2.17%

closed 2.2% lower. Stocks already had been taking a breather from their march toward record levels when Fitch on Tuesday evening made good on a threat to downgrade its U.S. debt rating a notch to AA+. Longer-dated Treasury yields rose Wednesday, with the 10-year Treasury rate TMUBMUSD10Y, 4.105%

touching 4.07%, according to FactSet. Treasurys and other haven assets are viewed as likely to benefit from a flight to safety in a scenario where investors get more jittery about the U.S. economic outlook.

Indonesian President Joko Widodo makes a speech during the Association of Southeast Asian Nations (ASEAN) Foreign Minister’s Meeting in Jakarta, Indonesia on July 14, 2023.

Murat Gok | Anadolu Agency | Getty Images

A new regional cross-border payment system recently implemented by Southeast Asian nations could deepen financial integration among participants, bringing the ASEAN bloc closer to its goal of economic cohesion.

The program, which allows residents to pay for goods and services in local currencies using a QR code, is now active in Indonesia, Malaysia, Thailand and Singapore. The Philippines is expected to join soon.

That’s according to each country’s respective central bank.

The move comes after the five Southeast Asian countries signed an official agreement late last year. At the recent ASEAN summit in May, leaders also reiterated their commitment to the project, pledging to work on a road map to expand regional payment links to all ten ASEAN members.

The scheme is aimed at supporting and facilitating cross-border trade settlements, investment, remittance and other economic activities with the goal of implementing an inclusive financial ecosystem around Southeast Asia.

Analysts say retail industries will particularly benefit amid an expected rise in consumer spending, which could in turn strengthen tourism.

Regional connectivity is considered crucial to reduce the region’s reliance on external currencies like the U.S. dollar for cross-border transactions, particularly among businesses. The greenback’s strength in recent years has resulted in weaker ASEAN currencies, which hurts those economies since the majority of the bloc’s members are net energy and food importers.

“The system will forgo the U.S. dollar or the Chinese renminbi as intermediary,” said Nico Han, a Southeast Asia analyst at Diplomat Risk Intelligence, the consulting and analysis division of current affairs magazine The Diplomat.

A unified cross-border digital payment system will “foster a sense of regionalism and ASEAN-centrality in managing international affairs,” he added. “This move becomes even more crucial in light of escalating tensions among major global powers.”

How it works

By connecting QR code payment systems, funds can be sent from one digital wallet to another.

These digital wallets effectively act as bank accounts but they can also be linked to accounts with formal financial institutions.

For instance, Malaysian tourists in Singapore can make a payment with Malaysian ringgit funds in their Malaysian digital wallet when making a transaction. Or, a Malaysian worker in Singapore can send Singapore dollar funds in a Singaporean digital wallet to a recipient’s wallet in Malaysia.

Fees and exchange rates will be determined by mutual agreement between the central banks themselves.

For now, a region-wide system like this doesn’t exist in other parts of the world but down the road, the Bank of International Settlements, based in Switzerland, hopes to connect retail payment systems across the world using QR codes and mobile phone numbers.

“The ASEAN central banks’ effort is innovative and novel,” said Satoru Yamadera, advisor at the Asian Development Bank’s Economic Research and Development Impact Department.

“In other regions like Europe, retail payment connection via credit and debit cards is more popular while China is well-known for advanced QR code payment, but they are not connected like the ASEAN QR codes,” he continued.

Economic benefits

QR payments don’t impose fees on cardholders and merchants. They also boast of better conversion rates than those set by private payment processors like Visa or American Express.

Micro enterprises as well as small- and medium-sized businesses, or SMBs will emerge as winners from regional payment connectivity, experts say. According to the Asian Development Bank, such companies account for over 90% of businesses in Southeast Asia.

“SMBs can avoid the expenses associated with maintaining a physical point-of-sale system or paying interchange fees to card companies,” explained Han from Diplomat Risk Intelligence.

Marginalized individuals from low-income backgrounds also stand to benefit. As the payment system works via digital wallets and doesn’t require a traditional bank account, it can be used by the unbanked population.

“The system has the potential to improve financial literacy and wellbeing for the underbanked population,” Han noted.

ASEAN’s new system will also enable merchants and consumers to build a robust payment history, and provide valuable data for credit scoring, said Nicholas Lee, lead Asia tech analyst at Global Counsel, a public policy advisory firm.

“That’s particularly advantageous for unbanked and underbanked segments of the population, who traditionally lack access to such credit assessment data.”

Moreover, “increased non-cash transactions would allow policymakers to capture transaction data and trade flow more effectively, assuming these data are accessible,” said Lee.

“This, in turn, could lead to better economic forecasting and policymaking.”

Currency pressure ahead

While strengthening payment connectivity within the region has the potential to reduce payment friction and accelerate digital transition, it could inadvertently put pressure on certain currencies, particularly the Singapore dollar.

“The potential scenario of the [Singapore dollar] emerging as a de facto reserve currency within the region poses a challenge that ASEAN states will need to confront,” said Lee.

“With the [Singapore dollar’s] strength and stability, both international and regional businesses may opt to hold more of their working capital in [Singapore dollars], relying on the new payment network for efficient currency conversion,” he explained.

If that happens, it could weaken the purchasing power of other currencies in the region and result in higher imported inflation if central banks don’t intervene.

In such a scenario, authorities may feel the need to impose capital restrictions in order to protect their respective currencies, which could undermine the very purpose of establishing a regional payment network.

Regulations pose another challenge.

Central banks will have to address security and fraud issues, plus undertake the task of educating the public to embrace the new payment system, said Han.

“These factors can collectively contribute to a time-consuming process,” he warned.

This kind of coordinated action will require strong political will from regional leaders and it remains to be seen if ASEAN members can come together to successfully implement such an ambitious venture.

Even with U.S. stocks in a new bull market, investors aren’t showing many signs of backing away from money-market funds and other cash-like investments offering yields of about 5%, the highest in about 15 years.

Money-market funds hit a record of $5.9 trillion in assets as of Tuesday, signaling a continuing drain out of bank deposits into higher-yielding “cash-like” investments, according to Peter Crane, president and publisher of Crane Data.

It is the notion that the Federal Reserve could deliver a hawkish jolt to markets even if it refrains from raising rates when its two-day policy meeting ends on Wednesday.

There are concerns that such an outcome could spark a turnaround in U.S. stocks, especially if an uncomfortably strong reading on May inflation — due this coming Tuesday just as the Fed’s policy meeting is slated to begin — pushes the central bank toward something even more extreme, like delivering a rate increase on Wednesday despite intimating that it plans to abstain.

On the other hand, signs that the economy has weakened and inflation has continued to fade would help the Fed to justify skipping a rate increase in June — as several senior officials have suggested it will — while signaling that a potential hike at its following meeting in July could be the final increase for the cycle.

“Softening U.S. data should support calls that a June skip could eventually turn into a July pause. Next week, most of the data is expected to remain weak or little changed: retail sales could be flat m/m, the Fed regional surveys should remain in negative territory, and consumer sentiment will waver,” said Craig Erlam, senior market analyst at OANDA, in emailed commentary.

Wednesday’s meeting comes at a critical time for the market. U.S. stocks have powered ahead for more than six months, with the S&P 500 SPX, +0.11%

having risen more than 20% off its Oct. 12 closing low, according to FactSet. Just this past week, the index exited bear-market territory for the first time in a year.

The index is up 12% so far in 2023, reversing some of its 19.4% decline from 2022, its biggest calendar-year drop since 2008, according to Dow Jones Market Data.

So far this year, highflying tech stocks have helped to paper over weakness in other areas of the market. This has started to change over the past two weeks, as small-cap and value-stocks have lurched suddenly higher, but there are fears that the Fed could hurt the most interest-rate sensitive technology names if Chairman Jerome Powell hints at rates rising higher than investors presently anticipate.

The so-called “Megacap eight” stocks — a group that includes both classes of Alphabet Inc. stock GOOG, +0.16%

GOOGL, +0.07%,

Microsoft Corp. MSFT, +0.47%,

Tesla Inc. TSLA, +4.06%,

Microsoft Corp. MSFT, +0.47%,

Netflix Inc. NFLX, +2.60%,

Nvidia Corp. NVDA, +0.68%,

Meta Platforms Inc. META, +0.14%

— have driven nearly all of the S&P 500’s gains this year, according to Ed Yardeni, president of Yardeni Research, who included his analysis in a note to clients.

But since the beginning of June, the Russell 2000 RUT, -0.80%,

a gauge of small-cap stocks in the U.S., has risen more than 6.6%, according to FactSet data. The Russell 1000 Value Index RLV, -0.15%

has also gained nearly 3.7% in that time. During this period, both have outperformed the tech-heavy Nasdaq Composite COMP, +0.16%,

although the Nasdaq remains the market leader, having risen 26.7% since Jan. 1.

Concerns about the Fed’s plans intensified this week after the Bank of Canada delivered a surprise interest-rate hike, ending a four-month pause. The BOC’s decision followed a similar move by the Reserve Bank of Australia, and partly as a result, U.S. Treasury yields rose and tech-heavy stocks tumbled, with the Nasdaq logging its biggest drop since April 25, according to FactSet.

While small-caps held up amid the chaos, the reaction stoked fears that something similar might be in store for markets when the Fed delivers its latest decision on interest rates Wednesday.

Consequences of a ‘hawkish pause’

Stocks could be in for more turbulence if the Fed signals it plans to follow the BOC and RBA with a hawkish surprise of its own. And it wouldn’t necessarily need to hike rates to pull this off, market strategists said.

Emerging signs of complacency in the market could complicate its reaction. That the Cboe Volatility Index has fallen back below 15 VIX, +1.32%

for the first time since before the arrival of COVID-19 is one such sign that investors aren’t worried enough about a potential selloff, said Miller Tabak + Co.’s Chief Market Strategist Matt Maley.

Another analyst likened the potential fallout from a hawkish Fed to the bad old days of 2022.

“If the Fed signals that rates will be going up again, the market playbook could read more like 2022 than what we have seen so far in 2023,” said Will Rhind, the founder and CEO of GraniteShares, during a phone interview with MarketWatch.

Perhaps the biggest wild card is Tuesday’s inflation report. If the numbers come in hot, Powell and his peers could face pressure to hike rates without priming the market first.

For this reason, Rhind believes investors are underestimating the likelihood of a hike next week, even as Fed funds futures currently see a roughly 70% probability that the central bank will stand pat, according to the CME’s FedWatch tool.

And Rhind isn’t the only one. Leslie Falconio, chief investment officer at UBS Global Wealth Management, says the Tuesday inflation report could be a make-or-break moment for markets, summing up fears expressed elsewhere on Wall Street in a recent note to clients.

“We believe another rate increase is on the table, and that the CPI release on 13 June, a day before the Fed decision, will be decisive. In our view, another hike won’t have a material impact on the pace of economic growth,” Falconio said.

What should investors watch out for?

Assuming the Fed does forego a hike in June, there are a few key tells that investors should watch for to determine whether a “hawkish pause” is under way.

Perhaps the most important will be how the Fed handles changes to its closely watched “dot plot.” A modestly higher median dot would send an unmistakable signal to the market that the Fed will continue with its campaign of tightening monetary policy, perhaps to the detriment of the market, said Patrick Saner, head of macro strategy at the Swiss Re Institute.

“If the Fed skips but wanted to avoid the impression of the hiking cycle being done, it would need to include a revision of the dot plot. They could justify that with a more resilient GDP forecast and a higher inflation outlook. So I think it is the dots and then the statement that will be in focus,” Saner said during a phone interview with MarketWatch.

Beyond that, whatever the Fed does or says will likely be viewed through the lens of economic data that is due out next week. In addition to the Tuesday inflation report, a report on May retail sales is due out Thursday, and a on consumer sentiment from the University of Michigan will land on Friday. All these data points could influence investors’ impressions of the state of the U.S. economy, and their expectations for how the Fed will behave as a result.

Lawmakers and the White House appear set to avert a calamitous U.S. government default, but stock-market investors need to be aware that what comes next could still make for a bumpy ride.

“Some time in the next several days, markets will trade their last bit of angst over raising the debt ceiling for what was always going to be the real problem — handling the massive fundraise by Treasury,” said Steven Blitz, chief U.S. economist at TS Lombard, in a Wednesday note warning of a “potent liquidity squeeze” ahead.

When the U.S. debt-ceiling fight finally is resolved, the Treasury is expected to unleash a flood of bill issuance to help refill its coffers run low by the protracted standoff in Washington, D.C., over the government’s borrowing limit.

Treasury bills are debt issued by the U.S. government that mature in four to 52 weeks. New bill issuance could reach about $1.4 trillion through the end of 2023, with roughly $1 trillion flooding the market before the end of August, according to an estimate from BofA Global strategists.

They expect the deluge through August to be about five times the supply of an average three-month stretch in years before the pandemic.

“The good news is that we have a high degree of confidence around who is going to buy it,” said Mark Cabana, rates strategist at BofA Global, in a phone interview with MarketWatch. “The bad news is that it’s not going to be at current levels. Things have to cheapen.”

Cabana sees a key buyer of bill supply unleashed by a debt-ceiling deal in money-market funds, which have climbed to nearly $5.4 trillion in assets managed since the regional banking crisis erupted in March (see chart).

So people who yanked billions of dollars in deposits from banks after the collapse of Silicon Valley Bank in March and parked them in money-market funds could end up playing an encore performance in this year’s debt-ceiling drama.

Money-market funds swell since March, topping $5 trillion in assets

Money-market funds have been the main reason why at least $2 trillion consistently sits overnight at the Federal Reserve’s reverse repo facility. The program was last offering a roughly 5% rate, a level Cabana said new Treasury bills might need to exceed by about 10-20 basis points.

“It’s an unintended consequence of a debt-ceiling deal getting done,” said George Catrambone, head of fixed income Americas at DWS Group, about market expectations for heavy short-term Treasury bill issuance, but he also expects money-market funds, foreign buyers and other institutions auctions to continue as buyers in the market.

“There’s always buyers. It’s a question of price.”

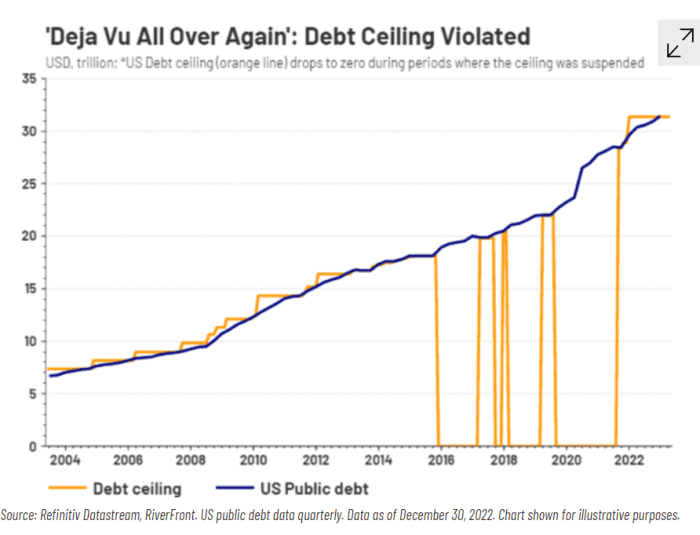

Congress has struck deals each time U.S. public debt has exceeded its debt ceiling in the past, including by suspending it eight times since 2016 (see chart).

In the past when the U.S. debt-limit has been violated, Congress extended or suspended it

Refinitive, RiverFront

That doesn’t mean financial markets have been sitting by idly. The 1-month Treasury yield TMUBMUSD01M, 5.616%

rose to 5.6% on Wednesday, while the 3-month yield TMUBMUSD03M, 5.350%

was 5.3%, according to FactSet. Bill maturing around the “X-date,” which could come as soon as June 1, have even higher yields.

“Those are obviously pretty heady yields,” Catrambone said. “But it also exemplifies the market having to price in potential market disruptions in the month of June,” even though his team, like many in financial markets, expect that eventually “cooler heads will prevail” in Washington as the debt-ceiling standoff heads down to the wire.

Stocks were lower Wednesday, with the Dow Jones Industrial Average DJIA, -0.75%

off almost 300 points, or 0.9%, on pace for a fourth day in a row of losses, according to FactSet. The S&P 500 index SPX, -0.83%

was off 0.9% and the Nasdaq Composite Index was down 0.9%.

Cash balances at the Treasury Department have since dwindled to less than $100 billion, according to economists at Jefferies. Barclays strategists estimate its cash balance may fall below $50 billion between June 5-15.

“Basically, we are just draining our cash account to fund operations while we wait to figure out the debt ceiling,” said Lindsay Rosner, senior portfolio manager at PGIM Fixed Income.

But when the battle over the debt limit ends in a resolution, she expects longer-dated Treasury yields to increase, as haven buying on fears of potentially a full U.S. government default and a credit rating downgrade will have been taken off the table.

“The Armageddon, whatever small probability people were pricing in of catastrophe, remove that,” she said. “And that means the worst economic outcome has been removed.”

That’s also a reason why Rosner has been avoiding ultrashort Treasurys in the eye of the debt-ceiling fight in favor of 2, 3 or 4-year bonds offering some of the highest yields in years.

“We’re being afforded good yield, good spread, a couple of years out the curve,” she said. “Play that game.”

Continued uncertainty about whether a debt-ceiling resolution can come together fast enough to avoid a government default pushed yields on Treasury bills maturing between early and mid-June toward 6% on Tuesday.

The yield on Treasury bills maturing on June 6 touched that level before slipping slightly to 5.997% Tuesday afternoon, according to Bloomberg data. Meanwhile, the rate on T-bills maturing on June 8 was at 5.905%.

In addition, the one-year T-bill issued in June 2022 and which matures on June 15 was yielding 6.141%, though analysts said that was likely being impacted by a government auction on Tuesday. That 6.141% yield was the highest of any government obligation maturing within two weeks after the so-called X-date of June 1 — when Treasury Secretary Janet Yellen said the government might be unable to pay all its bills if no action is taken on the debt ceiling.

The Treasury bill market is where debt-ceiling angst has played out the most and Tuesday brought wild trading as investors questioned whether the government will be forced to miss payments after June 1. At the moment, the T-bill market is in a state of dislocation — one in which yields ranged from as little as 2.924% on the government obligation maturing on May 30 to as high as 6.141% on the 1-year bill maturing in three weeks.

The higher the yield on a Treasury obligation, the more investors are demanding to be compensated for the risk of holding that bill. Yields also rise when investors are selling off or staying away from the underlying maturity. Tuesday’s moves suggest that investors and traders are factoring in at least some risk that the government could cross the X-date without a debt-ceiling resolution.

Right now, the market regards bills maturing between June 6 and June 15 as “the most at risk for a delayed payment and no one wants to own” them, said Lawrence Gillum, the Charlotte, N.C.-based chief fixed income strategist at LPL Financial.

“Ultimately, markets expect something to get done, but money managers who have to own those T-bills are not taking any chances,” he said via phone.

For much of Tuesday, the broader financial market appeared to be relatively confident that a debt-ceiling agreement could be reached by June 1, a day after President Joe Biden and House Speaker Kevin McCarthy each described talks as “productive” on Monday. Then came word of McCarthy telling House Republicans on Tuesday that negotiators were nowhere near a deal yet, with Bloomberg citing Republican Representative Ralph Norman and another unidentified person in the room.

COMP, -1.26%

finished lower, while Treasury yields beyond the 2-year rate slipped toward the end of Tuesday’s New York trading session — a sign of fading optimism in the outlook for the U.S. economy.

One of the financial market’s favorite indicators of impending U.S. recessions — the difference between the 2- and 10-year Treasury yields — has been persistently inverted since July 5, 2022. That’s the longest such streak since May 1980, and yet no recession has been declared so far by the only arbiters who matter, those at the National Bureau of Economic Research.

On Tuesday, fed funds futures traders priced in a 28.1% chance of another quarter-point rate hike by the central bank in June, which would take the main policy rate target to between 5.25%-5.5%. They also factored in a slight 5.6% likelihood of another similar-size rate hike in July.

Gillum and Greg Faranello, head of U.S. rates at AmeriVet Securities in New York, said they see a small chance of no debt-ceiling agreement by June 1. Under such a scenario, the Treasury market would fall into “disarray,” with T-bill yields spiking in a manner reminiscent of last year’s crisis of confidence in the U.K. bond market, they said. It would also make it harder for the Fed to hike rates on June 14, and likely lead to a flight-to-quality trade in longer-term Treasurys as equities sell off.

As of Tuesday, the T-bill market was “definitely showing some signs of stress, there’s no question about it,” Faranello said via phone. Meanwhile, “the economy is doing better than the narrative of recession,” even after the recent turmoil in regional banks, and a move toward 4% in the 10-year rate this year “can’t be ruled out.” However, that could change quickly based on the outcome of the debt-ceiling debate.

Getting something done on the debt ceiling by June 1 “is going to be a challenge,” Faranello said. The risk of default “is small but not a zero-percent probability,” as is the prospect of chaos if negotiators come too close to the wire and create a period of confusion in the Treasury market.

“At a minimum, there would be pretty severe economic damage” from a default or any confusion, it “could be chaotic,” and “you would see that impact on risk assets,” he said.

U.S. stocks closed mixed on Wednesday as weaker economic data weighed on equities and focus among investors returned to recession concerns. The Dow Jones Industrial Average DJIA, +0.24%

gained about 80 points, or 0.2%, ending near 33,482, according to preliminary FactSet data, but the S&P 500 index SPX, -0.25%

and Nasdaq Composite Index COMP, -1.07%

fell 0.3% and 1.1%, respectively. That left the S&P 500 down for two straight days and the Nasdaq lower for a third day in a row. Investors were focused on an ADP report showing that private-sector employers added 145,000 jobs in March, well below the 210,000 expected by economists surveyed by The Wall Street Journal. Also, the bellwether Institute for Supply Management’s service sector activity index showed business conditions at U.S. companies fell to a three-month low of 51.2% in March.

U.S. stocks rallied on Friday to end a rocky month higher, while the Nasdaq Composite also posted its best quarterly gain since 2020. The Dow Jones Industrial Average DJIA, +1.26%

jumped about 414 points, or 1.3%, ending near 33,273 on Friday and up 1.9% for the month, according to preliminary FactSet figures. The S&P 500 index SPX, +1.44%

and Nasdaq Composite Index COMP, +1.74%

posted higher daily gains of 1.4% and 1.7%, respectively, which elevated their monthly gains to 3.5% and 6.7%. Investors in stocks largely looked past turbulence earlier in March after the Federal Reserve acted to calm markets following the sudden collapse of Silicon Valley Bank and Signature Banks. The Fed opened a new facility for banks to tap for liquidity with the aim of preventing forced asset sales, if other banks experience sharp deposit outflows. Friday also marked the end of the quarter, with the Dow and S&P 500 both posting back-to-back quarterly gains. The Nasdaq booked a 16.8% quarterly gain, the best quarter since the 2020, according to Dow Jones Market Data.

Another bubble has emerged, courtesy of the bank-sector crisis which has already felled three U.S. regional banks.

Bank of America analysts led by the Michael Hartnett say money-market funds are the new hot asset.

They point out that assets under management for money funds has now exceeded $5.1 trillion, up over $300 billion over the past four weeks. They also counted the biggest weekly flows to cash since March 2020, the biggest six-week inflow to Treasurys ever, and the largest weekly outflow from investment-grade bonds since Oct. 2022.

The last two times money-market fund assets surged — in 2008 and in 2020 — the Federal Reserve slashed interest rates. Hartnett is fond of the saying, “markets stop panicking when central banks start panicking,” and he noted a surge in emergency Fed discount window borrowing has historically occurred around a big stock-market low.

There is one difference this time, in that inflation is a reality and that labor markets, not just in the U.S. but in other industrialized nations, remains exceptionally strong. The Bank of America team counted 46 interest rate hikes this year, including by the Swiss National Bank after its rescue of Credit Suisse last week.

History, according to the BofA team, says to sell the last interest rate hike. “Credit and stock markets are too greedy for rate cuts, not fearful enough of recession,” they say. After all, when banks borrow from the Fed in an emergency, they tighten lending standards, which in turn results in less lending, and that leads to less small-business optimism, which eventually cracks the labor market.

Bond yields TMUBMUSD10Y, 3.311%

and U.S. stock futures ES00, -0.84%

dropped on Friday, as shares of Deutsche Bank tumbled in Frankfurt.

The S&P 500 SPX, +0.30%

has gained just under 1% this week.

The Bank of England on Thursday matched the U.S. Federal Reserve by hiking interest rates by a quarter percentage point.

The 7-2 decision, the eleventh consecutive increase, brings the U.K. base rate to 4.25%, and comes after data showed inflation surprisingly accelerated in February to a year-over-year rate of 10.4%.

“Headline CPI inflation had surprised significantly on the upside and the near-term path of GDP was likely to be somewhat stronger than expected previously,” the Bank of England said in the simultaneously published minutes of the meeting. “The members put some weight on the possibility that the stronger domestic and global outlook for demand was also being driven by factors over and above the weaker path of energy prices, given that the strengthening had at least in part preceded the falls in prices.”

“If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required,” the central bank said.

The central bank did discuss the banking sector, and the failure of the U.S.’s Silicon Valley Bank and the run-up to UBS’s UBS, -3.09%

purchase of Credit Suisse CS, -5.48%.

SVB’s U.K. subsidiary was bought by HSBC for £1.

The central bank’s financial policy committee said the U.K. banking system maintains robust capital and strong liquidity positions and can “continue supporting the economy” even as interest rates rise.

The pound GBPUSD, +0.45%

traded over $1.23 after the decision. The yield on the 2-year gilt TMBMKGB-02Y, 3.388%

however slipped 7 basis points to 3.42%, after a big rise on Wednesday when the inflation data came out.

The run on Silicon Valley Bank (SVB) SIVB— on which nearly half of all venture-backed tech start-ups in the United States depend — is in part a rerun of a familiar story, but it’s more than that. Once again, economic policy and financial regulation has proven inadequate.

The news about the second-biggest bank failure in U.S. history came just days after Federal Reserve Chair Jerome Powell assured Congress that the financial condition of America’s banks was sound. But the timing should not be surprising. Given the large and…