Apple Inc. said Sunday that it now expects lower shipments of its high-end iPhone 14 Pro and iPhone 14 Pro Max devices than it did previously, as COVID-19 issues hamper production in China.

“We continue to see strong demand for iPhone 14 Pro and iPhone 14 Pro Max models,” the company announced in a Sunday evening press release. “However, we now expect lower iPhone 14 Pro and iPhone 14 Pro Max shipments than we previously anticipated and customers will experience longer wait times to receive their new products.”

Apple AAPL, -0.19%

acknowledged in its release that COVID-19 issues have “temporarily impacted” production of the devices at the Zhengzhou site that is the “primary” assembly facility for the iPhone 14 Pro and iPhone 14 Pro Max. That facility is currently seeing “significantly reduced” operating capacity.

“We are working closely with our supplier to return to normal production levels while ensuring the health and safety of every worker,” the company added in the release.

“Although Apple earnings were only a week ago, supply shortages at the high end of the market and recent COVID lockdowns in China impacting a Foxconn plant could negatively impact iPhone units in the December quarter,” UBS analyst David Vogt wrote Wednesday, ahead of Apple’s press release. “While we believe iPhone demand tends to not be perishable, a slippage of a couple of million units is possible below our 86 million forecast.”

After a Covid outbreak at a Foxconn factory in Zhengzhou, China, some workers chose to go home. Pictured here are the shuttle buses on Oct. 30, 2022.

VCG | Getty Images

Apple said in a statement on Sunday that it has temporarily reduced iPhone 14 production because of Covid-19 restrictions at its primary iPhone 14 Pro and iPhone 14 Pro Max assembly plant in Zhengzhou, China.

The factory, operated by Foxconn, is operating at “significantly reduced capacity,” Apple said. It warned that it would ship fewer units and that customers would experience longer wait times when ordering devices.

Apple’s warning brings up the possibility that it may sell fewer iPhones in the December quarter because it is having trouble making enough to meet demand. It previously signaled slowing growth in the December quarter last month.

It said that it continues to see strong demand for the affected models, which are higher-priced than other iPhone models and start at $999 and $1099.

In the past week, China has ordered lockdowns in Zhengzhou, where Apple does the majority of its iPhone production. The factory in China has grappled with employees fleeing the facility because of its Covid policies and outbreaks, according to Reuters.

China continues to pursue a “zero-Covid” policy that requires facilities like the iPhone facility in Zhengzhou to operate as “closed loops,” where workers isolate in dorms and work in factories separated from the outside world.

It currently takes 31 days to receive an iPhone 14 Pro if ordered from Apple’s website, longer than the average 2-day lead time for less-expensive iPhone models, JPMorgan analyst Samik Chatterjee said in a note on Sunday.

PayPal shares fell more than 5% in after-hours trading, despite beating earnings and revenue expectations for the third quarter, as the company’s Q4 revenue estimate came in behind analysts’ expectations.

Here’s what PayPal reported:

Earnings per share (EPS): $1.08 per share, ex-items, vs. 96 cents expected, according to a Refinitiv survey of analysts

Revenue: $6.85 billion, vs. $6.82 billion expected, according to Refinitiv

The company estimated Q4 revenues to come in at $7.38 billion, which is less than the $7.74 billion consensus expectations, according to analysts surveyed by Refinitiv

PayPal raised EPS guidance for the full fiscal year, saying it’s benefited from “ongoing productivity initiatives.” It expects to add 8 to 10 million net new active users in the fiscal year.

The company said it’s working with Apple to enhance its offerings for PayPal and Venmo, including by letting U.S. merchant customers accept contactless payments through their mobile wallets and adding PayPal and Venmo network-branded credit and debit cards to the Apple Wallet.

Wall Street had braced for a bumpy ride as Qualcomm Inc. navigated an oversupplied market for smartphone chips, but the chip maker’s stock still got T-boned Thursday after a disappointing holiday forecast.

“A weak market, and even a potential inventory correction, was likely not entirely unexpected,” Bernstein analyst Stacy Rasgon wrote, while adding that “the magnitude is probably worse than what some might have had in mind (though it is certainly not confined to Qualcomm, with virtually all handset-exposed players showing similar dynamics).”

More than half of the analysts who cover Qualcomm cut their price targets in reaction to the report, according to FactSet tracking. Evercore ISI analyst C.J. Muse cut his target to $120 from $130 while maintaining an in-line rating; he wrote that while Qualcomm set up for a miss, as it did last quarter, the actual read was much worse than expected.

“While the buyside was clearly set up for a miss, the magnitude for the December Q was clearly a lot worse than expected with revenues/EPS guided 20%/32% below consensus,” Muse said.

“Here, management highlighted demand weakness (CY22 handsets now expected down low double-digits% vs. prior down mid-single digits%; largely Android market and includes premium tier) and elevated channel inventory (now 8-10 weeks oversupply) as the key drivers of weakness,” the Evercore analyst noted.

Of the 32 analysts who cover Qualcomm, 20 have buy-grade ratings and 12 have hold ratings. Of those 32 analysts, 19 cut price targets resulting in an average target price of $153.75, down from a previous $172.71, according to FactSet data.

Qualcomm stock has declined more than 42% so far this year, in line with a 41.2% decline for the PHLX Semiconductor Index SOX, -0.65%,

but well past the 21.1% year-to-date decline for the S&P 500 index SPX, -0.50%.

How good is a company’s chief executive officer at investing your money most efficiently? This is an important question for long-term investors. It may underline the difference between a steady long-term performer and a flash in the pan.

And Apple Inc. AAPL, -4.24%

now makes up 7% of the SPDR S&P 500 ETF Trust SPY, -1.03%,

the first and largest exchange-traded fund (with $360 billion in assets), which tracks the benchmark S&P 500 SPX, -1.06%.

That’s close to an all-time record, and the iPhone maker has a whopping 14.1% position in the Invesco QQQ Trust QQQ, -1.95%,

which tracks the Nasdaq-100 Index NDX, -1.98%.

Looking at the full Nasdaq Index COMP, -1.73%,

which has 3,747 stocks, Apple takes a 13.5% position.

Apple now makes up 7.3% of the S&P 500 by market capitalization, close to the 8% record it set late in September.

FactSet

This is very much an Apple stock market, with the company topping the broad indexes that are weighted by market capitalization. You are likely to be invested in the company indirectly. You also might be feeling Apple’s impact in other ways. Apple’s App Store ecosystem drives more than $600 billion in annual revenue for developers.

Tim Cook’s tenure as Apple’s CEO has been nothing short of breathtaking when measured by the company’s financial performance. Apple is not one of the fastest-growing companies when measured by sales or earnings — it is too big for that. But its excellent stock performance has reflected Cook’s ability to deploy invested capital with improving efficiency. Cook has also been a market trendsetter in other important ways. He has Apple repurchasing $90 billion of its shares annually, setting the pace for stock buybacks in the market. Cook’s steady hand has also helped Apple withstand the market’s tech wreck and remain a stable pillar for the teetering Nasdaq Composite index generally. For all these reasons, Cook has earned a spot on the MarketWatch 50 list of the most influential people in markets.

Apple keeps improving by this important measure

Investors in the stock market are looking for growth over the long term. The best measure of that is whether or not a company’s share price goes up or down. But Cook isn’t just managing Apple’s stock. Digging a bit deeper into the company’s actual operating performance can provide some insight into what a good job Cook has done.

What should a corporate manager focus on? The stock price? How about the most efficient and most profitable way to provide goods and services? There are different ways to do this, and Apple has focused on quality, reliability and excellent service to build customer loyalty.

Apple’s commitment can be experienced by anyone who calls the company for customer service. It is easy to get through to a well-trained representative who will solve your problem. How many companies can say that at a time when it seems many companies cannot even handle answering the phone?

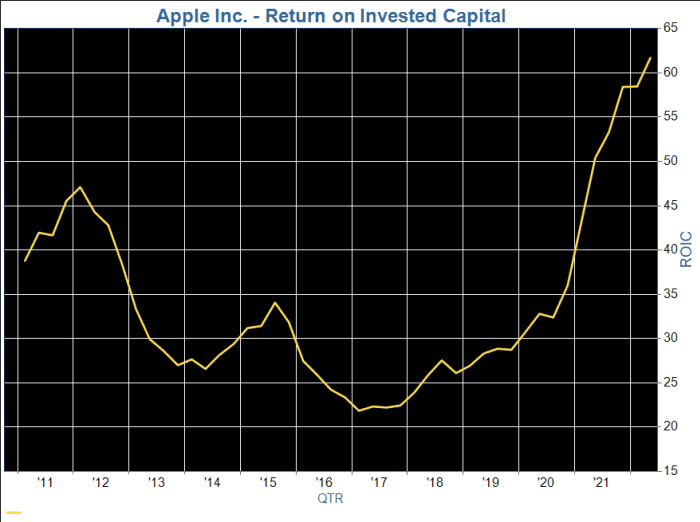

Apple’s returns on invested capital have increased markedly over the past six years.

FactSet

A company’s return on invested capital (ROIC) is its profit divided by the sum of the carrying value of its common stock, preferred stock, long-term debt and capitalized lease obligations. ROIC indicates how well a company has made use of the money it has raised to run its business. It is an annualized figure, but available quarterly, as used in the chart above.

The carrying value of a company’s stock may be a lot lower than its current market capitalization. The company may have issued most of its shares long ago at a much lower share price than the current one. If a company has issued shares recently or at relatively high prices, its ROIC will be lower.

A company with a high ROIC is likely either to have a relatively low level of long-term debt or to have made efficient use of the borrowed money.

Among companies in the S&P 500 that have been around for at least 10 years, Apple placed within the top 20 for average ROIC for the previous 40 reported fiscal quarters as of Sept. 1.

As you can see on the chart, Apple’s ROIC has improved dramatically over the past five years, even as the wide adoption of the company’s products and services has led to an overall slowdown in sales growth.

A quick comparison with other giants in the benchmark index

It might be interesting to see how Apple stacks up among other large companies, in part because some businesses are more capital-intensive than others. For example, over the past four quarters, Apple’s ROIC has averaged 52.9%, while the average for the S&P 500 has been a weighted 12.1%, by FactSet’s estimate.

Here are the 10 companies in the S&P 500 reporting the highest annual sales for their most recent full fiscal years, with a comparison of average ROIC over the past 40 reported quarters:

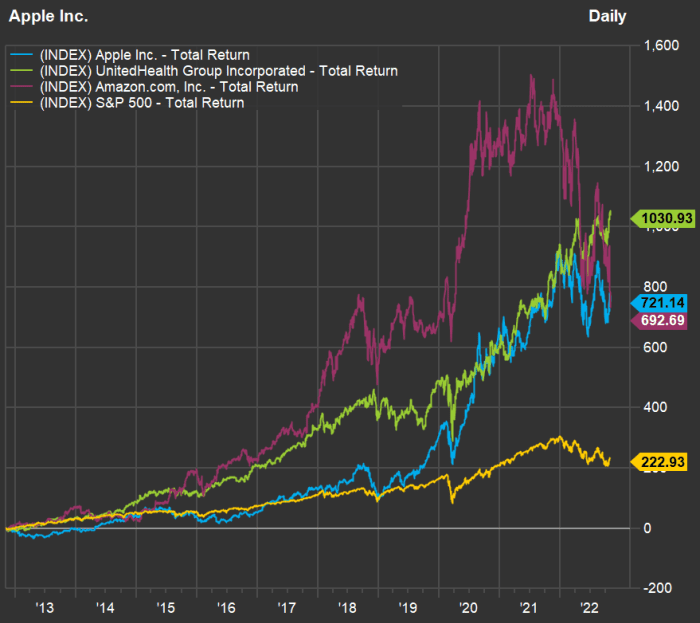

Among the largest 10 companies in the S&P 500 by annual sales, Apple takes the top ranking for average ROIC over the past 10 years, while ranking second for total return behind UnitedHealth Group Inc. UNH, +0.03%

and ahead of Amazon.com Inc. AMZN, -3.06%.

UnitedHealth has been able to remain at the forefront of managed care during the period of transition for healthcare in the U.S., in the wake of President Barack Obama’s signing of the Affordable Care Act into law in 2010.

Here’s a chart showing 10-year total returns for Apple, UnitedHealth Group, Amazon and the S&P 500:

FactSet

Apple is only slightly ahead of Amazon’s 10-year total return. But what is so striking about this chart is the volatility. Apple has had a smoother ride. During the bear market of 2022, Apple’s stock has declined 18%, while the S&P 500 has gone down 20%, the Nasdaq has fallen 32% (all with dividends reinvested) and Amazon has dropped 45%.

The broad indexes would have fared even worse so far this year without Apple.

Qualcomm Inc. shares fell in the extended session Wednesday following the chip maker’s poor outlook, and estimates of about two months or more of inventory it needs to clear in its core business.

On the call with analysts, Chief Executive Cristiano Amon said the accelerated weak demand was related to “macro economic headwinds and the prolonged COVID in China,” and “the rapid deterioration in demand and easing of supply constraints” across the chip industry.” would take out about 80 cents a share in first-quarter earnings.

“It’s the major factor,” Amon told analysts on the call. “It’s mostly a handset consumer story.” Earnings for the first quarter, as a results, would take a hit of 80 cents a share, the company said.

Another big factor is that companies are just spending less. Amon said “companies across the board had much higher inventory policies, supply chain got resolved, and you got that macro economic uncertainty, you have a drawdown trying to bring inventory to a different level than it was during the situation of demand constraint.”

Qualcomm forecast first-quarter earnings of $3 to $3.30 a share on revenue of $9.2 billion to $10 billion, while the Street estimated $3.43 a share on revenue of $12.02 billion.

Chief Financial Officer Akash Palkhiwala told analysts there is about eight to 10 weeks of elevated in the channel. In the meantime, Qualcomm was instituting a hiring freeze, and looking into cost-saving measures, execs told analysts.

While handset-chip sales surged 40% to a record $6.57 billion from a year ago, topping the Street’s expectation of $6.55 billion, the company’s forecast indicates a big glut in inventory in Qualcomm’s CDMA Technologies unit, the one that includes handset and RF chips as well as chips for autos and Internet of Things.

Qualcomm expects QCT sales of $7.7 billion to $8.3 billion, and sales from Qualcomm’s technology licensing, or QTL, segment of $1.45 billion to $1.65 billion. Analysts had forecast forecast $10.42 billion in QCT sales and QTL revenue of $1.71 billion.

Qualcomm reported fourth-quarter QCT revenue of $9.9 billion, a 28% gain from a year ago. Analysts had estimated $9.84 billion, based on the company’s forecast of $9.5 billion to $10.1 billion.

Fourth-quarter auto-chip sales zoomed up 58% to a record $427 million, and Internet of Things, or IoT, sales rose 24% to a record $1.92 billion. The Street was expecting auto sales of $362.4 million, and IoT sales of $1.82 billion.

Revenue from the QTL segment fell 8% to $1.44 billion compared with Wall Street estimates of $1.58 billion, based on a company forecast of $1.45 billion to $1.65 billion.

The company reported fiscal fourth-quarter net income of $2.87 billion, or $2.54 a share, compared with $2.8 billion, or $2.45 a share, in the year-ago period. The chip maker reported adjusted earnings, which exclude stock-based compensation expenses and other items, of $3.13 a share, compared with $2.55 a share in the year-ago period. Total revenue for the third quarter rose to $11.4 billion from $9.34 billion in the year-ago period.

Analysts had estimated earnings of $3.13 a share on revenue of $11.32 billion, based on Qualcomm’s forecast of $3 to $3.30 a share on revenue of $11 billion to $11.8 billion.

Year to date, Qualcomm shares are down 38%, compared with a 41% decline for the PHLX Semiconductor Index SOX, -3.09%,

a 21% decline by the S&P 500 index SPX, -2.50%

and a 33% drop by the tech-heavy Nasdaq Composite Index COMP, -3.36%.

Qualcomm Inc. shares fell in the extended session Wednesday following the chip maker’s poor outlook, and estimates of about two months or more of inventory it needs to clear in its core business.

On the call with analysts, Chief Executive Cristiano Amon said the accelerated weak demand was related to “macro economic headwinds and the prolonged COVID in China,” and “the rapid deterioration in demand and easing of supply constraints” across the chip industry.” would take out about 80 cents a share in first-quarter earnings.

“It’s the major factor,” Amon told analysts on the call. “It’s mostly a handset consumer story.” Earnings for the first quarter, as a results, would take a hit of 80 cents a share, the company said.

Another big factor is that companies are just spending less. Amon said “companies across the board had much higher inventory policies, supply chain got resolved, and you got that macro economic uncertainty, you have a drawdown trying to bring inventory to a different level than it was during the situation of demand constraint.”

Qualcomm forecast first-quarter earnings of $3 to $3.30 a share on revenue of $9.2 billion to $10 billion, while the Street estimated $3.43 a share on revenue of $12.02 billion.

Chief Financial Officer Akash Palkhiwala told analysts there is about eight to 10 weeks of elevated in the channel. In the meantime, Qualcomm was instituting a hiring freeze, and looking into cost-saving measures, execs told analysts.

While handset-chip sales surged 40% to a record $6.57 billion from a year ago, topping the Street’s expectation of $6.55 billion, the company’s forecast indicates a big glut in inventory in Qualcomm’s CDMA Technologies unit, the one that includes handset and RF chips as well as chips for autos and Internet of Things.

Qualcomm expects QCT sales of $7.7 billion to $8.3 billion, and sales from Qualcomm’s technology licensing, or QTL, segment of $1.45 billion to $1.65 billion. Analysts had forecast forecast $10.42 billion in QCT sales and QTL revenue of $1.71 billion.

Qualcomm reported fourth-quarter QCT revenue of $9.9 billion, a 28% gain from a year ago. Analysts had estimated $9.84 billion, based on the company’s forecast of $9.5 billion to $10.1 billion.

Fourth-quarter auto-chip sales zoomed up 58% to a record $427 million, and Internet of Things, or IoT, sales rose 24% to a record $1.92 billion. The Street was expecting auto sales of $362.4 million, and IoT sales of $1.82 billion.

Revenue from the QTL segment fell 8% to $1.44 billion compared with Wall Street estimates of $1.58 billion, based on a company forecast of $1.45 billion to $1.65 billion.

The company reported fiscal fourth-quarter net income of $2.87 billion, or $2.54 a share, compared with $2.8 billion, or $2.45 a share, in the year-ago period. The chip maker reported adjusted earnings, which exclude stock-based compensation expenses and other items, of $3.13 a share, compared with $2.55 a share in the year-ago period. Total revenue for the third quarter rose to $11.4 billion from $9.34 billion in the year-ago period.

Analysts had estimated earnings of $3.13 a share on revenue of $11.32 billion, based on Qualcomm’s forecast of $3 to $3.30 a share on revenue of $11 billion to $11.8 billion.

Year to date, Qualcomm shares are down 38%, compared with a 41% decline for the PHLX Semiconductor Index SOX, -3.09%,

a 21% decline by the S&P 500 index SPX, -2.50%

and a 33% drop by the tech-heavy Nasdaq Composite Index COMP, -3.36%.

Multiple police officers with weapons drawn surrounded a vehicle parked outside a government building in Mobile, Alabama, in a standoff that lasted for hours

MOBILE, Ala. — Multiple police officers with weapons drawn surrounded a vehicle parked outside a government building in downtown Mobile, Alabama, in a standoff that lasted for hours Monday.

Katrina Frazier, a police spokeswoman, told reporters that a man with an apparent gunshot wound was spotted in a parked car outside Government Plaza, which contains multiple Mobile County offices and courts. She said the man pointed a gun at his head when officers approached to see if he needed help, al.com reported.

“Officers backed away from the scene and we called in the SWAT teams and a negotiator,” said Frazier. It wasn’t clear whether the man shot himself or was shot by someone else.

Photos and video from the scene showed dozens of officers pointing handguns and rifles toward a car parked along a curb. Mental health professionals were on the scene talking to the person, and no hostages were involved, James Barber, an aide in the mayor’s office, told WALA-TV.

A main road through the city was blocked, as was a tunnel that passes under the Mobile River leading out of the city.

MOBILE, Ala. — At least five tornadoes have been confirmed after a severe weather outbreak Saturday along the Mississippi and Alabama Gulf Coast.

No injuries or deaths were reported as damage surveys continued.

The National Weather Service said Sunday that three tornadoes touched down in Jackson County, Mississippi, each with top winds estimated between 100 mph and 110 mph (160 kph and 175 kph).

In Alabama, two weak tornadoes with winds of 72 mph (115 kph) or less were confirmed, one in Theodore and one south of downtown Mobile. Surveyors were still looking Sunday for evidence of tornadoes in Alabama, where multiple funnel clouds were captured on video or in pictures.

A Mississippi twister in Vancleave had a path of 1.25 miles (2 kilometers) damaging trees, a home and some outbuildings. A 2.8-mile (4.5-kilometer) tornado damaged trees in Moss Point before crossing a marsh and Interstate 10. A 1-mile (1.6-kilometer) tornado damaged light poles at a park in Big Point.

Surveyors concluded that damage to Gautier Middle School was caused by straight line winds. Wind damage was also reported farther west in Pass Christian and Diamondhead, Mississippi.

Although tornadoes are rare in most of the United States in late fall and winter, they are more common along the Gulf Coast in those seasons, when cold fronts collide with warm Gulf of Mexico air.

In Alabama, multiple people made images of a funnel cloud crossing a highway that runs across Mobile Bay between Mobile and Spanish Fort. No damage was reported there.

Residents also reported wind damage in parts of western Mobile and in Theodore, southwest of the city. The Theodore tornado tore the roof off at least one house, blowing out windows. Other residents lost fences, trampolines and above-ground swimming pools.

“Opened this front door and the tree tops over there just parted and you could see a funnel not touching the ground, come through I slammed the door got in the hallway with the kids, and in a matter of 30 seconds the ramming and banging and it was gone,” homeowner Matthew McGilberry of Theodore told WKRG-TV on Sunday.

East across Mobile Bay, thousands were without power late Saturday around Magnolia Springs and Bon Secour. However utilities reported that almost all the outages had been restored by Sunday.

Claims that former U.K. Prime Minister Liz Truss’ mobile phone was hacked by foreign agents while she was serving as foreign secretary must be “urgently investigated,” the opposition Labour Party said.

Private messages exchanged between Truss’ personal phone and foreign officials — including detailed discussions about arms shipments to Ukraine — are thought to have been intercepted by foreign agents, the Mail on Sunday reported, citing security sources.

The newspaper claimed that the hack was uncovered during this summer’s Conservative leadership campaign, but that details were suppressed by then-Prime Minister Boris Johnson and Cabinet Secretary Simon Case, the U.K.’s most senior civil servant. Russia was suspected to be behind the hack, the report said.

Labour’s shadow home secretary, Yvette Cooper, said the allegations were “extremely serious.”

“There are immensely important national security issues raised by an attack like this by a hostile state,” Cooper said in a statement.

“There are also serious security questions around why and how this information has been leaked or released right now which must also be urgently investigated,” she said. “It is essential that all of these security issues are investigated and addressed at the very highest level.”

Speaking to Sky News’ Sophy Ridge on Sunday program, U.K. Housing Secretary Michael Gove did not deny the hack took place but insisted “very robust protocols” were in place to ensure the security of governmental communications.

“I don’t know the full details of what security breach, if any, took place,” Gove said. “I’m sure that the right protocols were followed. I’m sure that more information, as appropriate, will be released.”

Citing allies of Truss, the Mail on Sunday reported that the former foreign secretary had been worried that revelations about the hack would compromise her bid to become prime minister, with one claiming she “had trouble sleeping” until it was confirmed that news of the alleged security breach would not be disclosed by the government.

In this photo illustration, former U.S. President Donald Trump’s archived Twitter account is shown on a phone screen with the Twitter logo in the background.

Sheldon Cooper | Lightrocket | Getty Images

A decade ago, Twitter’s future was looking bright. The company was benefiting from a flood of funding into the social-networking space, eventually leading to an IPO in 2013 that raised $1.8 billion.

Now the company is back in private hands. And they happen to be the hands of Elon Musk, the richest person in the world and one of the app’s most high-profile provocateurs.

It’s a massive moment. Twitter has become a key place for people to debate, joke and pontificate in their own circles of politics, sports, tech and finance. It’s also served as a platform that gives voice to the voiceless, helping protesters organize and express themselves in repressed regimes around the world.

In recent years, however, Twitter and social media rivals like Facebook have been at the center of controversy over the distribution of fake news and misinformation, sometimes leading to bullying and violence.

Investors had grown concerned about Twitter as a business. The company was generally unprofitable, struggled to keep pace with Google and Facebook, and often killed popular products with no real explanation.

What follows is a brief history of Twitter, which — despite its many flaws — is one of the most iconic companies to come out of Silicon Valley in the past 20 years.

2006

In March, Jack Dorsey, Noah Glass, Biz Stone, and Evan Williams created Twitter, which was originally a side project stemming from the podcasting tool Odeo. That month, Dorsey would send the first Tweet that read, “just setting up my twttr.”

2007

In July, Twitter received a $100,000 Series A funding round led by Union Square Ventures. The app’s popularity started to explode after being heavily promoted by the tech community during the annual South by Southwest conference.

2008

Dorsey stepped down as CEO in October, and was replaced by Williams. According to the book “Hatching Twitter” by journalist Nick Bilton, Twitter’s board fired Dorsey over concerns about the executive’s management style and public boastings.

2009

Twitter’s popularity continued to soar, leading to a high-profile appearance from Williams on Oprah Winfrey’s talk show alongside celebrity Ashton Kutcher. Kutcher would also write about Williams and Stone as part of Time Magazine’sTime 100 issue. Twitter was now a mainstream phenomenon.

2010

Twitter reached space, with NASA Astronaut Timothy Creamer sending the first tweet live from outer orbit. Behind the scenes, however, management woes continued with Williams stepping down as CEO, replaced by operating chief Dick Costolo.

2011

Twitter became an essential social media tool used during the Arab Spring, the wave of antigovernmental protests throughout Egypt, Libya and Tunisia. Protesters used the site to post reports and to organize. As the Pew Research Center noted, Twitter’s role in “disseminating breaking news” was not “not limited to the Arab uprisings – the death of Whitney Houston, for example, was announced on Twitter 55 minutes prior to the AP confirming the story.”

2012

Twitter’s reach expanded to 200 million active users. Barack Obama used the “platform to first declare victory publicly in the 2012 U.S. presidential election, with a Tweet that was viewed approximately 25 million times on our platform and widely distributed offline in print and broadcast media,” according to corporate filings.

2013

Twitter went public in November. The combined wealth of Williams, Dorsey, and Costolo hit roughly $4 billion.

“I think we’ve got a tremendous set of thoughts and strategies to increase the slope of the growth curve,” Costolo told CNBC at the time. “I would consider some of them tactics, some of them broader strategies, in service of doing what I referred to as bridge the gap between the massive awareness of Twitter and deep engagement of the platform.”

2014

Slowing user growth led to several stock drops and analyst downgrades. Twitter also deemed 2014 the year of the “selfie.”

2015

Compared to rivals like Google, Facebook, and even LinkedIn, Twitter was starting to look like the runt of the Internet litter. Twitter was still unprofitable as its ad business struggled mightily against its larger competitors. Dorsey would also return as CEO of the company, while still maintaining the top job at his other company, Square (now Block).

2016

Rumors began circulating that Twitter was looking to be acquired, with Salesforce as a potential suitor. Meanwhile, Twitter and Facebook were criticized for their role in letting prominent users like Donald Trump, who would win the U.S. presidential election that year, spread misleading information without consequence.

“Having the president-elect on our service using it as a direct line of communication allows everyone to see what is on his mind in the moment,” Dorsey said at the time. “We’re definitely entering a new world where everything is on the surface and we can all see that in real time and we can have conversations about it.”

2017

For a moment, Twitter appeared to be on the upswing. Its stock was finally trending upward as the company’s finances were improving. Meanwhile, Trump as president continued to use Twitter as his megaphone. According to Twitter’s own data, “Trump was the most-tweeted-about global leader in the world and in the United States” that year, CNBC reported.

2018

Dorsey and Facebook’s then-operating chief Sheryl Sandberg testified before the Senate Intelligence Committee about alleged interference by Russia-linked actors in the 2016 election. Trump and fellow Republicans became increasingly vocal about alleged political bias by Twitter and other social media sites.

“In fact, from a simple business perspective and to serve the public conversation, Twitter is incentivized to keep all voices on the platform,” Dorsey said at the time.

2019

Analysts found correlations between President Trump’s voracious use of Twitter and various markets, including gold, underscoring the cultural power of Twitter. Trump met with Dorsey — a Twitter spokesperson said “Jack had a constructive meeting with the President of the United States today at the president’s invitation.”

“They discussed Twitter’s commitment to protecting the health of the public conversation ahead of the 2020 U.S. elections and efforts underway to respond to the opioid crisis,” the spokesperson said.

2020

As Covid-19 spread across the globe, the spread of misinformation dominated the online conversation. And Twitter continued to struggle to grow its business. The service was also hacked that year, and miscreants gained access to over a dozen high-profile accounts, including those controlled by Joe Biden, Jeff Bezos, and Musk

2021

Twitter permanently banned Trump over inflammatory comments the president made during the U.S. Capitol riots in January that the company said could lead to “further incitement of violence.” Trump would allege that Twitter workers “coordinated with the Democrats and the Radical Left in removing my account from their platform, to silence me.” Later, Dorsey suddenly stepped down as CEO and was replaced by Parag Agrawal, the company’s chief technology officer.

2022

Musk took over Twitter after a protracted legal spat that would have culminated this week in a trial in Delaware’s Court of Chancery. The Tesla CEO agreed in April to pay $44 billion for Twitter, but then attempted to renege on the deal. He changed course and opted to proceed, walking into the company’s San Francisco office on Wednesday with what appeared to be a porcelain bathroom sink in his hands.

“Entering Twitter HQ – let that sink in!” he tweeted, with a video of his entrance.

Musk immediately began making changes, firing Agrawal, finance head Ned Segal, and head of legal policy Vijaya Gadde.

Apparently it’s Apple Inc. AAPL, +7.56%,

which is set to become the only mega-cap technology company not to see a sharp post-earnings decline in its stock price this week, after the smartphone giant delivered a somewhat mixed earnings report but seemed to reassure Wall Street just enough about the state of its demand.

The stock was up 7.6% in Friday morning trading and on track to log its largest single-day percentage gain since July 31, 2020, when it increased 10.5%, according to Dow Jones Market Data.

Apple is “the bright spot amid mega-cap carnage,” wrote Wells Fargo analyst Aaron Rakers, as Apple topped expectations with its headline results despite the backdrop of “a lot of macro/geopolitical uncertainties” as well as foreign-exchange pressures.

While Apple fell short with its iPhone sales numbers for the September quarter, Rakers noted that the company has been constrained by supply for its Pro models. At the same time, he noted that Mac revenue easily exceeded the consensus view, which supported his thesis that “Apple is solidly positioned as share taker in PCs.”

He further pointed out that Apple results were burdened by a deeper-than-expected impact from foreign exchange. But “look past the FX headwinds & you’ll see why everyone is hiding in Apple,” he said.

Rakers rates the stock at overweight with a $185 price target.

Evercore ISI’s Amit Daryanani called Apple “the last FAANG standing.”

“Overall, revenue and EPS estimates will shift higher from current levels and given the broadly disappointing EPS calls from big tech this was an impressive set of numbers and guide,” he wrote in his note to clients.

Though Apple didn’t give formal financial guidance, it offered various pieces of commentary around the December quarter, including that it could see a 10-point headwind from foreign exchange in the period and recognize a “few hundred” basis points of impact from an extra week being added to the quarter, even as Mac revenue is set for a substantial decline.

“All this results in our assessment that revenue growth will be mid-single digits (our model is at 5% vs. Street was at 2%),” Daryanani wrote.

Admittedly, it’s not just about the December quarter, he noted.

“Eventually the question will be on durability of demand beyond Dec-qtr and the impact from macro not just on iPhones but also services,” Daryanani wrote, though he likes Apple’s long-term potential to grow sales at a mid- or high-single-digit clip and grow earnings at a mid- to low-teens rate.

He rates the stock at outperform with a $190 target.

Wedbush’s Dan Ives wrote that Apple was “the one bright spot” amid “a horror show week for Big Tech earnings.”

“Given the perfect storm of currency/macro this quarter, we would characterize Apple’s results and commentary around the December quarter as net bullish around underlying demand and help throw out the noise that iPhone 14 upgrades are slowing in this cycle,” he wrote, while keeping an outperform rating but cutting his price target to $200 from $220 to reflect a lower multiple.

The latest results could help change what Citi Research analyst Jim Suva said was a relatively negative attitude towards Apple’s stock when compared to the rest of Big Tech.

“The amount of investor negativity on mega-cap tech stocks, especially Apple, is well known as recent surveys show Apple as the least favored stock amongst its peers,” he wrote. “Yes there are valid concerns of electronic retailers working down inventory and consumers having less disposable income given inflation but we believe consumers will adjust their spending allocations and continue to spend on Apple’s growing platform of products and services.”

He rates the stock a buy with a $175 price target, down from $185 before.

Barclays analyst Tim Long stayed more cautious.

“Stepping back from the print, things get tougher heading into Dec-Q and beyond and we maintain our [equal-weight] rating, mainly on headwinds sustaining current demand levels as high-end consumers potentially weaken, tougher comps on Mac, Services weakening further, regulatory overhang (App Store, Google TAC), macro impacting digital advertising as well as a rich valuation,” he wrote as he bumped his price target up by a dollar to $156.

Whether that plays out in the shares is another question.

“Near term, we expect heightened macro uncertainty to remain an overhang for the stock, although some may view AAPL as a relative safe haven in the macro storm,” Long continued.

Iranians protest to demand justice and highlight the death of Mahsa Amini, who was arrested by morality police and subsequently died in hospital in Tehran under suspicious circumstances.

Mike Kemp | In Pictures via Getty Images

A bipartisan group of 13 lawmakers urged several U.S. tech CEOs to do more to help Iranian people stay connected to the internet as their government seeks to censor communications amid ongoing protests.

The Iranian regime has taken aggressive measures to block citizens from the internet and anti-government messages as people across the country continue to protest its restrictive standards. The protests began after 22-year-old Mahsa Amini died while in the custody of Iran’s so-called morality police, who had accused her of improperly wearing her hijab, an Islamic head-covering for women.

In the letter to the CEOs of Amazon, Apple, Google, Meta, Microsoft and cloud service DigitalOcean, the lawmakers asked the executives to be “more proactive” in getting important services to Iran. The Treasury Department last month issued guidance on U.S. sanctions on Iran to make clear that social media platforms, video conferencing and cloud-based services that deliver virtual private networks can operate in Iran.

“While we appreciate some of the steps your companies have taken, we believe your companies can be more proactive in acting pursuant to the broad authorization provided in GLD-2,” the lawmakers wrote, referencing the general license used to issue sanctions guidance.

They specifically pointed to four different types of tools they’d like to see the companies work to get into the hands of the Iranian people: cloud and hosting services, messaging and communication tools, developer and analytics tools and access to app stores.

The lawmakers said these types of tools would help Iranian citizens stay connected to the internet in secure ways amid government-imposed shutdowns and reduce their reliance on domestic infrastructure. The availability of multiple secure communications tools would make it harder for the Iranian regime to shut down all of them at once, they wrote.

The lawmakers also said that giving the Iranian people access to developer tools and app stores would allow them to “create and harden” their own communications apps and security tools and give them a place to distribute them without government surveillance.

Reps. Tom Malinowski, D-N.J., Claudia Tenney, R-N.Y., and Sens. Bob Menendez, D-N.J. and Marsha Blackburn, R-Tenn., took the lead in the letter.

“Iranians are fearlessly risking their lives for their fundamental rights and dignity,” they wrote. “Your tools and services may be vital in their efforts to pursue these aspirations, and the United States should continue to make every effort to assist them.”

A Google spokesperson said in a statement the company is working on ways to “ensure continued access to generally available communications tools like Google Meet and our other Internet services.” Google launched location sharing in Iran on Google Maps in September to let people let loved ones know where they are and the Jigsaw team within Google is working to make its tool more widely available so users in Iran can run their own VPNs that resist blocking, the spokesperson added.

Meta did not provide a comment. The Facebook-owner had made Instagram and WhatsApp available in Iran, but the services have been restricted by the government.

The other companies named in the letter did not immediately respond to CNBC’s requests for comment.

Apparently it’s Apple Inc. AAPL, +7.56%,

which is set to become the only mega-cap technology company not to see a sharp post-earnings decline in its stock price this week, after the smartphone giant delivered a somewhat mixed earnings report but seemed to reassure Wall Street just enough about the state of its demand.

The stock was up 7.6% in Friday morning trading and on track to log its largest single-day percentage gain since July 31, 2020, when it increased 10.5%, according to Dow Jones Market Data.

Apple is “the bright spot amid mega-cap carnage,” wrote Wells Fargo analyst Aaron Rakers, as Apple topped expectations with its headline results despite the backdrop of “a lot of macro/geopolitical uncertainties” as well as foreign-exchange pressures.

While Apple fell short with its iPhone sales numbers for the September quarter, Rakers noted that the company has been constrained by supply for its Pro models. At the same time, he noted that Mac revenue easily exceeded the consensus view, which supported his thesis that “Apple is solidly positioned as share taker in PCs.”

He further pointed out that Apple results were burdened by a deeper-than-expected impact from foreign exchange. But “look past the FX headwinds & you’ll see why everyone is hiding in Apple,” he said.

Rakers rates the stock at overweight with a $185 price target.

Evercore ISI’s Amit Daryanani called Apple “the last FAANG standing.”

“Overall, revenue and EPS estimates will shift higher from current levels and given the broadly disappointing EPS calls from big tech this was an impressive set of numbers and guide,” he wrote in his note to clients.

Though Apple didn’t give formal financial guidance, it offered various pieces of commentary around the December quarter, including that it could see a 10-point headwind from foreign exchange in the period and recognize a “few hundred” basis points of impact from an extra week being added to the quarter, even as Mac revenue is set for a substantial decline.

“All this results in our assessment that revenue growth will be mid-single digits (our model is at 5% vs. Street was at 2%),” Daryanani wrote.

Admittedly, it’s not just about the December quarter, he noted.

“Eventually the question will be on durability of demand beyond Dec-qtr and the impact from macro not just on iPhones but also services,” Daryanani wrote, though he likes Apple’s long-term potential to grow sales at a mid- or high-single-digit clip and grow earnings at a mid- to low-teens rate.

He rates the stock at outperform with a $190 target.

Wedbush’s Dan Ives wrote that Apple was “the one bright spot” amid “a horror show week for Big Tech earnings.”

“Given the perfect storm of currency/macro this quarter, we would characterize Apple’s results and commentary around the December quarter as net bullish around underlying demand and help throw out the noise that iPhone 14 upgrades are slowing in this cycle,” he wrote, while keeping an outperform rating but cutting his price target to $200 from $220 to reflect a lower multiple.

The latest results could help change what Citi Research analyst Jim Suva said was a relatively negative attitude towards Apple’s stock when compared to the rest of Big Tech.

“The amount of investor negativity on mega-cap tech stocks, especially Apple, is well known as recent surveys show Apple as the least favored stock amongst its peers,” he wrote. “Yes there are valid concerns of electronic retailers working down inventory and consumers having less disposable income given inflation but we believe consumers will adjust their spending allocations and continue to spend on Apple’s growing platform of products and services.”

He rates the stock a buy with a $175 price target, down from $185 before.

Barclays analyst Tim Long stayed more cautious.

“Stepping back from the print, things get tougher heading into Dec-Q and beyond and we maintain our [equal-weight] rating, mainly on headwinds sustaining current demand levels as high-end consumers potentially weaken, tougher comps on Mac, Services weakening further, regulatory overhang (App Store, Google TAC), macro impacting digital advertising as well as a rich valuation,” he wrote as he bumped his price target up by a dollar to $156.

Whether that plays out in the shares is another question.

“Near term, we expect heightened macro uncertainty to remain an overhang for the stock, although some may view AAPL as a relative safe haven in the macro storm,” Long continued.

At the end of a woeful week for Big Tech earnings, Apple Inc. managed to top expectations on revenue and earnings with the help of Macs selling at a record pace during the back-to-school season, which outweighed a slight miss on iPhone sales.

Apple AAPL, -3.05%

shares bounced between slight gains and losses in after-hours action Thursday, even as executives projected that revenue growth could slow in the holiday quarter. As has been the case throughout the COVID-19 pandemic, Apple executives declined to offer a traditional financial forecast, but Chief Financial Officer Luca Maestri told investors on a conference call that they expect a sequential slowdown in growth during the December quarter, driven in part by sharp currency impacts, tough comparisons for the Mac business and pressures on the services business.

The smartphone giant’s revenue grew 8% in its fiscal fourth quarter, to $90.1 billion from $83.4 billion a year earlier, and came in ahead of the FactSet consensus of $88.7 billion. Apple generated $42.6 billion in its biggest business, iPhone sales, up from $38.9 billion a year before, but analysts were projecting $43.0 billion.

A big driver of the upside came from Apple’s AAPL, -3.05%

Mac segment, which posted a massive beat even as iPhone sales came up light. The Mac business set an all-time quarterly revenue record at $11.5 billion in the back-to-school quarter, up from $9.2 billion a year before and easily above the FactSet consensus, which called for $9.3 billion.

Chief Executive Tim Cook explained on the call that the Mac category benefited from the launch of the MacBook Air with Apple’s custom M2 chip, as well as easing supply constraints that allowed Apple to meet a prior demand backlog. Maestri said he expects that Mac revenue will “decline substantially” on a year-over-year basis in the December quarter, however, as that period faces tough comparisons.

The company is supply-constrained on the iPhone 14 Pro and iPhone 14 Pro Max models, Cook said, adding that it is difficult for the company to “determine the accurate mix” of its phones until it is able to fulfill all of its demand.

Revenue performance across Apple’s product lines was mixed. While Mac sales were strong, iPad revenue fell to $7.2 billion from $8.3 billion, whereas analysts were modeling $7.8 billion in iPad revenue. That category saw “opposite” trends relative to the Mac business in that iPads were up against an “exceptionally strong iPad quarter” from a year before that included a product launch.

The company raked in $9.7 billion in revenue across its wearables, home and accessories category, up from $8.8 billion in the same period a year ago. Analysts had expected revenue of $9.2 billion.

Services revenue climbed to $19.2 billion from $18.3 billion but fell short of the FactSet consensus, which was for $20.0 billion. Maestri shared that while he expects the segment to grow in the December quarter, the business could be impacted by pressures on advertising and gaming, as well as foreign-exchange effects.

For the latest quarter, Apple recorded net income of $20.7 billion, or $1.29 a share, compared with $20.6 billion, or $1.24 a share, in the year-earlier period. Analysts tracked by FactSet were expecting $1.27 a share in earnings.

If Apple’s stock managed to hold gains through Friday’s close, it would likely be the only Big Tech company to see positive post-earnings stock performance this week. Shares of Microsoft Corp. MSFT, -1.98%,

Alphabet Inc. GOOG, -2.34%

GOOGL, -2.85%,

and Meta Platforms Inc. META, -24.56%

each posted sharp declines in the session after their respective reports, and Amazon.com Inc. AMZN, -4.06%

shares were off 12% in late trading Thursday.

Shares of Apple have lost 18% so far this year, as the Dow Jones Industrial Average DJIA, +0.61%

— which counts Apple as one of its 30 components — has declined 12%.

Apple Inc. joined the chorus of Big Tech woes Thursday, falling short of expectations on quarterly iPhone sales and sending its stock lower in late trading.

The smartphone giant delivered $90.1 billion in fiscal fourth-quarter revenue, up from $83.4 billion a year earlier and ahead of the FactSet consensus, which was for $88.7 billion. A big driver of the upside came from Apple’s AAPL, -3.05%

Mac business, which posted a massive beat even as iPhone sales came up light.

Apple generated $42.6 billion in iPhone sales during its latest quarter, up from $38.9 billion a year before, while analysts were projecting $43.0 billion.

The stock was down 1% to 4% in after-hours trading immediately following the release of the report Thursday.

As has been the case throughout the pandemic, Apple declined to offer a financial forecast in its release, so investors will need wait for the company’s earnings call to get a sense for how things have fared since the September quarter ended and what expectations are like going into the holiday period.

A key question coming into Apple’s report was how demand for the company’s new iPhone 14 line has held up, especially given reports that the company has scaled back earlier production goals. While the company isn’t likely to offer a traditional quantitative outlook on the call, executives could give some indication of how consumer behavior has played out recently amid the backdrop of economic pressure and more incremental upgrades within the newest family of iPhones.

For the latest quarter, Apple recorded net income of $20.7 billion, or $1.29 a share, compared with $20.6 billion, or $1.24 a share, in the year-earlier period. Analysts tracked by FactSet were expecting $1.27 a share in earnings.

Revenue performance across Apple’s product lines was mixed. The company saw $11.5 billion in Mac revenue, up from $9.2 billion a year prior, along with $7.2 billion in iPad revenue, down from $8.3 billion. Analysts tracked by FactSet were modeling $9.3 billion for the Mac line and $7.8 billion in iPad revenue.

The company raked in $9.7 billion in revenue across its wearables, home and accessories category, up from $8.8 billion in the same period a year ago. Analysts had expected revenue of $9.2 billion.

Services revenue climbed to $19.2 billion from $18.3 billion but fell short of the FactSet consensus, which was for $20.0 billion.

Shares of Apple have lost 18% so far this year, as the Dow Jones Industrial Average DJIA, +0.61%

— which counts Apple as one of its 30 components — has declined 12%.

Meta Platforms CEO Mark Zuckerberg speaks at Georgetown University in Washington on Oct. 17, 2019.

Andrew Caballero-Reynolds | AFP | Getty Images

Apple recently updated its App Store guidelines with changes that, yet again, impact Facebook’s ad business.

The new rule, introduced Monday, says that companies like Meta, which owns Facebook and Instagram, can offer apps that allow people to buy and manage advertising campaigns in dedicated apps without using Apple’s payment system, but it considers buying an ad in a social media app to be a digital purchase, from which Apple takes a 30% cut.

Meta wasn’t happy with the change. A Meta spokesperson told CNBC, “Apple continues to evolve its policies to grow their own business while undercutting others in the digital economy.”

The episode is the latest skirmish from companies like Meta that feel that Apple has too much power over mobile distribution and the ever expanding and changing rules of Apple’s App Store, which is the only way to install apps on an iPhone.

Meta and Apple have been battling for years, but the rivalry has grown more heated recently after Apple introduced App Tracking Transparency in the iPhone operating system last year. The privacy feature allows users to decline to offer app developers like Meta a unique device ID that can be used to track ad performance. Meta says the change could cost it $10 billion this year.

Meta and Apple also appear poised to compete in the world of consumer hardware, after Meta released the Quest Pro headset and Apple has been developing a competing VR headset for years that could reportedly launch next year.

Apple told CNBC that even before the new guideline the company considered social boosts to be the kind of digital purchase that needed to use Apple in-app purchases, and that the rule is more of a clarification than a new restriction.

“For many years now, the App Store guidelines have been clear that the sale of digital goods and services within an app must use In-App Purchase,” an Apple spokesman told CNBC. “Boosting, which allows an individual or organization to pay to increase the reach of a post or profile, is a digital service — so of course In-App Purchase is required. This has always been the case and there are many examples of apps that do it successfully.”

This individual restriction has long been a sticking point, and Meta, back when it was still named Facebook, negotiated with Apple over social media boosts and whether they would fall under Apple’s digital purchase rules, according to The Wall Street Journal.

Boosting features are offered by several social media companies. But most, like Twitter, already use Apple’s in-app purchase mechanism that lists boosted posts for $9.99 on Apple’s App Store. TikTok sells coins, or a currency used to promote posts, through in-app purchases as well.

For Meta, it thinks Apple’s recent clarification crosses a line in taking a piece of advertising revenue, not just app sales. Meta points to previous Apple executive statements, some made as part of the Epic Games trial over App Store rules, where it said it didn’t take a cut of ads.

“Apple previously said it didn’t take a share of developer advertising revenue, and now apparently changed its mind. We remain committed to offering small businesses simple ways to run ads and grow their businesses on our apps,” the Meta spokesperson told CNBC.

Apple isn’t asking for a cut of every ad served through the Facebook or Instagram apps. But Meta clearly feels targeted by Apple’s increasing power over its platforms, and worries that the company could argue that it deserves a piece of Meta’s total ad sales through its ads manager app, according to The Verge, which first reported Meta’s complaint.

It’s unclear how big the boost market is. Most big advertisers use dedicated portals or apps to buy ads. Eric Seufert, an ads industry watcher and the founder of Mobile Dev Memo, wrote Monday that he suspects it is a “negligible proportion of revenue” to the social media companies.

In a new proposed settlement, the Federal Trade Commission is seeking to hold a tech CEO accountable to specific security standards, even if he moves to a new company.

The agency announced Monday that its four commissioners had voted unanimously to issue a proposed order against alcohol delivery platform Drizly and its CEO James Cory Rellas for allegedly failing to implement adequate security measures, which eventually resulted in a data 2020 breach exposing personal information on about 2.5 million consumers.

The FTC claims that despite being alerted to the security concerns two years before the breach, Drizly and Rellas did not do enough to protect their users’ information.

While settlements like this are not that uncommon for the FTC, its decision to name the CEO and have the stipulations follow him beyond his tenure at Drizly exemplifies an approach favored by Democratic Chair Lina Khan. Some progressive enforcers have argued that naming tech executives in their lawsuits should create a stronger deterrence signal for other potential violators.

The proposed order, which is subject to a 30 day public comment period before the commission votes on whether to make it final, would require Rellas to implement an information security program at future companies where he’s the CEO, a majority owner or a senior officer with information security responsibilities, provided the company collects consumer information from more than 25,000 people.

Though Republican Commissioner Christine Wilson voted with the agency’s three Democrats to impose the proposed settlement against Drizly, she objected to naming Rellas as an individual defendant. In a statement, Wilson wrote that naming Rellas will not result in putting “the market on notice that the FTC will use its resources to target lax data security practices.”

“Instead, it has signaled that the agency will substitute its own judgement about corporate priorities and governance decisions for those of companies,” she wrote, adding that given CEOs’ broad overviews of their businesses, it’s best left to companies rather than regulators to determine what the chief executive should pay regular attention to.

In a joint statement, Khan and Democratic Commissioner Alvaro Bedoya responded to Wilson’s argument, writing that “Overseeing a big company is not an excuse to subordinate legal duties in favor of other priorities. The FTC has a role to play in making sure a company’s legal obligations are weighed in the boardroom.”

The order against Drizly would also require the company to destroy personal data it has collected but no longer needs, limit future data collection and establish a comprehensive security program including training for employees and controls on who can access data.

“We take consumer privacy and security very seriously at Drizly, and are happy to put this 2020 event behind us,” a Drizly spokesperson said in a statement.

Shoppers queue in like outside the Apple store during the launch day of the new iPhone 14 series smartphones in Hong Kong, on September 16, 2022.

Miguel Candela | Anadolu Agency | Getty Images

The closely-watched consumer price index continues to show headline inflation in the U.S. hovering at levels last seen in the mid-1980s.

Prices for a wide variety of goods and services, including food, airfare, and gasoline rose in the latest reading released last week. All told, on a 12-month basis, headline inflation was up 8.2%, according to the Bureau of Labor Statistics, which publishes the CPI.

But one product category monitored by the CPI recorded a 22% plunge, showing deflation: Smartphones.

That might seem counterintuitive. Most phones are expensive and prices for the best ones aren’t going down. Apple released new iPhones in September at the same U.S. prices as last year’s options, for example. And Samsung’s high-end devices cost as much as $1,800 this year. Average selling prices for smartphones continue to climb in markets around the world.

It turns out, smartphones aren’t getting cheaper. They’re getting better. And that’s why CPI shows them deflating instead of inflating like lots of other goods.

Here’s why: Normally, the CPI likes to compare prices for identical items which don’t change much from year-to-year. So, it might compare eggs against eggs, for example. But in the case of smartphones, BLS has to control for devices that get better each year. If smartphones are improving and the price is staying the same, then BLS records a price decline.

“There’s been a lot of declines in the [smartphone] index. And that’s really just in large part dealing with the quality improvements,” said Jonathan Church, an economist at BLS.

Twice a year, BLS looks at the new smartphone models and measures how they’ve improved — whether they have better cameras, displays, or other new methods.

“For smartphones, we’re talking about things like screen size, RAM, processor speed, phone camera or rear camera, whether it’s foldable, or things like that,” Church said.

Then, BLS makes a “quality adjustment.” If the price of the new iPhone didn’t rise, but it received new features, then the CPI would consider that device to be more valuable than the old one, and it assumes consumers get more value for the same money.

Estimating the size of the quality adjustments is done with a hedonic modeling method and BLS uses data from a third-party dataset that includes smartphone specs.

Or, as BLS puts it: “If a replacement smartphone is different from its predecessor and the value of the difference in quality can be accurately estimated, a quality adjustment can be made to the previous item’s price to include the estimated value of the difference in quality.”

BLS has indexed smartphone technologies to a starting point in late 2019, when Apple’s newest device was the iPhone 11 and Samsung’s best was the Galaxy S10. In fact, smartphone prices have been deflating since 2019, according to the CPI.

Eventually, Church said, smartphones may mature into the kind of product that would see price increases and inflation. But the rate of improvement would have to slow down.

“It’s really only that a certain mature point in the cycle that their price will start to go up again,” Church said. “It seems pretty early in the lifecycle still, smartphones in general.”

This may surprise you: Wall Street analysts expect earnings for the S&P 500 to increase 8% during 2023, despite all the buzz about a possible recession as the Federal Reserve tightens monetary policy to quell inflation.

Ken Laudan, a portfolio manager at Kornitzer Capital Management in Mission, Kan., isn’t buying it. He expects an “earnings recession” for the S&P 500 SPX, +2.78%

— that is, a decline in profits of around 10%. But he also expects that decline to set up a bottom for the stock market.

Laudan’s predictions for the S&P 500 ‘earnings recession’ and bottom

Laudan, who manages the $83 million Buffalo Large Cap Fund BUFEX, -2.86%

and co-manages the $905 million Buffalo Discovery Fund BUFTX, -2.82%,

said during an interview: “It is not unusual to see a 20% hit [to earnings] in a modest recession. Margins have peaked.”

The consensus among analysts polled by FactSet is for weighted aggregate earnings for the S&P 500 to total $238.23 a share in 2023, which would be an 8% increase from the current 2022 EPS estimate of $220.63.

Laudan said his base case for 2023 is for earnings of about $195 to $200 a share and for that decline in earnings (about 9% to 12% from the current consensus estimate for 2022) to be “coupled with an economic recession of some sort.”

He expects the Wall Street estimates to come down, and said that “once Street estimates get to $205 or $210, I think stocks will take off.”

He went further, saying “things get really interesting at 3200 or 3300 on the S&P.” The S&P 500 closed at 3583.07 on Oct. 14, a decline of 24.8% for 2022, excluding dividends.

Laudan said the Buffalo Large Cap Fund was about 7% in cash, as he was keeping some powder dry for stock purchases at lower prices, adding that he has been “fairly defensive” since October 2021 and was continuing to focus on “steady dividend-paying companies with strong balance sheets.”

Leaders for the stock market’s recovery

After the market hits bottom, Laudan expects a recovery for stocks to begin next year, as “valuations will discount and respond more quickly than the earnings will.”

He expects “long-duration technology growth stocks” to lead the rally, because “they got hit first.” When asked if Nvidia Corp. NVDA, +6.14%

and Advanced Micro Devices Inc. AMD, +3.69%

were good examples, in light of the broad decline for semiconductor stocks and because both are held by the Buffalo Large Cap Fund, Laudan said: “They led us down and they will bounce first.”

Laudan said his “largest tech holding” is ASML Holding N.V. ASML, +3.79%,

which provides equipment and systems used to fabricate computer chips.

Among the largest tech-oriented companies, the Buffalo Large Cap fund also holds shares of Apple Inc. AAPL, +3.09%,

Microsoft Corp. MSFT, +3.88%,

Amazon.com Inc. AMZN, +6.63%

and Alphabet Inc. GOOG, +3.91%

Laudan also said he had been “overweight’ in UnitedHealth Group Inc. UNH, +1.77%,

Danaher Corp. DHR, +2.64%

and Linde PLC LIN, +2.25%

recently and had taken advantage of the decline in Adobe Inc.’s ADBE, +2.32%

price following the announcement of its $20 billion acquisition of Figma, by scooping up more shares.

Summarizing the declines

To illustrate what a brutal year it has been for semiconductor stocks, the iShares Semiconductor ETF SOXX, +2.12%,

which tracks the PHLX Semiconductor Index SOX, +2.29%

of 30 U.S.-listed chip makers and related equipment manufacturers, has dropped 44% this year. Then again, SOXX had risen 38% over the past three years and 81% for five years, underlining the importance of long-term thinking for stock investors, even during this terrible bear market for this particular tech space.

Here’s a summary of changes in stock prices (again, excluding dividends) and forward price-to-forward-earnings valuations during 2022 through Oct. 14 for every stock mentioned in this article. The stocks are sorted alphabetically:

You can click on the tickers for more about each company. Click here for Tomi Kilgore’s detailed guide to the wealth of information available free on the MarketWatch quote page.

The forward P/E ratio for the S&P 500 declined to 16.9 as of the close on Oct. 14 from 24.5 at the end of 2021, while the forward P/E for SOXX declined to 13.2 from 27.1.