MicroStrategy will release software applications and solutions powered by the Bitcoin Lightning Network in 2023.

MicroStrategy executive chairman Michael Saylor spoke about his company’s plans in a Twitter Spaces room on Wednesday, shedding light on some of the offerings currently in the works at the software firm.

Saylor mentioned that as part of his transition from CEO to executive chairman, the company’s Bitcoin arm has been able to have a deeper focus on ways it can not only buy and hold BTC but also contribute to the ecosystem. As it seeks to branch out of regular software applications and into Bitcoin, MicroStrategy can leverage its existing knowledge to provide enterprises with tooling for the Bitcoin and Lightning ecosystem.

“We want to make it possible for any enterprise to spin up Lighting infrastructure in an afternoon” and onboard thousands of employees or customers, Saylor explained. “We want to plug it into enterprise technology and make it a marketing strategy for any forward thinking CMO.”

Areas that MicroStrategy is exploring for Lightning services include online content monetization, enterprise marketing, web paywalls, and internal corporate controls. Every chief marketing officer should be able give away satoshis –– Bitcoin’s smaller denomination unit –– as incentive for customers to post reviews or give feedback, Saylor said.

“We have teams working on it and are looking to bring something out by next year. We expect to show something in the first quarter.”

Saylor also said in the Twitter Spaces conversation that MicroStrategy’s upcoming Bitcoin event will feature a “Lightning for corporations” agenda, which should dive deeper into the company’s plans for how it wants to explore and contribute to the ecosystem and drive greater adoption.

Michael Saylor’s MicroStrategy bought 2,395 BTC for $42.8 million in cash between Nov. 1 and Dec. 21, 2022.

It then sold 704 BTC at a loss on Dec. 22 to offset previous capital gains.

MicroStrategy then bought 810 BTC on Dec. 24.

Software analytics company MicroStrategy has sold bitcoin for the first time since it first began adding the digital currency to its treasury in 2020.

The sale took place on December 22, 2022, according to a filing with the U.S. Securities and Exchange Commission (SEC). The move was carried out in order to generate a net tax benefit, as the losses involved in the sale are able to offset previous capital gains, per the filing. Two days later, MicroStrategy bought back more bitcoin than it sold, however at a higher price –– $16,845 per BTC on the 810 bitcoin purchase vs. $16,776 on the 704 bitcoin sale.

A larger purchase preceded the sale. MicroStrategy bought 2,395 bitcoin between November 1 and December 21, 2022, before embarking on the tax-loss harvesting strategy. The purchase cost about $42.8 million, translating to an average price of $17,871 per bitcoin, inclusive of fees and expenses.

Ultimately, the transactions resulted in an increase of MicroStrategy’s bitcoin holdings by 2,500 BTC. The company led by Michael Saylor now holds 132,500 BTC, acquired for about $4.03 billion at an average price of $30,397 per bitcoin. As a result, the Virginia-based firm currently faces an unrealized loss of over $1.8 billion.

Bitcoin users place a higher importance on a politician’s BTC-related policies and agenda than their party, a survey by Bitcoin Magazine has found. Over 72% of respondents said they would vote for a pro-Bitcoin candidate even if they were not part of their preferred political party.

The first edition of Bitcoin Magazine’s annual survey, which collected responses from over 6,600 Bitcoin holders from August 15 to October 19, 2022, also found that the majority of them considered themselves Bitcoin maximalists (56.2%). However, over 68% of respondents also own other cryptocurrencies. Interestingly, 60% said they would prefer to buy products from Bitcoin-only companies.

Intended for gathering feedback from the community on Bitcoin Magazine’s existing content as well as to better understand user’s preferences, the survey shed light on many interesting aspects of the Bitcoin community and its members.

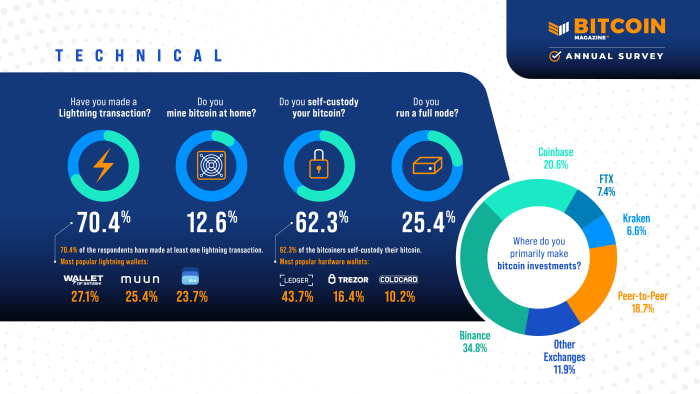

Three quarters of respondents purchase bitcoin through regulated exchanges, with top choices being Binance (34.8%), Coinbase (20.6%), FTX (7.4%) and Kraken (6.6%). FTX’s preference is naturally bound to drop near zero following the exchange’s filing for bankruptcy less than one month after the survey. Peer-to-peer (P2P) trading, which more closely resembles Bitcoin’s intended design of transactions without intermediaries, was shown to be a strategy for only 18.7% of the surveyed users.

Adoption of the Lightning Network, Bitcoin’s overlay network for faster and cheaper transfers, was found to be strong. Of all respondents, 70.4% shared that they have made at least one Lightning payment. The preferred wallets of users were Wallet of Satoshi (27.1%), Muun Wallet (25.4%) and Blue Wallet (23.7%).

When it comes to mining, participation was unsurprisingly more shy. Likely due to the technical complexity in setting up an ASIC miner at home, only 12.6% of respondents said they mined bitcoin at home. That’s about half of the percentage of those who run their own nodes –– more than a quarter of respondents (24.5%).

The majority of respondents self-custody their BTC, the survey found, amounting to 62.3% of users. The preferred hardware wallets are Ledger (43.7%), Trezor (16.4%) and Coldcard (10.2%).

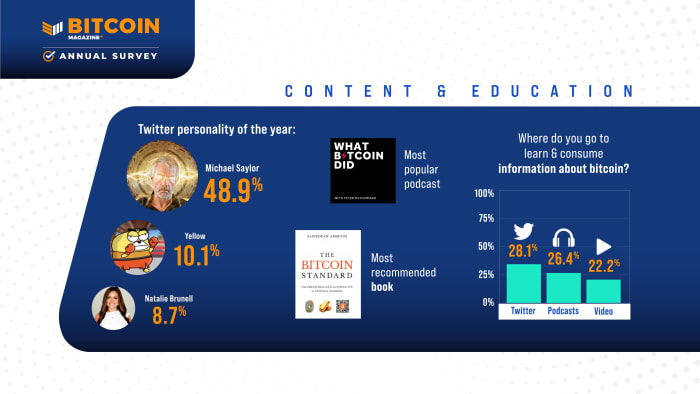

When it comes to learning and consuming industry information, the survey found Twitter as the main channel, with 28.1% of respondents saying that’s where they went primarily. Respondents elected Michael Saylor as the Twitter personality of the year (48.9%), followed by Yellow (10.1%) and Natalie Brunell (8.7%). Podcasts came in close second (26.4%), with the most popular of them being Peter McCormack’s “What Bitcoin Did.” Video trailed in third (22.2%). While not many respondents mentioned books as their main source of information, the most widely recommended text about Bitcoin was The Bitcoin Standard by Saifedean Ammous.

When the business is passing on Satoshi’s torch, the survey found that most Bitcoin users introduce their friends to bitcoin (70%), while some also share the good word with their parents (31.5%). Only 17.3% of respondents didn’t advocate for Bitcoin at all and preferred instead to keep quiet on the matter.

This is an opinion editorial by Tim Niemeyer, a Bitcoiner since circa-2018 and co-host of the Lincolnland Bitcoin Meetup in Springfield, Illinois.

Amidst the carnage of the FTX drama, a moment of clarity illuminated the Twittersphere. Michael Saylor’s words were the signal in the noise resulting from the dysfunctional trainwreck unaffectionately known as “crypto”. Before we can truly appreciate his insights, we should first meditate on what makes this relationship dysfunctional or, in the context of couples therapy, a toxic relationship.

While many in the cryptocurrency industry were happily going about their life viewing their relationship with money (trust, commitment, support, etc.) in a positive light, they were ignoring the warning signs that their relationship was anything but healthy. Sure, all good relationships have their ups and downs. Disagreements happen, but overall you share common goals and trust the other to have your best interests at heart. There’s a certain level of expectation that your partner will support you, communicate openly and honestly, and refrain from controlling behaviors. Life this way is freeing and you’re generally able to flourish.

But what if one side doesn’t have your best interests at heart? What if they are dishonest? What if there becomes a pattern of disrespect? What if they ignore your needs? Sure, you can hope for change, but you still feel drained, stressed, anxious, or depressed. Eventually, you want out. Your need for a positive, healthy relationship overwhelms the comfort of the known, current relationship. The first step is admitting there’s a problem. Acknowledging signs of a toxic relationship are necessary.

Signs Of A Toxic Relationship

In regards to our relationship with money, support may be displayed in many ways. One way we support each other is through the ability to trust that our counterpart has our best interests at heart. The overwhelming problem with the cryptocurrency sphere (defined here as everything other than Bitcoin) is that it’s still largely based on an expectation of trust. Whether it’s FTX, Celsius, LUNA or the countless other scams and Ponzis that are sewn into the fabric of the cryptocurrency industry, it’s clear that having centralized entities controlling your value requires you trust the fallible seamstresses and their incentives. It’s like the trust fall; an exercise in which one person lets him- or herself fall without trying to stop it, relying on their friend(s) to catch them. How many times do you allow yourself to fall to the ground before you lose trust?

These recent fallouts in crypto continue to illuminate the inherent dishonesty in its DNA. Investors are deceived into a false sense of security in the relationship; it’s a form of dishonest communication based on non-transparency and the over-leveraged nature of exchanges. Allowing humans to control money allows controlling behaviors to be coded into the system, which leads to growing resentment in the relationship … The relationship is further strained when the toxic side puts their needs ahead of your own. The needs of some CEOs often incentivize them into leveraging the customers’ trust to benefit their gain. This display of negative financial behaviors is becoming all too common in the cryptocurrency industry (again, non-Bitcoin-only entities). At some point, as my father would say, we need to separate the wheat from the chaff.

Steps To Fix A Toxic Relationship

The first step is to accept responsibility. Not that you caused the situation per se, but that you acknowledge the situation you’re in and begin advocating for yourself. This can be done by investing in yourself. In the context of this article, that investment is education in Bitcoin as well as understanding the unintended consequences of adopting a “digital fiat” mindset present throughout the altcoin and centralized exchange industries. Once we shift from blaming to understanding, we allow ourselves to begin healing. The pain resulting from the recent developments will linger for a while, but it is our responsibility to not dwell on the past but move forward with compassion. The next step in the journey to healing is allowing yourself to be vulnerable again. This can be attained by sharing your self-love with others; calmly and clearly explaining the benefits of Bitcoin, self-custody and proof of reserves to friends and family.

People recovering from a toxic relationship can benefit from finding support. It is the opinion of the author that Bitcoiners should be that support structure. It’s ironic that many Bitcoiners are known as the toxic ones when they are the ones trying to illuminate the toxicity inherent in the ecosystem. That being said, an “I told you so,” doesn’t assist in the healing process. This is the moment where we must rise above and lead with compassion. We should hold space in our heart and allow others the time to heal and change.

There will be many who do not recover from a toxic relationship of this magnitude. While we can continue to educate from a place of humility, we must remember that, “You can lead a horse to water, but you can’t make it drink.” Everyone will ultimately heal in their own way at their own pace. Some may never learn. We’ve probably all had a friend who’s jumped from one toxic relationship to another. As much as you may want to help, they need to first choose to help themselves. Even more, some people will continue to “Tinder around” with unhealthy cryptocurrency relationships. That’s their prerogative. If a friend of ours wants to be part of the hookup culture, that’s on them. They have to deal with the consequences of STDs and the like.

Regardless of the actions of certain exchanges or crypto in general, we must continue to espouse the benefits of Bitcoin in a positive light. Tell them how truth is born from trustlessness. Demonstrate how actual decentralization leads to pure democracy. Illuminate how immutability and permissionless systems allow for a free-flowing, cooperative society. Michael Saylor acutely recognized the toxicity we are allowing to proliferate through the perceived connection to crypto. We must choose to move forward towards a bitcoin standard for ourselves, our friends and family, and, ultimately, for society to flourish.

This is a guest post by Tim Niemeyer. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

MIAMI, FLORIDA – JUNE 04: MicroStrategy CEO Michael Saylor speaks at the Bitcoin 2021 Convention (Photo by Joe Raedle/Getty Images)

Getty Images

What Happened

MicroStrategy has been purchasing bitcoin since 2020 as a part of its capital allocation strategy. The company holds over 120,000 BTC as of the end of December 2021. As a U.S. public company, MicroStrategy is required to report earnings and transactions related to bitcoin under Generally Accepted Accounting Principles (GAAP) standard. However, properly accounting for these transactions in GAAP financial statements is an emerging area. The current GAAP standards that classify digital assets as intangible assets with indefinite lives (similar to goodwill and trademarks of a business), fail to capture the true financial behavior of bitcoin holdings. This treatment requires companies to report a loss when digital assets’ prices fall below the cost; however it prohibits marking up digital assets to it’s true value when prices later recover. This discrepancy can negatively impact a company’s net income, which could incorrectly translate into lower price per share.

The Financial Accounting Standards Board (FASB) is the IRS of the accounting world. The FASB is responsible for creating Generally Accepted Accounting Principles (GAAP). As of the date of posting, there are still no cryptocurrency specific GAAP rules.

In the absence of these crypto specific rules set by the FASB, in 2020, a working group formed by the American Institute of CPAs (AICPA) came up with a Digital Asset Practitioner Guide addressing how to classify cryptocurrencies in GAAP financial statements.

How Cryptocurrencies are Classified on GAAP Financials

According to the white paper issued by the AICPA, crypto assets cannot be classified as “cash or cash equivalents” on GAAP financial statements because they are not backed by a sovereign government or considered legal tender. They cannot be classified as a financial instrument or a financial asset because they are not cash (see above why) and do not represent any contractual right to receive cash or another financial instrument. Additionally, since cryptocurrencies are intangible, they do not clearly meet the definition of inventory and cannot be labeled as inventory on the balance sheet either.

After going through the process of elimination, we are left with only one category to classify cryptocurrencies under: intangible assets with indefinite life. This is how MicroStrategy currently classifies bitcoin in their financial statements.

(3) Digital Assets: The Company accounts for its digital assets as indefinite-lived intangible assets in accordance with Accounting Standards Codification (“ASC”) 350, Intangibles—Goodwill and Other. The Company’s digital assets are initially recorded at cost. Subsequently, they are measured at cost, net of any impairment losses incurred since acquisition” (10-Q, page 11)

Practical Mismatches with Intangible Asset Treatment

There are a few problems with classifying cryptocurrencies as intangible assets with indefinite life. Practically speaking, this accounting treatment does not align with the reality. Cryptocurrencies like bitcoin are liquid and work extremely similar to cash. The purpose of GAAP financial statements is to paint an accurate, unbiased picture of the underlying entity’s financial situation. By treating crypto assets as intangible assets, GAAP financials fails to communicate the high liquidity of crypto assets.

Second, once an item is classified as an indefinite life intangible asset, it should be tested for impairment. This means, if the value of the crypto asset has gone down at the end of the reporting period, the business gets to write off that amount as an impairment loss (not to be confused with tax losses) on the income statement. However, if the value goes back up (which is common due to high volatility), the business does NOT get to mark up the value of the asset. This overly conservative approach often results in businesses showing poor operating results under GAAP which negative affects investor sentiment and stock price.

For example, MicroStrategy reported $65,165,000 of impairment losses for the three months ending September 30, 2021, because the market value of bitcoins went below their purchase price. Although this 65M impairment loss was not a cash outflow from the business, it was the largest operating expense which contributed to a net loss of $36,136,000.

Similarly, during the three months ending September 30, 2021, Tesla reported 51M of impairment loss. Square reported 6M of bitcoin impairment loss in the same period.

MicroStrategy consolidated statement of operations

MicroStrategy

To clarify the situation and show the true performance of the business to investors, MicroStrategy added a section named, “Non-GAAP Financial Measures” in their 10-Q. This section shows what would their operating income be without taking impairment and few other non-GAAP amounts (not related to digital assets) into consideration.

According to this schedule, if impairment loss was not considered (and few other items not relevant to bitcoin), the company would have a net income of $18,566,000.

Reconciliation of non-GAAP net income schedule

MicroStrategy

SEC Letter to MicroStrategy

The SEC objected MicroStrategy’s Reconciliation of non-GAAP net income schedule above. On December 3, 2021, it sent the company a comment letter and advised the company to remove it under the Rule 100 of Regulation G.

Reg G requires public companies to “disclose or release such non-GAAP financial measures to include, in that disclosure or release, a presentation of the most directly comparable GAAP financial measure and a reconciliation of the disclosed non-GAAP financial measure to the most directly comparable GAAP financial measure”.

Although we don’t know the specifics of the situation, it is clear that MicroStrategy’s 10-Q includes GAAP financials & a reconciliation of non-GAAP net income schedule allowing readers to compare numbers easily. The company’s goal is to clearly communicate the true operating performance of the company minus the “paper bitcoin losses” which is required to report under incompatible GAAP rules. Therefore, the specific concern the SEC has with the presentation is unclear. It is also interesting to see that the letter is only talking about the “adjustment for bitcoin impairment charges” among other items included in the Reconciliation of non-GAAP net income schedule such as share-based compensation, interest expense and income tax effects.

On a subsequent letter from MicroStrategy dated December 16, 2021, the company accepted SEC’s comments and removed the adjustment for bitcoin impairment on the reconciliation of non-GAAP net income schedule.

Finally, the rising inflation and the uncertainly of interest rates have moved the market sentiment from investing in risky companies to value stocks of profitable companies. Microstrategy may find it challenging to show a net profit under GAAP in the coming months if the price of BTC moves sideways in a bearish market or declines further creating more impairment losses. Even when BTC goes up, Microstrategy will not be able to show a profit under GAAP unless they sell it. This situation could unfairly affect the stock price of the company. If a spot BTC ETF gets approved, investors might be better off directly investing in the ETF compared to using Microstrategy as a way to get exposure to BTC.

Next Steps

Keep an eye on how SEC approaches Non-GAAP disclosures related to bitcoin for other public companies holding bitcoin.