Gold futures ended Friday at their highest on record, with prices on the cusp if a so-called golden cross — signaling the potential for further upside in the precious metal.

Gold prices surged as the market reacted to the escalating tensions in the Middle East, said Bas Kooijman, CEO and asset manager of DHF Capital, in market commentary. The end of the truce in the region could “continue to fuel risk aversion and investors’ concerns.”

The escalation has “helped extend gold’s uptrend of the last two months as traders take into account changing expectations regarding monetary policy,” he said. “Traders have been betting on an end to the interest rate hiking cycle and possible rate cuts in the first half of next year, which could continue to support gold’s rise over the medium term.”

On Friday, gold for February delivery GC00, +0.10%

GCG24, +0.10%

climbed by $32.50, or 1.6%, to settle at $2,089.70 an ounce on Comex. Prices based on the most-active contracts, settled at an all-time high, surpassing the Aug. 6, 2020 record-high finish of $2,069.40, according to Dow Jones Market Data.

Prices traded as high as $2,095.70 on an intraday basis on Friday, surpassing the previous record intraday high of $2,089.20 from Aug. 7, 2020.

Gold’s rally started after the release of the October consumer-price index, Edmund Moy, senior IRA strategist for U.S. Money Reserve and a former director of the U.S. Mint, told MarketWatch. The data released Nov. 14 showed that the U.S. cost of living was unchanged in October.

The market viewed that reading as saying the Fed has “tamed inflation and is probably finished raising rates and will, in all probability, start reducing rates sooner and faster than previously predicted,” said Moy.

Lower Fed rates mean lower Treasury yields, and since Treasurys are purchased in dollars, falling demand for Treasurys means falling demand for the dollar, he said, which can boost the price for dollar-denominated gold.

“While gold’s current rally is a bit overheated, both the golden cross and the proximity of an all-time high acting like a magnet for the price means that we’re likely to see further gains in the very immediate term,” Brien Lundin, editor of Gold Newsletter, told MarketWatch.

Most-active gold futures on Friday were close to reaching a bullish indicator known as a golden cross, when an asset’s short-term moving average moves above its long-term moving average. The 50-day moving average was at $1,955.44, pennies below the 200-day moving average of $1,955.51 Friday.

Gold prices around the globe had already rallied to fresh record price highs in other currencies and with the U.S. dollar gold price joining the party, “you can expect another wave of buying momentum to come into the market now,” said Peter Spina, president of GoldSeek.com.

““The end of the stealth phase move of the gold bull market is over. It will finally be acknowledged and recognized by the mainstream.””

— Peter Spina, GoldSeek.com

“I fully expect significantly higher gold prices in the months ahead,” he told MarketWatch. “The end of the stealth phase move of the gold bull market is over. It will finally be acknowledged and recognized by the mainstream.”

Spina said it’s important to note that gold prices are “not hitting record highs, but rather the U.S. dollar is hitting record lows against superior money.”

That says the U.S. dollar’s purchasing power is “being eroded even further, more aggressively now,” he said. The ICE U.S. Dollar Index DXY,

a measure of the currency against a basket of six major rivals, is down 0.3% for the year to date after a November pullback.

The precious metal remains supported by Federal Reserve interest-rate cut bets even after Fed Chairman Jerome Powell signaled that it was too soon for the Fed to claim victory over the inflation beast, said Lukman Otunuga, manager, market analysis at FXTM.

The Fed’s ability to cut interest rates in March is likely to be influenced by key data including CPI and jobs data, among others,” said Otunuga. “Given how the Relative Strength Index (RSI) on the daily charts remains in overbought regions, gold could experience a technical throwback before pushing higher.”

Lundin, meanwhile, also warned that the all-time high for gold may mark a “quadruple top” unless gold is able to decisively break through a new plateau, probably somewhere over $2,100 an ounce.

Gold futures fell on Friday, as hawkish comments from Federal Reserve Chairman Jerome Powell on Thursday and weaker investor appetite for the haven metal prompted prices to post their first weekly decline since early October.

“The tailwind in gold has gone silent,” said Adam Koos, president at Libertas Wealth Management Group. The yellow metal was formerly supported, in part, by the thought that the U.S. would be hitting a ceiling on interest rates and dissipating inflation, but “none of that seems to matter under the shadow of the Fed.”

On Friday, gold for December delivery fell $32.10, or 1.6%, to settle at $1,937.70 an ounce on Comex, down 3.1% for the week, according to Dow Jones Market Data. Prices based on the most-active contract marked the biggest daily decline since mid-April and first weekly loss in five weeks.

Fed helps set overhead resistance

In remarks on a panel at the International Monetary Fund Thursday, Powell said Fed officials are “gratified” with the progress made so far to bring down U.S. inflation but weren’t yet confident that interest rates are high enough to bring inflation down to their 2% target over time.

“Gold is an inmate within the confines of overhead resistance, and the door to freedom resides at $2,060,” Koos told MarketWatch. “Just when an exit plan seems near — when a break-out with parole seems promising — Jerome Powell came in like the warden on Thursday, saying that he’s unconvinced that monetary policy has been sufficient thus far, and that inflation could still warrant future rate hikes.”

Gold prices have also been influenced by a fall in investor appetite, as fears that Middle East tensions will spill over to wider regions have eased, said Lukman Otunuga, manager, market analysis, at FXTM.

If concerns over the spread of the Middle East conflict continue to ease, that may “pave the way for further downside” in gold prices, he told MarketWatch.

However, should fears return and intensify over a potential spillover of the Israel-Hamas conflict, there may be a “fresh wave of risk aversion” that would send investors towards “safe-haven destinations” like gold, said Otunuga.

“It’s not only the developments in the Middle East, but also Russia’s invasion of Ukraine that could fan fears about a global recession,” he said.

Price potential

For now, gold has the potential to extend its losses, said Otunuga.

Ahead of Friday’s gold-price settlement, he warned that a “solid breakdown and daily close” below $1,945 would open the doors toward a fall to the 200-day simple moving average at $1,934, before the U.S. October consumer price index report on Nov. 14.

Koos, meanwhile, said gold is likely to remain in “price prison, staring at the ceiling of $2,060” an ounce, until the Fed decides to slow its role in fighting inflation.

A move beyond that price level represents “freedom and new all-time-highs,” he said. “Until then, patience will be a requirement, at the very least.”

Uranium prices have reached their highest level in more than a decade as a global supply shortage persists, with the bull market for uranium investments still in its “earliest days.”

The market is “definitely in a structural deficit as demand is growing at a 5% annual rate and the current (2023) gap between global production and consumption remains at over 50 million pounds,” Scott Melbye, executive vice president at mining company Uranium Energy Corp. UEC, +0.78%,

told MarketWatch.

Weekly spot uranium prices stood at $72.75 a pound as of Oct. 2, the highest since February 2011, according to data from nuclear-fuel consulting firm UxC, and were last at $69 as of Oct. 9. Weekly prices have climbed nearly 45% since the end of last year.

Weekly prices for uranium have climbed around 45% year to date, data from UxC show.

UxC

In late August, Jonathan Hinze, president at UxC, told MarketWatch that the market was seeing the “best set up for nuclear power expansion” that he’d ever seen. That observation still holds, he said.

It is clear that the uranium supply/demand balance remains “extremely tight, and it will likely only get tighter” in the coming 12 to 24 months as demand continues to rise, “while new supplies are taking more time to materialize, and inventories keep getting drawn down,” he said.

Since late August, financial players, including hedge and publicly traded funds active in uranium, have been quite active buying additional uranium off the spot market, said Hinze. These funds “clearly believe that prices are set to rise further, and investors are therefore adding money to their coffers to allow them to buy physical uranium.”

This is demand that isn’t fully anticipated in the market and this has added to the overall positive demand picture, he said.

Price pullback

Still, Melbye pointed out that uranium prices have pulled back a bit more recently as some traders took some “very handsome profits on their accumulated long positions.”

That pullback may have also come as an “overreaction,” he said, to news from Kazakhstan, which produced the world’s largest share of uranium from mines in 2022, according to the World Nuclear Association. Kazatomprom, Kazakhstan’s national operator for the export and import of uranium, announced in late September a return to full production in 2025 to meet global nuclear energy demand.

Melbye believes there was an overreaction in uranium prices because “this will ultimately have little impact on Western supply and demand as most analysts had them producing close to those levels by that time in their forecasts.”

Even with that production assumption, the market is “still dramatically undersupplied,” and based on Melbye’s estimation, requires eight to 10 new mines starting up globally by 2030, he said.

And while uranium has been among the best performing commodities year to date, it has only recently reached the level which “incentivizes the world’s best mines,” he said.

This bull market in uranium investments is “still in its earliest days,” said Melbye.

Among the exchange-traded funds, the Global X Uranium ETF URA

has gained more than 25% on the year through Friday afternoon, while the Sprott Uranium Miners ETF URNM

has added almost 36%. The Sprott Physical Uranium Trust SRUUF,

a closed-end fund, trades nearly 39% higher.

Broader new mine developments with significant capital investments in an inflationary environment require higher prices to move ahead, Melbye said. “Even at those levels, the long lead times needed to achieve these necessary start ups could leave the market in a short squeeze for several years.”

The recent spot market move lower in prices marks a “temporary pause, and not a peak,” he said. “Buyers should be active on this welcome dip.”

Supply ‘challenges’

Contributing to supply concerns, a July coup has disrupted mining operations in the country of Niger in West Africa. Niger produced just over 4% of the world’s uranium in 2022, according to World Nuclear News.

The coup caused borders to close, and major uranium mine and mill operation called Somair has been halted, said UxC’s Hinze. The mine, operated by the French company Orano, sells most of uranium to customers in Europe, he said.

Meanwhile, Cameco Corp. CCJ, +0.64%,

one of the world’s largest providers of uranium, said it’s encountered challenges at its mine and milling operation in Canada. The company now expects to produce nearly 3 million pounds of uranium concentrate less this year than previously anticipated, said Hinze.

“These production challenges add to the overall view that the supply/demand balance is very tight and will get even tighter,” he said.

Shares of Alcoa Corp. slumped to a multiyear low Monday as the aluminum company said that Roy Harvey had been replaced as chief executive officer after seven years in the role.

The company named William Oplinger as president and CEO, effective Sunday. Oplinger had served as Alcoa’s chief operations officer since February and before that as chief financial officer since November 2016.

Alcoa’s stock AA, -5.20%

dropped 5.1% in morning trading. That put it on track for the lowest close since March 1, 2021. It has tumbled 18% over the past three months and plunged 40.8% year to date, while the S&P 500 SPX

has rallied 12.8% this year.

“In our opinion, investors have expressed concern around cash flow and the company’s medium to long-term outlook,” B. Riley analyst Lucas Pipes wrote in a note to clients. “While the timing of the transition is somewhat unexpected, we believe Mr. Oplinger is the most well-positioned candidate for the CEO role.”

Harvey had been CEO since the company completed its separation from Arconic Inc. in November 2016. Arconic was acquired by Apollo Global Management Inc. APO, +1.55%

in a deal that was completed in August 2023.

“The transition of the president and CEO roles reflects the company’s succession planning process,” Alcoa said in a statement.

“Our board believes Bill’s extensive experience with Alcoa makes him well-positioned to carry the company forward,” said Steven Williams, Alcoa’s board chair.

B. Riley’s Pipes said that as Alcoa has faced challenging aluminum markets in recent quarters, and given the troubles associated with approvals of mine plans in Australia, he believes the change in leadership reflects the company’s desire to reposition its asset base for stronger cash-flow generation.

“While Mr. Harvey has successfully transformed Alcoa in recent years, particularly as [Alcoa] has aggressively deleveraged, we believe the transition will be viewed favorably by investors,” Pipes wrote.

Wall Street looks ready to build on Monday’s gains, the first in five sessions for the S&P 500 SPX

and Nasdaq Composite COMP.

That’s as expectations build around Nvidia, which has had a lackluster August, to knock it out of the park with earnings on Wednesday.

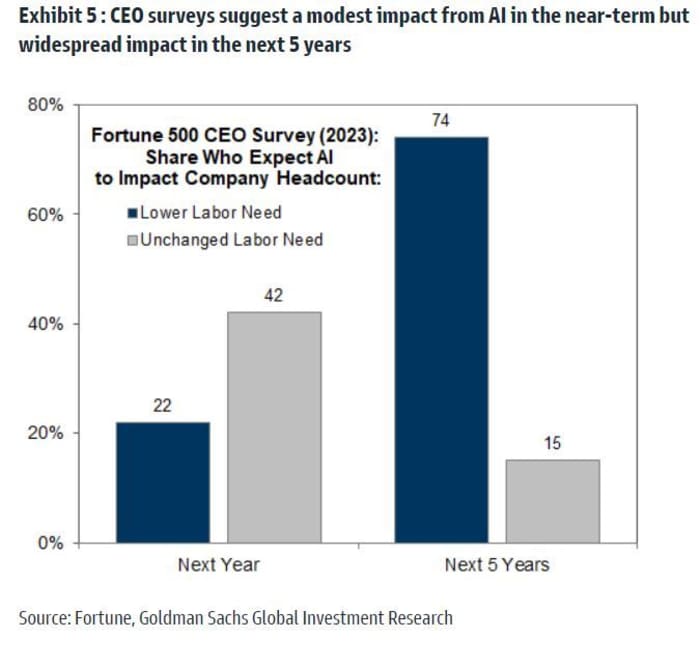

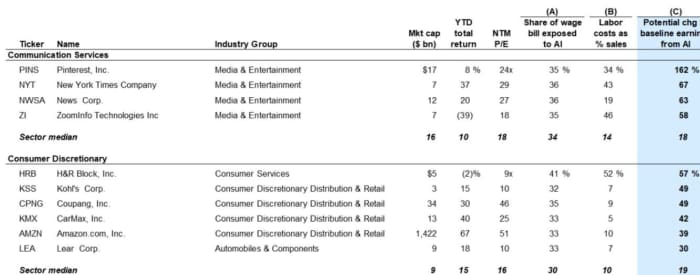

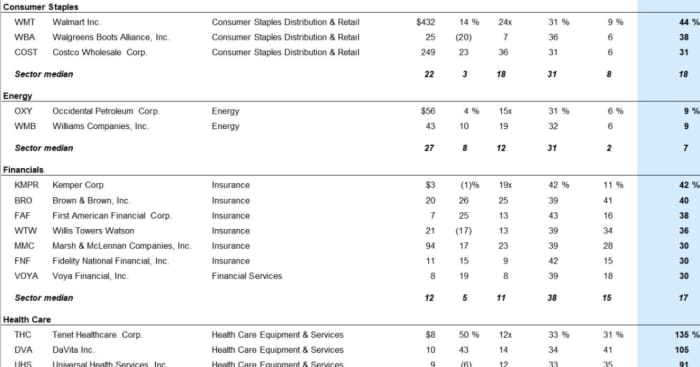

Investors have had months to focus on AI darlings such as Nvidia. In our call of the day, Goldman Sachs takes a look at stocks to trade after the big AI trade. A team led by strategists Ryan Hammond and David Kostin complied a basket of companies with the biggest potential long-term earnings per share boost from the impact of AI adoption on labor productivity.

Their analysis indicates that following widespread AI adoption, EPS for the median stock in that basket could be 72% higher than the baseline, versus 19% for the median Russell 1000 stock.

“We estimate the potential productivity-related EPS boost from increased revenues or increased margins, using a combination of company-level estimates of the share of the wage bill exposed to AI automation and the labor cost to revenue ratio,” said the Goldman team.

Since early 2023, when AI emerged as a theme for investors, they note their long-term basket of stocks has outperformed the equal-weight S&P 500 by just 6 percentage points, far less than near-term beneficiaries such as Nvidia NVDA, -0.49%,

Microsoft MSFT, +0.94%

or Meta META, +0.51%.

Goldman Sachs Investment Research

“The estimated AI-driven earnings boost is likely to occur over the next few years, but should be reflected in stock valuations sooner. However, the eventual share price impact will depend on the ability of companies to use AI to enhance earnings,” said Goldman.

While unable to pin it exactly, Goldman expects AI adoption will start to a have a “meaningful macro impact” between 2025 and 2030, with regulatory constraints and data privacy concerns likely to slow widespread adoption. Nearly 75% of CEOs see AI take-up impacting companies or cutting labor needs within the next five years, even if they don’t right now.

Firms with the biggest workforce exposure to AI and larger and more innovative ones, will likely adopt generative AI earlier than others, say the strategists. They say to “expect valuation multiples for these companies to increase first as the adoption timeline crystallizes, even if actual adoption and the associated EPS boost is occur later.”

Goldman’s estimates on the potential earnings boost for those long-term AI beneficiaries consist of several factors: the share of each company’s wage bill exposed to AI automation, how much of a company’s wage bill is exposed to AI automation and labor cost as a share of revenue.

“For the typical Russell 1000 stock, 33% of the wage bill is potentially exposed to AI automation and labor costs currently represent 14% of total sales. The potential boost from higher sales would increase earnings by 11% and reduced labor costs would increase earnings by 26%, all else equal,” say the strategists.

Here is a taster of their long-term AI beneficiaries basket:

The world’s biggest miner BHP BHP, -0.98%

reported a 58% slump in annual profit amid tumbling commodity prices in part due to China’s economic troubles. U.S.-listed shares are up 4%.

Arm Holdings filed its long-awaited IPO, which could be the year’s biggest. The chip designer aims to raise up to $10 billion with a valuation of $60 billion to $70 billion.

Existing home sales for July are due at 10 a.m., with several Fed speakers throughout the day: Richmond Fed President Tom Barkin at 7:30 a.m. and Chicago Fed President Austan Goolsbee and Fed. Gov. Michelle Bowman both at 2:30 p.m.

Is tech dancing to the beat of its own drum? The Chart Report flagged this one from Scott Brown, founder of Brown Technical Insights, showing performance of the Technology Select Sector SPDR ETF XLK

:

@scottcharts

“It’s only been a week, but consensus and conventional wisdom suggest higher yields are bad for Growth/Tech stocks. Meanwhile, Tech is acting like it never got the memo. It’s still too early to tell if Tech is trying to tell us something, but Scott points out that the sector is facing a crucial test this week at the March 2022 highs (around $163). $XLK is solidly above $163 after today’s bounce, but where it ends the week will likely hinge on $NVDA, as the company releases earnings on Wednesday evening,” says Patrick Dunuwila, editor and co-founder of The Chart Report.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Major U.S. stock indexes fell on Tuesday, with the Dow and S&P 500 both snapping a 4-session win streak, as economic data showed more signs of a sputtering U.S. economy. The Dow Jones Industrial Average DJIA, -0.59%

fell about 198 points, or 0.6%, ending near 33,403, while the S&P 500 index SPX, -0.58%

shed 0.6% and the Nasdaq Composite Index COMP, -0.52%

fell 0.5%, according to preliminary FactSet data. Investors were eyeing less robust economic data out Tuesday. The number of U.S. job openings in February fell to a 21-month low, while orders for manufactured goods fell for the third time in the past four months. Gold prices GC00, -0.04%

were flirting with a return to record territory, trading above $2,000 an ounce. The 2-year Treasury rate TMUBMUSD02Y, 3.854%

stayed below 4% at 3.84%.

David Rosenberg, the former chief North American economist at Merrill Lynch, has been saying for almost a year that the Fed means business and investors should take the U.S. central bank’s effort to fight inflation both seriously and literally.

Rosenberg, now president of Toronto-based Rosenberg Research & Associates Inc., expects investors will face more pain in financial markets in the months to come.

“The recession’s just starting,” Rosenberg said in an interview with MarketWatch. “The market bottoms typically in the sixth or seventh inning of the recession, deep into the Fed easing cycle.” Investors can expect to endure more uncertainty leading up to the time — and it will come — when the Fed first pauses its current run of interest rate hikes and then begins to cut.

Fortunately for investors, the Fed’s pause and perhaps even cuts will come in 2023, Rosenberg predicts. Unfortunately, he added, the S&P 500 SPX, -0.61%

could drop 30% from its current level before that happens. Said Rosenberg: “You’re left with the S&P 500 bottoming out somewhere close to 2,900.”

At that point, Rosenberg added, stocks will look attractive again. But that’s a story for 2024.

In this recent interview, which has been edited for length and clarity, Rosenberg offered a playbook for investors to follow this year and to prepare for a more bullish 2024. Meanwhile, he said, as they wait for the much-anticipated Fed pivot, investors should make their own pivot to defensive sectors of the financial markets — including bonds, gold and dividend-paying stocks.

MarketWatch: So many people out there are expecting a recession. But stocks have performed well to start the year. Are investors and Wall Street out of touch?

Rosenberg: Investor sentiment is out of line; the household sector is still enormously overweight equities. There is a disconnect between how investors feel about the outlook and how they’re actually positioned. They feel bearish but they’re still positioned bullishly, and that is a classic case of cognitive dissonance. We also have a situation where there is a lot of talk about recession and about how this is the most widely expected recession of all time, and yet the analyst community is still expecting corporate earnings growth to be positive in 2023.

In a plain-vanilla recession, earnings go down 20%. We’ve never had a recession where earnings were up at all. The consensus is that we are going to see corporate earnings expand in 2023. So there’s another glaring anomaly. We are being told this is a widely expected recession, and yet it’s not reflected in earnings estimates – at least not yet.

There’s nothing right now in my collection of metrics telling me that we’re anywhere close to a bottom. 2022 was the year where the Fed tightened policy aggressively and that showed up in the marketplace in a compression in the price-earnings multiple from roughly 22 to around 17. The story in 2022 was about what the rate hikes did to the market multiple; 2023 will be about what those rate hikes do to corporate earnings.

“ You’re left with the S&P 500 bottoming out somewhere close to 2,900. ”

When you’re attempting to be reasonable and come up with a sensible multiple for this market, given where the risk-free interest rate is now, and we can generously assume a roughly 15 price-earnings multiple. Then you slap that on a recession earning environment, and you’re left with the S&P 500 bottoming out somewhere close to 2900.

This is just pure mathematics. All the stock market is at any point is earnings multiplied by the multiple you want to apply to that earnings stream. That multiple is sensitive to interest rates. All we’ve seen is Act I — multiple compression. We haven’t yet seen the market multiple dip below the long-run mean, which is closer to 16. You’ve never had a bear market bottom with the multiple above the long-run average. That just doesn’t happen.

David Rosenberg: ‘You want to be in defensive areas with strong balance sheets, earnings visibility, solid dividend yields and dividend payout ratios.’

Rosenberg Research

MarketWatch: The market wants a “Powell put” to rescue stocks, but may have to settle for a “Powell pause.” When the Fed finally pauses its rate hikes, is that a signal to turn bullish?

Rosenberg: The stock market bottoms 70% of the way into a recession and 70% of the way into the easing cycle. What’s more important is that the Fed will pause, and then will pivot. That is going to be a 2023 story.

The Fed will shift its views as circumstances change. The S&P 500 low will be south of 3000 and then it’s a matter of time. The Fed will pause, the markets will have a knee-jerk positive reaction you can trade. Then the Fed will start to cut interest rates, and that usually takes place six months after the pause. Then there will be a lot of giddiness in the market for a short time. When the market bottoms, it’s the mirror image of when it peaks. The market peaks when it starts to see the recession coming. The next bull market will start once investors begin to see the recovery.

But the recession’s just starting. The market bottoms typically in the sixth or seventh inning of the recession, deep into the Fed easing cycle when the central bank has cut interest rates enough to push the yield curve back to a positive slope. That is many months away. We have to wait for the pause, the pivot, and for rate cuts to steepen the yield curve. That will be a late 2023, early 2024 story.

MarketWatch: How concerned are you about corporate and household debt? Are there echoes of the 2008-09 Great Recession?

Rosenberg: There’s not going to be a replay of 2008-09. It doesn’t mean there won’t be a major financial spasm. That always happens after a Fed tightening cycle. The excesses are exposed, and expunged. I look at it more as it could be a replay of what happened with nonbank financials in the 1980s, early 1990s, that engulfed the savings and loan industry. I am concerned about the banks in the sense that they have a tremendous amount of commercial real estate exposure on their balance sheets. I do think the banks will be compelled to bolster their loan-loss reserves, and that will come out of their earnings performance. That’s not the same as incurring capitalization problems, so I don’t see any major banks defaulting or being at risk of default.

But I’m concerned about other pockets of the financial sector. The banks are actually less important to the overall credit market than they’ve been in the past. This is not a repeat of 2008-09 but we do have to focus on where the extreme leverage is centered.

It’s not necessarily in the banks this time; it is in other sources such as private equity, private debt, and they have yet to fully mark-to-market their assets. That’s an area of concern. The parts of the market that cater directly to the consumer, like credit cards, we’re already starting to see signs of stress in terms of the rise in 30-day late-payment rates. Early stage arrears are surfacing in credit cards, auto loans and even some elements of the mortgage market. The big risk to me is not so much the banks, but the nonbank financials that cater to credit cards, auto loans, and private equity and private debt.

MarketWatch: Why should individuals care about trouble in private equity and private debt? That’s for the wealthy and the big institutions.

Rosenberg: Unless private investment firms gate their assets, you’re going to end up getting a flood of redemptions and asset sales, and that affects all markets. Markets are intertwined. Redemptions and forced asset sales will affect market valuations in general. We’re seeing deflation in the equity market and now in a much more important market for individuals, which is residential real estate. One of the reasons why so many people have delayed their return to the labor market is they looked at their wealth, principally equities and real estate, and thought they could retire early based on this massive wealth creation that took place through 2020 and 2021.

Now people are having to recalculate their ability to retire early and fund a comfortable retirement lifestyle. They will be forced back into the labor market. And the problem with a recession of course is that there are going to be fewer job openings, which means the unemployment rate is going to rise. The Fed is already telling us we’re going to 4.6%, which itself is a recession call; we’re going to blow through that number. All this plays out in the labor market not necessarily through job loss, but it’s going to force people to go back and look for a job. The unemployment rate goes up — that has a lag impact on nominal wages and that is going to be another factor that will curtail consumer spending, which is 70% of the economy.

“ My strongest conviction is the 30-year Treasury bond. ”

At some point, we’re going to have to have some sort of positive shock that will arrest the decline. The cycle is the cycle and what dominates the cycle are interest rates. At some point we get the recessionary pressures, inflation melts, the Fed will have successfully reset asset values to more normal levels, and we will be in a different monetary policy cycle by the second half of 2024 that will breathe life into the economy and we’ll be off to a recovery phase, which the market will start to discount later in 2023. Nothing here is permanent. It’s about interest rates, liquidity and the yield curve that has played out before.

MarketWatch: Where do you advise investors to put their money now, and why?

Rosenberg: My strongest conviction is the 30-year Treasury bond TMUBMUSD30Y, 3.674%.

The Fed will cut rates and you’ll get the biggest decline in yields at the short end. But in terms of bond prices and the total return potential, it’s at the long end of the curve. Bond yields always go down in a recession. Inflation is going to fall more quickly than is generally anticipated. Recession and disinflation are powerful forces for the long end of the Treasury curve.

As the Fed pauses and then pivots — and this Volcker-like tightening is not permanent — other central banks around the world are going to play catch up, and that is going to undercut the U.S. dollar DXY, +0.70%.

There are few better hedges against a U.S. dollar reversal than gold. On top of that, cryptocurrency has been exposed as being far too volatile to be part of any asset mix. It’s fun to trade, but crypto is not an investment. The crypto craze — fund flows directed to bitcoin BTCUSD, +0.35%

and the like — drained the gold price by more than $200 an ounce.

“ Buy companies that provide the goods and services that people need – not what they want. ”

I’m bullish on gold GC00, +0.22%

– physical gold — bullish on bonds, and within the stock market, under the proviso that we have a recession, you want to ensure you are invested in sectors with the lowest possible correlation to GDP growth.

Invest in 2023 the same way you’re going to be living life — in a period of frugality. Buy companies that provide the goods and services that people need – not what they want. Consumer staples, not consumer cyclicals. Utilities. Health care. I look at Apple as a cyclical consumer products company, but Microsoft is a defensive growth technology company.

You want to be buying essentials, staples, things you need. When I look at Microsoft MSFT, -0.61%,

Alphabet GOOGL, -1.79%,

Amazon AMZN, -1.17%,

they are what I would consider to be defensive growth stocks and at some point this year, they will deserve to be garnering a very strong look for the next cycle.

You also want to invest in areas with a secular growth tailwind. For example, military budgets are rising in every part of the world and that plays right into defense/aerospace stocks. Food security, whether it’s food producers, anything related to agriculture, is an area you ought to be invested in.

You want to be in defensive areas with strong balance sheets, earnings visibility, solid dividend yields and dividend payout ratios. If you follow that you’ll do just fine. I just think you’ll do far better if you have a healthy allocation to long-term bonds and gold. Gold finished 2022 unchanged, in a year when flat was the new up.

In terms of the relative weighting, that’s a personal choice but I would say to focus on defensive sectors with zero or low correlation to GDP, a laddered bond portfolio if you want to play it safe, or just the long bond, and physical gold. Also, the Dogs of the Dow fits the screening for strong balance sheets, strong dividend payout ratios and a nice starting yield. The Dogs outperformed in 2022, and 2023 will be much the same. That’s the strategy for 2023.

Investors cheered when a report last week showed the economy expanded in the third quarter after back-to-back contractions.

But it’s too early to get excited, because the Federal Reserve hasn’t given any sign yet that it is about to stop raising interest rates at the fastest pace in decades.

Below is a list of dividend stocks that have had low price volatility over the past 12 months, culled from three large exchange traded funds that screen for high yields and quality in different ways.

In a year when the S&P 500 SPX, -0.40%

is down 18%, the three ETFs have widely outperformed, with the best of the group falling only 1%.

That said, last week was a very good one for U.S. stocks, with the S&P 500 returning 4% and the Dow Jones Industrial Average DJIA, -0.32%

having its best October ever.

This week, investors’ eyes turn back to the Federal Reserve. Following a two-day policy meeting, the Federal Open Market Committee is expected to make its fourth consecutive increase of 0.75% to the federal funds rate on Wednesday.

The inverted yield curve, with yields on two-year U.S. Treasury notes TMUBMUSD02Y, 4.540%

exceeding yields on 10-year notes TMUBMUSD10Y, 4.064%,

indicates investors in the bond market expect a recession. Meanwhile, this has been a difficult earnings season for many companies and analysts have reacted by lowering their earnings estimates.

The weighted rolling consensus 12-month earning estimate for the S&P 500, based on estimates of analysts polled by FactSet, has declined 2% over the past month to $230.60. In a healthy economy, investors expect this number to rise every quarter, at least slightly.

Low-volatility stocks are working in 2022

Take a look at this chart, showing year-to-date total returns for the three ETFs against the S&P 500 through October:

FactSet

The three dividend-stock ETFs take different approaches:

The $40.6 billion Schwab U.S. Dividend Equity ETF SCHD, +0.15%

tracks the Dow Jones U.S. Dividend 100 Indexed quarterly. This approach incorporates 10-year screens for cash flow, debt, return on equity and dividend growth for quality and safety. It excludes real estate investment trusts (REITs). The ETF’s 30-day SEC yield was 3.79% as of Sept. 30.

The iShares Select Dividend ETF DVY, +0.45%

has $21.7 billion in assets. It tracks the Dow Jones U.S. Select Dividend Index, which is weighted by dividend yield and “skews toward smaller firms paying consistent dividends,” according to FactSet. It holds about 100 stocks, includes REITs and looks back five years for dividend growth and payout ratios. The ETF’s 30-day yield was 4.07% as of Sept. 30.

The SPDR Portfolio S&P 500 High Dividend ETF SPYD, +0.60%

has $7.8 billion in assets and holds 80 stocks, taking an equal-weighted approach to investing in the top-yielding stocks among the S&P 500. It’s 30-day yield was 4.07% as of Sept. 30.

All three ETFs have fared well this year relative to the S&P 500. The funds’ beta — a measure of price volatility against that of the S&P 500 (in this case) — have ranged this year from 0.75 to 0.76, according to FactSet. A beta of 1 would indicate volatility matching that of the index, while a beta above 1 would indicate higher volatility.

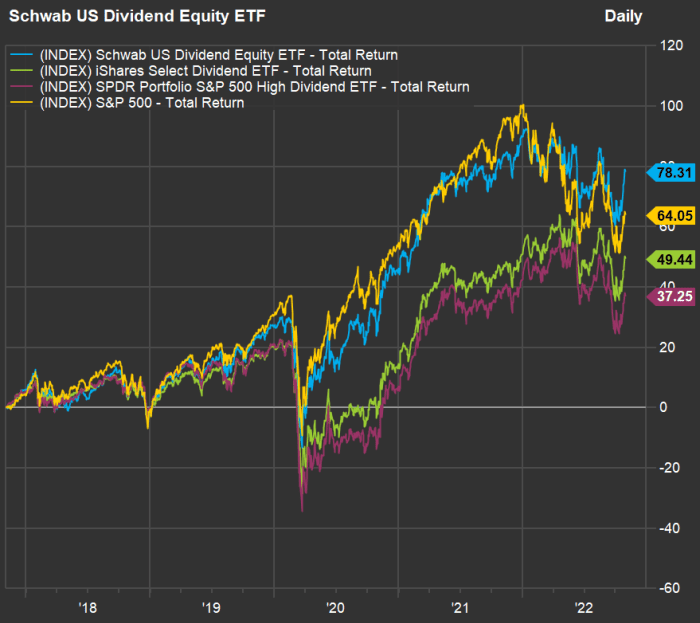

Now look at this five-year total return chart showing the three ETFs against the S&P 500 over the past five years:

FactSet

The Schwab U.S. Dividend Equity ETF ranks highest for five-year total return with dividends reinvested — it is the only one of the three to beat the index for this period.

Screening for the least volatile dividend stocks

Together, the three ETFs hold 194 stocks. Here are the 20 with the lowest 12-month beta. The list is sorted by beta, ascending, and dividend yields range from 2.45% to 8.13%:

Any list of stocks will have its dogs, but 16 of these 20 have outperformed the S&P 500 so far in 2022, and 14 have had positive total returns.

You can click on the tickers for more about each company. Click here for Tomi Kilgore’s detailed guide to the wealth of information available free on the MarketWatch quote page.