BARCELONA, SPAIN – MARCH 01: A view of the MasterCard company logo on their stand during the Mobile World Congress on March 1, 2017 in Barcelona, Spain. (Photo by Joan Cros Garcia/Corbis via Getty Images)

Mastercard said Tuesday that it’s agreed to acquire Minna Technologies, a software firm that makes it easier for consumers to manage their subscriptions.

The move comes as Mastercard and its primary payment network rival Visa are rapidly attempting to expand beyond their core credit and debit card businesses into technology services, such as cybersecurity, fraud prevention, and pay-by-bank payments.

Mastercard declined to disclose financial details of the transaction which is currently subject to a regulatory review.

The payments giant said that the deal, along with other initiatives it’s committed to around subscriptions, will allow it to give consumers a way to access all their subscriptions in a single view — whether inside your banking app or a central “hub.”

Minna Technologies, which is based in Gothenburg, Sweden, develops technology that helps consumers manage subscriptions within their banking apps and websites, regardless of which payment method they used for their subscriptions.

The company said it works with some of the world’s largest financial institutions in the world today. It already counts Mastercard as a key partner as well as its rival Visa.

“These teams and technologies will add to the broader set of tools that help manage the merchant-consumer relationship and minimize any disruption in their experience,” Mastercard said in a blog post Tuesday.

Consumers today often have tons of subscriptions to manage across multiple services such as Netflix, Amazon and Disney Plus. Owning multiple subscriptions can make it difficult to cancel them as consumers can end up losing track of which subscriptions they’re paying for and when.

Mastercard noted that this can have a negative impact on merchants because consumers who aren’t able to easily cancel their subscriptions end up calling on their banks to request a block on payments being taken.

According to Juniper Research data, there are 6.8 billion subscriptions globally, a number that’s expected to jump to 9.3 billion by 2028.

Financial services incumbents such as Mastercard have been rapidly growing their product suite to remain competitive with emerging fintech players that are offering more convenient, digitally native ways to manage consumers’ money management needs.

In 2020, Mastercard acquired Finicity, a U.S. fintech firm that enables third parties — such as fintechs or other banks — to gain access to consumers’ banking information and make payments on their behalf.

Earlier this year, the company announced that by 2030, it would tokenize all cards issued on its network in Europe — in other words, as a consumer, you wouldn’t need to enter your card details manually anymore and would only have to use your thumbprint to authenticate your identity when you pay.

Visa, meanwhile, is also trying to remain competitive with fintech challengers. Last month, the company launched a new service called Visa A2A, which makes it easier for consumers to set up and manage direct debits — payments which are taken directly from your bank account rather than by card.

The U.S. Justice Department on Tuesday sued Visa, the world’s biggest payments network, saying it propped up an illegal monopoly over debit payments by imposing “exclusionary” agreements on partners and smothering upstart firms.

Visa’s moves over the years have resulted in American consumers and merchants paying billions of dollars in additional fees, according to the DOJ, which filed a civil antitrust suit in New York for “monopolization” and other unlawful conduct.

“We allege that Visa has unlawfully amassed the power to extract fees that far exceed what it could charge in a competitive market,” Attorney General Merrick Garland said in a DOJ release.

“Merchants and banks pass along those costs to consumers, either by raising prices or reducing quality or service,” Garland said. “As a result, Visa’s unlawful conduct affects not just the price of one thing — but the price of nearly everything.”

Visa and its smaller rival Mastercard have surged over the past two decades, reaching a combined market cap of roughly $1 trillion, as consumers tapped credit and debit cards for store purchases and e-commerce instead of paper money. They are essentially toll collectors, shuffling payments between banks operating for the merchants and for cardholders.

Visa called the DOJ suit “meritless.”

“Anyone who has bought something online, or checked out at a store, knows there is an ever-expanding universe of companies offering new ways to pay for goods and services,” said Visa general counsel Julie Rottenberg.

“Today’s lawsuit ignores the reality that Visa is just one of many competitors in a debit space that is growing, with entrants who are thriving,” Rottenberg said. “We are proud of the payments network we have built, the innovation we advance, and the economic opportunity we enable.”

More than 60% of debit transactions in the U.S. run over Visa rails, helping it charge more than $7 billion annually in processing fees, according to the DOJ complaint.

The payment networks’ decades-old dominance has increasingly attracted attention from regulators and retailers.

In 2020, the DOJ filed an antitrust suit to block Visa from acquiring fintech company Plaid. The companies initially said they would fight the action, but soon abandoned the $5.3 billion takeover.

In March, Visa and Mastercard agreed to limit their fees and let merchants charge customers for using credit cards, a deal retailers said was worth $30 billion in savings over a half decade. A federal judge later rejected the settlement, saying the networks could afford to pay for a “substantially greater” deal.

In its complaint, the DOJ said Visa threatens merchants and their banks with punitive rates if they route a “meaningful share” of debit transactions to competitors, helping maintain Visa’s network moat. The contracts help insulate three-quarters of Visa’s debit volume from fair competition, the DOJ said.

“Visa wields its dominance, enormous scale, and centrality to the debit ecosystem to impose a web of exclusionary agreements on merchants and banks,” the DOJ said in its release. “These agreements penalize Visa’s customers who route transactions to a different debit network or alternative payment system.”

Furthermore, when faced with threats, Visa “engaged in a deliberate and reinforcing course of conduct to cut off competition and prevent rivals from gaining the scale, share, and data necessary to compete,” the DOJ said.

The moves also tamped down innovation, according to the DOJ. Visa pays competitors hundreds of millions of dollars annually “to blunt the risk they develop innovative new technologies that could advance the industry but would otherwise threaten Visa’s monopoly profits,” according to the complaint.

Visa has agreements with tech players including Apple, PayPal and Square, turning them from potential rivals to partners in a way that hurts the public, the DOJ said.

For instance, Visa chose to sign an agreement with a predecessor to the Cash App product to ensure that the company, later rebranded Block, did not create a bigger threat to Visa’s debit rails.

A Visa manager was quoted as saying “we’ve got Square on a short leash and our deal structure was meant to protect against disintermediation,” according to the complaint.

Visa has an agreement with Apple in which the tech giant says it will not directly compete with the payment network “such as creating payment functionality that relies primarily on non-Visa payment processes,” the complaint alleged.

The DOJ asked for the courts to prevent Visa from a range of anticompetitive practices, including fee structures or service bundles that discourage new entrants.

The move comes in the waning months of President Joe Biden‘s administration, in which regulators including the Federal Trade Commission and the Consumer Financial Protection Bureau have sued middlemen for drug prices and pushed back against so-called junk fees.

In February, credit card lender Capital One announced its acquisition of Discover Financial, a $35.3 billion deal predicated in part on Capital One’s ability to bolster Discover’s also-ran payments network, a distant No. 4 behind Visa, Mastercard and American Express.

Capital One said once the deal is closed, it will switch all its debit card volume and a growing share of credit card volume to Discover over time, making it a more viable competitor to Visa and Mastercard.

Visa said it plans to launch a dedicated service for bank transfers, skipping credit cards and the traditional direct debit process.

Visa, which alongside Mastercard is one of the world’s largest card networks, said Thursday it plans to launch a dedicated service for account-to-account (A2A) payments in Europe next year.

Users will be able set up direct debits — transactions that take funds directly from your bank account — on merchants’ e-commerce stores with just a few clicks.

Visa said consumers will be able to monitor these payments more easily and raise any issues by clicking a button in their banking app, giving them a similar level of protection to when they use their cards.

The service should help people deal with problems like unauthorized auto-renewals of subscriptions, by making it easier for people to reverse direct debit transactions and get their money back, Visa said. It won’t initially apply its A2A service to things like TV streaming services, gym memberships and food boxes, Visa added, but this is planned for the future.

The product will initially launch in the U.K. in early 2025, with subsequent releases in the Nordic region and elsewhere in Europe later in 2025.

The problem currently is that when a consumer sets up a payment for things like utility bills or childcare, they need to fill in a direct debit form.

But this offers consumers little control, as they have to share their bank details and personal information, which isn’t secure, and have limited control over the payment amount.

Static direct debits, for example, require advance notice of any changes to the amount taken, meaning you have to either cancel the direct debit and set up a new one or carry out a one-off transfer.

With Visa A2A, consumers will be able to set up variable recurring payments (VRP), a new type of payment that allows people to make and manage recurring payments of varying amounts.

“We want to bring pay-by-bank methods into the 21st century and give consumers choice, peace of mind and a digital experience they know and love,” Mandy Lamb, Visa’s managing director for the U.K. and Ireland, said in a statement Thursday.

“That’s why we are collaborating with UK banks and open banking players, bringing our technology and years of experience in the payments card market to create an open system for A2A payments to thrive.”

Visa’s A2A product relies on a technology called open banking, which requires lenders to provide third-party fintechs with access to consumer banking data.

Open banking has gained popularity over the years, especially in Europe, thanks to regulatory reforms to the banking system.

The technology has enabled new payment services that can link directly to consumers’ bank accounts and authorize payments on their behalf — provided they’ve got permission.

In 2021, Visa acquired Tink, an open banking service, for 1.8 billion euros ($2 billion). The deal came on the heels of an abandoned bid from Visa to buy competing open banking firm Plaid.

Visa’s buyout of Tink was viewed as a way for it to get ahead of the threat from emerging fintechs building products that allow consumers — and merchants — to avoid paying its card transaction fees.

Merchants have long bemoaned Visa and Mastercard’s credit and debit card fees, accusing the companies of inflating so-called interchange fees and barring them from directing people to cheaper alternatives.

In March, the two companies reached a historic $30 billion settlement to reduce their interchange fees — which are taken out of a merchant’s bank account when a shopper uses their card to pay for something.

Visa didn’t share details on how it would monetize its A2A service. By giving merchants the option to bypass cards for payments, there’s a risk that Visa could potentially cannibalize its own card business.

For its part, Visa told CNBC it is and always has been focused on enabling the best ways for people to pay and get paid, whether that’s through a card or non-card transaction.

From left to right: Johan Pihl, Doconomy’s chief creative officer and co-founder, and Mathias Wikstrom, chief executive officer and co-founder.

Doconomy

Swedish climate-focused financial technology startup Doconomy told CNBC on Thursday that it’s raised 34 million euros ($36.9 million) from leading European banks, including UBS and Commerzbank.

Doconomy, which offers tools to help bank customers measure the carbon footprint of their everyday spending, raised the cash in a Series B financing round co-led by UBS Next and CommerzVentures, the venture arms of UBS and Commerzbank, respectively.

Credit ratings agency S&P Global came on board as a new investor, while existing shareholders Motive Ventures, PostFinance and Tenity also participated.

Founded in Sweden in 2018, Doconomy works with the likes of Boston Consulting Group, Mastercard, S&P Global, and the United Nations Framework Convention on Climate Change to calculate the climate cost associated with financial transactions.

Among the firm’s tools is the AIand Index, a cloud-based service for banks that helps their customers convert every transaction into its corresponding CO2 footprint. The index is used by more than 100 financial institutions in more than 40 countries.

Doconomy plans to use the fresh cash to drive expansion into North America and roll out new products, CEO and co-founder Mathias Wikstrom told CNBC in an interview.

“Going forward, we want to enable every bank in every corner of the world to engage their clients in the ESG [environmental, social, and governance] work of the bank,” Wikstrom said. “We see a connection between the E and S, the environmental and the social. We can’t isolate those two different streams.”

Wikstrom said he was “very happy” to see partnerships emerging with the likes of UBS and Commerzbank, describing it as an “alliance of the winning both money and intellect into getting this issue under control.

News of Doconomy’s latest funding follows the firm’s February 2023 deal to acquire Dreams Technology, a platform that uses behavioral science to boosts customers’ digital engagement and financial wellbeing.

Wikstrom said that Doconomy’s valuation in its Series B round is unchanged from the price at which it raised funds in its Series A, which saw the firm raise cash from the likes of Citi Ventures, Mastercard, and Ikea parent company Ingka.

Doconomy’s growth story hasn’t come without its challenges. More recently, the firm faced attacks from right-wing online commentator Jordan Peterson and his followers.

It’s not really hurricane season anymore, it’s fear season.

Mathias Wikstrom

CEO, Doconomy

Last week, Peterson targeted the company in a post on social media platform X, labelling it the “soft positive planet-saving voice of the worst imaginable corporate/fascist/green tyranny.”

The Canadian psychologist, who gained internet fame critiquing so-called political correctness, is a noted skeptic who described climate change as “the idiot socialist get-out-of-jail-free card.” He once framed rising greenhouse gas emissions as a positive for making the planet “green in the driest areas.”

Climate scientists say this is misleading, as it doesn’t take into account the negative effects intensified droughts, wildfires and heatwaves caused by global warming have on plants and ecosystems.

Wikstrom told CNBC that the situation concerning Peterson’s attacks on his firm “illustrates that we need to educate a lot of people.”

“Fear will lead to frustration and frustration will potentially lead to protests, and protests will lead to violence and violence will lead to damage done,” he told CNBC.

Wikstrom said that he hopes that the more the likes of Peterson and other climate skeptics keep “banging the drum,” the likelier that their sentiments will eventually sound “hollow.”

“Looking at what’s happening in Hawaii, in Canada, in France, in Spain, in Greece — we have the floods, we have the fires, we have so many concerns now,” he said. “It’s not really hurricane season anymore, it’s fear season.”

Climate fintech is a niche area of financial technology that has attracted heightened interest from investors, as world governments push corporates to hit ESG targets and reduce carbon emissions associated with their operations.

Michael Baldinger, chief sustainability officer of UBS, said the bank’s venture investment into Doconomy “underscores our focus on fostering innovation to provide the data and actionable insights our clients need to make informed choices about their investments and effect the change they want to see.”

The boss of Swedish financial technology startup Trustly says an initial public offering for the company is still a year or two away from happening, even after a 51% jump in operating profit.

In an exclusive interview with CNBC, Johan Tjarnberg, CEO of Trustly, said that his firm still needs time to prove the value of its open banking technology to investors before going public.

“We need another year or two to really demonstrate to the market that open banking is happening happening, it’s here,” Tjarnberg told CNBC.

“For me, there is so much we want to demonstrate to the market in terms of user adoption, merchant adoption. We still need some time to execute on our existing playbook.”

Trustly is holding out on an IPO even after reporting a strong set of financials. Results shared exclusively with CNBC show the firm reported revenues of $265 million in its 2023 full year.

Growth accelerated significantly in the second half of the year, Trustly said, climbing 27% compared with the same period in 2022. That was as transaction volumes spiked 48% over the same period.

Tjarnberg told CNBC that the company’s performance in 2023 was heavily driven by the growth at its U.S. business. Trustly merged with American rival PayWithMyBank in 2020.

“We invested a lot into the U.S. market,” Tjarnberg said. “We were roughly 20 people there four years ago; we now have 500 supporting the U.S. market.”

Tjarnberg said that, in the first quarter of this year, Trustly saw heightened growth in areas like utilities, retail, and travel, with 22% of volumes coming from those core verticals, up 44% over 12 months.

Trustly increased operating profit by 51% in full-year 2023, with adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) climbing to $51 million from $33 million in 2022.

That was as overall transaction value processed during 2023 climbed by 79%, to $58 billion.

Trustly helps companies integrate the ability to accept payments via open banking technology.

This tech lets consumers make payments directly to a merchant’s bank account without the need for an intermediary such as a card issuer.

It provides an alternative to incumbent credit card programs such as Mastercard and Visa, which charge merchants high fees for transactions.

In the U.S., Tjarnberg said, Trustly is seeing heightened demand from merchants “trying to take down costs,” as high card processing fees have made them more price-conscious.

“There is no secret that our objectives and ambition is to bring a good alternative to other payment methods, including cards,” he told CNBC.

Open banking is a trend which has gained significant momentum, particularly across Europe.

That’s thanks to the introduction of regulations which require banks to open their clients’ account data and payment functionalities to third-party firms.

It has paved the way for new entrants into finance including fintechs, startups and tech companies. Founded in 2008, Sweden’s Trustly competes with the likes of GoCardless, TrueLayer, Volt, Bud, and Yapily.

Trustly expects to launch a feature that allows its merchants to set up recurring payments for customers. That will be targeted at things like telecom packages and subscription-based music streaming services.

Tjarnberg said Trustly is “bullish” on the mobile space, particularly in the U.S. after having seen early success in mobile billing partnerships with the likes of AT&T and T-Mobile.

Trustly is majority-owned by venture capital firm Nordic Capital, which owns a 51.1% stake in the business. Alfven & Didrikson is its second-biggest backer, with a 11.1% stake, while BlackRock holds an 8.9% stake.

Aberdeen Standard Investments and Neuberger Berman own 0.7% and 0.9% stakes in Trustly, respectively, while others including the Trustly management and employees own 27.4%.

Capital One’s recently announced $35.3 billion acquisition of Discover Financial isn’t just about getting bigger â gaining “scale” in Wall Street-speak â it’s a bid to protect itself against a rising tide of fintech and regulatory threats.

It’s a chess move by one of the savviest long-term thinkers in American finance, Capital One CEO Richard Fairbank. As a co-founder of a top 10 U.S. bank by assets, his tenure is a rarity in a banking world dominated by institutions like JPMorgan Chase that trace their origins to shortly after the signing of the Declaration of Independence.

Fairbank, who became a billionaire by building Capital One into a credit card giant since its 1994 IPO, is betting that buying rival card company Discover will better position the company for global payments’ murky future. The industry is a dynamic web where players of all stripes â from traditional banks to fintech players and tech giants â are all seeking to stake out a corner in a market worth trillions of dollars by eating into incumbents’ share amid the rapid growth of e-commerce and digital payments.

“This deal gives the company a stronger hand to battle other banks, fintechs and big tech companies,” said Sanjay Sakhrani, the veteran KBW retail finance analyst. “The more that they can separate themselves from the pack, the more they can future-proof themselves.”

The deal, if approved, enables Capital One to leapfrog JPMorgan as the biggest credit card company by loans, and solidifies its position as the third largest by purchase volume. It also adds heft to Capital One’s banking operations with $109 billion in total deposits from Discover’s digital bank and helps the combined entity shave $1.5 billion in expenses by 2027.

But it’s Discover’s payments network â the “rails” that shuffle digital dollars between consumers and merchants, collecting tolls along the way â that Fairbank repeatedly praised Tuesday when analysts queried him on the strategic merits of the deal. There are only four major card networks: giants Visa and Mastercard, then American Express and finally the smallest of the group, Discover.

Capital One and Discover credit cards arranged in Germantown, New York, US, on Tuesday, Feb. 20, 2024.Â

Angus Mordant | Bloomberg | Getty Images

“That network is a very, very rare asset,” Fairbank said. “We have always had a belief that the Holy Grail is to be able to be an issuer with one’s own network so that one can deal directly with merchants.”

From the time of Capital One’s founding in the late 1980s, Fairbank said, he envisioned creating a global digital payments tech company by owning the payment rails and dealing directly with merchants. In the decades since, Capital One has been ahead of stodgier banks, gaining a reputation in tech circles for being forward-thinking and for its early adoption of cloud computing and agile software development.

But its growth has relied on Visa and Mastercard, which accounted for the vast majority of payment volumes last year, processing nearly $10 trillion in the U.S. between them.

Capital One intends to boost the Discover network, which carried $550 billion in transactions last year, by quickly switching all of its debit volume there, as well as a growing share of its credit card flows over time.

By 2027, the bank expects to add at least $175 billion in payments and 25 million of its cardholders onto the Discover network.

The true potential of the Discover deal, though, is what it allows Capital One to do in the future if it owns the toll road, according to analysts.

By creating an end-to-end ecosystem that is more of a closed loop between shoppers and merchants, it could fend off competition from rapidly mutating fintech players like Block and PayPal, as well as buy now, pay later firms like Affirm and Klarna, who have made inroads with both businesses and consumers.

Capital One aims to deepen relationships with merchants by showing them how to boost sales, helping them prevent fraud and providing data insights, Fairbank said Tuesday, all of which makes them harder to dislodge. It can use some of the network fees to create new loyalty plans, like debit rewards programs, or underwrite merchant incentives or experiences, according to analysts.

“Owning a network allows us to deal more directly with merchants rather than a network intermediary,” Fairbank told analysts. “We create more value for merchants, small businesses and consumers and capture the additional economics from vertical integration.”

It’s a capability that technology or fintech companies probably covet. The Discover network alone would be worth up to $6 billion if sold to Alphabet,Apple or Fiserv, Sakhrani wrote Tuesday in a research note.

The Capital One-Discover combination could fortify the company against another potential threat â from Washington.

Proposed legislation from Sen. Dick Durbin, D-Ill., aims to cap the fees charged by Visa and Mastercard, potentially blowing up the economics of credit card rewards programs. If that proposal becomes law, the competitive position of Discover’s network, which is exempt from the limitations, suddenly improves, according to Brian Graham, co-founder of advisory firm Klaros Group. That mirrors what an earlier law known as the Durbin amendment did for debit cards.

Chairman Dick Durbin (D-IL) speaks during a US Senate Judiciary Committee hearing regarding Supreme Court ethics reform, on Capitol Hill in Washington, DC, on May 2, 2023.

Mandel Ngan | AFP | Getty Images

“There are a bunch of things aimed, in one way or another, at the card networks and that ecosystem,” Graham said. “Those pressures might be one of the things that creates an opportunity for Capital One in the future if they have control over this network.”

The biggest question for Capital One, its customers and investors is whether the merger will ultimately be approved by regulators. While Fairbank said he expects the deal to be closed in late 2024 or early 2025, industry experts said it was impossible to know whether it will be blocked by regulators, like a string of high-profile takeovers among banks, airlines and tech companies.

On Tuesday, Democratic Sen. Elizabeth Warren of Massachusetts urged regulators to swiftly block the deal, calling it “dangerous.” Sen. Sherrod Brown, D-Ohio, chairman of the Senate Banking Committee, said he would be watching the deal to “ensure that this merger doesn’t enrich shareholders and executives at the expense of consumers and small businesses.”

The Discover deal’s survival may hinge on whether it’s seen as boosting an also-ran payments network, or allowing an already-dominant card lender to level up in size â another reason Fairbank may have played up the importance of the network.

“Which thing you are more concerned about will define whether you think this is a good deal or a bad deal from a public policy point of view,” Graham said.

It will be an all-stock deal and Capital One, which already uses Visa and Mastercard networks, plans to keep the Discover brand, the Wall Street Journal said.

The news comes on the back of a Bloomberg News report on Monday that Capital One was considering an acquisition.

CNBC has reached out for comment from both Capital One and Discover.

The merger of the two companies, who are among the largest credit card issuers in the U.S., would expand Capital One’s credit-card offerings. The company bought digital concierge service Velocity Black, a premium credit card and luxury market platform, in June of last year.

Shares of Discover are down 1.7% lower for the year, putting the company at a $27.63 billion market cap. Capital One has a market cap of $52.2 billion and shares of the company are up 4.6% in 2024.

The Capital One-Discover merger would be one of the largest deals announced so far this year. Synopsys announced a deal to buy Ansys for $35 billion in January and Diamondback Energy‘s $26 billion deal to buy privately held oil and gas producer Endeavor Energy was announced on Feb. 12.

Housing is typically one of the biggest expenses in someone’s budget, and it’s natural to wonder about the best way to pay that bill.

For renters, sometimes it’s possible to pay with a credit card. While you could earn rewards and build credit by doing so, experts say it’s typically not a smart move.

“This is a very large payment. It could rapidly spiral in terms of additional interest rate costs,” said Susan M. Wachter, a professor of real estate at The Wharton School of the University of Pennsylvania.

An appeal of paying your rent with credit might be earning rewards on that expense. The typical cash back card offers 1.5% to 2% back.

But most third-party payment services and large property management companies charge credit card processing or transaction fees. Those can run between 1% and 3% of the rent charge.

“The cost of that fee may eat into the value of any rewards you might earn, so it might not even be worth it,” said Melissa Lambarena, a credit cards expert at NerdWallet.

The median apartment rent nationwide was $1,964 in January, according to Rent.com. That would generate nearly $60 in monthly credit card processing fees, or more than $700 over the course of a year.

Make sure you review the terms before you decide which card to use. Processing fees vary, and there are some cards that do not charge them, such as the Bilt Mastercard.

If you do not pay the card balance in full by the end of the statement period, you risk adding interest charges on top of your monthly rent.

“Don’t pay rent with a credit card if you’re going to be charged interest,” said Ted Rossman, an industry analyst at Bankrate.

Due to inflation, more people have been racking up and carrying debt, whether from credit cards or buy now, pay later loans.High interest rates can make some of these balances harder to pay off.

The average interest rate for all credit cards by the end of 2023 was 21.47%, the highest annual percentage rate since the Federal Reserve began tracking in 1994, according to LendingTree.

Using credit cards for large transactions can affect your credit utilization rate, the ratio of debt to total credit, which weighs heavily into your credit score, Lambarena explained.

“Putting rent on your card’s credit limit could hurt your credit score,” she said. “It’s usually recommended by experts not to use more than 30% of your amount of available credit.”

If you want to put the rent payment on your card, a good buffer is to make sure you have enough available balance. You can ask for a credit limit increase from your card issuer to minimize the effect to your score.

A flag outside the U.S. Securities and Exchange Commission headquarters in Washington, Feb. 23, 2022.

Al Drago | Bloomberg | Getty Images

Regulators around the world from Europe to Asia ramped up efforts to bring about formal laws for digital currencies in 2023 — but it was the U.S. that took some of the harshest legal actions against major players in the industry.

In a year that saw crypto heavyweight Binance ordered to pay more than $4 billion to U.S. authorities and its former CEO’s guilty plea, along with high-profile lawsuits against five crypto companies by the Securities and Exchange Commission, regulators overseas have been equally busy both adopting new legislation — and pushing for more — to rein in the sector’s bad actors.

Here’s the state of play globally for crypto regulation and enforcement in 2023 — and a look at what to expect in 2024.

The U.S. has proven to be one of the most active enforcers of penalties and legal action against crypto companies this year, as authorities looked to counter bad practices in the industry following the collapse of Sam Bankman-Fried’s crypto empire — including his FTX exchange and sister firm Alameda Research.

“To be clear, in some cases — like FTX — enforcement was necessary,” said Renato Mariotti, a former prosecutor in the U.S. Justice Department’s Securities and Commodities Fraud Section. “But U.S. enforcement actions against market participants that are more focused on compliance are questionable and the result of the U.S. ‘regulation by enforcement’ approach.”

While many regions have passed laws with potentially tough penalties, the U.S. is still the only country that has actively taken action against large-scale crypto companies and projects. Thus far, the U.S. has led that campaign against crypto firms by enforcement and has, by far, been the most punishing of regulators when it comes to penalties and fines.

“Other countries have a comprehensive regulatory framework in place. We don’t,” Mariotti told CNBC. “As a result, issues that should be determined by legislation or regulation are instead litigated.”

Indeed, in the absence of hard-and-fast rules from Capitol Hill, the SEC, the Commodity Futures Trading Commission, the Department of Justice, and Treasury’s Financial Crimes Enforcement Network (FinCen), have worked in parallel to police the space, in a sort of patch-quilt version of regulation-by-enforcement.

Richard Levin, a partner at Nelson Mullins Riley & Scarborough who has represented clients before the SEC, CFTC, and Congress, tells CNBC that these agencies have been some of the most active enforcers around the world concerning the regulation of digital assets and cryptocurrencies.

“These agencies have provided guidance to the industry on how digital assets and cryptocurrencies must be offered and sold, traded, and held by custodians,” said Levin, who has been involved in the fintech sector for 30 years.

“However, much of their work has involved providing guidance to the industry through enforcement actions,” continued Levin.

Since 2019, Justice’s Market Integrity and Major Frauds Unit has charged cryptocurrency fraud cases involving over $2 billion in intended financial losses to investors worldwide.

In its annual report summing up enforcement actions, the CFTC noted that nearly half of all cases in 2023 involved conduct related to digital asset commodities. Meanwhile, the SEC highlighted that 2023 was notable for its enforcement of “crypto-related misconduct, including fraud schemes, unregistered crypto assets and platforms, and illegal celebrity touting.” Since 2014, the SEC has brought more than 200 actions related to crypto asset and cyber enforcement.

The most stringent cases played out in the first half of the year when the SEC accused Binance and Coinbase of engaging in illegal securities dealing in a pair of lawsuits.

Most notably, the SEC alleges that at least 13 crypto assets available to Coinbase customers — including Solana’s sol, Cardano’s ada, and Protocol Labs’ filecoin — should be considered securities, meaning they’d need to be subject to strict transparency and disclosure requirements.

In Binance’s case, the SEC went a step further. In addition to securities law violations, the company and its co-founder and CEO Changpeng Zhao were also accused of commingling customer assets with company funds.

Concerning criminal enforcement, Damian Williams, the U.S. attorney for the Southern District of New York, has been leading some of Justice’s highest-profile crypto prosecutions, including the monthlong trial of Bankman-Fried, the disgraced FTX founder. In November, a jury found the former FTX chief executive guilty of all seven criminal counts against him following a few hours of deliberation.

But crypto companies have begun to push back, with some threatening to decamp from the U.S. entirely should this dynamic of policing by enforcement continue.

Coinbase CEO Brian Armstrong condemned the SEC’s actions against the exchange and suggested the company may be forced to move its headquarters overseas. Armstrong later walked back the threat of relocating abroad, but Coinbase and other major crypto firms have still begun to invest more heavily in their international operations.

Crypto market participants nevertheless hope that the spate of legal challenges brought to crypto companies in 2023 will bring clarity in the form of new regulations.

“Clearer regulatory frameworks and stance from regulators globally have provided a sense of legitimacy and security, encouraging more widespread participation in the bitcoin market,” Alyse Killeen, managing partner of Stillmark Capital, told CNBC.

The crypto industry saw the most legislative progress on crypto laws in the U.S. this year, with one of the competing digital asset bills making it past multiple House committees for the first time.

Even as U.S. lawmakers take steps toward crypto legislation, there remains no law in the U.S. tailored specifically for the industry. Nelson Mullins Riley & Scarborough’s Levin tells CNBC it’s unlikely that we’ll see much progress in a presidential election year and with a divided federal government.

He argues that even without rules on crypto from lawmakers, routine complaints that U.S. regulators are not providing guidance to the industry are without merit.

According to Levin, “The SEC, the CFTC and FinCEN routinely provide informal guidance on the regulation of digital assets and cryptocurrencies.”

“The SEC even went so far as to provide a framework for the analysis of digital assets and cryptocurrencies. The SEC also created a fake digital asset (Hosey Coin) that gave advice to the FinTech community on how not to launch a digital asset,” Levin added.

“Some members of the industry forget the SEC is relying on laws that were written when American football players wore leather helmets, and the SEC must apply those laws to the FinTech industry,” he said.

Despite crypto’s recent fading buzz, Killeen of Stillmark Capital doesn’t expect regulators to become fatigued by crypto in 2024. In the same time year that two of crypto’s leading figures were sent to jail, shares of Coinbase — and prices of digital currencies like bitcoin and ether — have rallied sharply.

Since the start of this year, Coinbase’s stock price has surged more than 400%. Bitcoin and ether, meanwhile, have both roughly doubled in price. That’s as investors anticipate that approval for a bitcoin exchange-traded fund by the SEC may be around the corner.

The European Union looks set to apply its Markets in Crypto-Assets legislation, which is aimed at taming the “Wild West” of the crypto industry, in full force starting next year.

The law, initially proposed in 2019 as a response to Meta’s digital currency project Diem, formerly known as Libra, aimed to clean up fraud, money laundering and other illicit financing in the crypto space, and stamp out the sector’s bad actors more broadly.

Read more about tech and crypto from CNBC Pro

It also sought to tackle a perceived threat from so-called stablecoins, or blockchain-based tokens that serve as a representation of government money but are backed by private companies. Stablecoins are effectively digital currencies that are pegged to the value of fiat currencies like the dollar.

While tether and Circle’s USDC aren’t perceived as “systemic” assets capable of disrupting financial stability, a private stablecoin from a massive company like Meta, Visa or Mastercard could pose a bigger threat and potentially undermine sovereign currencies, in several EU central bankers’ eyes.

The U.S.’s dominant role in global finance and its focus on consumer protection plays a crucial role in its leading position in crypto regulation enforcement. However, the landscape is evolving, and other jurisdictions are steadily enhancing their regulatory and enforcement frameworks in crypto.

Braden Perry

Former federal enforcement attorney and current partner at

Part of the EU’s framework for crypto is aimed at tackling threats — particularly that of the euro being undermined — by making it impossible for issuers to mint stablecoins backed by currencies other than the euro, like the U.S. dollar, once they meet the threshold of more than 1 million transactions per day.

Meanwhile, the European Union is moving towards a unified regulatory framework for cryptocurrencies with its Markets in Crypto-Assets Regulation (MiCA).

This year, the three main political institutions of the EU-approved MiCA, paving the way for the regulation to become law. MiCA came into force in June 2023, but it’s not expected to apply fully until December 2024.

Companies are already getting ready to take advantage of the new rules, with Coinbase submitting an application for a universal MiCA license in Ireland. If and when it is approved, this would allow Coinbase to “passport” its services into other countries like Germany, France, Italy, and the Netherlands.

Braden Perry, former federal enforcement attorney and current partner at law firm Kennyhertz Perry, said that while the U.S. remains a top enforcer for the crypto industry, its perception as a regulator “may be diminishing,” as other jurisdictions have stepped in with clearer rules.

“This perception stems from the proactive measures taken by U.S. regulatory bodies like the SEC, CFTC, and IRS, especially in addressing fraud and security issues in the crypto market. High-profile legal actions in the U.S. further cement its image as a strict enforcer,” he said.

“However, other regions, including Singapore, Dubai, Hong Kong, and the European Union, are also developing robust regulatory frameworks,” Perry added. “While these regions may not be as visible in international media for enforcement actions, they possess significant and sometimes stringent regulatory mechanisms.”

But while the broader EU has been racing to implement new crypto laws, individual European countries haven’t been resting on their laurels.

France has been tempting crypto companies and traders alike to its shores with the promise of tax cuts on crypto profits and a smoother registration process for digital asset firms.

Starting from Jan 1, 2024, France’s Financial Markets Authority, or AMF, is set to amend its registration requirements for crypto firms to better align with MiCA, according to an August statement from the regulator.

At the same time, French authorities have kept a skeptical eye on fraudulent activity among various crypto players. In September, French regulators added 22 fraudulent websites — including some that market trading in crypto and crypto-linked derivatives — to a blacklist of unauthorized foreign exchange providers.

In Germany, meanwhile, the financial regulator Bafin has said it wants to accelerate its approach to licensing crypto custody services, as part of a broader effort to instill trust and transparency in the crypto market.

The U.K., a non-member of the EU, passed a law in June that gives regulators the ability to oversee stablecoins. But there are no concrete rules for crypto just yet.

The U.K.’s Treasury department released its response to a consultation on new crypto rules earlier this year, confirming that it plans to bring a range of crypto activities, including crypto custody and lending, within existing laws governing financial services firms in the country.

Earlier this year, the Monetary Authority of Singapore, which is recognized for clear fintech and crypto regulations that do not rely heavily on enforcement actions, finalized rules for stablecoins, making it one of the world’s first jurisdictions to do so.

Singapore was notably bruised by the collapse of TerraUSD, a controversial algorithmic stablecoin, in 2022, as well as the fall of Three Arrows Capital, or 3AC. Both Terra Labs, the company behind Terra, and 3AC were headquartered in Singapore.

Singapore’s new framework requires stablecoin issuers to back them with low-risk and highly-liquid assets, which must equal or exceed the value of tokens in circulation at all times, return the par value of the digital currency to holders within five business days of a redemption request, and disclose audit results of reserves to users.

The region has been increasingly warming to crypto assets, despite a broader anti-crypto push from China, which banned bitcoin trading and mining in 2021.

The Hong Kong Securities and Futures Commission, or SFC, launched a registration regime for digital asset businesses earlier this year, with clear regulations for crypto exchanges and funds.

So far, only two firms, OSL Digital and Hash Blockchain, have been handed licenses.

The United Arab Emirates has emerged as a popular base for the fintech sector more broadly, given its lack of personal income tax, flexible visa policies, and competitive incentives for international businesses and workers.

In 2022, in a bid to lead the virtual assets sector in the Middle East and Africa, Dubai — the UAE’s most populous city — launched VARA, or the Virtual Asset Regulatory Authority.

“Dubai and the UAE have created favorable conditions for cryptocurrency businesses, offering specific zones and guidelines for crypto trading,” said Perry.

Blockchain analytics firm Chainalysis notes that regulators in the UAE were early to cryptocurrency, with Dubai leading the charge when it launched a blockchain strategy in 2016.

“Since then, UAE regulators have remained at the forefront of the industry,” according to a Chainalysis report.

Two years later, in 2018, Abu Dhabi Global Market created the world’s first regulatory framework for cryptocurrency to foster innovation while safeguarding consumers.

Earlier this year, the UAE passed further crypto regulations at the federal level to make it easier for regulators like VARA to police the sector and run economic-free zones.

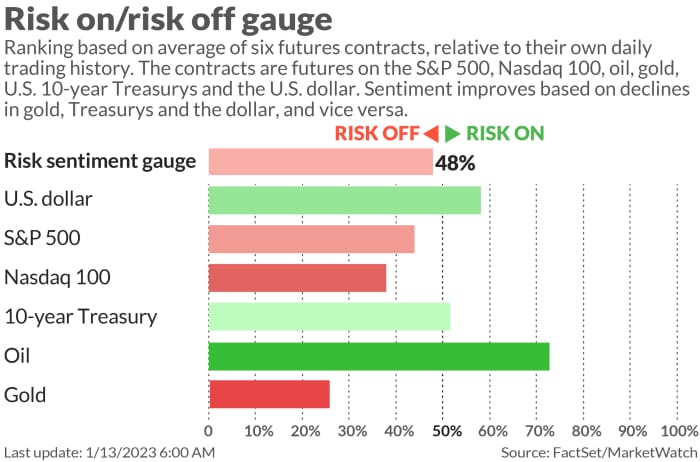

A group of 51 stocks in the benchmark equity index swept to record finishes on Tuesday, the most since April 20, 2022, according to a tally from Dow Jones Market Data.

Equities have been in a year-end rally mode, driven higher by tumbling benchmark yields that finance much of the U.S. economy and expectations of coming interest-rate cuts.

The 10-year Treasury rate BX:TMUBMUSD10Y

fell to 4.2% on Tuesday from a high of about 5% in October.

The Dow Jones Industrial Average DJIA

on Tuesday ended at its third-highest level on record, while the S&P 500 index SPX

and Nasdaq Composite Index COMP

added to a string of new closing highs for 2023. The Dow finished 0.6% away from its record close logged almost two years ago, while the S&P 500 was only 3.2% below its close from the same period, according to Dow Jones Market Data.

The push higher for stocks followed inflation data for November that showed price pressures continued to ease from peak levels, but still were above the Fed’s 2% annual target.

The consumer-price index pegged the annual rate of inflation at 3.1%, down from 3.2% in October, with the “last mile” of inflation expected to be the hardest part to tame.

Investors now will be focused on Wednesday’s Federal Reserve decision. Short-term interest rates are expected to remain unchanged at a 22-year high, but the central bank is expected to update its “dot plot” forecast of rates over a longer time horizon.

“Although the market will focus on the timing of rate cuts, we suspect Chair Powell will be keen to strike notes of caution to avoid financial conditions easing too much further to ensure the Fed continues to see encouraging progress on inflation,” said Emin Hajiyev, senior economist at Insight Investment, in emailed comments.

Wall Street is hoping to enter the last full month of trading in 2023 on a high note. On Friday, all three major indexes rose for the fourth consecutive week. Investors are hoping that the softer-than-expected October inflation print will give the Federal Reserve ample reason to cut benchmark interest rates. Investors as of late are partial toward shares of Mastercard and Norfolk Southern , which ended the week with healthy gains. CNBC screened FactSet data to find the most overbought and oversold stocks, based on the relative strength index (RSI). The relative strength index measures the strength and velocity of stock price moves, and is a useful gauge of whether shares are overbought or oversold. A 14-day RSI reading below 30 indicates a stock is oversold and may present a buying opportunity. A reading above 70 suggests that a stock is overbought and could point to an impending pullback. Mastercard made the list, with a 14-day RSI of 92.11, while shares have climbed more than 18% from the start of the year. Roughly 74% of analysts polled by FactSet maintain a buy rating on Mastercard stock, while their average price targets imply about 8% upside moving forward. In late October, Mastercard beat third-quarter earnings expectations, posting $3.39 per share in adjusted earnings, while analysts polled by FactSet called for $3.21 per share. Revenue came in line with the Street’s forecasts, however. Telecommunications firm Motorola is also overbought, with its 14-day RSI reading of 94.77. Roughly 42% of analysts polled by FactSet rate the stock as a buy, while shares have added more than 24% from the start of the year. Motorola recently increased announced plans to increase its quarterly dividend by 11% to 98 cents a share, and also expanded the company’s stock repurchase program. Other overbought stocks on the list include credit reporting agency Equifax and financial services company Nasdaq Inc . Stocks that are oversold and could be due for a bounce include health-care giant Cigna and oil giant ConocoPhillips . Cigna has a 14-day RSI of 21.57, while ConocoPhillips has a 29.22 reading. Shares of Cigna have have been under pressure from the start of the year, slipping more than 13%. UBS added ConocoPhillips to its tactical picks for November, with the firm noting a potential bounce in oil prices could benefit the stock, given its strong roster of assets and healthy balance sheet. – CNBC’s Fred Imbert contributed reporting.

Both new and existing Prime Visacardholders are in for an extra treat as they work their way through their holiday shopping list this year.

If you’re interested in signing up for this Amazon credit card, you’ll immediately earn a welcome bonus of a $200 Amazon gift card upon approval from now through Dec. 4, 2023. This is double the $100 Amazon gift card the Prime Visa typically offers new cardholders, so if you’ve been toying with the idea of getting this card, now’s the time to move.

Prime Visa

Rewards

Earn unlimited 5% back at Amazon.com, Amazon Fresh, Whole Foods Market and on Chase Travel purchases with an eligible Prime membership, unlimited 2% back at gas stations, restaurants and on local transit and commuting (including rideshare), 10% back or more on a rotating selection of products and categories at Amazon.com, unlimited 1% back on all other purchases

Welcome bonus

Get a $200 Amazon Gift Card instantly upon approval exclusively for Prime members

Annual fee

$0 (but Prime membership is required)

Intro APR

Regular APR

Balance transfer fee

Either $5 or 4% of the amount of each transfer, whichever is greater.

Foreign transaction fee

Credit needed

Both new and existing cardholders can take advantage of a limited-time offer of 10% cash back on eligible gift purchases. The selection of eligible gift purchases spans multiple shopping categories, so you have a ton of choices to shop and save on.

On top of that, if you have an eligible Prime membership and either a Prime Visa or another eligible Prime card, you can now earn an extra 1% cash back on orders if you choose the No-Rush Shipping option at checkout. Since cardholders with an eligible Prime membership already earn 5% back on their Amazon purchases, this brings the total rewards potential to up to 6% cash back on your orders. This offer is valid from now through Dec. 28, 2023.

CNBC Select highlights what you need to know about the offer, details about the Amazon credit card and which purchases qualify for 10% back in rewards.

Now through Dec. 4, new Prime Visa applicants will receive a $200 Amazon gift card immediately upon approval with no minimum spending requirement. The gift card will be automatically loaded onto your Amazon account so you can use it immediately.

Prime Visa cardholders need to have an Amazon Prime account to qualify for the card, although you can still get an Amazon credit card without a Prime membership. However, non-Prime members will earn less cash back on their Amazon and Whole Foods purchases instead of the 5% enjoyed by Prime members.

But it doesn’t stop there. Cardholders can also take advantage of 10% back when purchasing items from a variety of categories, including Amazon devices, home, kitchen, electronics, furniture and more. For example, you can get 10% cash back on select Ring Video Doorbell Pro 2, Kindle e-readers, TVs and more. You can find all eligible products here but note that the 10% cash back deal expires at different times for different products.

Plus, Prime Visa and Amazon Visa cardholders can now take advantage of My Chase Plan®. My Chase Plan® is a digital feature from Chase that allows eligible cardholders to pay off a purchase (of at least $100) in fixed monthly installments over a period of time. You won’t be charged interest on the monthly amount and My Chase Plan can only be used on purchases of at least $100.

Amazon Visa and Prime Visa cardholders can now use this feature by selecting a recent transaction (remember, it needs to be at least $100) and choosing a repayment timeframe and monthly amount that works best for them.

Earn 5X Membership Rewards® Points for flights booked directly with airlines or with American Express Travel up to $500,000 on these purchases per calendar year, 5X Membership Rewards® Points on prepaid hotels booked with American Express Travel, 1X points on all other eligible purchases

Welcome bonus

Earn 80,000 Membership Rewards® Points after you spend $8,000 on purchases on your new Card in your first 6 months of Card Membership. Apply and select your preferred metal Card design: classic Platinum Card®, Platinum x Kehinde Wiley, or Platinum x Julie Mehretu.

Earn 2% on every purchase with unlimited 1% cash back when you buy, plus an additional 1% as you pay for those purchases. To earn cash back, pay at least the minimum due on time. Plus, for a limited time, earn 5% total cash back on hotel, car rentals and attractions booked on the Citi Travel℠ portal through 12/31/24

Welcome bonus

Earn $200 cash back after you spend $1,500 on purchases in the first 6 months of account opening. This bonus offer will be fulfilled as 20,000 ThankYou® Points, which can be redeemed for $200 cash back.

Annual fee

Intro APR

0% for the first 18 months on balance transfers; N/A for purchases

Regular APR

Balance transfer fee

For balance transfers completed within 4 months of account opening, an intro balance transfer fee of 3% of each transfer ($5 minimum) applies; after that, a balance transfer fee of 5% of each transfer ($5 minimum) applies

Foreign transaction fee

Credit needed

Subscribe to the CNBC Select Newsletter!

Money matters — so make the most of it. Get expert tips, strategies, news and everything else you need to maximize your money, right to your inbox. Sign up here.

If you haven’t already started thinking about holiday shopping, Amazon’s Prime Visa welcome offer might inspire you to sign up and start working your way through your list. And if the online retailer isn’t your cup of tea, don’t forget that there are plenty of 0% APR cards, travel cards, and rewards cards that help you make the most from every swipe.

For rates and fees of the Platinum Card from American Express, click here.

Information about Amazon credit cards has been collected independently by Select and has not been reviewed or provided by the issuer prior to publication; if you purchase something through Select links, we may earn a commission.

Editorial Note: Opinions, analyses, reviews or recommendations expressed in this article are those of the Select editorial staff’s alone, and have not been reviewed, approved or otherwise endorsed by any third party.

BARCELONA, SPAIN – MARCH 01: A view of the MasterCard company logo on their stand during the Mobile World Congress on March 1, 2017 in Barcelona, Spain. (Photo by Joan Cros Garcia/Corbis via Getty Images)

Mastercard is doubling down on its efforts to detect and prevent fraud that’s routed through cryptocurrency exchanges.

The company told CNBC exclusively that it’s partnered with Feedzai, a regulatory technology platform that aims to combat money laundering and financial scams online using artificial intelligence.

Through the partnership, Feedzai will integrate directly with Mastercard’s CipherTrace Armada platform, which is used to help banks monitor transactions from over 6,000 crypto exchanges for fraud, money laundering and other suspicious activity.

CipherTrace Armada will be embedded directly in Feedzai’s technology, rather than accessed through an API, or application programming interface, with Feedzai “inhaling” the data to enable real-time alerts about suspicious crypto transactions.

“This will increase fraud detection by protecting unwary consumers, but will also detect potential money laundering activity and mule accounts,” Feedzai CEO and co-founder Nuno Sebastio told CNBC. Mule accounts are accounts of users that fraudsters exploit to launder their ill-gotten funds.

An estimated 40% of scam transactions exit directly from a bank account to a crypto exchange today, according to Feedzai data.

The tie-up will also give Mastercard access to Feedzai’s artificial intelligence smarts. Feedzai says its software can identify and block suspicious transactions in a matter of nanoseconds — but also recognize transactions that are legitimate.

Feedzai’s RiskOps platform analyzes transactions worth over $1.7 trillion annually. Co-headquartered in Coimbra, in Portugal, and San Mateo, California, in Silicon Valley, the firm holds close to 100 patents and secures an average of 10 patents per year to safeguard its technology.

“Numerous banks that believe they are preventing illegitimate cryptocurrency transactions are, in fact, only blocking transactions involving the widely recognised and regulated entities within the crypto space and omitting the rest,” Sebastio said.

The move marks a push from Mastercard into the market for legitimizing crypto as a mainstream financial asset that can be subjected to the same rules and compliance frameworks as traditional assets.

Banks and other large financial institutions have shown increased interest in experimenting with crypto in their products and services. But the next step, deploying commercially available crypto products as part of their core offerings, has proven more elusive.

Banks have been wary of digital assets’ lack of comprehensive regulations and applications in fraud and scams.

Last year, the amount of theft and scams led to a global increase of 79% in crypto-related losses from the previous year, according to data from blockchain analysis firm Chainalysis. Illicit addresses received $14 billion in 2022 year-over-year, almost twice what they received in 2020.

Mastercard’s vast network is used by banking institutions worldwide to process and monetize payments.

The company competes with fellow payments giant Visa, which is also in the business of supporting card payments, among other fintech services.

In the U.K., banks have shown hesitation when it comes to being associated with crypto. Several larger lenders have halted transactions with crypto exchanges on their networks, citing the risk of fraud.

Top banks including JPMorgan, NatWest, and HSBC have restricted or blocked crypto transactions. This led to criticisms from Coinbase CEO Brian Armstrong, who said the development jarred with the U.K.’s ambition to become a global “Web3” hub.

Ajay Bhalla, president of cyber and intelligence solutions for Mastercard, told CNBC that the “interconnectedness of life today and increasing digital penetration of finance has brought risk as well as opportunity.”

“Our latest data shows fraud on transactions where people are buying crypto is 5 times higher than regular fiat transactions,” Bhalla said via email, adding that, with Mastercard’s new tie-up with Feedzai, financial institutions will “be able to tell good transactions from bad.”

The partnership builds on Mastercard’s deal to acquire U.S. blockchain sleutching firm CipherTrace. Mastercard bought CipherTrace in 2021, and the following year launched its first product using the firm’s technology, called CryptoSecure, to analyze and block transactions from fraud-prone crypto exchanges.

BARCELONA, SPAIN – MARCH 01: A view of the MasterCard company logo on their stand during the Mobile World Congress on March 1, 2017 in Barcelona, Spain. (Photo by Joan Cros Garcia/Corbis via Getty Images)

SINGAPORE — There isn’t enough justification for the widespread use of central bank digital currencies right now, which makes broad adoption of such assets “difficult,” Ashok Venkateswaran, Mastercard‘s blockchain and digital assets lead for Asia-Pacific, told CNBC.

“The difficult part is adoption. So if you have CBDCs in your wallet, you should have the ability for you to spend it anywhere you want – very similar to cash today,” said Venkateswaran on the sidelines of Singapore FinTech Festival on Wednesday.

A retail CBDC, which is the digital form of fiat currency issued by a central bank, caters to individuals and businesses, facilitating everyday transactions. This is different from a wholesale CBDC which is used exclusively by central banks, commercial banks and other financial institutions to settle large-value interbank transactions.

The International Monetary Fund has said that CBDCs are “a safe and low-cost alternative” to cash, with approximately 60% of countries in the world exploring CBDCs. However, only 11 countries have adopted them, with an additional 53 in advanced planning stages and 46 researching the topic as of June, according to data from the Atlantic Council.

“But [building infrastructure to facilitate that] takes a lot of time and effort on a part of the country to do that. But a lot of the central banks nowadays have gotten very innovative because they are working very closely with private companies like ours, to create that ecosystem,” said the Asia-Pacific lead.

Even then, Venkateswaran said consumers are “so comfortable using today’s type of money” such as paper money and coins, that “there isn’t enough justification to have a CBDC.”

Mastercard, the second-largest card network in the U.S., said last week it has completed testing of its solution in the Hong Kong Monetary Authority’s e-HKD pilot program to simulate the use of a retail CBDC such as electronic Hong Kong dollars.

Hong Kong’s CBDC sandbox facilitates the trial of minting, distributing and spending of e-HKD within the program.

A total of 16 companies across the financial, payments and technology sectors including Mastercard participated in the pilot. Mastercard’s rival Visa also took part in the project alongside HSBC Bank and Hang Seng Bank, testing the viability of tokenized deposits in business-to-business payments.

Venkateswaran cited Singapore as an example where the case for retail CBDC is not compelling enough as the city-state has a “very efficient” payments system.

Last year, the IMF’s deputy managing director Bo Li named Singapore and Thailand as the countries in Asia which have made “quick progress” by connecting fast payment systems, therefore lowering transaction fees for cross-border payments.

“There isn’t a reason for a retail CBDC [in Singapore] but there is a case for a wholesale CBDC for interbank settlements,” said Venkateswaran.

During the pilot, the Monetary Authority of Singapore will collaborate with domestic banks to test the use of wholesale CBDCs to facilitate domestic payments, said the managing director of the Monetary Authority of Singapore, Ravi Menon.

It really depends on the need of the country or what problem they are trying to solve, said Mastercard’s Venkateswaran.

It won’t work “if you’re only trying to replace your existing domestic payment network,” he said.

“But if it’s a country where the domestic payment network is not as robust, it may make sense to have a CBDC.”

An Amazon.com Inc worker prepares an order in which the buyer asked for an item to be gift wrapped at a fulfillment center in Shakopee, Minnesota, U.S., November 12, 2020.

Amazon.com Inc | Reuters

The initial third-quarter report on gross domestic product showed consumer spending zooming higher by 4% percent a year, after inflation, the best in almost two years. September’s retail sales report showed spending climbing almost twice as fast as the average for the last year. And yet, bears like hedge-fund trader Bill Ackman argue that a recession is coming as soon as this quarter and the market has entered correction territory.

For an economy that rises or falls on the state of the consumer, third-quarter earnings data supports a view of spending that remains mostly good. S&P 500 consumer-discretionary companies that have reported through Oct. 25 saw an average profit gain of 15%, according to CFRA — the biggest revenue gain of the stock market’s 11 sectors.

“People are kind of scratching their heads and saying, ‘The consumer is holding up better than expected,'” said CFRA Research strategist Sam Stovall said. “Consumers are employed. They continue to buy goods as well as pursue experiences. And they don’t seem worried about debt levels.”

How is this possible with interest rates on everything from credit cards to cars and homes soaring?

It’s the anecdotes from bellwether companies across key industries that tell the real story: Delta Air Lines and United Airlines sharing how their most expensive seats are selling fastest. Homeowners using high-interest-rate-fighting mortgage buydowns. Amazon saying it’s hiring 250,000 seasonal workers. A Thursday report from Deckers Outdoor blew some minds — in what has been a tepid clothing sales environment — by disclosing that embedded in a 79% profit gain that sent shares up 19% was sales of Uggs, a mature line anchored by fuzzy boots, rising 28%.

The picture they paint largely matches the economic data — generally positive, but with some warts. Here is some of the key evidence from from the biggest company earnings reports across the market that help explain how companies and the American consumer are making the best of a tough rate environment.

How homebuilders are solving for mortgages rates

No industry is more central to the market’s notion that the consumer is falling from the sky than housing, because the number of existing home sales have dropped almost 40% from Covid-era peaks. But while Coldwell Banker owner Anywhere Real Estate saw profit fall by half, news from builders of new homes has been pretty good.

Most consumers have mortgages below 5%, but for new homebuyers, one reason that rates are not biting quite as sharply as they should is that builders have figured out ways around the 8% interest rates that are bedeviling existing home sellers. That helps explains why new home sales are up this year. Homebuilders are dipping into money that previously paid for other incentives to pay for offering mortgages at 5.75% rather than the 8% level other mortgages have hit. At PulteGroup, the nation’s third-biggest builder, that helped drive an 8% third-quarter profit jump and 43% climb in new home orders for delivery later, much better than the government-reported 4.5% gain in new home sales year-to-date.

“What we’ve done is simply redistribute incentives we’ve historically offered toward cabinets and countertops, and redirected those to interest rate incentives,” PulteGroup CEO Ryan Marshall said. “And that has been the most powerful thing.”

The mechanics are complex, but work out to this: Pulte sets aside about $35,000 for incentives to get each home to sell, or about 6% of its price, the company said on its earnings conference call. Part of that is paying for a mortgage buydown. About 80% to 85% of buyers are taking advantage of the buydown offer. But many are splitting the funds, mixing a smaller rate buydown and keeping some goodies for the house, the company said.

Wells Fargo economist Jackie Benson said in a report that builders may struggle to keep this strategy going if mortgage rates stay near 8%, but new-home prices have dropped 12% in the last year. In her view, incentives plus bigger price cuts than most existing homes’ owners will offer is giving builders an edge.

At auto companies, price cuts are in, and more are coming

Car sales picked up notably in September, rising 24% year-over-year, more than twice the year-to-date gain in unit sales. But they were below expectations at electric-vehicle leader Tesla, which blamed high interest rates, and at Ford.

“I just can’t emphasize this enough, that for the vast majority of people buying a car it’s about the monthly payment,” Tesla CEO Elon Musk said on its earnings call. “And as interest rates rise, the proportion of that monthly payment that is interest increases.”

Maybe, but that’s not what’s happening at General Motors, even if investor reaction to good numbers at GM was muted because of the strike by the United Auto Workers union.

GM beat earnings expectations by 40 cents a share, but shares fell 3% because of investor worries about the strike, which forced GM to withdraw its fourth-quarter earnings forecast on Oct. 24. Ford, which settled with the UAW on Oct. 25, said the next day it had a “mixed” quarter, as profit missed Wall Street targets due to the strike. Consumers came through, as unit sales rose 7.7% for the quarter, with truck and EV sales both up 15%. GM CEO Mary Barra said on GM’s analyst call that the company gained market share, posting a 21% gain in unit sales despite offering incentives below the industry average.

“While we hear reports out there in the macro that consumer sentiment might be weakening, etc., we haven’t seen that in demand for our vehicles,” GM CFO Paul Jacobson told analysts. But Ford CFO John Lawler said car prices need to decline by about $1,800 to be as affordable as they were before Covid. “We think it’s going to happen over 12 to 18 months,” he said.

Tesla’s turnaround plan turns on continuing to lower its cost of producing cars, which came down by about $2,000 per vehicle in last year, the company said. Along with federal tax credits for electric vehicles, a Model Y crossover can be had for about $36,490, or as little as $31,500 in states with local tax incentives for EVs. That’s way below the average for all cars, which Cox Automotive puts at more than $50,000. But Musk says some consumers still aren’t convincible. .

“When you look at the price reductions we’ve made in, say, the Model Y, and you compare that to how much people’s monthly payment has risen due to interest rates, the price of the Model Y is almost unchanged,” Musk said. “They can’t afford it.”

Most banks say the consumer still has cash, but not Discover

To know how consumers are doing, ask the banks, which disclose consumer balances quarterly. To know if they’re confident, ask the credit card companies (often the same companies) how much they are spending.

In most cases, financial services firms say consumers are doing well.

At Bank of America, consumer balances are still about one-third higher than before Covid, CEO Brian Moynihan said on the company’s conference call. At JPMorgan Chase, balances have eroded 3% in the last year, but consumer loan delinquencies declined during the quarter, the company said.

“Where am I seeing softness in [consumer] credit?” said chief financial officer Jeremy Barnum, repeating an analyst’s question on the earnings call. “I think the answer to that is actually nowhere.”

Among credit card companies, the “resilient” is still the main story. MasterCard, in fact, used that word or “resilience” eight times to describe U.S. consumers in its Oct. 26 call.

“I mean, the reality is, unemployment levels are [near] all-time record lows,” MasterCard chief financial officer Sachin Mehra said.

At American Express, which saw U.S. consumer spending rise 9%, the mild surprise was the company’s disclosure that young consumers are adding Amex cards faster than any other group. Millennials and Gen Zers saw their U.S. spending via Amex rise 18%, the company said.

“Guess they’re not bothered by the resumption of student loan payments,” Stovall said.

The major fly in the ointment came from Discover Financial Services, one of the few banks to make big additions to its loan loss reserves for consumer debt, driving a 33% drop in profit as Discover’s loan chargeoffs doubled.

Despite the fact that U.S. household debt burdens are almost exactly the same as in late 2019, and declined during the quarter, according to government data, Discover chief financial officer John Greene said on its call, “Our macro assumptions reflect a relatively strong labor market but also consumer headwinds from a declining savings rate and increasing debt burdens.”

At airlines, still no sign of a travel recession

It’s good to be Delta Air Lines right now, sitting on a 59% third-quarter profit gain driven by the most expensive products on their virtual shelves: First-class seats and international vacations. Also good to be United, where higher-margin international travel rose almost 25% and the company is planning to add seven first-class seats per departure by 2027. Not so good to be discounter Spirit, which saw shares fall after reporting a $157 million loss.

“With the market continuing to seemingly will a travel recession into existence despite evidence to the contrary from daily [government] data and our consumer surveys, Delta’s third-quarter beat and solid fourth-quarter guide and commentary should finally put the group at ease about a consumer “cliff,” allow them to unfasten their seatbelts and walk about the cabin,” Morgan Stanley analyst Ravi Shanker said in a note to clients.

One tangible impact: United is adding 20 planes this quarter, though it is pushing 12 more deliveries into 2024, while Spirit said it’s delaying plane deliveries, and focusing on its proposed merger with JetBlue and cost-cutting to regain competitiveness as soft demand for its product persists into the holiday season.

As has been the case throughout much of 2023, richer consumers — who contribute the greater share of spending — are doing better than moderate-income families, Sundaram said.

The goods recession is for real

Whirlpool, Ethan Allen and mattress maker Sleep Number all saw their stocks tumble after reporting bad earnings, all of them experiencing sales struggles consistent with the macro data.

This follows a trend now well-entrenched in the economy: people stocked up on hard goods, especially for the house, during the pandemic, when they were stuck at home more. All three companies saw shares surge during Covid, and growth has slacked off since as they found their markets at least partly saturated and consumers moved spending to travel and other services.

“All of the stimulus money went to the furniture industry,” Sundaram said, exaggerating for effect. “Now they’ve been falling apart for the last year.”

Ethan Allen sales dropped 24%, as the company said a flood in a Vermont factory and softer demand were among the causes. At Whirlpool, which said in second-quarter earnings that it was moving to make up slowing sales to consumers by selling more appliances to home builders, “discretionary purchases have been even softer than anticipated, as a result of increased mortgage rates and low consumer confidence,” CEO Marc Bitzer said during Thursday’s earnings call. Its shares fell more than 20%.

Amazon’s $1.3 billion holiday hiring spree

Amazon is making its biggest-ever commitment to holiday hiring, spending $1.3 billion to add the workers, mostly in fulfillment centers.

That’s possible because Amazon has reorganized its warehouse network to speed up deliveries and lower costs, sparking 11% sales gains the last two quarters as consumers turn to the online giant for more everyday repeat purchases. Amazon also tends to serve a more affluent consumer who is proving more resilient in the face of interest rate hikes and inflation than audiences for Target or dollar stores, according to CFRA retailing analyst Arun Sundaram said.

“Their retail sales are performing really well,” Sundaram said. “There’s still headwinds affecting discretionary sales, but everyday essentials are doing really well.

All of this sets the stage for a high-stakes holiday season.

PNC still thinks there will be a recession in early 2024, thanks partly to the Federal Reserve’ rate hikes, and thinks investors will focus on sales of goods looking for more signs of weakness. “There’s a lot of strength for the late innings” of an expansion, said PNC Asset Management chief investment officer Amanda Agati.