Friday, Oct. 10, witnessed the worst wipeout in the crypto market after President Donald Trump threatened to impose a 100% tariff on imports from China to the U.S.

The total crypto market capitalization fell from $4.1 trillion to $3.6 trillion within hours of the announcement. Bitcoin also fell from above $122,000 to $105,000 during the crash, with other cryptocurrencies following suit.

On Monday, Oct. 13 there are signs of a recovery. The total market cap has recovered to $3.8 trillion, with Bitcoin trading well above the $114,500 price mark.

But crypto analysts say it’s too early to take a sigh of relief.

A popular crypto analyst, with the handle on X, warned the trading community to exit the market as a “big dump” is coming on Oct. 13 in which both Bitcoin and altcoins will crash.

Another popular crypto analyst, known as @Prosperous_w_ on X, shared their views on the social media platform.

While many altcoins hit their “absolute bottom” on Friday, most altcoins are still trading well above their bottoms and will see further correction, they said. For example, SUI will see a 42% correction again, they predicted.

U.S. President Donald Trump holds up a chart while speaking during a “Make America Wealthy Again” trade announcement event in the Rose Garden at the White House on April 2, 2025 in Washington, DC. Touting the event as “Liberation Day”, Trump is expected to announce additional tariffs targeting goods imported to the U.S.

The market will now see strong resistance zones. Early buyers from the crash are accumulating profits and traders who short are entering the fray, they highlighted.

“This combo usually brings another hard correction. I expect altcoins to pull back 20–50% from current levels.”

@Prosperous_w_ also predicted “one more leg down” for Bitcoin. They rejected the theory that this is the beginning of a bear market following the 4-year cycle trend. The market now instead follows the liquidity cycle and the business cycle and this cycle will continue well into 2026, they predicted.

The analyst also shared their own trading plan for the future. They are “accumulating heavily” around current prices and flash crash lows. The future positions range from 5x to25x leverage, with higher leverage reserved for short-term trades and lower leverage for swing trades to hold into the next expansion phase.

Any trading profits or cash are stored in Bitcoin, @Prosperous_w_ shared with their followers.

“The USD, EUR, and most fiat currencies will continue to lose value. Bitcoin is the ultimate liquidity base and hedge in this evolving economy.”

Disclaimer: The information provided here is for general informational purposes only and should not be considered financial advice. You should consult with a licensed financial advisor before making any investment or financial decisions.

Elon Musk, already the world’s richest person, could become the first trillionaire after the Tesla board unveiled a massive new pay package for its CEO to keep his focus on the troubled EV maker.The package would grant him additional shares of Tesla stock if the company is able to grow far beyond its current value, with a market capitalization far greater than any company has ever approached. Musk’s previous pay package, which added significantly to his massive wealth, also laid out ambitious growth plans that once appeared to be a reach – but which Tesla proved able to reach easily.The new pay package could grant Musk 423.7 million additional shares of Tesla stock. Those shares would be worth $143.5 billion at today’s stock value.But Musk would get those shares only if the value of Tesla stock increases significantly in coming years. The company stock would need to reach an overall value of $8.5 trillion for Musk to get all the shares, significantly above the current market capitalization of $1.1 trillion and roughly double the current market value of Nvidia (NVDA), the current most-valuable company on the market.The company’s proxy statement that laid out Musk’s payment plan also included a shareholder proposal that Tesla take a stake in privately-held xAI, the artificial intelligence company that Musk also owns. That could help Elon Musk further consolidate his growing business empire.XAI recently purchased X, the social media platform formerly known as Twitter, which Musk bought for $44 billion of his own money in 2022. The company did not take a position for or against that shareholder proposal, which does not give any details of how large a stake Tesla should take in xAI, and at what price.Musk currently owns 410 million shares of Tesla shares, worth $139 billion at Thursday’s closing price. That stake, along with his stakes in xAI, rocket company SpaceX, and several other companies he has started and runs, have made him the richest person on the planet, worth $378 billion according to Bloomberg’s billionaire tracker.He currently has options to buy an additional 304 million shares of Tesla, but a judge in Delaware has twice struck down that 2018 pay package that granted him those options as illegal. Those rulings came despite overwhelming approval by Tesla shareholders – twice. The company again has tried to grant those options to Musk this year, and adding in those options, he now owns 18% of the company’s shares.Tesla shares nearly doubled in value to a record-high price for its shares between election day and mid-December 2024, as investors bet that his close ties to President Donald Trump would be a boon for Tesla. But as Tesla faced protests and dropping sales and falling profits in backlash to those ties (before he had a falling out with Trump), all those things resulted in Tesla’s stock losing those gains. The shares have recovered some of those losses, but they are still down 26% from the December peak.Still, Musk and his fans on Wall Street have insisted the company is well positioned to grow even larger and more successful in the future. He has continued to predict that his plans for self-driving cars – including a robotaxi service – will create massive profits and value for shareholders. The robotaxis would provide rides to passengers and also allow Tesla owners to rent out their cars for driverless rides when not in use.Musk has also promised a line of humanoid robots that could bring in even more sales than Tesla’s car business.“It’s a big pay package but Tesla needs to keep its biggest asset in Musk as CEO,” Wedbush Securities analyst Dan Ives told CNN Friday. Ives is one of the bigger Tesla bulls on Wall Street.“In this AI era Musk now will drive its next leg of growth,” Ives added. “The Board had a $1 trillion dollar decision and made the right one.”The board’s proxy statement spoke of the importance of keeping Musk focused on Tesla going forward. In addition to his many business interests, he remains active in politics, despite his falling out with President Trump. He has announced plans to form a third political party.Tesla, in its proxy statement, warned that it needed to incentivize Musk to focus his attention on growing the company. It said that during the negotiations on the pay package, “Musk also raised the possibility that he may pursue other interests that may afford him greater influence if he did not receive such assurances.”The board said it “believes that Mr. Musk singularly possesses the leadership characteristics necessary to transform Tesla and realize its long-term mission at an unparalleled level.”But, so far, those big ambitions have all been grand claims from a man and company that have often fallen short of their promises. Tesla is facing growing competition from Chinese EV makers. BYD, one of those Chinese automakers, is poised to pass Tesla for the most EV sales worldwide, even though it is not available for sale in the United States.Tesla also faces competition from other companies that are ahead of it in providing robotaxi services, including Waymo, the autonomous vehicle unit of Google parent Alphabet, which has its own service and has partnered with Uber in some cities.Shares of Tesla (TSLA) were slightly higher in premarket trading on the news.

Elon Musk, already the world’s richest person, could become the first trillionaire after the Tesla board unveiled a massive new pay package for its CEO to keep his focus on the troubled EV maker.

The package would grant him additional shares of Tesla stock if the company is able to grow far beyond its current value, with a market capitalization far greater than any company has ever approached. Musk’s previous pay package, which added significantly to his massive wealth, also laid out ambitious growth plans that once appeared to be a reach – but which Tesla proved able to reach easily.

The new pay package could grant Musk 423.7 million additional shares of Tesla stock. Those shares would be worth $143.5 billion at today’s stock value.

But Musk would get those shares only if the value of Tesla stock increases significantly in coming years. The company stock would need to reach an overall value of $8.5 trillion for Musk to get all the shares, significantly above the current market capitalization of $1.1 trillion and roughly double the current market value of Nvidia (NVDA), the current most-valuable company on the market.

The company’s proxy statement that laid out Musk’s payment plan also included a shareholder proposal that Tesla take a stake in privately-held xAI, the artificial intelligence company that Musk also owns. That could help Elon Musk further consolidate his growing business empire.

XAI recently purchased X, the social media platform formerly known as Twitter, which Musk bought for $44 billion of his own money in 2022. The company did not take a position for or against that shareholder proposal, which does not give any details of how large a stake Tesla should take in xAI, and at what price.

Musk currently owns 410 million shares of Tesla shares, worth $139 billion at Thursday’s closing price. That stake, along with his stakes in xAI, rocket company SpaceX, and several other companies he has started and runs, have made him the richest person on the planet, worth $378 billion according to Bloomberg’s billionaire tracker.

He currently has options to buy an additional 304 million shares of Tesla, but a judge in Delaware has twice struck down that 2018 pay package that granted him those options as illegal. Those rulings came despite overwhelming approval by Tesla shareholders – twice. The company again has tried to grant those options to Musk this year, and adding in those options, he now owns 18% of the company’s shares.

Tesla shares nearly doubled in value to a record-high price for its shares between election day and mid-December 2024, as investors bet that his close ties to President Donald Trump would be a boon for Tesla. But as Tesla faced protests and dropping sales and falling profits in backlash to those ties (before he had a falling out with Trump), all those things resulted in Tesla’s stock losing those gains. The shares have recovered some of those losses, but they are still down 26% from the December peak.

Still, Musk and his fans on Wall Street have insisted the company is well positioned to grow even larger and more successful in the future. He has continued to predict that his plans for self-driving cars – including a robotaxi service – will create massive profits and value for shareholders. The robotaxis would provide rides to passengers and also allow Tesla owners to rent out their cars for driverless rides when not in use.

Musk has also promised a line of humanoid robots that could bring in even more sales than Tesla’s car business.

“It’s a big pay package but Tesla needs to keep its biggest asset in Musk as CEO,” Wedbush Securities analyst Dan Ives told CNN Friday. Ives is one of the bigger Tesla bulls on Wall Street.

“In this AI era Musk now will drive its next leg of growth,” Ives added. “The Board had a $1 trillion dollar decision and made the right one.”

The board’s proxy statement spoke of the importance of keeping Musk focused on Tesla going forward. In addition to his many business interests, he remains active in politics, despite his falling out with President Trump. He has announced plans to form a third political party.

Tesla, in its proxy statement, warned that it needed to incentivize Musk to focus his attention on growing the company. It said that during the negotiations on the pay package, “Musk also raised the possibility that he may pursue other interests that may afford him greater influence if he did not receive such assurances.”

The board said it “believes that Mr. Musk singularly possesses the leadership characteristics necessary to transform Tesla and realize its long-term mission at an unparalleled level.”

But, so far, those big ambitions have all been grand claims from a man and company that have often fallen short of their promises. Tesla is facing growing competition from Chinese EV makers. BYD, one of those Chinese automakers, is poised to pass Tesla for the most EV sales worldwide, even though it is not available for sale in the United States.

Tesla also faces competition from other companies that are ahead of it in providing robotaxi services, including Waymo, the autonomous vehicle unit of Google parent Alphabet, which has its own service and has partnered with Uber in some cities.

Shares of Tesla (TSLA) were slightly higher in premarket trading on the news.

Apple is the most valuable company in the world right now with a market capitalization of $3.4 trillion, but it’s closely followed by two other tech giants, Microsoft(NASDAQ: MSFT) and Nvidia(NASDAQ: NVDA). It’s worth noting that both Microsoft and Nvidia have taken turns becoming the world’s most valuable company this year, but Apple has managed to regain the top spot, thanks to a recent surge in the stock price.

However, if we compare Apple’s prospects to those of Nvidia and Microsoft for the next five years, it won’t be surprising to see them becoming more valuable than the iPhone maker. Below is a look at the reasons why.

1. Microsoft

Microsoft’s market cap of $3.3 trillion means that it’s strikingly close to Apple right now. More importantly, Microsoft is clocking faster growth than Apple, a trend that’s likely to continue over the next five years, thanks to the growing adoption of artificial intelligence (AI) in multiple markets.

For instance, Microsoft’s revenue in the third quarter of fiscal 2024 (which ended on March 31) increased 17% year over year to $61.9 billion. Meanwhile, Apple’s fiscal 2024 second-quarter revenue (for the three months ended March 30) was down 4% year over year to $90.8 billion. This stark difference in the performance of the two tech giants is largely due to AI.

While Microsoft is capitalizing on multiple AI-driven growth trends such as cloud computing, personal computers (PCs), and workplace collaboration tools, Apple has been late to the AI smartphone market. Microsoft’s Intelligent Cloud segment reported a 21% year-over-year increase in revenue in fiscal Q3 to $26.7 billion, driven by the growing usage of its cloud-based AI services.

The company pointed out that its Azure cloud business received a boost of 7 percentage points, thanks to AI. The cloud-based AI services market is forecast to generate $647 billion in revenue in 2030, clocking a compound annual growth rate of nearly 40% through the end of the decade, and Microsoft is sitting on a potentially large incremental revenue opportunity in this market.

Also, Microsoft Azure’s 25% share of the cloud computing market means that it’s well-placed to tap this multibillion-dollar AI opportunity. But this isn’t where the AI-driven catalysts end for Microsoft. The company’s Copilot generative AI chatbot, which serves both individual and business users, is witnessing healthy adoption.

For example, Microsoft’s Copilot for GitHub, a developer platform used by more than 100 million users, boasted of 1.8 million paid subscribers at the end of March. Meanwhile, the enterprise adoption of Copilot for workplace productivity remains solid. In the words of CEO Satya Nadella:

This quarter, we made Copilot available to organizations of all types and sizes from enterprises to small businesses, nearly 60% of the Fortune 500 now use Copilot and we have seen accelerated adoption across industries and geographies with companies like Amgen, BP, Cognizant, Koch Industries, Moody’s, Novo Nordisk, Nvidia, and Tech Mahindra purchasing over 10,000 seats.

Microsoft is charging $30 per user per month from enterprise customers for its Copilot. The individual plan is priced at $20 per user per month. So the company is already monetizing the AI-assistant market, which is expected to grow eightfold over the next decade and generate almost $167 billion in revenue in 2033.

The above AI-related catalysts indicate why Microsoft’s annual earnings are expected to grow at 16% a year for the next five years compared to Apple’s projected growth rate of 10%. This could eventually help Microsoft stock deliver more upside and become more valuable than Apple in the long run.

2. Nvidia

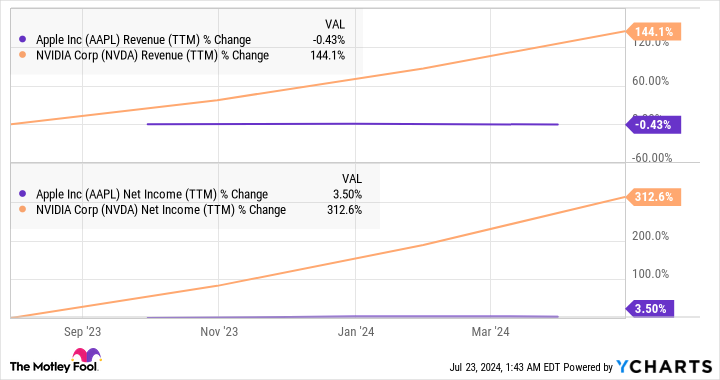

Nvidia is currently the third-largest company in the world, with a market cap of $3 trillion. Shares of the semiconductor specialist have surged a remarkable 745% since the beginning of 2023 as the likes of Microsoft and other tech giants have been looking to get their hands on its AI graphics processing units (GPUs) to train and deploy AI models and services.

More importantly, Nvidia controls over 90% of the AI chip market. This terrific market share is the reason behind its outstanding growth in recent quarters, resulting in a much better financial performance than Apple.

AAPL Revenue (TTM) Chart

With the global AI chip market estimated to grow tenfold in the next 10 years to become a $300 billion market, there’s a good chance that Nvidia’s outstanding growth will continue. According to some analysts, the company’s data center revenue alone could jump to $280 billion over the next four years from $47.5 billion in the previous fiscal year.

Throw in additional catalysts, such as the recovery in the PC market thanks to the adoption of AI-enabled PCs (which has started lifting Nvidia’s gaming business), and it’s easy to see why analysts are estimating Nvidia’s earnings to increase at 46% a year for the next five years. That’s significantly faster than the growth Apple is expected to deliver over the same period.

Of course, Apple could get a shot in the arm, thanks to the emergence of AI smartphones, but investors should note that the company is operating in a very competitive market. In the second quarter of 2024, Apple’s smartphone market share stood at 15.8%, down from 16.6% in the same quarter in 2023. Its shipments grew only 1.5% year over year as compared to the overall smartphone-market’s growth of 6.5%.

It’s easy to see why Nvidia’s growth is expected to be faster as it leads the AI chip market, while Apple operates in a crowded space where rivals have acted with alacrity in jumping onto the AI bandwagon. As such, the possibility of Nvidia overtaking Apple’s market share over the next five years, thanks to its faster bottom-line growth, can’t be ruled out, and AI is going to play a central role in helping the semiconductor company achieve that.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $692,784!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple, BP, Microsoft, Moody’s, and Nvidia. The Motley Fool recommends Amgen, Cognizant Technology Solutions, and Novo Nordisk and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

(Bloomberg) — Investors looking for an end to the freefall in shares of Chinese e-commerce company Alibaba Group Holding Ltd. may be in for a long wait, if options traders are correct.

Most Read from Bloomberg

The stock’s 75% tumble from a 2020 record high has driven its valuation to an all-time low and put its market capitalization on a par with upstart rival PDD Holdings Inc. The derivatives market indicates further pain, with the options skew showing increased bearishness ahead of Alibaba’s earnings report due Wednesday.

A put contract betting the stock will drop more than 10% by the end of April was the most traded on Monday. Still, the shares climbed as much as 7% in Hong Kong on Tuesday amid some optimism for positive earnings, especially given the fact that the company moved forward its reporting date.

Alibaba’s revenue for the three months through December is expected to have risen 5.6% from a year ago, the slowest growth in three quarters amid difficult economic conditions and steep discounting. Forward earnings estimates for the company have fallen about 4% over the past month.

China’s online retail market has grown crowded, with stalwarts Alibaba and JD.com Inc. facing new entrants including Douyin Mall, run by TikTok owner ByteDance Ltd. At the same time, persistent deflationary pressure and declining wages have driven a price war that is being won by discounters like Pinduoduo, the local equivalent of PDD’s Temu.

“The focus is whether Alibaba can survive the macro weakness,” said Tam Tsz-Wang, analyst at DBS Vickers Hong Kong Ltd. “The market is expecting it to lose market share as they face fierce competition from rivals like Douyin and PDD. Another focus would be whether they are able to import new drivers to maintain their overall growth.”

The stock is trading at 8 times forward earnings, near its lowest valuation ever and making it one of the cheapest technology stocks in China. In comparison, Hong Kong-listed utility CLP Holdings Ltd. is trading at around 13 times expected earnings, as is the Hang Seng Tech Index.

Alibaba spent $9.5 billion on share buybacks last year, a record high, according to data compiled by Bloomberg, and says it still has about $12 billion remaining through 2025 to spend on repurchases. The firm may spend half of its free cash flow on buybacks and could also announce special dividends after business divestments, according to Goldman Sachs Group Inc. analyst Ronald Keung. He maintains a buy rating on Alibaba, citing its attractive valuation.

Options traders are less sanguine, with the trading volume of put options spiking in recent days. The market is pricing in a 5.6% share move in either direction in the immediate aftermath of Wednesday’s results, which would be one of the biggest post-earnings moves for the stock in two years.

Revamp efforts led by the company’s new management include scaling down non-core business while stepping up investment in global expansion and artificial intelligence. It’s focusing on improving core operations, including moving resources from its Tmall site to Taobao in order to better meet demand for cheaper products, though it may take time to see results.

This focus on lower prices will lead to weaker revenue growth, which “is certainly negative to near-term sentiment and share price,” said JPMorgan Chase & Co. analysts including Alex Yao, who cut his estimate for Alibaba’s profit for the current year by 3% last month. The company’s core business growth will likely “remain lackluster in the next four quarters.”

Top Tech News

Potential investors in Elon Musk’s new artificial intelligence startup, xAI, are focusing on two key selling points: access to the billionaire’s constellation of companies — referred to as the “Muskonomy” — and the early success of one of its biggest competitors, OpenAI.

Palantir Technologies Inc. said that demand for its artificial intelligence products was driving sales, and gave a higher-than-expected profit outlook for 2024. The company’s shares climbed more than 15% in after-hours trading.

The Japanese government will provide an additional ¥150 billion ($1 billion) in support to a chipmaking joint venture between Kioxia Holdings Corp. and Western Digital Corp., the latest push by the country to bolster its domestic semiconductor industry.

(Updates with Alibaba’s stock move Tuesday, adds Top Tech News section)

(Bloomberg) — Alibaba Group Holding Ltd.’s market value has slumped to only about half that of rival Tencent Holdings Ltd. as the former’s e-commerce-centric business faces sluggish demand and intensified competition.

Most Read from Bloomberg

Alibaba, whose other main business line includes cloud computing, has a market capitalization of $201 billion, while Tencent, focused on social media and gaming, is valued at $391 billion, according to data compiled by Bloomberg. Alibaba’s shares now trade around eight times forward earnings multiples, versus 16 times for Tencent.

Alibaba on Thursday abruptly ended its plan to spin off its cloud unit, citing heightened US restrictions on chip sales to China. The announcement, along with lower-than-expected domestic e-commerce sales, sent the stock tumbling about 10% in Hong Kong, its largest decline this year.

The divergence in the market value of the two companies also highlights some of the regulatory and macroeconomic issues that have troubled Alibaba. In recent years, China has sought to rein in the country’s tech giants, with regulators probing Alibaba affiliate Ant Group Co. and imposing a $1 billion fine on the fintech company backed by Jack Ma. Its market value had largely been higher than Tencent before the crackdown started in late 2020.

Tencent earlier this week reported better-than-expected profitability across its main business lines for the third quarter. The Chinese social media operator delivered growth across divisions from gaming and advertising to fintech, driving a 10% increase in revenue.

“China’s tepid consumption recovery and the heightened competition in the e-commerce space all make it harder for Alibaba’s business environment,” said Willer Chen, a senior analyst at Forsyth Barr Asia Ltd. “There were also greater regulatory concerns for Alibaba earlier that weighed on investors sentiment.”

(An earlier version corrected day to Thursday in third paragraph)

Opinions expressed by Entrepreneur contributors are their own.

Even the most novice degens know that the only rule that applies to cryptocurrency markets is that there are no rules. Not even the world’s brightest minds can outpace the mayhem that is the world of digital assets. One minute, Michael Saylor and Microstrategy could be live on CNBC discussing their latest billion-dollar Bitcoin purchase, and the next, Jim Cramer could be telling America that he’d never touch Bitcoin with a ten-foot pole, only a couple of weeks after calling it digital gold — it’s crazy.

The market has been rather uninteresting due to asset prices traveling sideways for the better part of this year. Nevertheless, hope in the vision of the Federal Reserve’s mythical “soft” landing, combined with the upcoming Bitcoin halving, has the Web3 community salivating at the prospect of many life-changing opportunities that could be within reach soon. With greed in the air, it would be foolish to ignore the difference in the landscape as the market sentiment shifts.

Whether it’s the likes of BlackRock looking to issue ETFs to commercialize crypto exposure, corporate adoption, multiple IPOs, the rise of artificial intelligence or the attempted onslaught of regulation, there hasn’t ever been this much discourse around the digital asset class. That’s exactly why you need to know three key things to capitalize on what’s to come.

One of the most common mistakes prospective investors make, regardless of the target market, is outsourcing critical thinking skills instead of developing their own. Most investors would rather follow someone else’s investment decisions instead of doing their own analysis.

That’s not to say that there is anything wrong with seeking the guidance of someone with more experience; however, it’s important to remember that finances, goals, and risk appetite vary from person to person. Blindly following anyone’s advice, no matter who they are, is a surefire way to make losing trades. Instead, cultivate the ability to ascertain the fair market value of an asset so that you can capitalize on whatever arbitrage opportunities exist within a given market.

During times of prosperity, it’s quite common for novice investors to fall victim to scams. Whether it’s a personal security issue gone wrong that leads to a complete loss of funds or being fooled into investing heavily in a meme coin pump-and-dump, it’s important to remember that there’s no such thing as easy money. Being equipped with the tools to properly evaluate the viability of an investment on its merit alone is the biggest key to financial freedom.

2. Crypto’s tiny!

As I write this article, the crypto market capitalization (i.e., the total size) is hovering around $1 trillion. By all accounts, this is an outrageously large number for an asset class still unacknowledged by some of the nation’s elite. However, it pales compared to the vast majority of other asset classes. For context, the US stock market cap is about $47 trillion, while Apple ($AAPL) alone, with a market cap of $3 trillion, is roughly 3x larger than the entirety of crypto.

Should crypto’s mission to update our archaic financial system as well as financially connect the most economically ostracized parts of the world succeed, the potential upside is undeniable. For example, the recent progress we’ve seen in developing a Bitcoin spot ETF will drastically increase opportunities for the everyday person to gain crypto exposure without having to take on the operational risk of self-custody.

There is an astronomical disparity in the global sentiment towards digital assets. Namely, we’ve seen more liberated financial markets overseas, like the United Emirates or various countries in Latin America, embrace crypto with open arms while many Americans remain emotionally scarred by the narratives that have been weaponized against them to discourage participation.

According to a study done by the Pew Research Center, 75% of Americans are not confident in the safety and reliability of crypto. This stark contrast sets the stage for rapid price swings. It brings to light the potentially misaligned incentives that might’ve come into play amidst a weakening dollar and ever-changing geopolitical landscape.

Perhaps the most significant change that has occurred over the last market cycle is the influx of use cases that have finally come to fruition. The overwhelming success and adoption of non-fungible tokens (NFTs) in the world of art and ticketing and the likes of Gucci, El-Salvador and the world’s most prestigious brands and countries deeming cryptocurrency legitimate currency, Web3 is no longer possible; it’s happening.

Various breakthroughs in decentralized technologies have largely addressed the initial limitations of many decentralized protocols. The emergence of proof-of-stake and its many derivatives have enabled builders to put decentralized technologies in the hands of consumers and drastically expand their applications. And while most degens have been of the opinion that the world of distributed ledgers is ‘winner takes all,’ it now seems that the broader Web3 community is interested in finding ways to build bridges to bolster collaboration, an essential ingredient for mass adoption.

Conclusion

We are on the precipice of what could be the greatest transfer of wealth that has ever happened in human history. The essence of blockchain is to create an equitable world where no one would ever fall victim to the abuse of power.

Bitcoin’s creator, Satoshi Nakamoto, dreamed about a more financially free world where everyone can participate. And while he could not, in his wildest dreams, envision how it would all play out, he must be happy to see both the financial and lifestyle benefits of his technology becoming reality for so many people worldwide.