My name is Godspower Owie, and I was born and brought up in Edo State, Nigeria. I grew up with my three siblings who have always been my idols and mentors, helping me to grow and understand the way of life.

My parents are literally the backbone of my story. They’ve always supported me in good and bad times and never for once left my side whenever I feel lost in this world. Honestly, having such amazing parents makes you feel safe and secure, and I won’t trade them for anything else in this world.

I was exposed to the cryptocurrency world 3 years ago and got so interested in knowing so much about it. It all started when a friend of mine invested in a crypto asset, which he yielded massive gains from his investments.

When I confronted him about cryptocurrency he explained his journey so far in the field. It was impressive getting to know about his consistency and dedication in the space despite the risks involved, and these are the major reasons why I got so interested in cryptocurrency.

Trust me, I’ve had my share of experience with the ups and downs in the market but I never for once lost the passion to grow in the field. This is because I believe growth leads to excellence and that’s my goal in the field. And today, I am an employee of Bitcoinnist and NewsBTC news outlets.

My Bosses and co-workers are the best kinds of people I have ever worked with, in and outside the crypto landscape. I intend to give my all working alongside my amazing colleagues for the growth of these companies.

Sometimes I like to picture myself as an explorer, this is because I like visiting new places, I like learning new things (useful things to be precise), I like meeting new people – people who make an impact in my life no matter how little it is.

One of the things I love and enjoy doing the most is football. It will remain my favorite outdoor activity, probably because I’m so good at it. I am also very good at singing, dancing, acting, fashion and others.

I cherish my time, work, family, and loved ones. I mean, those are probably the most important things in anyone’s life. I don’t chase illusions, I chase dreams.

I know there is still a lot about myself that I need to figure out as I strive to become successful in life. I’m certain I will get there because I know I am not a quitter, and I will give my all till the very end to see myself at the top.

I aspire to be a boss someday, having people work under me just as I’ve worked under great people. This is one of my biggest dreams professionally, and one I do not take lightly. Everyone knows the road ahead is not as easy as it looks, but with God Almighty, my family, and shared passion friends, there is no stopping me.

Dan Loeb is known as a mover and a shaker in the investing world. He founded the New York-based hedge fund Third Point in 1995. It now has roughly $11.5 billion in assets under management. Loeb’s net worth stands at $3.3 billion, according to Forbes.

The activist investor did some moving and shaking in his hedge fund’s portfolio in the fourth quarter of 2023. Loeb reduced his stakes in Amazon(NASDAQ: AMZN) and Microsoft(NASDAQ: MSFT). However, the billionaire investor bought another “Magnificent Seven” stock.

Taking profits

Loeb sold 210,000 shares of Microsoft in Q4. While this reduced Third Point’s stake in the tech giant by over 9.4%, Microsoft remains the second-largest holding in the hedge fund’s portfolio.

The billionaire investor has owned Microsoft off and on since 2006. He most recently initiated a new position in the fourth quarter of 2022, just in time to ride the generative AI wave started by OpenAI’s launch of ChatGPT. Microsoft was a major beneficiary of this wave thanks to its partnership with OpenAI.

Third Point first owned Amazon in late 2019 and held the stock through the second quarter of 2022. Loeb didn’t stay on the sidelines long with the e-commerce and cloud services leader. He initiated a new position in Amazon in the second quarter of 2023. Although he reduced Third Point’s stake in the stock by nearly 10.3% in Q4 2023, Amazon still ranks as the hedge fund’s third-largest holding.

Why did Loeb trim his positions in Amazon and Microsoft? The most likely reason is he wanted to take some profits. Both stocks delivered impressive gains last year.

A bigger bet on Meta

Although Loeb cooled somewhat on two Magnificent Seven stocks, he placed a bigger bet on Meta Platforms(NASDAQ: META). The hedge fund manager increased Third Point’s stake in Meta by nearly 5.5% in Q4 2023. The $410.6 million value of the position made Meta the sixth-largest holding for Third Point at the end of 2023.

Loeb’s history with Meta goes back to the second quarter of 2016 when he first bought the stock. He owned shares of the social media company for a little over two years before exiting the position. The activist investor again bought Meta stock in the second quarter of 2020 and maintained a position through 2021 Q4. Loeb went back to the well in the third quarter of 2023 with another new stake in Meta.

Like Amazon and Microsoft, Meta enjoyed a generative AI tailwind last year. However, I suspect that wasn’t Loeb’s primary reason for adding to his position in the stock. Instead, my hunch is that Loeb liked Meta’s moves to increase its profitability.

Those efforts are paying off. Meta’s earnings more than tripled year over year in 2023 Q4. Full-year profits jumped 69%.

Did Loeb make the right moves?

In one sense, Loeb went one for three with these Magnificent Seven transactions. Loeb’s decision to increase Third Point’s stake in Meta is already paying off. Meta stock has skyrocketed over 45% since the end of 2023. However, Amazon and Microsoft are also up by double-digit percentages year to date. Loeb could have made more money by holding his shares in both companies.

However, trimming the positions in Amazon and Microsoft could still have been the right call for Loeb. Both stocks make up significant percentages of Third Point’s portfolio. You can’t blame any investor for wanting to ensure their holdings aren’t overly concentrated in a handful of stocks.

Over the long term, I think that Loeb — and other investors — will be well served by owning all three of these stocks. Amazon’s and Microsoft’s cloud businesses should continue to grow robustly thanks largely to AI. I like Meta’s focus on business messaging and smart glasses with embedded AI assistants. I predict Amazon, Microsoft, and Meta will remain magnificent for a long time to come.

Should you invest $1,000 in Meta Platforms right now?

Before you buy stock in Meta Platforms, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Meta Platforms wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Keith Speights has positions in Amazon, Meta Platforms, and Microsoft. The Motley Fool has positions in and recommends Amazon, Meta Platforms, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Many people know Michael Burry from the book The Big Short, or the movie that was based on it. Both chronicled the story of a ragtag group of investors who bet against the U.S. housing market before the 2008-2009 financial crisis, shorting mortgage-backed securities at a time when everyone else thought housing was set to go up forever. Burry is still investing today, and runs Scion Asset Management.

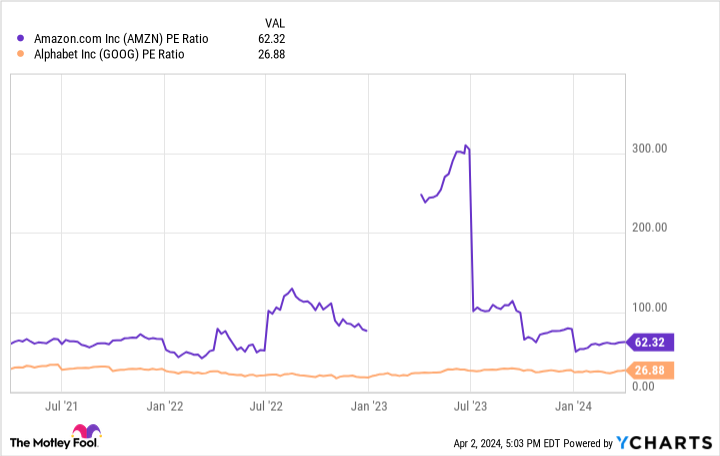

In 2023’s fourth quarter, Scion Asset Management reported two purchases that may surprise his value-investing followers: Amazon(NASDAQ: AMZN) and Alphabet(NASDAQ: GOOG). These “Magnificent Seven” growth stocks have typically been shunned by value investors due to their high earnings multiples. Yet as of the end of 2023, they made up 10% of Burry’s stock portfolio.

So why did Burry open positions in Amazon and Alphabet?

Amazon: Profits are finally arriving

At first glance, Amazon seems overvalued. Its price-to-earnings ratio (P/E) of 62 is more than twice the average of the S&P 500 index (28, as of this writing). However, when you look under the hood, it is clear that Amazon did not show its true profit potential in 2023. Throughout last year, the e-commerce and cloud computing giant expanded its operating margin, leading to approximately 7.5% margins for the last two quarters. That was up significantly from the 2.5% margins it posted in late 2022 and early 2023.

Had Amazon been earning a 7.5% profit margin for the entire year on its total revenue of $575 billion, it would have generated $43 billion in profits in 2023. Against its current market cap of $1.9 trillion, that would have given it a P/E of 44. But even this doesn’t tell the full story. Amazon’s profit margins should continue to move higher in 2024, for multiple reasons. First, its high-margin cloud computing division, Amazon Web Services (AWS), continues to shine. Second, it is seeing strong growth from higher-margin e-commerce services such as third-party selling management and advertising. Advertising revenues, for reference, grew by 26% year over year last quarter.

If Amazon’s profit margin reaches 10% in 2024 and its revenue grows by 10% to $630 billion, it will generate $63 billion in earnings this year. That would give it a P/E of 30, or right around the S&P 500’s average. Burry likely anticipates that profit inflection happening as well, which would explain why he is buying shares for Scion Asset Management’s portfolio.

Alphabet: From AI loser to AI winner

Burry’s other Magnificent Seven bet, Alphabet, is not optically expensive, but it faced some major negative narratives throughout 2023. At the beginning of 2023, the tech giant traded at a P/E ratio below 15, likely due to investor fears that it was losing the race in AI to upstarts such as OpenAI. Today, it trades at a P/E of 27, which is still slightly below the S&P 500 average, even though the stock is up 77% year to date.

Burry and other investors likely expect Alphabet to maintain its overwhelming share of the search market, which gives it a lucrative digital advertising business. Google Search’s market share has remained remarkably steady despite all these new AI competitors, at over 90% according to the latest estimates. In the fourth quarter of 2023, Google Search revenue grew 12.7% year over year to $48 billion.

Alphabet also has promising businesses in YouTube and Google Cloud. YouTube is the dominant player in video streaming worldwide, generating $9.2 billion in advertising revenue last quarter and hitting 100 million premium subscribers. Google Cloud does right around the same in quarterly revenue and is growing sales by 25% year over year.

If Alphabet maintains its lead in Google Search and keeps growing YouTube and Google Cloud, the stock will likely do well over the long term.

Learn from investing greats, but don’t copy them

Looking through the portfolio holdings of famous investors can be insightful. But nobody should be out there blindly buying up every company in Burry’s portfolio.

First off, we outsiders can’t know what Burry’s actual theses are on these two stocks. His reasons for holding them may differ from your own, and that could create some discomfort for you if the stocks start falling. Second, the investing public only finds out about hedge funds’ moves through their 13-F filings with the Securities and Exchange Commission. These filings are due a month and a half after the end of the quarter they cover, and the most recent ones describe where their portfolios stood at the end of 2023. As such, we can have no idea if Burry has bought or sold Amazon and Alphabet shares in 2024, or if he even has any exposure to the stocks right now. This informational time lag makes trying to copy the moves of famous investors a dangerous idea.

Learn from the investing greats, but don’t copy them. It’s better to build your portfolio with stocks you believe in, not stocks you believe that others believe in.

Should you invest $1,000 in Amazon right now?

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Brett Schafer has positions in Alphabet and Amazon. The Motley Fool has positions in and recommends Alphabet and Amazon. The Motley Fool has a disclosure policy.

When you think about magnificent stocks, I’m sure the “Magnificent Seven” tech-focused and innovative enterprises come to mind. Their returns in the past decade have certainly been spectacular.

But there are two lesser-known and definitely more boring companies that have also trounced the market. I’m talking about O’Reilly Automotive(NASDAQ: ORLY) and AutoZone(NYSE: AZO). The former is up 678% in the past 10 years, while the latter has risen 498% during that time.

Should you buy these two skyrocketing retail stocks with $100 and hold through 2024 and beyond?

Steady wins the race

These businesses won’t win any awards when it comes to excitement and disruptive potential. They are quite the opposite. However, being boring has clearly worked out well for investors.

Through their networks of thousands of stores, both O’Reilly and AutoZone sell aftermarket car parts and supplies to both DIY and commercial customers. That detail about aftermarket parts is critical, as these companies thrive when selling to consumers that own cars running past the original manufacturer’s warranty. With the average age of vehicles on the road slowly rising with each passing year, coupled with more miles driven, there is plenty of demand out there.

Basically, these businesses perform well when there’s more wear and tear on cars. It’s of the utmost importance for people to have working vehicles to manage their day-to-day life, whether it’s to run errands, drop off and pick up kids from school, or get to work. This makes both O’Reilly and AutoZone somewhat recession-proof.

That’s a fantastic quality to have in stocks that you own because you don’t need to be able to predict what the economy is going to do next. The companies in question will do well no matter what.

Capital returns

Given that they experience stable demand trends regardless of the economic environment, these companies are able to generate copious amounts of profits and cash. O’Reilly and AutoZone raked in $2 billion and $2.1 billion of free cash flow, respectively, in their last fiscal years. This is the true mark of a financially sound enterprise.

Neither business pays dividends. But both management teams are very aggressive when it comes to share buybacks. Just in the past five years, a time period that included various disruptions like the pandemic, supply chain bottlenecks, inflationary pressures, and higher interest rates, O’Reilly’s share count was reduced by 26%, while AutoZone’s shrunk by 30%.

For existing investors, this is a financial boon because it boosts earnings per share. Shareholders’ ownership stakes increase over time if they do nothing. That’s a powerful development.

What’s encouraging is that this attractive capital-return policy comes after executives reinvest in growth initiatives. After opening new stores or distribution facilities each year, share buybacks are done. That should lead to even greater revenue and earnings over time.

Is the price right?

With the overall market in record territory, it’s probably not surprising that both O’Reilly and AutoZone are also near all-time highs. Just like their underlying businesses, these stocks continue to deliver for investors.

This means that they aren’t necessarily trading at bargain prices. On a price-to-earnings (P/E) basis, both stocks are selling at some of their highest levels in the past decade. Consequently, it looks like these boring businesses have caught the eye of the market, with investors being incredibly optimistic about their prospects.

It’s important to ask yourself how much emphasis you place on valuation. Of course, it would be a much better situation if O’Reilly and AutoZone were trading at cheaper P/E multiples. But what gains would you be giving up if you waited on the sidelines? I believe the best move might simply be to spend $50 on each of these stocks and hold for the long term.

Should you invest $1,000 in AutoZone right now?

Before you buy stock in AutoZone, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and AutoZone wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

Neil Patel and his clients have no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Disney (DIS) CEO Bob Iger said Tuesday that he is trying his best to not let an ongoing proxy battle with activist investor Nelson Peltz divert his focus on turning around the business.

“I am working really hard to not let this distract me because when I get distracted, everybody who works for me is distracted and that’s not a good thing,” Iger said at Morgan Stanley’s media and telecom conference on Tuesday.

Last year, Peltz and his hedge fund Trian Fund Management renewed a push to shake up the company’s board as the stock price hit multiyear lows. Disney has been grappling with challenges that include a declining linear TV business, slower growth in its parks business, and losses in streaming.

Iger pointed to the complexities of running Disney’s multifaceted business as various segments like streaming face increased disruption.

“It’s [a business] that takes not only a significant amount of knowledge, but a tremendous amount of time and focus,” he said. “This campaign is in a way designed to distract us. … Time and focus is necessary to generate what we need to generate for the shareholders.”

Iger’s comments come after Trian published a 130-page white paper on Monday blaming the board for Disney’s underperformance and accusing its members of lacking “focus, alignment and accountability.”

Peltz is currently seeking board seats for himself, along with former Disney CFO Jay Rasulo. If the proxy battle continues to a vote, a shareholder meeting set to take place on April 3 will ultimately determine the board’s fate.

Another investment firm, Blackwells Capital, supports the company’s current board but has urged shareholders to vote for its three nominees as additions to it.

Disney’s stock has fought its way back from record lows with shares up about 11% year over year.

Since the start of 2024, shares have climbed about 25%, outpacing the S&P 500’s 6% rise over that same time period.

History is proof the U.S. stock market always climbs to new highs given enough time. But the stocks that lead the charge higher aren’t always the same. To help find the new leaders, Wall Street often groups them together to separate them from the rest of the market. For example, CNBC financial analyst Jim Cramer coined the FAANG acronym in 2017 to describe five of the largest technology companies at the time:

Facebook, which now trades as Meta Platforms

Apple

Amazon

Netflix

Google, which now trades as Alphabet

That leadership shifted in 2023 when a group of seven stocks drove the S&P 500 index to an annual return of twice its historical average. Bank of America analyst Michael Hartnett dubbed those stocks the “Magnificent Seven,” and they include:

Meta Platforms

Apple

Amazon

Alphabet

Microsoft

Nvidia (NASDAQ: NVDA)

Tesla

Image source: Getty Images.

It’s time for the “AI Five,” according to one analyst

With Tesla stock sinking 22% so far this year, Jim Cramer thinks it should be booted from the Magnificent Seven entirely. The company is facing sluggish electric vehicle sales in 2024, which could keep a lid on its stock price and weaken the power of the Magnificent Seven as a group.

It prompted one analyst — Glen Kacher from Light Street Capital — to rethink the stock market’s leadership altogether. He thinks investors should be focused on artificial intelligence (AI), so he has identified a new group of stocks and called it the “AI Five.” It includes:

Nvidia

Microsoft

Taiwan Semiconductor Manufacturing

Advanced Micro Devices(NASDAQ: AMD)

Broadcom (NASDAQ: AVGO)

Each company has a hand in developing the hardware and software necessary to bring AI to life. Here are two AI Five stocks investors should consider buying right now.

1. Advanced Micro Devices (AMD)

Advanced Micro Devices might be one of the best semiconductor stocks to own in 2024. Its new MI300 data center chips are designed to process AI workloads, and they are shaping up to be the main rivals to Nvidia’s industry-leading H100.

The MI300 comes in two configurations. The MI300X is a pure graphics processor (GPU) like the H100, whereas the MI300A combines GPU and central processing unit (CPU) hardware to create the world’s first accelerated processing unit (APU) for data centers. The MI300A will power the El Capitan supercomputer at the Lawrence Livermore National Laboratory, and it’s expected to be the most powerful in the world when it comes online later this year.

Some of the world’s largest data center operators, companies like Meta Platforms, Microsoft, and Oracle, are also racing to get their hands on MI300 chips. They have relied almost entirely on Nvidia up until now, but supply constraints are pushing them to look for viable alternatives, and AMD is ready.

In the fourth quarter of 2023, AMD issued a bullish forecast for the MI300. The company originally expected the GPU to pull in $2 billion worth of sales in 2024, but it raised that number to $3.5 billion, much to the delight of investors.

AI is also coming to personal computers, where users can process AI on-device for a faster experience, which reduces the reliance on external data centers. AMD’s Ryzen AI series of neural processing units (NPUs) already power more than 50 notebook designs, and the company is working with Microsoft to develop a new version of Windows that will run AI workloads more efficiently.

Millions of personal computers have already shipped with Ryzen AI chips, giving AMD a 90% market share in the segment. Ryzen AI drove the company’s Client segment revenue to $1.5 billion in the fourth quarter, representing a whopping 62% year-over-year increase. AMD expects that momentum to continue, especially because it’s preparing to launch a next-generation chip that could be more than three times faster.

Simply put, 2024 is set to be incredibly exciting for AMD, and the company could be on the cusp of a multiyear growth cycle on the back of its new hardware slate.

2. Broadcom

As far as being an AI stock, Broadcom lives in the shadow of glamorous names like AMD and Nvidia. However, Broadcom is developing AI on multiple fronts, and its stock has delivered a 343% return over the last five years, so it definitely warrants some attention. Despite being founded in 1991, the company really took a leap forward when it merged with semiconductor giant Avago Technologies in 2016.

Broadcom is now a conglomerate that not only includes Avago but also several acquired companies like semiconductor device supplier CA Technologies, cybersecurity giant Symantec, and cloud software developer VMware. Broadcom spent a whopping $98.6 billion on those three acquisitions since 2018.

VMware, which had a price tag of $69 billion alone, is an increasingly important company in the context of the AI boom. Its software allows users to run virtual machines to distribute cloud infrastructure more efficiently. For example, one user on one server might only utilize 10% of its capacity, but virtual machines allow multiple users to plug into that server so it operates at capacity. Considering so many companies are racing to access AI data center infrastructure, optimization is one way they can squeeze the most value out of what they have.

Broadcom itself is also considered a leader in networking and server connectivity solutions for the data center. It developed a high-bandwidth switch called Tomahawk 5, which is designed to accelerate AI and machine learning workloads. A switch regulates how fast data travels from one point to another, and considering developers are feeding billions of data points to powerful GPUs to train AI models, it has become an important piece of the infrastructure puzzle.

Broadcom generated a record-high $35.8 billion in revenue during fiscal 2023 (ended Oct. 29), which was an increase of 8% compared to fiscal 2022. However, Broadcom’s revenue is expected to grow by 40% in fiscal 2024 to $50 billion, thanks to the inclusion of VMware’s financial results for the first time.

Based on Broadcom’s $42.25 in non-GAAP (adjusted) earnings per share in fiscal 2023 and its current stock price of $1,226.55, it trades at a price-to-earnings (P/E) ratio of 29.1. That’s a 9% discount to the 32.1 P/E of the Nasdaq-100 index, which implies Broadcom is still cheap relative to its peers in the tech sector.

Given the company’s growing presence in AI through acquisitions and in-house development, Broadcom looks like a great AI Five stock to buy now and hold — especially at this price.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for two decades, Motley Fool Stock Advisor, has more than tripled the market.*

They just revealed what they believe are the 10 best stocks for investors to buy right now… and Advanced Micro Devices made the list — but there are 9 other stocks you may be overlooking.

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Bank of America is an advertising partner of The Ascent, a Motley Fool company. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Apple, Bank of America, Meta Platforms, Microsoft, Netflix, Nvidia, Oracle, Taiwan Semiconductor Manufacturing, and Tesla. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The S&P 500 (^GSPC) is creeping near 5,000 for the first time ever. And once again, the stocks leading it higher are the biggest members of the benchmark average.

Amazon (AMZN), Meta (META), Microsoft (MSFT), and Nvidia (NVDA) have produced a nearly 20% return to start the year, per analysis from Yahoo Finance’s Jared Blikre. The returns from these four stocks alone account for roughly 69% of the S&P 500’s gain this year.

But not all of the so-called “Magnificent Seven” tech stocks are off to a strong start. Apple (AAPL), Alphabet (GOOGL, GOOG), and Tesla (TSLA) are having a choppier start to the year. For some on Wall Street, this has become a concern as a shrinking number of stocks are leading the major average higher.

Fortunately for investors, even if top stocks are peaking, the marketshould probably still go up.

A recent analysis from BMO Capital Markets chief investment strategist Brian Belski showed that even when the top stocks driving an outsized part of the market action fall off, returns over the next year for the index historicallyhave been quite good.

A chart from Belski shows that since 1992,on average, the S&P 500 has risen 14.3% in the year following a peak in contribution from the top 10 stocks in the benchmark average. The only time the S&P 500 delivered a negative return in the next year was in 2001 amid the fallout from the tech bubble.

“While some investors may be concerned that the market is likely to struggle without these stocks leading the way, our analysis shows that the S&P 500 has performed just fine following peaks in relative performance of the 10 largest stocks,” Belski wrote in a note to clients on Tuesday.

Goldman Sachs equity strategist Ben Snider pointed out that while the degree to which topstocks are dragging the major index higher is currently abnormally high, the idea that a few winners lead the S&P 500 gains isn’t a new concept. In fact, Snider argued, in the long run it’s been a typical feature, not a bug, of the benchmark index.

“That’s part of why the S&P 500 or the US equity market broadly has been so strong over the years. … New companies grow, and they become larger weights in the index, and they drag the market higher with them,” the analyst told Yahoo Finance. “And eventually, there will be disruptors and new technologies that emerge and new businesses that emerge. And those will become larger. And then, it will be their turn to drag the market higher.”

For the S&P to hit new records without significant contributions from the Magnificent Seven, there would need to be a broadening out in the market, where other lagging sectors begin to pick up steam. This has been seen recently in areas such as large-cap Healthcare (XLV), which is up 17% from its October lows, and the Financial Select Sector ETF (XLF), which is up 24% from October lows.

With 70% of S&P 500 companies topping analysts’ earnings per share forecasts in the fourth quarter, above the historical average of 63%, Bank of America US and Canada equity strategist Ohsung Kwon pointed to the increased breadth in earnings growth as a positive catalyst moving forward.

“You’re seeing [an] even higher percentage [of] companies posting positive earnings this quarter than last quarter,” Kwon told Yahoo Finance on Tuesday. “So actually, earnings breadth is improving as well, and that’s a positive cycle for equities.”

Snider thinks this broadening out is the most likely scenario this year once investors feel more confident in the Federal Reserve’s interest rate-cutting path.

“As investors stop worrying so much about exactly when the Fed will start to cut rates, I think we’ll see a lot of these companies outside of the Magnificent Seven have pretty strong earnings growth, and that will cause them to do pretty well in turn,” Snider said.

A sign is posted at Nvidia headquarters on February 05, 2024, in Santa Clara, California. (Justin Sullivan/Getty Images) (Justin Sullivan via Getty Images)

Josh Schafer is a reporter for Yahoo Finance. Follow him on X @_joshschafer.

The “Magnificent Seven” stocks dominated the market in 2023. The worst performer in the group, Apple (NASDAQ: AAPL), rose 49%, and the best, Nvidia (NASDAQ: NVDA), jumped nearly 240%. But with such strong runs behind them, do any of them have room left to grow in 2024?

The answer: Yes, and some are still worth buying at their current prices.

Apple and Nvidia are both richly valued for their performance

I’m breaking the seven up into buy, sell, and hold groups. Starting with the sell set, I think Apple and Nvidia’s stock prices far outpaced their businesses.

Nvidia’s 2023 success has been spurred on by the artificial intelligence (AI) arms race, and its business has responded in kind. In its fiscal 2024 third quarter (which ended Oct. 29), revenue rose 206% year over year. Furthermore, management guided for $20 billion in fiscal Q4 revenue, up 231%. The stock’s movement was warranted given the company’s sales growth, but I’m concerned that investors are forgetting that Nvidia operates in a cyclical industry.

Nvidia goes through boom and bust cycles, and right now is certainly a boom. However, it’s unknown how many AI data centers will need to be built in the near to medium term. If demand for its high-powered chips is satisfied shortly, the stock may come crashing back down to earth. Plus, it’s trading at 65 times earnings — a quite expensive premium.

From a business standpoint, Apple is the opposite of Nvidia. Its sales declined throughout 2023. Even so, its stock skyrocketed. This makes little sense, and more headwinds are coming up: a U.S. International Trade Commission order this month forced Apple to halt the import and sale of some Apple Watches due to a patent dispute (although a court ruling temporarily allowed sales to resume). With all this in mind, 2024 could be a tough year for the company. And considering that Apple stock has a higher valuation than “Magnificent Seven” members Alphabet (NASDAQ: GOOG)(NASDAQ: GOOGL) and Meta Platforms(NASDAQ: META), it doesn’t make a lot of sense to own it compared to its peers.

Microsoft and Tesla need to show me some results

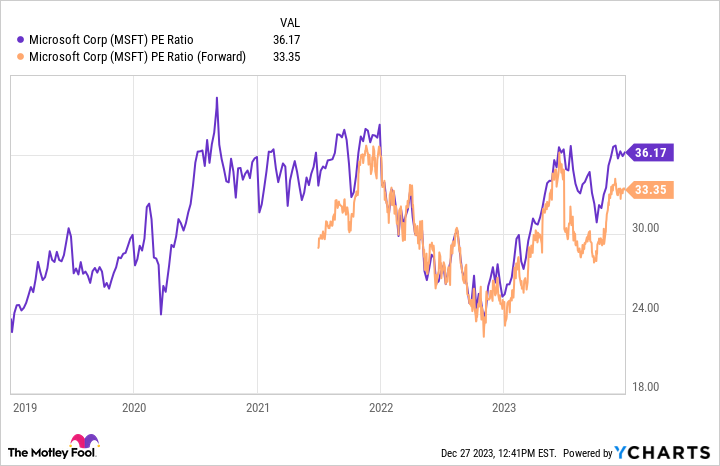

I view Microsoft(NASDAQ: MSFT) and Tesla(NASDAQ: TSLA) as holds currently. Microsoft had a strong year, as its revenues and earnings per share (EPS) steadily rose. However, Microsoft trades at a steep premium, even on a forward earnings basis.

Microsoft is executing well, but its valuation is a bit too much from a historical perspective to consider buying. Still, it’s far from a sell.

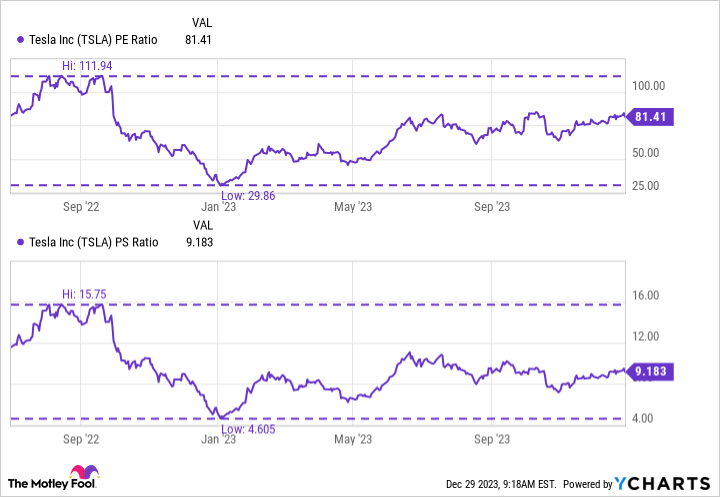

Tesla is one of the hardest companies to value on Wall Street, as its valuation is wrapped up in expectations for future products. It’s also set to face some added headwinds. Starting in 2024, some Tesla models will only qualify for half of the $7,500 federal EV tax credit due to where the automaker sources materials for their batteries and where it produces them.

When judging whether any given moment is a better time to buy or sell Tesla stock, I like to look at its price-to-earnings and price-to-sales ratio compared to historical trends. For Tesla, these are trading roughly near the midpoint of valuations seen since mid-2022.

TSLA PE Ratio Chart

I’m taking a wait-and-see approach to Tesla stock heading into the new year as the stock doesn’t look like a bargain at these prices.

Advertising should bounce back in 2024

That leaves Alphabet, Meta Platforms, and Amazon(NASDAQ: AMZN) in the buy now category. These stocks trade at reasonable levels and are expecting strong tailwinds next year.

Even though Alphabet and Meta have AI investments, they are mostly advertising businesses. In 2022 and 2023, the advertising market was fairly weak as companies pulled back on their marketing spending due to fears that a recession was coming. However, now that we have lapped that pullback, Alphabet and Meta are posting meaningful growth in their advertising businesses. Their ad revenues grew by 9% and 24%, respectively, in Q3.

Next year should be another strong recovery year for advertising, which will boost both companies.

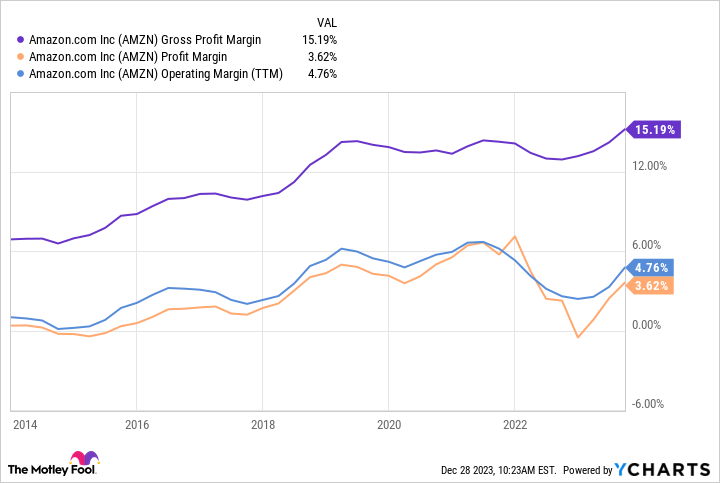

Amazon has also had a strong 2023, with its margins rising.

AMZN Gross Profit Margin Chart

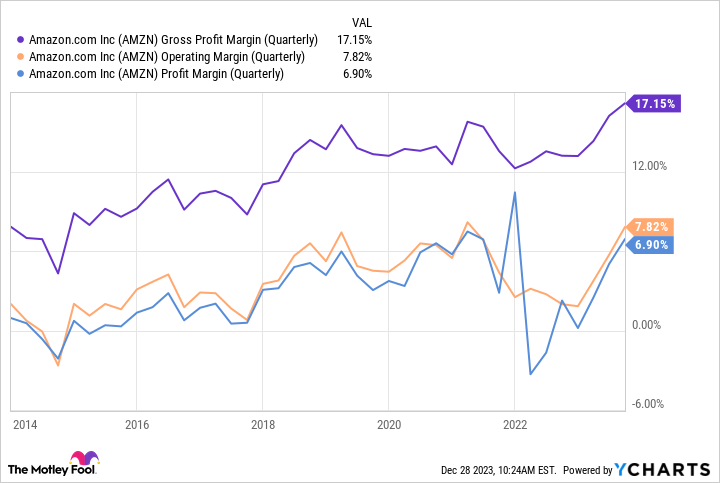

However, this chart doesn’t tell the full story, as this takes into account Amazon’s profits over the past 12 months. If you focus on its latest quarterly results, Amazon’s margins are nearing (or have already set) all-time highs.

AMZN Gross Profit Margin (Quarterly) Chart

The fact that Amazon posted solid results in historically weak quarters bodes well for Q4, which is usually its strongest one. No investor knows what a fully profitable Amazon looks like, but 2024 could give us a glimpse, making it a strong buy now.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in Alphabet, Amazon, and Tesla. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has a disclosure policy.

Jim Rogers expects a multi-asset bubble to burst and the American economy to run into trouble.

George Soros’ cofounder hopes to profit by shorting the “Magnificent Seven” stocks at the right time.

Rogers touted gold and silver, warned the inflation threat isn’t over, and slammed the Fed.

Jim Rogers expects asset prices to plunge and economic disaster to strike — and he plans to profit by betting against stock-market darlings like Tesla and Nvidia when the time is right.

“Bonds are a bubble, property in many countries is a bubble, stocks are getting ready for a bubble,” the veteran investor and travel author told Soar Financially in a recent interview.

Rogers has dumped many of his stocks and bonds in anticipation of a painful slump, but he’s “not shorting yet because often at the end there’s a blowoff and things get really crazy,” he said.

He flagged “warning signs” of an approaching collapse, including a handful of stocks dragging the major indices higher this year, and newbie investors boasting to all of their friends about how easy it is to make money trading stocks.

The markets guru, best known for cofounding the Quantum Fund and Soros Fund Management with George Soros, said he’s itching to bet against the “Magnificent Seven” stocks — Apple, Alphabet, Amazon, Microsoft, Meta, Tesla, and Nvidia.

“When the market comes to an end, the last high flyers are the best shorts,” he said. “The stocks that have done extremely well and are very expensive — that, I hope, is where I’m smart enough to short next time around.”

Rogers, 81, also predicted the US economy would run into trouble soon as a result of its ballooning debt pile.

“I would suspect that next year things are not going to look as happy,” he said. Rogers noted he wasn’t sure if a recession or mild downturn lies ahead, but he’s “worried” that there hasn’t been a prolonged economic slump since the 2008 financial crisis, and global debt loads have ballooned since then.

“The next problem has to be the worst in my lifetime because the debt is just unbelievable,” he said.

Rogers advised people to own precious metals, which tend to retain their value better than other assets during periods of panic.

“Everybody should have some silver and gold under the bed,” he said. “Look, all of us peasants know, when there’s a serious catastrophe, you better have some gold and silver in the closet, so I do.”

The “Adventure Capitalist” author also predicted inflation, which has cooled significantly in the past year, would reaccelerate to painful levels. Moreover, he accused the Federal Reserve of having no idea what it’s doing, and dismissed all but a couple of the central bank’s leaders over the last century as clueless “bureaucrats and academics.”

Rogers has a wealth of experience and a deep understanding of financial history, but it’s worth pointing out that he’s been predicting the worst downturn of his lifetime for several years now, yet both markets and the economy have defied his grave warnings.

The “Magnificent Seven” stocks — Apple (AAPL), Alphabet (GOOGL, GOOG), Microsoft (MSFT), Amazon (AMZN), Meta (META), Nvidia (NVDA), and Tesla (TSLA) — are the big drivers of this year’s market rally. With five weeks left in 2023, the S&P 500 (^GSPC) is up 19%.

Investors scooped up shares of megacap tech names throughout the year amid macro uncertainty, driven in part by the Fed’s aggressive interest rate hiking campaign.

Looking ahead to 2024, strategists are split on future returns. Morgan Stanley’s Mike Wilson, a staunch bear, sees stocks essentially flat while Goldman Sachs’ David Kostin sees limited upside, predicting the benchmark index will reach 4,700 by the end of 2024.

On the other hand, Bank of America and RBC strategists are more bullish. Bank of America’s Savita Subramanian and her team forecast the S&P 500 to reach a record of 5,000 as investors move beyond “maximum macro uncertainty.” RBC’s Lori Calvasina also sees the S&P 500 reaching 5,000, writing in a note to clients: “Our valuation and sentiment work are sending constructive signals.”

So what does all this mean for investors’ playbooks in 2024? Yahoo Finance Live put that question to some Yahoo Finance Live regulars — here’s a roundup of some big ideas and themes to consider for 2024.

Do you stick with the Magnificent 7 in 2024?

The “Magnificent Seven” mega-cap stocks played an outsized role in this year’s rally. The group has a combined weighting of 28% in the S&P 500, so their outperformance, largely driven by excitement surrounding artificial intelligence, dominated the performance of the broader index.

But whether or tech still has room to run is a hotly debated subject on Wall Street.

DoubleLine CEO Jeffrey Gundlach is in the bear camp, warning investors that the group will be among the “worst performers in the upcoming recession.”

“Whatever is leading the charge going into the economic downturn invariably must lead the charge on the way down. I would get out of them,” Gundlach said at Yahoo Finance’s Invest conference earlier this month.

His advice for investors: “Go into an equal-weighted basket as opposed to a market-weighted basket … and gradually diversify. … In particular, I would start thinking about emerging markets once the dollar index starts to fall, which has not happened yet. But it’s going to happen in the next recession.”

But others, including Goldman Sachs chief US equity strategist David Kostin, see the megacap group outperforming once again.

“The 7 stocks have faster expected sales growth, higher margins, a greater re-investment ratio, and stronger balance sheets than the other 493 stocks and trade at a relative valuation in line with recent averages after accounting for expected growth,” Kostin wrote in the firm’s 2024 outlook.

Emerging markets could be a stronger investing theme in 2024, some strategists say. (AP Photo/Eugene Hoshiko, File) (ASSOCIATED PRESS)

2024 ‘should be better’ for emerging markets

China’s stock market has struggled this year amid a lackluster economic recovery. The MSCI China Index has fallen more than 9% since Jan. 1.

But that could change in 2024, according to Charles Schwab strategist Jeffrey Kleintop.

Kleintop cited corporate investment in China, productive talks between President Biden and Chinese leader Xi Jinping, and economic stimulus as reasons to be more optimistic on the region.

“Broader support across the markets in Asia is really interesting right now. … That’s where I’m finding more opportunities and lower valuations,” Kleintop told Yahoo Finance Live. “Companies that are braced for a more different economic environment and one that I think we’re likely to see in 2024.”

While Kleintop’s outlook for China is brighter, he does caution investors to prepare for a “bumpy ride” given China’s historical volatility and unique challenges.

For specific plays, UBS strategist Andrew Garthwaite sees beaten-down Chinese internet stocks set for a turnaround. Garthwaite wrote in the bank’s 2024 outlook that the group’s “performance has lagged EPS momentum.”

Smalls caps and other ‘cheap interest rate sensitive plays’

Hard-hit areas of the market are a buying opportunity for investors as the Federal Reserve halts its rate-hiking campaign, according to eToro strategist Ben Laidler.

“The further we get into next year and the closer we get to the Fed cutting, look at those cheaper interest rate sensitive plays like real estate, banks, and small caps,” Laidler told Yahoo Finance.

October’s cooler inflation data prompted traders to move up expectations for Fed rate cuts to May, sending small caps surging earlier this month. The Russell 2000 (^RUT) rose over 5% last week.

Laidler’s comments on small caps were echoed by RBC capital markets head of US equity strategy Lori Calvasina. Calvasina told Yahoo Finance earlier this month that easing cycles typically help small caps. She and her team at RBC view the group as well positioned for the longer term.

“They tend to lag late in economic cycles and so there’s really a sense when times get dicey that’s when you want to go bargain hunting in the small-cap space,” Calvasina added.

Consumer discretionary stocks a ‘top idea’ for 2024

The S&P 500 is set to reach a new record by June of next year and consumer discretionary is a top way to play the index’s gains, JPMorgan Private Bank US equity strategist Abby Yoder told Yahoo Finance Live.

“You have all of these bears coming out saying the consumer is slowing, which we do agree with, but it’s slowing from very, very high levels,” Yoder said. “The sector has already been through an earnings recession period. … We expect a reacceleration on the top line along with margin support.”

It’s a contrarian call given the long list of retailers warning about a weakening consumer this holiday season. Best Buy, Macy’s, Walmart, and Target were among those flagging a shift in spending trends amid persistent inflation.

‘Be ready to shift’ your investment strategy

Starting the year with an investment plan always makes sense, but given uncertainty about interest rates, along with heightened geopolitical risk and the upcoming 2024 election, Truist chief market strategist Keith Lerner is wary about what’s ahead.

“Be ready to shift,” Lerner told Yahoo Finance. “We have all these remaining crosscurrents still in place — lagged impact of Fed policy, the election year, geopolitics, and ultimately which way the economy breaks. … This will likely force investors to be more tactical.”

If 2023 is a guide, it’s nearly impossible to predict the future. Unforeseen events prompted forecasters to adjust their outlooks and strategies on numerous occasions throughout the year. Remember, many CEOs, economists and strategists were convinced a recession was on the horizon, and nearly a year later, we still have yet to see it.

Seana Smith is an anchor at Yahoo Finance. Follow Smith on Twitter @SeanaNSmith. Tips on deals, mergers, activist situations, or anything else? Email seanasmith@yahooinc.com.