BOSTON — Massachusetts cities and towns are facing a “historic fiscal crisis” amid rising operating costs, lackluster state aid and restraints on property tax increases, according to a new report.

The “Perfect Storm” report, released by the Massachusetts Municipal Association, found that while state government spending has increased by an average of 2.8% per year since 2010 to meet its needs, restraints on local revenue sources – including Proposition 2 1⁄2 – have held city and town spending to just 0.6% per year.

This page requires Javascript.

Javascript is required for you to be able to read premium content. Please enable it in your browser settings.

BOSTON — The state’s economy may be on solid footing but employers are becoming increasingly pessimistic about the impact of President Donald Trump’s tariffs on their bottom lines, according to a new report.

The latest Business Confidence Index, which is compiled by the pro-business group Associated Industries of Massachusetts, shows overall enthusiasm among employers “grew darker” after slipping 1.4 points to 47.5 on a 100-point scale in September.

This page requires Javascript.

Javascript is required for you to be able to read premium content. Please enable it in your browser settings.

The below is an excerpt from a recent year-ahead report written by the Bitcoin Magazine PRO analysts. Download the entire report here.

Bitcoin Magazine PRO sees incredibly strong fundamentals in the Bitcoin network and we are laser-focused on its market dynamic in the context of macroeconomic trends. Bitcoin aims to become the world reserve currency, an investment opportunity that cannot be understated.

In our year-ahead report, we analyzed seven notable factors that we recommend investors pay attention to in the coming months.

Convicted Bitcoin Investors

We can put investor conviction into perspective by looking at the number of unique Bitcoin addresses holding at least 0.01, 0.1 and 1 bitcoin. This data shows that bitcoin adoption continues to grow with a growing number of unique addresses holding at least these amounts of bitcoin. While it is entirely possible for individual users to hold their bitcoin in multiple addresses, the growth of unique Bitcoin addresses holding at least 0.01, 0.1 and 1 bitcoin indicate that more users than ever before are buying bitcoin and holding it in self-custody.

Unique bitcoin addresses continues to grow across the board.

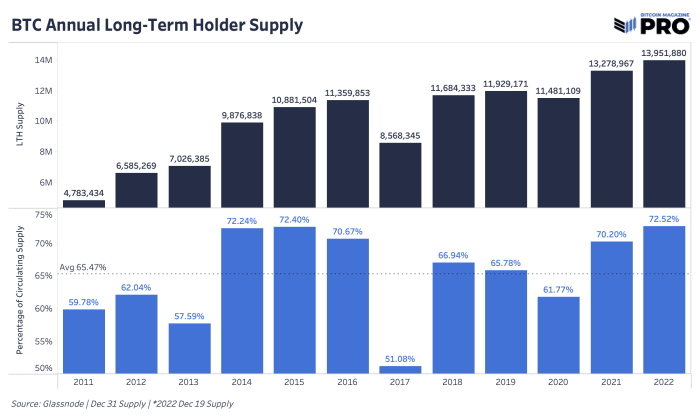

Another promising metric is the amount held by long-term holders, which has increased to almost 14 million bitcoin. Long-term holder supply is calculated using a threshold of a 155-day holding period, after which dormant coins become increasingly unlikely to be spent. As of now, 72.49% of the bitcoin in circulation is not likely to be sold at these prices.

Long-term holder supply reached 72.52% of the circulating bitcoin supply.

There is a large subset of bitcoin investors who are accumulating the digital asset no matter the price. In a December 2022 interview on “Going Digital,” Head of Market Research Dylan LeClair said, “You have people all over the world that are acquiring this asset and you have a huge and growing cohort of people that are price-agnostic accumulators.”

With a growing number of unique addresses holding bitcoin and such a significant amount of bitcoin being held by long-term investors, we are optimistic for bitcoin’s advancement and rate of adoption. There are many variables that demonstrate the potential for asymmetric returns as demand for bitcoin increases and adoption increases worldwide.

Total Addressable Market

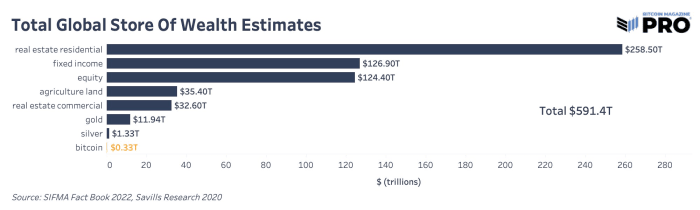

During monetization, a currency goes through three phases in order: store of value, medium of exchange and unit of account. Bitcoin is currently in its store-of-value phase as demonstrated by the long-term holder metrics above. Other assets that are frequently used as stores of value are real estate, gold and equities. Bitcoin is a better store of value for many reasons: it is more liquid, easier to access, transport and secure, easier to audit and more finitely scarce than any other asset with its hard-cap limit of 21 million coins. For bitcoin to acquire a larger share of other global stores of value, these properties need to remain intact and prove themselves in the eyes of investors.

Estimations of global stores of wealth.

As readers can see, bitcoin is a tiny fraction of global wealth. Should bitcoin take even a 1% share from these other stores of value, the market cap would be $5.9 trillion, putting bitcoin at over $300,000 per coin. These are conservative numbers from our viewpoint because we estimate that bitcoin adoption will happen gradually, and then suddenly.

Transfer Volume

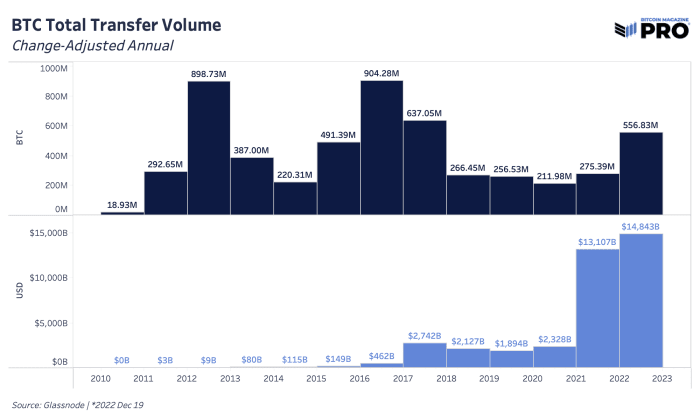

When looking at the amount of value that was cleared on the Bitcoin network throughout its history, there is a clear upward trend in USD terms with a heightened demand for transferring bitcoin this year. In 2022, there was a change-adjusted transfer volume of over 556 million bitcoin settled on the Bitcoin network, up 102% from 2021. In USD terms, the Bitcoin network settled just shy of $15 trillion in value in 2022.

Bitcoin transfer volume was higher than ever in USD terms.

Bitcoin’s censorship resistance is an extremely valuable feature as the world enters into a period of deglobalization. With a market capitalization of only $324 billion, we believe bitcoin is severely undervalued. Despite the drop in price, the Bitcoin network transferred more value in USD terms than ever before.

Rare Opportunity In Bitcoin’s Price

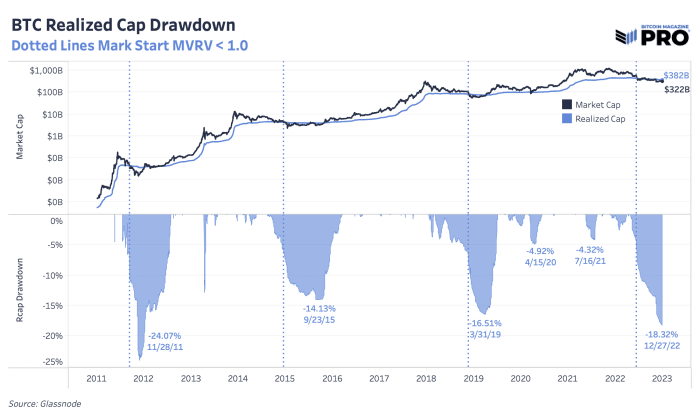

By looking at certain metrics, we can analyze the unique opportunity investors have to purchase bitcoin at these prices. The bitcoin realized market cap is down 18.8% from all-time highs, which is the second-largest drawdown in its history. While the macroeconomic factors are something to keep in mind, we believe that this is a rare buying opportunity.

The realized cap drawdown in 2022 was the second largest in bitcoin’s history.

Relative to its history, bitcoin is at the phase of the cycle where it’s about as cheap as it gets. Its current market exchange rate is approximately 20% lower than its average cost basis on-chain, which has only happened at or near the local bottom of bitcoin market cycles.

Current prices of bitcoin are in rare territory for investors looking to get in at a low exchange rate. Historically, purchasing bitcoin during these times has brought tremendous returns in the long term. With that said, readers should consider the reality that 2023 likely brings about bitcoin’s first experience with a prolonged economic recession.

Macroeconomic Environment

As we move into 2023, it’s necessary to recognize the state of the geopolitical landscape because macro is the driving force behind economic growth. People around the world are experiencing a monetary policy lag effect from last year’s central bank decisions. The U.S. and EU are in recessionary territory, China is proceeding to de-dollarize and the Bank of Japan raised its target rate for yield curve control. All of these have a large influence on capital markets.

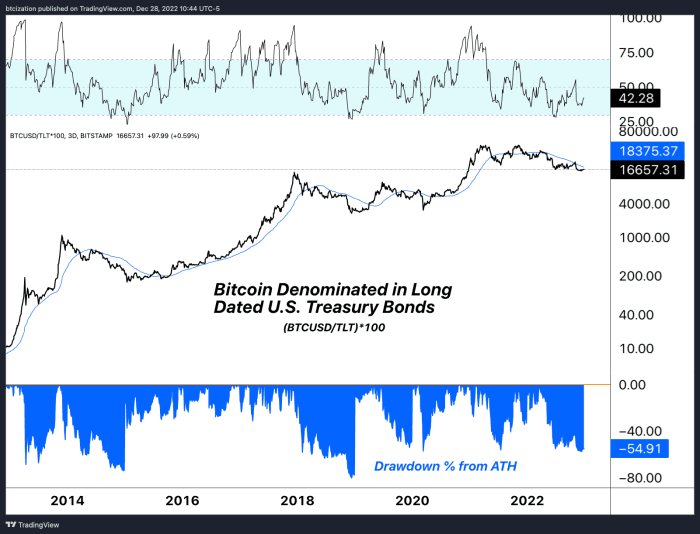

Nothing in financial markets occurs in a vacuum. Bitcoin’s ascent through 2020 and 2021 — while similar to previous crypto-native market cycles — was very much tied to the explosion of liquidity sloshing around the financial system after COVID. While 2020 and 2021 was characterized by the insertion of additional liquidity, 2022 has been characterized by the removal of liquidity.

Interestingly enough, when denominating bitcoin against U.S. Treasury bonds (which we believe to be bitcoin’s largest theoretical competitor for monetary value over the long term), comparing the drawdown during 2022 was rather benign compared to drawdowns in bitcoin’s history.

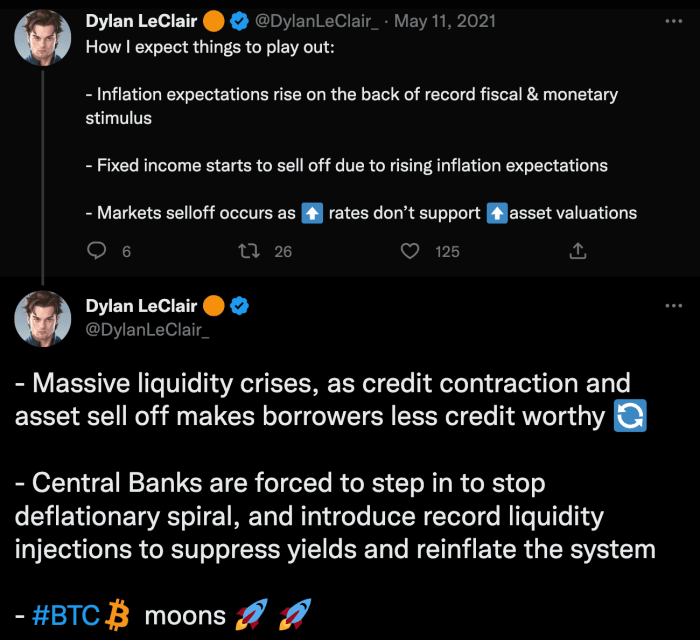

As we wrote in “The Everything Bubble: Markets At A Crossroads,” “Despite the recent bounce in stocks and bonds, we aren’t convinced that we have seen the worst of the deflationary pressures from the global liquidity cycle.”

In “The Bank of Japan Blinks And Markets Tremble,” we noted, “As we continue to refer to the sovereign debt bubble, readers should understand what this dramatic upward repricing in global yields means for asset prices. As bond yields remain at elevated levels far above recent years, asset valuations based on discounted cash flows fall.” Bitcoin does not rely on cash flows, but it will certainly be impacted by this repricing of global yields. We believe we are currently at the third bullet point of the following playing out:

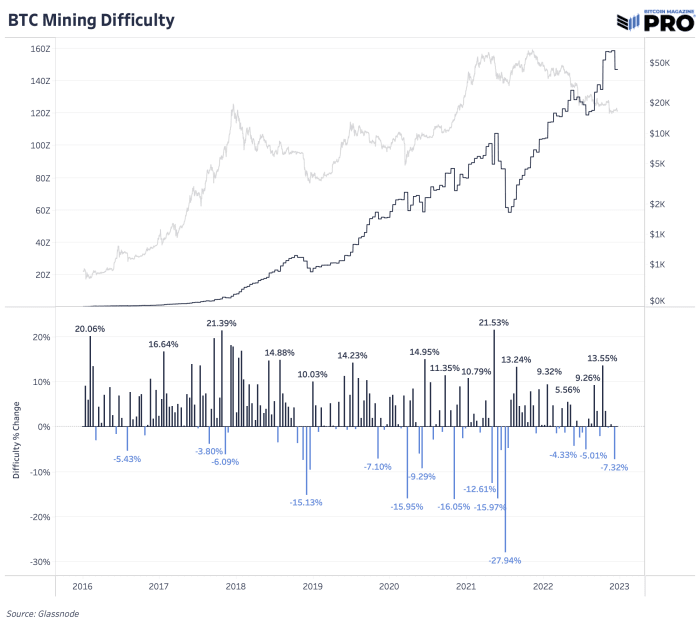

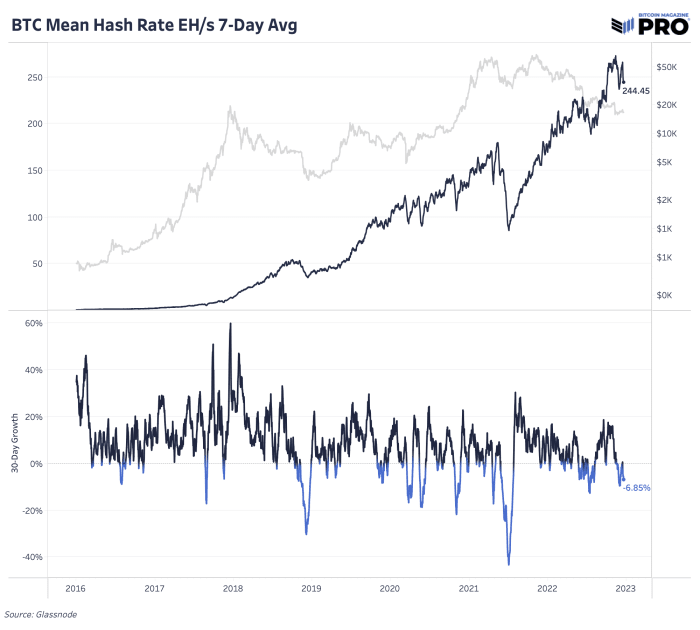

While the multitude of negative industry and worrying macroeconomic factors have had a major dampening on bitcoin’s price, looking at the metrics of the Bitcoin network itself tell another story. The hash rate and mining difficulty gives a glimpse into how many ASICs are dedicating hashing power to the network and how competitive it is to mine bitcoin. These numbers move in tandem and both have almost exclusively gone up in 2022, despite the significant drop in price.

Bitcoin mining difficulty continues to rise.

Bitcoin hash rate continues to rise.

By deploying more machines and investing in expanded infrastructure, bitcoin miners demonstrate that they are more bullish than ever. The last time the bitcoin price was in a similar range in 2017, the network hash rate was one-fifth of current levels. This means that there has been a fivefold increase in bitcoin mining machines being plugged in and efficiency upgrades to the machines themselves, not to mention the major investments in facilities and data centers to house the equipment.

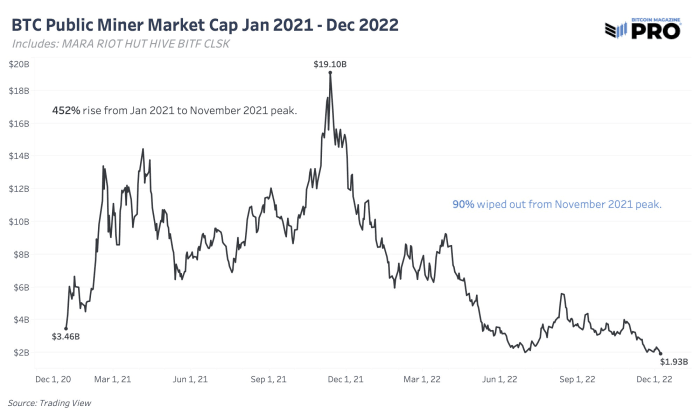

Because the hash rate increased while the bitcoin price decreased, miner revenue took a beating this year after a euphoric rise in 2021. Public miner stock valuations followed the same path with valuations falling even more than the bitcoin price, all while the Bitcoin network’s hash rate continued to rise. In the “State Of The Mining Industry: Survival Of The Fittest,” we looked at the total market capitalization of public miners which fell by over 90% since January 2021.

The market cap of all public mining equities has dropped by 9

We expect more of these companies to face challenging conditions because of the skyrocketing global energy prices and interest rates mentioned above.

Increasing Scarcity

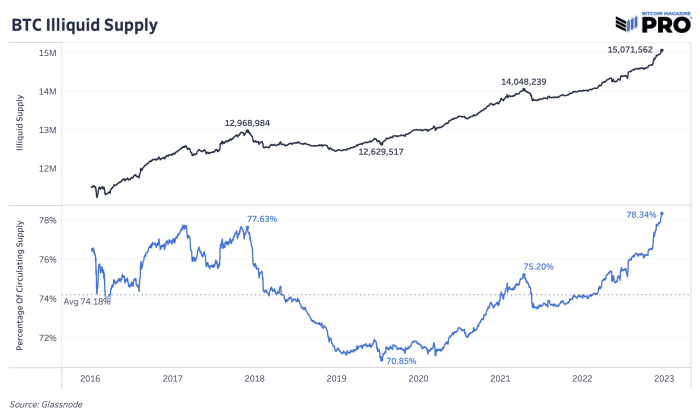

One way to analyze bitcoin’s scarcity is by looking at the illiquid supply of coins. Liquidity is quantified as the extent to which an entity spends their bitcoin. Someone that never sells has a liquidity value of 0 whereas someone who buys and sells bitcoin all the time has a value of 1. With this quantification, circulating supply can be broken down into three categories: highly liquid, liquid and illiquid supply.

Illiquid supply is defined as entities that hold over 75% of the bitcoin they deposit to an address. Highly liquid supply is defined as entities that hold less than 25%. Liquid supply is between the two. This illiquid supply quantification and analysis was developed by Rafael Schultze-Kraft, co-founder and CTO of Glassnode.

Bitcoin’s illiquid supply continues to grow.

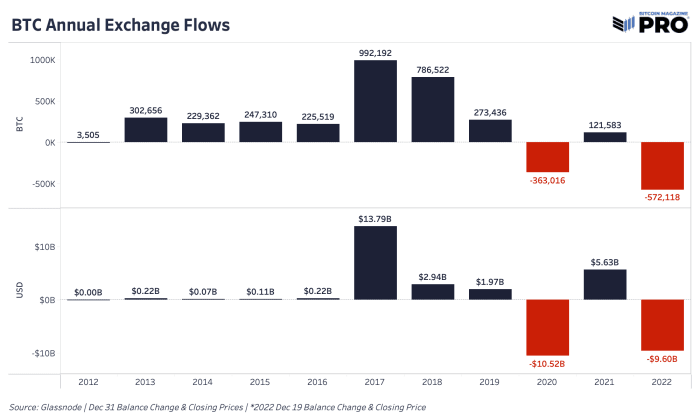

2022 was the year of getting bitcoin off exchanges. Every recent major panic became a catalyst for more individuals and institutions to move coins into their own custody, find custody solutions outside of exchanges or sell off their bitcoin entirely. When centralized institutions and counterparty risks are flashing red, people rush for the exit. We can see some of this behavior through bitcoin outflows from exchanges.

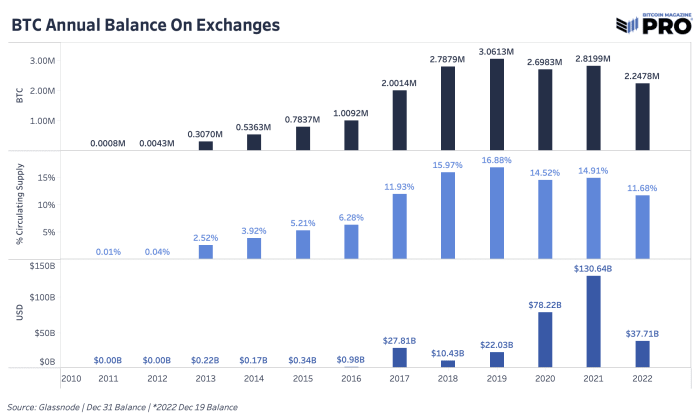

In 2022, 572,118 bitcoin worth $9.6 billion left exchanges, marking it the largest annual outflow of bitcoin in BTC terms in history. In USD terms, it was second only to 2020, which was driven by the March 2020 COVID crash. 11.68% of bitcoin supply is now estimated to be on exchanges, down from 16.88% back in 2019.

Exchanges saw a massive decrease in the bitcoin balances on their platforms.

Bitcoin balance on exchanges decreased in 2022.

These metrics of an increasingly illiquid supply paired with historic amounts of bitcoin being withdrawn from exchanges — ostensibly being removed from the market — paint a different picture than what we’re seeing with the factors outside of the Bitcoin network’s purview. While there are unanswered questions from a macroeconomic perspective, bitcoin miners continue to invest in equipment and on-chain data shows that bitcoin holders aren’t planning to relinquish their bitcoin anytime soon.

Conclusion

The varying factors detailed above give a picture for why we are long-term bullish on the bitcoin price going into 2023. The Bitcoin network continues to add another block approximately every 10 minutes, more miners keep investing in infrastructure by plugging in machines and long-term holders are unwavering in their conviction, as shown by on-chain data.

With bitcoin’s ever-increasing scarcity, the supply side of this equation is fixed, while demand is likely to increase. Bitcoin investors can get ahead of the demand curve by averaging in while the price is low. It’s important for investors to take the time to learn how Bitcoin works to fully understand what it is they are investing in. Bitcoin is the first digitally native and finitely scarce bearer asset. We recommend readers learn about self-custody and withdraw their bitcoin from exchanges. Despite the negative news cycle and drop in bitcoin price, our bullish conviction for bitcoin’s long-term value proposition remains unfazed.

This is an opinion editorial by Ansel Lindner, a bitcoin and financial markets researcher and the host of the “Bitcoin & Markets” and “Fed Watch” podcasts.

Two forces have dominated the globe economically and politically for the last 75 years: globalization and trust-based money. However, the time for both of these forces has passed, and their waning will bring about a great reset of the global order.

But this is not the global, Marxist kind of Great Reset promoted by Klaus Schwab and those who attend Davos. This is an emergent, market-driven reset characterized by a multipolar world and a new monetary system.

Globalization Is Ending

The first reaction I usually get to my claim that the age of hyper-globalization is ending is flippant disbelief. People have so completely integrated the environment of the dying global order into their economic understanding that they cannot fathom a world where the cost-to-benefit analysis of globalization is different. Even after COVID-19 exposed the fragility of complex supply chains, like when the U.S. very nearly ran out of surgical masks and basic medications or when the world struggled to source semiconductors, people have yet to realize the shift that is happening.

Is it that hard to imagine that the businessmen who designed such fragile, overcomplicated production processes didn’t properly weigh the risks?

All that is needed to break globalization is for risk-adjusted costs to change a few percentage points and outweigh the benefits. The pennies saved by outsourcing numerous tasks to numerous jurisdictions will no longer outweigh the possibility of complete collapse of supply chains.

Gone is the time when complex supply chains were robust against typical risks. The risks today are much more systemic. Sure, there were skirmishes around the world and disagreements among parliaments, but great powers did not openly threaten one another’s spheres of influence. Risk-adjusted costs and benefits to globalization have radically changed.

Credit Doesn’t Like Conflict

Very closely related to deglobalization of supply chains is deglobalization of credit markets. The same factors that affect business peoples’ physical, risk-adjusted costs and benefits are also felt by bankers.

Banks don’t want to be exposed to the risk of war or sanctions wrecking their borrowers. In the current environment of deglobalization and rising risks to international trade, banks will naturally pull back on lending to those associated activities. Instead, banks will fund safer projects, likely fully-domestic or friend-shoring opportunities. The natural reaction by banks to this risky global environment will be credit contraction.

The deglobalization of supply chains and credit will be as closely linked on the way down as they were on the way up. It will start slowly, but pick up speed. A feedback loop of rising risk leading to shorter supply chains and less credit creation.

The Credit-Based U.S. Dollar

The prevailing form of money in the world is the credit-based U.S. dollar. Every dollar is created through debt, making every dollar someone else’s debt. Money is printed out of thin air in the process of making a loan.

This is different from pure fiat money. When fiat money is printed, the balance sheet of the printer adds assets alone. However, in a credit-based system, when money is printed in a loan, the printer creates an asset and a liability. The borrower’s balance sheet then has an offsetting liability and asset, respectively. Every dollar (or euro or yen, for that matter) is therefore an asset and a liability, and the loan that created that dollar is both an asset and a liability.

This system works extremely well if two factors are present. One, highly-productive uses of new credit are available, and two, a relative lack of exogenous shocks to the global economy. Change either of these things and a breakdown is bound to occur.

This dual nature of credit-based money is at the root of both the dollar’s spectacular rise in the 20th century, and the coming monetary reset. As global trust and supply chains break down, the comingling of assets in banks becomes more risky. Russia found this out the hard way when the West confiscated its reserves of dollars held in banks abroad. How is trust possible in that sort of environment? When credit-based money’s creation is based on trust… Houston, we have a problem.

Bitcoin’s Role In The Future

Luckily, we have experience with a world that doesn’t trust itself — i.e., the entire history of man prior to 1945. Back then, we were on a gold standard for reasons which included all those that bitcoiners are very familiar with (gold scores highly in the characteristics that make good money), but also because it minimized trust between great powers.

Gold lost its mantle for one reason — and you’ve probably never heard this anywhere before: because the global economic, political and innovation environment post-WWII created an extremely fertile soil for credit. Trust was easy, the major powers were humbled and all joined the new international institutions under the security umbrella of the U.S. The Iron Curtain provided a stark separation between zones of trust economically, but after it fell, there was a period of roughly 20 years where the world sang “kumbaya” because new credit was still extremely productive in the old Soviet block and China.

Today, we are facing the opposite sort of scenario: Global trust is eroding and credit has exploited all productive low-hanging fruit, forcing us into a period that demands neutral money.

The world will soon find itself split between regions/alliances of influence. A British bank will trust a U.S. bank, where a Chinese bank will not. To bridge this gap, we need money that everyone can hold and respect.

Gold Vs. Bitcoin

Gold would be the first choice here, if not for bitcoin. This is because gold has several drawbacks. First, gold is owned mainly by those groups who are losing trust in one another, namely the governments of the world. Much of the gold is held in the United States. Therefore, gold is unevenly distributed.

Second, gold’s physical nature, once a positive holding profligate governments in check, is now a weakness because it cannot be transported or assayed nearly as efficiently as bitcoin.

Lastly, gold is not programmable. Bitcoin is a neutral, decentralized protocol that can be tapped for any number of innovations. The Lightning Network and sidechains are just two examples of how Bitcoin can be programmed to increase its utility.

As globalization of both trade and credit is breaking down, the economic environment favors a return to a form of money that doesn’t depend on trust between major powers. Bitcoin is the modern answer.

This is a guest post by Ansel Lindner. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

This is a transcribed excerpt of the “Bitcoin Magazine Podcast,” hosted by P and Q. In this episode, they are joined by Matthew Pines to talk about China’s plan for world domination and why FTX and Binance are “like a bug hitting the windshield” in terms of the general macroeconomic scene.

Matthew Pines: We made these typical imperial hubristic mistakes with Iraq and we had a Great Financial Crisis that sort of focused on internal politics, and geopolitics kind of went to the backburner or became a domain of Sunday news shows. “Are we gonna do an Iraq surge or are we gonna do a reset with Russia?” Or whatever.

Now, it’s gonna become present because it filters into every aspect of your lives Where you get your stuff. Is that gonna come the next time? I think COVID sort of woke us up to this. I think we felt that it was just gonna be like a temporary disruption and then everything was gonna just settle back to normal. That’s not the case.

That’s why Taiwan matters. That’s why these things matter because they’re highly path dependent. We live in a very highly non-linear, coupled dynamic system where the butterfly flaps its wings and you get a hurricane. It’s why you have to pay attention.

Why focus on all the little things? Because those little things can turn into very big things very quickly. FTX is a good example of this. “Oh, there’s some weirdness going on with CZ and why did he just post that thread?” And then, all of a sudden, the token falls by 90% in a day.

Like these systems we built look stable and then they break. That’s why I like Bitcoin because Bitcoin’s one of those systems that is by definition decentralized, so it can absorb lots of shocks. The China mining ban was a great example where it took a massive hit exogenous shock boom. But then the hash rate is at all-time highs. Doesn’t mean the dollar price is gonna be stable by any means; it’s gonna likely be highly volatile. But these are very different models for how you think about building systems and that’s what attracts me a lot about Bitcoin is that they model a type of system that assumes nothing’s gonna work out and assumes that things are gonna break. You just need to build resilience and redundancy, decentralization to those systems, so you’re not vulnerable to single points of failure. You’re not vulnerable to an opaque balance sheet or a single person making a bad decision, and then that has cascading implications to everyone who is anywhere nearby.

That’s sort of my broader thesis to kind of connect these things, why it’s so important to look at FTX and be like, “We should draw lessons learned on this.” You’ll see it reflected in asset prices, but if you’re not a day trader, if you’re not trying to time the tops and bottoms, it really doesn’t matter to you.

This is a transcribed excerpt of the “Bitcoin Magazine Podcast,” hosted by P and Q. In this episode, they are joined by Dr. Jeff Ross to discuss how current macro events are affecting bitcoin and what to expect from the bitcoin price.

Jeff Ross: Here’s what I like to say about bitcoin: I’m a wild fanatic about bitcoin for its long term prospects. I’m still very bearish macro-wise. I still think risk assets are gonna get hammered. I think it’s quite possible that bitcoin — let’s talk in terms of probability. This is a really long answer to your question. There’s a chance bitcoin is bottomed and $17,600 was the bottom and there’s a good chance that it could just do a slow grind higher. There’s also a chance that if the Fed pauses, that will get a really impressive rally in risk assets and that bitcoin will also catch a strong bid if that happens. But if things continue to get worse and we have a capitulation-type event in stocks, I think it sucks bitcoin down with it. I think if we get another crypto-contagion event that I’m sure you guys have already talked about today with SBF [Sam Bankman-Fried] and FTX and Alameda and Binance and all that garbage — if we have another crypto-contagion event, I think it pulls bitcoin down too. So even though bitcoin doesn’t deserve it and even though bitcoin has nothing to do with that garbage, it’s still gonna get sucked down alongside of it. That’s just what happens. Anyway, that’s my really long answer to say I’m sort of cautiously optimistic based on its price action for a trade, but I don’t think we’re out of the woods yet. I think in the next nine months things are gonna be still kind of rough and we’ll see what happens.