Citi added to its treasury product portfolio this week with the launch of Citi Real-Time Funding to help business clients keep up with liquidity needs in an automated fashion. “Our clients’ businesses are changing,” Ambrish Bansal, global head of liquidity and cash concentration products of Citi Services, told Bank Automation News, noting that clients are […]

The SEC is adopting stricter compliance rules for large capital investors in Treasury Markets, but some provisions seem to impact decentralized finance users.

On Feb. 6, the U.S. Securities and Exchange Commission (SEC) adopted two rules mandating that market participants engaging in substantial liquidity-providing activities register with the watchdog and join a self-regulatory organization, thus complying with regulatory obligations and federal financial laws.

Initially proposed in March 2022 and geared toward bolstering Treasury market safety, the rules include provisions that speak to crypto asset securities. Defi investors providing over $50 million in liquidity to automated market makers, like Uniswap, will fall under the SEC’s purview if this legislation is enforced.

A 3-2 vote settled the SEC’s deliberation on the rules, with Commissioner Hester Peirce and Mark Uyeda opposing the proposal. Commissioners Gary Gensler, Caroline Crenshaw, and Jaime Lizarraga supported the idea.

This rulemaking targets proprietary trading funds, private funds, and others who make money by buying low and selling high in the Treasury market, while creating additional regulatory confusion in other markets, including crypto asset securities.

Crypto proponents such as the Blockchain Association and the DeFi Education Fund pushed back on the policies in comments letter when the rules were first introduced. Miller Whitehouse Levine, CEO of the DeFi Education Fund, argued that the expanded definition of a market dealer was too ambiguous and left several unaddressed concerns regarding defi protocols.

Commissioner Peirce questioned how an automated market maker (AMM), essentially software, might register with the SEC and how many firms the new rules would impact. Haoxiang Zhu, the SEC’s director for the trading and markets division, said the proposal was aimed at individuals leveraging decentralized software rather than the technology itself.

Zhu added that limited information and sweeping non-compliance from defi actors made it difficult to pinpoint the participants who would be affected.

One of the reasons they’re not compliant is they can’t figure out what our rules are. They can’t even figure out when we think that something is a security.

Hester Peirce, SEC commissioner

🚨Very important exchange from today’s SEC hearing where SEC staff assert that the new broker-dealer rule will make all LPs in AMMs into securities dealers with a registration requirement. Paraphrase of @HesterPeirce ‘s incisive questioning of staff below: 🚨

Polish farmers ended a blockade of a Poland-Ukraine border crossing after reaching an agreement with Warsaw that met their demands, defusing a dispute that had become an early test of the new government of Prime Minister Donald Tusk.

Newly appointed Polish Agriculture Minister Czesław Siekierski signed the deal with Polish farmers blockading the Medyka-Shehyni border crossing with Ukraine late Saturday. The protest — which started over a month ago — was called off on December 24 following an agreement with the government, but it resumed on Wednesday amid farmers’ mistrust over the deal.

Farmers accused the new Polish government of failing to defend them against Ukrainian grain imports, but also demanded a series of financial support measures. Saturday’s deal finally implemented those financial demands — which include launching corn production subsidies, maintaining agricultural taxes at 2023 levels and increasing preferential liquidity loans — but didn’t include restrictions on Ukraine imports.

The measures “will be implemented after the legislative process is completed and acceptance by the European Commission is obtained,” the Polish Agriculture Ministry said.

Despite calling off the blockade, protesting farmers said that the “most important” demand now is “to limit the inflow of goods from Ukraine.” EU Agriculture Commissioner Janusz Wojciechowski told Polish media on Friday that he would demand an EU-wide restriction on items like sugar, eggs and poultry from Ukraine.

“These imports are growing in a way that threatens the competitiveness of the EU sector, including Polish poultry and sugar production,” he said. The Polish commissioner has already clashed with other members of the European Commission over full trade liberalization with Ukraine, which the EU executive is expected to recommend as early as next week.

“Ukraine is such a country that they just want to take, take, take, and give nothing back,” Roman Kondrów, one of the protest leaders, told POLITICO by phone on Thursday, warning about the risks of allowing the country to join the EU without restrictions.

In the meantime, Polish truckers are continuing to protest as they want the government to end an EU-Ukraine agreement that liberalized road transport rules in an effort to help the Ukrainian economy, crippled by the Russian invasion.

Underpinning the narratives of both groups are doomsday scenarios about the impact on Poland of Ukraine one day becoming a member of the EU. At a summit in December, EU leaders agreed to open accession talks with Ukraine.

Sandra Thompson, director of the Federal Housing Finance Agency, released a report Tuesday outlining potential changes to the Federal Home Loan Bank system — which FHFA supervises — that would more closely tether the FHLBs’ housing and liquidity missions to each other. But experts say doing that in practice will be challenging, particularly if the Home Loan Banks themselves oppose the measures.

Bloomberg News

The Federal Housing Finance Agency wants to more closely tie the liquidity that the Federal Home Loan Banks provide to financial institutions to the system’s mission of promoting housing and community development, but bringing those dual missions in line may be easier said than done.

A main takeaway of the 115-page report released Tuesday is that FHFA plans to issue a proposed rule that would clarify the mission of the Federal Home Loan Bank System while providing metrics and thresholds for measuring how each of the 11 FHLBs advance that mission. FHFA also is considering how to incorporate what it calls “mission achievement” in its exam processes, and may potentially include a stand-alone “mission examination” rating for each of the banks.

But one key concern about such a proposal is whether the Home Loan Banks will embrace the FHFA’s suggestions, given that the Home Loan Banks have been championing their role of providing liquidity and thus financial stability to member institutions, and the possibility that many of the proposed changes would cut into profits that members receive in the form of hefty dividends.

“There are ways to make this work, but at the end of the day none of this will work if the FHLBs don’t get engaged,” said Peter Knight, the cofounder of Policy Kinetics, who worked for 19 years as a director of government relations at the Federal Home Loan Bank of Pittsburgh.

Experts who have followed the FHLBs for decades called the report and its suggestions an ambitious undertaking. The FHFA’s recommendations are the beginning of a multi-year effort to encourage the government-sponsored enterprise to do more to promote liquidity alongside housing and community development. Most of the changes will be implemented through ongoing supervision, guidance and rules. But some of the more sweeping changes — such as increasing the amount of liquidity steered toward affordable housing and oversight of executive compensation — would require Congressional action.

Former FHFA Director Mark Calabria, a senior advisor at the Cato Institute, said the report’s findings and recommendations were in line with what he expected, and were reasonable given the lack of specificity in the Federal Home Loan Bank Act of 1932 about membership eligibility and other key provisions.

Calabria said the FHFA was justified in seeking congressional input on whether there should be a renewed focus on housing finance, one that could put stricter limits on the types of institutions that can access FHLB advances or the types of activities they can engage in. But he urged his former agency not to wait for Congress to take action, noting that some changes are already well within its reach.

“It would be great if Congress would come in and clarify some of these things, and FHFA is not without justification in asking if there should be a refocus of purpose,” Calabria said. “But there are aspects, like limiting the exposure of any one member, that FHFA can do on its own.”

Michael Ericson, president and CEO the FHLB Chicago, said in an interview that “a tremendous amount” of borrowing by members goes toward supporting housing and community development. As an example, he cited a program in Chicago that provides interest-free advances to member institutions that make direct small business loans that support community development. He said the FHLBs are not doing enough to promote their work.

“This report doesn’t change anything that we do today. We’re doing activities in our members’ districts to support economic development, to support small businesses, to support housing. These are all things that we’re doing today,” Ericson said. “I think what gets missed in a lot of this is, historically, we have not highlighted all of the great things that we’ve been doing. But this process has educated us that we need to do a much better job of informing others about the great things that we are doing. And I think that’s been missed in some of the narratives.”

Ericson pushed back against the FHFA’s plans to propose a rule that would require that certain members hold at least 10% of their assets in residential mortgage loans on an ongoing basis to remain eligible for FHLB financing. FHFA said in the report that it expects to analyze the impacts of a 10% asset requirement on different member institutions, such as insurance companies and community development financial institutions, as part of the rulemaking process.

“There are certain things in the report that we wouldn’t agree with and this is an area that we would object to,” Ericson said.

He noted that in 2014, the FHFA proposed a similar rule that the FHLBs also objected to.

“This isn’t really new ground that the finance agency is potentially charting here,” he said. “There are a number of factors in place that impact a member institutions’ assets they have on their balance sheet. One day, they could easily pass the test and the next day, they may not be able to. If you are a stable, reliable partner to your member institutions, they need to know that and they need to know what the rules are. And introducing volatility like that would be very difficult to manage, so it’s not something that we would agree to.”

The review of the Home Loan Bank began in July 2022, well before the March 2023 liquidity crisis led to increased scrutiny of FHLBs after it was discovered that they lent billions to three banks that later failed — Silicon Valley Bank, Signature Bank and First Republic Bank — and to another, crypto-friendly Silvergate Bank, which self-liquidated. Those banks all received short-term loans, known as advances, in an attempt to make up for massive declines in deposits. In the first week of March 2023 alone the FHLBs funded $675.6 billion in advances — the largest one-week volume in the history of the government-sponsored enterprise.

Calabria said it was predictable that the FHFA report would focus on the role federal regulators play in monitoring the health of member banks, given the string of large bank failures this spring. But he argued that the FHLBs already rely too heavily on the Fed, the Federal Deposit Insurance Corp. and the Office of the Comptroller of the Currency to assess the creditworthiness of banks. He urged the FHLBs to take a more discerning approach to issuing advances moving forward.

“The Federal Home Loan Banks need to take a separate view of their members than their primary regulators. They can share information but they shouldn’t be overly deferential,” Calabria said. “Supervising a bank and dealing with a counterparty are two different things with two different sets of goals. I worry that this report blurs that line.”

The FHFA specified in the report that the FHLBs should not be used as a “lender of last resort,” noting that banks should not be “overly reliant” on the FHLBs for liquidity. Moreover, banks should have the necessary agreements or collateral positions in place to borrow from the Federal Reserve’s discount window, the report said.

“The reliance of some large, troubled members on the FHLBanks, rather than the Federal Reserve, for liquidity during periods of significant financial stress may be inconsistent with the relative responsibilities of the FHLBanks and the Federal Reserve,” the FHFA report said.

To that end, FHFA plans to address weaknesses in the FHLB’s oversight of its members’ liquidity and credit risk management, which Ericson said is already underway.

“We will implement recommendations that the Finance Agency has provided to the Federal Home Loan Banks,” Ericson said. “The banks have robust credit risk management practices in place today and they had credit risk management practices in place going into the crisis. And we’re implementing the guidance that the Finance Agency has provided to us.”

Cornelius Hurley, an advisor to the Coalition for FHLB Reform and a former independent director of the FHLB of Boston, said the debate about the FHLBs should focus on the subsidy that members receive through the implied government guarantee on the debt the system issues.

“The Home Loan Banks and their members view the FHLB system as an entitlement to low-cost funds, and they are enriching themselves without providing something in return,” Hurley said.

The FHFA report estimated the value of the implicit guarantee at $4.7 billion in 2022. By comparison, the FHLBs collectively contributed roughly $200 million in affordable housing subsidies last year. The Bank Act requires that each FHLB contribute at least 10% of its prior year’s net earnings on an annual basis to fund affordable housing programs.

Kathryn Judge, a law professor at Columbia University who has researched the FHLBs, said the report was a step in the right direction, but said that more needs to be done. She said the report identifies several key challenges in the current system, including the risks to the Federal Deposit Insurance Corp. and the National Credit Union Administration, which are responsible for paying off advances to the FHLBs ahead of other creditors when institutions fail. She applauded many of the changes outlined in the report, including those that would require the FHLBs to ensure members are financially healthy before making advances.

“In light of what transpired this spring, those bank regulators should be eager to work more closely with the Federal Home Loan Banks,” she said.

But Judge said the report fails to meaningfully address what she sees as the core issue of the FHLB system: its mission. As it stands now, the FHLBs extend loans to banks of all sizes for all types of uses, a reality that she said goes against the spirit of the system, which was conceived to support thrifts at a time when they could not access the Fed’s discount window.

“The short-term goal should be to implement as many suggested rules as possible,” Judge said. “Then there should be conversations about how to help the public enjoy the benefits from the public subsidies the system enjoys and how to harness the system to support small institutions and create credit access.”

The below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

An independent bitcoin rally or a high-beta move? Either way, bitcoin holders are celebrating the latest action to start 2023. Bitcoin has shown some significant momentum and has powered through every key short-term price level across daily moving averages and on-chain realized prices. In fact, every major high-beta play in the market is showing the same strength which gives us more caution than confidence in this latest short squeeze highlighted last week in “Bitcoin Rips To $21,000, Shorts Demolished In Biggest Squeeze Since 2021.”

As much as we would like to see an independent bitcoin move higher, there’s plenty of signs in the market showing the opposite is likely. We’ve seen a relatively meaningful bounce in the most oversold names of 2022, with a short squeeze and subsequent round of FOMO off the 2022 lows.

Bitcoin versus high beta returns.

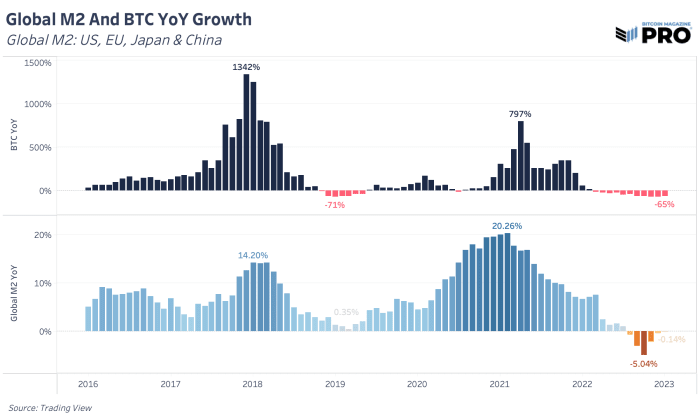

This recent risk rally has seen implied equity market volatility drift to new lows as the U.S. dollar continues to weaken over the short-term, National Financial Conditions Index (NFCI) loosens and global M2 money supply contracts at a much slower pace relative to the last few months.

Global M2 mapped against bitcoin’s year-over-year growth.

Net liquidity, a model we highlighted in our previous piece, shows a contraction compared to last year but hasn’t changed much over the last few months. If we’re to see a sustained rally continue, we’d like to see growth in net liquidity over the next couple of months to be the main driver accompanying this move.

In their recent meeting minutes, members of the Federal Reserve expressed concern about the “unwarranted easing in financial conditions” caused by the run-up in risky assets and subsequently hindering their efforts to cool inflation.

With the Bank of Japan deciding on whether to loosen their monetary policy, this could cause the carry trade to unwind. We view this to be one of the few ways where both the dollar could fall at the same time as global equity markets weaken, with equities repricing due to rising costs of U.S. capital.

Like this content? Subscribe now to receive PRO articles directly in your inbox.

The below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

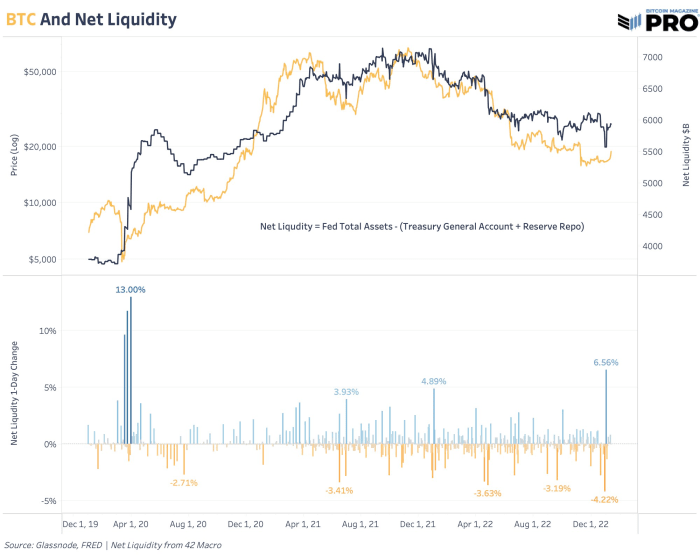

Net Liquidity And Moving Averages

One of the most useful models in tracking the cyclical tops for both the S&P 500 Index and bitcoin since March 2020 has proven to be net liquidity, an original model by 42 Macro. Net liquidity tracks the changes in Federal Reserve total assets, the U.S. Treasury general account balance and the reverse repo facility. A lower net liquidity translates to less capital available to deploy in markets. We find it useful as a key macro indicator to assess current liquidity conditions and how bitcoin trades in the market.

Bitcoin has acted as a liquidity sponge throughout its life and contracting liquidity in all markets has had a significant impact on the bitcoin price and trajectory. Ultimately, that’s one of the main drivers of our core long-term thesis that bitcoin’s growth depends on an environment of perpetual monetary debasement and expanding liquidity to work against current levels of unsustainable sovereign debt and deflationary forces. In the short-term, it’s not clear when overall liquidity will increase again en masse. That’s the trillion dollar question and the topic of conversation on which everyone is speculating. Net liquidity provides a view into that trajectory as a measure that’s updated weekly with fresh data.

Bitcoin is seeing some of its largest relative strength since January 2021, but it also comes at a time when we’re seeing a significant daily uptick in net liquidity after a period of historically low volatility. The uptick is driven by a much lower reverse repo balance since the start of the year. With the Fed’s position of “higher for longer,” a projected view of Core CPI at 3.5% for 2023 and continued balance sheet runoff, we will likely see net liquidity decline — barring a spontaneous or emergency policy reversal.

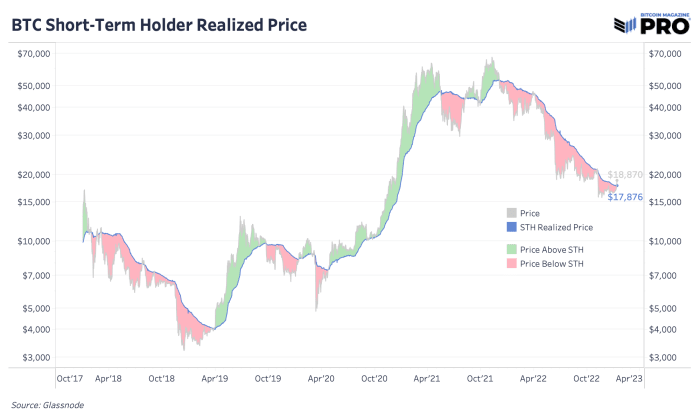

Price has broken above the short-term holder realized price. That’s happened only a few times in this bear market and these events were short-lived. As this price reflects the average on-chain cost basis of the more recent buyers, it will be key to see if these market participants are looking to sell here at cost or if they will stay to continue with the momentum.

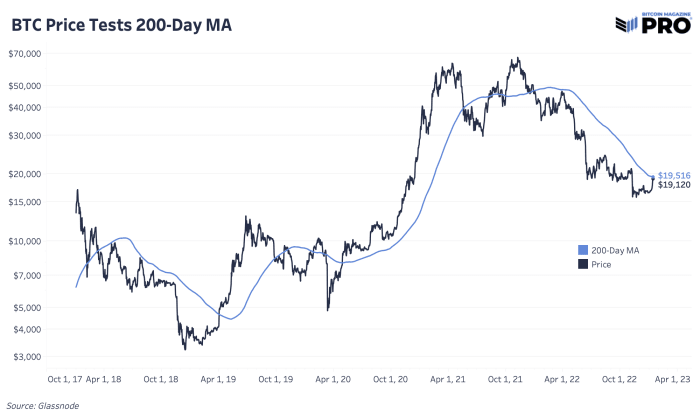

The 200-day moving average may seem somewhat arbitrary, but the mere fact that many technical traders and momentum- and trend-based investors monitor this level gives it significance. A clean break above could mean continued strength for bitcoin in the coming days and weeks ahead.

The price action to start the new year has been quite the promising sign for bitcoin bulls. Similarly, over the last week, shorts as a percentage of futures liquidations has reached its highest level in the history of the data. While shorts have been decimated as of late, it’s likely that this immediate upside could be capped.

While there is a long way to go in terms of surpassing previous bull market heights, the year-to-date performance has been hopeful following a year where the industry practically imploded.

Overall, this is a promising start to 2023.

Like this content? Subscribe now to receive PRO articles directly in your inbox.

Binance walks away from FTX deal following due diligence.

Firm also mentioned U.S. investigations of FTX.

Retail investors are left hanging without access to funds.

Binance will not move forward with the acquisition of rival exchange FTX, the company said in a tweet Wednesday afternoon.

“In the beginning, our hope was to be able to support FTX’s customers to provide liquidity, but the issues are beyond our control or ability to help,” Binance said.

The news leaves retail investors wondering whether they’ll ever gain access to funds held by FTX again after the exchange came under extreme liquidity pressures earlier this week. The turmoil likely stemmed from a CoinDesk article that detailed worrisome links between FTX, its native token FTT, and Alameda, a research and trading firm also owned by FTX boss Sam Bankman-Fried. The coverage got the attention of Binance chief Changpeng Zhao, who shortly after tweeted that his company would be selling all FTT tokens it held.

CZ’s tweet sparked a feud with SBF, who said, in a since-deleted tweet, that FTX was fine and assets held by the company were as well. Soon after, however, the deal between Binance and FTX came to light, with SBF then conceding to a “liquidity crunch.”

The bailout sparked optimism in the industry. However, CZ made it clear from the start that Binance could walk out from the deal “at any time.” Notably, the company had yet to perform due diligence by analyzing FTX’s financial books in order to decide whether to move forward with the acquisition.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Liquidity Is In The Driver Seat

By far, one of the most important factors in any market is liquidity — which can be defined in many different ways. In this piece, we cover some ways to think about global liquidity and how it impacts bitcoin.

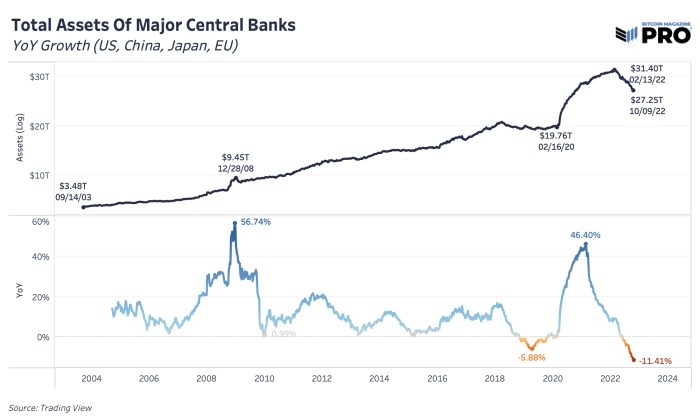

One high-level view of liquidity is that of central banks’ balance sheets. As central banks have become the marginal buyer of their own sovereign debts, mortgage-backed securities and other financial instruments, this has supplied the market with more liquidity to buy assets further up the risk curve. A seller of government bonds is a buyer of a different asset. When the system has more reserves, money, capital, etc. (however one wants to describe it), they have to go somewhere.

In many ways that has led to one of the largest rises in asset valuations globally over the last 12 years, coinciding with the new era of quantitative easing and debt monetization experiments. Central bank balance sheets across the United States, China, Japan and the European Union reached over $31 trillion earlier this year, which is nearly 10X from the levels back in 2003. This was already a growing trend for decades, but the 2020 fiscal and monetary policies took balance sheets to record levels in a time of global crisis.

Since earlier this year, we’ve seen a peak in central bank assets and a global attempt to wind down these balance sheets. The peak in the S&P 500 index was just two months prior to all of the quantitative tightening (QT) efforts we’re watching play out today. Although not the only factor that drives price and valuations in the market, bitcoin’s price and cycle has been affected in the same way. The annual rate-of-change peak in major central banks’ assets happened just weeks prior to bitcoin’s first push to new all-time highs around $60,000, back in March 2021. Whether it’s the direct impact and influence of central banks or the market’s perception of that impact, it’s been a clear macro driving force of all markets over the last 18 months.

There is a global attempt to wind down central bank balance sheets

At a market cap of just fractions of global wealth, bitcoin has faced the liquidity steamroller that’s hammered every other market in the world. If we use the framework that bitcoin is a liquidity sponge (more so than other assets) — soaking in all of the excess monetary supply and liquidity in the system in times of crisis expansion — then the significant contraction of liquidity will cut the other way. Coupled with bitcoin’s inelastic illiquid supply profile of 77.15% with a vast number of HODLers of last resort, the negative impact on price is magnified much more than other assets.

One of the potential drivers of liquidity in the market is the amount of money in the system, measured as global M2 in USD terms. M2 money supply includes cash, checking deposits, savings deposits and other liquid forms of currency. Both cyclical expansions in global M2 supply have happened during the expansions of global central bank assets and expansions of bitcoin cycles.

We view bitcoin as a monetary inflation hedge (or liquidity hedge) rather than one against a “CPI” (or price) inflation hedge. Monetary debasement, more units in the system over time, has driven many asset classes higher. Yet, bitcoin is by far the best-designed asset in our view and one of the best-performing assets to counteract the future trend of perpetual monetary debasement, money supply expansion and central bank asset expansion.

It’s unclear how long a material reduction in the Fed’s balance sheet can actually last. We’ve only seen an approximate 2% reduction from a $8.96 trillion balance sheet problem at its peak. Eventually, we see the balance sheet expanding as the only option to keep the entire monetary system afloat, but so far, the market has underestimated how far the Fed has been willing to go.

The lack of viable monetary policy options and the inevitability of this perpetual balance sheet expansion is one of the strongest cases for bitcoin’s long-run success. What else can central banks and fiscal policy makers do in future times of recession and crisis?