Every weekday the CNBC Investing Club with Jim Cramer holds a “Morning Meeting” livestream at 10:20 a.m. ET. Here’s a recap of Wednesday’s key moments. Stocks in the first half Why we trimmed P & G WFC, MS boost dividends 1. Stocks in the first half U.S. stocks started slightly lower Wednesday after the market notched a strong first half of 2023 last week. The S & P 500 shot up more than 15% in the first six months of this year. Since 1950, the benchmark gauge has only replicated this performance 11 times. If history repeats itself, July will be strong as well for equities. The last four times the index gained more than 15% in the first six months of the year, the S & P finished with a stronger full-year gain. The Dow , S & P 500 and tech-heavy Nasdaq have notched eight straight years of gains in July. 2. We trimmed P & G We sold 100 shares of Procter and Gamble (PG), shortly after the opening bell on Wednesday. This decreased the consumer staples giant’s weighting in Jim Cramer’s Charitable Trust to 2.78% from 3.3%, realizing a small loss since the stock was first purchased in April 2022. After a roughly 6% rally since early last month, P & G is trading near levels it once struggled to break above. 3. WFC, MS boost dividends After passing the Fed’s annual health check, Wells Fargo (WFC) and Morgan Stanley (MS) increased their quarterly dividends for shareholders. WFC’s annual dividend yield increased to around 3.23%, while MS’ dividend yield inched up to 3.93%. WFC said it has the capacity to continue to repurchase stock, while Morgan Stanley reauthorized an up to $20 billion multiyear buyback program. Jim Cramer said Wednesday, “It’s really a mistake not to be a buyer” of these two stocks. (Jim Cramer’s Charitable Trust is long WFC, MS and PG. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Club holdings Wells Fargo (WFC) and Morgan Stanley (MS) aced the Federal Reserve’s stress tests, showing new signs of improved resiliency and fresh hopes for the continued return of excess capital to shareholders. All 23 of the U.S. banks included in the Fed’s exercise passed with room to spare in their capital buffers. The annual health check aims to measure how financial institutions can withstand a severe economic downturn. This year’s results, out late Wednesday, came just months after the collapse of Silicon Valley Bank in March, which touched off other regional bank failures and a mini-banking crisis. “Bank stocks had a good day [Thursday]. Understandable because this year’s stress tests came against a backdrop of uncertainty for the sector. Markets certainly paid attention to the results by name,” Nicholas Colas, DataTrek Research co-founder, told CNBC, adding “the next big event” will be when banks will announce plans for dividends and buybacks based on the tests. The Fed told banks to wait until Friday after the bell to announce any actions they plan. As for the results, JPMorgan, Bank of America, and Wells Fargo were the “big improvers here” in the 2023 stress tests, Doug Butler, director of research at Rockland Trust, told CNBC. “Citi was the worst of the big banks,” he added, pointing to Citi’s marginal stock gain Thursday while the others finished sharply higher. In Friday trading, Wells Fargo and Morgan Stanley added to their prior-session gains. The stress tests Starting in the aftermath of the 2007-2009 Great Financial Crisis, bank stress tests were designed as a tool to ensure that so-called too-big-to-fail institutions could endure a similar calamity. Essentially, they hold firms accountable to manage themselves as if the next recession were always just right around the corner. These tests also give investors insight into how much excess capital the sector can be returned to its shareholders via dividends and buybacks. The tests subject banks to a worst-case scenario that was more extreme than last year. Firms endured a hypothetical “severe global recession” where unemployment surged to 10%, home prices declined 38% and commercial real estate values plunged 40%, according to the Fed. Despite that stimulated painful climate, banks largely performed better than in 2022. The good news Results indicated that Wells Fargo and Morgan Stanley can get by with lower stress capital buffers, which basically assess how much capital a bank has after factoring in losses in a stressed scenario plus the pre-funding of four quarters of dividends, with a 2.5% floor. The regulatory minimum ratios on Common Equity Tier 1 (CET1), which account for a bank’s liquid assets, declined at both banks as well, reinforcing the idea that both have strong capital positions with excess money to return to shareholders. WFC MS YTD mountain Wells Fargo vs. Morgan Stanley YTD performance It’s worth noting that Wells Fargo is in a unique situation compared to its rivals. In 2018, the Fed announced an enforcement action on Wells Fargo that caps the firm from managing over $1.9 trillion in assets. We believe the timing of a Fed decision to lift the asset cap as a when, not if scenario, which would allow the bank to increase its balance sheet and generate more profits. The unknowns Following the collapse of SVB and other regional lenders, regulators are watching the financial resiliency of Wall Street even closer. However, the Fed stress test was not updated to factor in rising interest rate risks, which was one of the factors that played into SVB’s failure. “The headlines are correct in that the tests showed that larger banks have sufficient capital to handle an economic shock. Two caveats, though. The first is that regionals fared less well, and they have been under increased scrutiny lately because of SVB,” Colas said. He added that the “stress tests only really address a macro environment where rates decline during a crisis. There is no stress test for an inflation shock that pushes rates higher and the economy lower.” Financial regulators may soon clamp down further on the banking sector. According to a Wall Street Journal report earlier this month, rule changes could require major banks to hold as much as 20% more capital. In theory, this could be negative because banks may lend less, eating into revenue streams like fees. Chris Kotowski, senior research analyst at Oppenheimer says that if implemented, big banks would likely adjust to tightening regulation. “Banks will adapt to capitals over time, but if there’s a sudden increase in capital requirements, you know, in the quarter or two or a year after, they can’t necessarily adjust to that instantly, but they will adjust,” Kotowski told CNBC. “If the capital charge on a certain kind of trading inventory is suddenly 20% more, all the market makers in that trading category are going to want to hold 20% less capital.” (Jim Cramer’s Charitable Trust is long WFC, MS. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

A sign is posted in front of a Wells Fargo Bank on April 14, 2023 in San Bruno, California.

Justin Sullivan | Getty Images

Club holdings Wells Fargo (WFC) and Morgan Stanley (MS) aced the Federal Reserve’s stress tests, showing new signs of improved resiliency and fresh hopes for the continued return of excess capital to shareholders.

Every weekday the CNBC Investing Club with Jim Cramer holds a Morning Meeting livestream at 10:20 a.m. ET. Here’s a recap of Thursday’s key moments. ‘Choppy’ market Watch WFC, MS Stick with DIS 1. ‘Choppy’ market Stocks were mixed in midmorning trading Thursday. The ongoing “choppy behavior,” as Club Director of Portfolio Analysis Jeff Marks called it, comes amid a spate of strong economic data. The U.S. economy grew at a 2% annualized rate in the first quarter of the year, well ahead of an initial estimate of 1.3%, the Commerce Department said Thursday. U.S. weekly jobless claims last week came in at 239,000, according to the Labor Department, fewer than Wall Street’s expectations. The Federal Reserve indicated again this week that it’s likely to push forward with further interest-rate hikes in the coming months, potentially weighing on equities, Marks said. Treasury yields climbed higher Thursday morning, while oil prices edged up. 2. Watch WFC, MS Big U.S. banks — including Club holdings Wells Fargo (WFC) and Morgan Stanley (MS) — passed the Fed’s annual stress test Wednesday. “Wells Fargo is the big standout,” Marks said Thursday. The bank stock soared roughly 3% midmorning to nearly $42 a share. Morgan Stanley shares also saw an uptick. Marks said we’ve seen the “passing of the storm” following the regional banking crisis that began with the collapse of Silicon Valley Bank in March and weighed on most financial stocks in recent months. 3. Stick with DIS KeyBanc on Thursday downgraded Club holding Walt Disney (DIS) to sector weight, or neutral, from a buy-equivalent, while abstaining from providing a price target. The firm cited stalling direct-to-consumer subscriber growth and high expectations at Disney’s domestic parks business, while arguing that “buying the dip has been a losing trade.” We continue to back CEO Bob Iger’s turnaround plan and expect the stock price will be higher a year from now. (Jim Cramer’s Charitable Trust is long WFC, MS, DIS. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Every weekday the CNBC Investing Club with Jim Cramer holds a “Morning Meeting” livestream at 10:20 a.m. ET. Here’s a recap of Wednesday’s key moments. Powell hints at future rate increases Strong demand outweighs potential AI crackdown Look out for the Fed’s stress tests 1. Powell hints at future rate increases Stocks are mixed on Wednesday as markets digested Federal Reserve Chairman Jerome Powell’s hawkish remarks on future monetary policy. The central bank head warned of “more restrictions coming,” citing a “very strong labor market.” The Fed had delivered 10 consecutive meetings of interest rate hikes and then a pause in June with a bias for some more this year. During a monetary policy session in Portugal, Powell did acknowledge that too much tightening could lead to an economic downturn. But, he added, it’s not “the most likely case, but it’s certainly possible.” 2. Strong demand outweighs potential AI crackdown Chipmakers are the story of the day after the Wall Street Journal reported that the U.S. government may impose new restrictions on AI chip exports to China. These are largely immaterial for Club holdings like Nvidia (NVDA), whose shares are down only slightly on the news. The Club’s view is that Nvidia has so much demand outside of China that looming regulations shouldn’t disrupt its AI narrative. Check out your email inboxes and texts later Wednesday for a closer look at the new rules and their impact on fellow Club chipmaker Advanced Micro Devices (AMD) 3. Look out for the Fed’s stress tests We’ll be watching out for the release of the annual bank stress test results after the stock market closes Wednesday afternoon These tests typically measure how the largest banks may weather an extreme economic downturn, giving insight into how much capital institutions can return to their shareholders. Club holdings’ Wells Fargo (WFC) and Morgan Stanley (MS) should be well capitalized. (Jim Cramer’s Charitable Trust is long NVDA, AMD, WFC, MS. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Every weekday the CNBC Investing Club with Jim Cramer holds a “Morning Meeting” livestream at 10:20 a.m. ET. Here’s a recap of Monday’s key moments. Equities down, as energy outperforms Stick with Palo Alto Networks Watch Wells Fargo 1. Equities down, as energy outperforms Stocks edged down in midmorning trading Monday, as Wall Street entered the final trading week of the first half of 2023. The S & P 500 was down 0.13%, even as energy — the index’s biggest loser year-to-date — was outperforming. The Club’s three oil-and-gas firms — Pioneer Natural Resources (PXD), Coterra Energy (CTRA) and Halliburton (HAL) — were solidly in the green Monday. The health-care sector, meanwhile, was pulled down by a more-than-5% decline in Pfizer (PFE) stock after the pharmaceuticals giant pulled the plug on a weight-loss pill trial amid safety concerns. 2. Stick with Palo Alto Networks Palo Alto Networks (PANW) is well on its way to becoming the first cybersecurity company to reach a $100 billion market capitalization, Morgan Stanley said Monday. Analysts at the firm designated the stock their top cybersecurity pick, and hiked their 12-month price target by 18%, to $302 per share. Jeff Marks, the Club’s director of portfolio analysis, said Monday that investors should be patient with Palo Alto shares as the stock hit a fresh all-time high Monday, climbing to around $247 apiece. “This would certainly be a name to turn to” if it were to pull back, he said. 3. Watch Wells Fargo Wells Fargo (WFC) will be in the spotlight after Wednesday’s close when the Federal Reserve releases the results of its annual bank stress tests. It’s been tough to own bank stocks this year, Marks noted Monday, following the regional banking crisis that started with the collapse of Silicon Valley Bank in March. But the stress tests are one of three important events the sector needs to get through, he explained. The other two are second-quarter earnings, which Wells Fargo is set to report before the bell July 14, and special fees the Federal Deposit Insurance Corporation plans to implement to help replenish its deposit insurance fund. Wells Fargo stock was up slightly Monday morning, trading around $40.60 a share. (Jim Cramer’s Charitable Trust is long PANW and WFC. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Not a great setup. There are too many articles and postings about how we are overdoing artificial intelligence, and how there’s not enough substance to justify recent market moves. There’s no question that the market, particularly the Nasdaq , has rallied endlessly on what amounts to the same information: Nvidia (NVDA) makes great cards; Adobe ‘s (ADBE) putting them to use; so is Meta Platforms (META) but we don’t know how; as are Microsoft (MSFT), Alphabet ‘s (GOOGL) Google and, most importantly, Oracle (ORCL); but don’t forget Broadcom (AVGO) and Marvell (MVRL). That’s worrisome, indeed. That’s why I am approaching this shortened week with a little trepidation There’s really nothing new that I can see short of analyst meetings from Samsara (IOT) and MongoDB (MDB), both loved, but both a little abstruse. They can’t move the needle. So, it seems to me this is the test week. Research right now is of no hope whatsoever. If a stock is up, we get price target boosts. If it is down, we get cuts. Nothing original, nothing against the grain. That’s been a major source of sustenance for a while now, but I think that we have had enough of it so perhaps that causes a pause. No matter, I think we get a pause, and we still don’t have a replacement for the AI theme. Do we go health care following President Joe Biden’s first campaign rally? Getting tougher. Financials ahead of the Federal Deposit Insurance Corporation penalties? Possibly, and a bunch of regional banks seem interesting. Have you seen that yield and price-to-earnings multiple on Truist, a truly good regional bank? The consumer-packaged-goods segment has been written off as past tense : Campbell ‘s (CPB) last quarter may be the template. Retail’s tough as nails: only Walmart (WMT) and Costco (COST) seem to pass muster. Transports? You are on your own because I think the Street is anxious to end the spell of revenge travel. How many times can you re-recommend the cruise ships? The industrials have been going up on the same thing for weeks now – a prospective Chinese stimulus plan that has not yet arrived and, perhaps, the Democrats’ infrastructure plan. I am not going to hide in oil and gas because I will be discovered in plain sight. Of course, there’s some hyperbole here, and heaven knows I am given to it. Still, I am worried about this week because for the first time in a bit I think we need to do some serious digesting. No, I just feel we have come to the point where I have more ideas to sell than buy. When I scan the market, I see many charts that are extended where, even though I like them, I wouldn’t be comfortable buying them. I am mindful that a stock like that of Adobe had a huge move into an excellent quarter and then raced up the hill even more on the numbers, supercharged by AI. That in itself is pretty amazing. But then, out of nowhere, sellers emerged and reversed much of the move. There’s some real fluff in the tape. I see fluff in a lot of places, maybe all but in the pathetic oils which seem to need a re-fill of the Strategic Petroleum Reserve pronto. At times like these, what I like to do is reflect on what it would take to put new money to work. We know now that we got no interest-rate hike from the Federal Reserve last week because the central bank seemingly didn’t know what to do – too many disparate folks trying to hammer out something they couldn’t, so why not postpone? But as I have been saying, we can’t seem to get unemployment up and wage growth down. The Fed knows you can’t get the stickiest part of inflation – rentals – down without more layoffs. We have them in tech and now finance, but not enough to make people abandon their homes or move back with their folks. That’s why I think they are really playing for time. They need more homes built, and they need the homebuilders to lose their discipline. To that I say, good luck. But what matters is that I feel we are fresh out of catalysts to go higher and that most stocks just don’t seem to be at levels that make sense to purchase. Why not just wait? That’s a tough one for most of us. We will want to jump at the first sign of a price break for fear of missing out. Yet, that, again, is worrisome. We don’t want to fear missing out. We want to buy things we want at our prices or else. Are these the prices we want for Microsoft? For Nvidia? So, let’s wait and see. I am willing to miss a percentage or two, maybe even three, to see if we can’t get a better basis on our stocks if we want to buy some. Given the market is officially overbought, I think I will wait until we have a couple of days down before it’s worth pulling the trigger. (Jim Cramer’s Charitable Trust is long NVDA, META, MSFT, GOOGL, COST. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Jim Cramer on Squawk on the Street, June 30, 2022.

Virginia Sherwood | CNBC

Not a great setup. There are too many articles and postings about how we are overdoing artificial intelligence, and how there’s not enough substance to justify recent market moves.

There’s no question that the market, particularly the Nasdaq, has rallied endlessly on what amounts to the same information: Nvidia (NVDA) makes great cards; Adobe‘s (ADBE) putting them to use; so is Meta Platforms (META) but we don’t know how; as are Microsoft (MSFT), Alphabet‘s (GOOGL) Google and, most importantly, Oracle (ORCL); but don’t forget Broadcom (AVGO) and Marvell (MVRL).

CNBC’s Jim Cramer on Friday said he feels the Federal Reserve needs to be transparent with its plans, especially in the wake of restaurant chain Cava‘s highly successful IPO, which he believes is a sign the market is heating up.

Cramer thinks a prosperous IPO market could lead to an influx of money on Wall Street and a hiring frenzy, the last thing the Fed wants when it’s trying to cool off the economy.

“The Fed needs to stop being so broad and opaque; what we need from them is narrow transparency,” he said. “Otherwise, the animal spirits will kick in again and companies will start going on a hiring binge, which is the last thing the Fed wants.”

He acknowledges that some may argue the economy is cooling on its own. Grocery giant Kroger just reported food costs coming down across the board, and Cramer said he is seeing figures that suggest used car and clothing costs are also declining.

However, according to Cramer, there is one major issue: housing. Cramer believes the Fed must provide a game plan of how it plans to bring the housing market down. He said he thinks the Fed’s ultimate plan is to increase unemployment so many young people move in with their parents, as is historically the case when unemployment is rampant.

But he called this plan “convoluted and, frankly, heartless,” and even though the central bank does not control long-term interest rates, he thinks there is another way to bring housing prices down.

“To me, the best thing the Fed can do is to figure out, maybe, a strategy where there’s more homebuilding and more apartment building. The only way to do that, though, is to stop scaring people who work, stop scaring the builders,” he said. “We’ve got a massive shortage of homes in this country, but who the heck would ever build more if they think the Fed wants to crush the whole economy once those homes and apartments are up?”

Jim Cramer’s Guide to Investing

Click here to downloadJim Cramer’s Guide to Investing at no cost to help you build long-term wealth and invest smarter.

Every weekday the CNBC Investing Club with Jim Cramer holds a “Morning Meeting” livestream at 10:20 a.m. ET. Here’s a recap of Tuesday’s key moments. ‘Don’t like the tape’ Stick with Apple Stay bullish on Wells Fargo 1. ‘Don’t like the tape’ U.S. stocks rose Tuesday, with the rate of inflation slowing to its lowest annual rate in more than two years in May, according to the Labor Department’s monthly consumer price index . The report bolstered investor hopes that the Federal Reserve would skip an interest-rate hike at its two-day policy meeting, which gets underway Tuesday. However, Jim Cramer urged caution. “I don’t like the tape here,” he said, noting some stocks seem to be on a one-way march higher, including Oracle (ORCL) and Adobe (ADBE). “Stop buying things that are up over-and-over again because of the same research,” he said. 2. Stick with Apple Speaking of research, Jim said he’s not a fan of the Apple (AAPL) downgrade at UBS, which on Monday night took its rating on the iPhone maker’s stock to neutral from buy. The firm bumped its price target on Apple shares to $190 each, from $180, implying 3.4% upside from the stock’s Monday close. UBS expressed concerns about slowing revenue growth in Apple’s key services segment, citing its analysis of App Store spending through May. The firm also said its surveys suggest demand for new iPhones in developed markets, including the U.S., has softened over the past six months. Jim said he believes Apple’s services revenue has actually accelerated and emphasized that iPhone demand in emerging markets, such as India, remains key to the Apple’s next chapter. Apple remains a stock that investors should own for the long term. 3. Stay bullish on Wells Fargo Wells Fargo (WFC) shares still look attractively valued, Jim said, despite their more-than-2% pop Tuesday. The stock is trading at less than 9-times forward earnings, compared with its five-year average of 11.4, according to FactSet. “People are choosing the bullish side of Wells, not the bearish side,” Jim said, contending that Wells Fargo CEO Charlie Scharf still has more opportunities to reduce expenses. Speaking at a conference earlier Tuesday, Wells Fargo CFO Mike Santomassimo said the bank expects upside to it outlook for net interest income. In April, Wells Fargo guided for net interest income to increase 10% in 2023. (Jim Cramer’s Charitable Trust is long AAPL and WFC. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Every weekday the CNBC Investing Club with Jim Cramer holds a “Morning Meeting” livestream at 10:20 a.m. ET. Here’s a recap of Tuesday’s key moments. Stocks climb MS is a buy Disney+ partners with Apple 1. Stocks climb Equities edged up Tuesday morning following a small selloff Monday, with bank stocks and Big Tech showing strength. But the market still remains largely range-bound ahead the Federal Reserve’s meeting next week, with investors closely watching whether the central bank will pause its interest-rate hikes in a likely catalyst for stocks. Treasury yields rose slightly, while oil prices retreated. Meanwhile, Goldman Sachs lowered its odds of a U.S. recession in the next 12 months to 25%, from 35%, following Washington’s debt-ceiling agreement last week and the stabilization in regional banks. 2. Morgan Stanley is a buy The stock market has misjudged Morgan Stanley (MS) amid the recent turmoil in the banking sector. The firm, which has spent years bolstering its wealth-and-asset-management business, “has the best model, and it is being treated very subpar,” Jim Cramer said Tuesday, alluding to the stock’s more-than-13% decline over the past three months. “I think members should be buying this stock, and buying it aggressively,” he added. That’s a view we alluded to in a commentary Monday, writing that we’d be more apt to view the latest rumblings about a possible boost to bank capital requirements through a buyer’s lens when it comes Morgan Stanley and Wells Fargo (WFC), our other Club financial stock. 3. Disney+ partners with Apple Jim said Club holding Walt Disney ‘s (DIS) decision to bring its flagship streaming service Disney+ to Apple ‘s (AAPL) Vision Pro headset is not a reason to buy Disney stock here. However, he suggested the partnership might be a reason for investors to stop selling Disney shares, which have fallen roughly 11% over the past month. “I was surprised to see [Disney CEO] Bob Iger at the Apple presentation because [he] has done a poor job. They’ve not been able to figure out how to get their costs down…maybe this is a sign of life for Disney,” Jim said. Meanwhile, here’s our take on Club holding Apple’s new product launch. (Jim Cramer’s Charitable Trust is long MS, WFC, DIS, AAPL. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

We’re more apt to view the latest rumblings about a possible boost to bank capital requirements through a buyer’s lens when it comes to our Club financials Morgan Stanley (MS) and Wells Fargo (WFC). The Wall Street Journal reported Monday that financial industry regulators could announce a proposal, as early as this month, seeking to increase the rainy-day funds of big banks. Ever since Silicon Valley Bank failed in March, followed closely by two others, it’s seemed likely that U.S. regulators would want banks to be better prepared to weather future crises. Morgan Stanley and Wells Fargo, while never a worry during the recent mini-banking crisis, have both seen their stocks decline in the wake of the SVB collapse and struggle to regain their footing. In our view, the substance of the Journal report was largely expected and bank stocks have already reflected the potential for increased regulatory scrutiny dating back to the first bank blowup. According to the Journal’s reporting, the changes could amount to as much as a 20% increase in overall capital requirements at large U.S. banks, which must maintain a certain buffer against their risk-weighted assets in order to protect the clients (and the business) in the event of losses. One popular metric used to measure this, which we highlight with every bank earnings report, is the Common Equity Tier 1 ratio, or CET1 for short. The Journal also indicates that regulators will look to take into account the bank’s business activities, in particular, fee-generating activities — impacting a name like Morgan Stanley which generates large fees from its wealth management business. Critics of the potential regulatory update don’t believe that a fee-based approach is the right move, arguing it would penalize banks for something that isn’t always an operational risk. As members know, we like fee-based revenues because they tend to be less volatile than non-fee-based sources, which are largely reliant on interest rates. Should Morgan Stanley really be penalized more than others just because it offers fee-based wealth management solutions, which through strong execution have grown? Details on the possible regulator proposal are limited at the moment. However, we’re inclined to consider a capital requirement change opportunistically, especially as it relates to Morgan Stanley. At a higher level, the WSJ news, along with certain agreements made to get the U.S. debt ceiling raised — such as the resumption of student loan repayments and work requirements around the Supplemental Nutrition Assistance Program (SNAP), also known as food stamps, supports the view that Federal Reserve should forgo another interest rate hike at its June meeting next week. According to the CME FedWatch tool as of Monday afternoon, the market is putting nearly 80% odds on such an outcome. A “hawkish pause” is what some are calling it — a scenario in which the Fed would refrain from its 11th straight rate hike in as many meetings to allow more economic data to roll in and to gauge the impact of the direct monetary tightening already done. But the other part of the “hawkish pause” would be for the Fed to reiterate that it remains data-dependent and that rate increases could resume if necessary. The market, at the moment, is viewing the possibility of a rate cut before the end of the year as less and less likely. (Jim Cramer’s Charitable Trust is long MS, WFC. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Bing Guan | Bloomberg | Getty Images

We’re more apt to view the latest rumblings about a possible boost to bank capital requirements through a buyer’s lens when it comes to our Club financials Morgan Stanley (MS) and Wells Fargo (WFC).

What the heck really did happen on Friday, when the Dow jumped 700 points on a strong jobs reading ? Why such a viscerally positive reaction to an employment number that was hotter than expected? Was it because wages didn’t spike? Was it all that perfect — a Goldilocks report? Here’s my take on Friday’s rally. Going into the debt ceiling crisis, there was a belief that House Speaker Kevin McCarthy couldn’t control his own Republican party. Senate Majority Leader Charles Schumer wasn’t much better off with the Democrats. Both had lost control of their parties to the extremists. That meant the United States would default on its debt. It seemed pretty logical. I truly believe the extremists never believed a default would mean more than a few weeks of setbacks and more brinkmanship. Who can blame them? President Joe Biden lamely floated that he could invoke the 14th Amendment to avoid this and any future debt limit fights; the amendment includes a clause that some legal scholars say overrides the statutory borrowing limit set by Congress. No matter what, it was pretty clear that chaos was our destiny. But when McCarthy and Biden agreed to temporarily suspend the debt ceiling and cap some federal spending in order to prevent a default, we got a deal that was even less contentious than the 2011 bargain . (The coming together brought to mind the legendary coalition of President Ronald Reagan and House Speaker Tip O’Neil in the 1980s, memorialized in Chris Matthews’ “Tip and the Gipper: When Politics Worked.”) It was the compromise debt limit deal — not the employment number — that caused the market to rally. Sure, the jobs report showed wage inflation was cooling, which is good news in the Federal Reserve’s fight against inflation. But the job creation in May and the revisions were insanely strong. What matters most is that Fed Chair Jerome Powell, who is far more powerful than the independents on the Fed’s board who have such a hard time keeping their mouths shut, is reasonable. He seems to understand that it’s time to wait a bit on any more rate hikes. Not because he thinks things are cooler, but because he actually doesn’t even know. We have a young workforce coming into the market akin to when I got out of school in 1977 — nary a job to be had anywhere. This is potentially a monumental moment. The new debt limit legislation sets the date for resuming federal student loan repayments, which have been on hold since March 2020. We have the end of Supplemental Nutrition Assistance Program (SNAP) benefits and other pandemic breaks. Why not wait two months to see if unemployment naturally goes up and wages come down? To sum things up: We came into Friday shocked that there was a shocker of a deal and a not-red-hot employment number (at least one that didn’t send rates higher). This is what triggered the long-awaited buying of stocks outside of the Magnificent Seven that have led the market all year: Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), Tesla (TSLA), Meta Platforms (META), Apple (AAPL), and Nvidia , which briefly joined the $1 trillion valuation club. We each have our own way of monitoring these things. I used Club name Caterpillar (CAT) as my judge. On Thursday afternoon, CEO Jim Umpleby went into the lion’s den of Sanford Bernstein and told a tale about de-cyclization. Shares of the heavy equipment maker had a tiny snap back. One day later and armed with the budget deal and the employment number, CAT shot up seventeen points — an unheard-of short squeeze. This took the stock back to when it reported a good number that was converted into a bad number by bearish analysts still unwilling to admit that the company had changed its bi-polar ways. Of course, the bears would say that it only went up because of one more silly stimulus by China, this time to adjust rents. I say Caterpillar went up because it was overly shorted, like so much of the market, including retail, health care, financials, other industrials including the commodities (the oils!). We even saw the imperfect chipmakers and heavily challenged enterprise software stocks come alive. The shorts were correct to press their bets if there was no debt deal and we got an employment number that was a steamer. But they were wrong on both counts. This plus a rare wave of new money coming in and massive buybacks by companies capable of plundering after their reports, caused the broadening that had been bemoaned as non-existent as recently as the day before. You could argue it was a short squeeze of monumental proportions. A short squeeze happens when short sellers having to buy stocks to cover their short positions, pushing prices higher. But every time there has been a broadening since FANG, it’s always been called a short squeeze. That’s just how things work, although it’s never been acknowledged by anybody. Which brings us up to date for Monday. We have a blackout of the Fed speakers. We have no real macroeconomic data. We have no landmines of earnings. And no Fed meeting until mid-June. A true interregnum. We are going to have to take more things off the table if we get a rally into an overbought setting. Yes, we have some real stinkers — Disney (DIS), Foot Locker (FL), Emerson Electric (EMR), Estee Lauder (EL) — and we can battle them. But the important thing is that we have so many winners that we have to ring the register on some stocks if all goes our way. Of course I obsess on the losers. I didn’t think that Fabrizio Freda at Estee Lauder and Mary Dillon at Foot Locker could both blow it that badly. I had reason to dislike the Emerson team, but it still gave me more than I can handle. I have no idea how Disney’s stock could be this weak in a long-on-money-short-on-time moment. I am furious at myself for not seeing around any of these corners. But I am not going to throw good money after bad and I see no good on these names — yet. This leaves us with the big question: Which winners to trim? As long as we are not subsidizing losers, we aren’t breaking protocol. But we have two tasks. One is to come up with a new name that hasn’t moved that we actually like. And two is to trim into strength as we get overbought. I want both resolved by our next Club meeting on June 14. That’s what I am working on right now. Do we need so much Salesforce (CRM), even as it reported a good quarter all things considering? Do we even need Advanced Micro Devices (AMD) when it has nothing to rival Nvidia? I just don’t know. I want the market to tell me what to do. I think it will. Where does this leave us? In a sanguine week that will allow us to see if the short squeeze continues. If it does and continues to broaden, we can both peel some winners. See which caterpillars can develop into, well, Caterpillars. Maybe add Take-Two (TTWO), which gave us a two-year outlook, possibly aided by a new Grand Theft Auto game and better Nvidia cards. Just one of many ideas. But one Jeff Marks and I are trying to get our arms around. Some who read might ask: “Shouldn’t there be more of a thesis behind a bullish move?” I say no, no more than you needed in 2011, when the debt ceiling deal led to a fantastic rally because Armageddon was avoided. We cannot sit back and relax. But what we can do is accept that it is a better moment than we thought not that long ago. There are cracks. The Dollar General (DG) call was a compendium of weakness for the lower middle class and the Macy’s (M) call was a confusion of negativity. But who is to say that these companies just don’t have the “it” of Five Below (FIVE) or Lululemon (LULU). We are close enough to the infrastructure money wave to handle another rate hike if we need it. But Powell recognizes the futility of another rate hike right now because it lowers mortgage rates, making his job even harder. What we can do is watch and wait as battlegrounds get resolved — like CAT did on Friday. We can anticipate better things from a Johnson & Johnson (JNJ) — especially with a 3M (MMM) deal — and from GE Healthcare (GEHC). We can lick our Estee and Foot Locker wounds. And we can be glad that we got through the debt deal and wax in the wave of new money that will at last be coming in. No, we can’t be complacent. Too many needs for the shorts to save themselves. They have been run over in so many places that they have to make a comeback somewhere. Their number didn’t get so strong before the debt ceiling deal that they can’t all cover at once. Nevertheless, we have enough money to put to work if we want to in a new name that hasn’t moved and has a special situation thesis. But I do not want to be so relieved as to think there is no woods, just that we are out of it for now. Personally, the last few weeks have been hard ones, ameliorated by members who have made money with the club. Some mistakenly believe that we missed this entirely rally. It galls me because I gave up being a hedge fund manager years ago and I know the truth: This may be the best we’ve ever been, and this time it is for you, not the entitled class. I thank you all for letting us have the floor to help and not be tools of the traders who have infiltrated our ranks. So let’s take and make some gains and be ready for the next storm after the calm, wherever it might be coming from. Rest up. We have gotten past the systemic chaos into business as usual, where we can glow in a world where stock picking matters. (See here for a full list of the stocks in Jim Cramer’s Charitable Trust.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

US President Joe Biden, accompanied by Speaker of the House Kevin McCarthy, Republican of California, arrives for the annual Friends of Ireland luncheon on St. Patrick’s Day at the US Capitol in Washington, DC, on March 17, 2023.

Saul Loeb | AFP | Getty Images

What the heck really did happen on Friday, when the Dow jumped 700 points on a strong jobs reading? Why such a viscerally positive reaction to an employment number that was hotter than expected? Was it because wages didn’t spike? Was it all that perfect — a Goldilocks report?

Here’s my take on Friday’s rally. Going into the debt ceiling crisis, there was a belief that House Speaker Kevin McCarthy couldn’t control his own Republican party. Senate Majority Leader Charles Schumer wasn’t much better off with the Democrats. Both had lost control of their parties to the extremists. That meant the United States would default on its debt. It seemed pretty logical.

I truly believe the extremists never believed a default would mean more than a few weeks of setbacks and more brinkmanship. Who can blame them? President Joe Biden lamely floated that he could invoke the 14th Amendment to avoid this and any future debt limit fights; the amendment includes a clause that some legal scholars say overrides the statutory borrowing limit set by Congress.

No matter what, it was pretty clear that chaos was our destiny. But when McCarthy and Biden agreed to temporarily suspend the debt ceiling and cap some federal spending in order to prevent a default, we got a deal that was even less contentious than the 2011 bargain. (The coming together brought to mind the legendary coalition of President Ronald Reagan and House Speaker Tip O’Neil in the 1980s, memorialized in Chris Matthews’ “Tip and the Gipper: When Politics Worked.”)

After a sour day in Washington and on Wall Street, CNBC’s Jim Cramer warned investors that lawmakers will inevitably cost them money as debt ceiling negotiations drag on.

“Get ready for our politicians to lose you some more money,” Cramer said, referencing the earlier impasse surrounding the debt ceiling in 2011. “They hurt you then. They aren’t done hurting you now. But unless you trade full time it’s very hard to get out and get back in early enough for it to make a difference, which means most of us need to take the pain.”

related investing news

Market watchers are also weighing the news of the emergence of a new Covid-19 variant in China, he said. It’s unclear whether this new wave will prompt Beijing to impose new travel restrictions, many of which eased up several months ago.

“We don’t know if travel will be banned or restricted, although the Macau casino stocks are trading like it’s gonna happen,” Cramer said. “And we don’t know if the psyche of the recently ebullient Chinese consumer will be impacted.”

With 2011’s fitful debt ceiling negotiations ringing in his ears, Cramer is pessimistic about lawmakers’ ability to come to a deal before chaos reigns.

“Even though we ultimately got a deal [in 2011] and averted the worst-case scenario, the standoff was enough to make Standard & Poor’s downgrade our government’s credit rating,” he said.

Cramer considered the merits of selling stocks before the potential market swoon, but worried that many will not be able to buy them back fast enough to see real gains.

“I would hate to advise you to sell and then buy back later, though, because we don’t know if you’ll be able to get back in before the all-clear,” Cramer remarked. “That said, if you think our leaders are serious about making a deal, then it might be worth trying to sidestep the coming decline — and if we’re following the 2011 script, there’d be about a 12% decline from here until the bottom.”

Jim Cramer’s Guide to Investing

Click here to downloadJim Cramer’s Guide to Investing at no cost to help you build long-term wealth and invest smarter.

In what Jim Carmer called a “classic” move, Morgan Stanley’ s (MS) longtime CEO James Gorman spooked the market Friday when he said he’ll be stepping down. We’re disappointed to see him go but have full confidence in the bank going forward — and see a potential buying opportunity. During the bank’s annual meeting, Gorman said he expects to retire from his 13-year stint in the top job sometime over the next 12 months, barring a “major change” to the external environment. At that point, Gorman said he intends to continue to serve as executive chairman for a period of time. He also said Morgan Stanley’s board of directors has identified three “very strong” internal candidates to replace him and lead the bank to another decade of growth. Jim on Friday matched Gorman’s confidence in the future of Morgan Stanley, saying its stock looked very attractive at current levels. “I got in touch with James Gorman this morning … This is actually classic James. This is the way he works. It was planned. It was long term,” he said. “I think it’s a screaming buy here.” While the news was not a complete surprise to investors, it did put a timeline on Gorman’s retirement for the first time. Morgan Stanley shares fell more than 2% Friday, to around $82 apiece — extending weakness in the stock that began in March with the onset of the U.S. regional banking crisis. The day before Gorman took over as CEO, on Jan. 1, 2010, Morgan Stanley stock closed at $29.60 per share. The stock has sharply outperformed the KBW Bank Index over his tenure. MS .BKX mountain 2009-12-31 Morgan Stanley’s stock performance versus the KBW Bank Index since Dec. 31, 2009. “A management transition often creates short-term stock weakness, and we feel that may be the case this time given the importance of Gorman’s role in reshaping the firm over the past decade,” Mike Mayo, an analyst at Wells Fargo Securities, wrote in a note Friday. “However, his willingness to stay on as executive chairman should dampen negativity,” he added. Gorman took over Morgan Stanley in the shadow of the Great Recession of 2007-2009 — a period of extreme tumult for the firm and the U.S. banking sector overall — and embarked on a strategic shift toward wealth-and-asset management, away from its traditional focus on the more volatile areas of investment banking and trading. “We’ve steadily de-risked parts of the business that got us in trouble during the [global financial crisis], and we obviously made a major push in building up wealth and asset management, and it worked,” Gorman said in a CNBC interview earlier this year . Acquisitions were a big part of that push. After taking full control of wealth manager Smith Barney a decade ago , Morgan Stanley bought brokerage E-Trade and investment management firm Eaton Vance in October 2020 and March 2021, respectively. “We’re delighted with where we got to,” Gorman said during the same CNBC interview. Morgan Stanley’s investment banking and trading division accounted for two-thirds of its revenues in 2008. That figure stood at roughly 45% in 2022. Wealth management revenues grew from $7 billion in 2008 to $24.4 billion in 2022 — from about 28% of the total, to 45%. The shift in revenue composition is good for shareholders because fee-based wealth and asset management is considerably more stable. Investors like steadiness, so they’re willing to pay more for every dollar of wealth-and-asset-management revenue compared with investment banking and trading. Over time, this dynamic should allow Morgan Stanley to command a higher price-to-earnings ratio. That has been a key part of our investment thesis in Morgan Stanley, which we’ve owned for about two years, and will remain so under new leadership. According to CNBC’s Hugh Son , Morgan Stanley’s three internal CEO candidates are Ted Pick, head of Institutional Securities Group; Andy Saperstein, head of Wealth Management; and Dan Simkowitz, who leads the firm’s investment management division. (Jim Cramer’s Charitable Trust is long MS. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

James Gorman, chairman and chief executive officer of Morgan Stanley, speaks during a Bloomberg Television interview in Beijing, China, on Thursday, May 30, 2019.

Giulia Marchi | Bloomberg | Getty Images

In what Jim Carmer called a “classic” move, Morgan Stanley’s (MS) longtime CEO James Gorman spooked the market Friday when he said he’ll be stepping down. We’re disappointed to see him go but have full confidence in the bank going forward — and see a potential buying opportunity.

We’re buying 45 shares of Morgan Stanley (MS), at roughly $84.29 apiece. Following Friday’s trade, Jim Cramer’s Charitable Trust will own 1,400 shares of MS, increasing its weighting in the portfolio to 4.35% from 4.21%. With Morgan Stanley shares coming under pressure this week as a result of the ongoing crisis of confidence in regional banks, we’re stepping in to take advantage as the stock finds support below our overall cost basis. Morgan Stanley has dropped 6% since its April 28, even with Friday’s roughly 2% advance in the broader stock market rally. While the issues at regional banks are lurking as a headwind for the market and will likely keep upside in the financials sector limited in the near term, we think that Morgan Stanley comes through this period of uncertainty as an even stronger bank than it was previously. MS YTD mountain Morgan Stanley YTD performance Less than two weeks ago, Morgan Stanley reported a very strong first quarter with management calling out about $110 billion in net new assets for the quarter, about $20 billion of which the team believes resulted from regional bank outflows following the collapse of Silicon Valley Bank in March. With the regionals coming under additional pressure following the news that PacWest Bancorp (PACW) was exploring strategic options, including the possibility of a sale, we wouldn’t be surprised if the bank was seeing additional money coming in now. PacWest has been all over the map this week — down some 70% from the April 28 close to Thursday’s close of $3.17, and then up some 85% on Friday. In addition to the very real likelihood that Morgan Stanley is continuing to benefit from the decline in confidence at regional banks, we know that management is working diligently to ensure they protect the bottom line, including an announcement this week that the team is looking to eliminate about 3,000 jobs by the end of June. While we wait for the pressure in financials to abate and for investors to start differentiating the banks that are actually in trouble from those that are benefiting fundamentally but suffering as collateral damage, we are happy to stay patient and collect Morgan Stanley’s nearly 4% annual dividend while management also takes advantage of the stock decline to repurchase shares. With this trade, we are upgrading shares to a 1-rating, in line with Friday’s buy. (Jim Cramer’s Charitable Trust is long MS. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

A person walks through the Wall Street subway station near the New York Stock Exchange (NYSE) in New York on May 27, 2022.

Angela Weiss | AFP | Getty Images

We’re buying 45 shares of Morgan Stanley (MS), at roughly $84.29 apiece. Following Friday’s trade, Jim Cramer’s Charitable Trust will own 1,400 shares of MS, increasing its weighting in the portfolio to 4.35% from 4.21%.

With Morgan Stanley shares coming under pressure this week as a result of the ongoing crisis of confidence in regional banks, we’re stepping in to take advantage as the stock finds support below our overall cost basis. Morgan Stanley has dropped 6% since its April 28, even with Friday’s roughly 2% advance in the broader stock market rally.

While the issues at regional banks are lurking as a headwind for the market and will likely keep upside in the financials sector limited in the near term, we think that Morgan Stanley comes through this period of uncertainty as an even stronger bank than it was previously.

Morgan Stanley YTD performance

Less than two weeks ago, Morgan Stanley reported a very strong first quarter with management calling out about $110 billion in net new assets for the quarter, about $20 billion of which the team believes resulted from regional bank outflows following the collapse of Silicon Valley Bank in March.

With the regionals coming under additional pressure following the news that PacWest Bancorp (PACW) was exploring strategic options, including the possibility of a sale, we wouldn’t be surprised if the bank was seeing additional money coming in now. PacWest has been all over the map this week — down some 70% from the April 28 close to Thursday’s close of $3.17, and then up some 85% on Friday.

In addition to the very real likelihood that Morgan Stanley is continuing to benefit from the decline in confidence at regional banks, we know that management is working diligently to ensure they protect the bottom line, including an announcement this week that the team is looking to eliminate about 3,000 jobs by the end of June.

While we wait for the pressure in financials to abate and for investors to start differentiating the banks that are actually in trouble from those that are benefiting fundamentally but suffering as collateral damage, we are happy to stay patient and collect Morgan Stanley’s nearly 4% annual dividend while management also takes advantage of the stock decline to repurchase shares. With this trade, we are upgrading shares to a 1-rating, in line with Friday’s buy.

(Jim Cramer’s Charitable Trust is long MS. See here for a full list of the stocks.)

As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade.

THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY, TOGETHER WITH OUR DISCLAIMER. NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

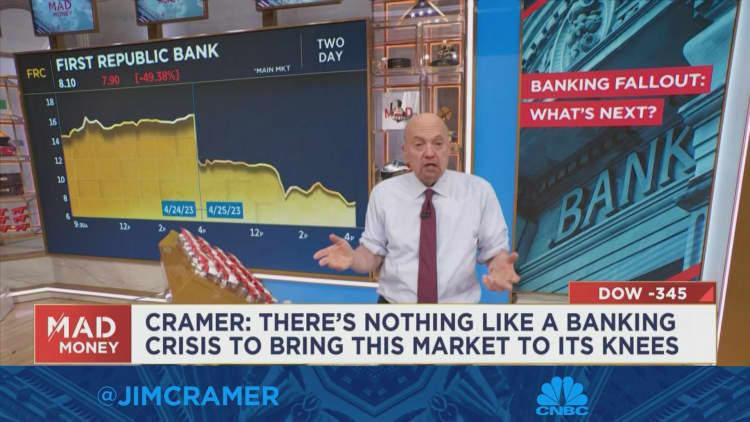

Unlike other bank failures, including Silicon Valley Bank’s recent collapse, First Republic’s troubles have largely stemmed from its inability to save itself, even with a multi-billion dollar lifeline from other major banks, he explained.

“There’s one big difference between now and 2008: This time there is no systemic contagion,” Cramer said. “It’s a miserable moment for First Republic — once a bank beloved by the rich and famous — but it’s an all-clear event for everyone else.”

Outside of First Republic, which saw its stock tumble over 49% on Tuesday, there were some other big losers on the day. UPS dropped nearly 10% on a disappointing earnings report, while life science and medical diagnostics company Danaher fell 8% and hit a 52-week low.

“While all three stocks jumped in after-hours trading, it might not matter, though, to tomorrow’s action, given the obsessive focus on this broken, darn bank,” Cramer said.

In response, a First Republic spokesperson told CNBC: “We remain fully committed to serving our communities, and we are grateful for the ongoing support of our clients and colleagues. Despite the uncertainty of the past two months, and while average account sizes have decreased, we have retained over 97% of client relationships that banked with us at the start of the first quarter.”

Jim Cramer’s Guide to Investing

Click here to downloadJim Cramer’s Guide to Investing at no cost to help you build long-term wealth and invest smarter.

Sign up now for the CNBC Investing Club to follow Jim Cramer’s every move in the market.

We just had three fantastic quarters from three disparate banks, and I didn’t read a good word about them. Think about this. JPMorgan (JPM) reported such an outstanding quarter that I had to read it twice to believe how it could possibly have been that good to rally this very big-cap stock by almost $10-per-share. Almost $10. This is not some tech stock beating faux estimates and being loved by idolatrous research analysts. This is JPMorgan, like the House of Morgan. I have not liked the stock of Citigroup (C) after it began to diverge immensely from its tangible book value (TVB). I do not understand how it could be double the price of the stock when the TVB means that if you closed the bank that’s what you would get. Hmmm, you buy Citi at $50 per share and you get almost a double if CEO Jane Fraser decides to close it? I don’t think so. Put aside that nagging oddity for a second and you have to be impressed with the quarter. I would go as far as to say that Citi seems to become just plain cheap, especially if it sells Banamex, one of Mexico’s biggest banks, for a good price. Looks like the celebration of the far-flung is, at last, joyously over. I know the stock of Wells Fargo (WFC) didn’t do much after it reported. That was just a wrong reaction. The bank, a core position of my Charitable Trust, really did beat the top and bottom line quarterly numbers handily, bought back $4 billion in stock — and yet, it added so much more capital that it has more than it did before the buyback started. It’s oozing with cash. WFC YTD mountain Wells Fargo YTD peformance More important, Wells Fargo is almost done peeling back the regulatory onion. It has had to spend fortunes in fines and technology and risk management hires that I can’t believe it had such a good efficiency ratio, a number I regard as important as all of those net interest income and margin numbers that everyone is so possessed about. Those were, of course, great, too, but that’s simply a question about how stupid the deposit base is. The dumber the base the less likely it is to leave for greener pastures. Wells Fargo’s base seems pretty dumb, but we might see dumber this week. Now, I offer the story of these banks as a preamble to what I see happening in the stock market right now. Bank stocks are notorious underperformers in the aggregate and have been labeled uninvestable by many including, at times, yours truly. That’s because they have become trading vehicles. They screw up too often. Which is why Friday was so remarkable. Bank trading is like playing Russian Roulette with three bullets. Usually, half are going to blow your head off. Instead, we went three for three. Have bank CEOs suddenly become the most brilliant CEOs in the world? No. But this is one special moment for the U.S. economy. First, you have everyone running scared, which is, by nature, good news because banks make far fewer mistakes when they run scared. And, they are making far fewer mistakes. Second, all three showed that the American consumer is still pretty flush and is not living beyond their means. There’s a little increase in bad debt, but nothing like we used to see before Covid. Maybe the aftermath of the pandemic has introduced still one more new wrinkle on the financial landscape: people want to spend but they don’t want to go broke. Third, this commercial real estate boogie man, while real, may not be real for those who know how to lend. We spill barrels of ink, or billions of characters, on how commercial real estate is the graveyard we whistle past or the most hated cliche of my era, the canary in the coal mine, and we never talk about who owns the bad loans on “Class C” and “D” buildings. I know who doesn’t: these banks. Now, I know the cynic says that the grade is in the eye of the beholder. That’s just not true, though, because what these companies do, quite cleverly, is describe where these buildings are because what seems to matter most is density. If there is a shortage of real estate then a not-so-hot piece of real estate earns a “B”, not a “C” or “D”. Yes, that’s me talking, but if you want to go over every building that has a loan that’s current and decide that it isn’t, well, don’t own any banks, period. Finally, there’s a really interesting backfire going on here with what the Federal Reverse is accomplishing, and it’s not all bad. The pandemic produced savers with miserable savings rates. Now these same savers are getting very big, safe, returns on their capital. Their frugality — except, I think we will find when they are on vacation — is matched by their better returns on their holdings. Sure, Wall Street snobs will laugh at those who have $100,000 and are now picking up a few extra percent. But these are the same jackasses who live six months and a day next to The Breakers resort in Palm Beach, Fla., where a dozen stone crabs cost $779 and they don’t mind. So, what they heck to do they know? This brings me back to the most important point of what happened Friday: Our worst fears about spiking bad loans of the auto, credit and home variety didn’t come true and therefore won’t come true this coming week. Amazingly, like the “stays-in-Vegas” cliche — what happened at a bank that loaned against pre-IPO companies while investing at a moronic part of the bond market yield curve, seems to have stayed at Silicon Valley Bank. Or, at least, it has stayed long enough that if there is another bank failure, there’s been plenty of time to come up with a plan. I don’t want to conflate a day of good bank earnings with a month of good stock prices. We are still overbought and are now getting less overbought, which is actually a time when stocks tend to go down. We also know that there are so many people who like to talk about the Fed that there will be a steady drumbeat of negativity. The Fed never inspires positivity — and if you ever say that it does, you are branded an idiot rather quickly. But if are going to name-call, I can tell you that the only thing easier to opine on without doing any homework besides politics is the Federal Reserve. Can there be any other explanation why recently you could go from a prediction of a 50-basis-point interest rate hike, to a 25-basis-point hike, to no hike, to a possible emergency cut, then back to no hike and then all the way back to a 25-basis-point hike, and still be taken seriously? Only if everyone is telling the same idiotic tale. Still, because we live and die by Fed chatter, you can’t rule out some rollercoaster action, not in the plain vanillas that define the week ahead— from the likes of Club holdings Johnson & Johnson (JNJ) on Tuesday, Morgan Stanley (MS) on Wednesday and Procter & Gamble (PG) on Friday — but in the over $500 billion club of techs that always manage to be at the forefront of stock despair. Not economic despair. Just stock despair. Bottom line Maybe that’s why nothing is grabbing us right now, nothing new, nothing exciting. It’s not like we demand lower prices, but believing that things aren’t as terrible as we thought and deciding to put money to work should not be confused. I think it’s fair to say that earnings could ratify prices not necessarily boost them, so why not wait for better prices for more committing of capital? We have made our sales. We have our cash. I am not asking for Dollar Tree pricing (the store, not the stock). But would a bit of a discount from Hermes and Vuitton be too much to ask? (See here for a full list of the stocks in Jim Cramer’s Charitable Trust.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

People walk past a Wells Fargo branch on January 10, 2023 in New York City.

Wells Fargo (WFC) reported better-than-expected first-quarter results on Friday, demonstrating its underlying fundamentals are strong. And the subsequent drop in share price is simply an opportunity for investors to buy up the stock. Total revenue advanced 17% year-on-year, to $20.73 billion, exceeding analysts’ expectations for $20.08 billion, according to estimates compiled by Refinitiv. Earnings-per-share of $1.23 came in well above the consensus estimate of $1.13 per share, Refinitiv data showed. Shares of Wells Fargo initially climbed more than 2% following the earnings release, before giving up most of those gains. Wells Fargo stock was trading down around 0.2% Friday afternoon, at $39.58 a share. Bottom line Though deposits and loans came in below expectations, those misses were more than offset by better-than-expected results on the net interest margin — which continued to benefit from higher interest rates — and return on tangible common equity and efficiency ratios. The bank’s common equity tier-1 ratio (CET1) improved on both a sequential and annual basis, supporting the repurchase of $4 billion worth of stock in the first quarter. Given the bank’s CET1 ratio remains comfortably above the regulatory minimum – and its liquidity coverage ratio is 22% above the regulatory minimum – the bank is sufficiently well-capitalized to pay out further cash returns to shareholders. Wells Fargo said it saw some benefit from deposit inflows in the wake of the collapse of Silicon Valley Bank (SVB) last month, but added that those have since abated. Wells Fargo management also noted that, like many other regional banks, it has a much broader business model and more diversified sources of funding than a bank like SVB. Meanwhile, consumer spending was strong through most of the first quarter, according to Wells Fargo management, with growth in both credit and debit usage, before softening in the latter part of the three months ended March 31. Despite an increase in provisions for credit losses, most of the bank’s business areas remain strong with little change in trends seen in the prior quarter and no meaningful update to its economic outlook. Still, management said it’s carefully monitoring any potential deterioration in asset classes or customer segments, noting that the commercial real estate market is under pressure. The bank has accordingly tightened lending standards on high-risk areas of that market. Looking ahead, Wells Fargo reiterated its guidance for net interest income (NII) and non-interest expenses for 2023 — welcomed news given the uncertainty that’s arisen in the banking sector since that guidance was first provided. That management was not forced to trim its outlook in the current environment is also a sign the guidance was conservative from the start. This quarter goes to show that the underlying fundamentals of Wells Fargo are strong, and only getting better as management continues to execute on cost-saving initiatives and works to resolve outstanding regulatory challenges. Ultimately, we find the stock decline on this report to be unwarranted and believe it represents a buying opportunity. Segment details Consumer banking and lending Consumer and small business banking (CSBB) revenue increased 28% year-over-year, as higher rates were only partially offset by lower deposits. Within consumer lending, home lending was down 42% from last year, while credit card revenue increased 3% annually. Auto loan revenue was down 12% year-over-year and personal lending increased 9% from last year. Commercial banking Middle market banking revenue increased 73% year-over-year, as higher interest rates and loan balances were only partially offset by lower deposits. Asset-based lending and leasing revenue was up 7% annually, as loan growth was partially offset by lower net gains from equities. Noninterest expenses increased 14% year-over-year, primarily due to higher personnel expenses and operating costs — though, efficiency initiatives served to partially offset the increase. Corporate and investment banking Total banking revenues increased 37% year-over-year, a result of higher interest rates and lending revenue on higher loan balances. Investment banking fees were down, given lower market activity. Commercial real estate revenue increased 32% year-over-year, due to higher interest rates and loan balances. Markets revenue was up 53% year-over-year, driven by higher trading revenue across all asset classes. Non-interest expenses increased 12% annually, due to higher operating costs and personnel expenses. But, as in commercial banking, efficiency initiatives served to partially offset the increase. Wealth and investment management Net interest income jumped 31% year-over-year, due to higher interest rates. But that figure was partially offset by a decline in deposits from customers reallocating cash into higher yielding securities. Non-interest income, however, fell 11% year-over-year, a result of lower asset-based fees driven by a decline in market valuations. Non-interest expenses fell 4% annually, primarily due to lower revenue-related compensation and efficiency initiatives. 2023 outlook Wells Fargo maintained its full year 2023 forecast for NII to be roughly 10% higher in 2023 than the $45 billion seen in 2022, implying a result of roughly $49.5 billion. The bank also reiterated its non-interest expenses guidance for 2023, at about $50.2 billion. That represents a roughly $100 million decrease on 2022 expenses (excluding the impact of $7 billion in operating losses in 2022 and an expectation for $1.3 billion in “ongoing business-related operating losses in 2023”). It remains a welcomed target, given many competitors’ plans for higher expenses in 2023. (Jim Cramer’s Charitable Trust is long WFC. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Smith Collection/Gado | Archive Photos | Getty Images

Wells Fargo (WFC) reported better-than-expected first-quarter results on Friday, demonstrating its underlying fundamentals are strong. And the subsequent drop in share price is simply an opportunity for investors to buy up the stock.