[ad_1]

Watch CBS News

Be the first to know

Get browser notifications for breaking news, live events, and exclusive reporting.

[ad_2]

[ad_1]

Watch CBS News

Be the first to know

Get browser notifications for breaking news, live events, and exclusive reporting.

[ad_2]

[ad_1]

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

We want to zoom out and revisit the broader macroeconomic picture and analyze some of the latest data that came out this week, which will heavily influence the market direction over the next few months.

After Jerome Powell’s Brooking Institution speech, it’s clear that markets are chomping at the bit to move higher with any possible Federal Reserve narrative and pivot scenario. There’s over hedging, short squeezes, options market dynamics and forced buying. This is beyond our expertise to say exactly why markets are exploding with volatility on any given data point or new Powell speech. However, these types of events and market movements have nearly always been a sign of unhealthy and heightened volatile swings in bear markets. Despite more talk from Powell with nothing new really said, markets perceived the speech as more “dovish” with his commentary around the concern of overdoing rate hikes. Yet, if this is another bear market rally taking shape for the major indices, we seem to be close to that rally turning over yet again.

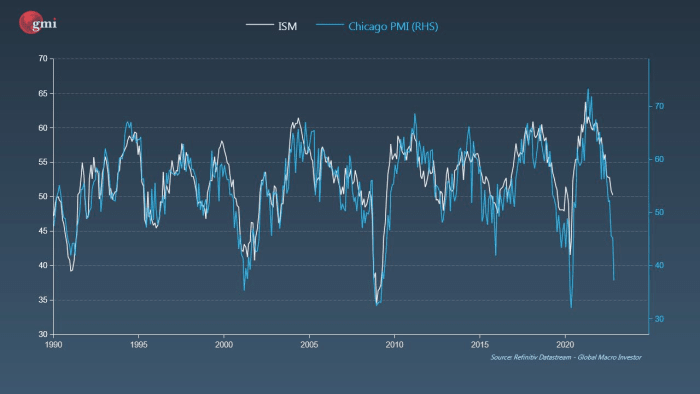

What is also concerning and expected to continue, is the trend of economic contraction as told by the data from the ISM manufacturing index (PMI). Today’s latest release shows a print of 49.0 below market expectations of 49.7. New orders are contracting, the backlog of orders are contracting and prices are decreasing. By all measures and survey responses, these are the signs of demand softening, conditions worsening and the economy moving into more cautious territory. The ISM PMI data highly correlates to the less impactful Chicago PMI data which just printed contraction lows similar to 2000, 2008 and 2020. This is the sign of an economic recession starting in the manufacturing sector.

Source: GMI, Julien Bittel

What does economic contraction mean for financial markets? It’s typically bad news when there’s a sustained contraction trend of ISM PMI below 50 and even below 40s playing out. It seems we’re in the early stages of a larger contraction trend playing out: The despair phase of the market.

The specific question for the bitcoin and macro relationship is now: Was this industry-leverage wipeout and capitulation event enough selling to mute the potential probability and effects of an equity bear market meltdown? Will bitcoin flatline and form a bottom if equities are to follow similar past bear market drawdown paths?

We’ve still yet to see a real blowout in stock market volatility which has always impacted bitcoin. It’s been a core part of our thesis this year that bitcoin will follow traditional equity markets to the downside.

The magnitude of the long-duration debt in real terms was, and still is, the biggest story here.

Furthermore, what does this mean going forward for asset valuations?

[ad_2]

Dylan LeClair And Sam Rule

Source link

[ad_1]

Markets were mixed on Friday after a surprisingly strong jobs report renewed worries about inflation and more rate hikes from the Federal Reserve.

The S&P 500 ended down 0.1% and the Nasdaq lost 0.2% after being down even more earlier in the day. The Dow ended slightly higher, closing up by 0.1%, at 34,429.

Stocks had been on the upswing for the last month on hopes the worst of the nation’s high inflation may have passed already. That fed expectations for the Federal Reserve to dial down the intensity of its big interest-rate hikes as it moves to slow the economy.

But Friday’s jobs report showed that wages for workers rose 5.1% last month from a year earlier, an acceleration from the 4.9% gain in October and higher than what economists had expected.

Such jumps in pay are helpful to workers struggling to keep up with soaring prices for everyday necessities. The Federal Reserve’s worry is that too-strong gains could cause inflation to become further entrenched in the economy. That’s because wages make up a big part of costs for companies in services industries, and those companies could end up raising their own prices further to cover higher wages for their employees.

“Inflation is certainly moving in the right direction,” said Adam Abbas, co-head of fixed income at Harris Associates, “but the market is still going to have to go through some calibration of the risk that we level off at 3% to 4% core inflation versus a natural, steady move down to” the 2% goal set by the Fed.

Employers also added 263,000 jobs last month, above forecasts for 200,000, while the unemployment rate held steady at 3.7%.

Fed officials have signaled that the unemployment rate needs to be at least 4% to slow inflation. It’s in the midst of raising interest rates quickly in hopes of slowing the economy just enough to undercut inflation.

Expectations are rising for what the Fed will do in 2023. Treasury yields jumped immediately after the jobs report’s release on speculation the Fed may ultimately hike rates higher than thought a few moments before.

The yield on the two-year Treasury jumped to 4.29% from 4.24% late Thursday. The 10-year yield, which helps set rates for mortgages and many other loans, rose to 3.52% from 3.51%.

“Another month with a strong jobs report and torrid wage gains is a reality check for where we stand in the inflation fight,” said Mike Loewengart, head of model portfolio construction at Morgan Stanley Global Investment Office.

Aside from the job market, the economic picture has been mixed. The nation’s manufacturing activity shrank in November for the first time in 30 months, for example, and the housing industry is struggling under the weight of much higher mortgage rates. Even though Friday’s report showed hiring was stronger than expected, it also clearly demonstrated that hiring is gradually slowing from its red-hot pace earlier in the year. November’s jobs gains matched the low seen in April 2021, which was the weakest since December 2020 when the number of jobs shrank.

Signs of weakening trade, especially for export-dependent economies in Asia, have deepened worries over slowing growth in China and its implications for the global economy.

More economists are still forecasting the U.S. economy to fall into a recession next year in large part because of higher interest rates.

“While the Fed won’t back away from” a hike of just half a percentage point “in December, they still have no clue what they’ll do in 2023,” said Brian Jacobsen, senior investment strategist at Allspring Global Investments.

[ad_2]

[ad_1]

A ‘help wanted’ sign is displayed in a window of a store in Manhattan on December 02, 2022 in New York City.

Spencer Platt | Getty Images

As far as jobs reports go, November’s wasn’t exactly what the Federal Reserve was looking for.

A higher-than-expected payrolls number and a hot wage reading that was twice what Wall Street had forecast only add to the delicate tightrope walk the Fed has to navigate.

In normal times, a strong jobs market and surging worker paychecks would be considered high-class problems. But as the central bank seeks to stem persistent and troublesome inflation, this is too much of a good thing.

“The Fed can ill afford to take its foot off the gas at this point for fear that inflation expectations will rebound higher,” wrote Jefferies chief financial economist Aneta Markowska in a post-nonfarm payrolls analysis in line with most of Wall Street Friday. “Wage growth remains consistent with inflation near 4%, and it shows how much more work the Fed still needs to do.”

Payrolls grew by 263,000 in November, well ahead of the 200,000 Dow Jones estimate. Wages rose 0.6% on the month, double the estimate, while 12-month average hourly earnings accelerated 5.1%, above the 4.6% forecast.

All of those things together add up to a prescription of more of the same for the Fed — continued interest rate hikes, even if they’re a bit smaller than the three-quarter percentage point per meeting run the central bank has been on since June.

The numbers would indicate that 3.75 percentage points worth of rate increases have so far had little impact on labor market conditions.

“We really aren’t seeing the impact of the Fed’s policy on the labor market yet, and that’s concerning if the Fed is viewing job growth as a key indicator for their efforts,” said Elizabeth Crofoot, senior economist at Lightcast, a labor market analytics firm.

Much of the Street analysis after the report was viewed through the prism of comments Fed Chairman Jerome Powell made Wednesday. The central bank chief outlined a set of criteria he was watching for clues about when inflation will come down.

Among them were supply chain issues, housing growth, and labor cost, particularly wages. He also went about setting caveats on a few issues, such as his focus on services inflation minus housing, which he thinks will pull back on its own next year.

“The labor market, which is especially important for inflation in core services ex housing, shows only tentative signs of rebalancing, and wage growth remains well above levels that would be consistent with 2 percent inflation over time,” Powell said. “Despite some promising developments, we have a long way to go in restoring price stability.”

In a speech at the Brookings Institution, he said he expected the Fed could cut the size of its rate hikes — the part that markets seemed to hear as grounds for a post-Powell rally. He added that the Fed likely would have to take rates up higher than previously thought and leave them there for an extended period, which was the part the market seemed to ignore.

“The November employment report … is precisely what Chair Powell told us earlier this week he was most worried about,” said Joseph LaVorgna, chief U.S. economist at SMBC Nikko Securities. “Wages are rising more than productivity, as labor supply continues to shrink. To restore labor demand and supply, monetary policy must become more restrictive and remain there for an extended period.”

To be sure, all is not lost.

Powell said he still sees a path to a “soft landing” for the economy. That outcome probably looks something like either no recession or just a shallow one, nevertheless accompanied by an extended period of below-trend growth and at least some upward pressure on unemployment.

Getting there, however, likely will require almost a perfect storm of circumstances: A reduction in labor demand without mass layoffs, continued easing in supply chain bottlenecks, a cessation of hostilities in Ukraine and a reversal in the upward trend of housing costs, particularly rents.

From a pure labor market perspective, that would mean an eventual downshifting to maybe 175,000 new jobs a month — the 2022 average is 392,000 — with annual wage gains in the 3.5% range.

There is some indication the labor market is cooling. The Labor Department’s household survey, which is used to calculate the unemployment rate, showed a decline of 138,000 in those saying they are working. Some economists think the household survey and the establishment survey, which counts jobs rather than workers, could converge soon and show a more muted employment picture.

“The biggest disappointment was the strong wage growth number,” Mark Zandi, chief economist at Moody’s Analytics, said in an interview. “We’ve been at 5% since the beginning of the year. We’re not going anywhere fast, and that needs to come down. That’s the thing we need to most worry about.”

Still, Zandi said he doubts Powell was too upset over Friday’s numbers.

“The inflation outlook, while very uncertain at best, has a path forward that is consistent with a Goldilocks scenario,” Zandi said. “263,000 vs 200,000 — that’s not a meaningful difference.”

[ad_2]

[ad_1]

Job growth was much better than expected in November despite the Federal Reserve’s aggressive efforts to slow the labor market and tackle inflation.

Nonfarm payrolls increased 263,000 for the month while the unemployment rate was 3.7%, the Labor Department reported Friday. Economists surveyed by Dow Jones had been looking for an increase of 200,000 on the payrolls number and 3.7% for the jobless rate.

The monthly gain was a slight decrease from October’s upwardly revised 284,000. A broader measure of unemployment that includes discouraged workers and those holding part-time jobs for economic reasons edged lower to 6.7%.

The numbers likely will do little to slow a Fed that has been raising interest rates steadily this year to bring down inflation still running near its highest level in more than 40 years. The rate increases have brought the Fed’s benchmark overnight borrowing rate to a target range of 3.75%-4%.

In another blow to the Fed’s anti-inflation efforts, average hourly earnings jumped 0.6% for the month, double the Dow Jones estimate. Wages were up 5.1% on a year-over-year basis, also well above the 4.6% expectation.

The Dow Jones Industrial Average fell more than 200 points after the report as the hot jobs data could make the Fed even more aggressive. Treasury yields jumped after the news, with the two-year note, the most sensitive to monetary policy, up more than 10 basis points to about 4.36%.

“To have 263,000 jobs added even after policy rates have been raised by some [375] basis points is no joke,” said Seema Shah, chief global strategist at Principal Asset Management. “The labor market is hot, hot, hot, heaping pressure on the Fed to continue raising policy rates.”

Leisure and hospitality led the job gains, adding 88,000 positions.

Other sector gainers included health care (45,000), government (42,000) and other services, a category that includes personal and laundry services and which showed a total gain of 24,000. Social assistance saw a rise of 23,000, which the Labor Department said brings the sector back to where it was in February 2020 before the Covid pandemic.

Construction added 20,000 positions, while information was up 19,000 and manufacturing saw a gain of 14,000.

On the downside, retail establishments reported a loss of 30,000 positions heading into what is expected to be a busy holiday shopping season. Transportation and warehousing also saw a decline, down 15,000.

The numbers come as the Fed has raised rates half a dozen times this year, including four consecutive 0.75 percentage point increases.

Despite the moves, job gains had been running strong this year if a bit lower than the rapid pace of 2021. On monthly basis, payrolls have been up an average of 392,000 against 562,000 for 2021. Demand for labor continues to outstrip supply, with about 1.7 positions open for every available worker.

“The Fed is tightening monetary policy but somebody forgot to tell the labor market,” said Fitch Ratings chief economist Brian Coulton. “The good thing about these numbers is that it shows the U.S. economy firmly got back to growth in the second half of the year. But job expansion continuing at this speed will do nothing to ease the labor supply-demand imbalance that is worrying the Fed.

Fed Chairman Jerome Powell earlier this week said the job gains are “far in excess of the pace needed to accommodate population growth over time” and said wage pressures are contributing to inflation.

“To be clear, strong wage growth is a good thing. But for wage growth to be sustainable, it needs to be consistent with 2 percent inflation,” he said during a speech Wednesday in Washington, D.C.

Markets expect the Fed to raise its benchmark interest rate by 0.5 percentage point when it meets later this month. That’s likely to be followed by a few more increases in 2023 before the central bank can pause to see how its policy moves are impacting the economy, according to current market pricing and statements from several central bank officials.

Powell has stressed the importance of getting labor force participation back to its pre-pandemic level. However, the November reports showed that participation fell one-tenth of a percentage point to 62.1%, tied for the lowest level of the year as the labor force fell by 186,000 and is now slightly below the February 2020 level.

[ad_2]

[ad_1]

Fed officials signal the pace of rate hikes may slow.

Mortgage rates fell to a two-month low this week as bond investors bet inflation will continue easing and the Federal Reserve signaled it will slow its pace of rate hikes.

The average U.S rate for a 30-year fixed mortgage dropped to 6.49% while the average rate for a 15-year fixed home loan fell to 5.76%, according to a Freddie Mac report on Thursday. Both averages retreated for the third consecutive week, according to Freddie Mac data.

“Mortgage rates continued to drop this week as optimism grows around the prospect that the Federal Reserve will slow its pace of rate hikes,” said Sam Khater, Freddie Mac’s chief economist.

Rates for home loans continued to fall as the investors who buy mortgage bonds reacted to economic data showing inflation easing from four-decade highs. When inflation is gaining, fixed-asset investors tend to demand higher yields to protect their returns, which results in higher mortgage rates.

The Fed lifted its benchmark rate six times this year to fight inflation, the most aggressive tightening campaign since the 1980s. Having the rate the Fed charges banks for overnight lending at a 15-year high doesn’t directly impact home loan rates, but it influences bond investors by signaling the direction of the economy.

Fed economists now put the risk of a recession at 50-50, according to minutes of the Nov. 1-2 meeting released last week. A “substantial majority” of voting members of the policy-setting Federal Open Market Committee support slowing down the tightening pace soon, the minutes said.

“The time for moderating the pace of rate increases may come as soon as the December meeting,” Fed Chairman Jerome Powell said on Wednesday in a speech at the Brookings Institution in Washington. “The timing of that moderation is far less significant than the questions of how much further we will need to raise rates to control inflation, and the length of time it will be necessary to hold policy at a restrictive level.”

Average rates for 30-year fixed mortgages likely will peak this quarter at 6.7% and fall to 5.2% in 2023’s fourth quarter, according to a forecast last week from the Mortgage Bankers Association.

“With signs of economic slowing both in the U.S. and globally, mortgage rates will remain volatile but are likely to continue to trend downward,” said MBA President Bob Broeksmit.

[ad_2]

Kathleen Howley, Senior Contributor

Source link

[ad_1]

The Federal Reserve will slow down the pace of interest-rate hikes, Chair Jerome Powell said on Wednesday, giving markets hope that the aggressive cycle of rate increases will ease up.

“The time for moderating the pace of rate increases may come as soon as the December meeting,” Powell said in remarks delivered at the Brookings Institution.

Stock markets surged in afternoon trading, with the S&P 500 gaining 3.1% to close at 4,080. The Dow rose 2.2%, to 34,590, while the tech-heavy Nasdaq soared 4.4%.

Powell noted that, while the central bank may ultimately raise rates to a higher level than it initially planned, it would do so in smaller increments.

“It is likely that restoring price stability will require holding (interest rates) at a restrictive level for some time,” Powell said. “History cautions strongly against prematurely loosening policy.”

Still, he sounded a note of caution.

“We don’t want to overtighten, so that’s why we are slowing down, and we are going to find our way to where the right level is,” Powell told the audience.

Powell acknowledged there has been some good news on the inflation front, with the cost of goods such as cars, furniture and appliances in retreat. He also said that rents and other housing costs — which make up about a third of the consumer price index — were likely to decline next year.

But the cost of services, which includes dining out, traveling and health care, are still rising at a fast clip and will likely be much harder to rein in, he said.

“Despite some promising developments, we have a long way to go in restoring price stability,” Powell said.

Powell emphasized that the labor market continues to be too hot for the Fed’s tastes. While job openings fell in October, there are still about 1.7 open jobs for every unemployed worker who is looking for work, signaling “a real imbalance between supply and demand” for workers.

He added that services costs are mostly pushed higher by rising wages, which have been growing at the fastest pace in four decades but are still below the rate of inflation.

The lack of workers reflects a jump in early retirements, the death of several hundred thousand working-age people from COVID-19, and a sharp decline in immigration and slower population growth, he said.

Many progressives have accused Powell of prioritizing price drops over full employment. Despite the Fed’s scrutiny of wages, there is no evidence that current inflation bout is caused by workers’ pay increases. Powell delivered a rebuke, saying that to have an economy that grows over the long term, inflation must come down.

“If you’re constantly fighting off inflation, and it goes on for five, 10 years, you can’t have full employment,” he said.

Last month’s inflation report showed that prices rose 7.7% in October from a year earlier, straining many families’ budgets but down from a 9.1% peak in June.

The Fed has lifted its key rate six times this year, to a range of 3.75% to 4%, the highest in 15 years. Those increases have sharply boosted mortgage rates, causing home sales to plunge, and it has raised costs for most other consumer and business loans.

Fed officials forecast in September that they would ultimately push their short-term rate somewhere between 4.5% to 4.75% by next year. Powell suggested Wednesday that rates will likely go higher than that. Many economists forecast the Fed’s key rate will rise to at least 5% to 5.25%.

At the Fed’s last meeting in November, it hiked rates by a hefty three-quarters of a point for the fourth straight time. Powell signaled at the time that its next increase would likely be only a half-point, still a significant step up. Typically the central bank moves interest rates in quarter-point increments.

CBS News’ Irina Ivanova contributed reporting.

[ad_2]

[ad_1]

Exhilaration is sweeping through Wall Street Thursday morning after a government report showed that U.S. inflation eased by even more than economists expected last month.

The S&P 500 jumped 156 points, or 4%, to 3,905 as of 10:31 a.m. Eastern. The Dow rose 872 points, or 3%, to 33, 385 and the tech-heavy Nasdaq surged 5.6%. Treasury yields fell dramatically as bond markets relaxed.

Even bitcoin rose, clawing back some of its steep plunge from prior days caused by the crypto industry’s latest crisis of confidence. A slowdown in inflation could mean the Federal Reserve won’t have to be so aggressive about raising interest rates. Such hikes have been the main reason for Wall Street’s troubles this year and are threatening a recession.

The yield on the 10-year Treasury, which helps set rates for mortgages and other loans, fell sharply to 3.93% from 4.10% late Wednesday.

All the moves stemmed from the consumer price index (CPI) showing that inflation slowed to 7.7% last month, from 8.2% in September. It’s the fourth straight month of moderation since inflation hit a peak of 9.1% in June, and it was an even better reading than the 8% that economists were expecting.

Inflation also slowed more than expected after ignoring the effects of food and energy prices. That’s the measure that the Fed pays closer attention to. So did inflation between September and October.

“The month-of-month rate of inflation is much more informative,” said Brian Jacobsen, senior investment strategist at Allspring Global Investments. “On that measure, inflation is still high, but not scary high.”

Slower inflation could keep the Fed off the most aggressive path in raising interest rates. It’s already raised its key lending rate to a range of 3.75% to 4%, up from close to zero in March.

While the data was an encouraging sign, analysts also cautioned against assuming that the battle against inflation is over.

“The Fed is still on track to increase the fed funds rate by 0.50% on December 14,” Jeffrey Roach, chief economist for LPL Financial, said in an email. “However, in the near term, investors should respond favorably to these encouraging moves in consumer prices.”

Mike Loewengart, head of model portfolio construction at Morgan Stanley Global Investment Office, also warns investors not to get carried away by the seemingly game-changing report.

“The Fed was adamant that it won’t hit the brakes on rate hikes until inflation slows, and while the market’s rally indicates investors may see light at the end of the tunnel, it will get one more reading before its decision next month,” he said. “Remember that even as we see a slowdown, prices remain elevated and have a long way to go before normalizing.”

Another potentially market-shaking report will also hit Wall Street Friday, when the latest reading arrives on how much inflation U.S. households see coming in future years. Fed Chair Jerome Powell has said he’s paying particularly close attention to such expectations.

One of the reasons the Fed has been so aggressive about hiking rates is because it wants avoid a debilitating cycle where expectations for high inflation push people to change their behaviors in ways that lead to even higher inflation.

Stocks have swung sharply this week, with several factors pushing the market both up and down. On one hand, investors hope Tuesday’s elections may result in a Washington where control is split between Democrats and Republicans. That could prevent the kind of sweeping economic changes that make investors nervous, but the outlook for that is still uncertain as votes are still being counted.

Huge losses in the crypto world, meanwhile, were threatening to spill over into other markets and at least dent confidence among investors. Bitcoin was sitting below $16,500 shortly before the inflation report, down from roughly $20,000 a week ago and nearly $69,000 a year ago. It quickly jumped $1,000 within a half hour before settling back around $17,400.

Much of this week’s furor for crypto has centered on one of the bigger trading exchanges, FTX, where the industry’s latest crisis of confidence caused customers to scramble to pull out their money. Sharp drops in crypto prices can trigger even steeper declines because of how much money many crypto investors have borrowed to make trades, which can amplify market moves.

Lenders are likely forcing those investors to put up more collateral, something called a margin call, and the process could take weeks to play out, according to strategists at JPMorgan. One challenge for the market is that the number of big, financially strong players that can bail out the weaker ones is shrinking, according to the strategists.

[ad_2]

[ad_1]

“Fed Watch” is a macro podcast, true to bitcoin’s rebel nature. In each episode, we question mainstream and Bitcoin narratives by examining current events in macro from across the globe, with an emphasis on central banks and currencies.

Watch This Episode On YouTube Or Rumble

Listen To The Episode Here:

In this episode, CK and I cover Jerome Powell and the FOMC policy decision in depth, analyzing statements from the Federal Reserve, Powell and other financial experts. Then we move onto charts, starting with bitcoin and the dollar, then moving on to Treasury rates. Lastly, we discuss the diesel shortage brewing on the east coast of the U.S.

CK and I agree that the level of importance of the Federal Reserve and the FOMC policy decision to the market is a sign of a very unhealthy economy, where central bank decisions are the only game in town.

The Fed raised interest rates by 75 basis points (bps) to a new Fed Funds target range of 3.75% to 4%. This was not a surprise. The market had been predicting the Fed to not pivot away from their course in this meeting, despite the global liquidity concerns appearing in the financial system.

The central bank maintained their policy trajectory, but the statement did contain some softening of their hawkish tone. The sentence that jumps out is the following:

“In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

“Cumulative” is the word people are focusing on. What does “cumulative” mean in this context?

The Fed is placing their meeting-to-meeting decisions within a broader scope of their tightening program as a whole since March 2022, as well as considering their globally important role. The reasoning Powell portrays in the press conference that followed is mixed. They want to place their decisions within a whole program, but also want to be data dependent on a meeting-to-meeting basis.

Overall, I think that their intention is to cause uncertainty. Uncertainty is key at the end of a hiking cycle. The Federal Reserve’s intention is to cause an economic slowdown to bring demand down to be in line with supply, but they can’t do that if the market is frontrunning the end of the hiking cycle.

That’s exactly what we’ve seen over the last several months. I’m sure Powell has mixed feelings about the stock market remaining resilient to their hiking, with the S&P 500 above where it was at the time of the June meeting’s hike. That was three meetings with 75 bps hikes, yesterday made it four, and yet the stock market was higher. He wants a “soft landing” — to achieve their policy goals without major damage to the economy — but at the same time their goal is to damage the economy. It’s a contradictory tightrope they are trying to walk.

The intentions of the last few hikes in the tightening program cannot be achieved if the market is frontrunning their slowdown, the pause, and then the eventual reversal. This is where the purposeful uncertainty comes in. If the Fed can send mixed messages and keep the market uncertain, the effects of their last few hikes can be more significant.

The charts on Fed Day were moving quickly. I delayed taking snapshots until 30 minutes after the Fed’s announcement, but the mixed messaging from Powell caused them to swing wildly. I won’t post them here because they are already out of date, but you can look at them on the slide deck for this episode.

The initial reaction was consistent across the board. Markets took the written statement, including the new language about cumulative effects, as a dovish pivot. Bitcoin spiked along with stocks and the dollar moved down.

However, as soon as Powell started to take questions at the press conference, and with his mixed messaging detailed above, markets reversed. Bitcoin and stocks headed down, the dollar up.

The one chart I will include on this companion post to the podcast is that of the 3-month and 10-year Treasury rates showing the most important inversion in the curve.

What you can notice on this chart is the 3-month yield going higher than the 10-year yield. Also, the 10-year yield is awfully close to being inside the Fed Funds target range.

What I’ve been saying for months is that the Fed will continue to raise rates until the market forces them to stop. That force applied by the market will show up as longer term rates simply not obeying the Fed anymore and going lower, like we can see with the 10-year yield here.

The Fed is admittedly “data dependent.” They tell us they are followers, but if you want to know where the Fed is going, all you have to do is look at the yields. If government security yields start heading down into the Fed Funds target range, by the next meeting their choices will be: raise rates again and lose confidence that they are in control of anything, or pause, or even do a “mid-cycle adjustment” and lower them. Powell has done what he calls a mid-cycle adjustment before. Back in 2019, the first rate cut in July was downplayed as just such a move. Of course, it was then followed by massive cuts in the following months.

There are other things happening in the economy than the Federal Reserve. There is concern about diesel shortages in the U.S. Reports are flying about there being only a couple weeks of diesel left in storage, and with the winter coming on, diesel and heating oil demand is set to increase.

To cover this story, I read from a great article by Tsvetana Paraskova. She covers the shortage and reasons behind it in great detail.

In short, U.S. refinery capacity is down due to some plants being switched to making biofuel and our imports from Russia are non-existent due to crazy sanctions.

On the show, we get sidetracked because I am not personally that worried about the diesel shortage. It will cause some pain, but the solution is through that pain. Higher prices will cause one of two things to occur — or both: higher prices will stimulate more production or higher prices will cause political changes to allow higher production.

There is an almost universal fear of higher prices and they are demonized as “inflation” at every turn. Of course, high prices aren’t bad if you are a producer. They aren’t bad in general, either. Prices are supposed to be neutral and give you information about the economy. The only price changes that are a net negative are those due to changes in the money supply. Since our current economic condition is not due to money printing but instead supply crises and bad government policies, the price increases are necessary to fix the problems today.

This is a guest post by Ansel Lindner. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.

[ad_2]

Ansel Lindner

Source link

[ad_1]

New York

CNN Business

—

One of the reasons for the record $1.9 billion jackpot for the Powerball drawing Monday night is something you wouldn’t expect — the recent run of steep interest rate hikes from the Federal Reserve.

That’s because the size of the advertised $1.9 billion top prize is the amount winners would get, which involves taking 30 equal payments of about $63 million spread out over the next 29 years. Those payments come from an annuity purchased by the lottery sponsors, and the payments factor in an average rate of return

But the thing is, the real prize is far more likely to be a much smaller lump sum, the “cash value” – in this case $929.1 million – that never gets any attention.

“All anyone ever talks about is the annuity prize,” said Victor Matheson, professor of economics and accounting at the College of the Holy Cross in Massachusetts. “It’s the number the lotteries market. It’s the number in the news story. But it’s the number that almost no one ever takes.”

No Powerball winner since 2014 has chosen the “larger” annuity amount over the cash prize.

The cash value is the amount the prize would actually cost the lottery, either in a lump-sum payment now, or to buy an annuity to make those 29 subsequent payments. The current environment of rising interest rates has opened the door to ever-larger annuity payments.

In the low interest rate environment of recent years, the advertised annuity price was only about 50% or 60% bigger than the cash value, or sometimes less.

The largest Powerball jackpot ever won was in January 2016 when three winners split a prize advertised at $1.586 billion. Each took their share of the cash value, which added up to $983.5 million, which was $54.4 million more than cash prize in Monday’s “record” drawing.

That advertised then-record annuity prize was 61% greater than the cash prize. This time, the estimated annuity prize is 104% greater than the cash prize. If it was the same ratio as in 2016, Monday’s annuity prize would be only $1.5 billion.

And interest rates were as low as they were in January of this year, Monday’s annuity rate would be only $130 million.

The current prize assumes a return on the cash value of about 5.75% a year, Matheson said.

But even a conservative investor in stocks could likely do better by taking the money up front and investing it, not withstanding the swings in the stock market. The Standard & Poor’s 500 has risen 728% in the 29 years since October 1993, or a compounded annual average growth rate of about 7.5%.

The larger assumed return associated with Monday’s annuity prize might make it more attractive to the next big winner or winners, said Matheson.

Then again, a disinclination to accept deferred gratification could overcome any investment assumptions or tax planning that goes into the winner’s calculations.

[ad_2]

[ad_1]

Job growth was stronger than expected in October despite Federal Reserve interest rate increases aimed at slowing what is still a strong labor market.

Nonfarm payrolls grew by 261,000 for the month while the unemployment rate moved higher to 3.7%, the Labor Department reported Friday. Those payroll numbers were better than the Dow Jones estimate for 205,000 more jobs, but worse than the 3.5% estimate for the unemployment rate.

Although the number was better than expected, it still marked the slowest pace of job gains since December 2020.

Average hourly earnings grew 4.7% from a year ago and 0.4% for the month, indicating that wage growth is still likely to serve as a price pressure as worker pay is still well short of the rate of inflation. The yearly growth met expectations while the monthly gain was slightly ahead of the 0.3% estimate.

Health care led job gains, adding 53,000 positions, while professional and technical services contributed 43,000, and manufacturing grew by 32,000.

Leisure and hospitality also posted solid growth, up 35,000 jobs, though the pace of increases has slowed considerably from the gains posted in 2021. The group, which includes hotel, restaurant and bar jobs along with related sectors, is averaging gains of 78,000 a month this year, compared with 196,000 last year.

Heading into the holiday shopping season, retail posted only a modest gain of 7,200 jobs. Wholesale trade added 15,000, while transportation and warehousing was up 8,000.

The unemployment rate rose 0.2 percentage point even though the labor force participation rate declined by one-tenth of a point to 62.2%. An alternative measure of unemployment, which includes discouraged workers and those holding part-time jobs for economic reasons, also edged higher to 6.8%.

Stock market futures rose following the nonfarm payrolls release, while Treasury yields also were higher.

September’s jobs number was revised higher, to 315,000, an increase of 52,000 from the original estimate. August’s number moved lower by 23,000 to 292,000.

The new figures come as the Fed is on a campaign to bring down inflation running at an annual rate of 8.2%, according to one government gauge. Earlier this week, the central bank approved its fourth consecutive 0.75 percentage point interest rate increase, taking benchmark borrowing rates to a range of 3.75%-4%.

Those hikes are aimed in part at cooling a labor market where there are still nearly two jobs for every available unemployed worker. Even with the reduced pace, job growth has been well ahead of its pre-pandemic level, in which monthly payroll growth averaged 164,000 in 2019.

But Tom Porcelli, chief U.S. economist at RBC Capital Markets, said the broader picture is of a slowly deteriorating labor market.

“This thing doesn’t fall of a cliff. It’s a grind into a slower backdrop,” he said. “It works this way every time. So the fact that people want to hang their hat on this lagging indicator to determine where we are going is sort of laughable.”

Indeed, there have been signs of cracks lately.

Amazon on Thursday said it is pausing hiring for roles in its corporate workforce, an announcement that came after the online retail behemoth said it was halting new hires for its corporate retail jobs.

Also, Apple said it will be freezing new hires except for research and development. Ride-hailing company Lyft reported it will be slicing 13% of its workforce, while online payments company Stripe said it is cutting 14% of its workers.

Fed Chairman Jerome Powell on Wednesday characterized the labor market as “overheated” and said the current pace of wage gains is “well above” what would be consistent with the central bank’s 2% inflation target.

“Demand is still strong,” said Amy Glaser, senior vice president of business operations at Adecco, a staffing and recruiting firm. “Everyone is anticipating at some point that we’ll start to see a shift in demand. But so far we’re continuing to see the labor market defying the law of supply and demand.”

Glaser said demand is especially strong in warehousing, retail and hospitality, the sector hardest hit by the Covid pandemic.

This is breaking news. Please check back here for updates.

[ad_2]

[ad_1]

A version of this story first appeared in CNN Business’ Before the Bell newsletter. Not a subscriber? You can sign up right here. You can listen to an audio version of the newsletter by clicking the same link.

New York

CNN Business

—

What will the Federal Reserve do at its meeting in December? Analysts can speculate all they want, but Fed officials say they will be using hard economic data to make their next decision.

That means key housing, labor, and inflation reports will likely have outsized effects on the market as investors speculate about what they might mean for the future of interest rates.

What’s happening: No one can move markets like Federal Reserve Chair Jerome Powell — with just a few words on Wednesday he crushed investors’ hopes of an interest rate pivot and sent stocks plunging. “We have a ways to go,” said Powell of the Fed’s current hiking regime meant to fight persistent inflation. “It’s very premature, in my view, to think about or be talking about pausing.”

But Powell did add an important caveat. The Fed could start to slow the pace of those painful hikes as soon as December. “Our decisions will depend on the totality of incoming data and their implications for the outlook for economic activity and inflation,” Powell said on Wednesday.

So what will the Fed be looking at between today and its next policy decision on December 14?

The labor market: The Fed’s biggest worry is the super-tight US labor market, and Friday’s jobs report isn’t likely to soothe any nerves.

The government report is expected to show the economy added another 200,000 positions in October — down from last month, but still a very solid number as demand for employment continues to outpace the supply of labor.

That means more inflation. Businesses have to pay higher wages to attract employees and are able to charge more for their goods and services. The Fed will be looking closely at hourly wage growth in the report. In September, wages rose by 5% from a year ago.

There is a possible upside: Another jobs report in December is expected ahead of the Fed meeting. If both reports show a downward trajectory in employment, that could be enough to placate Fed officials, even if the unemployment rate remains historically low.

Inflation data: Expect new data from two major indexes that measure the pace of inflation ahead of the next Federal Reserve meeting.

The Consumer Price Index (CPI) for October, which tracks changes in the prices of a fixed set of goods and services, is out on November 10.

Core CPI prices, which exclude oil and food, rose 0.6% in September month-over-month, matching August’s pace and coming in well above expectations of a 0.4% increase, not a great sign for the Fed. And analysts expect to see another large 0.5% increase in October.

The Fed will also get to see October data from its favored measure of inflation, Personal Consumption Expenditures (PCE), on December 1.

PCE reflects changes in the prices of goods and services purchased by consumers in the United States. The Fed believes the measure is more accurate than CPI because it accounts for a wider range of purchases from a broader range of buyers.

Core PCE climbed by 5.1% on an annual basis in September, higher than the August rate of 4.9% but below the consensus estimate of 5.2%, per Refinitiv.

Housing: The housing market has been deeply impacted by the Fed’s efforts to fight inflation, and is one of the first areas of the economy to show signs of cooling.

The 30-year fixed-rate mortgage averaged 6.95% last week, up from 3.09% just a year ago, and elevated borrowing costs are leading to a decline in demand.

“The housing market was very overheated for the couple of years after the pandemic as demand increased and rates were low,” said Powell on Wednesday. “We do understand that that’s really where a very big effect of our policies is.”

October’s new and existing home sales numbers, due on November 18 and 23, will show the continued impact of that policy ahead of the next meeting.

The US economy is still standing strong in the face of rising interest rates, but things are softening much more quickly across the pond.

The United Kingdom will face hard economic times and elevated interest rates well into next year, officials warned this week.

The Bank of England raised interest rates by three-quarters of a percentage point on Thursday, the biggest hike in 33 years, as it attempts to fight soaring inflation.

But the bank also issued a stark warning. It said that economic output is already contracting and that it expects a recession to continue through the first half of 2024 “as high energy prices and materially tighter financial conditions weigh on spending.”

A two-year recession would be longer than the one that followed the 2008 global financial crisis, though the Bank of England said that any declines in GDP heading into 2024 would likely be relatively small.

The central bank also doesn’t think inflation will start to fall back until next year. That will require more interest rate hikes in the coming months, warned policymakers.

Elon Musk has been busy over at Twitter HQ. Aside from tweeting and deleting a conspiracy theory, he’s talked about implementing some big changes at his $44 billion acquisition. Here’s what’s happened so far:

Layoffs begin: Elon Musk began laying off Twitter employees on Friday morning, according to a memo sent to staff. The email sent Thursday evening notified employees that they will receive a notice by 12 p.m. ET Friday that informs them of their employment status.

The email added that “to help ensure the safety” of employees and Twitter’s systems, the company’s offices “will be temporarily closed and all badge access will be suspended.”

Twitter had around 7,500 employees prior to Musk’s takeover.

Several Twitter employees have already filed a class action lawsuit claiming that the layoffs violate the federal Worker Adjustment and Retraining Notification Act.

The WARN Act requires any company with over 100 employees to give 60 days’ written notice if it intends to cut 50 jobs or more at a “single site of employment.”

Consolidating strength: In less than a week since Musk acquired Twitter, the company’s C-suite appears to have almost entirely cleared out, through a mix of firings and resignations.

Twitter’s board of directors was also dissolved last week, according to a securities filing.

The company filing states that all previous members of Twitter’s board, including recently ousted CEO Parag Agrawal and chairman Bret Taylor, are no longer directors “in accordance with the terms of the merger agreement.” That makes Musk, according to the filing, “the sole director of Twitter.”

Cashing blue checks’ checks: Musk on Tuesday said he planned to charge $8 a month for Twitter’s subscription service, called “Twitter Blue,” with the promise to let anyone pay to receive a coveted blue check mark to verify their account. That’s a steep haircut from his original plan to charge users $19.99 a month to get or keep a verified account.

In a tweet, the world’s richest man used an expletive to describe his assessment of “Twitter’s current lords & peasants system for who has or doesn’t have a blue checkmark.” He added: “Power to the people! Blue for $8/month.”

Advertisers hit pause: Elon Musk wrote an open letter to advertisers just hours before cementing his acquisition of Twitter, explaining that he didn’t want the platform to become a “free-for-all hellscape.” But that attempt at reassuring the advertising industry, which makes up the vast majority of Twitter’s business, doesn’t appear to be working.

General Mills

(GIS), Mondelez International

(MDLZ), Pfizer

(PFE) and Audi

(AUDVF) have reportedly joined a growing list of companies hitting pause on their Twitter advertising in the wake of Musk’s acquisition.

[ad_2]

[ad_1]

The Federal Reserve raised interest rates by three-quarters of a point in their sixth increase this year. Jerome H. Powell, the Fed chair, said “at some point” it would be appropriate to slow the pace of increases.

[ad_2]

The Associated Press

Source link

[ad_1]

Stocks fell sharply on Wall Street Wednesday after Federal Reserve Chief Jerome Powell signaled that it’s too early for the central bank to consider pausing its interest rate increases as it tries to crush the worst inflation in decades.

The S&P 500 fell 96 points, or 2.5%, closing at 3,760. It had been up by 1% earlier in the day. The Dow Jones Industrial Average shed 336 points, or 1.6%, at 32,148. The Nasdaq composite fell 3.6%. Before their brief afternoon rally, the indexes had all been in the red much of the day ahead of the Fed’s interest rate policy statement release at 2:00 p.m. Eastern.

Powell’s remarks came after the Fed announced a widely expected fourth straight extra-large rate increase of three-quarters of a percentage point. The market rallied briefly after the central bank released a statement that seemed to suggest it could ease back on the rate-increase program. That was welcome news for markets, which have been worried the recent pace of rate hikes could slow the economy so much that it goes into a recession.

But during a press conference, Powell said that to bring inflation down, the Fed will need to keep rates high enough to hurt the economy “for some time.”

“It’s very premature, in my view, to think about or to be talking about pausing our rate hikes,” Powell said. “We have a ways to go.”

Paul Ashworth of Capital Economics suggested the Fed’s latest policy statement is less dovish than it sounds, noting that Powell emphasized in his press conference that any pause in rate hikes are a long way away.

“Although market rate expectations fell in response to the release of the statement, those declines were more than reversed during Powell’s hawkish press conference, with the peak in the fed funds rate expected to be slightly above 5.0% next summer,” Ashworth said in a report.

Long-term Treasury yields jumped after a brief pullback. The yield on the two-year Treasury, which tends to track market expectations of future Fed action, rose to 4.61% from 4.55% shortly before the Fed released its statement. The yield on the 10-year Treasury, which helps set mortgage rates, climbed to 4.09% after having fallen to 3.98% earlier in the afternoon.

The Fed’s move raised its key short-term rate to a range of 3.75% to 4%, its highest level in 15 years. It was the central bank’s sixth rate hike this year, a streak that has made mortgages and other consumer and business loans increasingly expensive and heightened the risk of a recession.

The Fed’s statement said that, in coming months, it would consider the cumulative impact of its large rate hikes on the economy. It noted that its rate hikes take time to fully affect growth and inflation.

But any encouragement that gave investors faded when Powell said during a press conference that the central bank would rather make a mistake of taking interest rates too high than easing too quickly, noting that a premature pullback on rate hikes could lead inflation to become entrenched, which risks more pain for households.

“What the Fed statement giveth, the Fed chairman taketh away,” Chris Zaccarelli, chief investment officer for independent Advisor Alliance said in a note.

“The Fed statement – especially the part that referred to ‘cumulative tightening’ – made traders very excited that a step-down or pause in rate hikes was upon us, however, the press conference took that hope away once Chairman Powell spoke about how far in the future was the timeline for them to stop their rate hikes,” Zaccarelli said.

Powell said that regardless of whether the Fed dials down its interest rate hike in December, it may still end up pulling its key short-term rate ultimately to a higher level than previously thought because of data show inflation is worse than expected.

The path ahead for the Fed is closely tied to whether inflation cools from its hottest levels in four decades. Wall Street is concerned about inflation squeezing consumers and businesses while worries grow that the Fed could bring on a recession by slowing the economy too much.

“At the end of the day, the markets like certainty and they don’t have certainty from the Fed,” said Ryan Grabinski, managing director of investment strategy at Strategas, a Baird company.

Wall Street has been closely watching the latest economic data, which is heavy on the employment market this week. The job market has remained strong despite inflation, which is being taken as a sign that the Fed will have to remain aggressive in its fight against high prices.

The latest jobs data from private payroll company ADP shows that companies added positions at a greater pace than expected in October. The report follows hotter-than-expected data from the government Tuesday on job openings.

“It’s sort of confirming that the Fed still has more work to do,” Grabinski said.

Investors will get more employment data with the government’s weekly unemployment report on Thursday and a broader monthly jobs report on Friday. They have been closely watching the latest round of company earnings to get a better sense of inflation’s impact on corporate profits and outlooks. It’s been a mixed bag so far.

The 11 sectors in the S&P 500 were in the red after shedding all their gains after the brief rally following the Fed statement. Technology stocks and retailers were among the biggest weights on the index.

Drugstore operator CVS rose 3.6% after raising its profit forecast following a strong third quarter. Casino operator Caesars Entertainment rose 2.1% after beating Wall Street’s third-quarter profit and revenue forecasts.

Short-term vacation rental marketplace Airbnb fell 10.8% after warning investors that bookings growth will slow in the fourth quarter. Beauty products maker Estee Lauder slid 6.4% after slashing its profit forecast as COVID-19 lockdowns in China and inflation hurt business.

[ad_2]

[ad_1]

The Federal Open Markets Committee, the U.S. central bank’s body responsible for setting monetary policy, raised interest rates by 75 basis points on Wednesday for the fourth consecutive time as Federal Reserve governors attempt to battle stubborn inflation levels in the country.

Jerome Powell, Chairman of the Federal Reserve and the FOMC, joined a group of journalists for a press conference shortly after the data release, shedding more light on the central bank’s thoughts for future action.

Markets reacted positively to the 0.75% interest rate increase, which came in as expected, but trading became more volatile as the chairman started its speech. While the written statement announcing the interest rate decision showed a new dovish sentence, further fueling the rally, Powell’s press conference combated that feeling as the Fed Chair reiterated previous guidance.

“In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments,” the FOMC statement read, hinting at a more dovish Fed.

Powell, however, highlighted that the “ultimate level of rates will be higher than previously expected,” triggering an acute market drawdown.

The feeling markets are left with is of confirmation that a slow-down is near but surprise when it comes to the terminal funds rate, something that can be attested by the upswing and consequent downswing in the S&P 500 index.

The S&P 500 shoot up at 14:00 EST (2 p.m.) as soon as the FOMC statement was released with the more dovish language, only to come back down as Powell’s press conference began thirty minutes later. Investors likely left the livestream with a sour taste in their mouths, judging by the continued drawdowns in the index. (Chart/TradingView)

Bitcoin mirrored stock market moves, albeit falling less in percentage terms. At the time of writing, BTC is accumulating a 1% drawdown, while the S&P 500 ended the trading day bleeding by over double that amount (2.39%). The Nasdaq was seeing a similar fate, but extended its losses to 3.15%.

The fact that Bitcoin has been the least volatile of the three is quite remarkable as it defies history and mainstream media narratives altogether. While the peer-to-peer currency is still correlated with stocks, it isn’t the one doing the most severe swings, and that is going by unnoticed.

[ad_2]

Namcios

Source link

[ad_1]

The Federal Reserve on Wednesday approved a fourth consecutive three-quarter point interest rate increase and signaled a potential change in how it will approach monetary policy to bring down inflation.

In a well-telegraphed move that markets had been expecting for weeks, the central bank raised its short-term borrowing rate by 0.75 percentage point to a target range of 3.75%-4%, the highest level since January 2008.

The move continued the most aggressive pace of monetary policy tightening since the early 1980s, the last time inflation ran this high.

Along with anticipating the rate hike, markets also had been looking for language indicating that this could be the last 0.75-point, or 75 basis point, move.

The new statement hinted at that policy change, saying when determining future hikes, the Fed “will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

Economists are hoping this is the much talked about “step-down” in policy that could see a rate increase of half a point at the December meeting and then a few smaller hikes in 2023.

This week’s statement also expanded on previous language simply declaring that “ongoing increases in the target range will be appropriate.”

The new language read, “The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.”

Stocks initially rose following the announcement, but turned negative during Chairman Jerome Powell‘s news conference as the market tried to gauge whether the Fed thinks it can implement a less restrictive policy that would include a slower pace of rate hikes to achieve its inflation goals.

On balance, Powell dismissed the idea that the Fed may be pausing soon though he said he expects a discussion at the next meeting or two about slowing the pace of tightening.

He also reiterated that it may take resolve and patience to get inflation down.

“We still have some ways to go and incoming data since our last meeting suggests that the ultimate level of interest rates will be higher than previously expected,” he said.

Still, Powell repeated the idea that there may come a time to slow the pace of rate increases. He has said this at recent news conferences

“So that time is coming, and it may come as soon as the next meeting or the one after that. No decision has been made,” he said.

The chairman also expressed some pessimism about the future. He noted that he now expects the “terminal rate,” or the point when the Fed stops raising rates, to be higher than it was at the September meeting. With the higher rates also comes the prospect that the Fed will not be able to achieve the “soft landing” that Powell has spoken of in the past.

“Has it narrowed? Yes,” he said in response to a question about whether the path has narrowed to a place where the economy doesn’t enter a pronounced contraction. “Is it still possible? Yes.”

However, he said the need for still-higher rates makes the job more difficult.

“Policy needs to be more restrictive, and that narrows the path to a soft landing,” Powell said.

Along with the tweak in the statement, the Federal Open Market Committee again categorized growth in spending and production as “modest” and noted that “job gains have been robust in recent months” while inflation is “elevated.” The statement also reiterated language that the committee is “highly attentive to inflation risks.”

The rate increase comes as recent inflation readings show prices remain near 40-year highs. A historically tight jobs market in which there are nearly two openings for every unemployed worker is pushing up wages, a trend the Fed is seeking to head off as it tightens money supply.

Concerns are rising that the Fed, in its efforts to bring down the cost of living, also will pull the economy into recession. Powell has said he still sees a path to a “soft landing” in which there is not a severe contraction, but the U.S. economy this year has shown virtually no growth even as the full impact from the rate hikes has yet to kick in.

At the same time, the Fed’s preferred inflation measure showed the cost of living rose 6.2% in September from a year ago – 5.1% even excluding food and energy costs. GDP declined in both the first and second quarters, meeting a common definition of recession, though it rebounded to 2.6% in the third quarter largely because of an unusual rise in exports. At the same time, housing demand has plunged as 30-year mortgage rates have soared past 7% in recent days.

On Wall Street, markets have been rallying in anticipation that the Fed soon might start to ease back as worries grow over the longer-term impact of higher rates.

The Dow Jones Industrial Average has gained more than 13% over the past month, in part because of an earnings season that wasn’t as bad as feared but also due to growing hopes for a recalibration of Fed policy. Treasury yields also have come off their highest levels since the early days of the financial crisis, though they remain elevated. The benchmark 10-year note most recently was around 4.09%.

There is little if any expectation that the rate hikes will halt anytime soon, so the anticipation is just for a slower pace. Futures traders are pricing a near coin-flip chance of a half-point increase in December, against another three-quarter point move.

Current market pricing also indicates the fed funds rate will top out near 5% before the rate hikes cease.

The fed funds rate sets the level that banks charge each other for overnight loans, but spills over into multiple other consumer debt instruments such as adjustable-rate mortgages, auto loans and credit cards.

[ad_2]

[ad_1]

WASHINGTON (AP) — The Federal Reserve pumped up its benchmark interest rate Wednesday by three-quarters of a point for a fourth straight time but hinted that it could soon reduce the size of its rate hikes.

The Fed’s move raised its key short-term rate to a range of 3.75% to 4%, its highest level in 15 years. It was the central bank’s sixth rate hike this year — a streak that has made mortgages and other consumer and business loans increasingly expensive and heightened the risk of a recession.

But in a statement, the Fed suggested that it could soon shift to a more deliberate pace of rate increases. It said that in coming months it would consider the cumulative impact of its large rate hikes on the economy. It noted that its rate hikes take time to fully affect growth and inflation.

Those words indicated that the Fed’s policymakers may think borrowing costs are getting high enough to possibly slow the economy and reduce inflation. If so, that would suggest that they don’t need to raise rates as quickly as they have been doing.

Still, for now, the persistence of inflated prices and higher borrowing costs is pressuring American households and has undercut the ability of Democrats to campaign on the health of the job market as they try to keep control of Congress. Republican candidates have hammered Democrats on the punishing impact of inflation in the run-up to the midterm elections that will end Tuesday.

The Fed’s statement Wednesday was released after its latest policy meeting. Many economists expect Chair Jerome Powell to signal at a news conference that the Fed’s next expected rate hike in December may be only a half-point rather than three-quarters.

Typically, the Fed raises rates in quarter-point increments. But after having miscalculated in downplaying inflation last year as likely transitory, Powell has led the Fed to raise rates aggressively to try to slow borrowing and spending and ease price pressures.

Wednesday’s latest rate increase coincided with growing concerns that the Fed may tighten credit so much as to derail the economy. The government has reported that the economy grew last quarter, and employers are still hiring at a solid pace. But the housing market has cratered, and consumers are barely increasing their spending.

The average rate on a 30-year fixed mortgage, just 3.14% a year ago, surpassed 7% last week, mortgage buyer Freddie Mac reported. Sales of existing homes have dropped for eight straight months.

Blerina Uruci, an economist at T. Rowe Price, suggested that falling home sales are “the canary in the coal mine” that demonstrate that the Fed’s rate hikes are weakening a highly interest-rate sensitive sector like housing. Uruci noted, though, that the Fed’s hikes haven’t yet meaningfully slowed much of the rest of the economy, particularly the job market or consumer demand.

“So long as those two components remain strong,” she said, the Fed’s policymakers “cannot count on inflation coming down” close to their 2% target within the next two years.

Several Fed officials have said recently that they have yet to see meaningful progress in their fight against rising costs. Inflation rose 8.2% in September from 12 months earlier, just below the highest rate in 40 years.

Still, the policymakers may feel they can soon slow the pace of their rate hikes because some early signs suggest that inflation could start declining in 2023. Consumer spending, squeezed by high prices and costlier loans, is barely growing. Supply chain snarls are easing, which means fewer shortages of goods and parts. Wage growth is plateauing, which, if followed by declines, would reduce inflationary pressures.

Yet the job market remains consistently strong, which could make it harder for the Fed to cool the economy and curb inflation. This week, the government reported that companies posted more job openings in September than in August. There are now 1.9 available jobs for each unemployed worker, an unusually large supply.

A ratio that high means that employers will likely continue to raise pay to attract and keep workers. Those higher labor costs are often passed on to customers in the form of higher prices, thereby fueling more inflation.

Ultimately, economists at Goldman Sachs expect the Fed’s policymakers to raise their key rate to nearly 5% by March. That is above what the Fed itself had projected in its previous set of forecasts in September.

Outside the United States, many other major central banks are also rapidly raising rates to try to cool inflation levels that are even higher than in the U.S.

Last week, the European Central Bank announced its second consecutive jumbo rate hike, increasing rates at the fastest pace in the euro currency’s history to try to curb inflation that soared to a record 10.7% last month.

Likewise, the Bank of England is expected to raise rates Thursday to try to ease consumer prices, which have risen at their fastest pace in 40 years, to 10.1% in September. Even as they raise rates to combat inflation, both Europe and the U.K. appear to be sliding toward recession.

[ad_2]

[ad_1]

As expected, the US central bank – Federal Reserve – on Wednesday hiked interest rates by another 75 basis points in a bid to cool down persistent inflation. The move was on expected lines as inflation continues to be high despite previous rate hikes. On September 21, the Fed increased the rate by similar percentage points.

The US has been reeling under decades-high inflation caused by a combination of factors. The inflation number for September came in at 8.2 per cent, over four times the target set by the Fed. In September, Fed chairman Jerome Powell had said that he was strongly committed to bringing inflation back down to 2 per cent.

The Fed’s rate-setting committee – Federal Open Market Committee – said that recent indicators pointed to modest growth in spending and production. It said job gains had been robust in recent months, and the unemployment rate had remained low.

“Inflation remains elevated, reflecting supply and demand imbalances related to the pandemic, higher food and energy prices, and broader price pressures,” the Fed said, adding that Russia’s war against Ukraine is causing tremendous economic hardship and the war and related events are creating additional upward pressure on inflation and are weighing on global economic activity.

[ad_2]

[ad_1]

The Federal Reserve raised the target federal funds rate by 0.75 percentage point for the fourth time in a row on Wednesday, marking an unprecedented pace of rate hikes.

The U.S. central bank has raised the benchmark short-term borrowing rate a total of six times this year, including 75 basis point increases in June, July and September, in an effort to cool down inflation, which is still near 40-year highs and causing most consumers to feel increasingly cash strapped. A basis point is equal to 0.01 of a percentage point.

A policy statement after the announcement noted that the Fed is considering the “cumulative” impact of its hikes so far when determining future rate increases. Economists are hoping this signals plans to “step-down” the pace of increases going forward, which could mean a half point hike at the December meeting and then a few smaller raises in 2023. Still, stocks tumbled after Federal Reserve Chair Jerome Powell said there were more rate hikes ahead.

“Americans are under greater financial strain, there’s no question,” said Chester Spatt, professor of finance at Carnegie Mellon University’s Tepper School of Business and former chief economist of the Securities and Exchange Commission.

More from Personal Finance:

How Fed’s interest rate hikes made borrowing costlier

Tips to help stretch your paycheck amid high inflation

‘Ugly times’ are pushing record annuity sales

However, “as the Fed tightens, this also has adverse effects on everyday Americans,” he added.

The federal funds rate, which is set by the central bank, is the interest rate at which banks borrow and lend to one another overnight. Although that’s not the rate consumers pay, the Fed’s moves still affect the borrowing and saving rates they see every day.

By raising rates, the Fed makes it costlier to take out a loan, causing people to borrow and spend less, effectively pumping the brakes on the economy and slowing down the pace of price increases.

“Unfortunately, the economy will slow much faster than inflation, so we’ll feel the pain well before we see any gain,” said Greg McBride, Bankrate.com’s chief financial analyst.

Already, “mortgage rates have rocketed to 16-year highs, home equity lines of credit are the highest in 14 years, and car loan rates are at 11-year highs,” he said.

• Mortgage rates are already higher. Even though 15-year and 30-year mortgage rates are fixed and tied to Treasury yields and the economy, anyone shopping for a home has lost considerable purchasing power, in part because of inflation and the Fed’s policy moves.

Along with the central bank’s vow to stay tough on inflation, the average interest rate on the 30-year fixed-rate mortgage hit 7%, up from below 4% back in March.

On a $300,000 loan, a 30-year, fixed-rate mortgage at December’s rate of 3.11% would have meant a monthly payment of about $1,283. Today’s rate of 7.08% brings the monthly payment to $2,012. That’s an extra $729 a month or $8,748 more a year, and $262,440 more over the lifetime of the loan, according to LendingTree.

The increase in mortgage rates since the start of 2022 has the same impact on affordability as a 35% increase in home prices, according to McBride’s analysis. “If you had been approved for a $300,000 mortgage in the beginning of the year, that’s the equivalent of less than $200,000 today.”

For home buyers, “adjustable-rate mortgages may continue to be more popular among consumers seeking lower monthly payments in the short term,” said Michele Raneri, vice president of U.S. research and consulting at TransUnion. “And consumers looking to tap into available home equity may continue to look towards HELOCs,” she added, rather than refinancing.

Yet adjustable-rate mortgages and home equity lines of credit are pegged to the prime rate, so those will also increase. Most ARMs adjust once a year, but a HELOC adjusts right away. Already, the average rate for a HELOC is up to 7.3% from 4.24% earlier in the year.

• Credit card rates are rising. Since most credit cards have a variable rate, there’s a direct connection to the Fed’s benchmark. As the federal funds rate rises, the prime rate does as well, and your credit card rate follows suit within one or two billing cycles.

That means anyone who carries a balance on their credit card will soon have to shell out even more just to cover the interest charges. “This latest interest rate hike will most acutely impact those consumers who do not pay off their credit card balances in full through higher minimum monthly payments,” Raneri said.

Because of this rate hike, consumers with credit card debt will spend an additional $5.1 billion on interest, according to an analysis by WalletHub. Factoring in the rate hikes from March, May, June, July, September and November, credit card users will wind up paying around $25.6 billion more in 2022 than they would have otherwise, WalletHub found.

Already credit card rates are near 19%, up from 16.34% in March. “That’s the highest since the Fed began tracking in 1994 and is more than a full percentage point higher than the previous record set back in 2019,” according to Matt Schulz, chief credit analyst at LendingTree. And rates are only going to continue to rise, he said. “We’ve still got a ways to go before those rates hit their peak.”

The best thing you can do now is pay down high-cost debt — “0% balance transfer credit cards are still widely available, especially for those with good credit, and can help you avoid accruing interest on the transferred balance for up to 21 months,” Schulz said.

“That can be an absolute godsend for folks struggling with card debt,” he added.

Otherwise, consolidate and pay off high-interest credit cards with a lower-interest home equity loan or personal loan, Schulz advised.

• Auto loans are more expensive. Even though auto loans are fixed, payments are getting bigger because the price for all cars is rising along with the interest rates on new loans, so if you are planning to buy a car, you’ll pay more in the months ahead.

The average interest rate on a five-year new car loan is currently 5.63%, up from 3.86% at the beginning of the year and could surpass 6% with the central bank’s next moves, although consumers with higher credit scores may be able to secure better loan terms.

Paying an annual percentage rate of 6% instead of 5% would cost consumers $1,348 more in interest over the course of a $40,000, 72-month car loan, according to data from Edmunds.

Still, it’s not the interest rate but the sticker price of the vehicle that’s causing an affordability problem, McBride said. “Rising rates doesn’t help, certainly.”

• Student loans vary by type. Federal student loan rates are also fixed, so most borrowers won’t be affected immediately. But if you are about to borrow money for college, the interest rate on federal student loans taken out for the 2022-2023 academic year are up to 4.99%, from 3.73% last year and 2.75% in 2020-2021.

If you have a private loan, those loans may be fixed or have a variable rate tied to the Libor, prime or T-bill rates, which means that as the Fed raises rates, borrowers will likely pay more in interest, although how much more will vary by the benchmark.

Currently, average private student loan fixed rates can range from 3.22% to 14.96%, and from 2.52% to 12.99% for variable rates, according to Bankrate. As with auto loans, they vary widely based on your credit score.

Of course, anyone with existing education debt should see where they stand with federal student loan forgiveness.