As a serial entrepreneur and now CEO of Builderall, I’ve heard over 3,000 pitches and helped founders raise millions. From my experience, seven common mistakes often derail attempts to raise investment capital. If you’re looking to raise money for your startup in this uncertain economic environment, be sure to avoid the following:

Mistake #1: Rushing the pitch

Many founders rush through their pitch, but speed isn’t always your friend in the venture capital world. Your goal is to establish key points and let them resonate, not finish your presentation as quickly as possible.

Think of it like telling a good joke at a party — you wouldn’t rush to the punchline before everyone has had a chance to grasp the setup, right? The same principle applies when pitching. You want your investors to hang on to every word. But that’s impossible if you rush or gloss over crucial information.

One effective technique is to use strategic pauses. In between slides or after making a key point, pause for about three seconds to let it sink in and observe your audience’s reactions. Don’t be afraid of silence. Patience in delivery can be a powerful strategy.

Mistake #2: Skipping trust indicators and key differentiators

Balancing detail with brevity is tricky, but it’s essential. There are some critical signals you should share to help build trust and differentiate your business. While most founders want to focus on how great their product is, there are two questions that are arguably more important:

Why is your team uniquely qualified to lead this business?

How does your company stand out in the market?

As far as team qualifications, don’t be shy about including specifics on years of experience, prestigious university degrees, previous exits, existing patents and/or impressive startup or corporate experiences.

I once coached a founder who was struggling to raise capital. After reviewing his pitch deck, I said, “The problem is that you have no real startup experience.” He then proceeded to tell me that he and his co-founder sold their last company for $80 million, but he thought it wasn’t relevant since it was in a different industry. Let me tell you, your previous accomplishments are 100% relevant to whether or not investors will trust you with their money.

Next, I can almost guarantee that whatever amazing idea you are pitching — we have probably already seen it. This begs the question, how are you going to execute differently when you get to market? This is where your current traction becomes crucial: existing user base, early subscribers, accepted patents and strategic partnerships all come into play. These elements demonstrate that you’re not just another idea but a viable business that is already making waves.

Mistake #3: Talking too much and for too long

I know — this sounds like a contradiction based on the first point, but hear me out. Blathering on is another fatal mistake. You should plan for a nine-minute pitch, but you don’t want to “rush through” your nine minutes. Instead, be relentless about what to include – and what to cut – so the pacing feels natural and you’re still covering the key data points that make your business compelling.

I often ask new founders to introduce their startup in just two sentences: What do you do, and why should I care? After that, you have under 10 minutes to explain the market problem, the market size, your business model, your solution, your traction, your team, and your ask. That means you need to be very specific about what details will tell your story most effectively.

I’ve seen many founders get nervous and overcompensate by filling the conversation with unnecessary details and fillers. This often has the opposite effect of what they intend. If you talk too much or too quickly, investors might think you’re not being straightforward, or they may get bored and lose interest.

Remember, you’re pitching to investors, not potential clients. Investors are not interested in how great your product is; they want to know about your market, margins, and differentiation.

I once sat through a pitch for a young women’s jewelry startup where the founder spent the entire time trying to sell me on the jewelry. As an investor, I wasn’t the target audience and the pitch fell flat. Rather than sell me on the business, she was selling me on the product. When talking to investors, they want to hear about the business opportunity, not the product.

Mistake #5: Undermining your credibility with weak language

This might seem like needless semantics, but words like “hope” subtly signal uncertainty, and investors are not fond of taking chances on “hope.” They want clear-cut projections backed by data and logic.

Instead of saying “we hope,” use phrases like “we will” or “we project.” This shift instantly ramps up your pitch’s credibility. Be definitive; your words should exude confidence, not wishful thinking.

Here are a few more examples:

Instead of saying, “We think our product will be successful,” assert your confidence by stating, “Our product is positioned to be successful.” This subtle shift conveys certainty and strengthens your pitch.

Replace “We believe our revenue will grow” with “Our projections show our revenue will grow.” This not only sounds more authoritative but also indicates that your assumptions are based on concrete data.

Don’t say, “We aim to capture 10% of the market;” instead, say, “We are on track to capture 10% of the market.” This adjustment demonstrates that you are actively working toward a clear, achievable target.

Change statements like “We expect to launch by Q2” to “We will launch by Q2.” This minor change projects certainty and reliability, which are crucial to building investor trust.

These subtle language changes replace hesitation and probability with assertiveness. It emphasizes that your pitch is built on credibility and supported by a solid, well-thought-out plan.

Mistake #6: Using broad claims instead of precise data points

When pitching to investors, generalized claims can raise red flags, making investors wonder if you’re trying to obscure the truth or lack the necessary detail.

For example, instead of saying, “We have a huge subscriber list,” focus on concrete details like, “We have over 20,000 subscribers.” Specifics not only clarify your claims but also significantly boost your credibility and trustworthiness.

Here are a few more examples:

Don’t say, “Our team has a lot of experience.” Say, “Our team has eight years of experience in this industry.”

Replace “Our product is very sticky, and our customers rarely leave” with “Our product has an 89% customer retention rate.”

Instead of “We anticipate rapid growth,” say, “Our projections show 30% month-over-month growth in the fourth quarter.”

Swap “We dominate the market” with “We currently hold 45% of the market share in our region.”

These changes in phrasing turn vague assertions into solid, data-backed statements, which help to build investor confidence and convey that your pitch is grounded in reality.

Mistake #7: Telling instead of showing

Our final lesson: show, don’t tell. Depicting something visually instead of through words will have a greater impact and be more likely to be remembered. Instead of telling investors, “We have a great interface,” show the interface screens and let them make the determination themselves about whether it’s great or not. Instead of saying, “We’ve grown exponentially over the years,” show a line or bar chart illustrating your impressive growth.

One more example: telling investors how much your customers love you is far less impactful than showing screenshots of social media posts where your customers are raving about you in their own words. Keep this mantra in mind: less talk, more visuals.

Bottom line

Mastering the art of pitching involves more than just avoiding pitfalls — it’s about crafting a narrative that resonates with investors and builds trust. However, by avoiding these seven mistakes, you significantly increase your chances of securing the capital needed to take your startup to the next level.

In today’s challenging economic climate, precise communication, showing rather than telling, and delivering data-backed arguments will set you apart. Investors want to back entrepreneurs who can navigate adversity and drive their ventures to success. Keep refining your pitch, build strong relationships, and show investors why your startup is the one to bet on.

As AI technology and programs like ChatGPT evolve, the way venture capitalists think about investing in startups is changing.

Investor Leah Solivan, the founder of freelance marketplace TaskRabbit, which sold to Ikea in 2017, has been working as a venture capitalist for the last eight years. She currently works with startups building AI products as a general partner at early-stage fund Fuel Capital.

The process to build an AI company is “very expensive,” she says.

Leah Solivan. (Photo by Chance Yeh/WireImage)

“[AI] is a big game-changing technology, but the costs are still so high to launch something,” Solivan told entrepreneur Jeff Berman last week. “Startups need to raise a lot more money to get started right now.”

Solivan says the cost of AI is changing where a smaller, early-stage fund like Fuel Capital invests. Big industry players like Microsoft and Nvidia, which have invested billions of dollars into AI companies, can afford to invest in expensive AI startups — but smaller, early-stage funds might not see the return on investment they’re looking for.

So smaller funds could strategically choose to pass on AI startups because of the steep price, even if those startups are developing cutting-edge technology.

“It’s almost like when we used to look at hardware companies and we were like whoa this is going to take way too much capital, the ROI on our investment, the math just doesn’t work for our fund,” Solivan explained. “You need really, really deep pockets to be successful. I think it’s harder for the small funds to play here.”

AI was also the sector with the biggest jump in funding last year, with AI startups collectively raising $50 billion, even though the year was tough as a whole for startup fundraising.

Opinions expressed by Entrepreneur contributors are their own.

While AI has been in existence since the 1950s, it has only just recently become a household name with the introduction of OpenAI’s ChatGPT less than two years ago. As an investor in both OpenAI and xAI, I continuously ask myself the ethical ramifications of this new technology, how intelligent it is and whether it is the best path forward for humanity. As an experiment, I asked ChatGPT its opinion about artificial intelligence (AI) systems in today’s society, and this is what it had to say:

“As an artificial intelligence language model, I do not have personal opinions or beliefs. However, I can provide an objective analysis of AI systems in today’s society. AI has brought about numerous benefits to society, such as improved efficiency, accuracy, and decision-making processes. It has also contributed to advancements in medical research, transportation, and various other industries. However, the deployment of AI systems in today’s society also presents potential risks, such as job displacement, privacy concerns, and the possibility of biased algorithms. Therefore, it is crucial to ensure that AI is developed ethically and responsibly to mitigate these risks and ensure that the technology benefits society as a whole. In summary, AI systems have immense potential to positively impact society, but their deployment must be done with careful consideration and ethical responsibility.”

While this response shows AI is still robotic and objective in its methods of “thinking,” it is also, in fact, intimately aware of the ethical concerns bearing over its use. At this critical point in history, where we sit at the precipice of mass AI adoption, we still can’t seem to decide whether AI will be our savior or our villain. Ultimately, it comes down to the applications and responsible management of AI systems.

As an investor, I am in the unique position of being able to help push these new AI companies forward. In the last two years, we have seen a “gold rush” of AI startups. Many have raised impressive rounds; many have faltered, and some have already seen acquisitions. However, the first two I have invested in OpenAI and xAI are now well-known. The former for its ability to have tackled the challenge of global mass adoption and the latter for its commitment to building a more ethical system for the AI ecoverse.

When it comes to applications in AI, it’s safe to say that humans have always strived to create tools to make our lives easier; this is not new. Historically, “mechanical muscles” and outsourcing shifted physical labor. Now, we’re at the point where “mechanical minds” will unleash a cascade of applications across industries. Automation has evolved from more than just the physical.

One major development pushing forward the AI adoption frontier is Microsoft’s continued investment in OpenAI. This partnership will likely lead to everything from optimized Excels to AI-generated PowerPoints and even more support in email management. Upper-class work is now also ripe for disruption.

In finance, AI can be leveraged in various ways. AI algorithms can identify patterns of behavior, such as unusual transactions or identity theft, allowing financial institutions to detect and prevent activities quickly. AI can also analyze market trends and make assumptions about future trends, assisting institutions in making more accurate decisions.

While this is only one sample of industry transformation, there are some areas of work that will be impacted less by AI. These industries are those operating in information asymmetry — such as early-stage venture capital. For AI to work effectively, the model must have access to data. Industries whose data is private, segregated and complex cannot train and build inferences in the same way that a model based on publicly available information can. The strength of AI is dependent on the value of its underlying data and model, which in turn is dependent on the quality of the rules set forth by the humans crafting the algorithms.

In terms of management, we must continue to maintain an element of skepticism and criticism as the growing adoption of AI increases. These tools will continue to develop, but they should not be treated as an all-knowing source of truth. Again, this is critical because these systems only know what is in their underlying systems. As people, investors and business-minded individuals, we must acknowledge the strength of these systems while also considering the fact that they must be constantly maintained. While AI employs a constantly evolving algorithm that learns from itself and experiences, we must still continue to adjust the rules and data sources supporting these AI systems.

Diversity of thought and perspectives is critical for those who have the power to develop these systems. A system created by humans with biases will intrinsically be biased as well. We must maintain human values in control of the systems. In today’s society, where truth seems to be subjective, belief in these systems can be both extremely advantageous and extremely detrimental. We must refrain from programming systems to tell people what they want to hear. It is important for people to understand and respect the limitations of AI.

At the same time, just because humanity is capable of doing something doesn’t always mean it should. We could likely replace most jobs with AI, but should we? Where do we draw the line? How do we ensure honesty and integrity in future systems and platforms? This is part of what xAI and OpenAI have committed to tackling and why I have believed in and supported them from the beginning.

AI will undoubtedly transform all of our lives, but this transformation will only be positive if we continue to be critical stewards of truth and information. As investors, I encourage everyone to maintain a healthy dose of skepticism when investing in AI-powered solutions. Look at the human beings who stand behind those systems because their beliefs are the ones teaching and driving the solution.

(Reuters) – Cathie Wood, founder and CEO of ARK Investment Management, defended the strategy of the firm’s money-losing flagship fund, telling investors in a letter released late on Wednesday that its fortunes will reverse when interest rates fall.

The ARK Innovation ETF fund has taken investors on a rollercoaster ride in recent years. After a 67.6% gain in 2023, the ETF is down more than 12% so far this year. That compares to a gain of 16.9% for the S&P 500 index so far in 2024, closing above 5,600 for the first time Wednesday.

ARK’s ETF, meanwhile, has seen net outflows of more than $1.8 billion in the last six months, according to data from VettaFi.

In a letter posted on ARK’s website, Wood wrote she fully acknowledged “the macro environment and some stock picks have challenged our recent performance.” Nonetheless, she added, “our conviction in and commitment to investing in disruptive innovation have not wavered.”

ARK’s top investments as of May 31 were Tesla, Coinbase and Roku, according to LSEG data.

Wood argued many of the fund’s holdings were now in “rare, deep value territory” and poised to benefit disproportionately once interest rate cuts begin. She anticipated another blockbuster period for returns that would resemble the fund’s 152.8% gains during the initial stages of the coronavirus pandemic.

“Exiting our strategies now would crystallize losses that lower interest rates and reversions to the mean should transform into meaningful profits during the next few years,” Wood wrote. “We are resolute!”

ARK did not respond immediately to a request for further comment on the letter.

Morningstar, the Chicago-based investment analysis company, earlier this year calculated that ARK’s losses had destroyed $14.3 billion in shareholder value in the 10 years ended December 31, 2023. ARK and Wood did not respond to requests for comment on that report.

Wood believes a key to future returns will lie in artificial intelligence-related investments – but not necessarily in market darling Nvidia and other megacaps.

In the letter, she said she expected to see “a more diverse set of winners to which the current equity market concentration should give way.”

(Reporting by Suzanne McGee; Editing by Jamie Freed)

Bobby Garg and Priya Kumar, the co-founders of Indian rummy operator Passion Gaming, have re-acquired all company shares from their investors and are back in control of the company. The company’s shareholders included global gambling giant Rank Group.

Rank Group, through its Stride Investments subsidiary, had invested $5 million in Passion Gaming shares, comprising of $3.75 million through External Commercial Borrowing in the company.

However, Passion Gaming, best known for its Rummi Passion product, is now back in control after reacquiring its shares for an undisclosed sum. With 10 million registered users and a REimagined Unity-based tech stack, Passion Gaming is scalable and poised to capitalize on the Indian gaming market.

While the company is wary of the 28% tax in India, it is certain that its commitment to sustainability would help it navigate the challenging Indian gaming landscape. Despite that, Passion Gaming is hopeful that the government will implement fairer taxation policies.

Passion Gaming Is Passionate About Sustainability

Priya Kumar said that the Passion Gaming team is proud to re-achieve 100% ownership, calling it a “rarity in a founder’s journey.” He further added that this move will allow the company to pursue its vision with autonomy and tap into the Indian skill gaming market as it sees fit.

Bobby Garg also weighed in on the matter expressing optimism about the future of skill gaming in India.

Navigating the complexities of taxation and hopeful of a positive regulatory setup in the skill gaming industry, we aim to reach 10 crore (100 million) registered users on Rummy Passion over the next three years to establish a significant leadership role in the rummy market.

Bobby Garg, co-founder, Passion Gaming

Finally, Gagan Kharbanda, chief operating officer of the company, highlighted Passion Gaming’s ambition to prioritize safer gaming and sustainability. To that end, the company sports secure account balances, robust AML measures and a commitment to fair gameplay.

During its 8 years in operation, the company has managed to cultivate a strong relationship with its players, cementing itself as India’s number one rummy app, Kharbanda Concluded.

Speaking of India, Stake.com, a leading crypto betting operator, continues to capitalize on the local market. While many competitors have pulled out because of India’s new tax, the online gambling powerhouse chose to stay and tap into the growing demand for IPL betting.

BNY looks to client feedback and demand when planning the product pipeline within its technology arm, Pershing X.

“We’re hearing feedback from our clients, and we’re delivering solutions based on what we’re hearing,” Noam Tasch, head of revenue at Pershing X, told Bank Automation News.

For example, last year, the bank launched its advisory product and a year later rolled out its investor product Wove Investor, he said. When the advisory tool launched, the bank formed a group of clients and prospects to offer feedback on the solution and one response from the group was, “Don’t stop at advisers — and we didn’t,” Tasch added.

(Courtesy/BNY)

Wove Investor, which launched June 4, allows investors to view information from multiple accounts in one place, according to the Pershing X website.

“Advisers asked us to create a simple, interconnected portal for their clients, so we built Wove Investor,” Ainslie Simmonds, president of Pershing X and Pershing Global head of strategy, said in a June 4 release.

Along with Wove Investor, the bank added Wove Data and Portfolio Solutions on the platform on June 4.

“That goes a long way to show not only do we listen and we’re finding pockets of pain points (in the industry), but we’re actually relatively quickly delivering solutions,” he said.

Early-bird registration is now available for the inaugural Bank Automation Summit Europe 2024 in Frankfurt, Germany on Oct. 7-8! Discover the latest advancements in AI and automation in banking. Register now.

Stock splits generate a lot of buzz in the investing world, especially among the amateur crowd. You probably already know that a split doesn’t affect the company’s underlying value — if you have one share worth $100 and the company executes a 10-for-1 split, you would have 10 shares worth $10 each for the same $100 value.

However, there are some advantages to shrinking per-share prices. For example, it’s easier for smaller investors to accumulate a position. Let’s say you put $300 into an account monthly; it’s easier to accumulate a position in a stock selling for $100 than $2,000. The announcements also draw attention to the company, which is potentially of help.

Nvidia is the latest big tech company to announce a split (its second in the past three years). The stock split 10-for-1 last week after an incredible run over the previous few years, as shown below. But Nvidia isn’t the only company with a swelling stock price. The artificial intelligence (AI) boom sent several other stocks to all-time highs.

Could one of these below be next to split their stock?

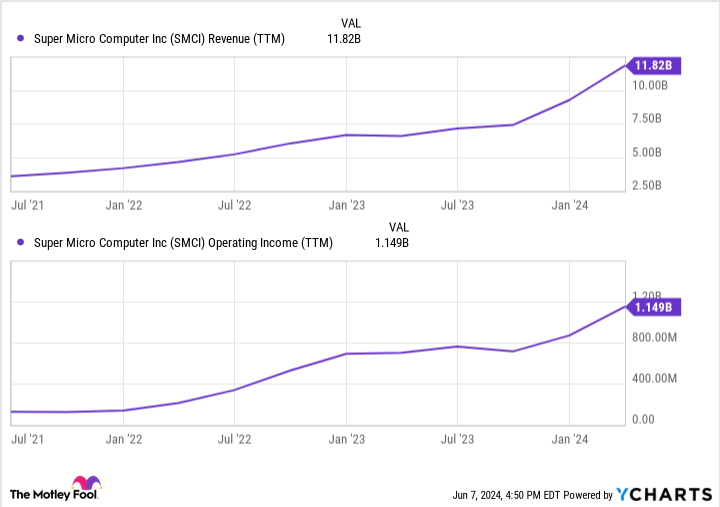

Super Micro Computer

Let’s look first at Super Micro Computer(NASDAQ: SMCI), which trades above $750 per share. This is well below its 52-week high of $1,229 but well above the 52-week low price of $213. Supermicro (as its known) is a nuts-and-bolts play in the AI sector, as its server, storage, and networking hardware are critical to data centers, edge computing, and more.

The intense customer demand, primarily driven by AI, caused revenue and operating income to skyrocket recently, as shown below.

SMCI Revenue (TTM) Chart

The company’s latest quarter saw 200% year-over-year sales growth to $3.9 billion, and Supermicro expects intense growth to continue next quarter with a forecast of $5.1 billion to $5.5 billion. The great thing about this sales growth is that Supermicro is doing it profitably, as you can see by the rising operating income in the chart above. Data center growth is a tailwind that should last for years (check out this article for details).

If the stock price stays high, the company could move to split the stock — potentially soon.

ServiceNow

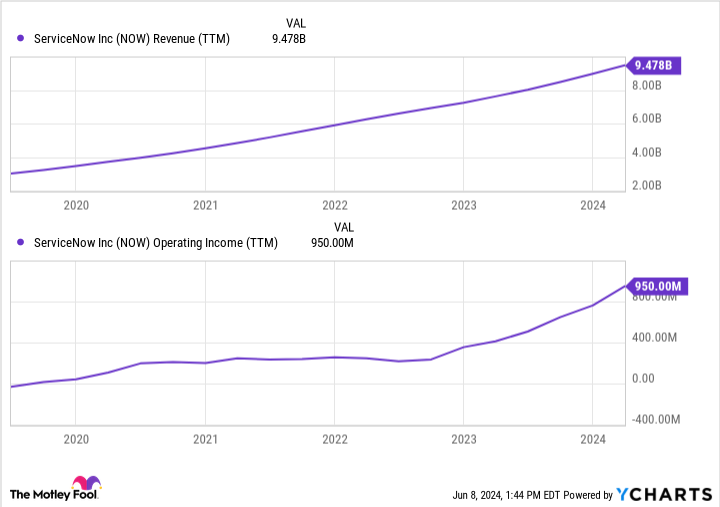

Companies are turning to automation like never before. Automating tasks is critical to efficiency, which is paramount in the hyper-competitive business world. With the Now Platform provided by ServiceNow(NYSE: NOW), customers get virtual customer service agents, process automation, and AI-based issue detection, routing, and problem-solving solutions.

ServiceNow has an expanding customer base of over 8,100, including 85% of the Fortune 500. This includes nearly 2,000 large customers that spend an average of $4.6 million each with ServiceNow annually. The company also boasts a 98% renewal rate. Like Supermicro, ServiceNow’s sales and operating profits are soaring, as shown below.

NOW Revenue (TTM) Chart

The $9.5 billion in trailing-12-month sales above include $2.6 billion in the first quarter, a 24% increase over the prior year. ServiceNow’s stock price has followed suit and trades near $700 per share. If the stock remains elevated, ServiceNow could follow other tech companies and consider a split.

In the grand scheme of the stock market, stock splits aren’t very consequential. They best serve investors by keeping most stocks trading within the same relative range. It would complicate things if all companies did what Berkshire Hathaway did; its stock trades for over $600,000 per share after decades of growth without splitting (although investors can still buy the Class B shares much more cheaply).

Still, stock splits garner attention, open the market up to smaller investors, and create fun topics of conversation. Nvidia is the latest titan to split; more could soon follow.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $740,886!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

Bradley Guichard has positions in Nvidia. The Motley Fool has positions in and recommends Berkshire Hathaway, Nvidia, and ServiceNow. The Motley Fool has a disclosure policy.

A man dubbed pickleball’s “ultimate ambassador” took nearly $50million from various investors, who now say they were duped out of the funds and are fighting to get some of their money returned.

Rodney “Rocket” Grubbs, 68, is now in involuntary bankruptcy after admitting to owe $47.5million plus interest to the investors. He said he always intended to repay investors, who say the process has been slow – if it happens at all.

“You just never would think he would do this,” Bob Zitnick told the Wall Street Journal. “And then you wonder: ‘Am I stupid?’”

Zitnick, 64, and his wife lent Grubbs $300,000 in 2007 for real estate deals. They have gotten some of the money back, but repayments ended in 2018 and the couple now holds promissory notes from Grubbs totaling $3million.

Rodney ‘Rocket’ Grubbs, 68, has been accused by business creditors of taking investments from them in the form of promissory notes and not paying them back (Facebook/Pickleball Rocks)

The couple is some of the 500 creditors across 30 states and countries that Grubbs owe money too. He took the money for pickleball and other investment ventures.

Grubbs is well known — and previously loved — entity in the town of Brookville, approximately 40 miles northwest of Cincinnati. He coached tennis and ran a pickleball shop in the town. He began making a name for himself in the sport by traveling to tournaments all over the world and selling his merchandise through his company, Pickleball Rocks.

Pickleball Rocks was, according to Grubbs, the “world’s most recognized pickleball apparel brand.”

Like many other businesses, it requires investors to operate, and Grubbs allegedly collected those investors from people he knows in the pickleball community. He issued promissory notes — typically for $25,000 at 12 percent interest over 18 months — with the promise that they would join a small group of investors, and that the money would be used to buy inventory for the company’s apparel store, authorities said.

Mr Grubbs said in court filings that he currently owes his investors a total of $47.5m, including interest.

In January, the Indiana Secretary of State securities division sent Grubbs a cease and desist warning to stop offering promissory notes he used to collect investment funds. He has not been charged with a crime in connection to the investigation.

Teri Siewert and her husband reportedly spent years trying to recoup the money they lent to Mr Grubbs, and realized that they might not be the only players to give the well-liked pickleballer their cash.

Ms Siewert, 67, described him as being like “Barney Fife,” the bumbling but lovable deputy sheriff sidekick to Andy Taylor on the Andy Griffith Show.

“He’s just this affable, you know, bumbling kind of character,” she told the paper. “And you wanted to help him.”

She said she was told by Grubbs in 2017 that one of six of his investors has dropped out of the business, and that her and her husband could take their spot, but that it had to be a secret to protect his funding sources. They agreed to help him and gave him $25,000 in 2019.

They tried to get their money back once in 2021, but he told them that the pandemic had left him unable to sell merchandise at tournaments, severely limiting the money he had on hand. They tried again in 2022, but he again said he couldn’t repay them. Siewert said that’s when she began to get suspicious that she was never going to see her money again.

She eventually began a Facebook group called “From Pickleball Rocks to Prison Rocks,” where people who had outstanding loans with Grubbs could share their issues.

Pickleball Rocks stopped operating this year after a group of his creditors forced him into involuntary bankruptcy. Grubbs has now stopped attending tournaments, and claimed assets of approximately $1.6m, far less than what court filings say he owes his creditors.

Grubbs told the Wall Street Journal he never issued any loans that he didn’t intend to repay, but noted his business took a hit during the pandemic and never fully recovered.

He began playing pickleball in 2008 and helped to build the sport’s base over the last 20 years. Grubbs visited tournaments in shirts that said “Pickleball Rocks — Ask Me How” which provided an in for courting potential customers and, possibly, potential investors.

Now, his once-popular shirts are a reminder of all those who claim they’re owed money by the man.

Global fintech funding dropped to a four-year low in the first quarter of 2024 but the number of deals ticked up, according to data intelligence company CB Insights. Fintech funding in Q1 fell to $7.3 billion, registering a 54% drop year over year, according to an April 18 report by CB Insights. While funding dollars […]

In the past five years, Chipotle has crushed it for shareholders, skyrocketing 340%. The Tex-Mex fast casual concept is still expanding rapidly, while posting incredible profitability. It makes sense that investors seeking the next big industry winner are now taking a closer look at Cava(NYSE: CAVA), a much smaller chain.

This surging restaurant stock is already up nearly 90% year to date. Does this powerful momentum make Cava a once-in-a-generation investment opportunity?

Big growth plans

Cava focuses on Mediterranean food, using a similar model to Chipotle that allows hungry patrons to build their own salads, grain bowls, or pitas. Clearly, this is catching on with consumers. Management points to a growing interest from the general public in making healthy food choices as a key tailwind, and Cava’s fast-casual approach only increases accessibility and convenience for its customers.

Despite inflationary pressures and general economic uncertainty, Cava continues to put up strong growth figures. In 2023, revenue jumped 59.8%, boosted by 72 new store openings and a 17.9% same-store sales growth. Last year’s sales figure of $729 million was 518% higher than five years ago in 2018.

Businesses that are investing aggressively in growth initiatives typically aren’t profitable, so it might be surprising to learn that Cava bucks this trend. It registered $13.3 million in net income last year after posting a $59 million net loss in 2022. The hope for shareholders is that consistent and rising earnings will become the norm.

By 2032, the executive team believes it can have 1,000 locations open across the U.S., up from 309 (as of Dec. 31, 2023). This growth potential is probably what investors are most excited about.

High expectations

It should come as no surprise that investors hope Cava can mirror the long-term success of Chipotle. Even with 3,500 existing locations, the fast-casual leader is expanding at a blistering pace with 271 store openings last year. Shares have been a huge winner for investors, thanks to the strong revenue and earnings growth that show no signs of slowing down.

The resulting expectations for Cava are high, and the stock trades at a price-to-sales ratio of 11.1, a 30% premium to Chipotle. I’m not sure if this steep multiple is warranted.

Cava’s valuation implies that management’s long-term target of opening 1,000 stores is a virtual certainty, perhaps at an even faster pace than the leadership team’s 2032 deadline. But I’m not as confident.

Growth is already forecast to slow dramatically. The company plans to open 50 net new locations (at the midpoint of guidance) in 2024, a meaningful drop from last year. Even worse, same-store sales are only set to rise 3% to 5%, an extremely disappointing outlook given the company’s double-digit growth last year. For comparison’s sake, Chipotle is projecting mid- to high-single-digit comparable-sales growth this year, even though it’s already a much bigger enterprise that’s further penetrated in the U.S.

Competition is a critical factor investors can’t ignore. The restaurant sector is perhaps the most competitive in the world, and finding lasting success is extremely difficult. Cava has to constantly win over diners who are overwhelmed with options — even the Mediterranean category is crowded with lots of choices. Without an economic moat, I have my concerns about the company’s success over the next decade and beyond.

To its credit, Cava is developing name recognition that people are excited about, but that’s not enough to make it a once-in-a-generation investment opportunity right now.

Should you invest $1,000 in Cava Group right now?

Before you buy stock in Cava Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Cava Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $652,342!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

Neil Patel and his clients have no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chipotle Mexican Grill. The Motley Fool recommends Cava Group. The Motley Fool has a disclosure policy.

Financial services is an industry desperate for some innovation. In an age when just about anything can be accomplished online, the idea of going to a brick-and-mortar bank to complete a basic transaction is not appealing.

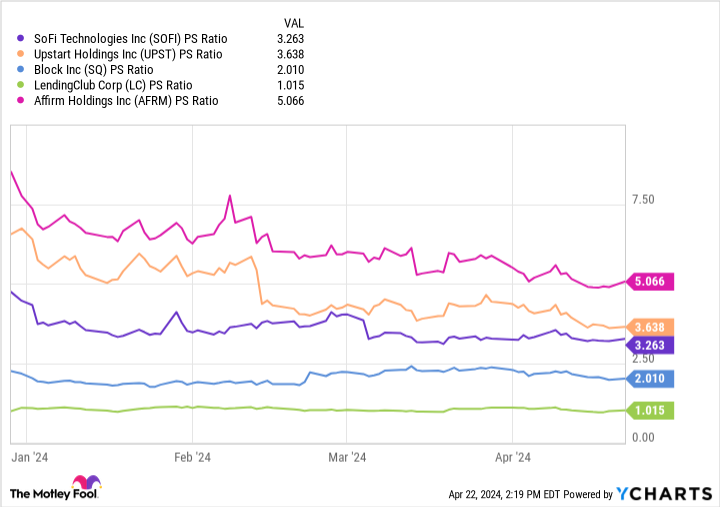

Fintech businesses that operate at the intersection of technology and finance, such as Stripe, Chime, Plaid, and others, have brought some much-needed disruption to legacy financial services. But investors can only access those companies through special investment vehicles as they are still private.

However, one emerging publicly traded fintech is SoFi Technologies(NASDAQ: SOFI). SoFi went public a few years ago following a merger with a special purpose acquisition company (SPAC) led by billionaire investor Chamath Palihapitiya.

With shares trading at a modest $7, investors might be wondering if SoFi is a lucrative opportunity in the budding fintech realm. Let’s dig into why it’s a unique investment prospect and see if the company has potential to generate returns strong enough to help make you a millionaire.

SoFi’s business model is interesting

SoFi is creating a one-stop shop for members on its platform, with access to a host of online services including student loans, mortgages, and stock market investing. This variety of products under one roof has allowed SoFi to cross-sell to its user base.

This approach is known as a flywheel business model. In theory, by cross-selling at a high rate, SoFi does not need to allocate as many resources to customer acquisition over time. Subsequently, the company can use its capital to double down on additional product innovation, thereby making SoFi a formidable competitor for traditional financial services companies.

Image source: Getty Images.

But the long-term potential could be enormous

SoFi’s business model might look attractive on the surface, but investors need to understand that this has been costly to create. Over the last several years, the company has completed a number of acquisitions to help build out its platform. These transactions, combined with efforts to amass a large member base, have resulted in staggering operating losses. Until now, that is.

During the fourth quarter, ended Dec. 31, SoFi surprised investors by posting its first-ever profit on the basis of generally accepted accounting principles.

What’s even better is that management told investors that ongoing profitability can be expected through 2026. This is encouraging because it legitimatizes SoFi’s differentiated business model.

With consistent profitability on the horizon, investors might wonder if SoFi has untapped potential capable of producing lucrative returns.

Could SoFi stock make you a millionaire?

The chart below compares SoFi with peers in fintech on a price-to-sales (P/S) basis. At a P/S of just 3.3, it is in the middle of this cohort.

The important idea for investors is to double down on their winners and hold their highest-conviction positions over the course of many years or even decades.

Take Warren Buffett as an example. The Oracle of Omaha has owned a lot of different stocks over the years. But financial services have consistently remained a top sector for him, with companies like Bank of America, American Express, Visa, and Mastercard representing pillars of the Berkshire Hathaway portfolio.

Investors with a long horizon should consider SoFi’s potential amid a growing fintech sector. The company’s ecosystem of services could make it a future leader as the sector evolves, and I am optimistic that management will make good on its guidance and that steady profits will become more of a staple of its business.

These factors should play a role in SoFi’s growth over time. I think the company’s best days could be ahead, and it has the potential to be a millionaire maker in the long run.

Should you invest $1,000 in SoFi Technologies right now?

Before you buy stock in SoFi Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and SoFi Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $537,557!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

American Express is an advertising partner of The Ascent, a Motley Fool company. Bank of America is an advertising partner of The Ascent, a Motley Fool company. Adam Spatacco has positions in Block and SoFi Technologies. The Motley Fool has positions in and recommends Bank of America, Berkshire Hathaway, Block, Mastercard, Upstart, and Visa. The Motley Fool recommends the following options: long January 2025 $370 calls on Mastercard and short January 2025 $380 calls on Mastercard. The Motley Fool has a disclosure policy.

The stock market has been showing some softness of late. And while that may be discouraging to investors, a pullback can make for a great buying opportunity, especially when you’re holding on for the long haul. There is no shortage of deals out there for investors to consider.

Three stocks trading at incredibly cheap valuations today are CVS Health (NYSE: CVS), Carnival Corp. (NYSE: CCL), and Toronto-Dominion Bank (NYSE: TD). Here’s a closer look at why you’ll want to consider loading up on these stocks right now.

CVS Health

CVS Health has evolved over the years from a pharmacy retailer into a much broader healthcare business. And the company continues to focus on getting bigger and more diverse. Last year, it acquired home health company Signify Health as a way to get deeper into healthcare and help meet the growing needs of seniors through in-home care options.

And in 2023, the company reported a profit of $8.3 billion on revenue of nearly $358 billion. This truly massive business is going to get bigger in the future. And while its margins may not be huge, there’s enough there to fund the company’s dividend, which yields 3.8%, and for CVS to pursue growth opportunities. Its free cash flow last year totaled $10.4 billion and CVS paid out just $3.1 billion in dividends.

At a dirt cheap forward price-to-earnings multiple (based on analyst estimates) of just 8.4, shares of CVS Health today could look like a steal in a few years.

Carnival Corp.

Another good long-term option for investors to consider is cruise line operator Carnival Corp. If not for the shutdowns during the pandemic, the company wouldn’t have needed to accumulate so much debt and its share price would likely be much higher today.

The good news, however, is that Carnival’s financials are improving and the company is in a position to pay down its debt, particularly as demand for cruises remains resilient. In March, the company reported record revenue and booking levels for its fiscal first quarter, ended Feb. 29. Revenue during the period rose by 22% year over year to $5.4 billion, and the company recorded an operating profit of $276 million (versus a loss of $172 million a year earlier).

Carnival has long-term debt totaling $28.5 billion on its books, which may spook some investors given its more modest cash balance of $2.2 billion. But with its financials trending in the right direction and the company having liquidity totaling more than $5.2 billion, Carnival is in strong shape and should be able to chip away at its debt over time.

At just 13 times its estimated future profits, investors are getting the growth stock at a good discount to help compensate for the risk that comes with its high debt load. But the risk may be overblown as the cruise ship company is doing exceptionally well at a time when many businesses are struggling.

Toronto-Dominion Bank

Top Canadian-based bank Toronto-Dominion rounds out this list of cheap stocks. At just 10 times its future profits and less than 1.4 times book value, investors can add this solid bank stock to their portfolios at a very reasonable valuation. Over the past 10 years, TD has averaged a price-to-book multiple of nearly 1.7.

The stock has fallen more than 5% in the past 12 months but this isn’t a risky bank stock that’s in danger of running into liquidity issues like some regional banks. TD is among the safest bank stocks you can own.

In the company’s most recent quarter, which ended on Jan. 31, TD’s revenue totaled 13.7 billion Canadian dollars and rose 12% year over year. Its net income of CA$2.8 billion was up an impressive 79% and its diluted earnings per share of CA$1.55 was far higher than the CA$1.02 that the company pays in dividends per share.

At a cheap price and a high yield of 5.2%, TD makes for a fantastic dividend stock to buy right now.

Should you invest $1,000 in CVS Health right now?

Before you buy stock in CVS Health, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CVS Health wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $505,010!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

David Jagielski has no position in any of the stocks mentioned. The Motley Fool recommends CVS Health and Carnival Corp. The Motley Fool has a disclosure policy.

Opinions expressed by Entrepreneur contributors are their own.

Entrepreneurs often have a deep, personal investment in their businesses, having dedicated years of hard work to bring their ideas to life. However, this emotional attachment can cloud their judgment and make it difficult to objectively assess their venture’s worth. They might find themselves attempting to translate personal effort, time and sacrifice into financial value, which can be problematic in the current environment.

Though Series A investment activities have been stable as of late, there’s been an uptick in down rounds. According to PitchBook and J.P. Morgan, down rounds grew from 8% in 2022 to 20% in 2023. That means less money is coming in than normal, which means more venture-backed startups are on the hunt for capital.

Complicating matters further is the valuation process itself. Many new businesses mistakenly set their value based on competitors, using similarity of goods or services to estimate worth. This type of comparison overlooks differentiators, such as operational, financial or execution risks. Failing to consider milestones that you’ve yet to achieve can lead to the misconception that all is equal.

It’s important to remember that a competitor’s current valuation is the result of their unique journey, and yours will be something entirely different. The challenge is separating personal bias from objective assessment, as you’ll need a clear-eyed view of what your business offers to arrive at an accurate and realistic valuation.

Merely launching a great business doesn’t automatically mean it’s ripe for investment. The fundamental economic principle behind raising capital is that the injection of outside funds should fuel growth and increase the value of the business, creating the potential for investors to see a return on investment. It’s not like investors invest out of the kindness of their hearts (at least, most don’t). They want to see a clear pathway to profitability. The question then remains: How exactly do you prepare for those inevitable funding rounds? Here are some suggestions to get you started:

1. Demonstrate the “why”

Rarely, if ever, will it be enough to simply offer a piece of the business to potential investors. When angling for funding, it’s important to articulate the precise benefits of backing your venture. This is especially important in light of the 30% drop in startup funding in 2023, according to Reuters. You should be able to answer at least these questions: Why should anyone invest in your business? What’s the economic rationale for the investment? How will an investor make money?

Whether it’s an ambitious tech innovation or a noble cause, go beyond the vision or mission of your company and present a plan that clearly shows how you intend to use the capital to achieve specific milestones. That means focusing on practical financial outcomes, which increases the chances that potential investors see a pathway to profitability. They also get a better understanding of the mechanisms in place for monitoring progress and achieving an exit. This clarity in the potential for financial return is what can make the difference in securing much-needed funding versus never getting a meeting.

2. Understand the story behind the numbers

In the context of venture capital and private equity, a compelling pitch will only get you so far. Rather, securing funding is more about what the concrete numbers reveal about the profitability of your venture. Profitmargin, for one, offers insights into your company’s financial health and potential for growth. The same can be said for customer lifetime value, cost structure and revenue.

For example, when my firm evaluates a business, understanding the cost of capital in the current market is crucial — even more so if we encounter a startup with an unclear equity distribution or no significant personal financial contribution. The issue arises when such a company claims that it’s worth a substantial amount, say $1 billion, without a defensible rationale. In other words, always provide tangible evidence that the hard work put into building the business translates into something of real value.

One aspect that entrepreneurs often overlook is the concept of “toxic minority control,” which refers to the disproportionate influence or power held by minority shareholders. Should some disruptive investor buy up enough shares to secure a place on the board, it could potentially lead to adverse outcomes for the venture and other investors. You need to be mindful of this when raising capital, as the terms of investment can have far-reaching implications beyond the immediate influx of funds.

Take Alphabet Inc., for example. Even though Larry Page and Sergey Brin own just 5.7% and 5.5% of the company, respectively, the two Google co-founders each own Class B shares, or “super-voting” shares, providing them with 10 times the control — or 51% of the votes, collectively. Meta and Walmart are other examples of companies with founders (or the heirs of founders) who still control the business even after the initial public offering.

4. Never underestimate (or overestimate) market trends

Though this should go without saying, where the market is headed can significantly influence your startup’s valuation. You need only look to last year for an example of that, with generative AI and AI-related startups raising nearly $50 billion in venture capital, per reporting from Crunchbase. However, don’t make the mistake of benchmarking yourself against corporations listed on the stock exchange.

While market trends certainly make one startup more attractive than another, being in the same industry doesn’t equate to having the same value. Consider the nuances of your company’s stage, market position and operational history in relation to those operating in the same space. PitchBook and Y Combinator are both great resources, as they regularly publish statistics on the average valuations of amounts raised for different funding rounds. Understand where your company truly stands in terms of where the market is headed, as well as your market reach and status, to arrive at a realistic valuation of your venture.

Entrepreneurs often begin with an idea and believe that its mere conception is equivalent to its potential realized. They look at the end goal, which can lead to unrealistic valuations. What truly matters, at least in the eyes of investors, is the ability to execute on that idea, which comes down to the numbers. Get clear on your standing, and then let that guide your discussions with potential investors.

When you think about magnificent stocks, I’m sure the “Magnificent Seven” tech-focused and innovative enterprises come to mind. Their returns in the past decade have certainly been spectacular.

But there are two lesser-known and definitely more boring companies that have also trounced the market. I’m talking about O’Reilly Automotive(NASDAQ: ORLY) and AutoZone(NYSE: AZO). The former is up 678% in the past 10 years, while the latter has risen 498% during that time.

Should you buy these two skyrocketing retail stocks with $100 and hold through 2024 and beyond?

Steady wins the race

These businesses won’t win any awards when it comes to excitement and disruptive potential. They are quite the opposite. However, being boring has clearly worked out well for investors.

Through their networks of thousands of stores, both O’Reilly and AutoZone sell aftermarket car parts and supplies to both DIY and commercial customers. That detail about aftermarket parts is critical, as these companies thrive when selling to consumers that own cars running past the original manufacturer’s warranty. With the average age of vehicles on the road slowly rising with each passing year, coupled with more miles driven, there is plenty of demand out there.

Basically, these businesses perform well when there’s more wear and tear on cars. It’s of the utmost importance for people to have working vehicles to manage their day-to-day life, whether it’s to run errands, drop off and pick up kids from school, or get to work. This makes both O’Reilly and AutoZone somewhat recession-proof.

That’s a fantastic quality to have in stocks that you own because you don’t need to be able to predict what the economy is going to do next. The companies in question will do well no matter what.

Capital returns

Given that they experience stable demand trends regardless of the economic environment, these companies are able to generate copious amounts of profits and cash. O’Reilly and AutoZone raked in $2 billion and $2.1 billion of free cash flow, respectively, in their last fiscal years. This is the true mark of a financially sound enterprise.

Neither business pays dividends. But both management teams are very aggressive when it comes to share buybacks. Just in the past five years, a time period that included various disruptions like the pandemic, supply chain bottlenecks, inflationary pressures, and higher interest rates, O’Reilly’s share count was reduced by 26%, while AutoZone’s shrunk by 30%.

For existing investors, this is a financial boon because it boosts earnings per share. Shareholders’ ownership stakes increase over time if they do nothing. That’s a powerful development.

What’s encouraging is that this attractive capital-return policy comes after executives reinvest in growth initiatives. After opening new stores or distribution facilities each year, share buybacks are done. That should lead to even greater revenue and earnings over time.

Is the price right?

With the overall market in record territory, it’s probably not surprising that both O’Reilly and AutoZone are also near all-time highs. Just like their underlying businesses, these stocks continue to deliver for investors.

This means that they aren’t necessarily trading at bargain prices. On a price-to-earnings (P/E) basis, both stocks are selling at some of their highest levels in the past decade. Consequently, it looks like these boring businesses have caught the eye of the market, with investors being incredibly optimistic about their prospects.

It’s important to ask yourself how much emphasis you place on valuation. Of course, it would be a much better situation if O’Reilly and AutoZone were trading at cheaper P/E multiples. But what gains would you be giving up if you waited on the sidelines? I believe the best move might simply be to spend $50 on each of these stocks and hold for the long term.

Should you invest $1,000 in AutoZone right now?

Before you buy stock in AutoZone, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and AutoZone wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

Neil Patel and his clients have no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Aya Pastry was a rare pandemic success story. While Chicagoans anxiously navigated the early days of COVID, the desire for comfort foods increased, and baker Aya Fukai — who rose through Chicago’s culinary ranks using her imagination and creativity as pastry chef at highly profitable Gold Coast hot spot Maple & Ash — was there with her baked goods: Fukai took inspiration from a variety of sources, including Girl Scout Cookies, which pushed her to create a supercharged doughnut, a decadent treat that looks like a Samoa cookie. Coffeehouses around town turned to Aya to supply pastries, and the bakery’s wholesale operation boomed, counting more than 50 clients including large grocery stores like Dom’s Kitchen & Market and independent coffee shops like Gaslight Coffee Roasters.

But behind the scenes, Fukai wasn’t exactly enjoying her tremendous success. She quietly left the bakery in October. Fukai’s exit came just 10 months after her backers at What If Syndicate dissolved the company. What If co-founder David Pisor brought Aya Pastry under his newly formed entity, Etta Collective.

Few knew about Fukai’s exit, as her name remained on the signs. She says that her deal to sell her 51 percent stake in the bakery for $700,000 closed on October 3. Meanwhile, Pisor told Eater on January 17 that she was still with the bakery.

Aya Pastry is just one of the dominoes to fall in Pisor’s restaurant empire, an empire that at one point consisted of five restaurants in three states. In the past month, Pisor closed the River North location of Etta and filed Chapter 11 bankruptcy papers for Etta Collective and Etta River North. On the same day, Thursday, February 1, his attorney made two more bankruptcy filings — one for Etta Bucktown and another for Aya Pastry. The Aya filing revealed Pisor owed $500,000 to Fukai (she received $200,000 upon closing, it went mostly to attorneys fees, she says). A fifth filing had been made on January 18 involving Etta in Scottsdale, Arizona. There are also reports of a $2.5 million loan defaulting and eviction orders, according to Crain’s. The Chapter 11 filings would allow the businesses to continue, and although messaging directed to customers indicate that things are business as usual, questions remain about Etta’s future. Also, plans for a suburban Etta location in Evanston are on hold, Pisor confirms.

Workers said they only received two hours’ notice before Etta River North closed.Barry Brecheisen/Eater Chicago

“Our aim is to best position the Etta brand for future success,” a statement provided to Eater from Pisor and his reps reads. “By filing for protection under Chapter 11, we will be able to restructure our financial position while continuing our daily operations and keeping our locations open. As has already happened in our Scottsdale location, we predict that we will emerge stronger both operationally and financially.”

Former workers have been calling out Etta Collective for months, alleging that the company left them without health care. Their final paychecks also arrived two days late. Fukai, along with 11 former Etta employees — servers, bartenders, and operations staff — from River North and Bucktown provide an inside look into the seeming slow-rolling collapse of a national restaurant group. Etta’s Chicago workers saw warning signs of the downfall in August when Etta Collective narrowly dodged eviction at its Culver City location and laid off 10 workers including a handful at the corporate level. The cost-cutting continued as nine Etta River North workers claimed that they saw lapses in their health care coverage despite having premiums deducted from their paychecks. They accuse Pisor and management of allegedly misleading customers about the distribution of a 3.5 percent staff benefits fee added to customer checks. Most have requested their names be kept out of the story for fear of being labeled as outspoken as they search for new hospitality jobs. Some say they are worried about becoming a target of what they describe as Pisor’s litigious temperament.

After the settlement, Pisor quickly touted the arrivals of three forthcoming restaurants in an afternoon interview with Eater on January 22 — Etta Evanston, Etta Dallas, and a yet-to-be-announced Downtown Chicago steakhouse. Yet the bankruptcy filings include a list of unpaid vendors across sectors — restaurant, health care, and construction — that may put the three projects in jeopardy. Familiar names like Slagel Family Farm, Sysco, Kilgus Farmstead, and Supreme Lobster are owed thousands of dollars, according to these filings.

“He’s got open tabs all around the city,” alleges a source who works in construction and design.

In a written response about money owed to vendors, Pisor writes that Etta filed for Chapter 11 in part to ensure day-to-day operations to restructure and “work to resolve those payments.”

Etta Collective’s decline comes in the aftermath of a split between Pisor and former business partner Jim Lasky following a legal battle that started in March 2022. The two opened Maple & Ash, in 2015 in Chicago’s Gold Coast. They went on to form What If Syndicate and opened a Maple & Ash in Scottsdale. However, along the way, Lasky and Pisor’s relationship became strained, according to court documents. In January 2023, the pair agreed to split What If into two companies. Pisor formed Etta Collective, taking Etta restaurants in River North and Bucktown, Aya Pastry, and Cafe Sophie in Gold Coast. Lasky formed Maple Hospitality Group, taking Maple & Ash, one of the highest-grossing restaurants in the country, according to Restaurant Business Online.

Pisor’s employees in this new company, Etta Collective, say the split was an unwelcome change. Fukai alleges it was made without her knowledge or input, despite her being the majority owner of Aya Pastry. Though she’s come to terms with leaving the business that bears her name, she is considering pursuing legal action against Pisor after seeing the bankruptcy filing.

Many other former employees believe they would still be employed under different leadership.

“Pisor was the only thing wrong with that company,” former Etta River North server Drew Riebhoff alleges of Etta Collective.

Pisor earned a reputation as a developer with big ideas. As a restaurateur, he relished creating lavish dining rooms. Before Maple & Ash, he served as the chief executive officer of Elysian Hotels and was a prolific real estate developer. In 2015, Lasky and Pisor founded Maple & Ash. Building on the success of that first steakhouse, the partners, along with executive chef and Elysian alum Danny Grant, opened a second location four years later in Scottsdale, Arizona.

Maple & Ash brought a brasher attitude compared to traditional steakhouses. It had to, as it takes guts to open a steakhouse on the perimeter of what Chicagoans have nicknamed “the Viagra Triangle,” with Morton’s and Gibsons already surrounding Mariano Park. Pisor and Lasky debuted a new brand centered on one of the trends of the moment: kitchens with wood-fired hearths.

An approach that mixed fine dining with approachable irreverence earned Maple & Ash national attention; then-Eater critic Bill Addison hailed the team for its embrace of “the steakhouse motif with unfettered playfulness.” Addison continued, “[Grant] oversees a 12-foot hearth that breathes fire over rows of steaks, as well as a coal-burning oven that produces the kitchen’s greatest stroke of genius: a seafood tower of roasted shrimp, oysters, lobster, Alaskan King Crab legs, and other oceanic treasures, kissing the shellfish with smoke and concentrating their flavors.”

When Etta Bucktown, a more casual restaurant than Maple & Ash, opened in 2018, customers soon made it one of the hottest tables in town, too. A prototypical neighborhood restaurant and easily scaled, a second Etta soon opened in River North with a third following in Culver City, California.

But the partnership reached a breaking point during the pandemic. Maple & Ash became caught up in a scandal over vaccinations earmarked for a safety net hospital on Chicago’s West Side. A Maple & Ash regular, the former chief operating officer of Loretto Hospital, broke protocol and secured a supply of COVID vaccines for the steakhouse’s staff. While all of this was going on, restaurants across the country fought for every dollar and applied for PPP funds, and staff donned masks to keep safe. Pisor and Lasky’s relationship continued to erode.

David Pisor came up with much of the design for Maple & Ash, the steakhouse he and Jim Lasky opened before the two split in January 2023.Barry Brecheisen/Eater Chicago

A lawsuit filed by Pisor in April 2022 alleged that Lasky and Grant were freezing him out of the company. A counter-lawsuit accused Pisor of allegedly showing up to a female employee’s house late at night unannounced. Rumors began to circulate on both sides, but before the powder keg could explode, Pisor and Lasky agreed to a settlement in January 2023, splitting the company and keeping any other stories away from the public eye.

Today, Pisor’s empire appears in shambles, and his former business partner at Maple & Ash, Lasky, is defending allegations of PPP fraud levied by restaurant investors. The claims of PPP abuse were used as punchlines during the 2024 Jean Banchet Awards, which recognizes local chefs and restaurants. On stage in January, host Michael Muser, a co-owner of two-Michelin-starred Ever, joked about the alleged purchase of a private jet using taxpayer funds that were supposed to benefit employees. But Maple & Ash’s reputation and brand, at least in the eyes of customers, remains strong. The steakhouse continues to attract crowds in Gold Coast and Scottsdale.

Maple & Ash’s owners declined to comment for this story.

Pisor had big plans in 2023 after breaking away from Lasky. In March, he hired a pair of big names with Michelin-star resumes. Alinea Group alum Dan Perretta served as a partner and executive chef. He brought over Micah Melton, the former beverage director of the Aviary — the upscale cocktail lounge operated by Alinea. Buoyed by a fresh start and new personnel, Pisor teased expansion through a series of media announcements in the spring and early summer. But by August, Melton was laid off and Perretta had quit, allegedly in protest of the layoffs.

For service staff, Etta looked like a great place to work from the outside. The company’s promise to pay 70 percent of medical expenses for employees was particularly attractive. But after those August layoffs — which included firing managers who handled payroll — Etta workers allege that they received mixed messages from management regarding their paychecks and benefits. One ex-employee claims he was told by a manager that Etta had underpaid him in August and that he would receive the missing amount in the next week’s paycheck. When the following payday arrived, he claims he was told he owed money to the restaurant because he was overpaid. Complicating matters, according to workers, was an alleged lapse in dental and vision coverage between July 31 and December 5. Eater reviewed emails from insurance provider Guardian and Etta that backed the claim.

“It was just becoming this big, big process of confusion and lies,” a former River North worker alleges.

In an interview from January and a written statement, Pisor denies any lapses, claiming Etta provided “same-day reimbursement checks” and payments before appointments.

Eater has reviewed worker pay stubs from January 2024 showing the deductions (around $15.56 bimonthly for dental and $67.14 for health insurance for employees without dependents). Another worker tells Eater that their dentist told them their “insurance was no longer active.” They claim management never bothered to tell workers.

“I got a call from my dentist for like $500 because they said that they canceled our insurance in August, but we had still been paying premiums since then,” that same worker says. “And that has been taken out of our checks.”

Similarly, Etta server Riebhoff received a letter dated December 12 from Guardian stating dental coverage had been terminated on July 31 before coverage was reinstated. Workers pushed back during a December pre-shift meeting and benefits were restored retroactively to August. Management allegedly told workers they would be reimbursed for any out-of-pocket health care expenses incurred during the lapse in coverage.

“All employees who attended their appointments and submitted a claim to us received a manual check reimbursement from us directly out of pocket, as we did not want any employee to have to fund their own vision and dental appointments while the billing dispute was still being resolved,” Pisor responded.

In January, Pisor told Eater that the health care concerns were not as widespread as alleged by employees, attributing the claim to just one outspoken worker complaining. However, Eater spoke with eight other employees who shared similar concerns about dental and vision coverage. Pisor added that Etta was in a dispute with Guardian, saying the insurance company overcharged Etta following its August layoffs.

Guardian does not appear on the restaurant’s bankruptcy filing as one of the vendors to whom Etta River North owes money. In a statement, Pisor writes that Etta and Guardian agreed to a payment plan in mid-December after receiving a notice on December 7 from Guardian, giving Etta its 30-day notice that it would discontinue coverage due to nonpayment. However, a $10,042.39 debt to United Healthcare appears on the Etta Collective filing.

Aya Fukai says she left Aya Pastry in October 2023.Aya Pastry

Workers want to know what their deductions were spent on. They also received notice of open enrollment going from December 20 to December 29, 2023. An email sent to workers dated December 29, 2023, announced that the dispute with Guardian had been settled. A representative from Etta’s dental and vision provider, Guardian, declined most questions but did say that Etta is no longer a client.

Etta also tacked on a 3.5 percent fee for customers, presenting it as a payment for “staff benefits.” Workers claim that’s not the case and allege the money goes toward credit card processing fees.

“We were required through management to tell people that that was to go toward our health care,” a former Etta worker alleges.

Pisor’s statement denies this claim, saying the charge is meant to cover health care: “We do not offer discounts for cash, nor do we communicate with customers in that manner.”

Multiple former workers, including Riebhoff, allege that they were told by managers that “if [customers are] paying with cash, we take that service charge off.”

Riebhoff continues, “Yep, I guess if you pay cash, you don’t have to help people with insurance.”

Former Etta workers claim pettiness played a role in the company’s fall, citing numerous instances of Pisor’s hubris. A former employee says they believe “it would be thriving” and alleges that Pisor “completely gutted the restaurant of all of its heart and soul.”

The menu changed so much that regular customers couldn’t recognize the restaurant they once enjoyed; management removed popular items like oysters, ricotta pillows, and fire pie. “They just didn’t want anything that Danny [Grant] created on our menu,” Riebhoff says.

A manager allegedly told Riebhoff that the decision to remove specific dishes was a reaction to the loss of chef Grant after What If’s split. Pisor dismissed that conclusion as untrue speculation, saying while dishes change due to seasonality, the classics remain. In addition, three workers and a source familiar with operations say that to underscore that feeling, someone had defaced a photo of Grant at Etta Bucktown, drawing a penis on the picture.

“That’s how petty that they were about the Danny Grant situation,” a former worker says. “And that’s up at the restaurant for employees to see and walk past every day.”

Cafe Sophie next found footing in Gold Coast.Barry Brecheisen/Eater Chicago

Pisor writes, “to the best of my knowledge, there’s no photo of Danny Grant in the restaurant with graffiti on it” and that “if I had been aware of any such photo, I would have had it removed and made sure we addressed that issue with staff immediately.”

Grant declined a request for comment.

A source familiar with Etta’s operations says they were stunned by how quickly the chain’s financials soured right after the split with Lasky in January 2023. That source claims Pisor didn’t realize that restaurants in Chicago slow down in the winter months and make the majority of money after March. Part of the reason, the source alleges, was that Pisor didn’t make any adjustments to his lifestyle, thinking he could live his life as if he was still a co-owner of Maple & Ash, which reported $32 million in sales in 2023. He wanted badly to see Etta succeed on the national level but Etta wasn’t ready to expand that quickly at that scale, the source says.

Pride also seems to have fueled Pisor’s desire to open another steakhouse — showing Grant and Lasky that he could exceed the success of Maple & Ash without them. Pisor had an opportunity to partner on a new restaurant at One Illinois Center. Maple & Ash’s reputation impressed the project’s owner who sought to replicate that success. But in the wake of the bankruptcy filings and eviction notes, the project owner confirms they have severed ties with Pisor. They declined further comment, stating they didn’t want their name in the story and didn’t want anything to do with Pisor. Two other sources allege that the owner was continually embarrassed by Pisor’s recent headlines.

Engineers, architects, and management companies haven’t been paid for a $5 million project that includes a new Etta in Evanston. Construction was supposed to start there in mid-February, but parties are pulling out of the project: “As far as right now, that project is dead,” a construction source says.

Pisor described Evanston as “on hold” and that Etta Collective’s focus is on restructuring.

Pisor’s attitude toward flipping the page in teasing new projects without facing accountability irked his former employees. The day he closed Etta River North, Pisor told Eater Chicago he had worked out a deal with his landlord to open a new restaurant in the space.

“When he said he was going to open a new restaurant in that space, that was a bit infuriating for me,” a former worker says. “Because if that is the case, why were we not informed about this and given the option to maybe pursue a future with the company?”

As the bankruptcies get sorted, there are parties interested in buying Etta from Pisor. Court documents identified John Leahy, who owns Lulu’s in Waikiki, Hawai’i, as a stalking horse investor. “He is a long-time colleague who is interested in helping us restructure and emerge stronger from this bankruptcy,” according to Pisor. “Each entity is being restructured so that we can emerge stronger from the filing. We’re excited to start growing again once we come out the other side of this.”

While Pisor talks expansion, grassroots campaigns from restaurant workers, including the activists at the CHAAD Project, have mounted with a goal of alerting members of the hospitality industry of Pisor and Etta Collective’s reputation.

Pisor writes that he’s unaware of such campaigns and feels Etta treats workers well: “We take very good care of them, and we have employees who have been with us for five years. We’re very proud of the team we’ve built.”

That’s contrary to Riebhoff’s frustrations which have built for months.

“In the court documents for the Scottsdale bankruptcy, there is a quote from him saying, ‘I want to keep this place open so I don’t negatively impact my employees there,’” Riebhoff says. “Meanwhile, he closes Etta River North two hours before our shift with no communication whatsoever. I fucking worked for Lettuce [Entertain You Enterprises] during COVID, and R.J. Melman called us to tell us about it — everyone. So for him to just like not acknowledge it at all, to have zero sympathy or empathy, is fucking disgusting.”