Federal Reserve interest rate cuts may help turn the tide for commercial real estate. Yet investors should tread carefully if they’re wading into the market. Central bank policymakers’ half-point reduction last month “marks the beginning of the end of the worst CRE downturn since the Global Financial Crisis,” Wells Fargo said in a Sept. 25 note. “Lower interest rates are not a magic bullet, but less restrictive monetary policy lays the groundwork for a commercial real estate recovery,” wrote senior economist Charlie Dougherty. “Decreased long-term interest rates appear to be easing upward pressure on cap rates and slowing declines in property valuations. Meanwhile, increased expectations for an economic soft-landing look to be giving capital the green-light to move off the sidelines,” he added. There are some bumps in the road. On Monday, the 10-year Treasury yield rose above 4% for the first time since August, following Friday’s better-than-expected jobs report . Bond yields move inversely to prices. One basis point equals 0.01%. Fed funds futures trading suggests a roughly 84% likelihood of a quarter-point rate cut at the next Fed meeting in November, while no one is expecting another half-point cut, according to the CME FedWatch Tool. Of course, there is no shortage of obstacles ahead for the market, particularly for office space, Dougherty said. “That said, reduced interest rates should prevent distress from spreading and shorten the hurdles coming down the road,” he added. Lower refi rates for borrowers Companies, who had been extending mortgage deals through the higher-rate environment, will see some relief and eventually be able to refinance at lower rates, said Douglas Gimple, senior portfolio specialist at Diamond Hill. His firm’s Short Duration Securitized Bond Fund (DHEIX) has about 25% of its portfolio in non-agency commercial mortgage-backed securities, as of Sept. 30. DHEIX YTD mountain Short Duration Securitized Bond Fund year to date “It’s not a cure all,” Gimple said. “It’s not going to happen overnight, as we know that when the Fed takes action — whether higher or lower — it takes a while for it to work its way through the system.” He thinks investors can find value now by focusing on a bottom-up process. “If you can find the diamonds in the rough that have been hurt from a pricing standpoint because of their association with commercial real estate, then you can find some really good opportunities,” he said. “You just have to be cautious.” Know what you’re buying Investors should understand what their managers are buying or if they are investing themselves, understand what they are purchasing, he said. Gimple specifically likes single-asset, single-borrower CMBS and commercial real estate collateralized loan obligations. The former, as the name implies, involves one asset — like a high-end hotel — or a single borrower, which can be a hotel chain with multiple locations. The latter are shorter-term deals that are floating-rate and are usually taken out by a company to upgrade a property, like putting in a pool or energy-efficient air conditioning into an apartment complex, he said. Each investment will also always be deal dependent, Gimple said. For instance, he isn’t buying office space in Los Angeles or New York, but may look at a suburban deal. He would look at offices that are class A, which are typically the most modern, and have a 95% occupancy rate with a diversity of occupants. Within hotels or lodging, he looks at “trophy” properties in areas like Miami or Hawaii. “It’s not really about the hotel, it’s about the location,” Gimple said. He also looks at single family rental and industrials, as well as retail to a certain degree. Any CMBS holdings should be just part of a diversified fixed-income portfolio that includes credit and Treasurys, he said. “It depends on the risk appetite that’s going to determine what kind of allocation they should be looking at,” Gimple noted. “You’re remiss as an investor if you’re just avoiding an entire part of the market because you read the headlines. There’s still opportunities there.”

Newfound optimism on Morgan Stanley helped its stock close Friday’s session at its highest level of the year. Jim Cramer is still unsure what the Club’s next move should be. Morgan Stanley’s persistent underperformance has made the stock one of our thornier positions — so much so that Jim has openly considered dumping it for investment banking rival Goldman Sachs . Dealmaking activity has picked up, but it’s not been enough to fully unlock Morgan Stanley shares. That is in large part because the bank’s wealth management division has failed to impress. Analysts at HSBC see better days ahead for Morgan Stanley and in a note to clients late Thursday upgraded the stock to a buy rating from hold, arguing its “long period of underperformance could be ending.” Among the reasons for the call: A healthy market backdrop should support the financial performance of both its investment banking and wealth management operations, analysts said. They added that negative sentiment around the stock more generally also seems to have bottomed. Shares of Morgan Stanley rose more than 3% Friday, to $107.88 each, helped by both HSBC’s upgrade and better-than-expected jobs data , which lifted the entire banking sector higher, including fellow portfolio name Wells Fargo . Morgan Stanley ended Friday within a dollar of its all-time closing high of $108.73 reached back in February 2022. Still, the stock is up only 15.7% year to date and 36.4% over the past 12 months, lagging behind the KBW Bank Index , which has climbed 19.4% and 52.6%, respectively, over those timeframes. For its part, Goldman Sachs has jumped 28.4% so far in 2024 and 60.5% in the past year. Friday’s positive developments are welcome news – but not enough to add clarity on our path forward for Morgan Stanley. We’re maintaining our hold-equivalent 2 rating on the stock. “Candidly, I think that [Morgan Stanley] is not priced for a good IPO market and [Goldman Sachs] is,” Jim said Friday. “The reason for that is because I think that people believe the wealth advisory business isn’t doing as well as it can be and the E-Trade buy seems to not be working out,” Jim said, referring to Morgan Stanley’s $13 billion acquisition of the brokerage firm in 2020. “We still do not have answers for that so I can’t say that we are going to upgrade.” However, there’s hope Morgan Stanley’s stock can climb higher if its sizable investment banking business continues its recovery. In order for that to happen, there must be a more meaningful resurgence in initial public offerings (IPO) and mergers and acquisitions (M & A) after more than two downbeat years for both dealmaking markets. Banks like Morgan Stanley and Goldman Sachs have long relied on fee-based revenues from deals. The more activity there is, the more fees available for them to collect. The nascent rebound has already showed up in Morgan Stanley’s results. In the second quarter, revenue for the firm’s investment banking segment surged 51% year over year. Meanwhile, advisory and equity underwriting fees both increased 30% and 56%, respectively, over the same period. The environment for deals is not back to normal just yet, though. During an industry conference in September, Morgan Stanley co-president Dan Simkowitz said that M & A and IPOs will likely remain below trend through year-end. To be sure, the executive also forecasted that this activity would accelerate in 2025 as the Federal Reserve’s interest rate-cutting efforts ripple through the economy. Morgan Stanley’s wealth management franchise — a major growth priority for the bank — is a lingering concern after a miss on revenues last quarter, which caused the stock to briefly sink. Meanwhile, Goldman Sachs beat analysts’ expectations for revenues in wealth. Morgan Stanley’s quarterly results on Oct. 17 will provide an important look at whether this challenged part of its business is showing any reason for optimism. For the time being, the Club is taking a wait-and-see approach with Morgan Stanley stock. If there is a surge in IPO and M & A activity that HSBC forecasted, Morgan Stanley is well-positioned to benefit. “If we get deals, [Morgan Stanley] will be a good place to be,” Jim said. (Jim Cramer’s Charitable Trust is long MS, WFC. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Bing Guan | Bloomberg | Getty Images

Newfound optimism on Morgan Stanley helped its stock close Friday’s session at its highest level of the year. Jim Cramer is still unsure what the Club’s next move should be.

Some experts speculate the real sticking point in negotiations isn’t about wages but protection from automation. The ILA refused to allow its members to work on automated vessels docking at U.S. ports. As a result, American ports are getting more and more inefficient, ranking not only behind ports in China, but also Colombo, Sri Lanka. (The Container Port Performance Index is put together annually by The World Bank and S&P Global Market Intelligence.)

For reference, the highest-rated port in Canada is Halifax, listed at 108th in the world. Halifax’s port efficiency was well behind not only Sri Lanka, but also economic powerhouses like Tripoli, Lebanon. To give further Canadian context, Montreal is 348th, and Vancouver is 356th, which is just ahead of Benghazi, Libya.

Something tells me that negotiating for USD$300,000-per-year dockworkers is not going to help these North American efficiency numbers. The higher salaries get, the more attractive automation strategies will quickly become. Clearly there will be an eventual reckoning. In the meantime, for at least one more important presidential news cycle, dockworkers will be able to extract large wage gains as they hold the broader economy hostage.

Why utilities aren’t “boring”—any more

As income-oriented Canadian investors start to grow less enamoured of high-interest savings accounts and guaranteed investment certificates (GICs), the dividend yields of dependable North American utility stocks should begin to look more attractive. Given how quickly interest rates are likely to fall, it’s clear that there is a stampede of investors heading for the stocks of utility companies.

The iShares U.S. Utilities ETF (IDU/NYSE) is up more than 30% year to date, and the iShares S&P/TSX Capped Utilities Index ETF (XUT/TSX) is up about 15% year to date. (Check out MoneySense’s ETF screener for Canadian investors.)

Most of the time utilities (especially those in sectors regulated by federal and local governments) are perceived as “boring.” Sure, the profits are dependable, but if the government is going to determine how much is paid for electricity or natural gas, then a company’s profit margins are tough to change. The dividend income is dependable. But that’s really the whole sales job in a nutshell.

Lately, however, due to AI’s electricity needs and possible AI-fuelled efficiency increases, utilities have been getting some glowing press. Falling interest rates mean that annual interest costs will drop (utilities often have to borrow a lot of money to complete big projects). Meanwhile, Canadian investors looking for safe cash flow are pouring in. Utility stocks make up about 4% of the S&P/TSX Composite Index. The largest utility companies—such as Fortis, Emera, Hydro-One and Brookfield Infrastructure—are some of Canada’s largest companies.

Some of the same income-oriented investors who like utility stocks may also be interested in two new exchange-traded funds (ETFs) that J.P. Morgan Asset Management Canada just launched. The JPMorgan US Equity Premium Income Active ETF (JEPI/TSX) and the JPMorgan Nasdaq Equity Premium Income Active ETF (JEPQ) use options strategies to “juice” the income already provided by higher-dividend-yielding stocks.

Feroze Azeez from Anand Rathi Wealth, discusses the issues barring the financial deployment of household savings in India, as well as some of the long-term challenges that Indian banks could face.

San Diego city officials and activists came together to call on business and government officials to address pay inequities for Latinas in San Diego, CA on Dec. 8, 2022.

Matthew Bowler | KPBS | Sipa USA

Latina women working full time, year-round earn 58 cents for every dollar paid to white, non-Hispanic men, according to data collected by the National Women’s Law Center.

Latina Equal Pay Day, which this year falls on Oct. 3, marks the additional days into the new year that Latinas must work to earn as much as the typical annual salary of white, non-Hispanic male workers.

That gap in pay translates to a loss of nearly $1.3 million over a 40-year career. Break that down further and Latinas lose $32,070 in wages per year, or $2,672 every month, compared with the dominant cohort.

While 58 cents per dollar is a penny improvement compared with the previous year, NWLC notes that even though wages have been increasing, so too has the total wage gap over a lifetime — which last year totaled $1,218,000.

“The increase in lifetime losses and widening of the wage gap for all Latina workers, including part-time workers, is likely because white men’s wages are increasing at a faster rate than other demographic groups,” said Ashir Coillberg, NWLC senior research analyst.

Assuming a Latina and her white, non-Hispanic male counterpart both begin work at age 20, NWLC notes, the wage gap means a Latina would have to work until she is 89 years old — eight years beyond her life expectancy — to be paid what a white, non-Hispanic man has been paid by age 60.

Despite the narrow improvement for full-time workers, the gap actually widens for part-time and part-year Latina workers, falling to 51 cents on the dollar compared with 52 cents last year.

The wage gap varies widely for certain Latina communities, and for some in the United States it’s even more extreme.

While full time, year-round Argentinean and Spanish Latina workers remain closest to parity at 84 cents and 81 cents, respectively, wages for Honduran, Guatemalan and Salvadoran women remained the widest at 47 cents, 48 cents and 51 cents, respectively.

“Most other marginalized populations — and women as a whole — saw a slight widening of the wage gap this year, for both full-time, year-round workers as well as when including part-time workers,” Coillberg said.

Guatemalan, Cuban and Spanish women saw the greatest increase in losses over a 40-year career.

Latinas are more likely to hold low-wage jobs, but NWLC research finds pay disparities at all education levels.

While continued education can be a benefit to earnings potential, NWLC data suggests getting more education does not shield them from the wage gap. Latinas are typically paid less than white, non-Hispanic men with the same educational attainment and are often paid less than white, non-Hispanic men with less educational attainment.

Some of the most educated Latinas have some of the most striking pay gaps compared to their white non-Hispanic men counterparts, according to the NWLC. For example, the center said a Latina with a professional degree stands to lose more than $2.9 million to the wage gap over a 40-year career.

“Unequal pay means Latinas have less money to cover current expenses and forces them to miss key opportunities to build wealth and build economic security throughout their lifetimes,” the NWLC notes in the report.

Instead of prioritizing continued education, pay equity experts are advocating for comprehensive legislative reform.

“A comprehensive approach includes requiring equal pay for equal work, pay transparency policies from lawmakers, eliminating the subminimum tipped wage, protection from caregiver discrimination, safety from harassment and health hazards for all workers, prohibiting salary history to determine future pay, and increased access to higher-paid jobs for women,” said Noreen Farrell, Equal Pay Today chair. “That’s how you actually close the gap.”

“The widening gap underscores the urgency of tackling this issue to ensure equitable economic opportunities for Latinas,” Farrell said. “Latinas do not have one more day to wait for equal pay.”

Great news for Club stocks Wells Fargo and Morgan Stanley : The rebound in investment banking isn’t over yet. The catalyst? Dealmaking is expected to continue to rise as the Federal Reserve delivers more interest rate cuts. This should, in turn, boost revenues for a key business within both Wall Street firms. We’ll find out to what extent when Wells Fargo reports earnings on Oct. 11 and Morgan Stanley delivers quarterly results on Oct. 16. Lower borrowing costs tend to spur mergers and acquisitions (M & A) and initial public offerings (IPO), which means more business for the banks. Recent numbers from consulting firm KPMG and financial data provider S & P Global Market Intelligence indicate a solid pickup in activity for M & A and IPOs already. So far in 2024, mergers and acquisitions transaction values and money raised from initial public offerings are largely outperforming all of last year’s lackluster activity. U.S. mergers and acquisitions rose 37% to $1.3 trillion in the first nine months of 2024 compared to the same period a year ago, according to KPMG, citing data through Sept. 15. Global M & A transaction values so far this year of roughly $2 trillion have already beat 2023’s total of $1.6 trillion, according to S & P Global data captured on Oct. 1. The IPO market has improved, too. According to KPMG, public offerings listed in the U.S. raised $28.3 billion during the first nine months of 2024. That’s up 50% year over year. All of this bodes well for the kind of advisory and underwriting fees that investment banks can charge to facilitate these deals. To be sure, M & A and IPO values are still down significantly from their Covid peaks in 2021 after the Fed delivered two emergency rate cuts in March 2020 that took the cost of borrowing to near zero. Rates remained that way until March 2022 when central bankers started their tightening cycle to fight inflation. The Fed hiked rates 11 times over 18 months before cutting rates by 50 basis points last month. Speaking at a National Association for Business Economics event in Nashville, Tennessee, Fed Chairman Jerome Powell said Monday that he expects an additional 50 basis points worth of rate cuts this year — 25 in November and 25 in December. The market is not quite ready to take Powell at his word. As of Tuesday, the CME FedWatch tool was putting roughly 66% odds on a 50 basis point cut in December. Rebecca Brokmeier, group head of KPMG’s investment banking platform, sees “an increase in new deals in the market in the fourth calendar quarter and expects this trend to continue as we move into 2025” while the Fed continues to lower rates. Brokmeier told CNBC Tuesday that a lot of this activity is expected to be driven by private equity, which is “more reliant on low interest rates for transactions than corporations and have record levels of dry powder to deploy as well as long-held assets that must be exited in order to return cash to their investors.” MS YTD mountain Morgan Stanley (MS) year-to-date performance For Morgan Stanley, a resurgence in its investment banking division is crucial to our investment thesis and why we stuck with it. Following nearly two downbeat years, we saw reason to be optimistic about Morgan Stanley’s IB business last quarter, which was out in July. IB segment revenue jumped 51%. Breaking IB down further, advisory and equity underwriting fees both surged 30% and 56%, respectively, from the prior year. Last month, however, Jim Cramer criticized the stock’s underperformance , adding that he was considering exiting Morgan Stanley and swapping in investment banking rival Goldman Sachs , where he used to work during his days on Wall Street. Part of that underperformance came after co-president Dan Simkowitz said that M & A and IPOs will remain below trend for the rest of 2024 at an industry conference. To be sure, he also predicted that this activity would accelerate in 2025 as the Fed lowers rates. “Morgan Stanley is in no man’s land, too low to sell and too high to buy. That means wait, which is exactly what we are doing,” Jim said during the Club’s Monthly Meeting on Sept. 12, two days after Simkowitz’s comments. “It might be time to say goodbye and pick up some of the much better run Goldman Sachs.” A week later, Morgan Stanley stock rose on the Fed rate cut, and the Club settled for trimming the position . Morgan Stanley has diversified its portfolio and moved more heavily into wealth management in recent years to reduce its exposure to the volatility of the IB business. So, it remains to be seen how investment banking performance fits into the whole profit picture. WFC YTD mountain Wells Fargo (WFC) year-to-date Morgan Stanley’s IB business is much larger than Wells Fargo’s. However, Wells Fargo, known for its roots as a traditional money center bank, has been working diligently to build out its dealmaking side of the shop. It’s kind of the opposite of Morgan Stanley. Wells Fargo, which has a strong wealth management franchise, is branching out to take a slice of the IB pie. Wells has made a series of senior-level hires in recent years to expand its corporate and investment banking (CIB) division. This helps the bank rely less on interest-based incomes from its consumer lending business, which have been long at the mercy of the Fed’s monetary policy decisions. We’ve seen positive signs already, as CIB revenue jumped 38% year over year in the July quarter. “We continued to see growth in our fee-based revenue offsetting an expected decline in net interest income,” Wells Fargo CEO Charlie Scharf said during the July 12 earnings call. “The investments we have been making allowed us to take advantage of the market activity in the quarter with strong performance in investment advisory, trading and investment banking fees.” In another positive development in Scharf’s bid to clean up the bank’s past missteps and get regulatory permission to expand, Bloomberg News reported last week that Wells Fargo submitted a third-party review of its risk and control overhauls to the Fed in an effort to get the central bank-mandated $1.95 trillion asset cap removed. The restriction was put in place by the Fed in 2018 after a series of scandals under previous leadership. (Jim Cramer’s Charitable Trust is long WFC, MS. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Federal Reserve Chairman Jerome Powell speaks during a news conference following the September meeting of the Federal Open Market Committee at the William McChesney Martin Jr. Federal Reserve Board Building on September 18, 2024 in Washington, DC.

Every weekday the CNBC Investing Club with Jim Cramer holds a “Morning Meeting” livestream at 10:20 a.m. ET. Here’s a recap of Friday’s key moments. 1. Wall Street was mixed Friday but still heading for solid weekly gains. The 10-year Treasury yield dipped, but the S & P 500 was little changed after the August reading of the Federal Reserve’s favorite inflation gauge came in tame. Headline and core PCE were getting closer to the Fed’s 2% inflation target. Next Friday, investors get the September jobs report, the latest look at the health of the second part of the central bank’s dual mandate: the labor market. The economic data between now and the Fed’s meeting on Nov. 6-7 will be key to how much further interest rates will be cut. 2. Shares of Best Buy rose more than 2% on Friday after JPMorgan added the stock to its analyst focus list. The analysts have had a buy-equivalent rating on the stock since February, which is around when we started buying. Looking back, that was a good call with shares up 30% year to date. JPMorgan sees value because investors are underappreciating the AI-powered personal computer cycle and the potential for TVs and appliances to inflect as housing improves. Other housing plays in our portfolio include Stanley Black & Decker and Home Depot . 3. Wells Fargo shares were slightly lower Friday, one day after popping 5% on an encouraging Bloomberg News report about the Fed-mandated asset cap, which was put in place at the bank in 2018. Bloomberg reported that Wells Fargo submitted a third-party review of its risk and control overhauls to the Fed for sign-off to remove the cap. Despite Thursday’s gains, Wells Fargo shares are having a tough month. The bank delivers quarterly earnings on Oct. 11. Our other financial name, Morgan Stanley , reports Oct. 16. (Jim Cramer’s Charitable Trust is long BBY, WFC. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

JPMorgan Chase CEO and Chairman Jamie Dimon gestures as he speaks during the U.S. Senate Banking, Housing and Urban Affairs Committee oversight hearing on Wall Street firms, on Capitol Hill in Washington, D.C., on Dec. 6, 2023.

Evelyn Hockstein | Reuters

Buried in a roughly 200-page quarterly filing from JPMorgan Chase last month were eight words that underscore how contentious the bank’s relationship with the government has become.

The lender disclosed that the Consumer Financial Protection Bureau could punish JPMorgan for its role in Zelle, the giant peer-to-peer digital payments network. The bank is accused of failing to kick criminal accounts off its platform and failing to compensate some scam victims, according to people who declined to be identified speaking about an ongoing investigation.

In response, JPMorgan issued a thinly veiled threat: “The firm is evaluating next steps, including litigation.”

The prospect of a bank suing its regulator would’ve been unheard of in an earlier era, according to policy experts, mostly because corporations used to fear provoking their overseers. That was especially the case for the American banking industry, which needed hundreds of billions of dollars in taxpayer bailouts to survive after irresponsible lending and trading activities caused the 2008 financial crisis, those experts say.

But a combination of factors in the intervening years has created an environment where banks and their regulators have never been farther apart.

Trade groups say that in the aftermath of the financial crisis, banks became easy targets for populist attacks from Democrat-led regulatory agencies. Those on the side of regulators point out that banks and their lobbyists increasingly lean on courts in Republican-dominated districts to fend off reform and protect billions of dollars in fees at the expense of consumers.

“If you go back 15 or 20 years, the view was it’s not particularly smart to antagonize your regulator, that litigating all this stuff is just kicking the hornet’s nest,” said Tobin Marcus, head of U.S. policy at Wolfe Research.

“The disparity between how ambitious [President Joe] Biden’s regulators have been and how conservative the courts are, at least a subset of the courts, is historically wide,” Marcus said. “That’s created so many opportunities for successful industry litigation against regulatory proposals.”

Those forces collided this year, which started out as one of the most consequential for bank regulation since the post-2008 reforms that curbed Wall Street risk-taking, introduced annual stress tests and created the industry’s lead antagonist, the CFPB.

In the final months of the Biden administration, efforts from a half-dozen government agencies were meant to slash fees on credit card late payments, debit transactions and overdrafts, among other proposals. The industry’s biggest threat was the Basel Endgame, a sweeping plan to force big banks to hold tens of billions of dollars more in capital for activities like trading and lending.

“The industry is facing an onslaught of regulatory and potential legislative change,” Marianne Lake, head of JPMorgan’s consumer bank, warned investors in May.

JPMorgan’s disclosure about the CFPB probe into Zelle comes after years of grilling by Democrat lawmakers over financial crimes on the platform. Zelle was launched in 2017 by a bank-owned firm called Early Warning Services in response to the threat from peer-to-peer networks including PayPal.

The vast majority of Zelle activity is uneventful; of the $806 billion that flowed across the network last year, only $166 million in transactions was disputed as fraud by customers of JPMorgan, Bank of America and Wells Fargo, the three biggest players on the platform.

But the three banks collectively reimbursed just 38% of those claims, according to a July Senate report that looked at disputed unauthorized transactions.

Banks are typically on the hook to reimburse fraudulent Zelle payments that the customer didn’t give permission for, but usually don’t refund losses if the customer is duped into authorizing the payment by a scammer, according to the Electronic Fund Transfer Act.

A JPMorgan payments executive told lawmakers in July that the bank actually reimburses 100% of unauthorized transactions; the discrepancy in the Senate report’s findings is because bank personnel often determine that customers have authorized the transactions.

Amid the scrutiny, the bank began warning Zelle users on the Chase app to “Stay safe from scams” and added disclosures that customers won’t likely be refunded for bogus transactions.

The company, which has grown to become the largest and most profitable American bank in history under CEO Jamie Dimon, is at the fore of several other skirmishes with regulators.

Thanks to his reputation guiding JPMorgan through the 2008 crisis and last year’s regional banking upheaval, Dimon may be one of few CEOs with the standing to openly criticize regulators. That was highlighted this year when Dimon led a campaign, both public and behind closed doors, to weaken the Basel proposal.

In May, at JPMorgan’s investor day, Dimon’s deputies made the case that Basel and other regulations would end up harming consumers instead of protecting them.

The cumulative effect of pending regulation would boost the cost of mortgages by at least $500 a year and credit card rates by 2%; it would also force banks to charge two-thirds of consumers for checking accounts, according to JPMorgan.

The message: banks won’t just eat the extra costs from regulation, but instead pass them on to consumers.

While all of these battles are ongoing, the financial industry has racked up several victories so far.

Some contend the threat of litigation helped convince the Federal Reserve to offer a new Basel Endgame proposal this month that roughly cuts in half the extra capital that the largest institutions would be forced to hold, among other industry-friendly changes.

It’s not even clear if the watered-down version of the proposal, a long-in-the-making response to the 2008 crisis, will ever be implemented because it won’t be finalized until well after U.S. elections.

If Republican candidate Donald Trump wins, the rules might be further weakened or killed outright, and even under a Kamala Harris administration, the industry could fight the regulation in court.

That’s been banks’ approach to the CFPB credit card rule, which aimed to cap late fees at $8 per incident and was set to go into effect in May.

A last-ditch effort from the U.S. Chamber of Commerce and bank trade groups successfully delayed its implementation when Judge Mark Pittman of the Northern District of Texas sided with the industry, granting a freeze of the rule.

A key playbook for banks has been to file cases in conservative jurisdictions where they are likely to prevail, according to Lori Yue, a Columbia Business School associate professor who has studied the interplay between corporations and the judicial system.

The Northern District of Texas feeds into the 5th Circuit Court of Appeals, which is “well-known for its friendliness to industry lawsuits against regulators,” Yue said.

“Venue-shopping like this has become well-established corporate strategy,” Yue said. “The financial industry has been particularly active this year in suing regulators.”

Since 2017, nearly two-thirds of the lawsuits filed by the U.S. Chamber of Commerce challenging federal regulations have been in courts under the 5th Circuit, according to an analysis by Accountable US.

Industries dominated by a few large players — from banks to airlines, pharmaceutical companies and energy firms — tend to have well-funded trade organizations that are more likely to resist regulators, Yue added.

The polarized environment, where weakened federal agencies are undermined by conservative courts, ultimately preserves the advantages of the largest corporations, according to Brian Graham, co-founder of bank consulting firm Klaros.

“It’s really bad in the long run, because it locks in place whatever the regulations have been, while the reality is that the world is changing,” Graham said. “It’s what happens when you can’t adopt new regulations because you’re terrified that you’ll get sued.”

— With data visualizations by CNBC’s Gabriel Cortes.

The Chinese government commands the economy to grow

Many people like to sort countries’ economies as either communist, socialist, capitalist or free markets. But these days, every country has some version of a mixed economy. The practical implementation of fiscal and monetary policy is becoming increasingly more grey than our old black-and-white economics textbooks would have us believe. Yet, even within the grey, China’s approach for its economic system is uniquely difficult to define.

Back in 1962, when asked about building a socialist market economy, future China leader Deng Xiaoping famously said, “It doesn’t matter whether the cat is black or white, so long as it catches mice.”

Well, the current China leaders have let the fiscal and monetary cats out of the bag, and they’re hoping those cats are hungry.

We wrote about China’s housing problems about a year ago, warning about rising deflation fears. These issues seem to have gotten worse, and the biggest news in world markets this week was that China’s government decided enough was enough. And in a “command” economy (which is probably the most accurate way to describe its approach), the government has a very high degree of control over economic levers. Consequently, markets reacted swiftly and positively to this news.

Here are the highlights of the multi-pronged fiscal and monetary stimulus that the Chinese government has decided to implement:

Banks cut the amount of cash they need in reserve (this is known as the reservation requirement ratio) by 0.50%. This will incentivize banks to lend more money (basically “creating” 1 trillion yuan, USD$142 billion).

The People’s Bank of China (PBOC) Governor Pan Gongsheng said another cut may come later in 2024.

Interest rates for mortgages and minimum down payments on homes were cut.

A USD$71 billion fund was created for buying Chinese stocks.

That last point is pretty interesting to me. Here you have a supposedly communist government essentially creating a big pot of money to spend within a free stock market. The fund is to directly purchase stocks, as well as providing cash to Chinese companies to execute stock buybacks. Good luck defining that action in traditional economic terms.

The idea is to give investors and consumers faith that they should go out there and buy or invest in China’s expanding economy. Clearly something major had to be done to jolt Chinese consumers out of their malaise.

Early reports are speculating that the Chinese gross domestic product (GDP) could fail to rise by less than the 5% target set by the government. If so, we’re about to see what happens when the commander(s) behind a command economy decide that the GDP will rise no matter what.

Investors looking to get in on the recent rise in real estate stocks should focus on quality, according to Bank of America. The real estate sector of the S & P 500 has been moving higher over the past month or so and is now up 10% year to date, after being in the red earlier this year. The sector hit a 52-week high last week. Real estate investment trusts are also an income play, often paying out attractive dividends. “Stocks with healthy yields become increasingly attractive in a Fed cutting environment,” Jill Carey Hall, an equity and quant strategist at the bank, wrote in a Sept. 9 note that focused on small-cap and midcap REITs. Her work with small-cap and midcap stocks also suggests that dividend yield is the best factor to hedge cycle risk, she added. .SPLRCR YTD mountain S & P 500 Real Estate Sector The Federal Reserve started its rate-cutting cycle last week, slashing the federal funds rate by 50 basis points. The central bank also indicated another 50 basis points of cuts by the end of the year. In this environment, Bank of America likes health care, residential and retail REITs. Health-care real estate is a play on the aging of America , which will see more people seeking medical services and senior housing, Hall said. Residential REITs continue to see demand given housing affordability issues and a majority of retail REITs have beat and raised guidance, she added. When it comes to choosing specific stocks, analyst Jeffrey Spector, the bank’s head of U.S. REITs, suggests looking at names with quality growth, quality value and — with the anticipation of a soft-landing scenario — quality risk. “Higher quality REITs will offer the best earnings and distribution growth,” he wrote in the same note. Quality REITs have resilient pricing power, multiyear earnings visibility based on secular growth drivers, strong and flexible balance sheets and the highest prospect for global inflows. Here are some of the names that made Spector’s top picks list. Welltower is the only large-cap stock that made the cut. The rest are small-cap and midcap REITs. Welltower owns and develops senior housing, skilled nursing/post-acute care facilities and medical office buildings. Near term, Welltower will benefit the most from accelerating occupancy gains amid the post-Covid recovery, Bank of America believes. “In addition, we believe senior housing rate growth will remain robust in 2024 & beyond. WELL has the highest exposure to senior housing operating assets within our coverage universe and based on our demographic analysis has the best positioned portfolio,” the bank said. “Longer term, demographic trends are favorable as baby boomers continue to age.” Shares of Welltower are up 40% year to date. Mid-America Apartment Communities and American Homes 4 Rent are both residential housing plays. The former is a multifamily REIT that operates in communities across the Sunbelt region, where the bank sees robust job growth and a lower cost of living. The latter owns the second-largest single-family rental REIT portfolio in the U.S., Spector wrote. “We remain positive on AMH’s portfolio, limited new supply of single-family homes, structural demographic tailwinds with aging millennials, accretive consolidation/development opportunities, and a strong management,” he said. Mid-America Apartment Communities has gained nearly 18% year to date, while American Homes 4 Rent is up close to 7%. Lastly, Federal Realty Investment Trust owns, operates and develops retail-based properties in coastal markets. Spector said this “blue-chip retail REIT” has a diverse portfolio of shopping centers and should produce growth above its peers in the long term. The stock has moved more than 9% higher so far this year.

While housing affordability remains a challenge for many buyers in the U.S., conditions are somewhat improving due to lower mortgage rates.

Buyers need to earn $115,000 to afford the typical home in the U.S., according to a new report by Redfin, an online real estate brokerage firm. That’s down 1% from a year ago, and represents the first decline since 2020.

Housing payments posted the biggest decline in four years, Redfin also found. The median mortgage payment was $2,534 during the four weeks ending Sept. 15, down 2.7% from a year ago.

Both declines stem from lower mortgage rates, said Daryl Fairweather, chief economist at Redfin.

As of Sept. 19, the average 30-year fixed rate mortgage is 6.09%, down from 6.20% a week prior, according to Freddie Mac data via the Fed. Rates peaked this year at 7.22% on May 2.

“The only reason mortgage payments are down is because of the rate effect,” Fairweather said.

Challenges remain: The typical household earns 27% less than what they need to afford a home, about $84,000 a year, per Redfin data. Home prices are still high, too. The median asking price for newly listed homes for sale is $398,475, up 5.4% from a year ago, Redfin found.

While housing overall continues to be unaffordable for most buyers, “this is as good as it gets,” said Orphe Divounguy, senior economist at Zillow, as the market is generally seeing lower mortgage rates, more inventory and low buyer competition.

Here’s what buyers can expect in the coming months.

Lower home loan rates provide “a great opportunity for buyers who have been waiting,” Divounguy said.

Just because the Federal Reserve cut interest rates, it doesn’t “necessarily guarantee mortgage rates will continue to fall,” he said.

While mortgage rates are partly influenced by the Fed’s policy, they are also tied to Treasury yields and other economic data.

“Mortgage rates will go by the way of the economy,” said Melissa Cohn, regional vice president of William Raveis Mortgage in New York.

“If the economy shows signs of weakening … rates will come down,” Cohn said. “If we see the opposite, and that the economy is chugging along and employment gets stronger, it’s quite possible that rates will go up.”

On top of lower mortgage rates, a higher inventory of homes for sale makes the housing market more favorable for buyers, said Divounguy.

There were 1,350,000 homes for sale by the end of August, up 0.7% from a month prior, according to the National Association of Realtors. That inventory level was up 22.7% compared with August 2023.

Meanwhile, homebuilder confidence in the market for newly built single family homes improved in September, according to the National Association of Home Builders, or NAHB. Its survey also shows that the share of builders cutting prices in September was 32%, down one point. It’s the first decline since April, according to NAHB.

“That tells me that some builders are probably starting to see some increase in foot traffic,” said Divounguy, and that the market could get competitive again.

Price growth will depend on the level of existing home inventory, said Robert Dietz, chief economist at NAHB.

“Existing home inventory is expected to rise as the mortgage rate lock-in effect diminishes, placing some downward pressure on prices as well,” Dietz said.

The housing market is not going to get generally worse over the next 12 months, said Fairweather. If house hunters are discouraged because they haven’t found a home, they might have a better chance next year when there are more listings, Fairweather said.

But they risk higher competition, she warned.

“You’re trading one difficulty for another difficulty,” Fairweather said.

If mortgage rates further decline next year, the number of homes for sale might grow. Most homeowners are sitting on loans with record-low mortgage rates, creating a so-called “lock-in effect,” or “golden handcuff” effect, where they don’t want to sell and finance a new home at a higher rate.

“We’ll probably see more people who are buying, or selling to buy again,” said Fairweather, because high borrowing costs held them back.

The U.S. Justice Department on Tuesday sued Visa, the world’s biggest payments network, saying it propped up an illegal monopoly over debit payments by imposing “exclusionary” agreements on partners and smothering upstart firms.

Visa’s moves over the years have resulted in American consumers and merchants paying billions of dollars in additional fees, according to the DOJ, which filed a civil antitrust suit in New York for “monopolization” and other unlawful conduct.

“We allege that Visa has unlawfully amassed the power to extract fees that far exceed what it could charge in a competitive market,” Attorney General Merrick Garland said in a DOJ release.

“Merchants and banks pass along those costs to consumers, either by raising prices or reducing quality or service,” Garland said. “As a result, Visa’s unlawful conduct affects not just the price of one thing — but the price of nearly everything.”

Visa and its smaller rival Mastercard have surged over the past two decades, reaching a combined market cap of roughly $1 trillion, as consumers tapped credit and debit cards for store purchases and e-commerce instead of paper money. They are essentially toll collectors, shuffling payments between banks operating for the merchants and for cardholders.

Visa called the DOJ suit “meritless.”

“Anyone who has bought something online, or checked out at a store, knows there is an ever-expanding universe of companies offering new ways to pay for goods and services,” said Visa general counsel Julie Rottenberg.

“Today’s lawsuit ignores the reality that Visa is just one of many competitors in a debit space that is growing, with entrants who are thriving,” Rottenberg said. “We are proud of the payments network we have built, the innovation we advance, and the economic opportunity we enable.”

More than 60% of debit transactions in the U.S. run over Visa rails, helping it charge more than $7 billion annually in processing fees, according to the DOJ complaint.

The payment networks’ decades-old dominance has increasingly attracted attention from regulators and retailers.

In 2020, the DOJ filed an antitrust suit to block Visa from acquiring fintech company Plaid. The companies initially said they would fight the action, but soon abandoned the $5.3 billion takeover.

In March, Visa and Mastercard agreed to limit their fees and let merchants charge customers for using credit cards, a deal retailers said was worth $30 billion in savings over a half decade. A federal judge later rejected the settlement, saying the networks could afford to pay for a “substantially greater” deal.

In its complaint, the DOJ said Visa threatens merchants and their banks with punitive rates if they route a “meaningful share” of debit transactions to competitors, helping maintain Visa’s network moat. The contracts help insulate three-quarters of Visa’s debit volume from fair competition, the DOJ said.

“Visa wields its dominance, enormous scale, and centrality to the debit ecosystem to impose a web of exclusionary agreements on merchants and banks,” the DOJ said in its release. “These agreements penalize Visa’s customers who route transactions to a different debit network or alternative payment system.”

Furthermore, when faced with threats, Visa “engaged in a deliberate and reinforcing course of conduct to cut off competition and prevent rivals from gaining the scale, share, and data necessary to compete,” the DOJ said.

The moves also tamped down innovation, according to the DOJ. Visa pays competitors hundreds of millions of dollars annually “to blunt the risk they develop innovative new technologies that could advance the industry but would otherwise threaten Visa’s monopoly profits,” according to the complaint.

Visa has agreements with tech players including Apple, PayPal and Square, turning them from potential rivals to partners in a way that hurts the public, the DOJ said.

For instance, Visa chose to sign an agreement with a predecessor to the Cash App product to ensure that the company, later rebranded Block, did not create a bigger threat to Visa’s debit rails.

A Visa manager was quoted as saying “we’ve got Square on a short leash and our deal structure was meant to protect against disintermediation,” according to the complaint.

Visa has an agreement with Apple in which the tech giant says it will not directly compete with the payment network “such as creating payment functionality that relies primarily on non-Visa payment processes,” the complaint alleged.

The DOJ asked for the courts to prevent Visa from a range of anticompetitive practices, including fee structures or service bundles that discourage new entrants.

The move comes in the waning months of President Joe Biden‘s administration, in which regulators including the Federal Trade Commission and the Consumer Financial Protection Bureau have sued middlemen for drug prices and pushed back against so-called junk fees.

In February, credit card lender Capital One announced its acquisition of Discover Financial, a $35.3 billion deal predicated in part on Capital One’s ability to bolster Discover’s also-ran payments network, a distant No. 4 behind Visa, Mastercard and American Express.

Capital One said once the deal is closed, it will switch all its debit card volume and a growing share of credit card volume to Discover over time, making it a more viable competitor to Visa and Mastercard.

Every weekday the CNBC Investing Club with Jim Cramer holds a “Morning Meeting” livestream at 10:20 a.m. ET. Here’s a recap of Monday’s key moments. 1. Stocks opened higher Monday in a continuation of last week’s momentum, which saw all major indexes gain more than 1%. The Dow closed Friday at a record while the S & P 500 did so Thursday . The strength followed the Federal Reserve’s half-percentage point interest rate cut Wednesday. Health care, a classic defensive sector, is underperforming Monday as investors grow more confident in the possibility of a soft landing for the U.S. economy. Meanwhile, technology — and the semiconductor industry, more specifically — are having a mixed day as Wall Street weighs reports around Intel . In addition to last week’s reports that Qualcomm has discussed buying Intel, Bloomberg News said private equity giant Apollo Global Management has approached the struggling chipmaker with an multibillion investment offer. 2. Despite a slight dip in the S & P 500 Friday, the S & P Short Range Oscillator moved further into overbought territory at 7.3%. A session prior, Jim Cramer’s trusted momentum indicator was at 6.68%. We want to see some market choppiness to work off the overbought reading — as a reminder, anything above 4% on the Oscillator is considered overbought. In this environment, we prefer to raise cash rather than buying stocks. That helps explain why we trimmed Morgan Stanley last week during the post-Fed rate cut rally. Another reason for offloading some shares is the possibility of switching to a different financial stock such as Goldman Sachs , a move Jim has been considering for some time now. 3. Wall Street’s early checks for Apple ‘s new iPhone 16, which hit stores Friday, remain all over the place. Barclays concluded there’s muted demand across both Pro and base models due to shorter lead times compared with last year. Conversely, JPMorgan observed expanding lead times mid-week, suggesting “healthy demand” overall, though lead times were a little softer versus last year on higher-end Pro and Pro Max models. Citigroup analysts also reported an increase in delivery times for the base and Pro models. Director of Portfolio Analysis Jeff Marks advised investors to minimize the noise. “If you’re trying to trade it on every headline, you would have missed such a fantastic move,” Jeff said, alluding to our “own it, don’t trade it” mantra. Additionally, last week T-Mobile’s CEO told Jim in an interview that initial demand for the iPhone 16 looked good relative to the iPhone 15 a year ago. (Jim Cramer’s Charitable Trust is long AAPL, MS. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Even before the Fed rate reduction, some homeowners had already taken advantage of recent declines in mortgage rates. Refinance activity increased to 46.7% of total applications during the week ended Sept. 6, up from 46.4% the week before, according to the Mortgage Bankers Association.

Others have been waiting for the Fed to take action. To that point, 18% of consumers said they planned to refinance a loan once rates go down, according to a report by NerdWallet. The financial services site polled more than 2,000 U.S. adults in July.

“You want to wait for rates to be at a place where you’re happy to keep that rate for a period of time,” said Melissa Cohn, regional vice president of William Raveis Mortgage in New York.

Plus, experts say applying for a refi doesn’t mean you’ll get approved. Your lender may say “no.”

“Regardless of what the Fed is doing, regardless of what’s happening in the broader economy, remember that you have a part to play in all of this, too,” said Jacob Channel, senior economist at LendingTree.

Make sure your finances are in order. Otherwise, your lender might not approve your mortgage refinance, experts say.

Applying to refinance is similar to applying for a mortgage. A change in your financial situation, like a layoff or lower income, or higher debt, could mean you don’t qualify.

“Your mortgage rate and whether or not you get approved for a loan or refinance … depends on you,” said Channel.

Think about all of the “variables that got you approved in the first place,” said Cohn, such as your credit score, your income and how much debt you’ve taken on recently. A change in those variables could affect your ability to be approved.

2. You haven’t had your loan long enough

How soon you can refinance your mortgage will depend on your loan time and lender’s requirements.

You can refinance within days of closing with some types of loans, while others may require a year’s worth of payments, according to LendingTree.

3. You refinanced recently

Technically, there are no hard limits on how many times you can refinance your mortgage, Channel said.

But some lenders will have waiting periods, he said. In those scenarios, if you refinance today, you might not be able to do so again in December if rates move lower after the Fed’s last meeting of the year.

“While there’s maybe not a hard limit on how many times you can refinance, you probably don’t really want to be doing it that often,” he said.

You’re paying closing costs each time you refinance, “so you don’t want to spend money unwisely,” Cohn said.

It may be in your best interest to only consider a mortgage refinance every few years, if your financial situation has changed or if rates are falling “really dramatically,” Channel explained.

“Otherwise, you put yourself in a situation where you’ve spent so much money refinancing that your monthly savings don’t really account for much,” he said.

In some instances, a mortgage modification, or changes to your original home loan to make your payments more manageable, might be an option.

“If you’re really, really struggling, and say something catastrophic has happened in your life … instead of a refinance, it may be worth talking about a mortgage modification with your lender,” said Channel.

To be sure, the broader housing market is not at a risk of a collapse and most homeowners are “not teetering on the edge of foreclosure,” he said.

But if you are experiencing financial hardship, your lender may be willing to modify the terms of your mortgage, said Channel. Reach out to your lender and see if you qualify.

Remember that whether a mortgage refinance makes sense will depend on factors like your income, how long you anticipate staying in your home and your closing costs, said Cohn.

“There’s no single rule of thumb that applies to everyone in the country,” she said.

Talk with your lender or broker, or reach out to a financial advisor to determine what may work best for you, said Channel.

“They’ll be able to walk you through the specifics of your situation,” he said.

U.S. Fed cuts rates for the first time in four years

The U.S. dollar remains the most important currency in the world, and the American economy is arguably the most important financial system as well. Consequently, when the U.S. Federal Reserve makes a big announcement, it creates an economic wave that ripples everywhere. That’s why Wednesday’s decision to cut the key overnight borrowing rate by 0.50% is a very big deal.

Many speculated the U.S. Fed would begin cutting rates this week, but it was generally thought it would go with a 0.25% drop to begin an interest rate-cut cycle. The 50 basis points cut lowers the federal funds rate range 4.75% to 5%.

The U.S. Fed announced in a statement: “The Committee has gained greater confidence that inflation is moving sustainably toward 2%, and judges that the risks to achieving its employment and inflation goals are roughly in balance.”

Federal Reserve Chair Jerome Powell said, “We’re trying to achieve a situation where we restore price stability without the kind of painful increase in unemployment that has come sometimes with this inflation. That’s what we’re trying to do, and I think you could take today’s action as a sign of our strong commitment to achieve that goal.”

Immediately after the news of the U.S.’s first interest rate cuts in four years, major stock market indices responded with a brief jump on Wednesday. But they ended the day nearly flat. That seemed to be a bit of a delayed reaction from investors, as the Bulls returned Thursday with Nasdaq soaring 2.5% and the Dow leaping 1.3% to pass 42,000 for the first time ever.

Notably, former U.S. President Donald J. Trump continued to criticize the monetary decisions made by the U.S. Federal Reserve. This despite centuries of financial wisdom telling us that politicians getting involved in short-term monetary policy is a bad idea. (See: Turkey – Erdoğan, Tayyip.) At bitcoin bar PubKey on Wednesday, Trump said, “The economy would be very bad, or they’re playing politics.”

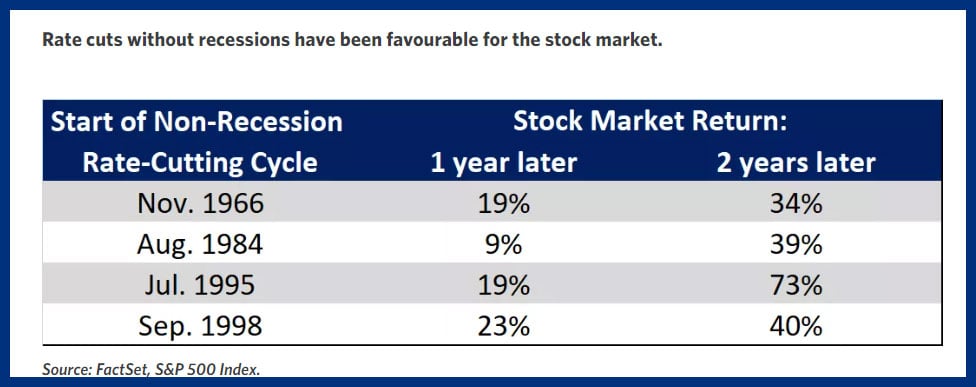

The larger-than-expected rate cut left some commentators questioning if this action would spook the markets. But, if the U.S. Fed manages to thread the needle and cut rates without a recession, it could be a good thing. The historical precedents are very positive for shareholders.

This large rate cut helps ease pressures on emerging markets that borrowed in U.S. dollars. And, it takes some of the pressure off other central banks around the world that didn’t want to see their currencies devalued too much relative to the mighty USD.

An American Airlines’ Embraer E175LR (front), an American Airlines’ Boeing 737 (C) and an American Airlines’ Boeing 737 are seen parked at LaGuardia Airport in Queens, New York on May 24, 2024.

Charly Triballeau | AFP | Getty Images

American Airlines is in talks to make Citigroup its exclusive credit card partner, dropping rival issuer Barclays from a partnership that dates back to the airline’s 2013 takeover of US Airways, said people with knowledge of the negotiations.

American has been working with banks and card networks on a new long-term deal for months with the aim of consolidating its business with a single issuer to boost the revenue haul from its loyalty program, according to the people.

Talks are ongoing, and the timing of an agreement, which would be subject to regulatory approval, is unknown, said the people, who declined to be identified speaking about a confidential process.

Banks’ co-brand deals with airlines, retailers and hotel chains are some of the most hotly contested negotiations in the industry. While they give the issuing bank a captive audience of millions of loyal customers who spend billions of dollars a year, the details of the arrangements can make a huge difference in how profitable it is for either party.

Big brands have been driving harder bargains in recent years, demanding a bigger slice of revenue from interest and fees, for example. Meanwhile, banks have been pushing back or exiting the space entirely, saying that rising card losses, scrutiny from the Consumer Financial Protection Bureau and higher capital costs make for tight margins.

Airlines rely on card programs to help them stay afloat, earning billions of dollars a year from banks in exchange for miles that customers earn when they use their cards. Those partnerships were crucial during the pandemic, when travel demand dried up but consumers kept spending and earning miles on their cards. Carriers have said growth in card spending has far exceeded that of passenger revenue in recent years.

While it says it has the largest loyalty program, American was out-earned by Delta there, which made nearly $7 billion in payments from its American Express card partnership last year, compared with $5.2 billion for American.

“We continue to work with all of our partners, including our co-branded credit card partners, to explore opportunities to improve the products and services we provide our mutual customers and bring even more value to the AAdvantage program,” American said in a statement.

It’s still possible that objections from U.S. regulators, including the Department of Transportation, could further delay or even scuttle a contract between American Airlines and Citigroup, leaving the current arrangement that includes Barclays intact, according to one of the people familiar with the process.

If the deal between American and Citigroup is consummated, it would end an unusual partnership in the credit card world.

Most brands settle with a single issuer, but when American merged with US Airways in 2013, it kept longtime issuer Citigroup on board and added US Airways’ card partner Barclays.

American renewed both relationships in 2016, giving each bank specific channels to market their cards. Citi was allowed to pitch its cards online, via direct mail and airport lounges, while Barclays was relegated to on-flight solicitations.

When the relationship came up for renewal again in the past year, Citigroup had good footing to prevail over the smaller Barclays.

Run by CEO Jane Fraser since 2021, Citigroup has the more profitable side of the AA business; their customers tend to spend far more and have lower default rates than Barclays customers, one of the people said.

Any renewal contract is likely to be seven to 10 years in length, which would give Citigroup time to recoup the costs of porting over Barclays customers and other investments it would need to make, this person said. Banks tend to earn most of the money from these arrangements in the back half of the deals.

With this and other large partnerships, Fraser has been pushing Citigroup to aim bigger in a bid to improve the profitability of the card business, said the people familiar.

“We are always actively working with our partners, including American Airlines, to look for ways to jointly enhance customer products and drive shared value and growth,” a Citigroup spokesperson told CNBC.

Meanwhile, Barclays executives told investors earlier this year that they aimed to diversify their co-branded card portfolio away from airlines, for instance, through added partnerships with retailers and tech companies.

Shortly after the opening bell, we’re selling 100 shares of Morgan Stanley at roughly $101 each. Following Thursday’s trade, Jim Cramer’s Charitable Trust will own 900 shares of MS, decreasing its weighting to roughly 2.65% from roughly 3%. Stocks were poised to open sharply higher Thursday, with the S & P 500 indicating a gain of more than 1.5%, one day after the Federal Reserve cut interest rates by 50 basis points and forecasted more easing before the end of the year. The S & P 500 gave up post-Fed gains Wednesday and closed modestly lower. Morgan Stanley should have a decent pop when trading opens because lower interest rates should boost parts of its business , including investment banking. Morgan Stanley’s roughly 3.7% annual dividend yield also looks a lot more attractive when rates fall . However, for about a week now, we have been talking about taking off some Morgan Stanley as we debate whether to switch the position to a different financial like Goldman Sachs with more leverage to the investment banking cycle. MS YTD mountain Morgan Stanley YTD We thought Morgan Stanley’s share price was too low to sell when we held our September Monthly Meeting last week. But that was when it traded below $97 per share. Based on premarket prices, Morgan Stanley shares were hovering around $101, representing a much better level to take some off. One more factor behind our trim is that the S & P Short Range Oscillator remained in overbought territory after Wednesday’s close. We don’t like to anticipate what the Oscillator will do next. But we have to imagine that it will become even more overbought if the stock market’s opening gains hold. Whenever the Oscillator signals an overbought market, it’s our investment discipline to raise some extra cash. We’ll realize a tiny gain of about 1% on stock purchased in November 2021. (Jim Cramer’s Charitable Trust is long MS. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

U.S. Federal Reserve Chair Jerome Powell speaks during a press conference following a two-day meeting of the Federal Open Market Committee on interest rate policy in Washington, U.S., July 31, 2024.

Kevin Mohatt | Reuters

The Federal Reserve projected lowering interest rates by another half point before the end of 2024, and the central bank has two more policy meetings to do so.

The so-called “dot plot” indicated that 19 FOMC members, both voters and nonvoters, see the benchmark fed funds rate at 4.4% by the end of this year, equivalent to a target range of 4.25% to 4.5%. The Fed’s two remaining meetings for the year are scheduled on Nov. 6-7 and Dec.17-18.

Through 2025, the central bank forecasts interest rates landing at 3.4%, indicating another full percentage point in cuts. Through 2026, rates are expected to fall to 2.9% with another half-point reduction.

“The Committee has gained greater confidence that inflation is moving sustainably toward 2 percent, and judges that the risks to achieving its employment and inflation goals are roughly in balance,” the post-meeting statement said.

The Fed officials hiked their expected unemployment rate this year to 4.4%, from the 4% projection at the last update in June.

Meanwhile, they lowered the inflation outlook to 2.3% from 2.6% previous. On core inflation, the committee took down its projection to 2.6%, a 0.2 percentage point reduction from June.

People shop at a grocery store on August 14, 2024 in New York City.

Spencer Platt | Getty Images

The Federal Reserve announced Wednesday it will lower its benchmark rate bya half percentage point, or 50 basis points, paving the way for relief from the high borrowing costs that have hit consumers particularly hard.

The federal funds rate, which is set by the U.S. central bank, is the interest rate at which banks borrow and lend to one another overnight. Although that’s not the rate consumers pay, the Fed’s moves still affect the borrowing and savings rates they see every day.

Wednesday’s cut sets the federal funds rate at a range of 4.75%-5%.

A series of interest rate hikes starting in March 2022 took the central bank’s benchmark to its highest in more than 22 years, which caused most consumer borrowing costs to skyrocket — and put many households under pressure.

Now, with inflation backing down, “there are reasons to be optimistic,” said Greg McBride, chief financial analyst at Bankrate.com.

However, “one rate cut isn’t a panacea for borrowers grappling with high financing costs and has a minimal impact on the overall household budget,” he said. “What will be more significant is the cumulative effect of a series of interest rate cuts over time.”

“There are always winners and losers when there is a change in interest rates,” said Stephen Foerster, professor of finance at Ivey Business School in London, Ontario. “In general, lower rates favor borrowers and hurt lenders and savers.”

“It really depends on whether you are a borrower or saver or whether you currently have locked-in borrowing or savings rates,” he said.

From credit cards and mortgage rates to auto loans and savings accounts, here’s a look at how a Fed rate cut could affect your finances in the months ahead.

Since most credit cards have a variable rate, there’s a direct connection to the Fed’s benchmark. Because of the central bank’s rate hike cycle, the average credit card rate rose from 16.34% in March 2022 to more than 20% today — near an all-time high.

Going forward, annual percentage rates will start to come down, but even then, they will only ease off extremely high levels. With only a few cuts on deck for 2024, APRs would still be around 19% in the months ahead, according to McBride.

“Interest rates took the elevator going up, but they’ll be taking the stairs coming down,” he said.

That makes paying down high-cost credit card debt a top priority since “interest rates won’t fall fast enough to bail you out of a tight situation,” McBride said. “Zero percent balance transfer offers remain a great way to turbocharge your credit card debt repayment efforts.”

Although 15- and 30-year mortgage rates are fixed, and tied to Treasury yields and the economy, anyone shopping for a new home has lost considerable purchasing power in the last two years, partly because of inflation and the Fed’s policy moves.

But rates are already significantly lower than where they were just a few months ago. Now, the average rate for a 30-year, fixed-rate mortgage is around 6.3%, according to Bankrate.

Jacob Channel, senior economist at LendingTree, expects mortgage rates will stay somewhere in the 6% to 6.5% range over the coming weeks, with a chance that they’ll even dip below 6%. But it’s unlikely they will return to their pandemic-era lows, he said.

“Though they are falling, mortgage rates nonetheless remain relatively high compared to where they stood through most of the last decade,” he said. “What’s more, home prices remain at or near record highs in many areas.” Despite the Fed’s move, “there are a lot of people who won’t be able to buy until the market becomes cheaper,” Channel said.

Even though auto loans are fixed, higher vehicle prices and high borrowing costs have stretched car buyers “to their financial limits,” according to Jessica Caldwell, Edmunds’ head of insights.

The average rate on a five-year new car loan is now more than 7%, up from 4% when the Fed started raising rates, according to Edmunds. However, rate cuts from the Fed will take some of the edge off the rising cost of financing a car — likely bringing rates below 7% — helped in part by competition between lenders and more incentives in the market.

“Many Americans have been holding off on making vehicle purchases in the hopes that prices and interest rates would come down, or that incentives would make a return,” Caldwell said. “A Fed rate cut wouldn’t necessarily drive all those consumers back into showrooms right away, but it would certainly help nudge holdout car buyers back into more of a spending mood.”

Federal student loan rates are also fixed, so most borrowers won’t be immediately affected by a rate cut. However, if you have a private loan, those loans may be fixed or have a variable rate tied to the Treasury bill or other rates, which means once the Fed starts cutting interest rates, the rates on those private student loans will come down over a one- or three-month period, depending on the benchmark, according to higher education expert Mark Kantrowitz.

Eventually, borrowers with existing variable-rate private student loans may be able to refinance into a less expensive fixed-rate loan, he said. But refinancing a federal loan into a private student loan will forgo the safety nets that come with federal loans, such as deferments, forbearances, income-driven repayment and loan forgiveness and discharge options.

Additionally, extending the term of the loan means you ultimately will pay more interest on the balance.

While the central bank has no direct influence on deposit rates, the yields tend to be correlated to changes in the target federal funds rate.

As a result of Fed rate hikes, top-yielding online savings account rates have made significant moves and are now paying more than 5% — the most savers have been able to earn in nearly two decades — up from around 1% in 2022, according to Bankrate.

If you haven’t opened a high-yield savings account or locked in a certificate of deposit yet, you’ve likely already missed the rate peak, according to Matt Schulz, LendingTree’s credit analyst. However, “yields aren’t going to fall off a cliff immediately after the Fed cuts rates,” he said.

Although those rates have likely maxed out, it is still worth your time to make either of those moves now before rates fall even further, he advised.

One-year CDs are now averaging 1.78% but top-yielding CD rates pay more than 5%, according to Bankrate, as good as or better than a high-yield savings account.