Netflix (NFLX/NASDAQ) shareholders were happy on Thursday, as they saw share prices rise 5% in after-hours trading on the back of another excellent earnings announcement. (All figures in U.S. dollars.) Earnings per share came in at $5.40 (versus $5.12 predicted) and revenues were $9.83 billion (versus $9.77 billion predicted).

Paid memberships also topped expectations, at 282.7 million, compared to the 282.15 million predicted by analysts. Netflix chalked up the increase in viewers to new hit shows such as The Perfect Couple, Nobody Wants This and Tokyo Swindlers, as well as new seasons of favourites Emily in Paris and Cobra Kai. Looking ahead to the next quarter, Netflix is banking on the new season of Squid Game and its foray into the world of live sports. Two National Football League (NFL) games and a massively anticipated boxing bout between Jake Paul and Mike Tyson represent new attractions for the streaming giant.

Photo courtesy of United Airlines

United Airlines shares take to the sky

Tuesday was a massive earnings day for United Airlines (UAL/NASDAQ) as earnings per share came in at $3.33, well outpacing the $3.17 that analysts were predicting. (All figures in U.S. dollars.) Revenues were $14.84 billion (versus $14.78 billion predicted). Shares were up more than 13% on the outperformance and the news that the airline was starting a $1.5-billion share buyback program.

Corporate revenue was up more than 13% year over year, while basic economy seat sales clocked an even more impressive 20% increase. Last week, the company announced new international routes headed to Mongolia, Senegal, Spain, Greenland and more.

The best online brokers in Canada

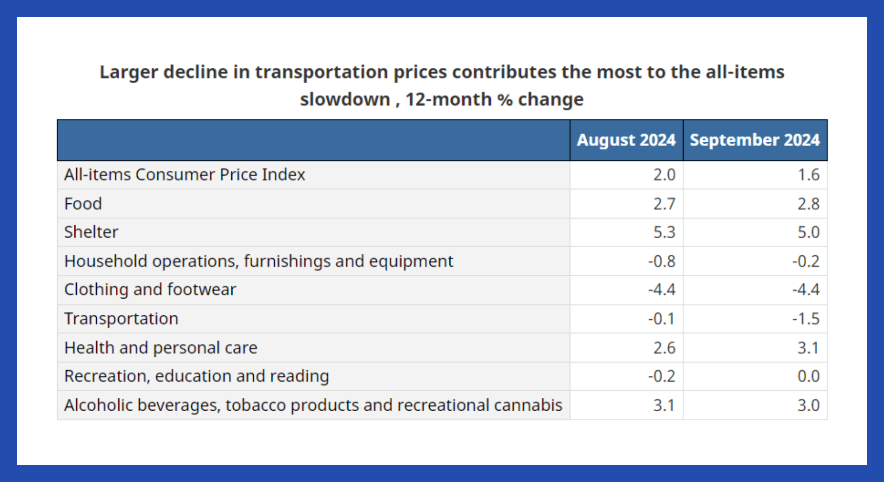

The inflation dragon has been slain

It doesn’t seem that long ago that annualized inflation rates were topping 8%, and there appeared to be no end in sight. Well, the end has arrived. Statistics Canada announced this week that the Consumer Price Index (CPI) annualized inflation rate for September had dropped all the way down to 1.6%. That’s substantially lower than the Bank of Canada’s 2% target.

Led by deflation in clothing and footwear, as well as transportation, the downward trend appears to be widespread. Gasoline was also down 10.7% from this time last year.

Of course, increased shelter costs remain the major concern for many Canadians. Rent increases were up 8.2% year-over-year; while that’s down from August’s figure of 8.9%, it’s still a bitter pill to swallow for many.

Two stocks are getting the call-up from our Bullpen stocks-to-watch list. We’re initiating positions for Jim Cramer’s Charitable Trust in BlackRock and CrowdStrike . We’re buying 17 shares of BLK at $1012.44 each. We’re buying 60 shares of CRWD at $305. Following Wednesday’s trades, BlackRock will have a roughly 0.5% weighting in the Trust, the portfolio used for the Investing Club. CrowdStrike will have a roughly 0.5% weighting. BlackRock is the world’s largest asset management manager and leading provider of investment, advisor, and risk management solutions. It offers a broad set of investment products in equity, fixed income, multi-asset, alternatives, and cash across different client types like Institutional, Retail, and ETFs, around the world. About 43% of its base fees come from actively managed products, 42% from ETFs, 8% from Index, and 7% from cash. Blackrock reported a strong set of third-quarter results last Friday. Total revenues increased 15% year over year to $5.2 billion thanks to the positive impact of markets on average assets under management, 5% organic base fee growth, and higher performance fees. And that 5% organic base fee growth was the company’s highest level in the last three years. BLK YTD mountain BlackRock YTD BlackRock lived up to its reputation as a premier asset gatherer, generating $221 billion of net inflows in the quarter – a company record. The company is having a huge year. Through the first three quarters of 2024, net inflows already surpassed the full-year net inflows of both 2022 and 2023. Assets under management stood at about $11.5 trillion at the end of its third quarter, up $2.4 trillion year over year. Profitability was another highlight. The company continues to deliver sustained asset and technology services growth at scale while remaining disciplined on expenses. Adjusted operating margins expanded 350 basis points year over year to 45.8%, leading to adjusted earnings per share of $11.46, well above estimates of $10.40. The company bought $375 million worth of shares in the quarter, slightly reducing its weighted average diluted shares. The company also pays a dividend yield of about 2% and has increased its payout for 15 straight years. One of the company’s biggest strategic pushes right now is in alternative strategies like private markets and infrastructure. Earlier this month, BlackRock completed its acquisition of Global Infrastructure Partners, a leading independent infrastructure fund manager. The company believes this combination “will provide clients access to investment and operating expertise across the infrastructure landscape.” Blackrock believes infrastructure is a $1 trillion market today and will continue to be one of the fastest-growing segments of private markets in the years ahead. The deal brought in an additional $116 billion of client AUM and $70 billion of fee-paying AUM. It also added long-dated, non-redeemable assets to Blackrock’s business, which the company likes because it diversifies its revenue and earnings mix. Management believes these private market assets will positively impact the company’s overall effective fee rate by 0.5 to 1 full basis point. The stock has had a big move this year, gaining roughly 24% but we think the gains can continue. It’s a pretty steady business with market-leading organic growth, margin expansion, plus a dividend and buyback. Also, BlackRock should see an acceleration of inflows into Fixed Income as central banks cut rates, pushing some of the record amount of assets in Money Markets to flow into bond funds and ETFs. CEO Larry Fink addressed the large cash holdings of investors on the earnings call, explaining that “investors will have to re-risk to meet their long-term return needs.” Fink sees opportunities for investors across several structural trends like “rapid advancements in technology and AI, and rewiring of globalization, and the unprecedented need for new infrastructure.” Fink is a thought leader in the banking industry. We’re starting the position off on the smaller side given its recent run to new highs, and we’ll take advantage of pullbacks to add to our position. Our price target is $1,150, which is roughly 24 times the consensus 2025 EPS forecast of $48.47 per FactSet. CRWD YTD mountain CrowdStrike YTD Next up is CrowdStrike, the cybersecurity company led by its co-founder and CEO George Kurtz, who Jim has had on “Mad Money” many times. CrowdStrike specializes in endpoint protection through its AI-native platform called Falcon. The Falcon platform operates entirely in the cloud, allowing for rapid updates, scalability, and ease of deployment. There’s a good whitepaper on CrowdStrike’s website published by IDC that explains the value of the CrowdStrike Falcon XDR platform. It stops breaches. But it also saves time by speeding up threat protection and response while also helping security teams do more with less. It saves money by reducing the cost of cybersecurity – companies can get rid of less effective platforms and consolidate point solutions. The IDC report found that customers realized a $6 return for every $1 invested with a 5-month payback period after they used the Falcon XDR platform. CrowdStrike was virtually unstoppable this year until July 19 when a faulty software update to its Falcon Sensor security software system caused a global problem with computers running Microsoft Windows. It was a major blow for a cybersecurity company, especially one with a pristine reputation. There was a lot of speculation that the outages would hurt their business from customers revolting, resulting in a loss in market share. However, when CrowdStrike reported at the end of August, the results were excellent with revenue up 32% year over year and adjusted earnings per share of $1.04 versus the 97-cent consensus. Even better, the company showed a gross retention rate of 98%, a sign that virtually no business was lost from the event. More recently, the company held its annual Fal.Con conference in September and it seemed to get a great reception, with attendance up 30% versus last year. Microsoft CEO Satya Nadella spoke at the event which suggested the two companies have buried the hatchet. They’ve had this rivalry for years, but ironically the incident brought the two companies closer together. Shares of CrowdStrike may be up almost 40% since bottoming in early August, but it is still down more than 10% from the July 19 incident and about 23% from its closing high of $392.15 on July 1. This could be an opportunity since virtually no business was lost. Our initial price target is $350, which is roughly where the stock traded right before the July 19th outage. We think the stock should return to these levels since virtually no business was lost. You might be wondering if adding CrowdStrike to the portfolio means that we are heading to the exit on Palo Alto Networks . Does having two cybersecurity companies violate our rules about diversification? We typically don’t like to double up in one area, but we think there is room in the portfolio for both of these best-of-breed names because of position sizing. Palo Alto Networks isn’t that big of a position in the portfolio anymore because of all the huge gains we’ve locked in. Cybersecurity is a great area to be invested in. We’re in an elevated threat environment given all the hostilities happening around the world. Artificial intelligence and Gen AI have made bad actors more sophisticated, so corporations need to invest with the leaders in the industry to stay protected. We’re almost a year into the new SEC rules surrounding the disclosure of cybersecurity incidents, and greater awareness of threats has been a tailwind. (Jim Cramer’s Charitable Trust is long BLK, CRWD, MSFT, PANW. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Morgan Stanley shares soared to all-time highs Wednesday after third-quarter beats on the bank’s top and bottom lines, with strength seen across the board. Revenue for the three months ended Sept. 30 increased nearly 16% year over year to $15.38 billion, outpacing expectations of $14.4 billion, according to estimates compiled by LSEG. Earnings per share (EPS) jumped over 36% versus the year-ago period to $1.88, exceeding the $1.58 expected, according to LSEG. MS YTD mountain Morgan Stanley YTD Club stock Morgan Stanley was up 7.5%. At one stage it was even higher, punching through our $120 price target. We are setting a new PT of $130 and keeping our wait-for-a-pullback 2 rating in deference to the stock’s hot streak — up over 13% from its July high before the August market swoon and up 33% from its Aug. 5 low. Bottom line This was as clean a quarter as anyone could have asked for. Morgan Stanley outpaced expectations in just about every aspect of each operating division and put up very strong quarterly results in terms of firmwide key performance indicators. Last quarter, when the results weren’t quite what we were looking for, we told members that patience was warranted, and we would likely see dynamics improve in wealth management — a key focus area for investors who want to see the bank’s durable fee-based revenue streams continue to grow. That’s exactly what we saw with Wednesday morning’s release. Investment banking also shined as it did for its rivals, including fellow Club name Wells Fargo , which saw its overall earnings report and commentary on Friday blow the doors off. Wells Fargo stock on Wednesday was trying to extend its winning streak to nine straight sessions. We continue to believe that the improvements we’re seeing at Morgan Stanley in terms of efficiency and disciplined execution will magnify the tailwinds of a resilient U.S. economy and stimulus activity internationally. Commentary Return on tangible common equity (ROTCE) is an important metric in valuing financial institutions, such as determining what multiple to put on tangible book value, which came in at $43.76 per share. Morgan Stanley’s third-quarter ROTCE of 17.5% blew away expectations of 14.8%, according to estimates compiled by Bloomberg. On a year-to-date basis, the bank has realized an 18.2% ROTCE. The common equity tier 1 (CET1) ratio, meanwhile, indicates a financial institution’s ability to return cash to shareholders via buybacks and dividend payments. For that reason, we’re very happy to see that stand at 15.1%. That’s a hair lower than the 15.3% the Street was expecting but not too concerning. Total client assets across wealth management and investment management have now exceeded $7.5 trillion, a nearly $1.4 trillion increase over what we saw a year ago as management continues to execute on its mission of reaching $10 trillion over the long term. The overall efficiency ratio , which is calculated by dividing total non-interest expenses by net revenue — so lower is better — came in well below expectations and declined 300 basis points versus the year-ago period – though importantly did not come at the cost of continued investments in the business. On the call, CFO Sharon Yeshaya noted that in addition to revenue growth, the efficiency ratio improvement was the result of “disciplined prioritization of our controllable spend.” Morgan Stanley repurchased $750 million worth of shares in the third quarter — 8 million shares total — at an average purchase price of $99.94 each, which in light of Wednesday stock price looks like a pretty good move for shareholders. Given its 15.1% CET1 ratio, Morgan Stanley has plenty of excess capital at its disposal to both continue investing in growth and return excess capital to shareholders. Morgan Stanley Why we own it : We own Morgan Stanley for the rebound taking place in IPO and M & A activity along with growth in wealth management, which provides more durable fee-based revenues. We also view the bank’s excess capital as supportive of further shareholder returns via buybacks and dividends while also providing for additional investments in growth. Competitors : Goldman Sachs Weight in Club portfolio : 3.5% Most recent buy : Oct. 18, 2023 Initiated : July 12, 2021 Segments Institutional Securities in the third quarter benefited from strong international performance, with management calling out an acceleration in activity exiting the quarter, indicating the fourth quarter was also off to a strong start. In line with our thesis, CEO Ted Pick noted on the call that “a broadening equity market and evolving interest rate policy are favorable backdrops for our markets businesses.” Morgan Stanley’s large footprint allowed the firm to benefit from “shifting expectations around the size and timing of the Fed’s first rate cut” during the quarter, the change in monetary policy at the Bank of Japan and Chinese stimulus. Investment banking saw a pick-up in equity underwriting due to higher IPO activity and fixed income underwriting increased significantly from a year ago. Wealth management reported record revenue and a record pre-tax profit. Net new assets in the quarter were about $64 billion, well above the $53.5 billion expected and brings year-to-date net new assets to $195 billion, a 5% annualized increase versus where we started the year. Yeshaya said that “year-to-date flows are on pace to exceed last year, supported by an ongoing contribution of assets from advisor-led brokerage accounts to fee-based accounts.” The CFO expects net interest income “to be modestly down from the third quarter results largely on the back of lower rate expectations consistent with the forward curve.” That’s not too much of a concern given the Street has been looking for about $1.73 billion of net interest income in the current quarter. The pre-tax profit margin of 28.3%, a key watch item for investors given the increased focus on fee-based performance, outpaced the 26.8% consensus estimate and represents a very strong sequential increase versus the 26.8% we saw in the prior quarter. Investment management got a boost from higher asset management and related fees, which came on the back of an increase in assets under management. On the call, Yeshaya highlighted the benefits of the prior acquisition of Eaton Vance. (Jim Cramer’s Charitable Trust is long MS, WFC. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Bing Guan | Bloomberg | Getty Images

Morgan Stanley shares soared to all-time highs Wednesday after third-quarter beats on the bank’s top and bottom lines, with strength seen across the board.

Morgan Stanley on Wednesday topped analysts’ estimates for third-quarter profit as each of its three main divisions generated more revenue than expected.

Here’s what the company reported:

Earnings:$1.88 a share vs $1.58 LSEG estimate

Revenue: $15.38 billion vs. $14.41 billion estimate

The bank said profit rose 32% to $3.2 billion, or $1.88 per share, and revenue jumped 16% to $15.38 billion.

Morgan Stanley had several tail winds in its favor, starting with buoyant markets that helped its massive wealth management business, a rebound in investment banking after a dismal 2023, and strong trading activity. The Federal Reserve began taking down rates in the quarter, which should encourage more of the financing and merger activity that Wall Street firms capitalize on.

“The firm reported a strong third quarter in a constructive environment across our global footprint,” Morgan Stanley CEO Ted Pick said in the release.

Shares of the bank rose 7.5% in early trading.

The bank’s wealth management division saw revenue jump 14% from a year earlier to $7.27 billion, exceeding the StreetAccount estimate by nearly $400 million.

Equity trading revenue rose 21% to $3.05 billion, compared with the $2.77 billion estimate, while fixed income revenue edged 3% higher to $2 billion, also higher than the $1.85 billion estimate.

Investment banking revenue surged 56% from a year earlier to $1.46 billion, exceeding the $1.36 billion estimate.

Investment management, the firm’s smallest division, also exceeded expectations, posting a 9% increase in revenue to $1.46 billion, modestly higher than the $1.42 billion estimate.

Morgan Stanley’s Wall Street rivals also posted better-than-expected Wall Street revenue. JPMorgan Chase, Goldman Sachs and Citigroup topped estimates on strong revenue from trading and investment banking.

This story is developing. Please check back for updates.

It’s been a stellar month for the U.S. stock market, driven largely by easing monetary policy. Since the Club’s last Monthly Meeting, investors have celebrated the Federal Reserve’s pivot to its rate-cutting era. The U.S. central bank announced its first interest rate reduction in more than four years on Sept. 18, sending stock benchmarks to all-time highs. Most recently, the S & P 500 and Dow Jones Industrial Average both closed at record levels Monday. The S & P and Dow are up 4.5% and 4%, respectively, since the Sept. 12 monthly gathering. We’ve taken advantage of the market highs. The rate cutting news sent Meta Platforms , Alphabet and Danaher higher, encouraging us to offload shares of each on Sept. 26 in an overbought market. The Club also exited Procter & Gamble on Oct. 8. The reasoning: There’s less need to hold onto traditional defensive names like consumer staples while the Fed is embarking on an easing cycle. We did hold onto our rate-sensitive names like Wells Fargo and Morgan Stanley , which were among the best performers since the last Monthly Meeting. (We sold a little of the latter, more details below). The improving macro backdrop on the back of loosening policy bodes well for Meta Platforms too. Meanwhile, continued investments around generative artificial intelligence boosted shares of Salesforce and Eaton , which rounded out the top five. Here’s a breakdown of what drove gains in each of these five Club stocks since the market close of the September meeting through Tuesday’s close ahead of Wednesday’s October Monthly meeting at noon ET . 1. Wells Fargo: 22% This stock got a boost after the Fed enacted its first rate cut in mid-September, which lifted the entire financials sector. That’s because lower borrowing costs can benefit Wells Fargo by stabilizing its interest-based revenue streams. The firm’s net interest income (NII) took hits during the higher-for-long rate environment as customers sought to park cash in higher-yielding alternatives. It weighed on the bank’s loan growth as well. Wells Fargo’s solid quarterly earnings release on Oct. 11, and subsequent positive Wall Street commentary in the sessions that followed, sent the stock to multi-year highs. We hiked our price target to $66 apiece from $61 on earnings, and reiterated our buy-equivalent 1 rating on the stock. 2. Morgan Stanley: 16.2% Following the Fed’s decision, shares advanced as investors became more optimistic about a soft landing for the U.S. economy. Morgan Stanley benefits from lower rates — and, in turn, a better economy — because it can usher in more Wall Street dealmaking such as initial public offerings and mergers and acquisitions. That’s great news for the turnaround story in Morgan Stanley’s crucial investment banking division. To be sure, we made a small sale of the financial stock on Sept. 19 after its post-Fed pop. That’s because the Club has been debating exiting Morgan Stanley altogether for a potentially better investment banking rebound play like Goldman Sachs. However, we hope to get more clarity on Morgan Stanley’s standing in the portfolio when the firm reports quarterly results Wednesday. 3. Salesforce: 13.8% What caused the double-digit percentage jump in this tech stock? Two words: artificial intelligence. Salesforce hosted its Dreamforce Conference last month, where CEO Marc Benioff touted Agentforce, the company’s AI-enhanced chatbot tools. Shares had their biggest single-day jump in nearly four months, at 5.4%, on Sept. 19 after management detailed more about the flagship offering. A flurry of positive Wall Street chatter followed suit, extending the run even further. Piper Sandler upgraded the stock to a buy rating from neutral on Sept. 24. A week later, Northland Capital Markets also raised its rating on the software maker to a buy-equivalent rating from hold. 4. Meta Platforms: 11.5% The social media giant trended higher after investors saw the unveiling of the Quest 3S , the latest VR headset from the company at the social media giants annual developer conference on Sept. 25. The stock continued to climb on positive signs for the company’s advertising business, which prompted UBS to hike the stock’s price target to $690 apiece from $635. Guggenheim raised the company’s price target to $665 from $600. Analysts at the firm argued that Meta was the top destination for incremental ad dollars, citing recent channel checks. 5. Eaton: 11.3% This industrial name doesn’t have one single catalyst for its outperformance. But increasing data center investments on the back of increased AI adoption, accompanied by upbeat Wall Street research, likely contributed to the stock’s climb. On Sept. 16, Citigroup initiated coverage of Eaton as a buy, sending shares higher. Analysts argued that Eaton will continue to benefit from the buildout of data center facilities, which will in turn increase demand for the company’s power management solutions. Morgan Stanley reiterated its buy-equivalent rating on Oct. 10, arguing that Eaton has a positive setup into earnings season. That same session, analysts at JPMorgan maintained their buy rating on Eaton and increased its price target to $349 apiece from $325. The stock traded near all-time highs on Tuesday. (See here for a full list of the stocks in Jim Cramer’s Charitable Trust.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Traders work on the floor of the New York Stock Exchange.

Angela Weiss | AFP | Getty Images

It’s been a stellar month for the U.S. stock market, driven largely by easing monetary policy.

Wells Fargo CEO Charlie Scharf gave CNBC’s Jim Cramer a positive read on the consumer landscape.

“The consumer’s been extremely resilient,” he said. “We don’t sit here and say risks don’t exist — But what we see looks pretty, pretty strong.”

According to Scharf, consumer spend is going up “at a very measured pace” in both debit and credit cards. Deposit balances, he added, remain strong and credit quality is “still performing extremely well.” He praised the Federal Reserve, saying the central bank managed the economy well under difficult circumstances.

Wells Fargo’s most recent quarter topped Wall Street’s expectations, and shares surged more than 4% last Friday just after the report. The company managed a substantial earnings beat, even as its net interest income — a measure of banks’ lending revenue — declined. By Tuesday’s close, Wells Fargo was up 1.40%.

While Scharf said Wells Fargo does care about its quarterly results, he suggested the market can obsess over reports more than management does. He pointed out that the stock fell after last quarter but jumped after the most recent one — even though trends are “not dramatically different,” and strategies, as well as progress on building business hasn’t changed significantly.

Scharf also remained neutral when asked about what results of the upcoming presidential election could mean for business.

“We’re going to work with both sides,” he said. “I’m encouraged by what both candidates are saying about the way they want to interact with business.”

Jim Cramer’s Guide to Investing

Sign up now for the CNBC Investing Club to follow Jim Cramer’s every move in the market.

Disclaimer The CNBC Investing Club Charitable Trust holds shares of Wells Fargo.

David Solomon, Chairman & CEO Goldman Sachs, speaking on CNBC’s Squawk Box at the World Economic Forum Annual Meeting in Davos, Switzerland on Jan. 17th, 2024.

Adam Galici | CNBC

Goldman Sachs is scheduled to report third-quarter earnings before the opening bell Tuesday.

Here’s what Wall Street expects:

Earnings: $6.89 per share, according to LSEG

Revenue: $11.8 billion, according to LSEG

Trading Revenue: Fixed Income of $2.91 billion, Equities of $2.96 billion, per StreetAccount

Investing Banking Revenue: $1.62 billion, per StreetAccount

Asset & Wealth Management: $3.58 billion, per StreetAccount

How much will falling interest rates help Goldman Sachs?

Over the past two years, the Federal Reserve’s tightening campaign has made for a less-than-ideal environment for investment banks like Goldman.

Now that the Fed is easing rates, that positions Goldman to benefit as corporations that have waited on the sidelines to acquire competitors or raise funds begin to take action.

Goldman’s asset and wealth management division is also positioned to benefit from rising asset values across markets as rates decline.

Last week, rival JPMorgan Chase set expectations high with better-than-anticipated results from trading and investment banking, factors that helped the bank top earnings estimates.

Wells Fargo also exceeded estimates on Friday on the back of its investment banking division.

This story is developing. Please check back for updates.

Wells Fargo stock hit new multi-year highs on Monday after Wall Street analysts praised the bank’s third-quarter earnings report. The news Shares of Club name Wells Fargo jumped more than 3% on Monday — a close above $63 would be the highest finish since January 2018. That’s on top of Friday’s more than 5.6% post-earnings rally, which extended its recent run to six straight sessions. Investors are mulling a slew of positive analysts’ calls after Wells Fargo’s better-than-expected quarterly earnings . While missing on revenue, the bank impressed with a surge in fee-based income streams that offset weakness in other parts of the business. WFC 5Y mountain Wells Fargo 5 years In response, Barclays raised Wells Fargo’s price target to $75 apiece from $66 on Sunday, implying roughly 23% upside from Friday’s prior close. The analysts cited both “increased confidence of a soft landing” and “improvements in operational risk and compliance, which should ultimately lead to [the] removal of its asset cap,” which was imposed by the Federal Reserve in 2018 following misdeeds before Charlie Scharf took over as CEO. Barclays maintained its buy-equivalent rating on the financial name. Piper Sandler hiked its Wells Fargo price target slightly to $62 from $60. “We are keeping our neutral rating, but note that the story becomes more interesting as net interest income begins to find its bottom, the fee base gains momentum, and regulatory issues seem to move forward,” analysts wrote in a Friday note. Big picture Big bank earnings are off to a great start. Not only did Wells Fargo post solid results, but so did JPMorgan Chase . On Friday, the Jamie Dimon-led bank topped analysts’ expectations on earnings and revenue on continued strength in non-interest income streams. Wall Street behemoths including Bank of America, Citigroup and Goldman Sachs are set to post results before Tuesday’s bell. The Club’s other financial name, Morgan Stanley, releases earnings on Wednesday morning. Getting a look at Goldman Sachs’ quarter and then Morgan Stanley should be interesting. Although Jim has previously said the Club would rather be in Goldman than Morgan Stanley, we’re taking a wait-and-see approach to the stock. That’s because Morgan Stanley can turn things around if Wall Street dealmaking picks up and eventually boosts the firm’s investment banking business. Bottom line We’re not surprised that Wells Fargo’s getting the recognition it deserves. After the earnings release. the Club on Friday raised our price target on the bank to $66 per share from $62. We also reiterated our buy-equivalent 1 rating on the stock. “What an amazing quarter,” Jim Cramer said Monday. “Friday was Charlie Scharf’s day.” Similar to the Wall Street analysts, we’re upbeat on the progress Wells Fargo is making toward convincing the Fed to lift the $1.95 trillion asset cap. The removal of this growth lid is crucial to Wells Fargo’s turnaround story and a big reason why the Club invested in the stock in the first place. In fact, in Jim’s Sunday column , he argued that Wells Fargo’s earnings report may be the best of the batch so far. He said he was “astounded that Wells Fargo had been able to start changing its business model to the point where it was more of an investment bank” than previously thought. That’s why we do have one qualm with Piper Sandler’s commentary, in particular. We don’t agree with the research firm’s choice to leave the stock at a hold-equivalent rating. (Jim Cramer’s Charitable Trust is long WFC, MS. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Wells Fargo bank signage is seen on Broadway on April 12, 2024 in New York City.

Michael M. Santiago | Getty Images

Wells Fargo stock hit new multi-year highs on Monday after Wall Street analysts praised the bank’s third-quarter earnings report.

The good times are still rolling on Wall Street. An intensifying earnings season will put that momentum to the test. The S & P 500 ended Friday at a record high, buoyed by strong quarterly results from Club holding Wells Fargo and other major financial firms, which reinforced the idea of a healthy U.S. economy. The index posted its fifth positive week in a row, advancing 1.1%. Meanwhile, the Dow Jones Industrial Average rose 1.2% in the week and also closed Friday at an all-time high. The tech-heavy Nasdaq Composite gained 1.1% and now sits just 1.6% below its July peak. The third-quarter earnings calendar starts to get crowded in the coming days, featuring more major U.S. banks, health-care heavyweights and a few industrial and tech players. All eyes will be on the numbers and what executives have to say on their outlooks — just as it should be, according to Jim Cramer. When consumer price index for September came in a bit hotter than expected Thursday morning , Jim cautioned investors against sweating every line in every economic report. Keep your “eye on the prize,” he said. Right now, he said, that prize is “companies which are about to have earnings.” The high-level takeaway from the economic data in recent days is what matters most: Inflation is broadly trending down. The CPI in September showed an annual inflation rate of 2.4%, slightly above consensus but below the 2.5% figure seen in August. In Friday’s look at wholesale inflation, the producer price index was unchanged month over month . Economists had expected a 0.1% monthly gain. As the market marched back to records, we mostly sat tight. Exiting Procter & Gamble on Tuesday was our lone trade of the week. Simply put: a defensive stock like the maker of Crest toothpaste and Dawn soap didn’t seem right for the portfolio as the Federal Reserve embarks on an easing cycle and the economy remains on solid ground. Wells Fargo and JPMorgan reinforced that notion Friday with their earnings reports. Shares of both banks surged — Wells up 5.6%, JPMorgan up 4.4% — and helped the financial sector climb the S & P 500 leaderboard for the week. Tech led the way, up 2.5%, followed by industrials and financials, which added 2.1% and 1.8%, respectively. Utilities and communication services were the main laggards, losing 2.6% and 1.4%, respectively. In the week ahead, a number of influential companies are set to report including UnitedHealth and Goldman Sachs on Tuesday. ASML on Wednesday and Taiwan Semiconductor Manufacturing Co . on Thursday will provide a glimpse at the state of the AI trade before the megacap tech companies report later in the month and beyond. We’ll hear from Club holdings Morgan Stanley and Abbott Laboratories on Wednesday morning. Morgan Stanley: The ongoing recovery in investment banking will be front and center. That was a key theme in the second quarter , and the hope is that the July-to-September period showed a continuation of the trend for Morgan Stanley. An encouraging sign arrived Friday, with JPMorgan reporting a better-than-expected number for its investment banking segment. Shares of Morgan Stanley had suffered through a period of underperformance, leading Jim to openly question whether owning rival Goldman Sachs was a better idea. Morgan Stanley has been strong lately, though. The stock is up more than 14% over the past month and closed Friday at a record $110.91 a share. Morgan Stanley’s results Wednesday should hopefully add more clarity on our next move. Indications that its growing wealth management segment has found its footing would be welcome news. Abbott Labs: The medical products maker’s legal fight over its premature infant formula looks more manageable after a trio of U.S. health agencies recently pushed back against claims that formulas like Abbott’s cause an intestinal illness commonly abbreviated as NEC. To be sure, a second trial on the matter is ongoing in St. Louis, so Abbott Labs is not out of the woods just yet. Nevertheless, agencies including the Food and Drug Administration lending their support to the formulas is a big deal. “You clean up the lawsuits, [the stock] goes to $125,” Jim predicted Friday. The reason it would be so positive? Abbott’s strong fundamentals have been obscured by the legal issues. On that front, we’ll be looking for updates on the U.S. launch of Abbott’s over-the-counter continuous glucose monitoring systems and the state of its medical devices business overall. Weak points in the second quarter were nutrition and established pharmaceuticals, but even with them, Abbott has reported back-to-back beat-and-raise quarters. A third would be nice. Week ahead Monday, Oct.14 Before the bell: Charles Schwab (SCHW) Tuesday, Oct. 15 Before the bell: Walgreens Boots Alliance (WBA), UnitedHealth (UNH), Citigroup (C), Bank of America (BAC), Johnson & Johnson (JNJ) and Goldman Sachs (GS) After the bell: United Airlines (UAL), Interactive Brokers (IBKR) and JB Hunt (JBHT) Wednesday, Oct.16 Before the bell: Morgan Stanley (MS), Abbott Labs (ABT), ASML (ASML), US Bancorp (USB), Citizens (CFG) and Prologis (PLD) After the bell: Alcoa (AA), PPG Industries (PPG), CSX (CSX), Kinder Morgan (KMI), Discover (DFS) and Crown Castle (CCI) Thursday, Oct. 17 8:30 a.m. ET: Initial Jobless Claims 8:30 a.m. ET: Retail Sales 8:30 a.m. ET: Industrial Production & Capacity Utilization Before the bell: Taiwan Semi (TSM), Travelers (TRV), Elevance (ELV), Huntington Bancshares (HBAN), Blackstone (BX), Truist (TFC) and KeyCorp (KEY) After the bell: Netflix (NFLX), Intuitive Surgical (ISRG) and Crown Holdings (CCK) Friday, Oct. 18 8:30 a.m. ET: Housing Starts & Building Permits Before the bell: American Express (AXP), SLB (SLB) and Procter & Gamble (PG) (Jim Cramer’s Charitable Trust is long WFC, MS and ABT. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

A view of the New York Stock Exchange building in the Financial District in New York City on Aug. 5, 2024.

Charly Triballeau | Afp | Getty Images

The good times are still rolling on Wall Street. An intensifying earnings season will put that momentum to the test.

Former President Donald Trump and Vice President Kamala Harris face off in the ABC presidential debate on Sept. 10, 2024.

Getty Images

With the U.S. election less than a month away, the country and its corporations are staring down two drastically different options.

For airlines, banks, electric vehicle makers, health-care companies, media firms, restaurants and tech giants, the outcome of the presidential contest could result in stark differences in the rules they’ll face, the mergers they’ll be allowed to pursue, and the taxes they’ll pay.

During his last time in power, former President Donald Trump slashed the corporate tax rate, imposed tariffs on Chinese goods, and sought to cut regulation and red tape and discourage immigration, ideas he’s expected to push again if he wins a second term.

In contrast, Vice President Kamala Harris has endorsed hiking the tax rate on corporations to 28% from the 21% rate enacted under Trump, a move that would require congressional approval. Most business executives expect Harris to broadly continue President Joe Biden‘s policies, including his war on so-called junk fees across industries.

Personnel is policy, as the saying goes, so the ramifications of the presidential race won’t become clear until the winner begins appointments for as many as a dozen key bodies, including the Treasury, Justice Department, Federal Trade Commission, and Consumer Financial Protection Bureau.

CNBC examined the stakes of the 2024 presidential election for some of corporate America’s biggest sectors. Here’s what a Harris or Trump administration could mean for business:

The result of the presidential election could affect everything from what airlines owe consumers for flight disruptions to how much it costs to build an aircraft in the United States.

The Biden Department of Transportation, led by Secretary Pete Buttigieg, has taken a hard line on filling what it considers to be holes in air traveler protections. It has established or proposed new rules on issues including refunds for cancellations, family seating and service fee disclosures, a measure airlines have challenged in court.

“Who’s in that DOT seat matters,” said Jonathan Kletzel, who heads the travel, transportation and logistics practice at PwC.

The current Democratic administration has also fought industry consolidation, winning two antitrust lawsuits that blocked a partnership between American Airlines and JetBlue Airways in the Northeast and JetBlue’s now-scuttled plan to buy budget carrier Spirit Airlines.

The previous Trump administration didn’t pursue those types of consumer protections. Industry members say that under Trump, they would expect a more favorable environment for mergers, though four airlines already control more than three-quarters of the U.S. market.

On the aerospace side, Boeing and the hundreds of suppliers that support it are seeking stability more than anything else.

Trump has said on the campaign trail that he supports additional tariffs of 10% or 20% and higher duties on goods from China. That could drive up the cost of producing aircraft and other components for aerospace companies, just as a labor and skills shortage after the pandemic drives up expenses.

Tariffs could also challenge the industry, if they spark retaliatory taxes or trade barriers to China and other countries, which are major buyers of aircraft from Boeing, a top U.S. exporter.

Big banks such as JPMorgan Chase faced an onslaught of new rules this year as Biden appointees pursued the most significant slate of regulations since the aftermath of the 2008 financial crisis.

Those efforts threaten tens of billions of dollars in industry revenue by slashing fees that banks impose on credit cards and overdrafts and radically revising the capital and risk framework they operate in. The fate of all of those measures is at risk if Trump is elected.

Trump is expected to nominate appointees for key financial regulators, including the CFPB, the Securities and Exchange Commission, the Office of the Comptroller of the Currency and Federal Deposit Insurance Corporation that could result in a weakening or killing off completely of the myriad rules in play.

“The Biden administration’s regulatory agenda across sectors has been very ambitious, especially in finance, and large swaths of it stand to be rolled back by Trump appointees if he wins,” said Tobin Marcus, head of U.S. policy at Wolfe Research.

Bank CEOs and consultants say it would be a relief if aspects of the Biden era — an aggressive CFPB, regulators who discouraged most mergers and elongated times for deal approvals — were dialed back.

“It certainly helps if the president is Republican, and the odds tilt more favorably for the industry if it’s a Republican sweep” in Congress, said the CEO of a bank with nearly $100 billion in assets who declined to be identified speaking about regulators.

Still, some observers point out that Trump 2.0 might not be as friendly to the industry as his first time in office.

Trump’s vice presidential pick, Sen. JD Vance, of Ohio, has often criticized Wall Street banks, and Trump last month began pushing an idea to cap credit card interest rates at 10%, a move that if enacted would have seismic implications for the industry.

Bankers also say that Harris won’t necessarily cater to traditional Democratic Party ideas that have made life tougher for banks. Unless Democrats seize both chambers of Congress as well as the presidency, it may be difficult to get agency heads approved if they’re considered partisan picks, experts note.

“I would not write off the vice president as someone who’s automatically going to go more progressive,” said Lindsey Johnson, head of the Consumer Bankers Association, a trade group for big U.S. retail banks.

Electric vehicles have become a polarizing issue between Democrats and Republicans, especially in swing states such as Michigan that rely on the auto industry. There could be major changes in regulations and incentives for EVs if Trump regains power, a fact that’s placed the industry in a temporary limbo.

“Depending on the election in the U.S., we may have mandates; we may not,” Volkswagen Group of America CEO Pablo Di Si said Sept. 24 during an Automotive News conference. “Am I going to make any decisions on future investments right now? Obviously not. We’re waiting to see.”

Republicans, led by Trump, have largely condemned EVs, claiming they are being forced upon consumers and that they will ruin the U.S. automotive industry. Trump has vowed to roll back or eliminate many vehicle emissions standards under the Environmental Protection Agency and incentives to promote production and adoption of the vehicles.

If elected, he’s also expected to renew a battle with California and other states who set their own vehicle emissions standards.

“In a Republican win … We see higher variance and more potential for change,” UBS analyst Joseph Spak said in a Sept. 18 investor note.

In contrast, Democrats, including Harris, have historically supported EVs and incentives such as those under the Biden administration’s signature Inflation Reduction Act.

Harris hasn’t been as vocal a supporter of EVs lately amid slower-than-expected consumer adoption of the vehicles and consumer pushback. She has said she does not support an EV mandate such as the Zero-Emission Vehicles Act of 2019, which she cosponsored during her time as a senator, that would have required automakers to sell only electrified vehicles by 2040. Still, auto industry executives and officials expect a Harris presidency would be largely a continuation, though not a copy, of the past four years of Biden’s EV policy.

They expect some potential leniency on federal fuel economy regulations but minimal changes to the billions of dollars in incentives under the IRA.

Both Harris and Trump have called for sweeping changes to the costly, complicated and entrenched U.S. health-care system of doctors, insurers, drug manufacturers and middlemen, which costs the nation more than $4 trillion a year.

Despite spending more on health care than any other wealthy country, the U.S. has the lowest life expectancy at birth, the highest rate of people with multiple chronic diseases and the highest maternal and infant death rates, according to the Commonwealth Fund, an independent research group.

Meanwhile, roughly half of American adults say it is difficult to afford health-care costs, which can drive some into debt or lead them to put off necessary care, according to a May poll conducted by health policy research organization KFF.

Both Harris and Trump have taken aim at the pharmaceutical industry and proposed efforts to lower prescription drug prices in the U.S., which are nearly three times higher than those seen in other countries.

But many of Trump’s efforts to lower costs have been temporary or not immediately effective, health policy experts said. Meanwhile, Harris, if elected, can build on existing efforts of the Biden administration to deliver savings to more patients, they said.

Harris specifically plans to expand certain provisions of the IRA, part of which aims to lower health-care costs for seniors enrolled in Medicare. Harris cast the tie-breaking Senate vote to pass the law in 2022.

Her campaign says she plans to extend two provisions to all Americans, not just seniors: a $2,000 annual cap on out-of-pocket drug spending and a $35 limit on monthly insulin costs.

Harris also intends to accelerate and expand a provision allowing Medicare to directly negotiate drug prices with manufacturers for the first time. Drugmakers fiercely oppose those price talks, with some challenging the effort’s constitutionality in court.

Trump hasn’t publicly indicated what he intends to do about IRA provisions.

Some of Trump’s prior efforts to lower drug prices “didn’t really come into fruition” during his presidency, according to Dr. Mariana Socal, a professor of health policy and management at the Johns Hopkins Bloomberg School of Public Health.

For example, he planned to use executive action to have Medicare pay no more than the lowest price that select other developed countries pay for drugs, a proposal that was blocked by court action and later rescinded.

Trump also led multiple efforts to repeal the Affordable Care Act, including its expansion of Medicaid to low-income adults. In a campaign video in April, Trump said he was not running on terminating the ACA and would rather make it “much, much better and far less money,” though he has provided no specific plans.

He reiterated his belief that the ACA was “lousy health care” during his Sept. 10 debate with Harris. But when asked he did not offer a replacement proposal, saying only that he has “concepts of a plan.”

Top of mind for media executives is mergers and the path, or lack thereof, to push them through.

The media industry’s state of turmoil — shrinking audiences for traditional pay TV, the slowdown in advertising, and the rise of streaming and challenges in making it profitable — means its companies are often mentioned in discussions of acquisitions and consolidation.

While a merger between Paramount Global and Skydance Media is set to move forward, with plans to close in the first half of 2025, many in media have said the Biden administration has broadly chilled deal-making.

“We just need an opportunity for deregulation, so companies can consolidate and do what we need to do even better,” Warner Bros. Discovery CEO David Zaslav said in July at Allen & Co.’s annual Sun Valley conference.

Media mogul John Malone recently told MoffettNathanson analysts that some deals are a nonstarter with this current Justice Department, including mergers between companies in the telecommunications and cable broadband space.

Still, it’s unclear how the regulatory environment could or would change depending on which party is in office. Disney was allowed to acquire Fox Corp.’s assets when Trump was in office, but his administration sued to block AT&T’s merger with Time Warner. Meanwhile, under Biden’s presidency, a federal judge blocked the sale of Simon & Schuster to Penguin Random House, but Amazon’s acquisition of MGM was approved.

“My sense is, regardless of the election outcome, we are likely to remain in a similar tighter regulatory environment when looking at media industry dealmaking,” said Marc DeBevoise, CEO and board director of Brightcove, a streaming technology company.

When major media, and even tech, assets change hands, it could also mean increased scrutiny on those in control and whether it creates bias on the platforms.

“Overall, the government and FCC have always been most concerned with having a diversity of voices,” said Jonathan Miller, chief executive of Integrated Media, which specializes in digital media investment. “But then [Elon Musk’s purchase of Twitter] happened, and it’s clearly showing you can skew a platform to not just what the business needs, but to maybe your personal approach and whims,” he said.

Since Musk acquired the social media platform in 2022, changing its name to X, he has implemented sweeping changes including cutting staff and giving “amnesty” to previously suspended accounts, including Trump’s, which had been suspended following the Jan. 6, 2021, Capitol insurrection. Musk has also faced widespread criticism from civil rights groups for the amplification of bigotry on the platform.

Musk has publicly endorsed Trump, and was recently on the campaign trail with the former president. “As you can see, I’m not just MAGA, I’m Dark MAGA,” Musk said at a recent event. The billionaire has raised funds for Republican causes, and Trump has suggested Musk could eventually play a role in his administration if the Republican candidate were to be reelected.

During his first term, Trump took a particularly hard stance against journalists, and pursued investigations into leaks from his administration to news organizations. Under Biden, the White House has been notably more amenable to journalists.

Also top of mind for media executives — and government officials — is TikTok.

Lawmakers have argued that TikTok’s Chinese ownership could be a national security risk.

Earlier this year, Biden signed legislation that gives Chinese parent ByteDance until January to find a new owner for the platform or face a U.S. ban. TikTok has said the bill, the Protecting Americans From Foreign Adversary Controlled Applications Act, which passed with bipartisan support, violates the First Amendment. The platform has sued the government to stop a potential ban.

While Trump was in office, he attempted to ban TikTok through an executive order, but the effort failed. However, he has more recently switched to supporting the platform, arguing that without it there’s less competition against Meta’s Facebook and other social media.

Both Trump and Harris have endorsed plans to end taxes on restaurant workers’ tips, although how they would do so is likely to differ.

The food service and restaurant industry is the nation’s second-largest private-sector employer, with 15.5 million jobs, according to the National Restaurant Association. Roughly 2.2 million of those employees are tipped servers and bartenders, who could end up with more money in their pockets if their tips are no longer taxed.

Trump’s campaign hasn’t given much detail on how his administration would eliminate taxes on tips, but tax experts have warned that it could turn into a loophole for high earners. Claims from the Trump campaign that the Republican candidate is pro-labor have clashed with his record of appointing leaders to the National Labor Relations Board who have rolled back worker protections.

Meanwhile, Harris has said she’d only exempt workers who make $75,000 or less from paying income tax on their tips, but the money would still be subject to taxes toward Social Security and Medicare, the Washington Post previously reported.

In keeping with the campaign’s more labor-friendly approach, Harris is also pledging to eliminate the tip credit: In 37 states, employers only have to pay tipped workers the minimum wage as long as that hourly wage and tips add up to the area’s pay floor. Since 1991, the federal pay floor for tipped wages has been stuck at $2.13.

“In the short term, if [restaurants] have to pay higher wages to their waiters, they’re going to have to raise menu prices, which is going to lower demand,” said Michael Lynn, a tipping expert and Cornell University professor.

Whichever candidate comes out ahead in November will have to grapple with the rapidly evolving artificial intelligence sector.

Generative AI is the biggest story in tech since the launch of OpenAI’s ChatGPT in late 2022. It presents a conundrum for regulators, because it allows consumers to easily create text and images from simple queries, creating privacy and safety concerns.

Harris has said she and Biden “reject the false choice that suggests we can either protect the public or advance innovation.” Last year, the White House issued an executive order that led to the formation of the Commerce Department’s U.S. AI Safety Institute, which is evaluating AI models from OpenAI and Anthropic.

Trump has committed to repealing the executive order.

A second Trump administration might also attempt to challenge a Securities and Exchange Commission rule that requires companies to disclose cybersecurity incidents. The White House said in January that more transparency “will incentivize corporate executives to invest in cybersecurity and cyber risk management.”

Trump’s running mate, Vance, co-sponsored a bill designed to end the rule. Andrew Garbarino, the House Republican who introduced an identical bill, has said the SEC rule increases cybersecurity risk and overlaps with existing law on incident reporting.

Also at stake in the election is the fate of dealmaking for tech investors and executives.

With Lina Khan helming the FTC, the top tech companies have been largely thwarted from making big acquisitions, though the Justice Department and European regulators have also created hurdles.

Tech transaction volume peaked at $1.5 trillion in 2021, then plummeted to $544 billion last year and $465 billion in 2024 as of September, according to Dealogic.

Many in the tech industry are critical of Khan and want her to be replaced should Harris win in November. Meanwhile, Vance, who worked in venture capital before entering politics, said as recently as February — before he was chosen as Trump’s running mate — that Khan was “doing a pretty good job.”

Khan, whom Biden nominated in 2021, has challenged Amazon and Meta on antitrust grounds and has said the FTC will investigate AI investments at Alphabet, Amazon and Microsoft.

Wells Fargo extended its recent winning streak to six straight sessions Friday despite missed expectations on third-quarter revenue. Investors focused instead on the bank running leaner and generating better-than-expected profitability. Total revenue for the three months ended Sept. 30 fell 2.4% versus last year, to $20.37 billion, missing analysts’ expectations of $20.42 billion, according to LSEG. Wells Fargo reported results before Friday’s opening bell. Earnings of $1.52 per share, however, was above Wall Street’s consensus estimate of $1.28 per share, LSEG data showed. Adjusted EPS excluded a 10-cent-per-share hit due to “losses on debt securities related to a repositioning of the investment securities portfolio.” That said, even before the adjustment, the reported EPS of $1.42, still looks good versus expectations. As for guidance , it was a bit mixed. However, the more important factor is that management believes net interest income (NII) pressure resulting from interest rate dynamics is bottoming out and expects it to rebound in 2025. WFC YTD mountain Wells Fargo YTD Shares of Wells Fargo surged 6% on the release to more than $61. That’s just shy of their 52-week high of $62.55 back in May, which was also the highest level since January 2018. Bottom line We’re raising our price target on the stock to $66 per share from $62 and reiterating our buy-equivalent 1 rating . The reasons are three-fold: We like the efficiency gains at the bank; the progress being made to get the Federal Reserve-imposed asset cap lifted; and the optimistic outlook for the economy and inflation. Commentary Wells Fargo’s quarterly revenue disappointed as net interest income came up short due to a miss in the bank’s net interest margin (NIM) as both loan and deposits were a bit lower than expected. That’s the bad. The good, however, more than offsets those misses. Non-interest income, or fee-based income, which has been a major focus for the Street, advanced nearly 12% year over year and exceeded expectations. Fee-based income growth is a major factor in our investment thesis as it is more predictable and allows the bank to be less at the mercy of interest rate dynamics that it can’t control. Wells Fargo Why we own it : We bought Wells Fargo as a turnaround story under CEO Charlie Scharf. He’s been making progress cleaning up the bank’s act and fixing its previously bloated cost structure after a series of misdeeds before his tenure. Scharf has also been working to get the Fed’s $1.95 trillion asset cap lifted and to boost Wells Fargo’s fee-generating revenue streams. Competitors : Bank of America and Citigroup Weight in Club portfolio : 4.76% Most recent buy : Aug. 7, 2024 Initiated : Jan. 8, 2021 CEO Charles Scharf kicked off his prepared remarks on the conference call by saying, “Our earnings profile is very different than it was five years ago, as we’ve been making strategic investments in many of our businesses and deemphasizing or selling others. Our revenue sources are more diverse, and our fee-based revenue has grown 16% during the first nine months of the year, largely offsetting the net interest income headwinds we have faced over the last year.” Wells Fargo’s overall efficiency ratio was also below expectations. That’s a positive as this is calculated by dividing total non-interest expenses by net revenue — so, the lower the ratio, the more efficiently the bank is operating. At the same time, the firm’s common equity tier 1 (CET) ratio — which compares a bank’s capital against its risk-weighted assets — was above expectations, indicating that Wells Fargo still has plenty of excess capital to reinvest in the business while still returning cash to shareholders. During Q3, management returned $3.5 billion to shareholders via buybacks and another $1.4 billion via dividends. Tangible book value per share (TBVPS) came in well ahead of expectations, increasing nearly 12% year over year, as did return on tangible common equity (ROTCE), a key metric that investors rely on to determine the appropriate valuation multiple to put on a financial institution. Higher level, indicating resilience in the broader U.S. economy Scharf said on the call, “Customers in our consumer businesses continue to hold up relatively well, benefiting from the strong labor market and wage growth. … We continue to look for changes in consumer health, but we have not seen meaningful changes in trends when looking at delinquency statistics across our consumer credit portfolios. Both credit card and debit card spend were up in the third quarter from a year ago. And although the pace of growth has slowed, it is still healthy. … The benefits of inflation slowing and interest rates starting to ease should be helpful to all customers but especially those on the lower end of the income scale.” Scharf added, “Looking ahead, overall, the U.S. economy remains strong with inflation slowing and a resilient labor market, boosting income and supporting consumer spending. Company balance sheets are strong, contributing to both consumption and investment in the economy but slowing demand for commercial lending. We continue to be prepared for a variety of economic environments, and we’ll balance our desire to increase returns and grow while protecting the downside.” Bank earnings are especially important for investors to focus on because of all the money and business that flows through these big institutions. Management teams like Wells Fargo’s are uniquely positioned to opine not only on the path ahead for their businesses but the economy more broadly. We come away from the call feeling good not only about Wells Fargo’s setup for next year. As Scharf continues to clean-up Wells Fargo after misdeeds that predated his tenure, we could see the bank’s $1.95 trillion asset cap lifted in 2025. That would allow the bank to grow its balance sheet and return more capital to shareholders. In advance of the asset-cap decision, Scharf has been ramping up Wells Fargo’s corporate and investment banking (CIB) division. He made a series of senior-level hires in recent years. A resurgence in Wall Street dealmaking — both mergers and acquisitions and initial public offerings — will benefit Wells Fargo. Our other financial name Morgan Stanley, which reports earnings next Wednesday, stands to gain even more from dealmaking because a greater percentage of its revenue is tied to investment banking. Guidance Wells Fargo’s management team updated its outlook for the remainder of the year, now expecting NII to be down about 9% versus the $52.4 billion result we saw in 2023. That puts us at the higher end of the down 8% to 9% range previously provided. A decline of 9% would mean roughly $47.66 billion in NII, below the $48.99 billion expected, according to FactSet. The update isn’t all that surprising given what we’ve seen with rates this year. More important is the team’s commentary that they still expect to see NII to trough this year before rebounding in 2025. NII in the current (fourth) quarter is expected to be in line with the third quarter result, which is what one would expect to see right before a rebound. (Jim Cramer’s Charitable Trust is long WFC. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Jim Cramer has been considering a potential investment in BlackRock, the world’s largest asset manager, and we’re now adding it to our Bullpen stocks-to-watch list. The news BlackRock shares surged to a record high Friday after the firm posted third-quarter earnings that crushed analysts’ expectations, yet again. Management also announced that assets under management reached another record high, an incredible $11.5 trillion, on surging inflows as the stock market rallied. “We’ve added $2 trillion organically over the last five years. $2 trillion is the equivalent of being in the ranks of the sixth largest asset managers,” CEO Larry Fink told CNBC on Friday after the release. Fink also praised BlackRock’s recent $12.5 billion acquisition of Global Infrastructure Partners, which added more than $100 billion in assets. Big picture The financial industry kicked off quarterly earnings Friday. In addition to BlackRock, Club name Wells Fargo was among the companies that delivered strong results. Morgan Stanley , also in the portfolio, reports next Wednesday. It’s been a murky operating environment for the Wall Street behemoths, which were forced to navigate higher-for-longer interest rates until the Federal Reserve finally cut rates last month. The Fed’s next move has been a point of debate. Right after last month’s jumbo 50-basis-point cut, the market had expected another 75 basis points worth of cuts before year-end. Now that odds favor just 50. Bottom line BlackRock’s stellar quarterly results highlight another reason for the Club to consider an initiation of the stock. That’s why we put the stock in the Bullpen. Management’s track record draws us in further as Fink expands the firm’s footprint in private markets, and delivers quarter after quarter of steller inflows. BlackRock shares have been on a tear recently – up more than 12% in the past month versus the S & P 500’s roughly 4% gain. Jim Cramer said Friday he knows the stock has run a lot, “but that doesn’t mean it can’t run more.” Why have we waited to pull the trigger on the stock? Jim said Thursday he wished he had but he’s been dealing with Wells Fargo and Morgan Stanley, and we don’t make these moves in haste. (Jim Cramer’s Charitable Trust is long MS, WFC. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

BlackRock CEO Larry Fink speaks during the New York Times DealBook Summit Nov. 30, 2022 in New York City.

Michael M. Santiago | Getty Images News | Getty Images

Jim Cramer has been considering a potential investment in BlackRock, the world’s largest asset manager, and we’re now adding it to our Bullpen stocks-to-watch list.

Every weekday the CNBC Investing Club with Jim Cramer holds a “Morning Meeting” livestream at 10:20 a.m. ET. Here’s a recap of Friday’s key moments. U.S. stocks jumped Friday, with the S & P 500 on pace for its fifth straight week of gains. The government’s producer price index was cooler than expected, one day after a slightly hotter consumer price index. Bank earnings are the star of the show. During the Club’s Morning Meeting, Jim Cramer said Wall Street is “starting earnings season off with a bang.” Club stock Wells Fargo rose more than 5.5% after quarterly profit exceeded estimates. Check your email inboxes and your texts shortly for our full Wells Fargo earnings commentary. Jim said he would like to buy some more Advanced Micro Devices if he weren’t restricted due to the Club’s trading rules. AMD dropped 1% on Wednesday and then another 4% on Thursday following its Advancing AI meeting. Melius Research said the stock sold off because the market wanted to see another cloud giant in attendance. Jim said the AMD slide was a bit unfair because Jensen Huang, CEO of AI chip leader Nvidia CEO, sucked all the oxygen out of the room during a three-day roadshow. Palo Alto Networks stock is having a great week, up 10% through early Friday, and our best weekly performer. Morgan Stanley raised its price target on the cybersecurity stock to $421 per share from $390. That implies 14% upside from Thursday’s close. We battled the stock, buying some on the dip in early August and then taking some profits later in the month. Jim has been considering adding cyber rival CrowdStrike to the portfolio, pointing out that Bullpen name CrowdStrike didn’t lose customers after its glitch caused a worldwide IT outage in July. Stocks covered in Friday’s rapid fire at the end of the video were: JPMorgan , BlackRock , Tesla , Affirm , and Ferrari . (Jim Cramer’s Charitable Trust is long WFC, AMD, PANW. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Every weekday the CNBC Investing Club with Jim Cramer holds a “Morning Meeting” livestream at 10:20 a.m. ET. Here’s a recap of Friday’s key moments.

For a decade now, big acquisitions by Canadian oil-and-gas producers have mostly been met with distaste by investors. So we’ll take it as a heartening sign how well the markets received Canadian Natural Resources’ (CNQ/TSX) decision to buy the Alberta upstream assets of Chevron Corp. (CVX/NYSE) for USD$6.5 billion in cash. CNQ stock rose 3.7% Monday in the wake of the announcement. Chevron was up 0.7% on a day when oil prices increased.

The assets in question comprise a 20% stake in the Athabasca Oil Sands Project, along with 70% of the Kaybob Duvernay shale play. That should add 122,500 barrels of oil equivalent per day to Canadian Natural Resource’s 2025 output, the company said. It also announced a 7% bump to its quarterly dividend, to 56.25 Canadian cents a share, beginning in January.

Chevron explained the asset sale in terms of freeing up cash for U.S. shale acquisitions as well as targeted positions abroad, such as in Kazakhstan, which it considers to hold better long-term profit potential.

Canada’s best dividend stocks

Nvidia moves up to number 2 in market cap

Reports of the death of the Magnificent 7 tech stocks’ decade-long run are greatly exaggerated, Nvidia (NVDA/Nasdaq) seemed to say this week as its shares rose past $130. (All figures in U.S. dollars.) That pushed its market capitalization ahead of Microsoft Corp. to $3.19 trillion. That leaves only Apple, with a market cap of $3.4 trillion, worth more than the AI-focused chip-maker.

Nvidia’s stock is up 26% in the past month, compared to a 6% advance for the S&P 500. Nvidia has grown tenfold in just two years. The price movement this week appeared to come from a positive report from Super Micro Computer, a provider of advanced server products and services. It found that sales of its liquid cooling products, deployed alongside Nvidia’s graphics processing units (GPUs), would be even stronger than expected this quarter. Analyst estimates of Nvidia’s adjusted EBITDA (earnings before interest, taxes, depreciation and amortization) for the three-month period ended this month is $21.9 billion.

The best online brokers in Canada

Pepsi earnings leave a sour taste

Posting its second straight disappointing set of quarterly results on Tuesday, beverage-and-snack maker PepsiCo lowered its full-year guidance for organic revenue unrelated to acquisitions.

Results were hampered by recalls of the company’s Quaker Foods products, related to potential salmonella contamination. PepsiCo also experienced weak demand in the U.S. and business disruptions in some overseas markets, such as the Middle East. Pepsi’s North American beverage volumes fell 3% year-over-year, mostly due to declines in energy drink sales. Meanwhile, its Frito-Lay division suffered a 1.5% decline.

“After outperforming packaged food categories in previous years, salty and savory snacks have underperformed year-to-date,” executives said in a prepared statement. Overall, PepsiCo revised its 2024 sales growth outlook from the previous 4% to low single digits.

Mobile homes surrounded by flood water after Hurricane Milton made landfall, in St. Petersburg, Florida, U.S. October 10, 2024.

Octavio Jones | Reuters

If your home is temporarily uninhabitable after a natural disaster, a provision in your homeowners or renters insurance policy may help you with new lodging and other living expenses.

Insured wind and flood damage from Hurricane Helene is estimated to be up to $17.5 billion, according to CoreLogic, a real estate data site. Insured losses from Hurricane Milton could range from $30 billion to $60 billion, per Morningstar DBRS.

Homeowners and renters affected by a natural disaster can ask about so-called “loss of use” or “additional living expenses” coverage from their insurance providers, experts say.

The provision is meant to help cover reasonable living expenses if your home is not suitable to live in as a result of a covered peril such as a hurricane, fire or burst pipe.

“I don’t know of any homeowners policy that doesn’t have it already there,” said Karl Susman, president and principal insurance agent of Susman Insurance Services, Inc. in Los Angeles.

As you file a claim, it will be important to ask your insurance company about the loss of use coverage and how quickly it can kick in, said Shannon Martin, a licensed insurance agent and analyst at Bankrate.com.

“If you call your carrier, they might be able to expedite the loss of use claim filing for you and issue a check early so that you’re not stuck trying to figure out how to pay for separate housing,” she said.

Here’s what the coverage is and what to consider before you use it, according to experts.

Loss of use coverage is a provision that is typically included in your homeowners insurance policy. It’s usually about 20% of the dwelling coverage and is paid out in the event that the home becomes uninhabitable and a policyholder needs funds for living expenses while the home is repaired or rebuilt, experts say. Eligible expenses might include a hotel or rental home, food, pet boarding or storage fees, among others.

For example, if you’re ensuring a house for $100,000, and that’s what it costs to rebuild the house, that is considered the dwelling coverage, Susman said.

“Then the policy would automatically come with $20,000 in coverage for loss of use,” he said.

“That way you and your family can pay for your hotel and pay for food, because you might be separated from your home for an extended period of time,” Martin said.