[ad_1]

CORRECT: Services sector of U.S. economy remained strong in September

[ad_2]

[ad_1]

The Republican Party has an edge again in the generic ballot, and that advantage has reached a level last seen in late July, according to a RealClearPolitics average for that closely watched indicator.

That could be another sign that the GOP may be getting back some momentum as November’s midterm elections approach, after Democratic prospects improved during the summer.

Republicans are now scoring 46.0% support in the RCP average of generic ballots, a percentage point ahead of Democrats at 45.0%.

The GOP hit a 1-point edge last Wednesday, then saw a dip, but as of Tuesday was back at that level, as shown in the chart below.

It’s not a big advantage, but it’s the best showing for Republicans in RCP’s data for generic ballots since July 28, as Democrats had the advantage for much of August and September.

Related: If this seat flips red, Republicans will have ‘probably won a relatively comfortable House majority’

Also read: ‘Republican control of the House is not a foregone conclusion,’ says political analyst

The generic ballot refers to a poll question that asks voters which party they would support in a congressional election without naming individual candidates. Analysts tend to see it as a useful indicator.

Other websites focused on political analysis and forecasting, such as FiveThirtyEight, still show Democrats with an edge in their data for generic ballots.

Election Day for the midterm contests is now five weeks away. Democrats have focused their campaigns on abortion rights after the Supreme Court’s June decision that overturned Roe v. Wade, while Republicans have seized on Americans’ frustration with high inflation.

The additional chart below is interactive and shows RCP’s data for the generic ballot over a longer time frame.

And see: New poll finds just 30% of Americans approve of how Biden is handling inflation

[ad_2]

[ad_1]

When the stock market has jumped two days in a row, as it has now, it is easy to become complacent.

But the Federal Reserve isn’t finished raising interest rates, and recession talk abounds. Stock investors aren’t out of the woods yet. That can make dividend stocks attractive if the yields are high and the companies produce more cash flow than they need to cover the payouts.

Below is a list of 21 stocks drawn from the S&P Composite 1500 Index

SP1500,

that appear to fit the bill. The S&P Composite 1500 is made up of the S&P 500

SPX,

the S&P 400 Mid Cap Index

MID,

and the S&P Small Cap 600 Index

SML,

The purpose of the list is to provide a starting point for further research. These stocks may be appropriate for you if you are looking for income, but you should do your own assessment to form your own opinion about a company’s ability to remain competitive over the next decade.

One way to measure a company’s ability to pay dividends is to look at its free cash flow yield. Free cash flow is remaining cash flow after planned capital expenditures. This money can be used to pay for dividends, buy back shares (which can raise earnings and cash flow per share), or fund acquisitions, organic expansion or for other corporate purposes.

If we divide a company’s estimated annual free cash flow per share by its current share price, we have its estimated free cash flow yield. If we compare the free cash flow yield to the current dividend yield, we may see “headroom” for cash to be deployed in ways that can benefit shareholders.

For this screen, we began with the S&P Composite 1500, then narrowed the list as follows:

For real-estate investment trusts, dividend-paying ability is measured by funds from operations (FFO), a non-GAAP figure that adds depreciation and amortization back to earnings. Adjusted funds from operations (AFFO) takes this a step further, subtracting cash expected to be used to maintain properties. So for the two REITs on the list, the FCF yield column makes use of AFFO.

For many companies in the financial sector, especially banks and insurers, free cash flow figures aren’t available, so the screen made use of earnings-per-share estimates. These are generally considered to run close to actual cash flow for these heavily regulated industries.

Here are the 21 companies that passed the screen, with dividend yields of at least 5% and estimated 2023 FCF yields at least twice the current payout. They are sorted by dividend yield:

| Company | Ticker | Type | Dividend yield | Estimated 2023 FCF yield | Estimated “headroom” |

| Uniti Group Inc. |

UNIT, |

Real-Estate Investment Trusts | 8.33% | 25.25% | 16.92% |

| Hanesbrands Inc. |

HBI, |

Apparel/ Footwear | 8.33% | 17.29% | 8.96% |

| Kohl’s Corp. |

KSS, |

Department Stores | 7.68% | 16.72% | 9.04% |

| Rent-A-Center Inc. |

RCII, |

Finance/ Rental/ Leasing | 7.52% | 17.26% | 9.73% |

| Macerich Co. |

MAC, |

Real-Estate Investment Trusts | 7.43% | 18.04% | 10.60% |

| Devon Energy Corp. |

DVN, |

Oil & Gas Production | 7.13% | 14.47% | 7.33% |

| AT&T Inc. |

T, |

Major Telecommunications | 6.98% | 14.82% | 7.84% |

| Newell Brands Inc. |

NWL, |

Industrial Conglomerates | 6.59% | 17.42% | 10.82% |

| Dow Inc. |

DOW, |

Chemicals | 6.18% | 15.63% | 9.45% |

| LyondellBasell Industries NV |

LYB, |

Chemicals | 6.09% | 16.07% | 9.99% |

| Scotts Miracle-Gro Co. Class A |

SMG, |

Chemicals | 6.04% | 12.68% | 6.65% |

| Diamondback Energy Inc. |

FANG, |

Oil & Gas Production | 5.56% | 13.63% | 8.08% |

| Best Buy Co. Inc. |

BBY, |

Electronics/ Appliance Stores | 5.53% | 14.08% | 8.55% |

| Viatris Inc. |

VTRS, |

Pharmaceuticals | 5.50% | 28.95% | 23.45% |

| Prudential Financial Inc. |

PRU, |

Life/ Health Insurance | 5.38% | 13.30% | 7.91% |

| Ford Motor Co. |

F, |

Motor Vehicles | 5.23% | 15.95% | 10.72% |

| Invesco Ltd. |

IVZ, |

Investment Managers | 5.23% | 14.95% | 9.73% |

| Franklin Resources Inc. |

BEN, |

Investment Managers | 5.17% | 13.21% | 8.04% |

| Kontoor Brands Inc. |

KTB, |

Apparel/ Footwear | 5.17% | 14.15% | 8.98% |

| Seagate Technology Holdings PLC |

STX, |

Computer Peripherals | 5.11% | 13.19% | 8.07% |

| Foot Locker Inc. |

FL, |

Apparel/ Footwear Retail | 5.03% | 15.52% | 10.49% |

| Source: FactSet | |||||

Any stock screen has its limitations. If you are interested in stocks listed here, it is best to do your own research, and it is easy to get started by clicking the tickers in the table for more information about each company. Click here for Tomi Kilgore’s detailed guide to the wealth of information for free on the MarketWatch quote page.

For the “estimated FCF yields,” consensus free cash flow estimates for calendar 2023 were used for all companies except the following:

Don’t miss: Dividend yields on preferred stocks have soared. This is how to pick the best ones for your portfolio.

[ad_2]

[ad_1]

The U.S. stock market is heading higher again Tuesday, with the S&P 500 index continuing to climb above its 2022 low, but Bespoke Investment Group cautions that history shows its recent bounce may not signal the bear market’s end.

Bespoke’s research on first-day gains from bear-market lows found that bear markets typically end with even bigger moves than the one seen Monday, when the S&P 500 jumped 2.6%. The average move higher is “actually above 4%!” the firm wrote in an Oct. 3 note.

U.S. stocks are trading up this week as Treasury yields fall and the soaring U.S. dollar loses some of its strength. The market moves come as investors look for any hints that the Federal Reserve might back off from its aggressive tightening of monetary policy.

On Monday, “markets clearly benefitted from huge declines in yields, which benefitted from Richmond Fed President Barkin echoing Governor Brainard’s speech Friday with concerns about the impact of dollar strength,” Bespoke said in its note. The reversal of the U.S. dollar, along with lower yields and higher stocks, showed investors “clearly bought that concern as the latest source of potential Fed dovishness.”

Bespoke was referring to comments by Fed Vice Chair Lael Brainard and Thomas Barkin, president of the Federal Reserve Bank of Richmond.

While the U.S. dollar’s strength has eased this week, the ICE US Dollar index

DXY,

is still up around 15% so far this year, according to FactSet data, at last check. The dollar has climbed as the Fed tightens monetary policy to combat high inflation.

“On balance, dollar appreciation tends to reduce import prices in the United States,” Brainard said in her speech Friday addressing global financial stability considerations. “But in some other jurisdictions, the corresponding currency depreciation may contribute to inflationary pressures and require additional tightening to offset.”

The Fed is “attentive to financial vulnerabilities that could be exacerbated by the advent of additional adverse shocks,” Brainard said in her speech. “For instance, in countries where sovereign or corporate debt levels are high, higher interest rates could increase debt-servicing burdens and concerns about debt sustainability, which could be exacerbated by currency depreciation.”

Read: U.S. dollar’s dominance tends to hurt these sectors of the stock market less, says RBC

As for the decline in Treasury yields, the 10-year Treasury note dropped 15.2 basis points Monday to 3.650%, while two-year Treasury yield fell 10.3 basis points to 4.103%, according to Dow Jones Market Data. Treasury yields continued to dip on Tuesday, with the two-year

TMUBMUSD02Y,

at 4.08% and the 10-year

TMUBMUSD10Y,

falling to 3.60%, FactSet data show, at last check.

Meanwhile, the ICE US Dollar index, a measure of the dollar’s strength against a basket of rival currencies, was down more than 1% around midday Tuesday.

The U.S. stock market was moving sharply higher again on Tuesday, with the Dow Jones Industrial Average

DJIA,

jumping 2.6%, the S&P 500

SPX,

climbing 2.9% and the Nasdaq Composite

COMP,

surging 3.3%, FactSet data show, at last check.

But after this week’s bounce, the S&P 500 remains down more than 20% this year, based on trading around midday Tuesday.

“It’s easy to read-in to very high two-way volatility across assets as signaling a Fed pivot is finally here, but we just haven’t seen any reason for that,” Bespoke said. “Until the Fed durably shifts away from their concern over inflation, headwinds for stocks and bonds alongside tailwinds for the dollar will continue.”

[ad_2]

[ad_1]

Elon Musk is not a Chief Executive Officer like the others.

Tesla’s (TSLA) boss is atypical.

He refuses to obey the rules often imposed on executives of public companies.

The billionaire did not hesitate to relaunch the showdown with the U.S Security and Exchange Commission (SEC) despite a 2018 settlement with the regulator.

In September 2018, the two sides agreed to end an investigation into a tweet from Musk, posted on August 7, 2019, that caused the price of Tesla shares to fall.

“Am considering taking Tesla private at $420. Funding secured,” the billionaire wrote at the time.

The tweet shook Tesla stock. The SEC filed a complaint against Musk.

A settlement was reached and announced on September 29, 2018. It required Musk to step down as Tesla’s chairman. Tesla and Musk agreed to pay $40 million in penalties. Tesla also agreed to have the company’s lawyers pre-approve tweets with material information about the company.

Last April, a New York federal judge told the billionaire in a ruling that he would not end the agreement that called for him to have his social media posts approved by a company attorney if they consisted of material information about Tesla.

Musk pushed backed and said that the previous agreement hindered his freedom of speech. He said the SEC used the agreement to “launch endless, boundless” investigations of his public statements.

“None of the arguments hold water,” Judge Lewis J. Liman of the U.S. District Court for the Southern District of New York wrote in a ruling.

Few CEOs would risk attacking the SEC the way Musk does. These tensions also suggest that the billionaire values his uniqueness and he has just proven it once again.

On October 2, Tesla shareholder Ross Gerber wrote to Musk on Twitter, asking how investors should view Tesla, after the company presented on September 30 the progress of Optimus, the company’s humanoid robot. Musk’s response was scathing.

“Hey @elonmusk- love to discuss the long term global economic implications of Optimus and how investors should view tesla moving forward. $tsla,” Gerber posted on Twitter.

“I don’t care about boosting the stock,” the billionaire responded. “But the economic implications are obvious.”

Very few CEOs would dare to make such a statement for fear of reprisals from their Board of Directors and a sanction from the markets. Not Musk, who sees himself as a visionary, not just an entrepreneur. He has made it his mission to transform civilization as it is today.

The tech tycoon showcased a dancing Optimus on September 30, gesturing with one of his hands and bending his knees during Tesla AI Day. He promised a mass-production of his robot as soon as possible.

Optimus will cost less than $20,000.

“Our goal is to make a useful humanoid robot as quickly as possible. We’ve also designed using the same discipline that we use in designing the car which is, to say, to design for manufacturing, such that it’s possible to make the robot at a high volume at low cost with high reliability,” the billionaire said.

Optimus will herald a “future of abundance,” Musk said. It will be “a future where there is no poverty, where people can have whatever they want, in terms of products and services. It really is a fundamental transformation of civilization as we know it.”

The robot nevertheless remains a work in progress.

Tesla will work on different use cases, including cooking and gardening. Musk wants to replace human labor with humanoid robots, made from the artificial intelligence software used by Tesla for its cars.

[ad_2]

[ad_1]

While September lived up to its reputation as a brutal month for stocks, October tends to be a “bear-market killer,” associated with historically strong returns, especially in midterm election years.

Skeptics, however, are warning investors that negative economic fundamentals could overwhelm seasonal trends as what’s traditionally the roughest period for equities comes to an end.

U.S. stocks ended sharply lower on Friday, posting their worst skid in the first nine months of any year in two decades. The S&P 500

SPX,

recorded a monthly loss of 9.3%, its worst September performance since 2002. The Dow Jones Industrial Average

DJIA,

fell 8.8%, while the Nasdaq Composite

COMP,

on Friday pushed its total monthly loss to 10.5%, according to Dow Jones Market Data.

Read: Stocks and bonds are ‘discounting for a disaster’ after the worst stretch for investors in 20 years

The indexes had booked modest gains in the first half of the month after investors fully priced in a large interest-rate hike at the FOMC meeting late September as August’s inflation data showed little sign of easing price pressures. However, the central bank’s more-hawkish-than-expected stance caused stocks to give up all those early September gains. The Dow entered its first bear market since March 2020 in the last week of the month, while the benchmark S&P slid to another 2022 low.

See: It’s the worst September for stocks since 2008. What that means for October.

October’s track record may offer some comfort as it has been a turnaround month, or a “bear killer,” according to the data from Stock Trader’s Almanac.

“Twelve post-WWII bear markets have ended in October: 1946, 1957, 1960, 1962, 1966, 1974, 1987, 1990, 1998, 2001, 2002 and 2011 (S&P 500 declined 19.4%),” wrote Jeff Hirsch, editor of the Stock Trader’s Almanac, in a note on Thursday. “Seven of these years were midterm bottoms.”

Of course 2022 is also a midterm election year, with congressional elections coming up on Nov. 8.

According to Hirsch, Octobers in the midterm election years are “downright stellar” and usually where the “sweet spot” of the four-year presidential election cycle begins (see chart below).

“The fourth quarter of the midterm years combines with the first and second quarters of the pre-election years for the best three consecutive quarter span for the market, averaging 19.3% for the DJIA and 20.0% for the S&P 500 (since 1949), and an amazing 29.3% for NASDAQ (since 1971),” wrote Hirsch.

Skeptics aren’t convinced the pattern will hold true this October. Ralph Bassett, head of investments at Abrdn, an asset-management firm based in Scotland, said these dynamics could only play out in “more normalized years.”

“This is just such an atypical period for so many reasons,” Bassett told MarketWatch in a phone interview on Thursday. “A lot of mutual funds have their fiscal year-end in October, so there tends to be a lot of buying and selling to manage tax losses. That’s kind of something that we’re going through and you have to be very sensitive to how you manage all of that.”

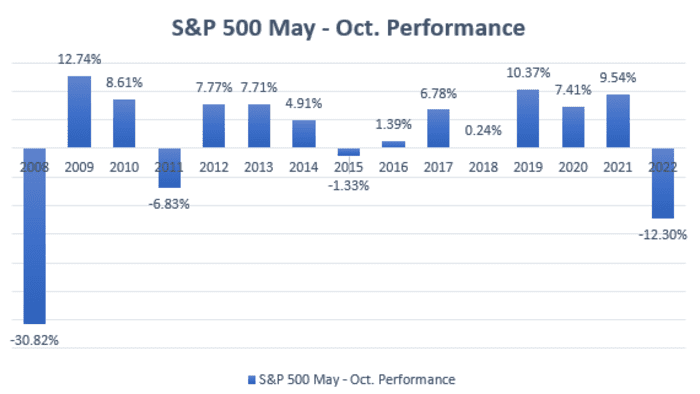

An old Wall Street adage, “Sell in May and go away,” refers to the market’s historical underperformance during the six-month period from May to October. Stock Trader’s Almanac, which is credited with coining the saying, found investing in stocks from November to April and switching into fixed income the other six months would have “produced reliable returns with reduced risk since 1950.”

Strategists at Stifel, a wealth-management firm, contend the S&P 500, which has fallen more than 23% from its Jan. 3 record finish, is in a bottoming process. They see positive catalysts between the fourth quarter of 2022 and the start of 2023 as Fed policy plus S&P 500 negative seasonality are headwinds that should subside by then.

“Monetary policy works with a six-month lag, and between the [Nov. 2] and [Dec. 14] final two Fed meetings of 2022, we do see subtle movement toward a data-dependent Fed pause which would bullishly allow investors to focus on (improving) inflation data rather than policy,” wrote strategists led by Barry Bannister, chief equity strategist, in a recent note. “This could reinforce positive market seasonality, which is historically strong for the S&P 500 from November to April.”

Seasonal trends, however, aren’t written in stone. Dow Jones Market Data found the S&P 500 recorded positive returns between May and October in the past six years (see chart below).

Anthony Saglimbene, chief markets strategist at Ameriprise Financial, said there are periods in history where October could evoke fear on Wall Street as some large historical market crashes, including those in 1987 and 1929, occurred during the month.

“I think that any years where you’ve had a very difficult year for stocks, seasonality should discount it, because there are some other macro forces [that are] pushing on stocks, and you need to see more clarity on those macro forces that are pushing stocks down,” Saglimbene told MarketWatch on Friday. “Frankly, I don’t think we’re going to see a lot of visibility at least over the next few months.”

[ad_2]

[ad_1]

For the past two years, since the covid pandemic hit in late-February 2020, the cruise industry has taken one punch after another. And, while the situation has improved from the extended period when cruises were not allowed to sail from United States ports, that does not mean that it’s back to 2019 for Royal Caribbean International (RCL) , Carnival Cruise Line (CCL) , and Norwegian Cruise Line (NCLH) .

The industry has done a remarkable job bringing operations back to near-normal. All three cruise lines not only have put all their ships back in service, they’re also still moving forward with plans for new ships and other investments including improvements to private islands, and developing new ports.

That being said, Carnival just reported its second-quarter earnings and the market did not like the numbers at all. Shares of all three cruise lines were down double digits on Sept. 30, but traders clearly missed that aside from rising costs and a loss (both of which were expected) the cruise line largely delivered good news.

Carnival reported a GAAP net loss of $770 million for the quarter. That was driven by higher costs with the company specifically citing advertising expenses and having some of its fleet unavailable to produce revenue.

While the company’s year-to-date adjusted cruise costs excluding fuel per ALBD during 2022 has benefited from the sale of smaller-less efficient ships and the delivery of larger-more efficient ships, this benefit is offset by a portion of its fleet being in pause status for part of the year, restart related expenses, an increase in the number of dry dock days, the cost of maintaining enhanced health and safety protocols, inflation and supply chain disruptions. The company anticipates that many of these costs and expenses will end in 2022.

If you’re investing in any cruise line you have to do so on a very long-term basis. That makes profitability less of a concern than the company building back its business and Carnival showed some very positive signs in that direction.

Total customer deposits were $4.8 billion as of August 31, 2022, approaching the $4.9 billion as of August 31, 2019, which was a record third quarter.

New bookings during the third quarter of 2022 primarily offset the historical third quarter seasonal decline in customer deposits ($0.3 billion decline in the third quarter of 2022 compared to $1.1 billion decline for the same period in 2019).

Carnival (and likely all the cruise lines) is being hurt by prices generally being depressed and some passengers paying for their trips using future cruise credits from cruises canceled during the pandemic. That’s not really what matters though. Carnival has been increasing passenger loads and getting people back on its ships.

“Since announcing the relaxation of our protocols last month, we have seen a meaningful improvement in booking volumes and are now running considerably ahead of strong 2019 levels,” Carnival CEO Josh Weinstein said. “We expect to further capitalize on this momentum with renewed efforts to generate demand. We are focused on delivering significant revenue growth over the long-term while taking advantage of near-term tactics to quickly capture price and bookings in the interim.”

Basically, cruise prices are cheap right now because it’s more important to get customers back on board than it is to maintain pricing integrity. That’s a tactic that could hurt long-term pricing, but the cruise industry is less vulnerable than other vacation options because there have always been large pricing variations based on the calendar and the age of the ship being booked.

Carnival was trading at its 52-week low after it reported. That’s a pretty major overreaction given that the cruise industry was barely operating in the fall of 2021.

Yes, the industry has a long way to go. All three major cruise lines took on billions of dollars of debt during the pandemic. Refinancing that debt in an environment with higher interest rates is a challenge, but it’s one Carnival (and its rivals) have been meeting.

That has come with some shareholder dilution. Carnival sold $1.15 billion in new stock during the quarter, but the company has over $7.4 billion in liquidity. Weinstein is optimistic (he has to be, that’s part of his job) about the future.

“During our third quarter, our business continued its positive trajectory, achieving over $300 million of adjusted EBITDA and reaching nearly 90% occupancy on our August sailings. We are continuing to close the gap to 2019 as we progress through the year, building occupancy on higher capacity and lower unit costs,” he said.

Usually it’s easy to dismiss a CEO making upbeat comments after posting a loss, but in this case, Carnival has basically followed the recovery path it laid out once it returned to sailing. Both Royal Caribbean and Norwegian have followed similar paths and while meaningful shareholder returns may take time, these are strong companies built for the long-term that made a lot of money before the pandemic and should do so again.

[ad_2]

[ad_1]

Most financial planners advise young people to start saving early — and often — for retirement so they can take advantage of the so-called eighth wonder of the world – the power of compound interest.

And many advisers routinely urge those entering the workforce to contribute to their 401(k), especially when their employer is matching some portion of the amount the worker is contributing. The matching contribution is – essentially – free money.

New research, however, indicates that many young people should not save for retirement.

The reason has to do with something called the life-cycle model, which suggests that rational individuals allocate resources over their lifetimes with the aim of avoiding sharp changes in their standard of living.

Put another way, individuals, according to the model which dates back to economists Franco Modigliani, a Nobel Prize winner, and Richard Brumberg in the early 1950s, seek to smooth what economists call their consumption, or what normal people call their spending.

According to the model, young workers with low income dissave; middle-aged workers save a lot; and retirees spend down their savings.

The just-published research examines the life-cycle model even further by looking at high- and low-income workers, as well as whether young workers should be automatically enrolled in 401(k) plans. What the researchers found is this:

1. High-income workers tend to experience wage growth over their careers. And that’s the primary reason why they should wait to save. “For these workers, maintaining as steady a standard of living as possible therefore requires spending all income while young and only starting to save for retirement during middle age,” wrote Jason Scott, the managing director of J.S. Retirement Consulting; John Shoven, an economics professor at Stanford University; Sita Slavov, a public policy professor at George Mason University; and John Watson, a lecturer in management at the Stanford Graduate School of Business.

2. Low-income workers, whose wage profiles tend to be flatter, receive high Social Security replacement rates, making optimal saving rates very low.

Middle-aged workers will need to save more later

In an interview, Scott discussed what some might view as a contrary-to-conventional wisdom approach to saving for retirement.

Why does one save for retirement? In essence, Scott said, it’s because you want to have the same standard of living when you’re not working as you did while you were working.

“The economic model would suggest ‘Hey, it’s not smart to live really high in the years when you’re working and really low when you’re retired,’” he said. “And so, you try to smooth that out. You want to save when you have relatively high income to support yourself when you have relatively low income. That’s really the core of the life-cycle model.”

But why would you spend all your income when you’re young and not save?

“In the life-cycle model, we are assuming you are getting the absolute most happiness you can out of income each year,” said Scott. “In other words, you are doing your best at age 25 with $25,000, and there is no way to live ‘cheaply’ and do better,” he said. “We also assume a given amount of money is more valuable to you when you are poor compared to when you are wealthy.” (Meaning $1,000 means a lot more at 25 than at 45.)

Scott also said that young workers might also consider securing a mortgage to buy a house rather than save for retirement. The reasons? You’re borrowing against future earnings to help that consumption, plus, you’re building equity that could be used to fund future consumption, he said.

Are young workers squandering the advantage of time?

Many institutions and advisers recommend just the opposite of what the life-cycle model suggests. They recommend that workers should have a certain amount of their salary salted away for retirement at certain ages in order to fund their desired standard of living in retirement. T. Rowe Price, for instance, suggests that a 30-year-old should have half their salary saved for retirement; a 40-year-old should have 1.5 times to 2 times their salary saved; a 50-year-old should have 3 times to 5.5 times their salary saved; and a 65-year-old should have 7 times to 13.5 times their salary saved.

Scott doesn’t disagree that workers should have savings benchmarks as a multiple of income. But he said a high-income worker who waits until middle age to save for retirement can easily reach the later-age benchmarks. “Savings for retirement probably is more in the zero range until 35 or so,” Scott said. “And then it is probably faster after that because you want to accumulate the same amount.”

Plus, he noted, the home equity a worker has could count toward the savings benchmark as well.

So, what about all the experts who say young people are best positioned to save because they have such a long timeline? Aren’t young workers just squandering that advantage?

Not necessarily, said Scott.

“First: saving earns interest, so you have more in the future,” he said. “However, in economics, we assume that people prefer money today compared to money in the future. Sometimes this is called a time discount. These effects offset each other, so it depends on the situation as to which is more significant. Given interest rates are so low, we generally think time discounts exceed interest rates.”

And second, Scott said, “early saving could have a benefit from the power of compounding, but the power of compounding is certainly irrelevant when after-inflation interest rates are 0% – as they have been for years.”

In essence, Scott said, the current environment makes a front-loaded lifetime spending profile optimal.

Low-income workers don’t need to save either

As for those with low income, say in the 25th percentile, Scott said it’s less about the “income ramp that really moves saving” and more that Social Security is extremely progressive; it replaces a large percentage of one’s preretirement income. “The natural need to save is not there when Social Security replaces 70, 80, 90% (of one’s preretirement income),” he said.

In essence, the more Social Security replaces of your preretirement income, the less you’ll need to save. The Social Security Administration and others are currently researching what percent of preretirement income Social Security replaces by income quintile, but previously published research from 2014 shows that Social Security represented nearly 84% of the lowest income quintile’s family income in retirement while it only represented about 16% of the highest income quintile’s family income in retirement.

Is it worth auto-enrolling young workers in a 401(k) plan?

Scott and his co-authors also show that the “welfare costs” of automatically enrolling younger workers in defined-contribution plans—if they are passive savers who do not opt-out immediately—can be substantial, even with employer matching. “If saving is suboptimal, saving by default creates welfare costs; you’re doing the wrong thing for this population,” he said.

Welfare costs, according to Scott, are the costs of taking an action compared to the best possible action. “For example, suppose you wanted to go to restaurant A, but you were forced to go to restaurant B,” he said. “You would have suffered a welfare loss.”

In fact, Scott said young workers who are automatically enrolled into their 401(k) might consider when they’re in their early 30s taking the money out of their retirement plan, paying whatever penalty and taxes they might incur, and use the money to improve their standard of living.

“It’s optimal for them to take the money and use it to improve their spending,” said Scott. “It would be better if there weren’t penalties.”

Why is this so? “If I didn’t understand that I was being defaulted into a 401(k) plan, and I didn’t want to save, then I suffered a welfare loss,” said Scott. “We assume people figure out after five years that they were defaulted. At that point, they want their money out of the 401(k), and they are optimally willing to pay the 10% penalty to get their money out.”

Scott and his colleagues assessed welfare costs by figuring out how much they have to compensate young workers at that five-year point so that they are OK with having been inappropriately forced to save. Of course, the welfare costs would be lower if they didn’t have to pay the penalty to cash out their 401(k).

And what about workers who are automatically enrolled in a 401(k)? Are they not creating a savings habit?

Not necessarily. “The person who is confused and defaulted doesn’t really know it’s happening,” said Scott. “Maybe they’re getting a savings habit. They’re certainly living without the money.”

Scott also addressed the notion of giving up free money – the employer match — by not saving for retirement in an employer-sponsored retirement plan. For young workers, he said the match isn’t enough to overcome the cost of, say, five years of below-optimal spending. “If you think it’s for retirement, the match-improved benefit in retirement doesn’t overcome the cost of losing money when you’re poor,” said Scott. “I’m simply noting that if you are not consciously making the choice to save, it is hard to argue you are making a saving habit. You did figure out how to live on less, but in this case, you did not want to, nor do you intend to continue saving.”

The research raises questions and risks that must be addressed

There are plenty of questions the research raises. For instance, many experts say it’s a good idea to get in the habit of saving, to pay yourself first. Scott doesn’t disagree. For instance, a person might save to build an emergency fund or a down payment on a house.

As for the folks who might say you’re losing the power of compounding, Scott had this to say: “I think the power of compounding is challenged when real interest rates are 0%.” Of course, one could earn more than 0% real interest but that would mean taking on additional risk.

“The principle is about, ‘Should you save when you are relatively poor so you can have more when you are relatively rich?’ The life-cycle model says, ‘No way.’ This is independent of how you invest money between time periods,” Scott said. “For investing, our model does look at riskless interest rates. We argue that investment expected returns and risks are in equilibrium, so the core result is unlikely to change by introducing risky investments. However, it is definitely a limitation of our approach.”

Scott agreed there are risks to be acknowledged, as well. It’s possible, for instance, that Social Security, because of cuts to benefits, might not replace a low-income worker’s preretirement salary as much as it does now. And it’s possible that a worker might not experience high wage growth. What about people having to buy into the life-cycle model?

“You don’t have to buy into all of it,” said Scott. “You have to buy into this notion: You want to save when you’re relatively rich in order to spend when you’re relatively poor.”

So, isn’t this a big assumption to make about people’s career/pay trajectory?

“We consider relatively rich wage profiles and relatively poor wage profiles,” said Scott. “Both suggest young people should not save for retirement. I think the vast majority of median wage or higher workers experience a wage increase over their first 20 years of working. However, there is certainly risk in wages. I think you could rightly argue that young people might want to save some as a precaution against unexpected wage declines. However, this would not be saving for retirement.”

So, should you wait to save for retirement until you’re in your mid-30s? Well, if you subscribe to the life-cycle model, sure, why not? But if you subscribe to conventional wisdom, know that consumption might be lower in your younger years than it needs to be.

[ad_2]

[ad_1]

This week Freddie Mac said the average interest rate on a 30-year mortgage loan in the U.S. had climbed to 6.70% from 6.29% the week before and 6.02% two weeks ago. The average rate a year ago was 3.01%.

Would-be sellers who have low-rate mortgage loans are reluctant if it means they need to take out a new loan to fund their next home. Would-be buyers are forced out of the market, as the monthly principal and interest payment for a new 30-year loan, based on Freddie Mac’s figures, has increased 53% from a year ago.

Home-sale contracts are being canceled at a record pace in some areas.

But these factors could lead to a buyer’s market in 2023 if prices plunge. Here are the areas economists expect to see the largest home price declines.

The dollar has strengthened as the Federal Reserve has taken the lead among central banks in raising interest rates. This is reverberating across the world, making it more costly for countries to make interest payments on dollar-denominated debt and increasing the cost of any commodity traded in dollars.

The rising dollar lowers prices on imported goods for Americans and can also lower their international travel costs. But Michael Wilson, Morgan Stanley’s chief equity strategist, warns that earnings for the S&P 500

SPX,

would decline as a direct result of the strong dollar and called the current foreign-exchange backdrop an “untenable situation” for the stock market.

On the other hand: Companies are trying to blame weak earnings on the strong U.S. dollar, but that’s a lame excuse

Michael Brush interviews David Baron, co-manager of the Baron Focused Growth Fund

BFGFX,

who describes opportunities cropping up as institutional investors dump stocks. He also explains his winning long-term strategy, which has included a very long-term investment in Tesla Inc.

TSLA,

A a positive sign for the stock market: These 12 stocks have seen strong insider buying

When interest rates rise, bond prices fall. But it also means that if you have money to put to work, bond yields have become much more attractive.

Khuram Chaudhry, a European equity quantitative strategist at JPMorgan in London, makes the case for buying bonds now.

Preferred stocks feature stated dividend yields and prices that move the same way bond prices do. That means prices for many issues are now heavily discounted to face value and that current yields are much higher than they were at the end of 2021. Here’s an in-depth guide on how to research preferred stocks and make your own selections.

Related: 22 dividend stocks screened for quality and safety

Bloomberg

Stanley Druckenmiller predicted a U.S. recession in 2023 as a result of monetary policy tightening by the Federal Reserve. That may not be much of a stretch, considering that the U.S. economy contracted during the first half of 2022, according to revised GDP figures from the Bureau of Economic Analysis.

But investors should be careful — macro forecasts often turn out to be incorrect, Mark Hulbert warns.

More on stocks: It’s the worst September for stocks since 2008. What that means for October.

Alessandra Malito has advice on how retirees and people planning for retirement can prepare for tough economic times.

Agence France-Presse/Getty Images

After the new U.K. government of Prime Minister Liz Truss announced a massive tax cut along with a new spending program to help counter rising fuel costs and new borrowing, the pound hit a new low against the dollar on Sept. 26 as investors and money managers panicked and sold-off U.K. government bonds. Steve Goldstein explains how and why the Bank of England came tot the rescue.

Beth Pinsker digs deeply to explain how to use a reverse mortgage as a financial planning tool.

After Tesla CEO Elon Musk said the upcoming Cybertruck would be sufficiently waterproof to “serve briefly as a boat,” the San Francisco Bay Ferry offered this advice to patrons.

Want more from MarketWatch? Sign up for this and other newsletters, and get the latest news, personal finance and investing advice.

[ad_2]

[ad_1]

This is a Real-time headline. These are breaking news, delivered the minute it happens, delivered ticker-tape style. Visit www.marketwatch.com or the quote page for more information about this breaking news.

[ad_2]

[ad_1]

President Joe Biden speaks about the March jobs report in the State Dining Room of the White House, Friday, April 1, 2022, in Washington. (AP Photo/Patrick Semansky)

ASSOCIATED PRESS

On March 28th, 2022, the Department of Treasury issued the 2023 Fiscal Year Revenue Proposal (The Green book) outlining a number of proposed tax policies designed to increase revenues, improve tax administration, and make the tax system more equitable and efficient. The proposal had several key policies that will have a direct impact on crypto taxpayers if adapted as proposed.

The proposal has three major tax policy changes focused on high income earner in the US. First, the treasury wants the highest marginal income tax rate to increase from 37% to 39.6% effective December 31, 2022. This increased marginal rate would apply to taxable income over $450,00 for married filers and $400,000 for individual filers. If your total taxable income is above these thresholds, your short-term cryptocurrency gains (coins & NFTs sold after holding them for less than 12 months) and other types of crypto income such as staking, mining & interest would be subject to this higher rate.

Second, the proposal is planning to subject long-term capital gains (which are generally subject to a lower tax rate than ordinary income tax rate) to a higher tax rate for taxpayers with over 1 million of taxable income. For example, if your overall taxable income is over 1 million, long-term gains in excess of 1 million would be subject to a much higher ordinary income tax rate vs the maximum 20% rate under the current law. Furthermore, the proposal aims to make transfers of appreciated property as gift and at death as taxable events for wealthy individuals.

Third and arguably the most aggressive tax proposal included in the document is the 20% minimum tax on “Total income” for taxpayer’s worth over 100 million. Total income includes regular taxable income such as wages and investment income and surprisingly unrealized capital gains on assets you own.

The proposal includes four digital assets specific tax policy changes. Let’s first go through the three policies that have a direct impact on taxpayers.

The first proposal talks about cryptocurrency lending activity which has expanded rapidly over the past several years. The treasury aims to make cryptocurrency-based loans tax-free similar to loans based on stocks & securities, as a long as certain criteria is met. This is good news for taxpayers who are involved in lending activity.

Certain specified financial assets (foreign bank accounts, brokerages, etc.) held by US individuals in foreign countries have been subject to IRS reporting for many years. To comply with the rules, US taxpayers with foreign accounts in excess of $50,000 are required to file a Form 8938 (Statement of Specified Foreign Financial Assets) disclosing various information about those assets. Whether digital assets held in overseas exchanges are subject to Form 8938 reporting has been a grey area for several years. The treasury proposal finally adds clarity to this lingering question and want to subject digitals assets to Form 8939 reporting.

The next digital asset-specific tax policy change involves day traders of cryptocurrency. Section 475(f) tax election has been a taxpayer-friendly election active day traders of stocks have been enjoying for many years. When this election is properly made, day traders can mark-to-market their positions at year end and treat gains and losses as ordinary income. This allows them to deduct unlimited amounts of losses and override the $3,000 annual cap on capital loss deduction other taxpayers are subject to. If we strictly follow the current law, this favorable tax election is only applicable to stocks and commodity traders. The treasury has clearly identified the growth of crypto markets and proposed to extend this favorable election to active digital asset traders. This is another positive policy change.

The final proposal related to cryptocurrency is aimed at US cryptocurrency exchanges. To effectively combat offshore tax evasion, the US tax regulators heavily rely on information shared by foreign financial institutions and governments on financial accounts owned by US individuals in foreign countries. The success of this system heavily depends on reciprocity. In simple terms, the US must share information about US financial accounts owned by foreign individuals to those respective countries; Foreign countries must report to the US when US individuals hold financial accounts in foreign countries. This continuous information sharing enables regulators to catch bad actors using offshore strategies to evade taxes.

To strengthen reciprocity when it comes to crypto-related information sharing, the treasury would require US digital asset exchanges to report account balance for all financial accounts maintained at a US office held by a foreign person to the IRS.

“This would allow the United States to share such information on an automatic basis with appropriate partner jurisdictions, in order to reciprocally receive information on U.S. taxpayers”

All aforementioned proposals would be effective after December 31, 2022, except the rule that mandates US exchanges to report foreign account holder information, which is planned to be effective after December 31, 2023. According to treasury estimates, these digital assets specific rules will raise approximately 11 billion in tax revenue between 2023 and 2032.

Monitor how the proposed rules are processed through the legislative process in the coming months.

Quick Guide To Filing Your 2021 Cryptocurrency & NFT Taxes

How The Infrastructure Bill Is Brewing A Crypto Tax Compliance Nightmare

IRS May Not Tax Passive Income From Holding Crypto Right Away

[ad_2]

Shehan Chandrasekera, Senior Contributor

Source link

[ad_1]

Market Advisory Group founding partner Danny Goolsby discusses important details prior to retiring

Press Release

–

updated: Jan 30, 2018

WICHITA, Kan., January 30, 2018 (Newswire.com)

–

If decisions about where and what to invest in are keeping you up at night, it’s no wonder: retiring today has gotten more complicated. Our great-grandparents retired with a pension and an amount from Social Security with the confidence that their income needs would be guaranteed. Any earnings their investments made were like icing on the cake.

Today, pensions have gone the way of the dinosaur, Social Security benefits are under threat and investors are left to figure out things on their own using the money in their retirement and brokerage accounts. Through no fault of their own, we’re seeing people make dire mistakes when it comes to the allocation of these resources. Given today’s longer life expectancies and the volatility of a global market, it’s even more important than ever before that you do the right thing at the right time with the money you’re relying on for retirement.

Here are the biggest mistakes we see investors making, along with a suggestion about what you can do instead to make sure that you don’t run out of money before you run out of life.

MISTAKE #1: Not Understanding What You Own

There are many different ways you can be charged commissions and fees inside of an investment but typically speaking, you pay those fees whether the account earns money or not. Too many investors keep their account statements sealed in a drawer because they’re either too afraid to look or they don’t understand what they’re looking at. Here’s the thing, though: just because you’re not looking at the bad news doesn’t mean it goes away.

High fees create an unnecessary drag on your returns and may prevent you from reaching your retirement goals. As fiduciaries, we’ve even seen some situations where, after adding up all the fees paid out over a period of years, there were more fees charged than what the consumer earned. Don’t keep your head in the sand. Get a second opinion. Ask a fiduciary professional to walk you through the fees you’re paying on the investments you own and find out if you have better options.

MISTAKE #2: Not Knowing How Much Risk You’re Exposed To

It’s been said that convincing investors to stay in the market is the horsepower that drives the market. The more investors, the more the market grows. It’s easy to make money in the market when the markets are going up, the question is, how much of that money will you get to keep?

There are several adages — such as buy and hold — that don’t necessarily apply to the investor who is at or near the time of retirement. If you are five or fewer years away from your full retirement age, for example, then you might be in what we call the retirement red zone. This is the time in your life when losing money matters the most; make a fumble now, and it could negatively affect the earning power of your portfolio over the long term. Instead of focusing on risk and growth, protect what you have before it’s gone.

MISTAKE #3: Not Having a Plan

A lot of people hear the term “protection” and instantly jump to the conclusion that they won’t earn any returns. This couldn’t be further from the truth. Having a plan in place is the process of coordinating the different aspects of a portfolio — including taxes, Social Security and Medicare decisions — along with your market investments to seek both growth and protection. This is how you can get a cohesive strategy with minimal fees and less risk for maximum returns.

If you’ve worked multiple decades to get your nest egg to where it’s at now, then you’ll want to take steps to ensure that what you need for retirement is protected. Protect first, grow second and build a plan around your goals. Do that and you’ll be able to achieve what we want for our all clients: peace of mind.

Are you paying too much in fees? Worried about your exposure to risk? Ready to get your retirement ducks in a row? Schedule your complimentary consultation by filling out this simple form and one of our advisors will be happy to get back to you. We take this step seriously, as it is crucial that you understand your current situation based on facts, not persuasion or sales pressure. We look forward to helping you avoid these mistakes so that you can enjoy the retirement you deserve.

Investment advisory services offered through Foundations Investment Advisors LLC, an SEC-registered investment adviser.

Source: Market Advisory Group

[ad_2]