Disclosure: Our goal is to feature products and services that we think you’ll find interesting and useful. If you purchase them, Entrepreneur may get a small share of the revenue from the sale from our commerce partners.

Entrepreneurs often have a lot of money tied up in their businesses, but that doesn’t mean they shouldn’t be on the lookout for good investments. After a volatile 2022, there’s a mixed outlook on the 2023 stock market, which makes now a great time to invest in your financial education. If you want to be a smarter trader in 2023, check out The Complete 2023 Stock Trading & Investing Bundle while it’s on sale.

StackCommerce

This bundle includes 12 courses geared toward investors of all experience levels. If you’re new to investing, you’ll learn the tools you need for fundamental stock analysis so you can analyze a stock in a few minutes to know if a company is worth investing in. You’ll learn the art of value investing, understand how to make better investment choices, and develop a stream of passive income with your stocks. In addition, you’ll be able to evaluate a company’s Price-to-Earnings (P/E) Ratio and other key ratios, develop a repeatable investment process, and learn how successful investors like Warren Buffett operate.

Beyond the basics, there are courses covering technical analysis using candlestick patterns, options and futures trading, Forex trading, swing trading, and more. You’ll learn how to day trade successfully to maximize your profit, manage your trading risk and protect against losses, and learn to formulate robust trading strategies no matter what your investment appetite. By the end of the courses, you’ll have a more comprehensive understanding of how the stock market works and how you can manage your portfolio to maximize your returns and mitigate your risk.

“It’s like being robbed in a library, but you can’t shout ‘Thief!’ because there are ‘Silence, please’ signs everywhere.”

That’s how Roger Hamilton, chief executive of Genius Group Ltd. GNS, +55.02%,

describes the powerlessness he feels as U.S. securities rules prevent him from discussing his company’s share price, even as it comes under attack from a group of naked short sellers.

The Singapore-based education company on Thursday announced it had appointed a former FBI director to lead a task force investigating alleged illegal trading in its stock that it first addressed in early January.

The news sent the stock up a record 290% on Thursday, and it climbed another 59% on Friday. Volume of about 270 million shares traded in Thursday’s session crushed the daily average of about 634,000 — another indicator, Hamilton told MarketWatch in an interview Friday, of wrongdoing, given that the company’s float is just 10.9 million shares. “Clearly, that’s far more shares than we created,” he said.

Genius Group has evidence from Warshaw Burstein LLP and Christian Levine Law Group, with tracking from Share Intel, that certain individuals and/or companies sold but failed to deliver a “significant” amount of its shares as part of a scheme seeking to artificially depress the stock price.

The company is now exploring legal action and is planning an extraordinary general meeting in the coming weeks to get shareholder approval for its planned actions. These include paying a special dividend as a way to flush out bad actors and working with regulators to share information.

Share Intel uses tracking software in real time to determine exactly where there are discrepancies in the market and where brokers are opening large positions, Hamilton said. The software can measure the number of shares that are being naked shorted and has found multiple instances where significant amounts of fake shares were being created, said Hamilton.

Naked short selling is illegal under Securities and Exchange Commission rules, but that hasn’t stopped the practice, which Hamilton said affects far more companies than is generally known.

In regular short trading, an investor borrows shares from someone else, then sells them and waits for the stock price to fall. When that happens the shares are bought cheaper and returned to the prior owner, with the short seller pocketing the difference as profit.

In naked short selling, investors don’t bother borrowing the stock first and simply sell shares with a promise to deliver them at a later date. When that promise is not fulfilled, it’s known as failure to deliver.

By repeating that process again and again, bad actors can generate massive profits and manipulate a stock’s price lower, with an ultimate goal of driving a company to bankruptcy, at which point all the equity is wiped out and the naked shorts no longer need to be covered.

Hamilton said the evidence gathered by Genius Group shows a great deal of the illegal activity is happening on U.S. exchanges, but there’s also activity happening off-exchange and involving dark pools.

The company is fighting back “because we want this to stop,” Hamilton told MarketWatch. “They’re taking value away from our shareholders. They’re predators. They’re doing something illegal, and we want it to stop, whether that means getting regulators to enforce existing regulations or put new ones in place.”

Public companies have to have committees to monitor and report internal fraud to protect shareholders, he said. But there is no such team looking for external fraud and many retail investors see stocks being manipulated, he said.

“Hopefully, regulations will change and regulators will see there are as many, if not more, threats from outside a company,” he said.

Genius Group is not alone, said Hamilton. He cited among other examples Torchlight, an oil- and gas-exploration company that decided to merge with Metamaterial Inc. to thwart a naked-short-selling attack.

The stock rose from 30 cents to $11 in the six months after the deal was completed, and the company was able to raise about $183 million through a combination of convertible debt and equity. An interview Hamilton conducted with Torchlight’s former CEO, John Brda, can be found below.

Then there’s Jeremy Frommer, CEO of Creatd Inc. CRTD, +4.14%,

which aims to unlock creativity for creators, brands and consumers, who is behind Ceobloc, a website that aims to end the practice of naked short selling.

“Illegal naked short selling is the biggest risk to the health of today’s public markets,” is how the site introduces its mission.

On Friday, the stock of Helbiz Inc. HLBZ, +65.48%

joined Genius Group in rocketing higher in high volume, after that company said it, too, was taking on naked short sellers.

The New York–based maker of e-scooters and e-bicyles said that it was following Genius Group’s example and that it believes “certain individuals and/or companies may have engaged in illegal short selling practices that have artificially depressed the stock price.” The stock had plummeted 64% over the three months through Thursday’s close at 12.31 cents.

Genius Group’s stock, which went public in April 2022 at $6 a share, has gained more than 600% this week. The S&P 500 SPX, +1.89%

has gained 1.1% over the same four trading sessions.

The stock of a Singapore-based ed-tech and education company called Genius Group Ltd. rallied more than 200% on Thursday, after it said it appointed a former F.B.I. director to lead a task force investigating alleged illegal trading in its stock that it first disclosed in early January.

The stock was last up 264% to mark its biggest-ever one-day percentage gain. Volume of 197.76 million shares traded crushed the 65-day average of just 634,17. Genius Group GNS, +290.29%

also said it would issue a special dividend to shareholders to help expose the wrongdoing and is considering a dual listing that would make illegal naked short selling more difficult.

The task force will be led by Timothy Murphy, a former deputy director of the F.B.I. who is also on the board. It will include Richard Berman, also a Genius Group Director and chair of the company’s Audit Committee, and Roger Hamilton, the chief executive officer of Genius Group.

“The company has been in communication with government regulatory authorities and is sharing information with these authorities to assist them,” the company said in a statement.

Genius Group said it has proof from Warshaw Burstein LLP and Christian Levine Law Group, with tracking from Share Intel, that certain individual and/or companies sold but failed to deliver a “significant” amount of its shares as part of a scheme seeking to artificially depress the stock price.

It will now explore legal action and will hold an extraordinary general meeting in the coming weeks to get shareholder approval for its planned actions.

Genius’ IPO priced at $6 a share in April of 2022, he wrote in a blog. The company, which aims to develop an entrepreneur education system, then completed five acquisitions of education companies to build out its portfolio and reported more than 60% growth in its last earnings report.

Analysts at Diamond Equity assigned it an $11.28 stock price target, while Zacks assigned it a $19.20 stock price target.

“By all measures, we believed we were doing all the right things to justify a rising share price,” said Hamilton.

The company then announced two funding rounds totaling $40 million to grow its balance sheet to more than $60 million, yet its stock fell to under 40 cents, or less than 25% of the cash raised and less than 20% of its net assets.

“This didn’t happen gradually,” the executive wrote. “It happened in two month intervals from our IPO, in June, August, October and December. Each time, over a period of a few days, massive selling volume that was a multiple of our float (As most of our shares are on lock up, only around 4 million are tradeable) was sold into the market, making our share price drop by 50% or more.”

The company has since drawn on Wes Christian, a short-selling litigator from Christian Levine Law Group, who has helped it understand how naked short selling works, and then Share Intel helped find the proof that that’s what has happened.

Individuals or groups get together and sell shares in a target company that they don’t own, with the aim of getting the share price to fall 50% in a short period. They use small-cap firms that have low buying volume, allowing them to scare off buyers.

“The broker doesn’t bother to find shares to borrow,” said Hamilton. “They simply sell shares they don’t have and after a few days book them as FTDs (failure to deliver) or hide them as long sales instead of short sales. The people who bought the shares have no idea they bought a fake share, and suddenly there’s plenty more shares in the market than there should be.”

If these groups sell 6 million shares from $12 to $6 each, and then buy back over two months at under $6, they double their money. That allows them to make up to $30 million out of thin air. They can then repeat the whole process a few months later.

“If they don’t buy back all the shares, they simply leave them as FTDs or hide them in offshore accounts,” he wrote. “At no point do they need to put up any cash to make this happen, as they’re making money from the moment they start selling fake shares.”

The ultimate goal is to push a company into bankruptcy, where the equity will be wiped out, meaning they never have to cover the short position on the fake shares.

By issuing a special dividend, Genius is hoping to find who is responsible, as all brokers are forced to disclose to the Depository Trust & Clearing Corp. (DTCC) how many shares their clients hold and how many dividends will be paid. Theoretically, that should expose the oversold shares and dishonest brokers will be forced to cover their position, said Hamilton.

In practice, dishonest brokers will not declare the fake shares and just pay the dividend out of their own pockets.

“If you issue a dividend that isn’t straight cash—such as a spinoff of a company so you are issuing shares, or a blockchain based asset, then the brokers can’t do that are a forced to either cover or be exposed,” he wrote.

Embattled crypto lender Genesis announced that it had filed for bankruptcy late Thursday, the latest firm to be taken amid a widespread rout among crypto companies driven by plunging prices and charges of fraud at major players like FTX.

Genesis, which froze customer withdrawals in November following the collapse of FTX, filed for Chapter 11 bankruptcy protection in federal court in Manhattan for its lending units, saying it was the best way for it to achieve “an optimal outcome for Genesis clients.”

“While we have made significant progress refining our business plans to remedy liquidity issues caused by the recent extraordinary challenges in our industry, including the default of Three Arrows Capital and the bankruptcy of FTX, an in-court restructuring presents the most effective avenue through which to preserve assets and create the best possible outcome for all Genesis stakeholders,” said Derar Islim, Genesis’ interim chief executive, in a statement on the company’s website.

According to its bankruptcy filing, Genesis’ lending unit said it had both assets and liabilities in the range of $1 billion to $10 billion and had over 100,000 creditors. The firm said it had about $150 million in cash on hand to support its operations during restructuring.

Genesis was the main partner of Gemini’s “earn” program, in which its retail investors received payments for allowing their crypto assets to be loaned out to others.

Cameron Winklevoss welcomed Genesis’ bankruptcy filing, saying it would provide Gemini a better venue for getting its clients’ money back.

“We will use every tool available to us in the bankruptcy court to maximize recovery for Earn users and any other parties within the bankruptcy court’s jurisdiction,” he wrote in a post on Twitter.

Both Genesis and Gemini were charged by the Securities and Exchange Commission last week with illegally selling securities to investors through the Earn program.

Genesis and its parent company, Digital Currency Group, had said they were seeking outside investment to help bolster the books and pay customers back in the months before filing for bankruptcy.

As part of its restructuring, Genesis said it would seek to possibly sell the company and also continue to look for additional investment.

This is an opinion editorial by Nicholas Otieno, a freelance writer focused on fintech and crypto.

Bitcoin has received growing attention from investors, the media and regulatory authorities as its price rises and adoption develops worldwide. However, relatively little is known about the black investors who have been attracted to it. Whether you are purchasing bitcoin or not, you can learn important lessons from these black Americans and become a more intelligent investor in any field.

In the late 2010s, a significant number of black Americans began researching Bitcoin with enthusiasm. They saw the promise of its blockchain technology, a distributed ledger that provides an immutable record of transactions. They watched the price movement of bitcoin hitting record highs, which doubtlessly appealed to them as well.

Many bitcoin investors started investing in cryptocurrency during that period — a time that later coincided with the distribution of COVID-19 stimulus checks in 2020. Millions of people who had never had much to invest or save suddenly had cash on hand, and many chose to put them into bitcoin.

The Crypto Bubble

Following this period, in which many black investors found bitcoin, the overall crypto market has started to shrink.

Black investors were among the thousands of Americans who witnessed their cryptocurrency holdings disappear after these digital currencies entered into a winter market.

The crypto crash hit black Americans as hard or harder than any other demographic community, in part because bitcoin had become so popular in that community. According to data collected by Harris Poll, 23% of black Americans own digital assets, while 11% of white Americans own such assets.

The crypto market fall has been costly and tragic, but that has not deterred many within the Black community, as they have such a strong desire to discover financial autonomy.

Addressing Financial Inclusion

Bitcoin naturally holds practical appeal for small-dollar investors from historically marginalized communities who distrust traditional finance. For instance, Black Americans can purchase BTC on digital platforms without a credit check, a step that may hold them back from financial inclusion in other assets.

Many Black investors have invested funds into bitcoin because they found it hard to build generational wealth in the traditional system. Overlooked by investment managers and discriminated against by banks, many Black investors have turned to more sovereign opportunities.

This long history of discrimination around investments explains why the world now witnesses a wide demography of interest and inclusivity in Bitcoin — because it is new, open and has fewer barriers to entry.

Another reason why people of color are adopting Bitcoin at a higher rate than others is likely because the cryptocurrency offers a cheaper remittance method than sending funds through banks.

Surviving In A Bear Market

It is true to say that the cryptocurrency market can be a risky place due to its volatility. Profits are made and lost within minutes. But despite this, many black investors have remained bullish on Bitcoin.

A good example of a successful black cryptocurrency investor can be found in Jefferson Noel, a 27-year-old. Noel gained his first exposure to cryptocurrency in January 2019 when he accidentally invested $5 in bitcoin while using a payment platform called Cash App. By May 2020, the value of his unintentional investment rose to $70. This inspired him and, as a result, he put another $20,000 of his savings into cryptocurrency. Recently, Jefferson said he is buying more altcoins despite persistent losses that have seen more than 20% of his cryptocurrency investment wiped out this year. Clearly, Bitcoin opened his eyes about becoming a more active investor.

Another can be found in Charlene Fadirepo, a banker who used to work at the Federal Reserve’s inspector general’s office, who has become a convicted bitcoin holder.

“Last year, she and her husband bought $6,000 worth (of bitcoin),” Time reported. “No investment has ever generated the kinds of returns for them that Bitcoin has.”

In A Nutshell

A lot can be learned from Black investors as they demonstrate that having the right mindset and resilience to deal with setbacks is the key to successful Bitcoin investing. Those who want to make money through bitcoin investing should be willing to hold on to their investments through the ups and downs and consider the fact that it can grant a form of financial security that is often barred from the underbanked. For many, this can be much more valuable than any quick gains.

This is a guest post by Nicholas Otieno. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Opinions expressed by Entrepreneur contributors are their own.

Thanks to record-high inflation, geopolitical instability and the first interest rate increases in years, the current market is, simply put, incredibly volatile. Existing investors are making strategic changes to their portfolios, and new investors are unsure if they want in at all. But for those fortunate enough to have disposable funds, is now the right time to get started?

Here are three reasons to wade in — slowly.

1. Time in the market is better than timing the market

Generally, when one starts investing isn’t as impactful as how long one invests. With a long enough time horizon, a well-diversified portfolio, and the power of compounding, portfolio volatility usually smooths out. This has been historically proven repeatedly as it pertains to the stock market.

By contrast, “timing the market” or waiting for stocks to hit a new low or drop from recent highs so that an investor can snag a bargain is risky. Short-term market behavior tends to be unpredictable, with current trends reversing on a dime. Waiting for the “perfect” moment to invest may mean passing up potential gains.

In other words, for many traders in waiting, now is as good a time as any to invest because markets are down. But exceptions may arise for those who need their money soon, as a short-term downturn can wipe out a portfolio overnight. If you are a new investor looking for a long-term “buy and hold” strategy, this is one of the best times to enter the markets and begin investing.

Many investors view short-term volatility as a risk that negatively impacts their portfolio. In the short term, this is true: volatility often drags down the total value of one’s investments.

That said, one of the primary ways that the stock market generates returns is when investors buy low and sell high. And what better way to profit off large price differences than buying in when the market swings downward? Forget timing the market — a good strategy for long-term growth is to buy when the market is down.

It may help to view market volatility as a form of bargain hunting. By buying high-quality investments when they go “on sale,” investors can increase their future profit margins when the market recovers. The trick is sorting the junk from the gems.

There’s no guarantee that any individual security will turn a profit. But historically, given enough time and increased economic activity, the stock market always performs — eventually.

That said, the time between a crash and recovery varies widely, and it certainly cannot be forecasted when that will happen. As such, pinpointing how long investors have to wait to realize gains is nearly impossible.

For instance, most stocks took 12 years to recover following the Great Depression. But during the COVID-19 pandemic, many stocks recovered within just four months. This a sobering reminder that there is no way to time bull or bear market cycles and that a market recovery can even mount in some of the worst economic conditions.

Start slowly to establish good habits and “feel out” the market

So, is now the right time to invest? For investors who aren’t on the cusp of retirement, the answer may be yes. Every investor should consider their risk tolerance and time horizon before deciding when and where to invest. Starting slowly can ease new investors into the market without introducing excessive risk.

Novices may also start simply with a dollar-cost averaging method, which involves investing small sums at regular intervals to even out the market’s ups and downs. While it’s not as exciting as day trading, dollar-cost averaging reduces the temptation to time the market and can even lead to more significant gains for investors.

As scary as the current market may seem, competent investing is less about day-to-day developments and more about the future. Be strategic, stay focused, and only risk what you can afford not to touch over the future.

Trading right now is chaotic. We’re watching earnings land and misses pile up, while the narrative on the economy shifts from inflation to a recession.

The producer price index report on Wednesday morning was lower than expected, which helped to cause a strong open as price fears continued to drop. In addition, retail sales were weaker than expected, which illustrates slowing demand and will also temper inflationary pressures, but it raises concerns about a sputtering economy. The Fed may have already tightened too much, and we are starting to see the economy respond accordingly.

Early breadth was very strong but is starting to slip as the S&P 500 falls into the opening gap. The Nasdaq and Nasdaq 100 have had seven-straight positive days, so a “sell the news” reaction would not be a big surprise. There also is some poor positioning that is providing support for now.

Conditions are now ripe for an intraday reversal, and we are seeing some signs of that now. The economic news on Wednesday is a mixed bag as it indicates inflation is cooling, but the likelihood of recession is increasing. A quarter percentage-point hike is now expected at the next Fed meeting — with the odds now at 97% — so weaker inflation is already discounted.

In response to the market action, I’m managing positions tightly, holding high levels of cash and see little opportunity to build longer-term positions right now. One name I’ve added to is small-cap pharma stock, Actinium Pharmaceuticals Inc., (ATNM) , but otherwise, I’m working on some index shorts.

So far this week we has seen 18 earnings reports, and 11 earnings per share misses. That is highly unusual. Typically EPS beats are 70% or more. But stocks have not been hit too hard on these misses so far. We have to watch this closely.

(Please note that due to factors including low market capitalization and/or insufficient public float, we consider this stock to be a small-cap stock. You should be aware that such stocks are subject to more risk than stocks of larger companies, including greater volatility, lower liquidity and less publicly available information, and that postings such as this one can have an effect on their stock prices.)

Get an email alert each time I write an article for Real Money. Click the “+Follow” next to my byline to this article.

As you might have learned from watching the mainstream news, the bitcoin price has been pumping as of late. If you bought the top and held until now, you may consider taking advice from good ol’ Mr. Goldshill himself, Peter Schiff, and use this opportunity to sell. If you’re someone who missed the boat, though, you may reasonably wait for confirmation and buy closer to $70,000. For those thinking to make a quick buck, you might hop on for a ride just to try and cash out near the next all-time high. If you’re a Communist who doesn’t believe we need a noncoercive way to coordinate human action… well, then, I can’t help you.

Whatever your story or specific situation is, one thing is clear: buying bitcoin is not going to help you.

Yes, you read that right. The physical act of trading one monetary good for another does next to nothing for you. Sure, you might make a few dollars in the short term (save for as much as 37% on short-term gains taxes). You may even get a girlfriend. Pay for that next vacation? Lambo? Why not?! But none of that matters because the ultimate value of bitcoin is not merely quantitative, but qualitative. And to get the qualitative benefits, you’ll need to prove you’ve done some work…

The gift of bitcoin lies in the unfathomable unlocking of understanding that you receive from putting in the time and effort to study it. The bad news is that there’s so many different rabbit holes down which to go. You could spend months to years learning about any of the following: cryptography, computer science, distributed systems, open-source software, network effects, game theory, economics, monetary theory, eleventh grade math, energy production, geopolitics, history, human rights, philosophy, human psychology, personal responsibility, just to name a… few. The good news is that there’s so many rabbit holes down which to go. I’ve been studying Bitcoin since 2018, and I’ve yet to even come close to exhausting the depth and breadth that Bitcoin offers. On top of that, the wisdom derived is rooted in reason and logic; it acts as an anchor in a world where reality is constantly and increasingly manipulated.

Initially, it’s hard to grapple with the fact that you’ve grown accustomed to living with a relatively short-term mindset, as we all have at some point in our lives. This short-term mindset is what Bitcoiners refer to as “high time preference.” It might take some time, but understanding how the money we choose changes individuals’ incentive structure is the first step to understanding why bitcoin is the best form of money. Inflationary fiat incentivizes its users to make decisions based on the needs of the present, while disinflationary bitcoin incentivizes its users to plan for the future while deprioritizing present consumption. It took me years of intent study to get to a point where I could articulate that point and truly grasp its effect on society. Don’t expect to get there in one conversation, article or podcast. This knowledge can only be spoon fed so much. You have to build a “proof-of-work” mindset. Unfortunately, many of your friends think they already know what they don’t know…

Dunning-Kruger Around And Find Out

Source: author

Wikipedia states that the Dunning–Kruger (DK) effect is a cognitive bias whereby people with low ability, expertise or experience regarding a certain type of task or area of knowledge tend to overestimate their ability or knowledge. One main reason that most normies won’t take the time and effort to do their own research, or DYOR, is because of hubris.

The most recent and obvious example of this in regards to Bitcoin came during Joe Rogan’s recent interview with geopolitical strategist, speaker and New York Times best-selling author, Peter Zeihan. While this guy is seemingly intelligent and well versed on much of what he writes and speaks about, he completely exposed his utter lack of knowledge and understanding of Bitcoin (and basic monetary theory) in less than a three-minute time span. For a great breakdown of how epically wrong he was about Bitcoin, listen to Guy Swann’s brilliant “Bitcoin Audible” podcast.

The point here is not to beat up on Zeihan (too much). The point is that we are all human and are able to easily make incorrect assumptions based on misconceptions and ignorance. To approach Bitcoin, you must begin with a level of humility and intellectual honesty. Unfortunately, too many of us will outsource this to “trusted” media sources filled with people who have yet to do the work themselves. This is a core concept within Bitcoin: don’t trust, verify. If you choose to trust those who show bravado but are void of any depth of knowledge, you’ll end up sharing their same misconceptions. You have to do the work yourself and come to your own conclusion. It takes… time (pun indeed intended).

The physical act of purchasing bitcoin is not the pinnacle of virtue. If you want to capture the entire value that Bitcoin offers, you need to show the mental proof of work required to comprehend at least a fraction of what this invention can do. Most of your normie friends won’t, though. Many will continue believing that the solution to life’s ills can be solved through subjugating their will to an equally-flawed human, whether they be red or blue. Others will go back to their bread and circuses. Most will lose focus in order to support “the next thing.” Everyone will have their reasons and justifications. Some of your friends will even become salty haters or remain intellectually dishonest.

I recently made a panic decision to withdraw all my money from one retirement account and I am now closing on a house in February (about $200,000). I am 36 years old, married and have a 1-year-old. Half of me is regretting it, and I’m worried about next year’s taxes due to the withdrawal and the 10% penalty I paid.

I have been saving up money with my family in order to buy our first home. Recently, however, interest rates have risen, making me worry that this window to get an affordable house was closing. In a fit of panic, I withdrew all of our $26,000 saved money from my 401(k), putting it in a high-yield savings account (3.75%). We have now chosen a home and will be using around $18,000 of this money for the down payment.

I am now worried that I might have to pay income taxes and a penalty for the withdrawal itself. I am extremely anxious over this situation as I feel I have destroyed our family’s financial future and that we cannot afford to pay taxes on the money I withdrew.

My main concern or question is, is there a way to tell the IRS that this money is being used toward a house? Retroactively?

The first thing you need to do: Take a breath. Most decisions should not be made in a panic, especially when involving money.

Because you withdrew from your 401(k), yes, you will have to pay taxes and a penalty. Had it been a loan, you’d have to pay interest on what you borrowed, but it would be to your own account. Keep in mind however that loans from your employer-based retirement plans are also risky – if you were to separate from your job, for whatever reason, you’d be responsible to pay it back or it would be treated as a distribution.

I understand your sense of urgency in wanting to buy a home during a more favorable market, but your time now should be spent on getting yourself financially situated and saving for the future.

“I wouldn’t advise this or done it this way, but he’s not stuck and it’s not detrimental – it’s just a tough lesson to learn,” said Jordan Benold, a certified financial planner at Benold Financial Planning.

Get very serious about your current finances and find a way to earmark a portion of your income to savings if at all possible. There are a few things you should be doing.

First, assess how much you will be paying in taxes and penalties. I’m not sure what your tax bracket is, but did this distribution push you into a higher tax bracket? You can use a calculator or talk to an accountant to see what that withdrawal will incur in taxes – then make sure you can pay it, or talk to the Internal Revenue Service about an extension. There are penalties for failing to file your taxes or pay them, and you don’t want to add that on top of your stress.

The IRS may not be able to do anything for you in terms of waiving those penalties – though it doesn’t hurt to ask, even if you have to wait on the phone for a while to talk to someone – but communication and attention to detail are key when it comes to your taxes. Getting an IRS agent on the phone and talking through your situation won’t be time wasted. There are so many rules, and an agent can help make sense of your options.

Once you get that sorted, look extremely carefully at whatever money you have coming in and what’s going out. You’re about to close on a home, and that costs money – not just the home itself, but all of the extras associated with closing. You may also need money for insurance, furniture, any repairs and so on if you haven’t factored that in yet, so fit that into your budget for when you sign the papers. Beyond that, list every expense you expect to have for the next 12 months – home insurance and taxes, a mortgage or utilities, groceries, medicine, any other nonnegotiable costs and add it all up. Don’t forget anything – ask your partner if there’s anything you may have forgotten.

Then compare it to your income. Are you under? Are you over? What changes can you make without totally draining your happiness? I always advocate for a balance…yes, in some cases you have to omit a few expenses for the time being when building up an emergency savings account or paying down debt, but don’t completely rob yourself of joy or all of your hard work may backfire. If you really need to buckle down, make a separate list of activities and entertainment you can get for free (or as close to free as possible)—walks in the park or on the beach with your partner and child, museums on free days, pot lucks and at-home movie nights with family and friends and so on.

Want more actionable tips for your retirement savings journey? Read MarketWatch’s “Retirement Hacks” column

Earmark a portion of your income to replenish your retirement savings before you try saving for any other goals. (This is separate from an emergency savings account, however – you should have one of those.) You may do that with payroll deductions in your 401(k), or also by allocating some of your savings to an IRA outside of the 401(k).

Take some time to learn the rules of your retirement plans. For example, an IRA allows an investor to take $10,000 out of the account penalty-free if it’s for a first-time home purchase (whereas a 401(k) does not have that exception). It may be too late for that, but there are other perks with various retirement accounts.

The 401(k) has a higher contribution limit and also comes with the possibility of employer matches (if your company offers it), whereas an IRA allows for penalty-free withdrawals for college. With a traditional IRA, you’d have to pay taxes on the withdrawal, whereas with a Roth IRA you’ve already paid the taxes and won’t have to pay any more for withdrawing from your contributions (you may have to pay taxes on the earnings portion, so follow distribution rules closely).

Remember – you don’t want to make distributions from your retirement savings for just anything. You can borrow money for a home or college, but you can’t borrow money for retirement, so it’s important to protect those accounts. Familiarize yourself with the pros and cons of all accounts so that you can maximize your savings and diversify your withdrawal options when you finally get to retirement.

So just buckle down, get yourself in order and think of the future. “He’s got plenty of time – 30 to 40 years to work,” Benold said. “This might be a distant memory that he hopes he can forget.”

Have a question about your own retirement savings? Email us at HelpMeRetire@marketwatch.com

Readers: Do you have suggestions for this reader? Add them in the comments below.

Many people are good at saving up money for retirement. They manage expenses and build up their nest eggs steadily. But when it comes time to begin drawing income from an investment portfolio, they might feel overwhelmed with so many choices.

Some income-seeking investors might want to dig deeply into individual bonds or dividend stocks. But others will want to keep things simple. One of the easiest ways to begin switching to an income focus is to use exchange-traded funds. Below are examples of income-oriented exchange-traded funds (ETFs) with related definitions further down.

First, the inverse relationship

Before looking at income-producing ETFs, there is one concept we will have to get out of the way — the relationship between interest rates and bond prices.

Stocks represent ownership units in companies. Bonds are debt instruments. A government, company or other entity borrows money from investors and issues bonds that mature on a certain date, when the issuer redeems them for the face amount. Most bonds issued in the U.S. have fixed interest rates and pay interest every six months.

Investors can sell their bonds to other investors at any time. But if interest rates in the market have changed, the market value of the bonds will move in the opposite direction. Last year, when interest rates rose, the value of bonds declined, so that their yields would match the interest rates of newly issued bonds of the same credit quality.

It was difficult to watch bond values decline last year, but investors who didn’t sell their bonds continued to receive their interest. The same could be said for stocks. The benchmark S&P 500 SPX, -0.20%

fell 19.4% during 2022, with 72% of its stocks declining. But few companies cut dividends, just as few companies defaulted on their bond payments.

One retired couple that I know saw their income-oriented brokerage account value decline by about 20% last year, but their investment income increased — not only did the dividend income continue to flow, they were able to invest a bit more because their income exceeded their expenses. They “bought more income.”

The longer the maturity of a bond, the greater its price volatility. Depending on the economic environment, you might find that a shorter-term bond portfolio offers a “sweet spot” factoring in price volatility and income.

And here’s a silver lining — if you are thinking of switching your portfolio to an income orientation now, the decline in bond prices means yields are much more attractive than they were a year ago. The same can be said for many stocks’ dividend yields.

Downside protection

What lies ahead for interest rates? With the Federal Reserve continuing its efforts to fight inflation, interest rates may continue to rise through 2023. This can put more pressure on bond and stock prices.

Ken Roberts, an investment adviser with Four Star Wealth Management in Reno, Nev., emphasizes the “downside protection” provided by dividend income in his discussions with clients.

“Diversification is the best risk-management tool there is,” he said during an interview. He also advised novice investors — even those seeking income rather than growth — to consider total returns, which combine the income and price appreciation over the long term.

An ETF that holds bonds is designed to provide income in a steady stream. Some pay dividends quarterly and some pay monthly. An ETF that holds dividend-paying stocks is also an income vehicle; it may pay dividends that are lower than bond-fund payouts and it will also take greater risk of stock-market price fluctuation. But investors taking this approach are hoping for higher total returns over the long term as the stock market rises.

“With an ETF, your funds are diversified. And when the market goes through periods of volatility, you continue to enjoy the income, even if your principal balance declines temporarily,” Roberts said.

If you sell your investments into a declining market, you know you will lose money — that is, you will sell for less than your investments were worth previously. If you are enjoying a stream of income from your portfolio, it might be easier for you to wait through a down market. If we look back over the past 20 calendar years — arbitrary periods — the S&P 500 increased during 15 of those years. But its average annual price increase was 9.1% and its average annual total return, with dividends reinvested, was 9.8%, according to FactSet.

In any given year, there can be tremendous price swings. For example, during 2020, the early phase of the Covid-19 pandemic pushed the S&P 500 down 31% through March 23, but the index ended the year with a 16% gain.

Two ETFs with broad approaches to dividend stocks

Invesco Head of Factor and Core Strategies Nick Kalivas believes investors should “explore higher-yielding stocks as a way to generate income and hedge against inflation.”

He cautioned during an interview that selecting a stock based only on a high dividend yield could place an investor in “a dividend trap.” That is, a high yield might indicate that professional investors in the stock market believe a company might be forced to cut its dividend. The stock price has probably already declined, to send the dividend yield down further. And if the company cuts the dividend, the shares will probably fall even further.

Here are two ways Invesco filters broad groups of stocks to those with higher yields and some degree of safety:

The Invesco S&P 500 High Dividend Low Volatility ETF SPHD, -0.33%

holds shares of 50 companies with high dividend yields that have also shown low price volatility over the previous 12 months. The portfolio is weighted toward the highest-yielding stocks that meet the criteria, with limits on exposure to individual stocks or sectors. It is reconstituted twice a year in January and July. Its 30-day SEC yield is 4.92%.

The Invesco High Yield Equity Dividend Achievers ETF PEY, -0.70%

follows a different screening approach for quality. It begins with the components of the Nasdaq Composite Index COMP, +1.39%,

then narrows the list to 50 companies that have raised dividend payouts for at least 10 consecutive years, whose stocks have the highest dividend yields. It excludes real-estate investment trusts and is weighted toward higher-yielding stocks meeting the criteria. Its 30-day yield is 4.08%.

The 30-day yields give you an idea of how much income to expect. Both of these ETFs pay monthly. Now see how they performed in 2022, compared with the S&P 500 and the Nasdaq, all with dividends reinvested:

Both ETFs had positive returns during 2022, when rising interest rates pressured the broad indexes.

8 more ETFs for income (and some for growth too)

A mutual fund is a pooling of many investors’ money to pursue a particular goal or set of goals. You can buy or sell shares of most mutual funds once a day, at the market close. An ETF can be bought or sold at any time during stock-market trading hours. ETFs can have lower expenses than mutual funds, especially ETFs that are passively managed to track indexes.

You should learn about the expenses before making a purchase. If you are working with an investment adviser, ask about fees — depending on the relationship between the adviser and a fund manager, you might get a discount on combined fees. You should also discuss volatility risk with your adviser, to establish a comfort level and to try to match your income investment choices to your risk tolerance.

Here are eight more ETFs designed to provide income or a combination of income and growth:

Company

Ticker

30-day SEC yield

Concentration

2022 total return

iShares iBoxx $ Investment Grade Corporate Bond ETF

The following definitions can help you gain a better understanding of how the ETFs listed above work:

30-day SEC yield — A standardized calculation that factors in a fund’s income and expenses. For most funds, this yield gives a good indication of how much income a new investor can be expected to receive on an annualized basis. But the 30-day yields don’t always tell the whole story. For example, a covered-call ETF with a low 30-day yield may be making regular dividend distributions (quarterly or monthly) that are considerably higher, since the 30-day yield can exclude covered-call option income. See the issuer’s website for more information about any ETF that may be of interest.

Taxable-equivalent yield — A taxable yield that would compare with interest earned from municipal bonds that are exempt from federal income taxes. Leaving state or local income taxes aside, you can calculate the taxable-equivalent yield by dividing your tax exempt yield by 1 less your highest graduated federal income tax bracket.

Bond ratings — Grades for credit risk, as determined by ratings agencies. Bonds are generally considered Investment-grade if they are rated BBB- or higher by Standard & Poor’s and Fitch, and Baa3 or higher by Moody’s. Fidelity breaks down the credit agencies’ ratings hierarchy. Bonds with below-investment-grade ratings have higher risk of default and higher interest rates than investment-grade bonds. They are known as high-yield or “junk” bonds.

Call option — A contract that allows an investor to buy a security at a particular price (called the strike price) until the option expires. A put option is the opposite, allowing the purchaser to sell a security at a specified price until the option expires.

Covered call option — A call option an investor writes when they already own a security. The strategy is used by stock investors to increase income and provide some downside protection.

Preferred stock — A stock issued with a stated dividend yield. This type of stock has preference in the event a company is liquidated. Unlike common shareholders, preferred shareholders don’t have voting rights.

These articles dig deeper into the types of securities mentioned above and related definitions:

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

Opinions expressed by Entrepreneur contributors are their own.

Some projections state that a new startup could take as long as four years to start earning a profit. Your business may be growing, but waiting four years may not be an option. If you want to start earning passive income that you can use to grow your business, then the stock market may be a viable option. If this is your first foray into stock investing, then the 2023 Stock Candlestick and Options Profit Trading Bundle could help you learn to be a wise investor.

StackCommerce

This course can help you mitigate your risks and maximize potential payouts. It contains 25 hours of instruction, starting from the basics. Get your first look at investing strategies in Options Trading 101 and Learn to Trade Options from Some of the Industry Greats. Both of these courses are led by professionals from MoneyShow, an investment advising organization with 40 years of experience.

Once you’re confident in your investment strategy, you can automate it using Python and a style of coding you could learn in the course Automatic Stock Trading with Python. It even comes with its own automatic trading bot that can make investments for you based on parameters you input.

The below is an excerpt from a recent year-ahead report written by the Bitcoin Magazine PRO analysts. Download the entire report here.

Bitcoin Magazine PRO sees incredibly strong fundamentals in the Bitcoin network and we are laser-focused on its market dynamic in the context of macroeconomic trends. Bitcoin aims to become the world reserve currency, an investment opportunity that cannot be understated.

In our year-ahead report, we analyzed seven notable factors that we recommend investors pay attention to in the coming months.

Convicted Bitcoin Investors

We can put investor conviction into perspective by looking at the number of unique Bitcoin addresses holding at least 0.01, 0.1 and 1 bitcoin. This data shows that bitcoin adoption continues to grow with a growing number of unique addresses holding at least these amounts of bitcoin. While it is entirely possible for individual users to hold their bitcoin in multiple addresses, the growth of unique Bitcoin addresses holding at least 0.01, 0.1 and 1 bitcoin indicate that more users than ever before are buying bitcoin and holding it in self-custody.

Unique bitcoin addresses continues to grow across the board.

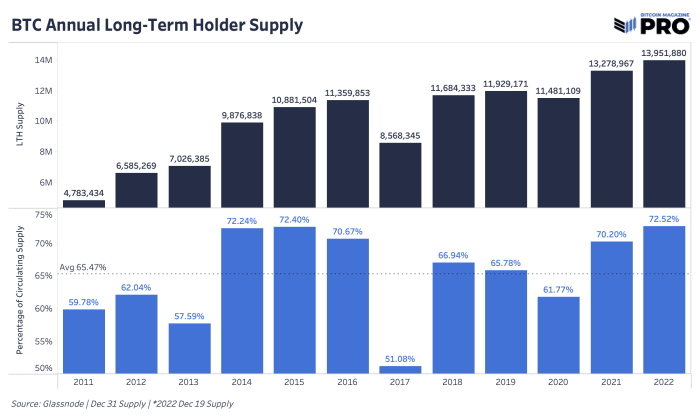

Another promising metric is the amount held by long-term holders, which has increased to almost 14 million bitcoin. Long-term holder supply is calculated using a threshold of a 155-day holding period, after which dormant coins become increasingly unlikely to be spent. As of now, 72.49% of the bitcoin in circulation is not likely to be sold at these prices.

Long-term holder supply reached 72.52% of the circulating bitcoin supply.

There is a large subset of bitcoin investors who are accumulating the digital asset no matter the price. In a December 2022 interview on “Going Digital,” Head of Market Research Dylan LeClair said, “You have people all over the world that are acquiring this asset and you have a huge and growing cohort of people that are price-agnostic accumulators.”

With a growing number of unique addresses holding bitcoin and such a significant amount of bitcoin being held by long-term investors, we are optimistic for bitcoin’s advancement and rate of adoption. There are many variables that demonstrate the potential for asymmetric returns as demand for bitcoin increases and adoption increases worldwide.

Total Addressable Market

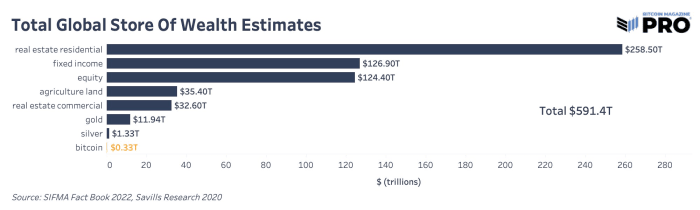

During monetization, a currency goes through three phases in order: store of value, medium of exchange and unit of account. Bitcoin is currently in its store-of-value phase as demonstrated by the long-term holder metrics above. Other assets that are frequently used as stores of value are real estate, gold and equities. Bitcoin is a better store of value for many reasons: it is more liquid, easier to access, transport and secure, easier to audit and more finitely scarce than any other asset with its hard-cap limit of 21 million coins. For bitcoin to acquire a larger share of other global stores of value, these properties need to remain intact and prove themselves in the eyes of investors.

Estimations of global stores of wealth.

As readers can see, bitcoin is a tiny fraction of global wealth. Should bitcoin take even a 1% share from these other stores of value, the market cap would be $5.9 trillion, putting bitcoin at over $300,000 per coin. These are conservative numbers from our viewpoint because we estimate that bitcoin adoption will happen gradually, and then suddenly.

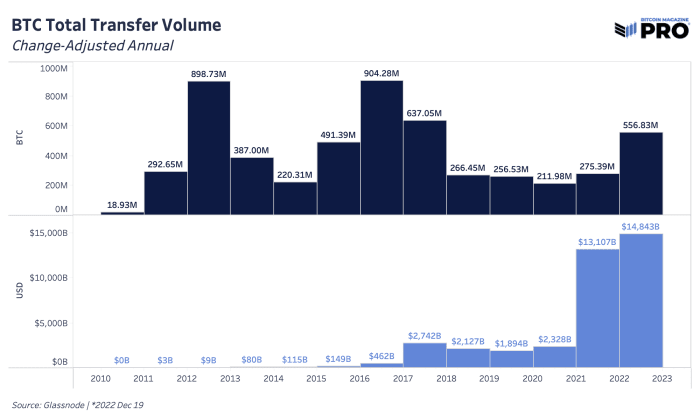

Transfer Volume

When looking at the amount of value that was cleared on the Bitcoin network throughout its history, there is a clear upward trend in USD terms with a heightened demand for transferring bitcoin this year. In 2022, there was a change-adjusted transfer volume of over 556 million bitcoin settled on the Bitcoin network, up 102% from 2021. In USD terms, the Bitcoin network settled just shy of $15 trillion in value in 2022.

Bitcoin transfer volume was higher than ever in USD terms.

Bitcoin’s censorship resistance is an extremely valuable feature as the world enters into a period of deglobalization. With a market capitalization of only $324 billion, we believe bitcoin is severely undervalued. Despite the drop in price, the Bitcoin network transferred more value in USD terms than ever before.

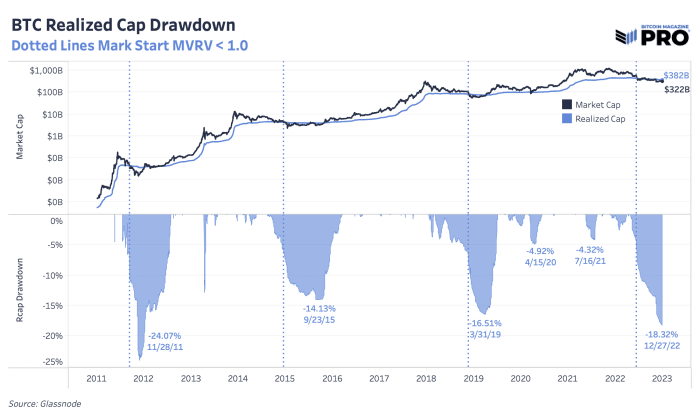

Rare Opportunity In Bitcoin’s Price

By looking at certain metrics, we can analyze the unique opportunity investors have to purchase bitcoin at these prices. The bitcoin realized market cap is down 18.8% from all-time highs, which is the second-largest drawdown in its history. While the macroeconomic factors are something to keep in mind, we believe that this is a rare buying opportunity.

The realized cap drawdown in 2022 was the second largest in bitcoin’s history.

Relative to its history, bitcoin is at the phase of the cycle where it’s about as cheap as it gets. Its current market exchange rate is approximately 20% lower than its average cost basis on-chain, which has only happened at or near the local bottom of bitcoin market cycles.

Current prices of bitcoin are in rare territory for investors looking to get in at a low exchange rate. Historically, purchasing bitcoin during these times has brought tremendous returns in the long term. With that said, readers should consider the reality that 2023 likely brings about bitcoin’s first experience with a prolonged economic recession.

Macroeconomic Environment

As we move into 2023, it’s necessary to recognize the state of the geopolitical landscape because macro is the driving force behind economic growth. People around the world are experiencing a monetary policy lag effect from last year’s central bank decisions. The U.S. and EU are in recessionary territory, China is proceeding to de-dollarize and the Bank of Japan raised its target rate for yield curve control. All of these have a large influence on capital markets.

Nothing in financial markets occurs in a vacuum. Bitcoin’s ascent through 2020 and 2021 — while similar to previous crypto-native market cycles — was very much tied to the explosion of liquidity sloshing around the financial system after COVID. While 2020 and 2021 was characterized by the insertion of additional liquidity, 2022 has been characterized by the removal of liquidity.

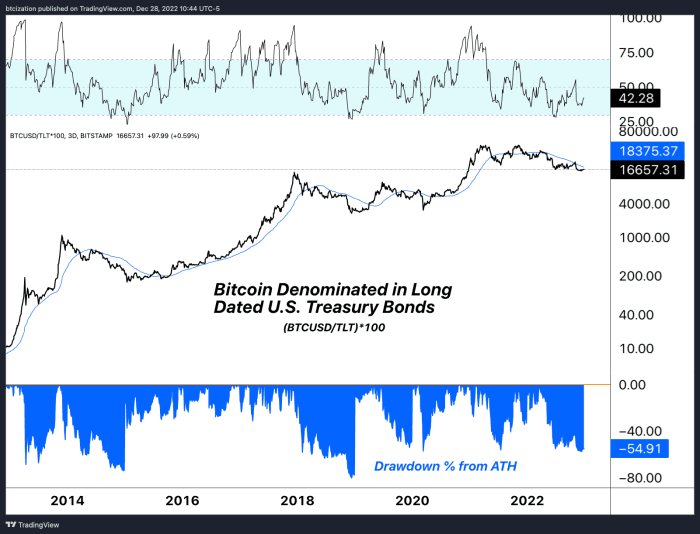

Interestingly enough, when denominating bitcoin against U.S. Treasury bonds (which we believe to be bitcoin’s largest theoretical competitor for monetary value over the long term), comparing the drawdown during 2022 was rather benign compared to drawdowns in bitcoin’s history.

As we wrote in “The Everything Bubble: Markets At A Crossroads,” “Despite the recent bounce in stocks and bonds, we aren’t convinced that we have seen the worst of the deflationary pressures from the global liquidity cycle.”

In “The Bank of Japan Blinks And Markets Tremble,” we noted, “As we continue to refer to the sovereign debt bubble, readers should understand what this dramatic upward repricing in global yields means for asset prices. As bond yields remain at elevated levels far above recent years, asset valuations based on discounted cash flows fall.” Bitcoin does not rely on cash flows, but it will certainly be impacted by this repricing of global yields. We believe we are currently at the third bullet point of the following playing out:

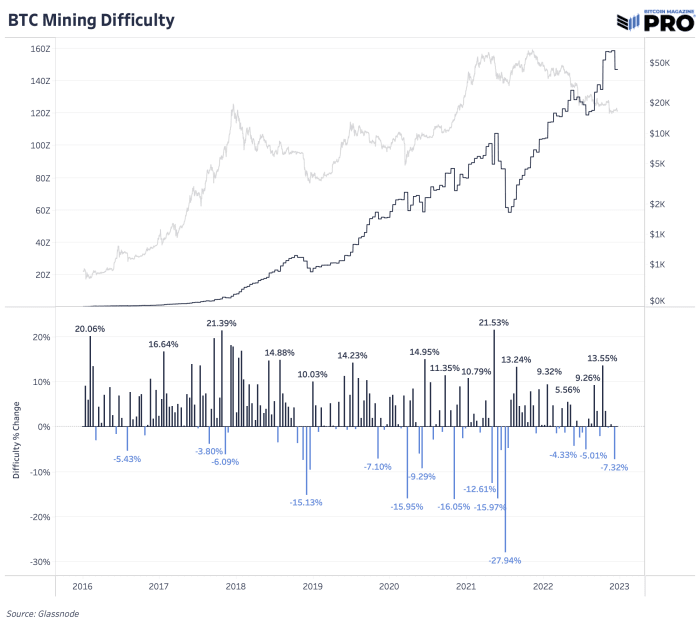

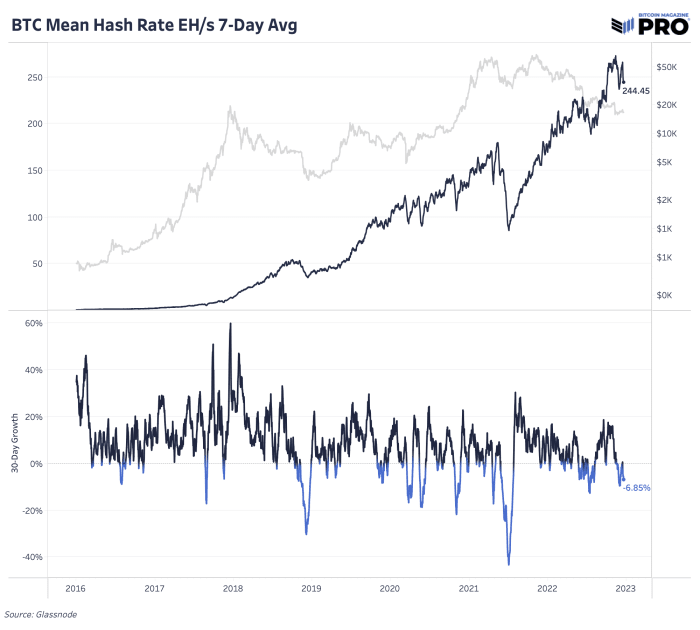

While the multitude of negative industry and worrying macroeconomic factors have had a major dampening on bitcoin’s price, looking at the metrics of the Bitcoin network itself tell another story. The hash rate and mining difficulty gives a glimpse into how many ASICs are dedicating hashing power to the network and how competitive it is to mine bitcoin. These numbers move in tandem and both have almost exclusively gone up in 2022, despite the significant drop in price.

Bitcoin mining difficulty continues to rise.

Bitcoin hash rate continues to rise.

By deploying more machines and investing in expanded infrastructure, bitcoin miners demonstrate that they are more bullish than ever. The last time the bitcoin price was in a similar range in 2017, the network hash rate was one-fifth of current levels. This means that there has been a fivefold increase in bitcoin mining machines being plugged in and efficiency upgrades to the machines themselves, not to mention the major investments in facilities and data centers to house the equipment.

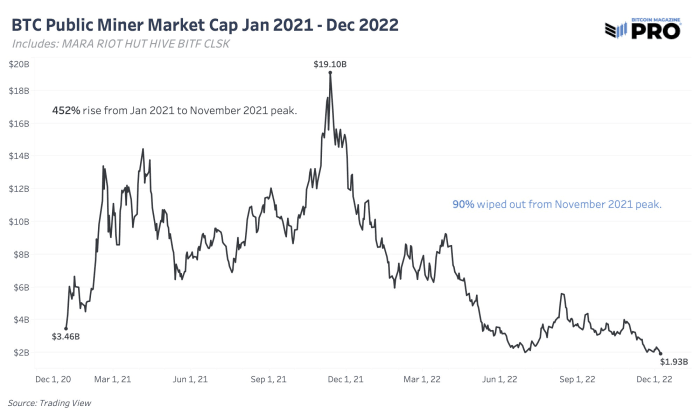

Because the hash rate increased while the bitcoin price decreased, miner revenue took a beating this year after a euphoric rise in 2021. Public miner stock valuations followed the same path with valuations falling even more than the bitcoin price, all while the Bitcoin network’s hash rate continued to rise. In the “State Of The Mining Industry: Survival Of The Fittest,” we looked at the total market capitalization of public miners which fell by over 90% since January 2021.

The market cap of all public mining equities has dropped by 9

We expect more of these companies to face challenging conditions because of the skyrocketing global energy prices and interest rates mentioned above.

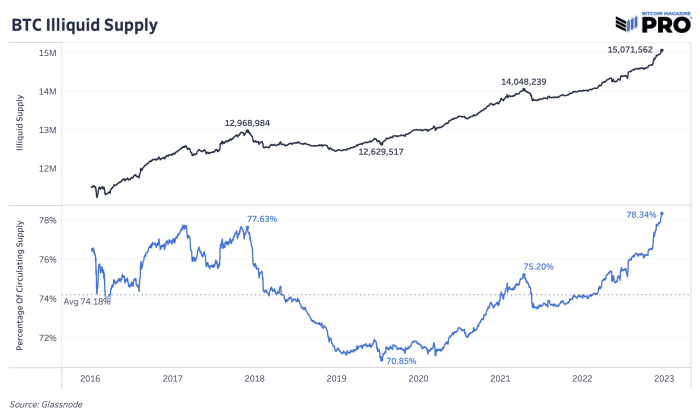

Increasing Scarcity

One way to analyze bitcoin’s scarcity is by looking at the illiquid supply of coins. Liquidity is quantified as the extent to which an entity spends their bitcoin. Someone that never sells has a liquidity value of 0 whereas someone who buys and sells bitcoin all the time has a value of 1. With this quantification, circulating supply can be broken down into three categories: highly liquid, liquid and illiquid supply.

Illiquid supply is defined as entities that hold over 75% of the bitcoin they deposit to an address. Highly liquid supply is defined as entities that hold less than 25%. Liquid supply is between the two. This illiquid supply quantification and analysis was developed by Rafael Schultze-Kraft, co-founder and CTO of Glassnode.

Bitcoin’s illiquid supply continues to grow.

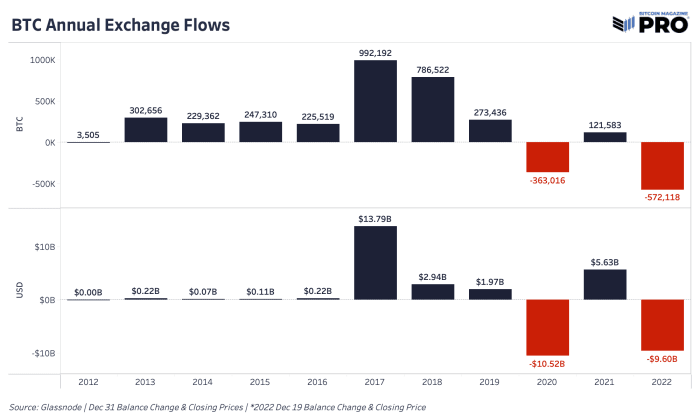

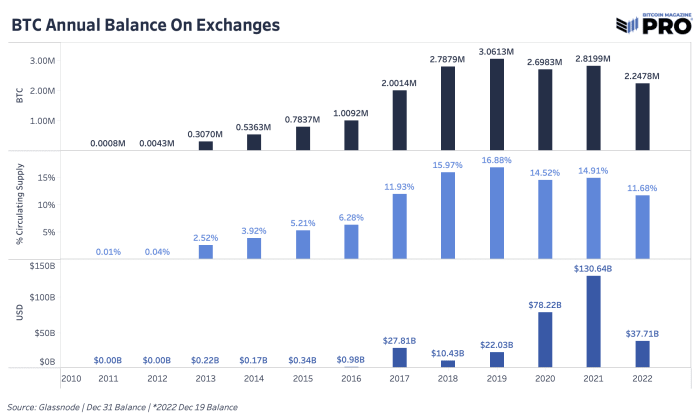

2022 was the year of getting bitcoin off exchanges. Every recent major panic became a catalyst for more individuals and institutions to move coins into their own custody, find custody solutions outside of exchanges or sell off their bitcoin entirely. When centralized institutions and counterparty risks are flashing red, people rush for the exit. We can see some of this behavior through bitcoin outflows from exchanges.

In 2022, 572,118 bitcoin worth $9.6 billion left exchanges, marking it the largest annual outflow of bitcoin in BTC terms in history. In USD terms, it was second only to 2020, which was driven by the March 2020 COVID crash. 11.68% of bitcoin supply is now estimated to be on exchanges, down from 16.88% back in 2019.

Exchanges saw a massive decrease in the bitcoin balances on their platforms.

Bitcoin balance on exchanges decreased in 2022.

These metrics of an increasingly illiquid supply paired with historic amounts of bitcoin being withdrawn from exchanges — ostensibly being removed from the market — paint a different picture than what we’re seeing with the factors outside of the Bitcoin network’s purview. While there are unanswered questions from a macroeconomic perspective, bitcoin miners continue to invest in equipment and on-chain data shows that bitcoin holders aren’t planning to relinquish their bitcoin anytime soon.

Conclusion

The varying factors detailed above give a picture for why we are long-term bullish on the bitcoin price going into 2023. The Bitcoin network continues to add another block approximately every 10 minutes, more miners keep investing in infrastructure by plugging in machines and long-term holders are unwavering in their conviction, as shown by on-chain data.

With bitcoin’s ever-increasing scarcity, the supply side of this equation is fixed, while demand is likely to increase. Bitcoin investors can get ahead of the demand curve by averaging in while the price is low. It’s important for investors to take the time to learn how Bitcoin works to fully understand what it is they are investing in. Bitcoin is the first digitally native and finitely scarce bearer asset. We recommend readers learn about self-custody and withdraw their bitcoin from exchanges. Despite the negative news cycle and drop in bitcoin price, our bullish conviction for bitcoin’s long-term value proposition remains unfazed.

Nearly two years after biotechnology stocks began to tumble, executives at small and midsize companies in the space are finally accepting that share prices aren’t bouncing back anytime soon.

With reality setting in, it’s a buyer’s market for companies looking for acquisitions and partnerships, according to many of the pharmaceutical and medical technology executives who gathered at this year’s

J.P. Morgan

healthcare investor conference, which wrapped up in San Francisco on Thursday.

Pour one out for the beleaguered economists, who for once got an important indicator, the consumer price index, right on the nose, after CPI fell 0.1% in December, while core prices rose 0.3%.

“The 2021 surge in durable goods demand normalized, and the resulting collapse in durable goods price inflation was stunningly fast,” says Paul Donovan, chief economist of UBS Global Wealth Management.

“The commodity wave of inflation is fading, and that leaves the profit margin expansion in focus,” he adds. What a good time for earnings season to be upon us, and what do you know, it is, kicking off with the banking sector on Friday before broadening out next week.

Strategists at Goldman Sachs have a new note out, saying that the market is pricing in a soft landing even though the trend of earnings revisions points to a hard landing.

They’re not that optimistic — even in the soft-landing scenario, the team led by David Kostin say the S&P 500 SPX, +0.40%

will end the year right around current levels, at 4,000. But they identify 46 stocks that could benefit — profitable, cyclical companies that are trading at price-to-earnings valuations below their 10-year median, among other factors.

One name jumps out: Tesla TSLA, -0.94%,

which trades at 22 times forward earnings versus the 10-year median of 117 times. But the other 45 names are less flashy, ranging from Capital One COF, +1.81%

and Carlyle Group CG, +0.54%,

to a host of industrials including 3M MMM, +0.12%,

Parker-Hannifan PH, +0.73%

and Otis Worldwide OTIS, +0.42%.

As a whole, these typically $10 billion companies are trading at 12 times earnings, versus 17 times usually.

In the hard landing scenario, S&P 500 profit margins would shrink by 125 basis points, to 10.9% — about in line with the median peak-to-trough decline during the eight recessions since 1970, which has been 132 basis points. Consensus expectations are for a 26 basis-point margin decline.

The Goldman team also have a 36 stock screen for a hard landing — profitable companies in defensive industries with a positive dividend yield. They’re typically food, beverage and tobacco companies as well as software and services companies — including Costco Wholesale COST, +0.58%,

Kroger KR, -0.99%,

Altria MO, +0.48%,

Tyson Foods TSN, +0.23%,

Microsoft MSFT, +0.30%,

MasterCard MA, -1.13%

and Visa V, -0.25%.

As a whole, these $37 billion companies are trading at 22 times earnings vs. a historical 24 times.

The market

After a 2.3% advance for the S&P 500 SPX, +0.40%

over the last three sessions, U.S. stock futures ES00, +0.39%

JPMorgan shares slumped after forecast-beating earnings, though investment bank revenue came in light of estimates. Delta shares also declined after topping earnings estimates.

Virgin Galactic SPCE, +12.34%

surged after saying it’s on track to launch space-tourism flights in the second quarter.

Apple AAPL, +1.01%

says CEO Tim Cook requested, and received, a pay cut after investor criticism.

The University of Michigan’s consumer-sentiment index is due at 10 a.m. Eastern, and Minneapolis Fed President Neel Kashkari and Philadelphia Fed President Patrick Harker are due to speak.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Do you ever hear news reports that the stock market rallied, or that it tanked due to a piece of worrisome news? Often in these reports, the stock market refers to the S&P 500 index, which represents about 80% of the U.S. stock market.

An S&P 500 index fund is a fund that tracks the performance of the S&P 500 index. These are among the most popular investments on the planet, and for good reason. An S&P 500 index fund can make practically anyone wealthy, given enough time and patience.

Here’s how S&P 500 index funds work and why they’re a safe and reliable choice for most investors.

What Is an S&P 500 Index Fund?

The S&P 500 is a stock index that tracks the performance of stocks in the S&P 500 index. (There are actually 503 stocks in the S&P 500 because three of the companies issue two classes of shares.)

It’s the most widely tracked stock index in the U.S., followed by the Dow Jones Industrial Average and the Nasdaq. When you hear in the news that stocks rallied or stocks plunged, often that means that the overall prices of those 503 stocks in the S&P 500 trended upward or downward.

An S&P 500 index fund is a pool of stocks designed to track the S&P 500. With one single investment, you’re automatically invested across all 500 companies in the index.

If the S&P 500 index goes up by 20% in a year and you’ve invested in an S&P 500 index fund, you’d expect returns of about 20%, minus investment fees, which are usually minimal. If the index falls by 20%, you’d expect the value of your investment to drop by 20% as well.

The goal isn’t to beat the market. Instead, an S&P 500 index fund aims to replicate the performance of the S&P 500 index as closely as possible.

Though some years, like 2022, the S&P 500 index will drop, it has about a 75% chance of gaining value in any given year, with annual returns averaging about 10%. Maybe that doesn’t sound like a lot, particularly in comparison to the mind-boggling returns investors saw in 2020 and 2021. But over long periods of time, those returns can produce substantial returns.

If you invested $500 a month and earned 10% annual returns, you’d have nearly $1 million after about 30 years. Your total investment? Just $180,000.

S&P 500 index funds have a phenomenal track record of building wealth over time. In fact Warren Buffett, who’s arguably the most successful stock picker on the planet, believes most investors should stick with S&P 500 funds instead of choosing their own stocks. In 2008, the Oracle of Omaha famously waged a bet with investment managers that an S&P 500 index fund could beat a pool of hedge funds over 10 years — and won.

Buffett believes in S&P 500 funds so much so that he’s directed the trustee of his estate to invest 90% of his money in S&P 500 funds for his wife when he dies. The remaining 10% will go to short-term Treasury securities.

What Is the Best S&P 500 Index Fund?

There’s no “best” S&P 500 index fund. They’re made up of the same investments, so they pretty much deliver the same returns. And you don’t need to own more than one S&P 500 index fund since they all track the same index.

You can find S&P 500 funds that are exchange-traded funds (ETFs), which are traded like individual stocks on stock exchanges, or mutual funds, which you can buy directly from an investment company or with a brokerage account.

Pro Tip

If you have a 401(k), you may already own S&P 500 index funds, as they tend to be popular options for retirement plans.

The main thing you should focus on is low fees. Look for an expense ratio of 0.1% or less. Choosing a fund with a low minimum upfront investment is also a good bet. With ETFs, you can often invest as little as $1 thanks to fractional investing. Some mutual funds require an upfront investment of $1,000 to $2,000, but many have no minimum investment.

Some low-cost options include the SPDR S&P 500 ETF Trust (SPY), Vanguard S&P 500 ETF (VOO), iShares Core 500 ETF (IVV) and the Fidelity 500 Index Fund (FXAIX).

The Pros and Cons of Investing in an S&P 500 Index Fund

Here are the pros and cons of S&P 500 index funds. Spoiler alert: There are a lot more pros than cons, especially if you’re a beginning investor.

S&P 500 Index Fund Pros

With a single investment, you get an automatically diversified portfolio. That’s a fancy investor way of saying you spread out your risk instead of putting all your eggs in one basket. You’re invested in 500 companies across all 11 stock market sectors. That’s why investing in an S&P 500 index fund is a lot less risky than investing in stocks of individual companies.

The S&P 500 produces reliable long-term returns. Over the past 30 years, the S&P 500 has delivered average annualized returns of around 10%. That doesn’t mean you can’t lose money. The S&P 500 fell more than 50% during the Great Recession of 2007 to 2009. In 2022, the index has tanked by nearly 20%, putting it close to bear market territory. But historically, the S&P 500 has always rebounded over the long term.

Their fees are minimal. Because you’re not paying for professionals to handpick investments for you, investment costs are low. Many S&P 500 index funds have an expense ratio of less than 0.1%, meaning that less than 0.1% of your investment is spent on non-investment costs. If you invest $1,000 in a fund with a 0.1% expense ratio, $999 of your money will go toward the actual investment.

Passive management typically beats active management. Don’t let the idea of sitting back and letting your money roll with the overall S&P 500 scare you. After fees, most active managers underperform their benchmark index.

You’re investing in major corporations with a profitable track record. To be included on the S&P 500, a company needs to have a $14.6 billion market capitalization, which is the total outstanding value of all its shares. They’re also required to have at least four consecutive profitable quarters under their belts. If a company runs into financial trouble, it risks being delisted.

S&P 500 Index Fund Cons

There’s less potential for big rewards. A drawback of investing in any index fund is that you don’t have the potential to hit the jackpot by picking the next Google or Amazon. You also won’t outperform the market, because the fund’s performance goes hand-in-hand with the S&P 500’s performance.

The S&P 500 is heavily concentrated on a few giants. Yes, you become an investor in 500 corporations when you buy an S&P fund. But because the index is weighted by market cap, your money isn’t distributed evenly across those companies. At the end of 2022, the top 10 S&P 500 companies by market capitalization accounted for 25% of the S&P 500’s value. That can pose problems when one sector becomes heavily weighted. For example, at the end of 2020, five tech stocks represented more than 20% of the index’s value. That spelled trouble for the S&P 500 index in 2021 and 2022, as tech stocks faltered.

Giant corporations have less room for growth. The companies in the S&P 500 are among the most successful and stable in their respective industries. One downside to that: They’re already so big that they have less room to grow. Small-cap stocks, or those with a market cap under $2 billion, usually have the most growth potential, though they’re also a lot riskier.

Robin Hartill is a certified financial planner and a senior writer at The Penny Hoarder. She writes the Dear Penny personal finance advice column. Send your tricky money questions to [email protected]

Katie St. Ores has a 100% track record of getting her tax clients out of paying the steep penalty for missing a required minimum distribution from their retirement funds. That amounts to only two households getting forgiveness, but it represents a lot of dollars, because the fee for any sort of mistake with RMDs is 50% of what’s missing, which could be tens of thousands of dollars.

Now’s the time to make things right if you forgot to make your RMD payment by Dec. 31 for 2022, paid the wrong amount or realized you got it wrong in a past year. The faster you correct it, the more likely the IRS is likely to waive the fines — and your chances are good overall, despite the agency’s stern reputation.

Beware, though, that new rules are going into effect in 2023 that could make the IRS less accommodating. For one thing, the age to start RMDs is going to 73 this year, and then 75 in 2033, which means the government is going to be hungry for the missing revenue. Even more important, the penalty will be reduced to 25% — or 10% if you’re really quick about reporting it.

The IRS doesn’t publicly track how many people miss or make mistakes with their RMDs, but financial advisers and tax professionals say it happens often enough, and they consider the IRS to be quite liberal about granting waivers.

St. Ores, who is a financial adviser and tax preparer based in McMinnville, Ore., thinks the IRS has responded generously so far because they know the rules are complex and mistakes happen.

“They know people are getting up there in age, and so they’ve probably said up to now, let’s just grant it,” says St. Ores.

But the new penalties seem worded to avoid waivers in the future, especially because of the extra reduction to 10% if you act to quickly correct mistakes. Up to now, the IRS has taken pains to point out how to ask for a forgiveness on its website, but now there will be new emphasis on the lower penalties.

“The 50% penalty effectively ‘scared’ taxpayers to withdraw RMDs, so reducing the penalty could reduce the fear of additional tax, leading to more taxpayers missing their RMDs,” says St. Ores. “Between more taxpayers that potentially neglect to take their RMDs because of a not-as-high penalty and confusion over the current required age, the IRS will probably collect more taxes overall.”

What to do about past mistakes

There are a lot of different ways to mess up your required minimum distributions. The amount you’re supposed to pay is calculated according to a formula that takes your account balance of all your qualified tax-deferred accounts and multiplies it by a factor related to your age.

When you get started taking the money out, it works out generally to about 4% of the account value. You keep taking RMDs every year from your designated start time until the accounts are empty (or you die). The beginning age in the past was 70½, then it moved to 72, and now it’s changing to 73.

“These things can get complicated,” says Isaac Bradley, director of financial planning at Homrich Berg, an investment firm based in Atlanta. He advised one couple that accidentally took the distribution from the wrong spouse.

Another easy mistake is taking the wrong amount because of a math error. Sometimes, the problem is just about communication, because people tend to have multiple 401(k)s at old employers or several rollover IRAs that aren’t consolidated. The adviser helping make the calculations might not know of an account held at a different custodian, and that could throw off the whole equation.

David Haas, a financial adviser and president of Cereus Financial Advisors, based in Franklin Lakes, N.J., has had to help family members correct RMDs, mostly having to do with inherited IRA accounts.

“You’re supposed to take RMD for the person who died, if they didn’t already take it,” he says, but a lot of people miss those in the confusion of grief.

Then once you inherit the account, you have to take RMDs over a 10 year period to empty the account.

“With one relative, she just kept on missing it and that was her fault. She didn’t realize what she was supposed to do. People don’t know the law, and it’s very confusing,” Haas says.

The first step is realizing you made a mistake, and then once you know that, pay the amount that’s missing. You need to file a special form with the IRS for the tax year in question (Form 5329), which you can send in at any point — you don’t have to wait until you file your next tax return.

If you want to ask for a waiver, you need to attach a letter explaining the mistake. If your request is not granted, then you pay the penalty.

While the process isn’t excessively complicated, you might want to consult with a tax professional to make sure you’re not making more mistakes in calculating the amount that’s missing. It could turn out to be a lot of paperwork if you have missed multiple years.

Kenneth Waltzer, a financial planner based in Los Angeles, had a client who did not realize he had inherited an IRA and missed the RMDs on it for five years. “He ignored emails about it,” says Waltzer. “When he came to us, it added up to over $100,000.”

For Katie St. Ores, the message going forward is going to be: Get it right the first time. Forgiveness may not be so easy to come by in the future. “I’m trying to stay on top of my clients taking their RMDs on time,” she says.

U.S. securities regulators on Thursday charged Genesis Global Capital and crypto exchange Gemini Trust Co. with offering and selling of unregistered securities to retail investors, bypassing disclosures and other requirements aimed at protecting market participants.

Genesis and Gemini raised billions of dollars’ worth of crypto assets from hundreds of thousands of investors through unregistered offers, using a crypto asset-lending program called Gemini Earn, the Securities and Exchange Commission said.